Futures Flat At All Time High As Oil Tumbles, Bank Earnings Shine

US equity futures pointed to an unchanged open as earnings from Bank of America and Goldman Sachs beat expectations while megacap tech stocks showed modest moves. As of 8:00am ET, S&P futures were unchanged after closing at a 46th record high on Monday, while Nasdaq futures dipped 0.1% as Nvidia shares fell 1% in premarket after Bloomberg reported Biden administration officials have discussed capping sales of advanced AI chips from Nvidia and other companies. Bond yields are lower and USD is weaker; 2-, 5-, 10-yr yields are down 0.36bp, 1.75bp, 3.53bp respectively. Oil tumbled as much as -5% from yesterday close after the WaPo reported that Israel may avoid targeting Iran’s crude infrastructure, although Israel later denied the claim. Chinese stocks slumped: HSI and CSI closed -2.6% and -3.7% lower today after the WSJ reported that the motivation behind the recent policies is not “massively stimulate demand but to fend off a brewing financial crisis.” Aluminum and Copper are both more than -1% lower this morning. On the macro front we get October Empire manufacturing (8:30am) and September New York Fed 1-year inflation expectations (11am), and three Fed speakers. All eyes on earnings from BofA and Goldman today.

In premarket trading, Bank of America climbed 2% after its Wall Street operations performed better than expected as the company reaped the benefits of volatile markets. Net interest income topped analysts’ estimates. Goldman rose more than 3.3%, after it also reported earnings that beat across the board. Nvidia and AMD dell after Bloomberg reported the Biden administration discussed capping sales of advanced AI chips to some countries. Here are some other notable premarket movers:

- Coty drops 4% after the beauty company provided some preliminary 1Q results that disappointed.

- Etsy declines 5% after Goldman Sachs cut the online retailer to sell, citing a more selective approach to e-commerce stocks ahead of earnings.

- Schwab climbs 3% after posting adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Trump Media & Technology rises 7%, putting the stock on course to extend its rally into a fourth consecutive session.

- UnitedHealth slips 3% after the health insurer trimmed the higher end of its profit forecast for the full year.

- Walgreens Boots gains 5% after the pharmacy chain gave a sales forecast for its 2025 year that exceeded the average analyst expectation.

- Wolfspeed rises 21% as the company is in line to win $750m in US government grants as well as $750m in financing led by Apollo Global Management Inc. to support its factory expansion plans.

Energy shares fell premarket trading, as oil prices plunged below $75 a barrel after a WaPo report that Israel will hold off attacking Iranian oil facilities. Israel later denied this, saying “it is listening to US misgivings about its planned counter-strike against Iran but will act based on its own assessments” but by then it was too late and the oil selling CTAs had been engaged. The IEA added to the selling pressure as they warned swelling American production is set to create an oil glut in early 2025.

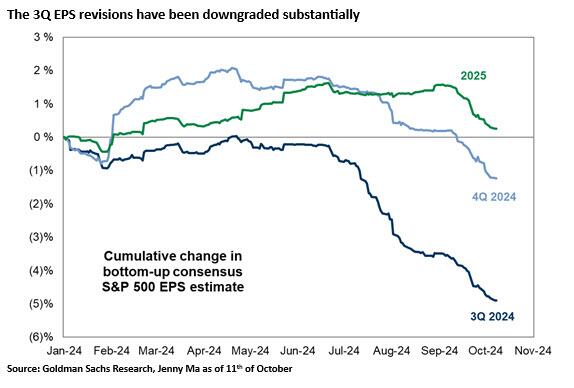

Elsewhere, Citigroup, Goldman and Bank of America are among the companies reporting Tuesday, while Netflix and JB Hunt will also present results later this week. Investors appear undeterred by reduced profit forecasts and are instead betting on positive surprises. Nathan Thooft, chief investment officer and senior portfolio manager at Manulife Investment Management, expects earnings season to be pretty good, but mostly because expectations have been lowered. “Consensus is around 4% year-over-year. It’s a fairly low bar,” he said.

Oil’s drop fed through to energy stocks, which dragged European stocks lower. Europe’s Stoxx 600 index slipped 0.2%, dragged down by declines in energy shares such as TotalEnergies SE and BP Plc. Beauty stocks LVMH, L’Oreal SA, Puig Brands SA also fell after US outfit Coty Inc. lowered its sales-growth guidance overnight.

Earlier int he session, Asian stocks reversed gains of as much as 0.7%, driven by sharp losses in Chinese and Hong Kong stocks. The MSCI Asia Pacific Index declined as much as 0.4%, reversing a 0.7% climb, with Chinese technology stocks including Meituan, Tencent and Alibaba the top laggards. Stocks in both mainland and Hong Kong dropped, raising doubts over the outlook for a market that is struggling to sustain the ferocious rally of late September. Energy was the worst-performing sector on the regional index, as oil dropped after a report that Israel may avoid targeting Iran’s crude infrastructure eased concerns over a major supply disruption. Sentiment took a hit after China’s export growth slowed in dollar terms from last year, hurting one of the few bright spots in the economy. Investors are still trying to assess the scope for government stimulus after its latest pledge for support.

“This is Beijing’s ‘whatever it takes’ moment,” Yan Wang, chief of emerging markets and China strategist at Alpine Macro, told Bloomberg TV. “If Beijing is really committed to boosting the economy, they need to use the balance sheet of the central bank and the central government to reflate the economy,” he said.

And yet according to the WSJ, this is anything but China’s whatever it takes moment: citing “people familiar with the decision-making”, the WSJ said that this isn’t a stimulus measure, but rather a derisking step, indicating that this is just another half-baked “half-measure” from the Xi admin, assuring that much more stimulus will be needed eventually: “Absent from the measures are any significant moves to boost consumption. People close to the ministry say such measures are in the works but nothing substantial is imminent.”

In FX, the Bloomberg Dollar Spot Index held steady after rising 0.3% Monday. “The bias is for a stronger USD,” Elias Haddad, senior markets strategist at Brown Brothers Harriman & Co., wrote in a note. “Encouraging US economic activity and sticky underlying inflation argue for a cautious Fed easing cycle.” The pound rose 0.1% after mixed UK jobs data, while the Japanese yen tops the G-10 FX leader board with a 0.5% gain: USDJPY briefly dipped below 149 after rising just shy of 150 on Monday.

In rates, treasuries and European government bonds rise as traders gravitate toward safe-haven assets. Treasury yields are richer by 1bp to 4bp across maturities with the curve flatter in cash trading after Monday’s holiday, during which stocks and futures were open. 10-year yields at around 4.07% are ~3bp richer on the day with bunds and gilts in the sector outperforming by an additional 1bp. Bull-flattening in Treasuries leaves 2s10s, 5s30s spreads about 2.5bp tighter vs Friday’s close. Bonds have support from slide in oil prices spurred by a report Israel may avoid targeting Iran’s crude infrastructure, which eased concerns about supply disruption.

In commodities, brent crude futures fall some 4.8% to below $74 a barrel after the WaPo reported that Israel may avoid targeting Iran’s crude infrastructure eased concerns over a major supply disruption. The IEA added to the selling pressure as they warned swelling American production is set to create an oil glut in early 2025. Amusingly, even though Israel later denied the WaPo report – which was meant precisely to hammer oil – the price of the commodity failed to rebound. Spot gold reversed an earlier fall to rise $6.

Looking at today’s calendar, we get the October Empire manufacturing (8:30am) and September New York Fed 1-year inflation expectations (11am). Fed speakers scheduled include Daly (11:30am), Kugler (1pm) and Bostic (7pm).

Market Snapshot

- S&P 500 futures little changed at 5,904.25

- STOXX Europe 600 down 0.1% to 524.23

- MXAP down 0.2% to 191.98

- MXAPJ down 0.7% to 609.24

- Nikkei up 0.8% to 39,910.55

- Topix up 0.6% to 2,723.57

- Hang Seng Index down 3.7% to 20,318.79

- Shanghai Composite down 2.5% to 3,201.29

- Sensex down 0.3% to 81,766.76

- Australia S&P/ASX 200 up 0.8% to 8,318.37

- Kospi up 0.4% to 2,633.45

- German 10Y yield down 3.6 bps at 2.24%

- Euro little changed at $1.0904

- Brent Futures down 4.2% to $74.24/bbl

- Brent Futures down 4.2% to $74.24/bbl

- Gold spot up 0.2% to $2,655.02

- US Dollar Index down 0.14% to 103.15

Top Overnight News

- China is starting to enforce a tax on overseas investment gains by the country’s wealthiest citizens, an initiative aimed at both driving gov’t revenue (to help pay for fiscal stimulus) and pursuing Xi’s “common prosperity” initiative. BBG

- Xi isn’t looking to massively stimulate demand or ease his iron grip on the country’s economy but instead stave off a financial crisis by providing support to overindebted local governments and bolster the stock market (his shift on policy was more tactical than strategic). WSJ

- Chinese banks are set to trim rates on 300 trillion yuan ($42.3 trillion) of deposits as soon as this week after the latest barrage of stimulus policies further squeeze their profitability. BBG

- The International Energy Agency trimmed its forecast for this year’s oil-demand growth for the third month in a row, as a rapid slowdown in Chinese consumption weighs on the global outlook. WSJ

- Global sovereign debt will hit $100T by the end of 2024, or ~93% of aggregate GDP, with the figure headed to 100% by 2030 as it warned governments will be forced to make difficult fiscal decisions. BBG

- Israel has told Washington it will hit Iranian military targets, not oil or nuclear infrastructure, as Netanyahu looks to retaliate without escalating the situation. WaPo

- The Swiss financial regulator has ordered UBS to bolster its emergency and recovery plans in light of the added risk it has taken on following its takeover of Credit Suisse last year. FT

- Biden administration officials have discussed capping sales of advanced AI chips from Nvidia Corp. and other American companies on a country-specific basis, people familiar with the matter said, a move that would limit some nations’ artificial intelligence capabilities. BBG

- Home builders are still offering mortgage rate buydowns to attract buyers, despite falling mortgage rates. The cost of buydowns is eating into home-builder profits, and they might need to turn to other strategies such as price reductions. Home-builder share prices have been rising, but the outlook is more challenging if more previously owned homes come on the market. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as most major indices followed suit to the gains stateside where a tech rally led the S&P 500 and Dow to fresh all-time highs, although Chinese markets lagged following weak trade data. ASX 200 climbed to a record high with advances led by the top-weighted financial sector and miners. Nikkei 225 outperformed and gapped back above the 40,000 level on return from the long weekend. Hang Seng and Shanghai Comp were pressured after weak trade data and stimulus disappointment, while trade frictions also lingered with the US mulling capping NVIDIA and AMD AI chip sales to some countries.

Top Asian News

- Chinese banks mull cutting rates on CNY 300tln of deposits as early as this week with the major banks to be guided by the PBoC’s interest rate self-disciplinary mechanism to lower rates on a number of deposit products, according to Bloomberg.

- China began enforcing an up to 20% tax on overseas investment gains by the country’s ultra-rich.

- US weighs capping NVIDIA (NVDA) and AMD (AMD) AI chip sales to some countries, according to Bloomberg.

- China and NDRC are to hold a meeting on financing for small businesses on October 21st

- Reuters Poll, China: growth & CPI forecasts cut.

European bourses, Stoxx 600 (-0.1%) began the session generally on a modestly firmer footing, but sentiment has waned as the session progressed, but with no fresh catalyst emerging in European hours. European sectors are mixed; Travel & Leisure takes the top spot, benefiting from lower oil prices, but also in a paring to some of the significant losses seen in the prior session. Telecoms follows closely behind, lifted by post-earning strength in Ericsson. Energy is found at the foot of the pile, alongside Basic Resources, which is hampered by continued Chinese demand fears. US Equity Futures (ES -0.1% NQ -0.2% RTY +0.1%) are trading tentatively on either side of the unchanged mark, taking a breather from the hefty gains seen in the prior session. US weighs capping NVIDIA (NVDA) and AMD (AMD) AI chip sales to some countries, according to Bloomberg. UBS Global Research has increased its 2024 year-end S&P 500 target from 5600 to 5850 and increased its 2025 target from 6000 to 6400 Earnings include: Ericsson (headline beat, CEO pointed to increasing customer momentum and N. America stabilising) Unitedhealth Group Inc (UNH) Q3 2024 (USD): adj. EPS 7.15 (exp. 7.01), Revenue 100.8bln (exp. 99.28bln). FY adj. EPS view 27.50-27.75 (exp. 27.70), FY Revenue view (exp. 399.42bln); results which sparked marked pressure in the DJIA.

Top European News

- Dutch to Cut ABN Amro Stake Further as Exits Gather Pace

- Israel: Hamas in Turkey Directed Aug. Tel Aviv Suicide Bombing

- EU Agrees COP29 Climate Stance With Money Quandry Unanswered

- UBS Must Revise Post-Takeover Emergency Plans, Finma Says

- Orange Gets Holder Consent to Amend Terms of 2031 Notes

FX

- USD is mixed vs. peers alongside a lack of fresh macro drivers for the US other than comments from Fed’s Waller who said the Fed should proceed with more caution on rate cuts than was needed at the September meeting. For now, DXY is holding above the 103 mark and within Monday’s 102.91-103.45 range.

- EUR is flat vs. the USD with not much in the way of follow-through from a mixed batch of ZEW data; focus no doubt will be on the ECB on Thursday. EUR/USD has made its way back onto a 1.09 handle but is yet to approach yesterday’s 1.0936 peak.

- GBP is incrementally firmer with not much in the way of follow-through from the latest UK jobs report, which on the surface looked hawkish given the stronger than expected employment change and unexpected decline in the unemployment rate. However, the ONS stated in the release that the report may be overstating underlying employment growth.

- JPY is attempting to claw back some lost ground vs. the USD after USD/JPY stopped shy yesterday of the 150 mark, topping out at 149.98. USD/JPY has delved as low as 149.04 vs. yesterday’s 149.01 trough.

- Antipodeans are both softer vs. the USD and towards the bottom of the G10 leaderboard. AUD/USD is just about holding above Monday’s low at 0.6701 and the 0.67 mark. NZD/USD has extended its move below the 0.61 mark and 200DMA at 0.6093, ahead of the region’s CPI later on.

- PBoC set USD/CNY mid-point at 7.0830 vs exp. 7.0840 (prev. 7.0723).

Fixed Income

- Benchmarks are bid in a continuation of Monday’s modest rebound with upside today driven by marked crude pressure and Final inflation readings from France.

- Bunds at a 133.74 peak, resistance at 133.80 and 134.03, upside spurred by the crude moves (see commodities) and French final inflation which saw the harmonised numbers revised down and factor in favour of the doves into Thursday.

- Session high for benchmarks in the wake of remarks that the EU’s fiscal burden for upcoming Ukraine aide could be reduced if the US gets involved.

- Gilts gapped higher on the above energy angle and also the regions latest employment data which shouldn’t stand in the way of continued BoE easing; 96.71 session peak printed after a robust DMO tap.

- USTs firmer with the above applying, at a 112-07+ peak; yield curve mixed (returning from holiday outages for cash) with the short end seemingly propped up by Fed’s Waller on Monday while the long-end slumps given energy.

- UK sells GBP 2.25bln 4.375% 2054 Gilt: b/c 3.08x (prev. 2.89x), average yield 4.735% (prev. 4.329%), tail 0.3bps (prev. 0.9bps)

Commodities

- Crude benchmarks are well into the red, weighed on at the beginning of the APAC session on reports that Israeli PM Netanyahu informed the US that their response to Iran will target military facilities, not nuclear or oil sites. The complex then took another leg lower after the IEA OMR saw a downgrade to their 2024 world oil demand view, primarily driven by China. Brent’Dec currently near session lows around USD 73.50/bbl.

- Spot gold is firmer, but only modestly so. At a USD 2654/oz peak, a point which is over USD 10/oz shy of Monday’s USD 2666/oz best.

- Pressured, base metals in the red across the board and 3M LME Copper within reach of USD 9.5k from a high point just shy of USD 9.7k.

- WSJ article on Chinese stimulus: “Absent from the measures are any significant moves to boost consumption. People close to the ministry say such measures are in the works but nothing substantial is imminent.”

- IEA OMR (Oct): 2024 world oil demand growth forecast to 860k bpd (prev. forecast 900k); says China is the main drag on global oil demand growth, with China’s demand expected to rise only 150k bpd in 2024.

- Russia’s seaborne oil product exports in September are up 5% on the month, according to Reuters.

Geopolitics: Middle East

- Iranian government says “Our response will be at the right time and place and we will not hesitate or rush”, via Al Arabiya.

- Israeli Broadcasting Corporation reports that a full agreement has been reached on the method, timing and strength of the response to an attack Iran, via Al Jazeera; the strike plan is awaiting the approval of the Ministerial Council for implementation.

- Israeli Broadcasting Corporation reports that a full agreement has been reached on the method, timing and strength of the response to an attack Iran, via Al Jazeera; the strike plan is awaiting the approval of the Ministerial Council for implementation.

- Israeli PM Netanyahu told the US that Israel will strike Iranian military, not nuclear or oil, targets, according to officials cited by The Washington Post.

- Israel Broadcasting Corporation cited Israeli PM Netanyahu’s office stating that they listen to the views of the US administration, but will make decisions based on Israel’s interests, according to Al Jazeera.

- UN Security Council expressed strong concern after several UN peacekeeping positions in Lebanon came under fire, while it urged all parties to respect the safety and security of UNIFIL peacekeepers and premises, as well as expressed deep concern for civilian casualties and the destruction of civilian infrastructure.

- US President Biden asked the National Security Council to inform Iran that any attempt on former President Trump’s life would be considered an act of war, according to Fox News. The White House later said it has been closely tracking Iranian threats against Trump and former Trump administration officials for years, while it warned Iran will face severe consequences if it attacks any US citizen.

Geopolitics: Other

- German official says if the US participates in the USD 50bln loan for Ukraine, the EU’s share of the loan may be reduced.

- NATO Secretary General Rutte in his first visit to Ukraine mission, welcomed plans for temporary deployment of US long-range missiles to Germany from 2026, while he said NATO will not be cowed by Russian threats and will keep its strong support of Kyiv.

- North Korea blew up part of inter-Korean roads, according to South Korea’s military. It was separately reported that South Korea’s military fired warning shots south of the demarcation line after North Korea destroyed inter-Korean roads.

US Event Calendar

- Oct. 15-Oct. 25: Sept. Monthly Budget Statement, est. $37.5b, prior -$380.1b

- 08:30: Oct. Empire Manufacturing, est. 3.6, prior 11.5

- 11:00: Sept. NY Fed 1-Yr Inflation Expectat, prior 3.00%

Central Bank speakers

- 11:30: Fed’s Daly Gives Keynote Remarks

- 13:00: Fed’s Kugler Participates in Moderated Discussion

- 19:00: Fed’s Bostic Participates in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

Even though it was a partial US holiday with US fixed income closed, the S&P 500 (+0.77%) notched up its 46th record high of 2024 last night. The next hurdle is US earnings seasons that swings back into action today with Bank of America, Citigroup, Goldman Sachs and Johnson & Johnson all reporting.

Markets got another boost right before the US open, as a Caixin report came out saying that China may issue 6tn yuan of ultra-long special government bonds as part of its fiscal stimulus. So that helped to support risk appetite, and the S&P 500 is now up +22.85% on a YTD basis, making this its strongest performance at this point in the year since 1997. Moreover, in the last 50 weeks it’s managed to advance for 36 of them, which is a joint record back to 1989.

Tech stocks were the largest driver of that rally, with information technology (+1.36%) the strongest performing sector within the S&P 500. The Magnificent 7 (+0.82%) saw a decent advance, led by a +2.43% gain for Nvidia. This saw the chipmaker post a new all time closing high, capping off a +39.6% gain from its low on August 7. This also helped the NASDAQ (+0.87%) to close less than 1% beneath its all-time high from July. There is a report overnight that the US is mulling over whether to place more limits on chipmakers exports of advanced AI chips to certain countries but the story doesn’t seem to have impacted Nasdaq futures which are flat.

Even with the tech moves yesterday, equity gains were pretty broad beyond that, with 80% of the S&P 500 constituents higher on the day and the small-cap Russell 2000 rising +0.64%. Over in Europe, the story of tech outperformance dragging up the broader indices was a clearer one, with the STOXX 600 (+0.53%) ending the day also less than 1% below its own all-time high from last month.

Whilst risk assets were climbing to new highs, oil prices started the week on a lower note amid some disappointment around the urgency surrounding China’s stimulus details as well as pricing out of geopolitical risk premium. On the China angle, investors were also concerned about several data releases, including the weekend inflation data that showed price pressures were even weaker than anticipated. Then yesterday, we had another set of trade data for September, which showed imports were only up by +0.3% year-on-year (vs. +0.8% expected), and exports only rose by +2.4% as well (vs. +6.0% expected). So the numbers were underwhelming, and yesterday also saw OPEC cut its forecast for oil demand growth in its latest report.

With this backdrop, Brent crude fell -2.00% yesterday, and it is down another -2.9% overnight amid reduced perceptions of escalation risks in the Middle East. The overnight fall follows a Washington Post report that Israeli PM Netanyahu has agreed to limit its retaliation in response to the October 1 strikes to Iran’s military targets rather than its oil facilities or nuclear installations.

Moving onto rates, it was an uneventful session thanks to the bond holiday in the US. But futures markets were open, and there were some indications that investors were becoming a bit more sceptical about rapid rate cuts from the Fed. For instance, the probability of a rate cut in November was dialled back slightly to 87%, having been at 89% at Friday’s close. And looking further out, the rate priced in by the Fed’s June 2025 meeting was up +3.2bps on the day to 3.65%. The moves came as Fed speakers continued to steer us away from expecting rapid easing, with Minneapolis Fed President Kashkari saying that “further modest reductions” would be appropriate over the quarters ahead, while Fed Governor Waller noted that “policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting”. The oil move over the last 36 hours may temper some of these more hawkish rate expectations today but Treasuries have reopened fairly flat in Asia hours after the holiday.

One reason that investors have been dialling back their expectations for rate cuts is a growing focus on inflation risk. Henry pointed out yesterday that the US 5yr inflation swap has now seen its biggest jump over five weeks since early March 2023, just before SVB’s collapse. That’s been driven by several factors, but it’s clear that inflationary pressures have been building, with commodities bouncing back thanks to China’s stimulus and developments in the Middle East, whilst central banks have engaged in faster easing than was expected only a few weeks earlier, not least with the Fed cutting by 50bps last month. So with the ECB widely expected to become the latest central bank to cut rates again this week, that’s one to keep an eye on.

Ahead of the ECB’s decision, sovereign bond yields were fairly steady in Europe, with those on 10yr bunds (+0.8bps), OATs (-0.3bps) and BTPs (-1.4bps) not seeing big moves in either direction. The main exception to that pattern was here in the UK, where yields on 10yr gilts (+3.1bps) moved up to 4.24%. It also pushed the UK-German 10yr spread up to 197bps, which is the widest it’s been since August 2023.

In Asia, the Nikkei is leading the gains in the region, up by +1.58%, and reaching a three-month high as trading resumed after a holiday. The S&P/ASX 200 is also up by +0.77%, and the KOSPI has seen minor gains of +0.13%. In contrast, the Hang Seng is down by -1.24%, the CSI by -0.53%, and the Shanghai Composite by -0.52%, following weak inflation and trade data released over the past two days.

To the day ahead now, and data releases include the German ZEW survey for October, UK unemployment data for August, and Euro Area industrial production for August. There’s also Canada’s CPI release for September, and in the US there’s the Empire State manufacturing survey for October. Central bank speakers include the ECB’s Nagel, and the Fed’s Daly and Kugler. Finally, today’s earnings releases include Bank of America, Citigroup, Goldman Sachs and Johnson & Johnson.

Tyler Durden

Tue, 10/15/2024 – 08:07

via ZeroHedge News https://ift.tt/GlH0DIW Tyler Durden