Campari Shares Crash With Cash-Strapped Consumers Denting Profit

Shares of Italian beverage giant Davide Campari-Milano crashed on Wednesday following a disappointing third-quarter report that underscored the deepening global luxury slowdown. The company reported negative organic sales growth, attributing the decline to “pressure on disposable income from inflation and consumer and distributors reduced confidence.”

Campari’s portfolio includes over 50 brands, including Aperol, Appleton, Cinzano, SKYY vodka, Espolón, Wild Turkey, Grand Marnier, and Forty Creek whisky. It reported adjusted earnings before interest and taxes that tumbled 13% in the third quarter compared with the same period one year ago to 139.4 million euros, missing the Bloomberg-compiled consensus estimate of 178.5 million euros.

Here’s a snapshot of third-quarter results (courtesy of Bloomberg):

-

Adjusted Ebitda EU171.8 million, -9.7% y/y, estimate EU209 million (Bloomberg Consensus)

-

Adjusted Ebit EU139.4 million, -13% y/y, estimate EU178.5 million

-

Sales EU753.6 million, +1.4% y/y, estimate EU820.3 million

-

Adjusted pretax profit EU114.4 million, -23% y/y

-

Pretax profit EU107.9 million, -20% y/y

And financial results for the nine months of the year.

-

Adjusted Ebitda EU590.7 million, -1.8% y/y

-

Adjusted Ebit EU499.4 million, -4.1% y/y

-

Sales EU2.28 billion, +3.4% y/y

-

Americas rev. EU1.03 billion

-

Asia Pacific rev. EU147.6 million

-

EMEA rev. EU1.10 billion

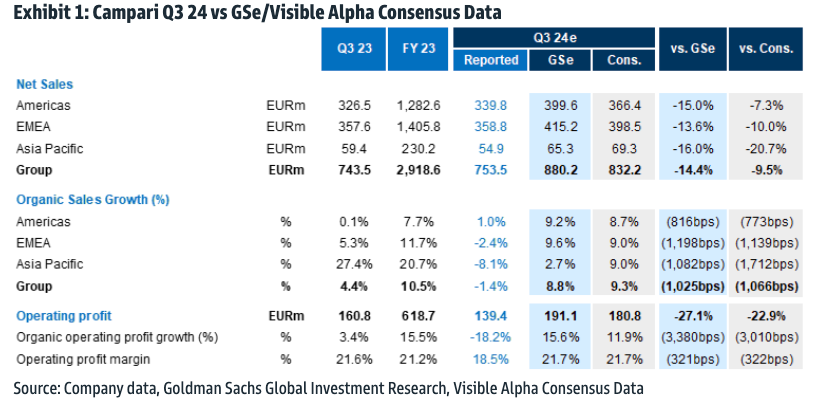

Shedding more color on the earnings report, Goldman analysts Olivier Nicolaï and Aron Adamski wrote in a note to clients this morning that quarterly earnings were very weak and missed across all geographies…

Campari reported weak Q3 results with -1.4% in organic sales, significantly below +9.3% Visible Alpha Consensus Data. EMEA sales declined -2.4% (vs +9% cons) with a -7% decline in Italy due to wholesaler de-stocking and customer de-listing, while sell-out was down -1%. Americas sales grew +1% (vs +8.7% cons) with a drag from Jamaica (-20%) caused by product availability constraints following a hurricane. USA sales were flat, with strong growth of Aperol and Campari offset by weak performance of SKYY as well as soft trends in Wild Turkey and Grand Marnier. APAC sales were -8.1% (vs +9% cons) due to a challenging macro in China and route-to-market change in India, while the competitive environment stepped-up in Australia (-4%) particularly in Wild Turkey. EBIT margin was 18.5% leading to a -23% miss on reported EBIT.

Guidance downgrade and share buyback €40m; Campari expects low-single digit organic sales growth in FY24 (+2% GSe), implying return to some growth in Q4. The company thinks US consumption will remain soft, while Jamaica should see the tail-end impact of the hurricane. While Italy de-stocking is done, EMEA should see further inventory reduction, ongoing competition & low consumer confidence in select markets. Management expects EBIT margin (-150bps GSe) to be negatively affected by adverse mix and operating de-leverage, despite a raw materials tailwind. While Q1 25 will likely remain soft, Campari is confident in a gradual return to mid-to-high single digit sales growth in the medium term with EBIT margin progression. The company also announced a €40m share buyback by November 2025.

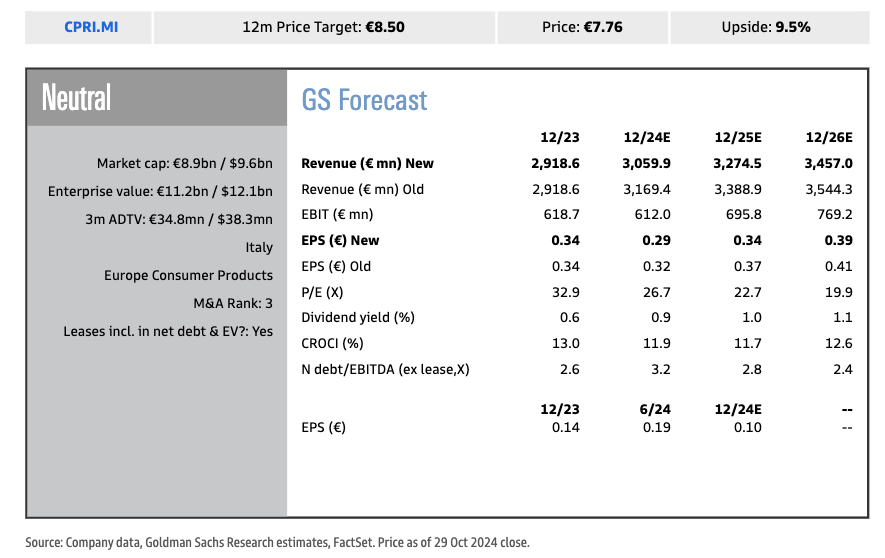

Cut EPS FY24/25 estimate by -9%/-7%; At 23x CY25E P/E and 14x EV/EBITDA, we remain Neutral rated on Campari in light of limited visibility into FY25 amid ongoing weakness in US Spirits consumption and increased competition there and in Europe.

We highlight key developments during Q3 below…

Americas (44% of FY23) delivered +1% OSG in 3Q, driven by strength in Espolòn, Aperol and Campari, partially offset by SKYY, Wild Turkey and the hurricane in Jamaica. In the US, Q3 sales were flat, with consumer confidence subdued in both the on and off-trade. The July hurricane in Jamaica impacted distilling and bottling capacity, leading to supply shortages in the local Jamaican market as well as in the UK and US. Management highlighted that the disruption will end in Q4 albeit outlining longer-term issues in reaching full distilling capacity.

EMEA (48% of FY23 sales) sales declined -2.4% in Q3 on an organic basis. In Italy sales were down -7.0% in the third quarter impacted by unfavourable weather conditions in Spring/Summer and September which was exaggerated by aggressive destocking. The region also saw a retailer dispute, which resulted in a €1m sales impact in Q3. Germany declined -6.2%, against a high-base, while France saw a soft sector backdrop. In the UK, sales declined -9.7%, impacted by poor weather and supply shortages in Jamaican Rums and Magnum Tonic Wine linked to the Jamaican hurricane. Management expects no recovery of the shortfall in Q3 sales, due to the seasonality of Aperitifs. They expect to see a continuation of the impact from destocking, as well as low consumer demand and competition in selected markets.

APAC (8% of FY23 sales) declined -8.1% organically, driven by a particularly soft Australia and China. Australia declined -4% on an organic basis, with Aperol and Campari delivering double-digit growth momentum despite a challenging macro and competitive environment. Excluding the co-packaging segment, the country would have grown +8% in Q3, with the Espolòn RTD gaining traction. The rest of APAC saw a -12% organic decline, with India, South Korea and China offsetting growth in Japan.

In markets, shares crashed as much as 15% in Italy – the biggest one-day decline since early 2020.

Is the party over?

Back to the earnings report, Campari blamed weak disposable income on the inflation storm across the West, with consumers dialing back on expensive liquor. Then, of course, weak consumers in China as the property market and economic turmoil show no signs of abating anytime soon, despite Beijing offering another round of stimulus on Tuesday.

One week ago, the world’s largest luxury goods company, LVMH, missed earnings estimates for third-quarter organic sales amid a worsening slowdown in China. Analysts at Goldman called LVMH’s earnings report a “clear negative” for the global luxury industry.

Tyler Durden

Wed, 10/30/2024 – 07:20

via ZeroHedge News https://ift.tt/RQBL8U5 Tyler Durden