Submitted by AWD via The Burning Platform blog,

Maybe 2015 will be the year of the collapse.

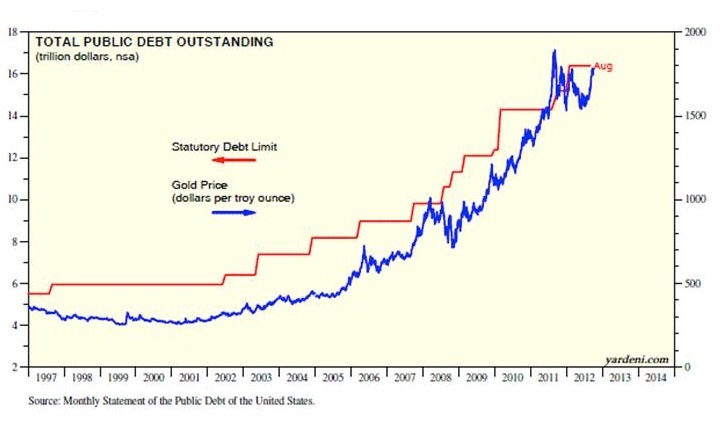

Our entire economy runs on debt creations, vis-a-vis financialization, since we import $500 billion a year more than we export.

2015 is the year when increasing debt results in ZERO GDP growth. The end of the line. But that won’t stop the Federal Reserve and the criminals in Washington. Enjoy what time we have left before it all collapses.

Government Intervention in Economic Downturns…Makes Things Worse

Every time government intervenes in an economic downturn, the downturn (or recession) gets longer, and deeper. History has borne this out, yet politicians can’t resist the impulse to “do something” when recession comes. Left to its own devices, the economy will recover much more quickly than if we tinker with monetary policy or inject massive amounts of taxpayer dollars into the equation. Thomas Sowell makes this case one more time in a piece at Townhall:

The idea that the federal government has to step in whenever there is a downturn in the economy is an economic dogma that ignores much of the history of the United States.

During the first hundred years of the United States, there was no Federal Reserve. During the first one hundred and fifty years, the federal government did not engage in massive intervention when the economy turned down.

No economic downturn in all those years ever lasted as long as the Great Depression of the 1930s, when both the Federal Reserve and the administrations of Hoover and of FDR intervened.

The myth that has come down to us says that the government had to intervene when there was mass unemployment in the 1930s. But the hard data show that there was no mass unemployment until after the federal government intervened. Yet, once having intervened, it was politically impossible to stop and let the economy recover on its own. That was the fundamental problem then– and now.

The Keynesians that are busy trying to turn the magic levers in our economy right now still aren’t getting the message, more than two years later: government spending can’t make the economy grow. Until they stop trying (and racking up immense, almost unfathomable amounts of debt), things are likely to continue to get worse. What we need is some level of certainty about policies that the current administration is trying to enact. Businesses don’t invest in growth, and thus hire new employees, because they don’t know what’s going to happen.

The policies of this administration make it risky to lend money, with Washington politicians coming up with one reason after another why borrowers shouldn’t have to pay it back when it is due, or perhaps not pay it all back at all. That’s called “loan modification” or various other fancy names for welching on debts. Is it surprising that lenders have become reluctant to lend?

Private businesses have amassed record amounts of cash, which they could use to hire more people– if this administration were not generating vast amounts of uncertainty about what the costs are going to be for ObamaCare, among other unpredictable employer costs, from a government heedless or hostile toward business.

As a result, it is often cheaper or less risky for employers to work the existing employees overtime, or to hire temporary workers, who are not eligible for employee benefits. But lack of money is not the problem.

Uncertainty is killing opportunities for growth. We don’t need more government intervention in the form of stimulus, or easing, or regulation. We need to government to get out of the way.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/0F_FDPqqTmw/story01.htm Tyler Durden