Submitted by Brandon Smith of Alt Market

The Hidden Motives Behind The Federal Reserve Taper

“The powers of financial capitalism had (a) far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent meetings and conferences. The apex of the systems was to be the Bank for International Settlements in Basel, Switzerland; a private bank owned and controlled by the world’s central banks which were themselves private corporations. Each central bank… sought to dominate its government by its ability to control Treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence cooperative politicians by subsequent economic rewards in the business world.” – Carroll Quigley, member of the Council on Foreign Relations

If one wishes to truly understand the actions behind private Federal Reserve policy, one must come to terms with a fundamental reality – everything the Fed does it does for a reason, and the most apparent reasons are not always the primary reasons. If you think that the Fed simply acts on impulsive stupidity or hubris, then you haven’t a clue what is going on. If you think the Fed only does what it does in order to hide the numerous negative aspects of our current economy, then you only know half the story. If you think the Fed does not have a plan, then you are sorely mistaken…

Central Bankers and their political proponents espouse a globalist ideology, meaning, they are internationalists in their orientation and motivations. They do not have loyalties to any particular country. They do not take an oath to any particular constitution. They do not have empathy for any particular culture or social experiment. They have their own subculture, with their own “values”, and their own social hierarchy. They are a kind of “tribe” or “sect”; a cult,if you will, that views itself as superior to all others. This means that when the central bankers that run the Fed act, they only act with the intention to support and promote globalization, not the best interests of America and Americans.

The process of globalization REQUIRES the dissolution of the U.S. economy as it exists today. Period. There is no way around it. America can no longer remain a superpower in the face of what globalists call “harmonization”. The dollar can no longer maintain its petro-currency status or its world reserve status if total centralization under a new global currency is to be achieved. Globalists believe that America must be sacrificed on the altar of “progress”, and diminished into a mere enclave, a feudal colony of a greater global system. The globalists at the Fed are no different.

Once this driving philosophy is understood, the final conclusion is obvious – the Fed exists to destroy the U.S. financial system and the U.S. currency mechanism. That is what they are here for.

This is why the dollar has lost 98% of its value since the Fed was established in 1913. This is why the Fed deliberately engineered the derivatives bubble crisis through the implementation of artificially low interest rates. This is why their response to the crisis was to create yet another massive bubble in stocks and bonds through QE stimulus. This is why the Fed is cutting stimulus today.

How does the taper play into the long running program of dollar destruction and globalization? Let’s take a look…

The Multifaceted Taper Strategy

In my article ‘Is The Fed Ready To Cut America’s Fiat Life Support’, and my article ‘Expect Devastating Global Economic Changes In 2014’, I predicted that a Fed taper was highly likely. Central banks almost always implant policy shift rumors into the mainstream media a few months before they implement them. They did this for TARP, for QE1, QE2, QE3, and the Taper. In fact, the Fed spent the better part of the past quarter conditioning investors to the idea of stimulus cuts, so I was not at all surprised when they followed through.

The Fed has, of course, now announced a $10 billion QE reduction just in time for Christmas and the 100th anniversary of the privately run institution. In the past, I have pointed out the tendency of central banks to enforce detrimental policy changes while the government, the economy and/or the bank itself is in the midst of a major transition. The Fed’s taper announcement comes just in time for the end of Ben Bernanke’s term as chairman, and the expected nomination of Janet Yellen.

This is done, I believe, because it provides an opportunity to divert blame for a crisis event they know is on the horizon. If attention is ever focused on the Fed specifically for a market downturn or bond disaster triggered by the ever present dollar bubble, Yellen can simply blame the QE policies of Bernanke (who will be long gone), while promising that her “new” policies will surely repair the damage. This placates the public and buys the central bankers time to do even MORE damage.

The taper itself is not just a “head fake”, however. It is a far more complex action. Tapering provides a method of psychologically distancing the Federal Reserve from the consequences of market movements. The banksters are essentially proclaiming to the public that their work is done, they have saved the economy, and now they are moving on, be it only $10 billion at a time. Whatever happens from here on is “not their fault”.

Most alternative analysts expected no taper of QE, and for good reason. While the mainstream touts the propaganda of economic recovery, independent financial experts understand that little to nothing was actually accomplished by the bailouts. Virtually no stimulus was absorbed in a localized way by mainstreet business. Real unemployment counting U-6 measurements still stands at around 20%. Real estate markets and home prices have a received a small boost, which at first glance appears positive until one examines who is actually buying; namely big banks and international investment firms snapping up properties only to reissue them on the market as rentals:

http://dealbook.nytimes.com/2013/06/03/behind-the-rise-in-house-prices-wall-street-buyers/?_r=0

U.S. holiday retail sales and annual retail sales have been the weakest since 2009:

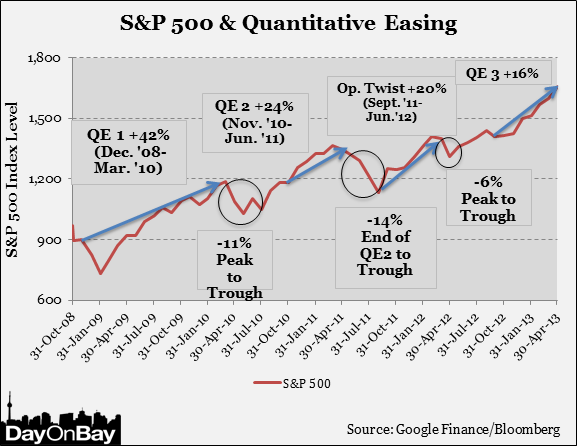

The only thing that QE ultimately accomplished was a spectacular rise in stocks through direct manipulation, which Fed agents like Alan Greenspan and Richard Fisher now openly admit to. The problem is, while gamblers in equities proudly boast about the Fed induced bull run in the Dow and how much money they have made, they remain oblivious to the underlying cost of the charade. Market investors have been enriched, yes, but little do they know that stock legitimacy is about to be sacrificed.

The price to earnings ratio of stocks (the market value of stocks versus what they SHOULD be valued according to the actual earnings of the companies listed) in the S&P 500 today stands at around 15, which is the highest it has been since before the 2008 market crash. Mainstream economists attempt to dismiss the issue by using a 15 year average while claiming that the P/E ratio in 2013 is mild compared to the tech bubble of the late 90’s. What they don’t seem to grasp is that the market of the past four to five years is an entirely different animal compared to 15 years ago.

Stocks in general have received considerable support through purchases by Fed bolstered banks and the Fed itself, creating an atmosphere of artificial demand for equities using QE fiat injections. Though no full audit of the bailouts exists (TARP is the only measure audited so far), it is projected that the banking sector alone has garnered tens of trillions in Fed fiat, which they have used to bolster their otherwise debt ridden holdings. It is only logical to expect that this capital tsunami has been used by numerous companies as a way to present false earnings. Goldman Sachs, JP Morgan, and Morgan Stanley all reported substantial profits for 2009 while at the same time reporting massive liabilities caused by the derivatives crash so that they could collect on the bailout bonanza.

So which one is it? Are companies making profits, or are they wallowing in insurmountable debt while presenting government stimulus as a form of profit?

What the Fed and corporate banks have done is create a market in which neither earnings, nor stock values can be trusted. The fact that the P/E ratio is higher than it has been since 2008 despite this manipulation should concern anyone with any sense.

Worst of all, the Fed’s monetization of U.S. Treasury debt has only expanded while foreign investment in long term debt has contracted. With our official national debt growing by at least $1 trillion per year, our country cannot continue to function without an ever increasing amount of foreign investment, or, Federal Reserve printing. The Fed cannot make cuts to QE if our system is to survive (if you want to call it survival), the Fed must expand QE forever, or at least until the dollar implodes due to hyperinflation.

So then, why has the taper been introduced at all? No one wants it. The government shouldn’t want it. Investors certainly don’t want it. Our economy is utterly dependent on the opposite. What purpose does it serve?

The assumption has always been that the Fed wants to keep the system afloat. I submit that things have changed. I submit that the Fed no longer wishes to prop up our fiscal structure, or at least, no longer wishes to be seen as propping it up. I submit that the Fed is not pursuing dollar destruction through standard hyperinflation, but rather, they are preparing the U.S. for default, which also will result in currency implosion.

The Taper Parallels

“It must not be felt that the heads of the world’s chief central banks were themselves substantive powers in world finance. They were not. Rather they were the technicians and agents of the dominant investment bankers of their own countries, who had raised them up, and who were perfectly capable of throwing them down. The substantive financial powers of the world were in the hands of these investment bankers who remained largely behind the scenes in their own unincorporated private banks. These formed a system of international cooperation and national dominance which was more private, more powerful, and more secret than that of their agents in the central banks. “ – Carroll Quigley, Tragedy And Hope

Initial shock over the taper scenario has not sunk into the markets yet (as Zero Hedge points out, the last time a major central bank cut stimulus measures to a dependent country, stocks rallied, then crashed within months). Few people see much difference between $75 billion per month and $85 billion per month, but the size of the cuts is not really the issue. Rather, it is the Fed’s act of fading into the background that should concern us.

The taper announcement parallels perfectly with the accelerating debate over the U.S. debt ceiling, and I do not think this is at all a coincidence. Tapering seems inconceivable to many, but for the Fed it makes perfect sense if the goal of the globalists is to generate a default scenario while diverting blame. I believe that Americans are being prepared psychologically for just such an event. Already, the White House is warning that government funding will essentially disappear by the end of February:

http://www.reuters.com/article/2013/12/19/us-usa-fiscal-idUSBRE9BF1FW20131219

The expectation fostered by the mainstream media is that a debt fight similar to the October theater will not happen again. I agree. I believe the next debate will be much worse. The vast majority will assume that the “can” will be kicked down the road again, and they may be right, but given the Fed’s behavior, and given that they have begun to taper despite what appears logical, many people may be in for a shock when our government also suddenly decides one day soon to buck assumptions and default rather than prolong the pain.

The full spectrum failure of Obamacare only adds excuse and incentive. There is no longer a legislative centerpiece rationale for further spending. Obama’s approval rating is at historic lows for any president. The stage has been set for the most epic of fake political battles.

The Left and Right leadership, at the top of the pyramid, are nothing more than flunkies for the global elite. If globalists have decided that it is time to apply the final death blows to the dollar, default would be the quickest and most efficient way, and political puppetry can easily make it happen. The calamity would be blamed on “partisan bickering” and “government gridlock”, or even the inefficiency of “democracy”. The Fed, with its taper in place and its fake recovery established, would be presented as the only “sane” institution at America’s disposal.

Perhaps at this point even more pervasive QE programs would recommence, perhaps not. At bottom, though, the taper is not a peripheral issue. It is an action at the center of a much more elaborate process, an action that seems to have been undertaken in preparation for a larger event. The next year is shaping up to be the most chaotic since the debt crisis began in 2008, and as the situation progresses, the subtleties of the Federal Reserve and the international banks that back it must not go unnoticed, or in the end, unpunished.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Hi00kjSXY9Y/story01.htm Tyler Durden

{kind=link}