Larry Summers, who was nearly picked by Obama as the next Fed Chairman before for some inexplicable reason the Economist lobby deemed him “hawkish” and that he would put a halt to the Fed-Treasury cross monetization complex, is no stranger to providing hours of entertainment with his aphoristic quotes. Recall from October 2011, where he said that the solution to record debt is more debt:

“The central irony of financial crisis is that while it is caused by too much confidence, too much borrowing and lending and too much spending, it can only be resolved with more confidence, more borrowing and lending, and more spending.” Larry Summers, source

Or his follow up from June 2012, where he submitted that insolvent governments can “improve their creditworthiness” by becoming more insolvent:

“Rather than focusing on lowering already epically low rates, governments that enjoy such low borrowing costs can improve their creditworthiness by borrowing more not less.” Larry Summers, source.

This of course led to his pronouncement last month that the US economy needs “bubbles” to “grow“, which promptly won him accolades from none other than his former basher Paul Krugman, best known for this line from 2002: “To fight this recession the Fed needs…soaring household spending to offset moribund business investment. Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.” Yes, somehow this person was seen as hawkish.

Either way, it seems Larry was modestly disgruntled with the prevailing assessment of the media world ascribing to him the title of the next Krugs, in proposing a policy of endless bubble booms and busts, and as a result, he decided to take to the pages of that hallowed bastion of “free and efficient markets”, the FT, to explain what he really meant. His full essay is below but the punchline is as follows:

Some have suggested that a belief in secular stagnation implies the desirability of bubbles to support demand. This idea confuses prediction with recommendation. It is, of course, better to support demand by supporting productive investment or highly valued consumption than by artificially inflating bubbles. On the other hand, it is only rational to recognize that low interest rates raise asset values and drive investors to take greater risks, making bubbles more likely. So the risk of financial instability provides yet another reason why preempting structural stagnation is so profoundly important.

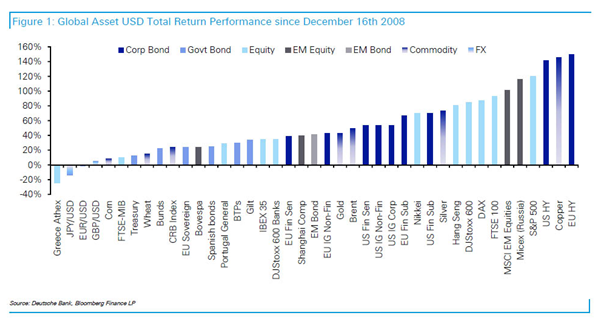

Apparently “some” does not include Larry, but what his clarification seems to clarify, is that while proposing bubbles as a policy tool is short-sighted, should they indeed arrive (and many have stated that the current “stock market” on the back of $10 trillion in central bank liquidity and another $25 trillion in Chinese bank asset increases is nothing else), well then – we’ll cross that bridge when we come to it. In the meantime, “stagnation may be the new normal.” Stagnation for the 90% mind you – not the 10% whoe actually benefit day in and day out from the Fed’s ceaseless attempt to get the world to said bridge as fast as possible…

From Larry Summers:

In the past decade, before the crisis, bubbles and loose credit were only sufficient to drive moderate growth

Is it possible that the US and other major global economies might not return to full employment and strong growth without the help of unconventional policy support? I raised that notion – the old idea of “secular stagnation” – recently in a talk hosted by the International Monetary Fund.

My concern rests on a number of considerations. First, even though financial repair had largely taken place four years ago, recovery has only kept up with population growth and normal productivity growth in the US, and has been worse elsewhere in the industrial world.

Second, manifestly unsustainable bubbles and loosening of credit standards during the middle of the past decade, along with very easy money, were sufficient to drive only moderate economic growth.

Third, short-term interest rates are severely constrained by the zero lower bound: real rates may not be able to fall far enough to spur enough investment to lead to full employment.

Fourth, in such situations falling wages and prices or lower-than-expected are likely to worsen performance by encouraging consumers and investors to delay spending, and to redistribute income and wealth from high-spending debtors to low-spending creditors.

The implication of these thoughts is that the presumption that normal economic and policy conditions will return at some point cannot be maintained. Look at Japan, where gross domestic product today is less than two-thirds of what most observers predicted a generation ago, even though interest rates have been at zero for many years. It is worth emphasizing that Japanese GDP was less disappointing in the five years after the bubbles burst at the end of the 1980s than the US GDP has since 2008. In America today, GDP is more than 10 per cent below what was predicted before the financial crisis.

If secular stagnation concerns are relevant to our current economic situation, there are obviously profound policy implications. But before turning to policy, there are two central issues regarding the secular stagnation thesis that have to be addressed.

First, is not a growth acceleration in the works in the US and beyond? There are certainly grounds for optimism: note recent statistics, the strong stock markets and the end at last of sharp fiscal contraction. One should also recall that fears of secular stagnation were common at the end of the second world war and were proved wrong. Today, secular stagnation should be viewed as a contingency to be insured against – not a fate to which we ought to be resigned. Yet, it should be recalled that the achievement of escape velocity has been around the corner in consensus forecasts for several years and we have seen several false dawns – just as Japan did in the 1990s. More fundamentally, even if the economy accelerates next year, this provides no assurance that it is capable of sustained growth at normal real interest rates. Europe and Japan are forecast to have grown at levels well below the US. Across the industrial world, inflation is below target levels and shows no signs of picking up – suggesting a chronic demand shortfall.

Second, why should the economy not return to normal after the effects of the financial crisis are worked off? Is there a basis for believing that equilibrium real interest rates have declined? There are many a prior reasons why the level of spending at any given set of interest rates is likely to have declined. Investment demand may have been reduced due to slower growth of the labor force and perhaps slower productivity growth. Consumption may be lower due to a sharp increase in the share of income hel

d by the very wealthy and the rising share of income accruing to capital. Risk aversion has risen as a consequence of the crisis and as saving – by both states and consumers – has risen. The crisis increased the costs of financial intermediation and left major debt overhangs. Declines in the cost of durable goods, especially those associated with information technology, mean that the same level of saving purchases more capital every year. Lower inflation means any interest rate translates into a higher after-tax rate than it did when inflation rates were higher; logic is supported by evidence. For many years now indexed bond yields have been on a downward trend. Indeed, US real rates are substantially negative at a five year horizon.

Some have suggested that a belief in secular stagnation implies the desirability of bubbles to support demand. This idea confuses prediction with recommendation. It is, of course, better to support demand by supporting productive investment or highly valued consumption than by artificially inflating bubbles. On the other hand, it is only rational to recognize that low interest rates raise asset values and drive investors to take greater risks, making bubbles more likely. So the risk of financial instability provides yet another reason why preempting structural stagnation is so profoundly important.

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/sv-XRJr4_mw/story01.htm Tyler Durden