Who Will Win And What Does It Mean?

By Peter Tchir of Academy Securities

Who Will Win and What Does it Mean?

We obviously need to start addressing the election more closely, but there are a few other “contests” or “battles” going on that deserve some attention as well.

Iran versus Israel

We published a SITREP on Friday night – Israel Commences Retaliatory Strikes on Iran based on what our Geopolitical Intelligence Group was hearing, seeing, and estimating using their collective experience. It does seem that the retaliation was very limited (i.e., not just the first in a series of attacks). Israel claims to have done serious damage to Iran’s ability to identify and target Israeli fighters and missiles, leaving them exposed to further attacks. Iran is messaging that they stopped almost all munitions from hitting their intended targets, and that the damage was minimal.

At this stage, the outcome is likely not much different regardless of which side is telling the truth (or if the truth is somewhere in between), as neither side seems intent on escalating further. Yes, there have been some comments out of Iran calling for preparations for war, but does either side really want to escalate at the moment?

Look for this to revert back to proxies and for oil prices to decline on the back of this controlled retaliation that is unlikely to provoke a direct response from Iran. I do like buying oil on any dip as this still does not put us on the path to a cessation of hostilities.

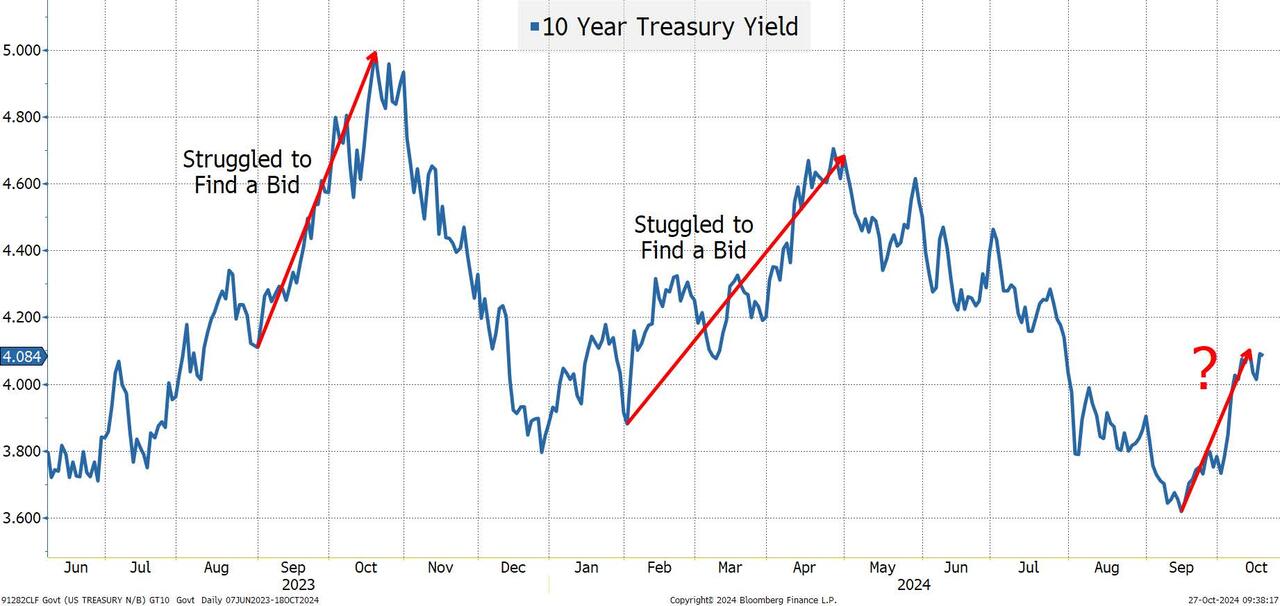

Bond Vigilantes

Bond vigilantes have appeared again!

From a “fundamental” standpoint, I’m at the point that Treasuries and bond yields are at the higher end of my range (instead of below, which they were just a couple of weeks ago). Fed cut projections have approached our base case (still a tiny bit more aggressive than we expect, but not by much).

What concerns me is that last autumn, we saw Treasury yields march higher. Relentlessly. Almost every day yields went higher. If there was bad news for bonds, it drove yields much higher. Good news for bonds sent yields briefly lower, then “poof,” there went the gains, and we saw higher yields.

While not as pronounced, we saw a similar pattern earlier this year.

While there were a lot of moving parts back then, there are a few similarities (ignoring the big difference, which is of course that the Fed has now cut rates).

- Inflation might not be dead. For the past month or so we’ve been harping on the idea that while we are not likely to see a big surge in inflation, the market is exposed to any reasonable uptick, which is our current base case.

- The debt ceiling. Certainly, the swoon last autumn had a lot to do with the debt ceiling debate. At some level, maybe the debt ceiling discussions just remind everyone that no one in D.C. actually cares about the debt. They just want an excuse to get a few more pet projects approved to raise it, until the next time, when they will re-enact the “drama” of caring, but will just spend more and raise it.

- Positioning. Many missed the rally. Many (including ourselves) missed how low yields would get (3.8% seemed too low, yet we got to 3.62% on 10s). Presumably, that stopped out most shorts, dragged in reluctant buyers, and had momentum buyers build up. Also, from experience dealing in the retail space, many retail investors (and their cheerleaders) seem to equate Fed cuts with lower yields across the curve, which is far from a given, as we’ve seen. That likely brought in buyers who now regret it.

- The election? We’ve argued that once people really start thinking about the economic policies, we will realize that regardless of the winner, we will have higher debt. While tariffs have received a lot of attention, let’s not forget that things like student loan “forgiveness” are really just shifting debt that was owed by individuals to debt that is now owed by the taxpayers. Any form of “sweep” is likely to spook bond markets to much higher yields.

- Foreign selling? Given everything that is going on in the world on the geopolitical front, maybe foreigners are selling again? China, launching their own stimulus, may be further reducing their holdings. They have gone from $1.1 trillion as recently as 2021, down to $775 billion as of the end of August.

I want to bet against the bond vigilantes (which seems to be betting against myself), but at the very least you need to own some options or something to protect you from a move to much higher yields.

We may be at the high end of our range (I might have to nudge that higher), but I remain convinced (as we’ve discussed recently) that the risk of a 50 bp move higher is far greater than the chance of getting a move 50 bps lower on 10s.

I guess I’m saying that I don’t think they will win, but I’m certainly hoping they will, and will bet a bit with my heart on this one!

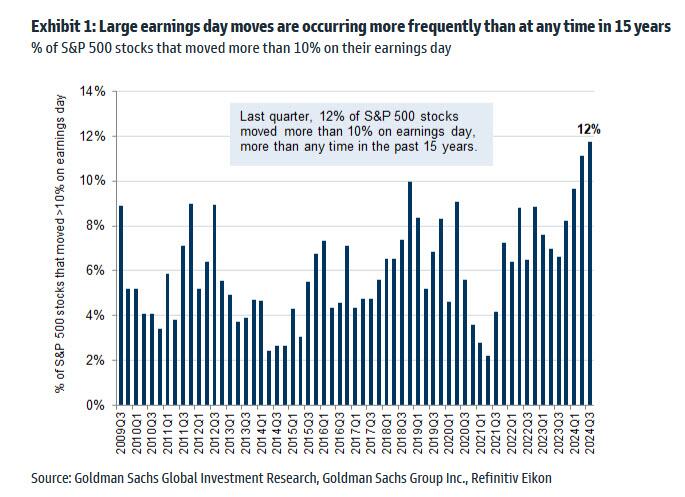

Earnings

We are once again seeing large moves post-earnings, often big enough to move the entire market (which I don’t think is a good statement on the health of the market). Though the overall market has often faded (which I also think is a really negative statement on the health of the market).

We have several key market leaders reporting earnings this week. Maybe they will all beat and go higher. Maybe each beat will drive the overall market higher. Somehow, I think the hurdle is high and the overall market feels “squishy” enough (the S&P 500 finished the week down 1%) that I think the market favors the bears (especially if the bond vigilantes keep “winning”).

The Election

Here we are just over a week from the election, and I only know 2 things for certain:

- Academy Securities and members of our Geopolitical Intelligence Group will be ringing the bell on the New York Stock Exchange on the morning of November 6th. I’m trying not to write “for whom the bell tolls” but I couldn’t help myself. In any case, it should be an interesting open.

- I will be guest hosting Bloomberg TV’s election coverage from 9pm to 10pm ET on election night. Hopefully by then some counts will roll in and we will have a clear picture of how the night is developing.

Let’s start with the betting markets.

Polymarket has garnered a lot of attention. As of Sunday morning, it had the “odds” of Trump winning at 65.1%. Other betting platforms such as Kalshi and Predictit also have Trump in the lead. Let’s think about the betting markets for a moment.

The negatives. There are many issues with the betting markets.

- Tightly controlled, or manipulated? There is a lot of concern about how much effort (or $$$) may be put into manipulating markets. Certainly, since people have started paying attention to what the betting markets are telling them, it makes sense that both parties (and their supporters) would be interested in “jacking up the odds” on their candidate. Which is why maybe Polymarket is attracting so much attention – it is a crypto-based betting platform. So, the argument is that Trump is more “pro-crypto,” and the crypto community is heavily betting on Trump (maybe betting with their heart or on the candidate they believe is in their best interest). It is difficult to deny that could be the case (though I’ve seen some arguing vehemently that it isn’t the case). If it is the case, then Polymarket could be propping up the odds on all other betting sites as someone tries to “arbitrage” the election. Bet against Trump at 63 on Polymarket and bet for him on another market at 57. That seems to give a lot of credit to these markets (more than I think they deserve).

- Translating prices into odds is tricky at best. In any market, supply and demand play a role. We wouldn’t spend too much time analyzing valuations and trading if we thought the stock (or bond) market was perfectly priced. It is far from clear that we do justice to the election when we equate these prices (which may have their own set of issues) to percentage chances of winning (which may or may not be a correct translation of the prices). If you want to get into the weeds on this (and I mean, really into the weeds), I was pointed to Market Prices are Not Probabilities by people who I trust to point me in the right direction on these sorts of things.

- In elections, one person equals one vote. In betting, one dollar equals one vote. There are risks that those with dollars (that are willing to spend them) outweigh others in betting markets, skewing the results.

The positives (at least versus polls).

- I have no idea why we still have “’national” polls!!! Actually, I have several ideas on why we still have them. They are easier to conduct and get results with tolerable margins for error. They include places like New York and California, where many of the companies that do the polling are based, and are important in many ways, except (at least currently) for the election results. Seriously, good, state level polling data is the only thing that is relevant given the electoral college. We still get a lot of national polling data, which sounds interesting, but is fairly useless in predicting the winner of each state (especially since elections only happen every 4 years and it is difficult to calibrate what national polling means for each state with such a small sample size). The state polling we get, I think, is of dubious quality. If you think the national polling is of dubious quality (I do, due to sample size, collection techniques, etc.), it is likely to be far less accurate when conducted on a state level (especially since the state level surveys don’t seem as well funded or as well developed as the national surveys). So maybe the betting gives us a better assessment of what is happening at the Electoral College level compared to current polling? That to me is what probably scares people the most who completely dismiss the betting markets – the fact that the betting markets might cut through all the polling, media, ads, etc. better than the pundits?

I’m left paying attention to the betting markets, but I am not convinced that they are correct.

I keep trying to imagine what it will be like to vote for those who are “undecided.” I am a Canadian citizen and cannot vote.

At this point, I think “undecided” is a euphemism for “I really don’t like the candidate my party has selected.” Whether it is personality, experience, policies, age, whatever it is, I suspect that most undecided voters who are registered are at least considering voting against their party’s presidential nominee. Otherwise, why would you be registered and undecided at this stage? It is less clear what is going on in the minds of people who are not registered to a party and are still undecided. I don’t see a lot of enthusiastic people running into the ballot box trying to decide between the Lamborghini or the Bentley. Both are great choices, and it is difficult to choose between them, but you really can’t go wrong. Maybe I’m out on a limb here and apologize to anyone offended, but I suspect that most people who are undecided going into the booth are spending more time worrying about the risks of voting one way or another.

Do you cringe as you check the box? If that is the behavior of many voters at the margin, then I think both the polling and even the betting markets are going to have difficulty predicting how people will behave when the moment comes down to having to finalize your decision.

If I’m correct in assessing the mindset of the undecided (especially undecided, but registered to a party) voters, then I expect to see a lot of split tickets – leading to gridlock!

The ability for either party to sweep, when neither presidential candidate seems to have mobilized a large majority of the population, seems low, which is good for markets.

What will the winner do? Far, far, far less than what they have discussed (or spouted) on the campaign trail. Yes, there will be differences, but they are less likely to be radical and they will likely take more time to implement than people expect.

Three months ago, you could have argued that there would be a massive difference in the border policies. While differences will remain, especially regarding how some in this country are treated, the policies, as touted on the campaign, have moved closer.

Ultimately, the market and the economy will be driven by whether the politician who wins can create a vision and execute a plan for that vision. Reshoring, chips, how we treat our allies, how we project power and deterrence, rare earths and critical minerals, space, etc. There are many issues, too few of which have been addressed comprehensively (for my tastes), let alone turned into action plans. Whatever the market does in the days after the election won’t matter. What will matter is whether the winner starts putting together a plan and a team to execute that plan, and that I think, quite frankly, remains a question mark. Both candidates (and parties) seem to have their positives and negatives. Typically, whatever fears and hopes we have coming into the election evolve as the winner takes power and the rest of the world goes about its business.

When will we know who won?

I see scenarios where very early on, we see some “shocking” results that quickly tell us someone is going to win in a landslide. That some blocks of voters completely surprise everyone and turn this from a potentially close election, dependent on a handful of voters in a handful of states, to an obvious wave.

Having said that, it seems much easier to envision a world where we don’t know things at the presidential level (and certainly not at the Senate or House level) until the next morning, or even days after the election. It is easy to see a world where some key states or races need recounts. That the margin of victory is small enough that results need to be double-checked.

Given the vitriol about the validity of all the voting heading into this election, there is some small risk (I think it is low, but above 0) that the results and counts become very contentious. Hopefully, it all remains in the realm of legal action, where it belongs (to the extent that the legal questions are legitimate).

I expect that even in an incredibly close election, the proper procedures will be followed, and a winner will be determined, even before Academy rings the bell the morning of the 6th. I suspect that there will be some “surprise” force at work, making the election more cut and dried than people believe (or fear). If I knew what that surprise would be, then it wouldn’t be a surprise.

I guess I’m still stuck on gridlock and candidates shifting actual policy focus closer to the middle than their campaign rhetoric has suggested.

Bottom Line

Despite the election looming, bond vigilantes and earnings are likely to be bigger drivers of this market than anything else as we head into month-end.

Tyler Durden

Mon, 10/28/2024 – 07:45

via ZeroHedge News https://ift.tt/pGri8UW Tyler Durden