Submitted by Charles Hugh-Smith of OfTwoMinds blog,

Would printing the cash to fund pensions for low-income retirees trigger inflation? It's more of an open question than we might imagine at first glance.

Correspondent D.L.J. recently suggested an alternative way of looking at Social Security–and our entire scheme of central bank-created money. Let's start by noting that the U.S. Treasury does not create new money (commonly known as printing money) to fund the Federal government's deficit spending–it borrows the money by selling Treasury bonds on the global bond market.

The Federal Reserve has the right to create money out of thin air: it digitally creates money which it uses to buy Treasury bonds, mortgages, etc. The new cash ends up in the hands of whomever sold the Fed the bonds and mortgages–usually primary dealers, Wall Street banks, etc.

The Fed also creates credit out of thin by loaning immense sums or establishing lines of credit for "too big to fail" banks and equally insolvent foreign banks. During the 2008-09 global financial crisis, the Fed extended $16 trillion in credit to global banks. That is roughly equivalent to the entire gross domestic product (GDP) of the U.S.

As millions of Baby Boomers start drawing their Social Security benefits, the system has slipped into deficit. The Social Security Administration (SSA) collected $725 billion in Social Security tax revenues and paid $773 billion for benefits and overhead expenses in 2012, a $48 billion deficit. (Recall that employers and employees each pay 7.65% in payroll taxes on earned income, a total payroll tax of 15.3% of which 12.4% is for Social Security and 2.9% is for Medicare.)

The Treasury raised that $48 billion by selling Treasury bonds that accrue interest, basically forever, as the U.S. is running monumental $1+ trillion deficits every year.

Based on the none-too-pleasant historical results of printing money with abandon, many people are convinced that printing money will trigger a devaluation in the dollar that we experience as inflation, i.e. everything costs more because our money is worth less.

Inflation effectively robs everyone who holds dollars, and it is especially destructive to wage earners, as they are less likely to get raises to keep up with inflation as compared to those with capital and unearned income from stocks, bonds, real estate, oil, etc.

High inflation wipes out savings and destroys the underpinnings of the economy. Venezuela is providing a real-time example of what happens when devaluation of the currency and distortions in the economy triggered by that devaluation take hold: the shelves empty of goods and inflation rises to levels that implode the economy (40% to 50% is usually enough to do the trick).

The Fed has created $2.7 trillion in new money since 2008, yet inflation is tame–less than 2% acording to the Consumer Price Index (CPI). There are several reasons why this money creation has not resulted in the high inflation we would normally expect when $400+ billion of new money is created every year:

1. It isn't enough new money to spark inflation in the vast multi-input U.S. economy.

2. Most of it isn't actually going into the economy, so it has had no inflationary effect.

3. The velocity of money is so low that even a few trillion dollars in new money can't trigger inflation.

There are good reasons to conclude each statement has some validity.

The bloated, debt-dependent status quo is so mired in diminishing returns and state-cartel rentier skimming that a strong case can be made that the system needs a rather substantial quantity of new money and credit to be created every year just to keep the system from imploding.

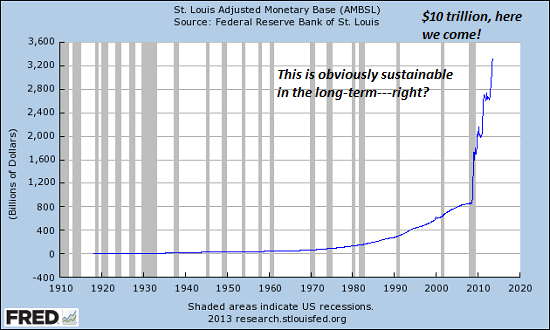

Here is the monetary base, which just hit $3.5 trillion. Note that this is not the same as cash in circulation, but it does show the Fed is still pedal-to-the-metal in terms of creating money out of thin air.

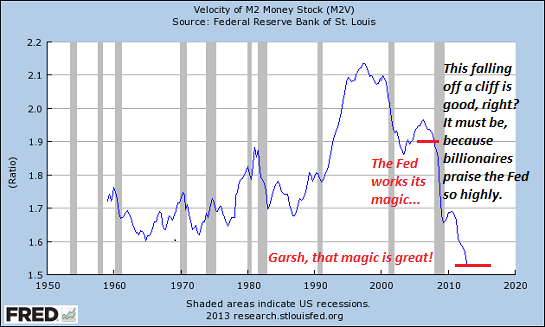

Here is money velocity, diving to new lows.

D.L.J. suggested an alternative to the current system of taxing workers and employers for Social Security, letting the Fed print trillions of new dollars for its banker buddies and borrowing money to fund Social Security deficits that future generations have to pay interest on forever:

Eliminate the Fed (or at least its right to create money) and Social Security, its bogus Trust Funds, its 12.4% (highly regressive) tax altogether and pay retirees with cash printed by the Treasury, not the Fed. Eliminating the Fed (or at a minimum, its ability to create money out of thin air) means there is no "new money" inflationary pressure other than the money printed to pay pension benefits in lieu of Social Security.

Since nobody is paying Social Security taxes, employees and employers both get a hefty 6% tax reduction.

With the system and its promises of a pension to everyone who paid into the system gone, there is no need to pay retirement benefits to those with substantial income from other sources. The program can revert to providing a pension to those with no other substantial income. Those with incomes above $50,000 (i.e. the top 25%) from all sources, earned and unearned, have no need for a Treasury-funded pension; they're hardly at risk of living in a cardboard box. The current system's skewing to lower-income workers would be maintained, so individuals in the top 40% would receive less than those with no other income.

This would slice a major chunk off the annual pension outlays. Let's guesstimate that total outlays would fall to the $600 billion a year range.

The new pension system would not be universal; it would retain the SSA requirement that only those who worked the requisite number of quarters would qualify for a pension.

Would printing and distributing $600 billion a year trigger high inflation? I think that is an open question for the reasons noted above. Is that enough money to unleash inflation in a $16 trillion economy with numerous deflationary pressures? Distributing the newly created cash to retirees rather the Fed's banker buddies will undoubtedly increase the velocity of money, because the new money will be placed in the hands of people who will spend much or most of it.

The government would reduce its liabilities (the bogus Trust Funds) by roughly $4 trillion, and taxpayers will no longer be paying interest on Social Security deficits.

The effect of printing and distributing $600 billion a year is not as straightforward as we might imagine because the economy has many inputs. Consider what would happen once the Fed could no longer print money and use it to suppress interest rates and funnel the cash to its banker cartel.

The stock market would nosedive, interest rates would rise, crushing the bond market, and real estate's current Fed-induced bubble would burst. Trillions of dollars in assets would disappear in a matter of weeks as the economy renormalizes to a state of free-market discovery of asset prices and the end of the Fed's manipulation.

Such a renormalization would be deflationary, as those losing the trillions of dollars in assets will be significantly poorer.

As part of this thought experiment, we can also ask: since the Fed already "prints" $400+ billion a year, would an additional $200-$250 billion in newly created money be enough to tip the $16 trillion U.S. economy into dangerously high inflation?

I think it is fair to say that the answer is contingent on all the other other moving parts and inputs of the economy. If $10 trillion in assets vanishes as a result of the Fed losing its power to manipulate interest rates and reward the bankers, that deflationary tsunami would very likely overwhelm the injection of $600 billion of Treasury-printed pensions.

Would inflation rise in the future after this renormalization? Possibly. But once again the answer depends not simply on the creation of money but all the other factors mentioned above.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/EfhZ7w8WTC4/story01.htm Tyler Durden