Platner’s Replacement May Not Be Eligible For Nomination

Maine Democrats gathered in Bangor on Saturday to select a replacement for Graham Platner, whose Senate campaign collapsed under allegations of sexual assault – which he denied – that surfaced after his June primary win. Former Senate President Troy Jackson formally won the nomination. He will face Republican Sen. Susan Collins in one of the nation’s most closely watched Senate races, a race that Democrats have deemed critical if they hope to win the majority in the Senate.

However, one inconvenient detail threatens to complicate Jackson’s coronation: a Republican state lawmaker says Jackson may not be legally eligible to accept the nomination at all.

State Rep. James White (R-Guilford) sent a letter to Secretary of State Shenna Bellows asking her office to determine whether Jackson, or any candidate who lost a primary for a different federal, state or county office in June, qualifies as a replacement nominee under Maine law. White wanted the question settled before Bellows certifies whatever comes out of Saturday’s convention, but that didn’t happen, which could be a problem.

Rep. James White has sent a letter to Shenna Bellows suggesting that Troy Jackson is not legally allowed to become the Senate nominee:

“The apparent justification for Mr. Jackson’s eligibility depends entirely on treating the June primary and November general election as… pic.twitter.com/NnTS3bSxFp

According to White, Jackson’s own ballot history might make him legally ineligible. Jackson ran for governor earlier this year, lost that Democratic primary in June, and became his party’s Senate nominee through a replacement process rather than a primary vote of his own.

Under Title 21-A, Section 331 of Maine election law, “a person may not file, whether by primary election or nomination petition, as a candidate for more than one federal, state or county office at any election.” He also points to Section 351, which imposes similar restrictions, and Section 363, which requires that a political committee filling a nomination vacancy “shall choose a qualified person to fill the vacancy.”

Whether Jackson still counts as a “qualified person” after losing a statewide primary is the crux of White’s argument. “The Department should resolve this question before accepting or certifying any replacement nomination,” he wrote.

White reaches back to 1974 for precedent, citing the U.S. Supreme Court’s ruling in Storer v. Brown, which described primary elections as “an integral part of the entire election process.” His argument is that treating June’s primary and November’s general election as two separate contests cuts against both the Court’s reasoning and the Legislature’s stated intent to keep candidates from seeking more than one office “at any election.” White’s letter frames this as standard sore loser logic. Laws of this type exist across the country to stop a candidate who loses one race from reaching the general election through a side door.

Maine has no explicit sore loser statute on the books, unlike several other states that spell out the prohibition in plain language. White’s position is that the existing patchwork of Title 21-A provisions accomplishes the same result even without a dedicated clause. Maine law does allow parties to replace nominees who withdraw after winning a primary, which is how Democrats find themselves in this position following Platner’s exit, but the statute never quite addresses what happens when the proposed replacement lost a separate statewide primary of his own.

Reasonable election law observers could land on either side of this question, and if a legal challenge follows Jackson’s nomination, according to The Maine Wire, a court may end up settling the matter, and depending on how that plays out, could put Democrats in a real bind.

The Secretary of State’s office did not issue a public response to White’s letter before the convention, and it remains unclear whether Bellows intends to produce a formal legal opinion. And Bellows is no neutral arbiter here: she was herself a candidate in this very Senate race, one of the contenders who dropped out and cleared the path for Jackson in the days before the convention. Regardless, Bellows, a Democrat, wouldn’t rule against her own party’s interest anyway, but clearing Jackson’s candidacy, especially now, won’t end the matter, since a court challenge could still follow.

If such a challenge were to proceed, and in the unlikely event it were to prevail, disqualifying Jackson would upend the Democratic Party’s effort to field any candidate against Collins with barely four months remaining before Election Day, a scramble that could pave the way for Collins to win in November easily.

19 Million Eggs Pulled As Salmonella Outbreak Sickens 98 Across 17 States

The FDA and CDC have tied a growing Salmonella outbreak to eggs produced by Texas-based Midwest Poultry Services, which recalled roughly 1.5 million cartons – more than 19 million eggs – after the contamination surfaced. As of July 24, 98 people across 17 states had been sickened, according to the FDA, which said the recalled eggs are “a likely source of illnesses in this outbreak” and that its investigation is ongoing.

The recall itself went out through an FDA notice on July 22, before the illness count was attached. The eggs may be contaminated with Salmonella Enteritidis, a subtype that can cause serious and occasionally fatal infections in young children, the elderly, and the immunocompromised.

“Midwest Poultry Services identified the issue on its two Texas farms through proactive environmental monitoring practices and root cause analysis,” the company said, adding that it “is not distributing fresh eggs produced on its Texas farms at this time.” The company said it began diverting eggs to a breaking plant, where they would be pasteurized to kill any pathogens, and characterized the recall as precautionary. It did not respond to a request for more detail on how it detected the possible contamination.

There is a wrinkle worth noting. The recalled eggs were produced between June 6 and July 3, but the outbreak’s illness onsets stretch from Nov. 21, 2025 all the way to June 30, 2026 – a seven-month span far wider than the production window. That is why the FDA is describing the eggs as a likely source “in part” and says it is still investigating whether other foods are involved.

How To Check Your Carton

The eggs carried “sell by” or “best by” dates ranging from July 20 to Aug. 17. The recalled cartons carry an identifying code of P-1950 or 0840962 with a Julian date between 157 and 184, printed in date-coding ink on the side of the carton. No other Midwest Poultry Services products are affected.

The eggs were available at Kroger stores in Louisiana and Texas and Brookshire Grocery stores in Arkansas, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas, as well as smaller retailers not named in the notice. They were also shipped to foodservice customers in Texas, Oklahoma, and Louisiana. Kroger and Brookshire Grocery did not respond to requests for comment.

People who bought the eggs can return them for a full refund. Salmonella infection typically sets in 12 to 72 hours after exposure, with symptoms – diarrhea, fever, nausea, vomiting, abdominal cramps – usually lasting four to seven days.

Stealers Wheel’s 1973 hit “Stuck in the Middle with You” could well become the theme song for today’s middle-income, first-time home buyers who don’t qualify for affordable housing programs yet cannot afford market-rate homes.

The household income required to purchase a starter home, currently priced under $350,000 in the United States, has surged more than 80 percent to $78,000 from $43,000 in 2019, according to a July 20 report from Realtor.com.

By contrast, the median household income was $83,730 in 2024, representing an increase of under 22 percent from $68,703 in 2019, according to the latest Census Bureau estimates.

This gap in growth between home prices and household incomes has made it increasingly difficult for even middle-income households to own a home, real estate professionals, economists, and recent research say.

Caught In The Middle

Vlora Sejdi, an associate broker with HomeSmart in White Plains, New York, recently told The Epoch Times about the challenges her young clients face in buying a home.

She is currently working with a childless couple under 40 who are living with parents while saving for a down payment on a home in Westchester County, an affluent suburb north of New York City, which had a median home price of $867,398 in May, according to Redfin.

“Home prices here just keep going up and up,” she said. “It’s a seller’s market and people who can afford to buy are willing to go above and beyond. We’re still seeing bidding wars.”

“They’re very unhappy with the current situation, and I think there’s also a shock factor for what their monthly payments will be with mortgage, taxes, and insurance,” she said.

Sejdi said another of her clients, a woman in her 20s, also from Westchester County, is currently renting while searching for a co-op, a type of housing in which residents purchase shares in a cooperative corporation that owns the building, rather than own individual units, according to Apartments.com.

Co-ops tend to be much less expensive than condos or single-family homes. According to OneKey MLS, in Westchester County, the median sales price for co-ops was $223,750 in May, compared with $576,500 and $1,200,000 for condos and single-family homes, respectively.

However, these properties are controlled by a co-op board of directors that can set stringent financial requirements for anyone seeking to purchase an apartment.

“My client actually had one accepted offer, but the board would not approve her, despite the fact that she now pays significantly more in monthly rent than she would for monthly maintenance at the co-op,” Sejdi said.

Sejdi will continue to search for other possibilities but admits the journey has been challenging for both of them.

“There’s definitely a lack of attainable housing for the middle class in Westchester,” she said. “These are people who make too much money to qualify for affordable housing, but don’t have enough to afford market-rate homes.”

Sejdi’s clients requested anonymity.

The Pew Research Center classifies households earning between 67 percent and 200 percent of the overall median household income, adjusted for household size, as “middle-income” households.

Based on the Census Bureau median of $83,730, this means those households had annual incomes of between $56,100 and $167,460.

In Westchester County, the median household income was $118,596 in 2024.

According to Westchester County government documents, the county’s affordable housing programs include developments for households earning up to 120 percent of the area median income (AMI), though the income limits vary by development.

The current 120 percent AMI income limits for one-person and two-person households in the county are $162,800 and $142,450, respectively.

The situation is not limited to high-priced markets like New York. Middle-income, first-time buyers in more affordable areas, such as Texas, also face affordability challenges.

“North Texas is still considerably more attainable than markets like New York or California, but affordability has become one of the biggest challenges facing first-time buyers here as well,” Johnny Mowad, associate broker with Ebby Halliday Realtors in Dallas, told The Epoch Times.

At the end of May, Redfin reported that the median sales price was $498,702 in Dallas and $337,798 in Fort Worth.

As in many other parts of the country, Mowad noted that wages have not kept pace with housing costs, and the demand in Northern Texas remains high as more people relocate to the area.

“That puts more pressure on inventory,” he added.

Housing Mismatch

A joint May report by NAR and Realtor.com indicates that the much-needed housing recovery is not reaching the people who are most likely to restart the market.

“Buyers earning about $75,000 can afford only 23 percent of active listings nationwide,” the report states. In a balanced market, they would be able to access about 44 percent.

The report notes that the gap represents about 311,000 missing listings priced below their maximum purchase point, which is estimated at $261,000.

“Too much of the inventory available today remains concentrated at higher price points, leaving a shortage of options for entry-level and middle-income buyers,” Nadia Evangelou, NAR principal economist, said in the report.

According to a June 24 Pew Research Center survey, 89 percent of America’s adults younger than 40 said it’s harder for them to own a home than for their parents’ generation.

The report attributes the perception primarily to rising housing costs and a challenging job market, which have made homeownership feel out of reach for many young adults.

The Harvard Joint Center’s June 17 State of the Nation’s Housing report states that, with a nationwide median price of about $417,400 for new single-family homes in 2025, most new housing was unaffordable for median-income households based on the standard affordability threshold of 30 percent of income.

Existing homes were less attainable. With the median price rising 54 percent since 2020 to $419,300, according to the National Association of Realtors (NAR), a typical single-family home sold at five times the median household income in 2025, the Harvard report notes. By contrast, the report said the average price-to-income ratio was 3.2 in the 1990s.

The median existing home price rose further to $440,600 in June, reaching an all-time high, the NAR said on July 9.

Using first-quarter data, a May 12 analysis by HSH Associates, a private mortgage and housing finance information company, found that U.S. households needed an annual income of $103,419 to afford a median-priced home. The calculation assumed buyers obtained a 30-year fixed-rate mortgage with a 20 percent down payment, while taking into account principal, interest, property tax, and insurance payments.

Of the 50 largest metropolitan areas analyzed, only 12 had required incomes below the national average for buying a median-priced home, the report shows. For high-priced markets such as San Jose, California, and New York City, the required incomes were $477,409 and $197,521, respectively. The median home prices of these cities were $2,030,000 and $750,000, respectively. In Dallas, households needed $105,798 to afford a median-priced home, according to the HSH Associates report.

Millions Of Adults Living At Home

With housing costs and a challenging job market, the Harvard report says, “Many young adults cannot afford to form new households, instead doubling up or living with family.”

The report shows that household growth, a primary driver of housing demand, slowed for the third straight year to 1.1 million in 2025, down from an average annual growth of 2.0 million in 2020 and 2021.

A mid-June report from Realtor.com indicates that one in three adults under the age of 35 – about 25.2 million people – lived with their parents in 2025, as they were priced out of the housing market.

“The adults living with their parents today are largely employed, and many hold college degrees. What’s holding them back isn’t a lack of qualifications, but rather, at least in part, a lack of housing they can actually afford,” Realtor.com senior economist Hannah Jones said in the report.

The data show that about nine in 10 adults aged 25 to 34 living with parents have never been married and about one in three aged 25 to 29 hold a four-year college degree. Men comprise the majority of this group at every age level.

Meanwhile, according to a June 25 report from the Census Bureau, the nation’s fertility rates have dropped almost every year since 2007, although they have risen in certain counties throughout the country.

The Year Of ‘Starter Homes’

Robert Dietz, chief economist at the National Association of Home Builders (NAHB), recently told Siyamak Khorrami, the host of EpochTV’s “Market Insider,” that a decade and a half of underbuilding, especially of entry-level housing, is a key factor contributing to the housing affordability issue Americans are facing.

While Realtor.com estimated in March that the United States was short by about 4.03 million homes in 2025, NAHB put the number at about 1 million using different methodology.

Dietz said the current housing shortage suggests pent-up demand is building among young homebuyers – there are just not enough homes on the market that fit their budgets.

“One really interesting data point that we track is the number of young adults who live with their parents. Right now, one out of five of those 25- to 34-year-olds live with their parents. Back 20 years ago it was one out of 10, so that share has doubled,” he said, citing a May NAHB analysis.

A northern California-based developer, Chris Duffy, founder and CEO of Hummingbird Development, agrees that the nation needs more entry-level housing, but providing that is very difficult due to rising construction costs.

“The cost of construction has gone up so much over the past 20 years,” he told The Epoch Times. “With land, materials, labor, permits, architect costs, and other regulatory fees, the economics of building less expensive homes just doesn’t work. Most new developments have to go with luxury housing to make a profit.”

Duffy noted that depending on where they decide to build, it can take years to jump through all of the local government regulations.

In the organization’s July 9 report, NAR chief economist Lawrence Yun warned that home prices could accelerate if housing inventory continues to stagnate.

The solution, noted Dietz, is to build more housing of all types, including single-family and multifamily for both sale and rent. He noted that construction of more multifamily options can help builders adapt to the challenges of creating more affordable homes.

“For example, we’ve seen a big rise in townhouse construction,” he said. “These are homes that are connected; they require less land.”

In its June 30 Housing Market Indicators report, the American Enterprise Institute called 2026 “the Year of ‘Starter Homes’ and ‘Small Lot, Small Lot, Small Lot.'”

The institute said 188 housing bills had been introduced so far this year, including 26 pending, enacted, or passed bills in 15 states that align with the AEI Housing Center Playbook. The Playbook outlines policy recommendations to increase the supply of naturally affordable housing.

AEI projects that enacted, passed, and pending bills aligned with the Playbook’s three policy options – smaller lots for new homes, greater flexibility on existing residential lots, and more housing near jobs and amenities – could add about 281,000 homes annually.

Because land prices are more affordable in the Sun Belt and Midwest, Dietz said new home construction has experienced growth in those areas. Demand for lower-entry-home price points continues to be strong throughout the nation, he said.

Mowad said while home purchasing remains challenging for younger buyers, starter homes do come up in the market, though they may not represent someone’s dream home. He noted that younger, middle-income buyers who are determined to make a purchase may start with a condo or townhome.

“While affordability has certainly tightened over the last several years, I’d much rather be a first-time buyer in Dallas than in many coastal markets,” he said. “In many parts of the Northeast, buyers are competing against housing costs that simply don’t align with middle-income salaries.”

Mowad said the region has been attracting many new residents due to a lower cost of living relative to other major metropolitan areas, a large concentration of Fortune 500 company headquarters, and no state income tax.

“People aren’t just moving here for cheaper homes; they’re moving here for careers and long-term opportunities,” he said.

Meanwhile, Sejdi is serving on the newly created Westchester County Board of Legislators’ Affordability and Economic Development Task Force that will address how to bring more affordable and middle-income housing into one of America’s most expensive areas.

“We are hopeful that together we can develop some solutions that will help people in the lower and middle-income brackets be able to afford to make their homes here,” she said.

India’s Education Minister Resigns, Delhi Protests End As Modi Caves To ‘Cockroach’ Youth Movement’s Demands

India’s education minister, Dharmendra Pradhan, resigned on Saturday and the government agreed to every demand raised by youth demonstrators, bringing weeks of protests – the gravest political crisis of Prime Minister Narendra Modi’s third term – to a jubilant close.

Pradhan’s exit was the core demand of the self-styled Cockroach Janta Party (CJP), the youth movement that has camped at Delhi’s Jantar Mantar since late June over the leak of medical school entrance exam papers. The May leaks forced the cancellation of results and a retest for some 2 million students, and have been linked to several student suicides.

Word of the resignation set off celebrations at the protest site, where thousands of young people danced, chanted victory slogans and handed out sweets as the national anthem played over loudspeakers. “We have done it,” CJP founder Abhijeet Dipke told the crowd. Roads around the neighbouring Connaught Place business district were shut as revellers poured in.

In a post on X announcing his decision, Pradhan said he had sent his resignation to the prime minister so that forces hostile to the country could not take advantage of the situation, and voiced deep respect for the aspirations and legitimate expectations of India’s young people.

Hours later, Health Minister J.P. Nadda and Jitendra Singh, a junior minister in the prime minister’s office, held a joint press conference with CJP representatives following a further round of talks. Nadda confirmed the government had accepted the movement’s full list of demands, which included an overhaul of the examination system, the withdrawal of police cases filed against protesters, and compensation for the families of students who died by suicide after the leaks.

CJP spokespeople formally declared the agitation over and urged supporters across the country to head home peacefully.

The settlement prompted a swift unwinding of the security clampdown that had paralysed parts of central Delhi through the week. Mobile data services around the protest site – which the government had ordered telecom companies to switch off, leaving shopkeepers, vendors and restaurants unable to take digital payments for much of the week – were restored on Saturday. The 16 Delhi Metro stations shut in and around the area, closed for most of the past four days, reopened.

The outcome amounts to a rare climbdown for Modi, who is known for standing firm under public pressure. Pradhan, 57, the son of a veteran Bharatiya Janata Party politician and himself a senior figure once floated as a possible party president, had held the education portfolio since 2021. He is just the second minister in Modi’s 12 years in power to leave office amid a scandal, after M.J. Akbar stepped down as junior foreign minister in 2018 during India’s #MeToo movement.

The protests were the biggest youth revolt Modi has faced since taking office in 2014, and they had intensified sharply over the past week. Tens of thousands marched on parliament on Monday, where police responded with tear gas and cane charges; on Wednesday night, a crowd of more than 10,000 gathered at Jantar Mantar and some protesters pelted police with stones and bottles. Solidarity rallies spread to cities including Ranchi, Pune, Thiruvananthapuram and Kolkata, while opposition parties, echoing the students’ demands, held up the monsoon session of parliament all week.

Modi’s first public attempt to calm the unrest – a pledge on Thursday to create special courts to try those behind paper leaks, alongside his declaration on X that “Nothing is more important than the welfare and future of our youth!” – was dismissed by the CJP, which countered that punishing culprits after the fact did nothing to address why papers keep leaking in the first place.

Beyond the exam scandal, the movement tapped deeper frustration among young Indians over scarce jobs and official accountability – discontent that carries echoes of the youth uprisings that toppled governments in neighbouring Sri Lanka, Nepal and Bangladesh in recent years. With young voters a key constituency for the BJP and major state elections due next year, the political stakes for Modi were considerable.

Among those marking the moment was activist Sonam Wangchuk, who had spent 26 days on hunger strike in support of the students and hailed the outcome as proof of what peaceful persistence can achieve.

The United States said on Friday it will end a ban on imports of Mexican cattle implemented more than a year ago to combat the New World screwworm (NWS), a flesh-eating livestock pest that has already made it into Texas and New Mexico.

In its announcement, the U.S. Department of Agriculture (USDA) said it would coordinate a phased reopening of southern cattle ports beginning Aug. 24.

USDA officials said the United States will first start taking Mexican cattle again at Douglas, Arizona, with two more ports in New Mexico to follow.

The reopening will be staged and depends on Mexico sticking to its New World screwworm control plan. Officials called the move safe to begin now.

Ports in Arizona and New Mexico sit farther from the heaviest infestations in Mexico, livestock traders noted, which lowers the immediate risk compared with Texas crossings.

“Every animal entering the United States through these ports will undergo a full USDA inspection to ensure it is free of any signs of New World screwworm (NWS),” the USDA said.

The United States suspended imports of live Mexican cattle and related livestock on May 11, 2025, as part of efforts to curb the spread of the parasite.

Also on Friday, Mexican President Claudia Sheinbaum said that she had directed local authorities to speed preparations for the reopening.

“I have instructed that we accelerate our work and collaboration with the United States even further to have everything ready as soon as possible to restart the movement of cattle,” she said in a post on X.

“Exports will resume starting in the last weeks of August through Agua Prieta, Sonora, followed shortly thereafter by two additional points in the state of Chihuahua.”

The USDA said it has identified Sonora and Chihuahua as the lowest-risk Mexican states for New World screwworm due to their strong, well-established inspection programs and their geographic distance from southern Mexico, where most cases are concentrated.

On Friday, U.S. Secretary of Agriculture Brooke L. Rollins said, “The closure of the Southern ports of entry for the last year has been a tough but necessary action to control the spread of NWS in Mexico and protect the American livestock industry.”

The New World screwworm is a parasitic fly whose females lay eggs in open wounds or mucous membranes of any warm-blooded animal. The hatched larvae burrow into living flesh and can kill the host if left untreated.

The pest has pushed north through Central America. It appeared in June on Texas farms and in New Mexico, representing the first confirmed U.S. cases since 2017. One early case involved a 3-week-old calf in south Texas, with others found in goats, calves, and a dog.

Beef Industry In Turmoil

The United States typically imports more than 1 million head of cattle from Mexico each year, roughly 5 percent of the animals that go through American processing plants. Those calves usually head to U.S. feedlots for finishing, and prices spiked.

The decision also comes after domestic cattle supplies in the United States fell to a 75-year low. Beef prices rose to records this year, with meat processors struggling; Tyson Foods closed a large processing plant in Nebraska in January, and JBS said it would shutter one in Pennsylvania in mid-August.

The $100 billion U.S. beef industry contracted most sharply in Texas, the nation’s top cattle state.

Texas Agriculture Commissioner Sid Miller called the reopening the right thing for ranchers and consumers, though he said it should have happened earlier.

“While I’m pleased to see this important trade relationship restored, the prolonged closure has already taken a toll on producers, disrupted supply chains and created uncertainty that could have lasting consequences for the cattle industry,” Miller said.

He added that while action has moved in the right direction, “the pace and scale of the screwworm response have not gone far enough.”

USDA has invested in sterile-fly production, which is the main tool used to push the pest back in past decades. It has renovated facilities in Mexico and activated dispersal sites in Texas.

Yet production remains under the hundreds of millions of sterile flies needed weekly to push the infestation south, as the pest entered the country despite the ban.

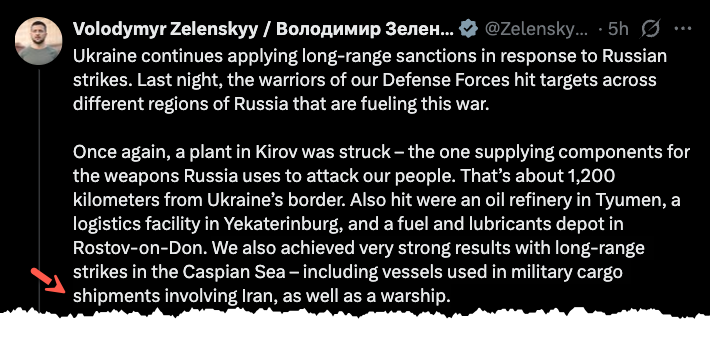

War Zones Converging? Zelensky Says Ukraine Hit Ship “Transporting Military Cargo” From Iran

Ukraine has rapidly expanded its one-way attack-drone campaign from the Sea of Azov into the Black Sea, claiming strikes against more than 180 vessels and maritime targets around the Crimean region over the past three weeks, according to Reuters. The widening maritime offensive follows a summer campaign in which Ukrainian drones struck dozens of Russian energy assets, warehouses and logistics hubs.

The risk of the Russia-Ukraine conflict merging with the US-Iran conflict seems plausible, but remains low at this point, despite overnight signals from Ukrainian President Volodymyr Zelensky on X that Ukrainian forces had hit “military cargo shipments involving Iran.”

Zelensky noted, “We also have very good results from long-range strikes in the waters of the Caspian Sea. In particular, these are vessels that were involved in transporting military cargo from Iran, and a warship.”

In August 2025, Ukraine struck the Russian cargo ship Port Olya-4 at a Caspian Sea port, saying it was loaded with Iranian Shahed drone components and ammunition.

An Estonian-born blogger on X, who goes by “WarTranslated,” cited Iranian Telegram channels claiming that Tehran is “threatening ballistic missile strikes on Ukraine after Zelensky said they hit a military vessel carrying cargo between Russia and Iran.”

Iranian Telegram channels are threatening ballistic missile strikes on Ukraine after Zelensky said they hit a military vessel carrying cargo between Russia and Iran. pic.twitter.com/t6TXWAaoUQ

The Ukrainian drone strike on the Iran-linked vessel points to deeper Russia-Iran military cooperation, likely centered on Tehran’s transfer of Shahed drone technology, components and munitions to Moscow.

More or less, this is just noise from both sides. Still, the two Eurasian war zones remain connected through Russia-Iran military cooperation, creating an ongoing risk that any escalation could cause the conflicts to converge into a broader confrontation. That risk remains low, but it cannot be dismissed.

Canadian authorities seized nearly 1.7 metric tons of illegal drugs during a cross-border investigation named Project Bay. The haul included suspected cocaine, methamphetamine and opium. Authorities estimated the products’ street value above $139 million. Investigators called it one of Ontario’s most significant seizures from a single case.

Traffickers used broker-style transportation model

Windsor Police launched the investigation in January 2025. The Canada Border Services Agency joined the effort the following month. Investigators worked to identify a trafficking network with connections to the international border. Ontario Provincial Police later supported the cross-border and interprovincial portions.

Investigators found a broker-style model operating within the commercial transportation sector. The organization used established connections to arrange cross-border drug movements. Drivers knowingly transported the illegal products within legitimate supply chains, according to the release. Authorities continue investigating the network’s source and full scope.

U.S. Homeland Security Investigations and the Drug Enforcement Administration assisted with international aspects. Toronto Police and Peel Regional Police also provided operational and investigative support. Several specialized Canadian units participated during the searches. Those agencies included local, provincial and federal law enforcement partners.

Searches uncover drugs, firearms and cash

Police teams executed 18 search warrants on June 25. The locations included Windsor, Corunna, LaSalle, Brampton and Kleinburg. Authorities conducted two additional searches in Markham and Caledon on July 14. Investigators then carried out two more in Brampton on July 20.

Authorities seized 973 kilograms of suspected cocaine and 660 kilograms of suspected methamphetamine. They also recovered 49 kilograms of suspected opium and 230 oxycodone tablets. Officers found 17 firearms, including an anti-tank rifle. The haul also contained ammunition, brass knuckles, magazines and a baton.

Investigators recovered C$80,000 and US$10,000 during the operation. Officers also took one vehicle as offense-related property. Additional items included high-end jewelry, money counters, 43 cellphones and six laptops.

Twenty-one people face 104 offenses

Authorities charged 21 people with 104 offenses under two Canadian laws. Those statutes include the Criminal Code and the Controlled Drugs and Substances Act. Police arrested 19 defendants during the operation. Two others remain wanted under outstanding arrest warrants.

The OPP Provincial Asset Forfeiture Unit joined the case. Its investigators will examine possible offenses involving criminal proceeds. The unit will also assist with taking property connected to alleged crimes. Project Bay’s broader investigation remains active.

“This seizure reflects the scale of criminal activity that crosses borders and impacts communities across Ontario,” OPP Chief Superintendent Mike Stoddart said. He credited cooperation among municipal, provincial, federal and international partners. “We have significantly disrupted the flow of harmful substances,” Stoddart said. He also said authorities removed substantial profits from the criminal economy.

“This investigation began as the result of information obtained by the Windsor Police Service,” Chief Jason Crowley said. He said the operation later expanded across several Ontario jurisdictions. Crowley credited law enforcement partners with dismantling the network. He said the organization moved dangerous drugs and firearms into communities across the province.

CBSA’s Southern Ontario region has seized 5,555 kilograms of illegal drugs at land ports this year. Officers there have also seized 206 firearms during that period. Regional Director General Michael Prosia credited cooperation among domestic and international agencies. He specifically thanked Ontario Provincial Police and Windsor Police for their work.

Project Bay remains an active investigation. Before publication, FreightWaves contacted OPP for additional information about the transportation operation. OPP did not provide a response before publication. FreightWaves will update this article as officials release more details.

Why it matters

The case shows how criminal networks can place illegal products inside legitimate commercial supply chains. Transportation professionals can use these details to recognize how traffickers may exploit industry connections.

Fauci no longer faces any realistic risk of criminal exposure for perjury or other past federal offenses covered by the pardon.

Next week, Dr. Anthony Fauci is scheduled to testify before Sen. Rand Paul’s Senate Homeland Security and Governmental Affairs Committee. After years of stonewalling, evasions, carefully parsed denials, and outright lies, this hearing presents a rare opportunity to get answers from America’s most notorious mad scientist, who recklessly funded dangerous animal experiments that likely caused COVID-19 and financed beagle torture in labs worldwide.

This time is different.

In one of his final acts in office, in January 2025, President Joe Biden granted Fauci a sweeping pardon that conspicuously covered a decade-long period starting when he first funded the infamous grant that paid the Wuhan lab, which was first exposed by White Coat Waste in early 2020 and cut days later by President Donald Trump.

This means that Fauci no longer faces any realistic risk of criminal exposure for perjury or other past federal offenses covered by the pardon. So, the usual Fifth Amendment justification for refusing to answer questions about potentially self-incriminating conduct is largely off the table.

Paul should press Fauci on three false statements he has repeatedly made to Congress, the press, and the American people about the Wuhan lab and BeagleGate – claims debunked by evidence obtained by White Coat Waste.

First, Fauci needs to finally fess up about funding gain-of-function animal experiments at the Wuhan Institute of Virology.

But White Coat Waste has receipts. Our Freedom of Information Act investigations uncovered damning internal government emails from 2016 showing that NIH officials told EcoHealth Alliance that its Fauci-funded animal experiments with the Wuhan lab “appear to involve” gain-of-function research that was banned at the time.

Instead of stopping the experiments, NIH worked with disgraced EcoHealth president Peter Daszak to skirt the ban. Daszak gleefully celebrated the decision, writing, “This is terrific! We are very happy to hear that our Gain of Function research funding pause has been lifted.”

In May 2024, then-acting NIH Director Lawrence Tabak finally admitted to the House Oversight Committee that NIH did, in fact, fund gain-of-function in Wuhan.

Paul should ask a simple question: Does Fauci still stand by his testimony, or will he finally acknowledge that his previous statements to Congress were false or misleading?

Second, Fauci should answer for his testimony denying that he used his personal email for official NIH business.

During House testimony in 2024, Fauci declared to Chairman James Comer, “To the best of my recollection and knowledge, I have never conducted official business via my private email.”

Yet White Coat Waste’s FOIA investigations uncovered official NIH emails showing Fauci telling a Washington Post reporter covering the BeagleGate scandal, “I will send you an email via my Gmail account.”

Records have also emerged showing that David Morens, Fauci’s longtime advisor who was indicted in April for FOIA violations, told Daszak and others in 2021, “I can either send stuff to Tony on his private Gmail or hand it to him at work. . . He is too smart to let colleagues send him stuff that could cause trouble.”

Will Fauci come clean?

Finally, Paul should revisit BeagleGate – the viral dog testing scandal first exposed by White Coat Waste that Fauci and his allies spent years falsely dismissing as a conspiracy.

In a 2021 Washington Postcover story written by the same reporter Fauci said he would contact through his personal Gmail account, he called the dog testing claims “ridiculous accusations and outright lies.” In his 2024 memoir, Fauci again dismissed the story as “lies,” “lunacy,” and “off-the-wall accusations” and defended himself by awkwardly saying, “I am a passionate animal lover, especially of dogs.”

But government documents obtained by White Coat Waste prove that Fauci funded countless dog labs, including the infamous experiments in Tunisia, where beagles were drugged and had their heads locked in mesh cages full of biting sand flies. After reviewing these records, even the Washington Post, which had aggressively defended Fauci and smeared White Coat Waste, finally acknowledged in 2024 that it published NIH disinformation, acknowledging that “NIH was not fully transparent as it tried to handle a public-relations nightmare.”

Paul was one of the lawmakers who led the charge with White Coat Waste to hold Fauci accountable for funding beagle abuse and lying about it.

Americans deserve answers.

Next week’s hearing may be Congress’s last meaningful opportunity to confront Anthony Fauci directly and finally set the record straight on Wuhan and BeagleGate. Paul should seize it.

* * * [ZH]: Not everyone is convinced Rand can bring the heat. What say you?

Fuck this guy too. He’s a powerless loser who is essentially a blow off valve for the disaffected pic.twitter.com/XJJb4PUnBo

Democrats Are Worried The GOP’s Cash Advantage Could Hurt Their Chances In The Midterms

The Democratic Party heads into the midterms with generic congressional ballot polling and historical precedent on its side. It is nevertheless worried that the majorities it so desperately wants could still slip away.

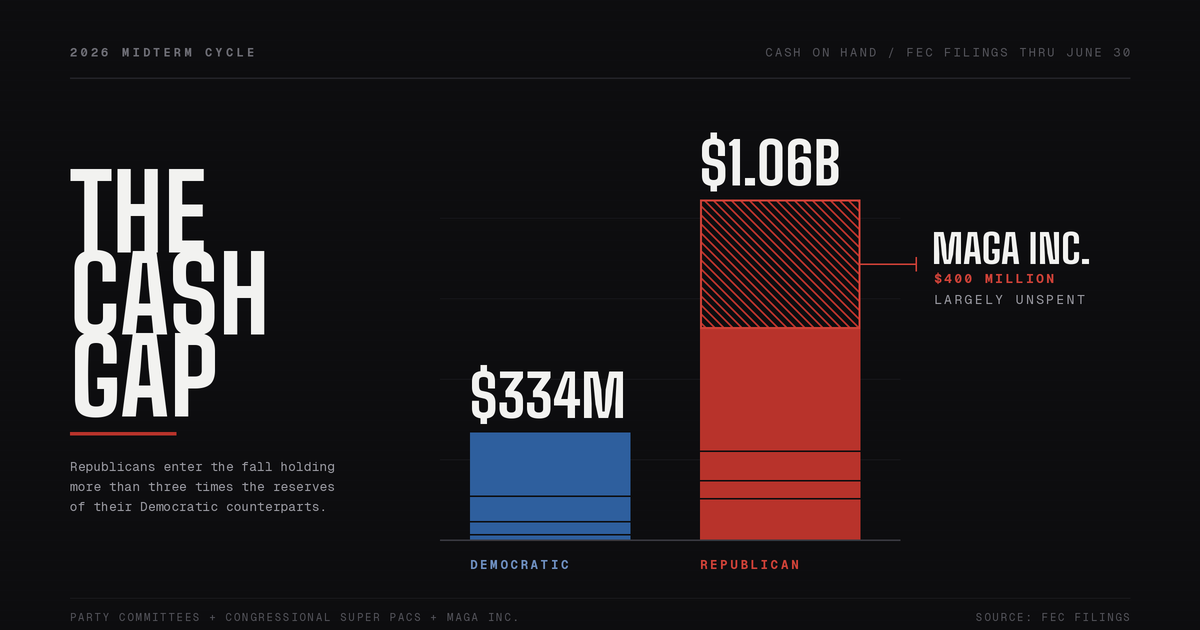

Politicoreported this week that Democratic strategists increasingly fear their favorable political environment could be overwhelmed by a Republican cash stockpile that dwarfs their own.

Federal Election Commission filings through the end of June show the three main GOP national committees and their affiliated congressional super PACs sitting on a combined $657 million. Their Democratic counterparts held $334 million. Add President Trump’s MAGA Inc. super PAC, which reported more than $400 million on hand several weeks earlier, and the Republican reserve runs to more than three times what Democratic Party committees and congressional super PACs can muster between them.

That gap matters more this cycle than it would have in any previous one. On June 30, the Supreme Court ruled in NRSC v. FEC that federal limits on coordinated party spending violate the First Amendment, overturning a 2001 precedent and freeing national party committees to spend without ceiling in direct coordination with their candidates. Committee money that once had to be routed through independent expenditures can now be aimed straight at a race.

Democratic strategist Morgan Jackson, an adviser to former Gov. Roy Cooper’s Senate campaign in North Carolina, calls the imbalance the central threat to his party’s hopes this cycle.

“What is putting the House majority and the Senate majority, nationally, in danger is the Republicans’ massive stockpile of resources that they’re putting together to push back,” Jackson said.

He warned that the spending gap could erode the advantage Democrats have built everywhere else. “If you get outspent five to six to eight to one, that can alleviate the environmental advantage that Democrats have this cycle,” Jackson said.

The committee-level numbers are lopsided almost everywhere. The Republican National Committee reported $128 million in cash against $16 million for the Democratic National Committee, which is also carrying $18 million in debt. The National Republican Senatorial Committee held $55.9 million to the Democratic Senatorial Campaign Committee’s $41 million. The National Republican Congressional Committee held $92.7 million to the Democratic Congressional Campaign Committee’s $79 million.

The super PAC gap is wider still. Senate Leadership Fund, the leading Republican Senate super PAC, reported roughly $112 million more on hand than the Democratic-aligned Senate Majority PAC. Congressional Leadership Fund, its House counterpart, held about $51 million more than House Majority PAC.

The national totals obscure a more complicated picture in the marquee Senate races, where the money runs the other way. Democratic Sen. Jon Ossoff holds roughly $40 million more on hand than Rep. Mike Collins in Georgia. In Texas, Democrat James Talarico has nearly $20 million more than Attorney General Ken Paxton. In North Carolina, Cooper is about $17 million ahead of former Republican National Committee Chairman Michael Whatley. In several of the contests that will decide both chambers, individual Democratic candidates are burying their opponents even as the national party apparatus falls behind.

The picture inside the party gets messier once primary season is factored in. A wave of insurgent challengers aligned with the Democratic Socialists of America has forced sitting Democratic incumbents into costly primary fights this cycle, draining accounts well before anyone gets near a Republican opponent.

Senate Majority PAC spokeswoman Lauren French rejected the idea that the committee gap tells the whole story. “Republicans can crow all they want about getting massive checks from donors and businesses and billionaires, but we’re going to win because we have the actual support from people who are voting,” French said.

Other Democratic strategists are less confident that grassroots enthusiasm can offset a structural disadvantage. Jesse Ferguson argued that the media environment itself has made the shortfall more expensive than it would have been in past cycles. “Too many people think that fragmentation of media meant more efficiency and spending less. Wrong – it means you have to spend more,” Ferguson said. The proliferation of streaming platforms, social media, and other digital outlets has driven up the price of political advertising, strategists say, raising the stakes for whichever side can deploy the deepest reserves of outside money.

What should worry Democrats most is that the Republican advantage has barely been touched. Trump political director James Blair said last month that Republican spending would begin “very soon,” without offering a timetable. The fear on the Democratic side is that the bulk of MAGA Inc.’s $400 million war chest is being held back deliberately, to be dumped into competitive House and Senate races in the closing weeks – at the exact moment undecided voters start paying attention and Democratic committees have the least room left to answer.

President Donald Trump issued an executive order on July 24 directing signs to be placed outside one of the Smithsonian Institution’s history museums warning visitors that some exhibits contain inaccurate information.

The order references a July report by the White House Domestic Policy Council, which alleges that the National Museum of American History “cannot be trusted to tell America’s story honestly and in a way that is inspiring, unifying, and worthy of our great republic.”

Trump said in his order that the report shows that “the Smithsonian leadership does not present American history as a shared national inheritance to be taught and celebrated, but instead views American history as a ‘prime tool’ to advance ideas of social justice and the radical transformation of our society.”

The president directed his administration to use “all available authorities” to encourage the Smithsonian Institution to correct the issues identified in the report and ensure compliance with the laws, funding requirements, and contract conditions.

The order instructs the Interior Department to place temporary signage along the sidewalks and walkways that are maintained by the National Park Service and used by the public to access the museum, informing visitors of the report’s findings.

The signage will direct visitors to locations and resources presenting what the president deems accurate information regarding America’s history, according to the order.

The Smithsonian Institution did not return a request for comment by publication time.

The National Museum of American History, located in Washington, was originally named the National Museum of History and Technology when it was opened in January 1964. The museum was renamed in October 1980.

The museum’s collection includes more than 1.7 million objects representing the nation’s heritage in the areas of science, technology, society, and culture, according to its website.

Anthea Hartig, director of the National Museum of American History, defended the museum during a July 21 congressional hearing, saying its work is guided by the Smithsonian’s standards of scholarship and independence.

“The museum does not take sides in America’s political debates,” Hartig said. “We preserve and document the evidence of American life in all of its breadth, so that the public can encounter the past and draw their own conclusions.”

The White House report followed Trump’s March 2025 executive order directing the Interior Department to ensure that public monuments “do not contain descriptions, depictions, or other content that inappropriately disparage Americans past or living.”

The report said the museum has not established any exhibit specifically dedicated to the Founding Fathers, the Second Continental Congress, the Declaration of Independence, the American Revolutionary War, or the nation’s path to independence and the establishment of constitutional rule of law.

“Our central finding is not that the museum has simply added overlooked stories, corrected perceived errors, or broadened its historical scope,” the report stated.

“Rather, it is that museum leadership has explicitly adopted an ideological framework that no longer treats the American story as a shared national inheritance to be taught or celebrated, but as a political instrument to divide, dispirit, and discourage our citizens.”