By Peter Tchir of Academy Securities

From Grok:

“For Soviet youth especially, blue jeans represented more than just fashion; they embodied individuality, rebellion, and a connection to the freedoms of the West, standing in stark contrast to the collectivist and restrictive Soviet system. Owning or wearing them became a subtle act of defiance, reflecting a broader yearning for personal expression and a lifestyle beyond the constraints of Soviet rule.”

We will circle back to why I think this is very important but let’s set the stage:

Two weeks ago we published Where the Economy is Headed.

- One point was that much of the current data, particularly on the job front, seemed “optimistic” and would likely decline and/or be revised down.

- We highlighted several areas of the economy that were causing concern, and those concerns have only increased in the past two weeks.

Last weekend we published You Ain’t Seen Nothing Yet.

- We presented our arguments for why there is no Trump Put, at least anywhere near today’s levels.

- We first started to fixate on the risk that all the attention on trade deficits would impact capital flows, which have materially helped the U.S. and were a part of the American Exceptionalism trade.

- We highlighted that a large percentage of revenue for companies in the S&P 500 comes from other countries! (This will tie into today’s title).

- We laid out two scenarios that could turn markets around, and we haven’t seen either occur yet.

On Friday, we published An American Brand, which to some extent was a prelude to today’s report.

- Is the American Brand being affected in such a way that it could hurt sales of American brands?

As I am increasingly nervous about the steps being taken and their impact on our economy and brands, and want to take the time to re-iterate why late last year and early this year we were optimistic.

We specifically use Grok as a source in this piece, under the assumption that of all the AI out there, Grok is most aligned with the administration.

The Goal

The working assumption, one that has solidified over time, is that:

- The president wants to return manufacturing to the U.S. and leave a legacy of rebuilding the middle class!

Fully in support of rebuilding the middle class. How can you not be? A middle class that feels safe and secure in their jobs, a middle class that can afford the American Dream, etc. would be awesome. It is not like the middle class is non-existent, but there is room for improvement.

Completely support the need to manufacture more, especially things we need to ensure safety and security. We’ve been pounding the table from an investment standpoint that anything that can be construed as important to National Security should equate to National Production. “Drill Baby Drill” is merely the tip of the iceberg. We’ve argued for “Refine Baby Refine,” where it is not just the extraction of commodities, but the extraction AND processing that is crucial to our success from a National Security standpoint. But it goes well beyond raw materials and their processed or refined versions. It extends to other areas, most noticeably the semiconductor industry, AI, medicine, and space (to name a few).

One caveat of this policy is that the Trump Put is not going to be executed any time soon.

- If we are going to see a transfer of wealth to the middle class (and growth in that class) it is likely to come somewhat from overseas, but possibly, at least in the short term, at the expense of profit margins. The administration believes that to achieve their goal, they must be comfortable with rattling markets (equities more so than bonds). I cannot disagree with this, but it does make me bearish on risk assets.

A separate goal, not quite related to the economy, but one that I think needs to be stated is that:

- This administration abhors the loss of life.

Members of our Geopolitical Intelligence Group consistently say that when they have worked directly with President Trump, he truly does not like risking lives in conflict. Not just our own, but also those of civilians and victims in conflict zones.

Since the tone of this report is negative on many of the steps taken (particularly on the economic front), I wanted to highlight this, as it is yet another laudable goal and characteristic that is good. I am not completely sure how it is affecting our negotiations in conflict zones, but one can take some degree of comfort that the president has this value.

Since I’m on board with the goals, why am I so bearish?

- If the current policies work in the long run there is still plenty of risk in the short run, especially if the state of the economy is weaker and more susceptible to a recession than many in D.C. (including the Fed) believe.

- Increasingly, when I examine the range of possible outcomes of the policies being implemented (and discussed openly about being implemented), the “good” or “great outcomes” have a reduced probability of occurring and the tail risk scenarios seem to be getting more plausible by the day.

Basically, I think the policies were due to disrupt the economy and markets even if they work out, and I have less conviction that the policies, as implemented, will achieve the stated goals.

Steel

I had a pleasant chat with Grok about the steel industry. I will paraphrase and use some rough estimates of the numbers as it would take too much space to cut and paste all the conversations, and the numbers weren’t always consistent anyways.

The good news:

- The maximum production would be around 115 million metric tons (I’m a bit surprised Grok would use metric measurements).

- Based on current usage, that would leave around 35 million tons of excess capacity.

- The U.S. imports 20-30 million metric tons of steel annually.

At a first glance, we should be able to tariff the heck out of steel and replace it with existing facilities!

But it may not be so simple:

- Utilization rates of over 90% have been cited during boom times. Typically, 70% to 80% utilization is the norm for several reasons.

- Maintenance, repairs, and inefficiencies keep utilization typically below.

- Scaling is not as easy for some types of operations as others.

- The availability of scrap steel or iron ore often restricts production.

- There are various grades of steel and certain specialty steels that are imported that are not likely to be replaceable with current domestic production capabilities.

Even if we don’t increase steel demand in this country (which presumably we would as the U.S. manufactures more) we will still need imports until we build more mills.

Grok thinks it takes 3 to 7 years from concept to full operation to build a steel mill in the U.S. (depending on the type of mill, etc.).

- Planning and permits (1-2 years). In theory permits could be fast-tracked, but the issue we hear from a variety of industries is that they need a degree of certainty that these permits and any regulatory waivers will last for the shelf life of their projects (typically measured in decades, not two-year midterm and four-year presidential election cycles).

- Design and Engineering (6 months to 1 year). Maybe AI speeds it up?

- Construction (2-3 years). Mini-mills, which often just melt scrap, can go up sometimes in the 2 year range, but 3 years might be optimistic for a large facility (and it sounds like that would require ordering things well in advance, performing grading of the land, etc., which would require a fairly high degree of certainty of the project’s success).

- Commissioning and Testing (6 months to 1 year). Not something that I had even thought about.

So, even if the tariffs are massively successful on steel alone, we would need to import reasonably high levels. I have not done the full analysis of how much could be reduced, but it seems reasonable to assume only a portion, until more mills come online, potentially some that specialize in grades the U.S. currently doesn’t produce.

If the policies are successful, we will need even more steel (presumably demand for steel would increase). That would certainly require more plants (which require steel to be built). Leaving the U.S. potentially importing as much or more steel than before (for a number of years) but at a higher price.

That is assuming that the plans to grow production in the U.S. work and other countries don’t respond in ways that make it more difficult to achieve the goals here.

Maybe I’m thinking too linearly here (or circularly) and don’t understand 3D chess, but there seem to be a lot of timing issues that make the policy goals difficult to achieve, without a “measured” transition period. Assuming every country will fall in line with the “trap” being set for them, this also seems a bit difficult to swallow.

And this is just one industry, while we are potentially going to be doing something similar across so many more industries with so many more countries if the reciprocal tariffs are implemented (and they do something about the VAT).

I am finding it incredibly difficult to see how the tariffs are certain to achieve the desired goals as they are currently being presented and implemented.

What vs. How

Basically my “disagreement” has less to do with the what (the goals) and more to do with the how.

This applies to the handling of tariffs, DOGE, and conflict zones. I know there is going to be a range of opinions on this, so I’m not even going to get into any detail.

What I can say is that:

- In Trump 1.0 the how didn’t seem to affect the what. In many cases the goals, at least on a transactional level, seemed to be achieved regardless of the process of getting there.

- While it might be too early to tell, the how this time might get in the way of the what. We will discuss that a bit more in the final section, but it is important. It seemed like during Trump 1.0, there were not as many agenda items (so global and so early) in his administration, so there was less time for the “how” of one deal to affect the “what” of the next deal. Also, it felt like world leaders had no idea how to respond (or play) Trump 1.0, whereas they seem to be deploying different strategies (and not everyone is rushing to the table begging for a deal).

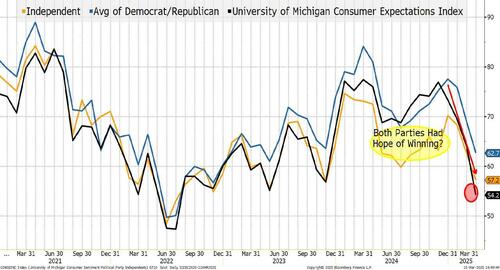

Maybe I’m reading too much into this next chart, but I find it interesting and wonder if it isn’t just starting to express concern about polices, but also concerns about the “how.”

We have highlighted in the CONsumer CONfidence report the difference by party. (I really don’t love the report, but sometimes it has the data you need).

It is almost comical (if it wasn’t kind of scary) that Republicans “boosted” their 1-year inflation expectation from 0.1 deflation to 0.1 inflation, while Democrats chimed in at 4.9% (up from 4.3% last month and 3.3% the prior month). That gap is unusually large.

But today we use the example of the sentiment data. We compare the sentiment data to the average of the Republican/Democrat data and to the Independents.

In theory you would expect to see them all roughly aligned. The Independents should, in theory, be in around the Dem/Rep average which should also be the survey result.

You get that a lot. We had a deviation where the average of the two parties was much higher than the Independents, presumably because both sides thought they were going to win and were optimistic.

What I found most interesting is how after seeing rising sentiment post-election, we have started to see a decline. Initially led by Independents and now, not just followed by, but led by, the overall number.

That data is not encouraging, especially as sentiment can affect behavior.

Something not good is happening out there and the Independents are leading the way lower, which I think means something as they should be less subjective about the party in charge and more focused on actual policies.

Again, I have lots of issues with these surveys, but I feel it is capturing something this time around that we should all watch for, and unfortunately fits many of the themes we’ve been writing about – especially the state of the economy and about the impact of policies so far.

The American Brand

I’ve seen very little discussion about the risk to sales of American brands globally. Even we didn’t focus on that too much last week. We focused more on the potential costs incurred by U.S. companies with global businesses, than the possible damage to brands.

While jeans and the Soviet Union might be too specific of a case, I think there is a lot that is relevant to today’s global marketplace.

American brands still have a certain je ne sais quoi about them (I probably shouldn’t use a foreign language in this section, but if Grok can use metric and spell tonne incorrectly, why not?).

There is an “aspirational” quality associated with American brands. The power, the lifestyle, so many things feed into that global demand for U.S. goods. Yes, quality, and other things are incredibly important, and while the “USSR and Jeans” is a likely overstatement on today’s global demand for U.S. brands, I would be shocked if it had zero impact!

There is, I believe, a risk that sales of U.S. brands could be adversely affected. I cannot believe I am about to quote Warren Buffett two weeks in a row (I must be getting old), but here it goes (from Grok):

“It takes 20 years to build a reputation and five minutes to destroy it. If you think about that, you’ll do things differently.”

I’m not saying that we have hit that point, but I certainly think it deserves some thinking about (especially as one of our concerns has been about “re-trading” and in recent social media posts about Panama, the president harps on the sale of the canal for $1. It may have been a bad deal, I have no idea of the context at the time or what (if anything) else was received outside of the $1, but our industry doesn’t like people who re-trade and I find it impossible to believe that nations won’t find it difficult to trust over time.

It is also a good time to point out that I had complaints during the prior administration about how our policies (particularly with Ukraine and Isreal) were affecting how the world perceived the U.S. So not all of the potential reputational damage is new.

I could be wrong about reputational damage risk and its potential to impact how countries deal with us and how it affects our brands globally! But one of the GIG members I was traveling with this past week mentioned this particular quotation at several meetings. You can find in on Yahoo! I will admit that the Singapore Defense Minister is not huge on the world stage, and the event he was speaking at isn’t a global forum for the leaders of the biggest countries, but it is probably worth a minute of your time to read. It is even possible that other important people in their respective countries have a remotely similar view (I wouldn’t be sharing it if I didn’t think it is plausible). He used the phrase “willy-nilly” leading up to this point:

“The image has changed from liberator to great disruptor to landlord seeking rent.”

Two countries, Canada and Portugal, have announced that they are reconsidering purchases of an American made fighter jet. Nothing has changed about the jet or its competitive advantages versus their competition, but something has changed. It could merely be a “reactionary” step with no real teeth that will fail, and they will be embarrassed that they even went down this path. It could be that even after reconsidering they go forward with the purchase. It could also be that they decide to move away from U.S. equipment. Not ideal for U.S. manufacturing, but possible.

There is a risk that how the country implements policies, let alone the policies themselves, will have unintended consequences.

Xi and Taiwan

According to Grok, Taiwan manufactures about 90% of the chips used in AI – the most important growth story across the globe.

Many of our GIG members argued that the isolation Putin faced after his invasion of Ukraine (that was how it used to be described) would give Xi pause. While there are still a lot of questions about China’s ability to take over Taiwan militarily (almost impossible if the U.S. intervenes), he must be watching the potential reintegration of Russia into the global trading community with some “curiosity.” China interfering with Taiwan remains a low risk in most of our assessments, but it is worth taking a fresh look at this in light of what is going on across the globe with U.S. policy – both economically and geopolitically – though the two are difficult to separate.

Bottom Line

Is the U.S. underestimating the intangible benefits from its status (like demand for American brands and capital inflows)?

Maybe the Fed saves the day this week with a strong pivot to rate cuts. I don’t see it. Will go into more detail ahead of the Fed, partly because we’ve already taken too much of your time, and because quite frankly I don’t see the Fed acting in a “big enough” way to offset the risks that I see:

- An economy that was already weaker than the data showed.

- An economy that is getting hit not just by government cost cutting (and how it is being done), but also by companies being “frozen” as they need to have a clear understanding of what policies are here to stay, before making hiring decisions.

- Capital flows, and now the risk to sales globally, compounding the problem.

I am clearly in the “recession” camp. Things could change, but the convergence of so many policies seems to risk a recession before any probability of seeing the benefits (that the administration expects to see) shows up in the economy and markets.

While I’m not there yet, and a lot could change (like backing off from the April 2nd tariffs, an aggressive Fed, or new fiscal spending surprising us all), I wouldn’t be surprised to see some analysts bring up the D word.

With Friday’s bounce and crypto trading well so far this weekend (yeah, we have to keep an eye on it) and the Fed coming up, maybe we’ve bottomed for now. All of the 200-DMA purchases will turn out to be good, and some things like reciprocal tariffs haven’t been implemented yet, providing more breathing room. Buying the dip has been surprisingly strong. TQQQ, mentioned on Friday, now has the most shares outstanding since late September. If inflows keep coming, maybe this rally continues.

However, I remain cautious for all the reasons listed above and cited over the past two weeks. Underweight sectors or factors make sense to own, and I still like the National Security = National Production trades. I’m the most nervous about corporations that rely on global sales. Any near-term benefits from policy are likely to accrue to smaller companies rather than those with a global presence which not only may face issues on the selling side, but are also likely to have a lot to deal with regarding their manufacturing and supply chain.

FX – dollar weakness seems to be the play until the messaging out of D.C. changes. DXY, a basket of currencies at 104, is still above pre-election levels of around 100 and I see no reason why in the coming weeks it won’t succumb to a return to those levels, like so many other asset classes have.

The front end of the yield curve, not pricing in its first cut until June and only getting to 3 cuts by next April, is not aggressive enough. I’d be shocked, given what I see, if the Fed doesn’t cut as early as May (though that may not get telegraphed at this week’s meeting) and if they don’t have to cut 4 times by the end of the year – which fits my outlook for the economy. 10s I suspect won’t respond as positively as commitment to true deficit reduction (or the ability to achieve it) may have been given too much of the benefit of the doubt by the market, and I suspect capital outflows, 10-year German yields at almost 3%, and 40-year JGB yields at almost 3% will compete for funds in their own regions, offsetting some money that used to find its way into Treasuries.

Credit is the lynchpin of so much. We finally saw more people grow concerned and some moments of buyer strikes. We ended the week strong, but given my economic and fund flow outlook, expect to see that widen. If that does happen you can be sure that the “cottage industry” of bond blow up pundits will be out in force, trying to drive already jittery equity markets lower.

While I’m not oblivious to the risk that the rally is real and policies change, I’m glad I got this report off my chest. I would love to see policies more along the lines of what I expected when I was all bulled up. Policies that seem likely to work in the long run and have less short-term risk. Maybe we get that. Maybe I’m horribly wrong in my assessment of whether the current and planned policies will achieve their goals with minimal damage. I’d be happy for that to be the case, but for now, I feel I need to keep sounding the alarm on risk assets.

{kind=link}