- MOAR: BOJ Said to See Significant Room for More Bond Purchases (BBG)

- Meltdown Averted, Bernanke Struggled to Stoke Growth (Hilsenrath)

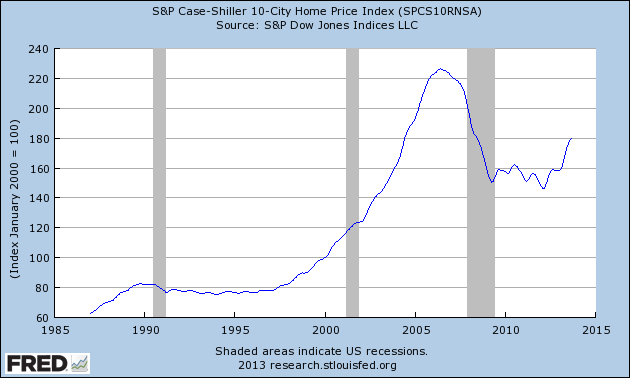

- New Mortgages to Get Pricier Next Year (WSJ)

- Republicans to Seek Concessions From Obama on Debt Limit (BBG)

- Hunting for U.S. arms technology, China enlists a legion of amateurs (Reuters)

- Jury Begins Deliberating in Case of SAC Portfolio Manager (WSJ)

- BP to Write Off $1 Billion on Failed Well (WSJ)

- Rajan Unexpectedly Keeps India Rates Unchanged to Support Growth (BBG)

- Thai protesters say they will rally to hound PM from office (Reuters)

- SEC Brings Fewer Enforcement Actions, Slows Early-Stage Probes (WSJ)

- Eurozone agrees ‘backstop’ for failing banks (FT)

- Merkel Prods EU Finance Chiefs as Bank-Failure Talks Heat (BBG)

- China confirms near miss with U.S. ship in South China Sea (Reuters)

Overnight Media Digest

WSJ

* Russia lavished Ukraine with a bailout package worth at least $20 billion on Tuesday, trumping the West in a Cold War-tinged struggle that keeps the former Soviet republic in Moscow’s orbit.

* Inflation is slowing across the developed world despite ultra-low interest rates and unprecedented money-printing campaigns, posing a dilemma for the Federal Reserve and other major central banks as they plot their next policy moves.

* A five-year battle between the largest U.S. bank and one of its regulators escalated Tuesday when JP Morgan Chase & Co sued the Federal Deposit Insurance Corp over the messy 2008 purchase of Washington Mutual Inc’s banking operations.

* First-year enrollment at U.S. law schools plunged this year to levels not seen since the 1970s as students steered away from a career that has left many recent graduates loaded with debt and struggling to find work.

* Xiaomi Inc, the startup that has rattled China’s smartphone market with its fast-selling handsets, is looking to tap its international fan base for help as it tries to expand abroad, according to its new American executive.

* Private-equity firm Centerbridge Partners LP backed out of a deal to acquire LightSquared Inc, the telecommunications firm in bankruptcy proceedings, amid uncertainty over when federal regulators would clear the way for the company to build out its wireless network, said people familiar with the matter.

* Frontier Communications Corp agreed to buy AT&T Inc’s landline telephone, broadband and TV operations in Connecticut for $2 billion in cash, expanding its base of operations and shoring up the ability to pay its dividend.

* The world may be anxious to welcome Microsoft Corp’s next chief executive. The company’s board isn’t in a rush. John W. Thompson, the Microsoft director leading the search, said in a blog post Tuesday that the board doesn’t expect to name a new CEO until next year.

* After fighting over everything from arcane spectrum rules to telecom mergers, Dish Network Corp and Sprint Corp are showing signs of becoming friends. Sprint, the No. 3 U.S. cellphone carrier by subscribers, and Dish, a satellite TV company, said Tuesday they will work together to test a fixed wireless broadband service in Corpus Christi, Texas, beginning in the middle of next year.

* A coming vote for control of the board of Telecom Italia SpA could finally dispel confusion over the strategy of the telecommunications company, allowing it to pursue an investment plan to address Italy’s “hypercompetitive” telecom market, Chief Executive Marco Patuano said in an interview.

* China’s Wanda Cinema Line Corp is expanding its partnership with IMAX Corp signing on 80 new IMAX theaters in a deal that would make China the big-screen company’s largest market.

FT

BP Plc accused a U.S. lawyer of making “misrepresentations” about the number of clients he represented in his legal action against the energy giant over the 2010 Deepwater Horizon disaster.

3M, whose products range from Post-It notes to films used in flat-panel TVs, said it may buy back up to $22 billion worth of shares in the five years until 2017, jumping on the bandwagon of U.S. companies announcing sizable capital returns to investors.

JPMorgan Chase & Co, the largest U.S. bank, has sued the Federal Deposit Insurance Corporation, which managed the receivership of Washington Mutual after the it failed during the financial crisis and then sold most of its assets to JPMorgan.

Britain’s Airports Commission on Tuesday outlined two ways to grant Heathrow a third runway, while casting severe doubt on proposals for a hub in the Thames estuary that had been championed by Mayor of London Boris Johnson.

British retailer House of Fraser is in advanced, exclusive talks to be bought out by French department store chain Galeries Lafayette, according to two sources familiar with the situation.

NYT

* William Morris Endeavor, working with its private equity partner, Silver Lake Partners, beat out two other groups with an offer of about $2.3 billion for IMG, according to people with direct knowledge of the matter, who spoke on the condition of anonymity because the companies intend to announce the acquisition on Wednesday.

* Facebook is betting the patience of some of its users against the hundreds of millions of dollars it could make on video advertisements. The company will place video ads into some news feeds – the stream of items on a Facebook page – starting this week.

* The first initial in the ABC television network stands for “American,” but it might well stand for “asterisk.”

* A bipartisan tax-and-spending plan designed to bring some normalcy to Congress’s budgeting after three years of chaos cleared its final hurdle on Tuesday when 67 senators voted to end debate on the measure and bring it to a final vote before it goes to President Obama for his signature.

* Frank Darabont, the creator of one of television’s biggest hit shows, “The Walking Dead,” escalated his long feud with the AMC network on Tuesday, charging in a lawsuit that he had been cheated out of tens of millions of dollars because of “self-dealing” by the network.

* President Obama has chosen a former Microsoft executive, Kurt DelBene, to replace Jeffrey Zients as head of the effort to finish repairs on the government’s health insurance website, administration officials said on Tuesday.

* BP on Tue

sday accused a Texas lawyer of fraudulently driving up its settlement costs in the 2010 Gulf Coast oil spill by claiming to represent tens of thousands of clients who turned out to be “phantoms.”

* Some e-commerce marketers are having a challenging holiday season, and they blame Google for it. A change to Gmail that relegated retailers’ emails to a separate inbox for promotions has had a big effect during the busiest shopping period of the year, according to three services that manage mass emails. And another change to Gmail, involving the way it shows images in messages, made it harder for retailers to track who opens their emails.

* The deal world remained muted this year in terms of big transactions and activity. According to Dealogic, the number of announced takeovers in the United States so far this year was down about 22 percent, while volume was $1.1 trillion, up about 15 percent from last year but still below the level in the years before the financial crisis.

* The Bill & Melinda Gates Foundation has tapped Susan Desmond-Hellmann, chancellor of the University of California, San Francisco, as the next chief executive of the charitable organization.

Canada

THE GLOBE AND MAIL

* Manitoba is calling for a recount of its population, claiming Statistics Canada’s estimate is too low and is ultimately shortchanging the province in transfer payments.

The province believes it has 18,000 more people than the 1,265,015 residents Statscan says it has, with the province arguing it will lose $100 million in federal transfers because of the discrepancy.

* Toronto city council met to discuss water rates and rules with the integrity commissioner on Tuesday, but instead, all eyes were on the controversial mayor, Rob Ford, as he stood twice to apologize, danced in the chamber, argued with a councillor and received a personal visit from Santa Claus in his office.

Reports in the business section:

* Two of Barrick Gold Corp’s independent directors – Robert Franklin and Donald Carty – resigned suddenly on Tuesday, the company said in a surprise announcement that came less than two weeks after it overhauled its board and nominated four new independent board members.

* Imperial Oil Ltd has applied to build a $7-billion steam-driven Alberta oil sands project during a period in which industry-wide costs are expected to climb because numerous major developments will be under construction.

* The dozens of First Nations along the route of TransCanada Corp’s Energy East pipeline should not expect offers for equity stakes in the $12-billion project as the company seeks approval, although a host of other economic benefits would accrue to the communities, TransCanada’s chief executive said.

NATIONAL POST

* Ontario’s elite private schools have won a court battle to enforce their own discipline free from judicial oversight, following the controversial expulsion of a student caught smoking a bong on his last day of high school.

* Oil sands advocacy group Ethical Oil has filed a formal complaint against a judge who participated in a mock trial of well-known environmentalist David Suzuki. Held at Toronto’s Royal Ontario Museum in November, the live theater performance put Suzuki on “trial” for seditious libel.

FINANCIAL POST

* The National Energy Board will release a verdict on Enbridge Inc’s Northern Gateway pipeline on Thursday, setting the stage for a decision on the contentious pipeline by the federal cabinet next year.

* BlackBerry Ltd’s interim Chief Executive John Chen has found the man he wants to lead the struggling company’s enterprise services business.

Late Tuesday, BlackBerry officials announced John Sims, formerly the president of SAP AG’s mobile service business, as the new president of the division.

* After receiving nearly 200 submissions from market players during months of consultations, Canadian regulators have decided to combine scrutiny of mutual fund compensation with a separate consideration of whether they need to overhaul the rules governing the relationship between financial advisers and retail clients.

China

CHINA SECURITIES JOURNAL

– The most severe threat to China’s economy in 2014 could come from its volatile property market, experts and analysts told the paper. The real estate environment could lead to the weakening of investment and a hard landing, they said.

– China’s banking regulator discussed drafting regulations on the establishment of private banks and the use of private capital to establish small and medium-sized banks in a meeting held on Monday, the paper said.

SHANGHAI DAILY

– Online sales of masks and air purifiers on China’s online marketplace Taobao have reached 870 million yuan ($143.3 million) so far this year amid the country’s worsening smog. Rival JD.com said similar sales had increased 685 percent versus 2012.

SHANGHAI SECURITIES NEWS

– Chinese search engine firm Baidu Inc is set to launch a new financial management product “Baifa” on Dec. 20 in conjunction with asset management firm Harvest Fund. The product will have a 1 yuan threshold for investment.

CHINA DAILY

– Authorities in China’s northeastern Hebei province began the demolition of 18 cement factories on Tuesday in a bid to clean up soaring levels of pollution. Seventy-four plants on the outskirts of Shijiazhuang, the provincial capital, are targeted for destruction by March.

PEOPLE’S DAILY

– Some of China’s government units have become complacent about mass education, said a commentary in the paper that acts as the Party’s mouthpiece. Such complacency only underlines the importance of educating the masses, it said.

Britain

The Telegraph

NETWORK RAIL TO ADD 30 BLN STG TO GOVERNMENT DEBT

Network Rail is to be reclassified as a public-sector company, adding 30 billion pounds ($48.72 billion) to public sector net debt. The change to the status of the state-owned company that manages Britain’s railway network, will take place next September, the Office for National Statistics said.

CO-OP BONDHOLDERS BACK 1.5 BLN STG RECAP

The Co-op Bank’s 1.5 billion pound emergency recapitalisation has passed its final investor hurdle as the lender received the support of bondholders for the deal.

SIR MARTIN SORRELL BUYS INTO DAVOS

Martin Sorrell’s WPP Plc has bought a 30 percent stake in Richard Attias & Associates, the conference producer behind the annual meeting of political and business leaders in Davos in the Swiss Alps.

The Guardian

MARK CARNEY STANDS BY FORWARD GUIDANCE POLICY

Bank of England Governor Mark Carney has robustly defended his forward guidance policy in parliament against critics who argue it is confusing and has done little to persuade markets that an interest rate rise can be delayed for three years while the economy mends.

GLAXOSMITHKLINE TO STOP PAYING DOCTORS TO PROMOTE DRUGS

Britain’s biggest pharmaceutical company, GlaxoSmithKline , has said it will stop paying doctors tens of millions of pounds a year to promote its drugs.

LIBOR RATE-RIGGING SCANDAL TRADER PLEADS NOT GUILTY

A former UBS and Citigroup trader has pleaded not guilty in a London court to charges that he had sought to manipulate Libor benchmark interest rates with employees from around 10 leading banks and brokerages.

BOB DIAMOND COULD GAIN MILLIONS FROM NEW AFRICAN INVESTMENT VENTURE

Bob Diamond, ousted as boss of Barclays last year after the Libor-rigging scandal, potentially stands to reap millions of pounds from a new stock market venture set up to acquire financial services companies in Africa.

HEATHROW AND GATWICK SHORTLISTED FOR NEW RUNWAYS

A new battle looms over a Heathrow third runway –

or a second at Gatwick airport – after the Airports Commission said that additional capacity was needed in the south-east of England. Extra runways at London’s two biggest airports are on the shortlist the commission will study before issuing its final recommendation.

CAR INSURANCE TOO HIGH, SAYS COMPETITION COMMISSION

Car insurance premiums are too high, with the way no-fault claims are settled and contracts between insurers and price comparison sites among the issues driving up costs for consumers, the competition watchdog has said.

The Times

MANUFACTURING SECTOR HOLDS ITS MOMENTUM

Growth in factory orders and output has remained at its highest since the mid-1990s, confirming that the manufacturing recovery has kept its momentum. The Confederation of British Industry’s survey of nearly 400 factory bosses found that nearly all industry sectors reported growth for a second consecutive month.

HOUSE OF FRASER CLOSE TO FALLING INTO FRENCH HANDS

House of Fraser, one of Britain’s oldest retail chains, is in late-stage talks with a view to being bought by the family owned French department store Galeries Lafayette, it emerged last night.

The Independent

UK INFLATION FALLS TO A 4-YEAR LOW AT 2.1 PCT IN NOVEMBER

The lowest inflation for four years added to the UK’s economic purple patch yesterday, following strong quarterly growth and declining unemployment in boosting the nation’s recovery prospects next year.

MEGA DISCOUNTERS LURING CUSTOMERS AWAY FROM BIG FOUR SUPERMARKETS IN RECORD NUMBERS, SAYS KANTAR

Half the country shopped at an Aldi or Lidl in the last three months for the first time on record, with cash-conscious shoppers love-affair with discount supermarkets shows no signs of slowing down.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

Luxottica (LUX) upgraded to Overweight from Neutral at HSBC

Pan American Silver (PAAS) upgraded to Neutral from Underweight at JPMorgan

Roadrunner (RRTS) upgraded to Buy from Hold at Stifel

Southern Copper (SCCO) upgraded to Buy from Neutral at Citigroup

Downgrades

Avon Products (AVP) downgraded to Neutral from Buy at BofA/Merrill

El Paso Electric (EE) downgraded to Hold from Buy at Jefferies

Jabil Circuit (JBL) downgraded to Sell from Neutral at Citigroup

Kinross Gold (KGC) downgraded to Neutral from Overweight at JPMorgan

LATAM Airlines (LFL) downgraded to Sell from Neutral at Goldman

Nanometrics (NANO) downgraded to Hold from Buy at Stifel

Royal Bank of Scotland (RBS) downgraded to Underweight from Neutral at HSBC

Targacept (TRGT) downgraded to Neutral from Buy at MKM Partners

Tower Group (TWGP) downgraded to Neutral from Buy at Compass Point

Initiations

Alere (ALR) initiated with an Outperform at JMP Securities

Arc Logistics (ARCX) initiated with a Buy at Citigroup

ArrowHead Research (ARWR) initiated with a Buy at Jefferies

Cognex (CGNX) initiated with a Buy at BB&T

DaVita (DVA) initiated with a Buy at KeyBanc

Envision Healthcare (EVHC) initiated with a Buy at KeyBanc

Eros International (EROS) initiated with a Buy at UBS

Fabrinet (FN) initiated with a Buy at B. Riley

Foundation Medicine (FMI) initiated with an Outperform at JMP Securities

GigOptix (GIG) initiated with a Buy at B. Riley

Groupon (GRPN) initiated with an Outperform at Northland Securities

Illumina (ILMN) initiated with an Outperform at JMP Securities

LabCorp (LH) initiated with a Market Perform at JMP Securities

MEDNAX (MD) initiated with a Hold at KeyBanc

Mirati Therapeutics (MRTX) initiated with a Buy at Jefferies

NeoPhotonics (NPTN) initiated with a Buy at B. Riley

Organovo (ONVO) initiated with a Market Perform at JMP Securities

Plains GP Holdings (PAGP) initiated with a Buy at Citigroup

QIAGEN (QGEN) initiated with an Outperform at JMP Securities

Quidel (QDEL) initiated with a Market Perform at JMP Securities

Rackspace (RAX) initiated with a Neutral at UBS

Restoration Hardware (RH) initiated with a Buy at KeyBanc

Tableau Software (DATA) initiated with a Neutral at RW Baird

United Rentals (URI) initiated with a Buy at Jefferies

World Point Terminals (WPT) initiated with an Outperform at Wedbush

HOT STOCKS

Amazon Web Services (AMZN) announced upcoming China region for cloud computing platform

Kraft Foods (KRFT) authorized $3B share repurchase program

Jabil Circuit (JBL) to sell aftermarket services unit for $725M, announced $200M share repurchase program

Blackstone (BX) purchased three Texas power plants from Direct Energy for $685M cash

BorgWarner (BWA) acquired all shares in Gustav Wahler, terms not disclosed

Teva (TEVA) confirmed agreement with Pfizer (PFE) to settle generic Viagra patent litigation

iRobot (IRBT) CEO Angle told CNBC he sees ‘a high growth year’ in 2014

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Lennar (LEN), HEICO (HEI), VeriFone (PAY)

NEWSPAPERS/WEBSITES

- Some advertisers rejoiced when Facebook (FB) introduced long-awaited video advertisements. A bigger question is how users will react and some are wary, the Wall Street Journal reports

- Consumers can expect to pay more to get a mortgage next year, the result of changes meant to reduce the role that Fannie Mae (FNMA) and Freddie Mac (FMCC) play in the market, the Wall Street Journal reports

- The Fed will decide today whether the U.S. economy is finally resilient enough to withstand less policy support, or whether it is prudent to wait a bit longer. A policy announcement is expected at 2 p.m., Reuters reports

- Boeing (BA) is narrowing its list of sites for building its newest jetliner, the 777X, to “a handful,” signaling its determination to consider locations outside Washington state where it now builds similar planes, Reuters reports

- New BlackBerry (BBRY) CEO John Chen, rejecting calls to exit the hardware business, gets a chance this week to convince investors he has the time and vision to revive a unit that’s dragging sales back down to 2007 levels, Bloomberg reports

- Goldman Sachs (GS) is among as many as 11 companies set to be fined early next year in a four-year-old EU antitrust probe into an underwater power cables cartel that tests regulators’ ability to penalize private-equity investors, sources say, Bloomberg reports

SYNDICATE

AMC Entertainment (AMC) 18.421M share IPO priced at $18.00

MarkWest Energy (MWE) announces 4.75M unit sale under equity distribution agreement

Opexa Therapeutics (OPXA) 4.12M share Spot Secondary priced at $1.70

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/n3mWGw3bVA8/story01.htm Tyler Durden