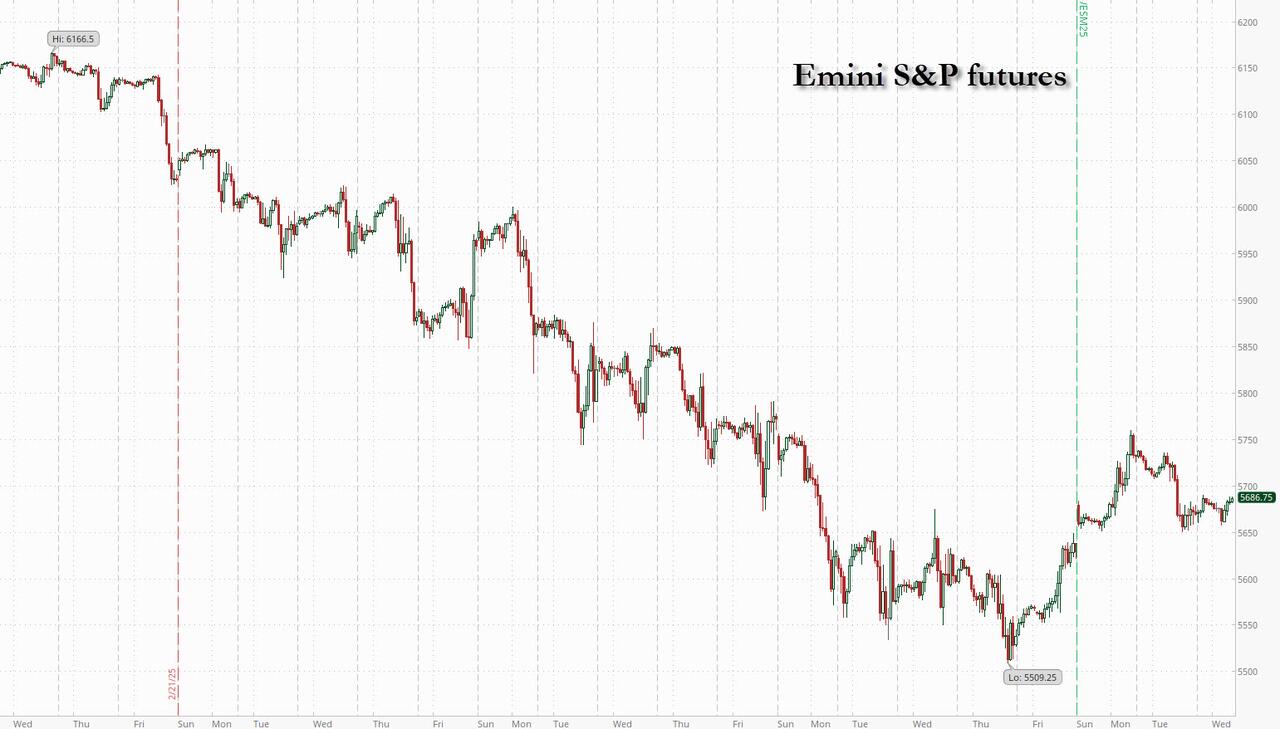

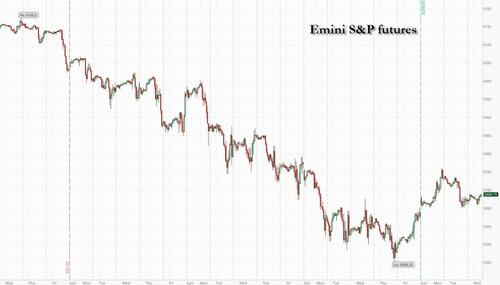

US equity futures are higher into Fed day, rebounding from Tuesday’s losses, with both tech and small caps outperforming, while European stocks inch higher having recovered from an earlier drop after Turkey assets and FX imploded following the latest political crackdown in the banana republic. As of 8:00am ET, S&P and Nasdaq futures are 0.3% higher with all Mag7 names higher premarket led by TSLA (+3%) after the electric-vehicle maker received California’s approval to start carrying passengers. NVDA rose +1% after CEO Jensen Huang promised a clearer payoff to customers. The shares had dropped 3.4% Tuesday. China ETF KWEB is outperforming QQQ pre-mkt on Tencent earnings. Financials are also catching a bid with bond yields flat and the USD is higher for the first time in 4 sessions, boosted in part by the 10% plunge in the Turkey lira, which is spilling over across EMs. Commodities are weaker as 3 complexes are under pressure; WTI is flat reversing an earlier loss on Ukraine energy-based de-escalation. Reuters is reporting that the US is suspending some multi-agency and multi-country efforts to counter Russian sabotage, potentially to help a deal move through. Today’s pre-market rally may gain strength depending on whether the FOMC dots are modestly lowered, whether Powell’s press conference is seen as dovish and any adjustments to QT.

In premarket trading, Tesla is leading gains among the Magnificent Seven stocks after the electric-vehicle maker was granted approval in California to begin carrying passengers in its vehicles in a step toward ride-hailing services (Alphabet +0.3%, Amazon +0.2%, Apple +0.3%, Microsoft +0.2%, Meta +0.1%, Nvidia +1% and Tesla +3%). Black Diamond Therapeutics (BDTX) rises 27% after the company entered into a licensing agreement with Servier, a pharmaceutical group governed by a non-profit foundation. Here are some other notable premarket movers:

- Cargo Therapeutics (CRGX) soars 19% after appointing Anup Radhakrishnan as interim CEO to lead the company through a reverse merger or other business combination.

- General Mills (GIS) slips 3% after the packaged-food company cut its organic net sales forecast for the full year.

- Gilead Sciences (GILD) drops 2% after the Wall Street Journal reported that the US Department of Health and Human Services was weighing plans to cut federal government funding for domestic HIV.

- HealthEquity (HQY) drops 14% as fraud-related costs weighed on results.

- Signet Jewelers (SIG) jumps 14% after the owner of Kay Jewelers said sales are recovering following a disappointing holiday season

- StoneCo (STNE) climbs 10% after the Brazilian fintech posted 4Q adjusted net income that beat.

- Venture Global (VG) gains 6% after Bloomberg reported that the Trump administration is prepared to give the company conditional approval to export natural gas from a planned facility in Louisiana that had stalled under former President Joe Biden.

Today’s main event is the FOMC decision (full preview here), where the Fed is expected to hold interest rates steady, while its latest dot plot should offer clues on the central bank’s thinking on the economy. Powell’s news conference will also be scrutinized for his views on the potential impact of the trade tariffs and how much support could be offered to the economy this year.

“Investors continue to search for a policy circuit breaker, either from the White House or the Fed,” said Robert Griffiths, an equity strategist at L&G Investment Management. Griffiths noted the Fed’s dovish pivot in late-2019 had come after a 30% drop in the Nasdaq, a far steeper decline than the index has suffered this year. What’s more, the full impact of the tariffs on inflation and the economy remains unclear, implying “the Fed’s ability to act pre-emptively on this occasion is extremely limited,” he added.

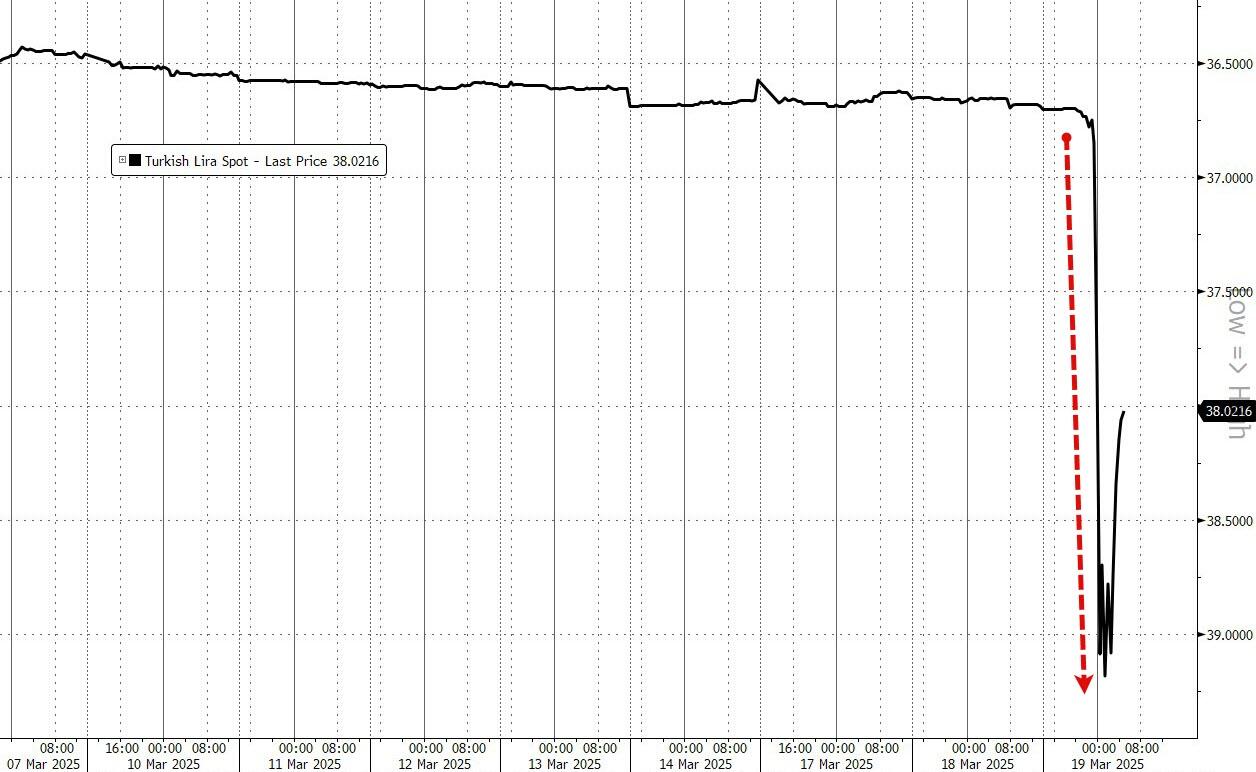

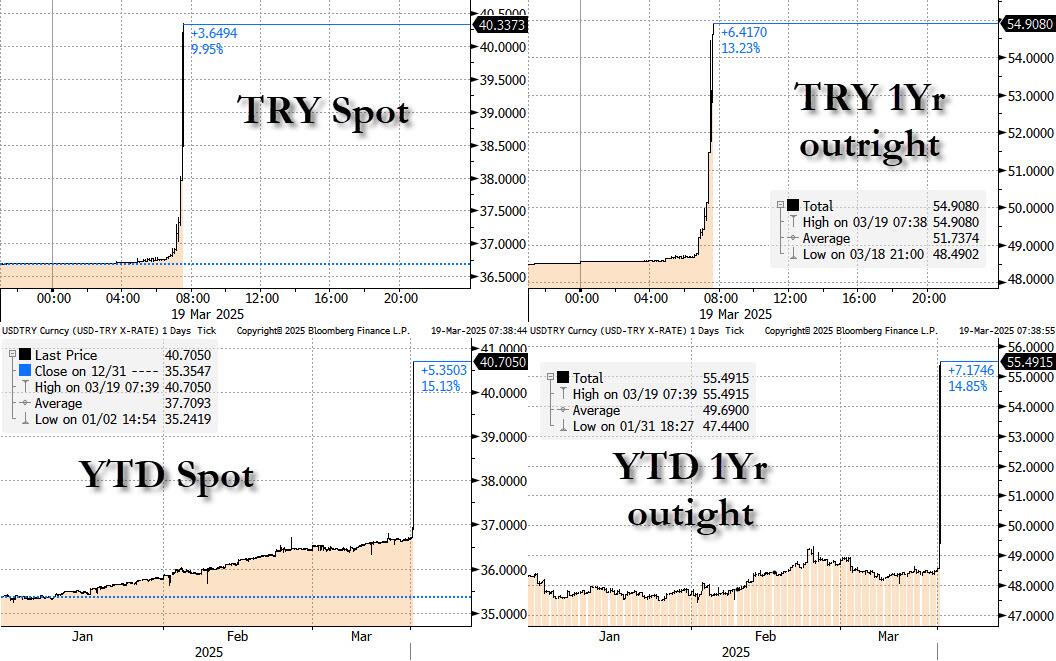

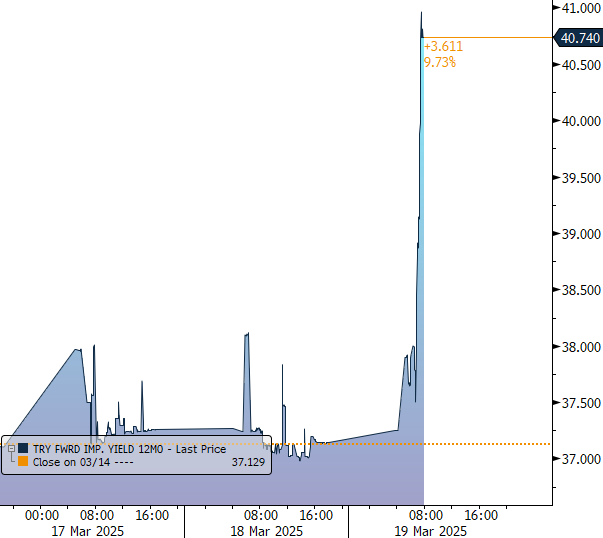

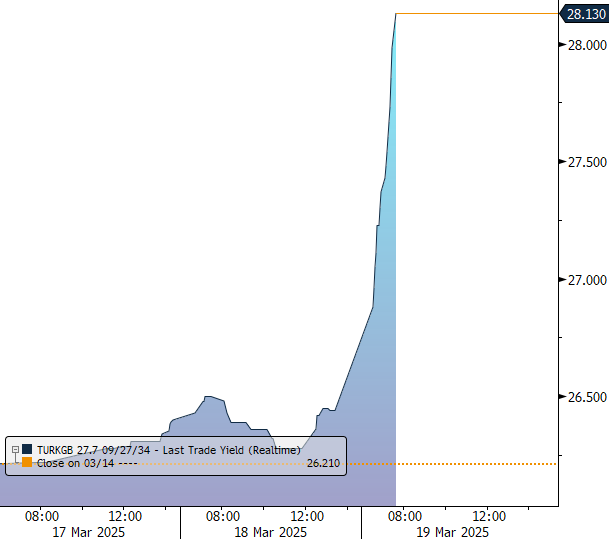

Meanwhile, geopolitics remains front and center and adds a fresh layer of worry, as the Gaza truce ended, Russia rejected Trump’s ceasefire proposal in Ukraine and Turkey ignited a selloff in its markets by detaining a key opposition figure. The lira plunged more than 10% to record lows and the main equity index dropped after the detention of Istanbul mayor Ekrem Imamoglu.

Europe’s Stoxx 600’s three-day winning streak stalled, with Turkey-exposed stocks such as BBVA and ING posting losses; technology and energy shares were the best performing sectors, while mining and personal care stocks are the biggest laggards. The Stoxx 600 is now up 0.1%, led by gains in consumer products, technology and energy names. Here are the biggest movers Wednesday:

- Softcat shares rally as much as 13% to the highest since June, after the UK IT reseller raised guidance for operating profit growth and reported first-half results that beat estimates

- Cargotec gains as much as 7.5%, the most in almost five months, as Danske Bank lifts its rating on the Helsinki-listed cargo-handling equipment maker to buy from hold

- Bridgepoint shares rise as much as 5.6% after being upgraded to buy by analysts at Citi, who argue the risk-reward profile looks attractive following the stock’s recent underperformance

- M&G shares rise as much as 4.5%, hitting their highest level in almost a year, after the investment manager’s results for 2024 came in better than expected, according to Jefferies

- Saab drops as much as 7.2%, slipping from yesterday’s record closing high, as Danske Bank double-downgrades to sell and says valuation is “perhaps not attractive enough” to reflect potential headwinds

- Compass Group shares fall as much as 6.1%, hitting the lowest level since Oct. 15, after BNP Paribas Exane downgraded the stock to underperform from outperform

- Raysearch falls as much as 13%, the most since Aug. 29 2022, after the Swedish medical technology firm’s CEO Johan Lof sold some of his Class B shares in the company at a 10.1% discount vs. Tuesday’s close

- Pan African Resources shares fall as much as 6.8% in London, after Tembo Capital Mining Fund sold its entire stake at a discount to the last close

- Ferrexpo falls as much as 15% in London, the most since Feb. 20, after the miner reported revenue for the 2024 full year that missed the average analyst estimate

- Steyr Motors drop 61% in Frankfurt, paring 1170% rally over previous 12 days, after majority owner Mutares said it plans to sell further shares in the company

Earlier in the session, Asian stocks were mixed as traders await more clues on the economic outlook from the Federal Reserve’s policy decision later Wednesday. Indonesian stocks bounced back from Tuesday’s steep selloff. The MSCI Asia Pacific Index erased earlier gains of as much as 0.4% to trade little changed. While the US central bank is expected to hold interest rates steady, officials may offer more clarity amid President Donald Trump’s tariff threats and fears of a US recession. Chinese benchmarks were mixed as uncertainties lingered over Beijing’s policy-direction in boosting consumer spending and stoking local demand. In a note Monday, Bank of America strategists warned of a “meaningful correction” for China’s stock rally, given its similarities with the 2015 boom-and-bust cycle. Meanwhile, Japanese shares gained after the central bank held rates steady as expected. South Korea’s stock benchmark also climbed, ahead of an imminent verdict in the impeachment of Yoon Suk-Yeol.

In FX, the Bloomberg Dollar Spot Index climbs 0.3%. The Swedish krona is the weakest of the G-10 currencies, falling 0.7% against the greenback. The euro retreated from five-month highs, after gains sparked by Germany’s plan for hundreds of billions of euros in debt financing. Lawmakers green-lit the package in Berlin on Tuesday. The yen is down 0.3% after the Bank of Japan kept its benchmark rate unchanged and cited worries over the potential impact from US tariff policies. The Turkish lira fell by more than 12% to a fresh record low after the detention of President Recep Tayyip Erdogan’s most prominent rival stoked concern that recent investor-friendly economic policies may be rolled back. It has since trimmed some losses.

In rates, treasuries dip, pushing the 10 Year Treasury yield 1bp higher to 4.29%, marginally cheaper on the day, trailing German counterparts by 3bp; US curve spreads are likewise little changed in muted trading conditions ahead of Fed decision. Bunds pared an earlier rally, although German 10-year borrowing costs are still down 3 bps at 2.78%. Traders have been piling into hawkish hedges that anticipate the central bank remaining on hold through June; Fed-dated OIS contracts currently price in around 58bp of easing by year-end with the first move fully priced by the July policy meeting

In commodities, oil prices are unchanged, reversing an earlier loss after Russian President Vladimir Putin declined Donald Trump’s bid for a 30-day ceasefire in Ukraine, agreeing instead to limit attacks on the country’s energy infrastructure. WTI is flat at $66.75 a barrel. Spot gold is steady around $3,036/oz having hit another record high earlier today. Bitcoin rises 2% to around $83,700.

On today’s calendar, besides the all important FOMC decision, it’s quiet: we get MBA mortgage applications (which dropped 6.2% after jumping 11.2% last week) and the January TIC flows at 4pm.

Market snapshot

- S&P 500 futures up 0.3% to 5,627.50

- STOXX Europe 600 down 0.1% to 553.60

- MXAP little changed at 189.77

- MXAPJ down 0.2% to 594.00

- Nikkei down 0.2% to 37,751.88

- Topix up 0.4% to 2,795.96

- Hang Seng Index up 0.1% to 24,771.14

- Shanghai Composite little changed at 3,426.43

- Sensex up 0.3% to 75,491.07

- Australia S&P/ASX 200 down 0.4% to 7,828.25

- Kospi up 0.6% to 2,628.62

- German 10Y yield little changed at 2.78%

- Euro down 0.3% to $1.0908

- Brent Futures down 0.7% to $70.10/bbl

- Gold spot down 0.1% to $3,032.05

- US Dollar Index up 0.28% to 103.53

Top Overnight News

- The Fed’s quarterly dot plot due today may look hawkish, with Bloomberg Intelligence calling it a coin flip whether the median will show one or two 25-bp cuts this year. Traders are pricing in at least three. The central bank is expected to keep the key rate unchanged. BBG

- WSJ’s Timiraos wrote central banks can lower rates because of good or bad news and the window for ‘good’ cuts is closing due to new inflation risks, while he noted that most officials are expected to pencil in one or two rate cuts this year but projections are likely to obscure how the Fed’s wait-and-see holding pattern has undergone an important reset because of the threat of an expansive trade war that sends up prices.

- Tesla (TSLA +3.6% in premarket) receives the first approvals in California needed to run a fleet of robotaxis in the state. RTRS

- A federal judge ruled that Elon Musk probably exercised unconstitutional power in orchestrating DOGE’s efforts to shutter USAID. The White House said it will appeal. BBG

- US crude inventories rose by 4.59 million barrels last week, API data is said to show. That would take total holdings to the highest since July if confirmed by the EIA. Trump will meet with oil industry execs later today. BBG

- Volodymyr Zelenskiy will have a phone call with Donald Trump today, he said. Earlier, US officials told European counterparts they’ll need to be involved in negotiations given its sanctions on Russia, people familiar said. BBG

- The lira sank after Istanbul’s mayor was detained at his home this morning. Ekrem Imamoglu is widely seen as Recep Tayyip Erdogan’s main rival and a top contender for the presidency. Turkish lenders were said to have sold about $8 billion to support the currency. BBG

- Chinese banks are slashing rates on consumer loans to record lows as policymakers ramp up stimulus to stabilize growth and counter US President Donald Trump’s tariffs. Lenders across the wealthier areas of Shanghai, the nation’s financial capital, and Hangzhou, a key tech hub, are engaged in a price war, offering annual interest rates as low as 2.58% on loans to fuel restaurant visits and shopping, according to online ads. That compares to rates as high as 10% about two years ago. BBG

- Euro-area inflation was revised down in February, strengthening calls for the ECB to continue cutting rates. CPI rose 2.3%, less than the 2.4% Eurostat first flagged. BBG

- Indonesia’s securities regulator eased share buyback rules after this week’s stock rout. The benchmark equity index closed higher for the first time in five sessions. The central bank held its key rate at 5.75%, as expected, and said it sees one cut this year. BBG

- The Bank of Japan kept interest rates steady on Wednesday and warned of heightening global economic uncertainty, suggesting the timing of further rate hikes will depend largely on the fallout from potentially higher U.S. tariffs. But Governor Kazuo Ueda also said rising food costs and stronger-than-expected wage growth could push up underlying inflation, highlighting the central bank’s attention to mounting domestic price pressures. RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as the region lacked firm conviction following the negative handover from Wall St and as participants braced for central bank announcements including the BoJ decision which lacked any major fireworks. ASX 200 was subdued for most of the session and finished lower in the absence of any fresh bullish catalysts. Nikkei 225 initially benefitted from recent currency weakness which helped the index shrug off disappointing machinery orders and weaker-than-expected trade data to briefly reclaim the 38,000 level. However, the index then gradually pared its gains following the lack of surprises from the BoJ’s unsurprising decision to maintain rates at 0.50%, Hang Seng and Shanghai Comp were choppy with participants cautious as they digested recent earnings releases and with tech stocks contained heading into Tencent’s results due later today.

BOJ

- Policy Announcement: maintained its short-term interest rate target at 0.5%, as expected with the decision made by unanimous vote. BoJ said Japan’s economy is recovering moderately, albeit with some weak signs, while consumption is increasing moderately as a trend and inflation expectations are also heightening moderately. BoJ stated they must be vigilant to the impact of financial and FX market moves on Japan’s economy but added that Japan’s economy is likely to continue growing above potential. Furthermore, it expects underlying inflation to converge towards a level consistent with the price target in the latter half of the three-year period projected under the Outlook Report but noted uncertainty surrounding Japan’s economy and prices remains high.

- Ueda: will adjust the degree of easing if its economic and price outlook is realised; not pessimistic about Q1 GDP growth compared to its recent forecast. Still the BoJ’s view that the neutral rate has a wide range, BoJ has still not narrowed-down what the neutral rate is. The BoJ will respond ‘nimbly’ if there are abnormal long-term yield moves; adds that we are not in such a situation now. This Shunto result is largely in line with its view from January, wage trends are ‘on track’, or slightly stronger. There was a view at today’s meeting that there was upward pressure on inflation. Will not raise interest rates when the economy is in bad shape.

Top Asian News

- Tencent Holdings (TCEHY) (CNY) Q4 adj. net of 55.3bln (exp. 53.3bln), revenue 172.5bln (exp. 168.7bln); to raise dividend and buyback

European bourses kicked off the session on the backfoot amid a bout of general risk pressure following the European cash open with a few factors potentially influencing though there was not one clear driver; Stoxx 600 -0.1%. Sectors are mostly negative with Basic Resources lagging on pressure in Rio Tinto (-0.9%) after it pushed back on calls for a unified listing in Australia. Stateside, futures are firmer across the board but only modestly so; ES +0.3%, NQ +0.3%. Early doors, the benchmarks were knocked as part of a broader risk move with numerous factors potentially exerting influence; namely, Putin-Trump digestion and potential breach of the energy ceasefire, Ueda’s hawkish language, Turkish turmoil and ongoing tariff uncertainty. More broadly, focus remains on the Fed. NVIDIA’s (+1%) GTC saw a flurry of partnership announcements, Apple’s (+0.2%) Siri AI may miss Spring launch target, Oracle (+0.4%) mulls a stake in TikTok US, JPMorgan (+0.2%) hikes its dividend, Morgan Stanley (-0.1%) to cut jobs, Citi (+0.4%) lowers bonuses.

Top European News

- UK Chancellor Reeves is planning a new multi-billion pound public spending squeeze in next week’s Spring Statement, following an announcement on Tuesday of GBP 5bln in welfare cuts, according to FT.

- Irish Central Bank warned of significant impact from higher tariffs and cannot rule out a recession, while it lowered its GDP growth forecast for 2025 to 4.0% from 4.2% and 2026 forecast to 4.0% from 4.5%.

- TRY and Turkish equities pressured after the detention of Imamoglue. Borsa Istanbul temporarily halted trading.

- Head of France’s BNIC Cognac lobby says French Foreign Minister plans to visit China at the end of March.

FX

- USD is firmer vs. peers as we count down to the FOMC. Focus for the meeting is on the dot plot, Powell/statement commentary on tariffs and the US economy in addition to anything on QT. DXY at the upper-end of a 103.25-103.71 band.

- EUR/USD lower early doors, hit by EUR/JPY action during the Ueda presser. Down to a 1.0874 base at worst. Specifics for the bloc a little light after the Bundestag vote and ahead of the Bundesrat on Friday.

- JPY choppy but ultimately softer in wake of the BoJ where rates were kept on hold, as expected. The subsequent presser sparked some JPY strength as Ueda turned slightly more hawkish throughout it and as the risk tone deteriorated. USD/JPY currently firmer but off best in a 149.15-150.15 band.

- Sterling on the backfoot given JPY action with general USD strength also factoring. Pressure which comes despite favourable EUR/GBP movement. For the UK, specifics are light as we count down to the BoE on Thursday. Cable finds itself at the lower-end of a 1.2958-1.3004 band and pulling back from Tuesday’s 1.3010 YTD peak.

- TRY hit by the arrest of the likely main opposition candidate to Erdogan, with USD/TRY hitting a record 41.0132 peak after this.

- Antipodeans are both extending on the downside seen yesterday with the latest leg lower coinciding with selling in European equity futures ahead of the cash open. From a fundamental perspective, little reaction was seen from the relatively stable Australian Leading Index and softer-than-expected New Zealand Current Account data.

Fixed Income

- Benchmarks bid early doors as the risk tone deteriorated with, as discussed elsewhere, no one factor behind this. Since, as sentiment recovers, benchmarks are off best with USTs just into the red, Gilts near-unchanged and Bunds around 30 ticks off best.

- JGBs came under pressure into and after the BoJ itself. Thereafter, Ueda’s press conference began with him sitting on the fence and as such JGBs got back to their 138.25 peak before pulling back sharply to a 138.07 base, where it remains, as Ueda turned slightly more hawkish.

- USTs hit a 110-27 peak on the deterioration in the risk tone, stalling just before the proceeding sessions’ 110-29 and 110-30 respective highs. Specifics a touch light this morning as we digest the readout from Putin-Trump and count down to the FOMC; USTs back toward 110-20+ lows most recently.

- Bunds are firmer but also off best as the general fixed income rally seen in the European morning takes a slight breather and with Bunds specifically also acknowledging dual tranche supply.

- Gilts find themselves back to trading between USTs and Bunds after leading the action for a change on Tuesday. Focus for today, aside from the above macro points, is on PMQs where details will be sought on the disability reform Labour announced and whether the cost savings from this go far enough to restore headroom.

Commodities

- Crude futures remain under pressure after Tuesday’s constructive geopolitical developments, with both WTI and Brent trading at weekly lows of USD 66.21/bbl and USD 69.90/bbl respectively.

- Trump-Putin talks were described as productive, with the leaders agreeing on a temporary halt to energy infrastructure strikes and immediate talks on a complete ceasefire. However, it does appear that this agreement may have already been breached by Russia, with attacks reported on power supplies in the Dnipropetrovsk region this morning. Most recently, IFX citing Russia’s Defence Ministry reports that Ukraine attacked Russian infrastructure overnight.

- Dutch TTF is firmer, supported by the lack of a full ceasefire in Ukraine, along with reports of Russian and Ukrainian breaches of this energy agreement, as mentioned in the crude section.

- Spot gold has given back some of the gains from Tuesday, with the yellow metal still comfortably clear of the USD 3k/oz mark, but shy of the USD 3045/oz ATH which printed after the Putin-Trump call.

- Base metals are, broadly speaking, little changed with the risk tone tentative as we count down to the FOMC and updates on the multiple other in-focus macro drivers.

- US Private Inventory Data (bbls): Crude +4.6mln (exp. +0.9mln), Distillate -2.1mln (exp. -0.3mln), Gasoline -1.7mln (exp. -2.4mln), Cushing -1.1mln.

Geopolitics: Middle East

- Israeli army attacked Khan Yunis and conducted heavy shelling in the southern Gaza Strip, according to Al Jazeera.

- Hamas leader said continuation of the Israeli bombardment of Gaza will lead to the death of many Israeli prisoners and the movement is communicating with mediators to force Israel to respect its commitments to the ceasefire.

- US bombed targets in areas east of Hodeidah in Yemen and there were at least 10 US strikes that targeted areas in Yemen, according to Houthi media.

Geopolitics: Ukraine

- Russia’s Medvedev said the Putin-Trump call showed there is only Russia and the US in the ‘dining room’ eating a ‘Kyiv-style cutlet’ as a main course.

- US Special Envoy Witkoff said talks with Russia on the Ukraine war will take place on Sunday in Jeddah.

- Ukrainian President Zelensky said Russia launched over 40 drones targeting civilian infrastructure and it is precisely such night attacks by Russia that destroy Ukraine’s energy and civilian infrastructure. Zelensky added the fact that Tuesday night attacks were no exception shows the need to continue pressure on Russia for the sake of peace, as well as noted that Russian President Putin de facto rejected the proposal for a complete ceasefire and it would be right for the world to reject any attempts by Putin to drag out the war in response.

- UK PM Starmer spoke with Ukrainian President Zelensky on Tuesday evening and discussed progress US President Trump had made towards a ceasefire in talks with Russia, according to Downing Street.

- Regional governor in Russia’s Belgorod region said the situation remains difficult, a day after Russia said its forces had thwarted Ukrainian attempts to push across the border in Belgorod. It was separately reported that a drone attack sparked a fire at an oil depot in Russia’s Krasnodar region, according to regional authorities.

- UK Foreign Secretary said the EU and UK are to accelerate shipments of arms to Ukraine ahead of a potential full ceasefire, according to Bloomberg.

- Russian Defence Ministry says Ukraine attacked Russia’s energy infrastructure overnight, according to IFAX; CPC Kropotkinskaya oil pumping station stopped operating after damage, according to Tass.

- Ukraine State Railways in the Dnipropetrovsk region says Russian forces have attacked its power system on Wednesday morning.

- Finland President Stubb says if Russia refuses to agree, will need to increase its efforts to strengthen Ukraine and ratchet up pressure on Russia to convince it to come to the negotiating table.

- Ukrainian President Zelensky says he hopes a ceasefire will eventually be implemented; says Russian President Putin’s words are at “odds with reality”, in relation to the halt on energy strikes. Will speak to US President Trump on Wednesday.

Geopolitics: Other

- US Secretary of State Rubio warned unless Venezuela’s government accepts a flow of deportation flights, the US will impose new and escalating sanctions, while Venezuela’s government said sanctions are an economic war and responsible for hardships.

US Event Calendar

- 07:00: March MBA Mortgage Applications, prior 11.2%

- 14:00: March FOMC Decision

- 16:00: Jan. Total Net TIC Flows

DB’s Jim Reid concludes the overnight wrap

Welcome to FOMC decision day which we’ll preview later. Ahead of that, the air continues to deflate from the tech balloon (or bubble depending on your view) with the interesting question being whether this would have happened without the tumultuous trade headlines of the last month. The market is understandably fixated with how negative the trade headlines have been for US equities but the reality is that in February when the S&P 500 was only down -1.42%, the Mag-7 were down -8.77%. So don’t underestimate the tech sell-off as being the primary reason for US equity weakness of late.

This sell-off continued yesterday with the Mag-7 down -2.47% to the lowest levels since September, dragging the S&P down -1.07%. Tesla (-5.34%) and Nvidia (-3.43%) again lagged, while Meta (-3.73%) became the last of the Mag-7 to fall into the negative territory YTD. The rest of the Mag-7 are down by between -9% and -44% YTD. Overall the Mag-7 is down -16.19% so far this year, with the S&P 500 -4.54%. Interestingly the equal weight S&P 500 (-1.00% YTD) is only slightly lower, so outside of the Mag-7 it’s just a small sell-off so far. So when we think about the US market falls this year I would say sentiment changes towards the Mag-7 are a bigger impact domestically than the trade headlines even if both matter.

Over the other side of the pond your crystal ball would probably have been launched in the bin had you predicted that the DAX (+17.44% YTD) would be up as much at this stage of the year in absolute terms and especially versus the Mag-7 and the overall US market. However the news out of Germany continues to be positive with the CDU/SPD/Greens yesterday achieving the two-thirds majority needed for the debt brake reform containing the huge potential defence spending boost, and the €500bn infrastructure fund. So it was another day of European out-performance with the DAX (+0.98%) and the STOXX 600 (+0.61%) strong but with the IBEX (+1.58%) and FTSE-MIB (+1.31%) even stronger showing the halo impact of German spending. European bond yields largely held steady, with 10yr bund yields -0.8bps lower, but with the Euro (+0.21%) edging higher and to a fresh five-month high of 1.0945.

Incoming German Chancellor Friedrich Merz’s next test will be Friday’s vote in the Bundesrat – the second chamber comprising the 16 state governments – at 8:30AM GMT. As we said on Monday, the hurdle for the constitutional amendments to pass the Bundesrat is lower than it was in the Bundestag, especially as Bavaria has confirmed that it will support the package. So the execution risk is declining still further from already low levels.

Back to the US, and today brings the Federal Reserve’s second policy decision of 2025 and their latest Summary of Economic Projections. For the headline decision, we expect the Fed to hold rates steady and, given heightened uncertainty, provide limited guidance about the policy path ahead. And in a closer call, our US economists expect the Fed to announce a pause in QT beginning in April, coupled with forward guidance indicating that QT should resume once the debt ceiling is resolved. For details, see their Fed preview here. Although this is unlikely to be an exciting meeting, plenty has happened since the last meeting so the press conference could see a whole host of challenging questions for Powell. We suspect they will mostly be answered with a straight, non-commital bat, but will make for interesting viewing.

Ahead of that, the latest slew of US data yesterday leaned a little hawkish. Industrial production accelerated to +0.7%m/m (+0.2% expected) from +0.3%m/m in January, and manufacturing production rose +0.9%m/m (+0.3% expected). US housing starts increased +11% to a seasonally adjusted rate of 1.50mn units in February (+1.4% expected), though building permits were more in-line and tend to be more indicative of the underlying trends with starts often weather influenced. Meanwhile, monthly import prices came hotter at +0.4% m/m (vs. 0.0% expected), which included a sizeable jump in imported international airfares (+0.9%) that should add a little upside to next week’s core PCE print.

With all that data, market expectations of Fed rate cuts edged lower, with the amount of easing priced in by the December meeting (-1.2bps to 59bps) falling to its lowest level in three weeks. At the longer end of the rates curve, 10yr Treasury yields swung around but ultimately fell amid the risk off tone with 10yr yields down -1.5bps to 4.29%. The modest rally in Treasuries was also helped by a solid 20yr auction that saw $13bn of bonds issued at 4.63%, -1.4bps below the pre-sale yield. This morning in Asia 10yr USTs have edged back up a basis point.

In geopolitical news, the anticipated Trump-Putin call delivered only one element of definitive progress, with Moscow agreeing “to mutually refrain from attacks on energy infrastructure facilities for 30 days”. While both US and Russian readouts struck a constructive tone, Putin declined the US proposal for an unconditional ceasefire that Ukraine had agreed to, with the Kremlin emphasising that a “key condition” for working towards resolution of the conflict was “the complete cessation of foreign military aid and the provision of intelligence information to Kyiv”. Later in the day, Ukraine’s President Zelenskiy said that the Trump-Putin call showed Russia wasn’t ready for a truce.

The signal of a pause in strikes against energy targets did help Brent crude close -0.72% lower on the day at $70.56/bbl. It had earlier been +1.5% higher intra-day after Israel said it would continue to strike Hamas targets across Gaza but had already reversed this gain by the time headlines from the Trump-Putin call came through. Lastly, Gold continued to set new record highs, rising +1.14% to $3,035/oz amidst Middle East tensions escalating once more.

Asian equity markets are fairly quiet this morning with the KOSPI (+0.70%) leading with the Nikkei (+0.06%) fairly flat after the BoJ left policy unchanged at their meeting. The press conference will start just around the time this hits your inboxes. Chinese markets are all broadly flat but S&P 500 (+0.19%) and NASDAQ 100 (+0.29%) futures are edging back up.

In the statement accompanying the BoJ decision, they cited concerns about the impact of US trade policies on Japan’s economic recovery, noting continued uncertainty around economic activity and prices. The Yen and JGBs are relatively unmoved so far.

In terms of data, Japanese exports climbed +11.4% y/y in February (v/s +12.6% expected) up for a fifth straight month driven by strong demand from both the US and China. It followed a revised increase of +7.3% in January. Imports fell -0.7% y/y in February, marking its first drop in three months and compared with the Bloomberg estimate of a +0.8% gain. As such, Japan’s trade balance switched back into the black, with a surplus of ¥584.5 billion (v/s ¥688.3 billion expected).

To the day ahead, aside from the Fed decision, the EU commission will be presenting its White Paper on defense today, with EU leaders expected to discuss their ReArm EU plan on Thursday and Friday. We’ll also get data on Eurozone Q4 labour costs. For earnings releases, expect Tencent, Vonovia, Ping An Insurance and General Mills.