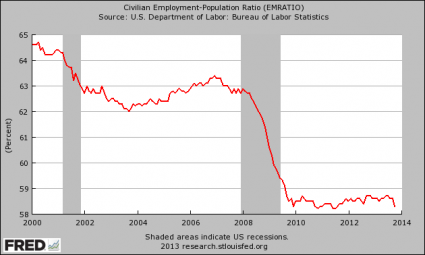

A decision by the FHFA requiring the GSEs to finally release detailed information on loans they acquired and guaranteed uncovers an ugly truth about the GSEs that many should be aware of (as we noted the exuberance here). The release was only required on 35 million fully-amortizing, full documentation, 30-year fixed rate mortgages, which means as JPMorgan's Michael Cembalest notes the underwriting histories on another 20-30 million loans (e.g., the riskier ones) remain a mystery (and likely will forever). As Cembalest concludes, some people made up their minds on all the factors causing the housing crisis in 2009, and others in 2011. As long as new information keeps coming out, it seems premature to close the book on it, he adds, first, the private sector descent into underwriting hell took place well after the multi-trillion dollar GSE balance sheets had gone there first; and second, there are many reasons to wonder how bad the former would have been had the latter not preceded it.

Via JPMorgan's Michael Cembalest,

"The Course of Empire": A Retrospective On The US Housing Crisis

Thomas Cole’s 19th century paintings entitled Course of Empire, chronicling the rise and fall of civilizations, have been reinterpreted below as a commentary on the US housing crisis. Why now? This retrospective is made possible in part by a decision by the Federal Housing Finance Authority requiring Freddie Mac and Fannie Mae to finally release detailed information on loans they acquired and guaranteed1. The release was only required on 35 million fully-amortizing, fulldocumentation, 30-year fixed rate mortgages, meaning that the underwriting histories on another 20-30 million loans (e.g., the riskier ones) remain a mystery. Some people made up their minds on all the factors causing the housing crisis in 2009, and others in 2011. As long as new information keeps coming out, it seems premature to close the book on it; it took 30 years for Friedman to diagnose the Great Depression. This latest disclosure, though partial and purposefully incomplete, adds to the evolving understanding of what took place, why, and in what sequence. Everyone is entitled to their opinion; the charts and the data below explain mine.

“The Pastoral State”

Informed by the experience of the 1980’s housing crisis, by 1990, government sponsored enterprises Fannie Mae and Freddie Mac adhered to prudent underwriting on single family mortgages. The GSEs had a small allowance for loans outside traditional investment-grade standards: loans with debt-to-income ratios above 38%, loan-to-values above 90% on purchase loans, or loan to values on cash-out refinancing loans above 75%2. However, these exceptions were typically justified by compensating factors such as higher cash reserves or higher levels of equity. Even the Federal Housing Administration, which focuses on lower income households and first time homebuyers, acted with more restraint than in later years when measured by their LTVs over 97%.

The GSEs had a one third share of outstanding mortgages compared to GSE plus private sector lending. Private sector subprime had existed for decades, but was limited in size at ~10% of annual residential mortgage origination. Home ownership rates and home prices relative to income and replacement cost were stable at post-war averages.

“Consummation of Empire”

The era of sound GSE lending did not last. The 1992 “Federal Housing Enterprises Financial Safety and Soundness Act” enabled the Department of Housing and Urban Development to set formalized minimum affordable lending standards for the GSEs. Only George Orwell could have named a bill that was so fundamentally contradicted by its purpose and consequence. HUD first set Low & Moderate Income standards at 30% of annual GSE acquisitions, and raised them to 50% in the week before the November 2000 election. In the wake of the bill, in 1994, Fannie Mae issued a press release citing its commitment to transforming the housing finance system, vowing to provide $1 trillion in targeted lending, and citing a goal of eliminating the “no” in the mortgage application process. Prudent 1990 GSE underwriting standards, designed to benefit future borrowers and not just current ones, were discarded. Home ownership rates jumped, and home prices relative to replacement cost, rent and household income began to rise above historically stable levels.

By 2002, the revolution is complete: the GSEs increased their market share from one third to 60% as the size of the mortgage market rose by 2.5x vs. 1990; Freddie Mac’s non-traditional loans were ~45% of their annual acquisitions and guarantees; Fannie Mae claimed that the FHA was its only competitor, asserting that it had become overwhelmingly an affordable housing company; and more than 40% of Fannie Mae’s Alt A (low documentation) loans qualified for the HUD-determined affordable housing goals. These developments were celebrated by HUD as a “revolution” in affordable lending. In 2002, Nobel Laureate Joseph Stiglitz and future OMB Director Peter Orszag cited the probability of a shock to GSE balance sheets as “substantially less than one in 500,000”, and estimated the expected cost to the government of guaranteeing $1 trillion of mortgages at $2 million. Yes, you read that correctly.

Note that the GSE revolution takes place before the explosion in private sector subprime and Alt A loans. The private sector, seeing its market share shrink, organizes several not-so-successful efforts to constrain GSE expansion. Private sector subprime and Alt A market shares remain constant, but its underwriting becomes riskier as the GSEs encroach on their territory with a multi-trillion dollar balance sheet.

“Prelude to Destruction”

GSE non-traditional loans eventually converge to 40%-50% of their annual underwriting, culminating with a warning from Fannie Mae to shareholders about losses from affordable lending. There are some remarkable quotes from HUD in 2000 on how it expected this GSE revolution to result in a private sector revolution as well; it eventually did. The private sector finds a way to compete: the deepening of private mortgage backed securities markets. Propelled by demand when the Fed cut policy rates to 1% in 2002, PMBS markets did not price much of a differential between subprime and traditional risk. As a result, the funding advantage enjoyed by GSEs was conveyed to private sector originators. Privately securitized mortgages skyrocket, home prices surge further, and the mortgage market doubles in size vs. 2002. The private sector regains market share, mostly through subprime and Alt A loans which rose to 40% of annual origination. To be clear, private sector defaults and losses per dollar on subprime were much worse than on GSE loans, particularly when related to malignant derivative offshoots. To complete the circle, the GSEs support private sector origination by purchasing $275 billion of mostly subprime mortgage-backed securities by 2005. With these trends in place, it’s only a matter of time before it all comes undone.

I did not reproduce Cole’s last painting in the series (“Desolation”) since we know what came next. The paintings above convince me of 2 things. First, the private sector descent into underwriting hell took place well after the multi-trillion dollar GSE balance sheets had gone there first. Second, there are many reasons to wonder how bad the former would have been had the latter not preceded it. I have doubts that public consciousness is aware of this timeline and the impact of public policy on it, and stronger doubts that data on the millions of undisclosed, riskier Fannie Mae and Freddie Mac loans will ever be released. Let’s just leave it at that.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/cZGkd1tesdk/story01.htm Tyler Durden