- Investors are stampeding into initial public offerings at the fastest clip since the financial crisis (WSJ)

- Kerry hails disgruntled Saudi Arabia as important U.S. ally (Reuters)

- SAC Capital prepares for a second life (FT)

- BlackBerry’s Fate Goes Down to the Wire (WSJ)

- Dutch Gamble on U.S. Housing Debt After Patience Wins (BBG)

- Tensions with allies rise, but U.S. sees improved China ties (Reuters)

- China berates foreign media for Tiananmen attack doubts (Reuters)

- China manufacturers squeezed as costs rise (FT)

- European Borders Tested as Money Is Moved to Shield Wealth (NYT)

- Zurich Probe Finds No ‘Undue Pressure’ Put on Late CFO (BBG)

- Johnnie Walker One Shot at a Time Boosts Diageo in Africa (BBG)

- Obamacare Birth Control Mandate Ruled Unconstitutional (BBG)

- NQ Mobile Sales Search Leads to Suburban Beijing Office (BBG)

Overnight Media Digest

WSJ

* BlackBerry’s future may become clearer as soon as Monday when a tentative agreement from Fairfax Financial to take the company private for $4.7 billion is scheduled to be firmed up. Other bids are possible.

* Investors are stampeding into initial public offerings at the fastest clip since the financial crisis, fueling a frenzy in the shares of newly listed companies that echoes the technology-stock craze of the late 1990s.

* SAC and federal prosecutors in Manhattan are expected to announce a record insider-trading settlement Monday. Under the deal, the firm run by Steven Cohen is expected to agree to pay about $1.2 billion in criminal penalties, plead guilty to an indictment obtained in July by prosecutors alleging the firm encouraged rampant insider trading, and stop managing outside money.

* The Obama administration ruled that drugmakers can help pay prescription-drug costs for patients on health-care exchanges. Pharmacy-benefit managers object, preferring generic drugs.

* Years of low interest rates are taking their toll on universal life insurance policies, affecting the policy holders as well as the charities and institutions that would benefit from the policies.

* Federal approval to use electronic devices throughout flights has revived a related debate over whether airline passengers should also be able to make voice calls while airborne.

* Suntech Power agreed to sell its core assets in China for $492 million to a smaller rival, attempting to pay back creditors after defaulting on billions of dollars in debt.

* Cooper Tire’s lawsuit against Apollo Tyre of India, to force it to close on a previously agreed-upon acquisition, heads to court on Tuesday.

* The Federal Trade Commission cleared the way for Office Depot Inc and OfficeMax Inc to complete their $1.2 billion merger after concluding the corporate marriage wouldn’t harm competition.

* U.S car shoppers brushed off Washington’s fiscal battles last month and, emboldened by steady gas prices, bought more trucks and sport-utility vehicles and boosted the Detroit Three auto makers over their rivals.

FT

Steve Cohen’s $15-billion hedge fund SAC Capital Advisors, currently fighting criminal insider trading charges, will plead guilty to securities fraud and pay over $1 billion in fines, a person familiar with the matter said. The announcement on the plea and fine is expected as soon as Monday, the source said.

Twitter , which is expected to list with a valuation of as much as $13.9 billion this week, is set to make a “substantial investment” after the initial public offering, to expand research and development including buying other companies for their products, technologies and staff.

The number of new jobs in London’s financial district dropped slightly in October despite renewed optimism in the financial services sector, according to specialist recruiter Astbury Marsden.

Europe’s largest banks have increased their risk exposure to sovereign debt by more than a quarter in 2011 and 2012, while reducing corporate lending as they prepare for stricter global capital rules, according to findings by Fitch Ratings.

Private equity group Blackstone will offer investors a novel security this week, backed by cash flow from more than 3,000 foreclosed homes across the United States that it bought and converted into rental properties.

NYT

* Federal subsidies will pay the entire monthly cost of some plans being offered in the online marketplaces, a surprising figure that has not gotten much attention, in part because the zero-premium plans come with serious trade-offs.

* A plea deal for SAC Capital Advisors would resolve a criminal case involving insider trading charges, but the firm’s owner, Steven Cohen, would still face a civil lawsuit.

* Hard as it may be to believe, the price per square foot for luxury apartments in New York City is considerably less than it is for luxury elsewhere in the world.

* Though three-quarters of Twitter users are outside the United States, only a modest portion of its ad revenue is generated there. But it’s growing fast.

* Backed by the billionaire Koch brothers, Americans for Prosperity has campaigned against taxes and spending in Coralville, Iowa, but some voters are skeptical of its motives.

* With the pace of delayed television viewing increasing, networks want advertisers to pay for seven days of commercial viewing to cover computer screens and tablets as well as TV sets.

* Technology giant Samsung, known for playing its cards close to the vest, is holding only its second meeting of management with analysts.

* Zola Books is trying to persuade book buyers to flock to its website, a hybrid that is designed to be a bookseller, curator and social-networking site all in one.

* A sweeping distribution deal between television giants, the Walt Disney Co and Dish Network, expired more than a month ago, and there is still no new deal in sight.

Canada

THE GLOBE AND MAIL

* Montrealers turned to a veteran federal politician with a populist touch to lead Montreal into a critical era of rebuilding, sending Denis Coderre to city hall as mayor but ensuring he faces strong opposition on city council.

* Quebec

voters are hoping to turn the page on an era of scandal-ridden leadership as they cast their ballots in municipal elections across the province on Sunday.

Reports in the business section:

* It’s decision week for BlackBerry Ltd, the battered former champion of Canada’s technology industry. Monday is the day by which Fairfax Financial Holdings Ltd is expected to finalize a deal to buy the smartphone maker for $4.7 billion.

* Canada’s jobless rate has ebbed to a five-year low, reflecting solid job creation in some sectors and – in the case of September – fewer young people looking for work.

NATIONAL POST

* Toronto Mayor Rob Ford said on Sunday that he has to ‘slow down on his drinking.’ He promised to ‘make changes in my life,’ but did not admit to drug use.

* Canadian Prime Minister Stephen Harper has been given his marching orders from a Conservative party not frightened to embrace social conservatism and a hard-core shift to the right.

FINANCIAL POST

* Despite all the challenges Canada’s oil patch has faced, it’s been a pretty good year for Canadian energy stocks – and some ‘are very cheap and very strong on earnings.’

China

CHINA SECURITIES JOURNAL

– In the first nine months of the year, 10 A-share listed Chinese companies invested a total of $1.2 billion in overseas mining projects, accounting for 36.8 percent of their aggregate investments, according to information gathered at a mining conference.

CHINA DAILY

– Police have detained 17 people in four Chinese provinces on suspicion of making and selling $3.28 million worth of counterfeit drugs and vaccines, the Ministry of Public Security said on Saturday.

– Western media, in particular those from the U.S., have employed double standards in their reporting of the Tiananmen crash on Oct. 28, said an editorial. There is no confrontation between the Chinese government and the Uighurs in the Xinjiang Uighur autonomous region, it said.

PEOPLE’S DAILY

– China’s development strategy should not be fixated only on GDP growth, said an editorial in the paper that acts as the government’s mouthpiece. Attention also needs to be paid to the by-products of growth, such as pollution and development efficiency, it said.

SHANGHAI DAILY

– Shanghai will see a 73 percent on-month increase in land supply in November, according to Soufun.com, operator of China’s largest real estate website. A site area of 818,000 square meters of land will be released for auction this month, it said.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

AK Steel (AKS) upgraded to Buy from Sell at Goldman

Abaxis (ABAX) upgraded to Neutral from Underperform at BofA/Merrill

Abercrombie & Fitch (ANF) upgraded to Buy from Neutral at SunTrust

Alcatel-Lucent (ALU) upgraded to Buy from Neutral at UBS

Alcatel-Lucent (ALU) upgraded to Neutral from Underperform at Exane BNP Paribas

BP (BP) upgraded to Equal Weight from Underweight at Morgan Stanley

BT Group (BT) upgraded to Overweight from Neutral at HSBC

Boston Beer (SAM) upgraded to Outperform from Perform at Williams Capital

Dril-Quip (DRQ) upgraded to Buy from Accumulate at Global Hunter

GrafTech (GTI) upgraded to Buy from Hold at Jefferies

Kohl’s (KSS) upgraded to Buy from Neutral at UBS

Occidental Petroleum (OXY) upgraded to Overweight from Equal Weight at Barclays

Omnicom (OMC) upgraded to Outperform from Market Perform at BMO Capital

Ruth’s Hospitality (RUTH) upgraded to Market Perform at Raymond James

STAG Industrial (STAG) upgraded to Overweight from Equal Weight at Evercore

Salesforce.com (CRM) upgraded to Overweight from Neutral at Atlantic Equities

Steel Dynamics (STLD) upgraded to Buy from Neutral at Goldman

Time Warner Cable (TWC) upgraded to Buy from Hold at Deutsche Bank

U.S. Steel (X) upgraded to Buy from Sell at Goldman

Downgrades

AXIS Capital (AXS) downgraded to Market Perform from Outperform at BMO Capital

Accuride (ACW) downgraded to Neutral from Buy at B. Riley

Aflac (AFL) downgraded to Neutral from Buy at Citigroup

AstraZeneca (AZN) downgraded to Neutral from Buy at UBS

Bridgepoint Education (BPI) downgraded to Sell from Hold at Deutsche Bank

Calpine (CPN) downgraded to Hold from Buy at Jefferies

Calumet Specialty Products (CLMT) downgraded to Sector Perform at RBC Capital

Computer Programs (CPSI) downgraded to Outperform from Strong Buy at Raymond James

Digital Realty (DLR) downgraded to Neutral from Outperform at RW Baird

Eni SpA (E) downgraded to Equal Weight from Overweight at Morgan Stanley

Gap (GPS) downgraded to Neutral from Buy at Goldman

Marathon Petroleum (MPC) downgraded to In-Line from Outperform at Imperial Capital

NetApp (NTAP) downgraded to Neutral from Overweight at Piper Jaffray

Piedmont Office Realty (PDM) downgraded to Underperform at Wells Fargo

Range Resources (RRC) downgraded to Underweight from Equal Weight at Barclays

Reliance Steel (RS) downgraded to Neutral from Buy at Goldman

Teva (TEVA) downgraded to Underweight from Neutral at JPMorgan

Initiations

Antero Resources (AR) initiated with an Overweight at Barclays

Cell Therapeutics (CTIC) initiated with a Buy at H.C. Wainwright

Evoke Pharma (EVOK) initiated with a Buy at Cantor

Gaming and Leisure Properties (GLPI) initiated with a Buy at Deutsche Bank

LDR Holding (LDRH) initiated with an Overweight at Piper Jaffray

MacroGenics (MGNX) initiated with a Neutral at BofA/Merrill

MacroGenics (MGNX) initiated with an Outperform at Leerink

QTS Realty Trust (QTS) initiated with a Buy at Goldman

QTS Realty Trust (QTS) initiated with a Buy at Jefferies

SFX Entertainment (SFXE) initiated with a Buy at UBS

Western Refining Logistics (WNRL) initiated with a Neutral at Goldman

Western Refining Logistics (WNRL) initiated with an Outperform at Credit Suisse

Western Refining Logistics (WNRL) initiated with an Outperform at Wells Fargo

HOT STOCKS

HSBC (HBC) said being investigated for foreign exchange trading

TRI Pointe Homes (TPH) to combine with WRECO (WY) in transaction valued at $2.7B

Caterpillar (CAT) disclosed probe into railroad unit from U.S. District Court for the Central District of California

Morgans Hotel (MHGC) confirmed $8.00 per share offer from Yucaipa Cos.

Honda (HMC) recalled 344,000 Odyssey vehicles for braking issue

Samsung (SSNLF) extended patent license agreement with Nokia (NOK) for five years

Hyatt Hotels (H) in deal for Hyatt-branded hotel in Iraq

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Spectra Energy (SE), Realogy (RLGY)

Companies that missed consensus earnings expectations include:

Synta Pharmaceuticals (SNTA), Zogenix (ZGNX)

NEWSPAPERS/WEBSITES

- Investors are stampeding into IPOs at the fastest clip since the financial crisis, fueling a frenzy in the shares of newly listed companies that echoes the technology-stock craze of the late 1990s, the Wall Street Journal reports

- BlackBerry’s (BBRY) future may become clearer as soon as today when a tentative agreement from Fairfax Financial Holdings (FRFHF) to take BlackBerry private for $4.7B is scheduled to be firmed up. Bids from any others are due then too, and it is possible the deadline could be extended, the Wall Street Journal reports

- Anadarko Petroleum (APC) is considering the sale of its holdings in oil and gas projects in China, in a deal that could be valued at about $1B, sources say, Reuters reports

- Chinese police investigating allegations of widespread corrupt practices at GlaxoSmithKline (GSK) are likely to charge some of its Chinese executives b

ut not the British drugmaker itself, sources say, Reuters reports - Mitsubishi Corp. (MSBHY), Asia’s largest trading company by market value, is expanding into property development in Southeast Asia as the slowdown in China shrinks profits from its commodity businesses, Bloomberg reports

BARRON’S

Twitter (TWTR) looks promising at $20 IPO price, not at $30

Discover (DFS) could gain over 20% next year

Boeing (BA) could rise 30% by 2015

Covanta (CVA) could rise 40% or more

Coke (KO) a good play for low-volatility, income seeking investors

T-Mobile (TMUS) looks to ‘unseat’ Verizon (VZ), AT&T (T)

SYNDICATE

Seadrill (SDRL) files to sell 10M common units for holders

Spherix (SPEX) raises $2M in a private placement

Tetraphase (TTPH) files to sell 3.3M shares of common stock

Xinyuan Real Estate (XIN) files to sell 18.63M American Depositary Shares

Zogenix (ZGNX) files to sell $60M in common stock

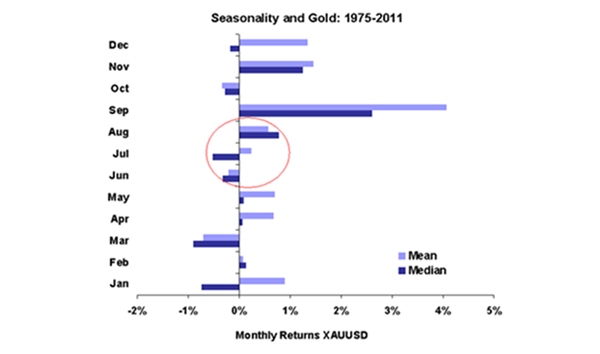

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/sBzgwbhsuVU/story01.htm Tyler Durden