S&P 500 futures edged lower along with European shares, as the “peace in our time” optimism that pushed stocks on a history bear market short and gamma squeeze rally in the past two weeks fizzled and was instead replaced with the far less pleasant reality that de-escalation of the war in Ukraine is exaggerated as the Kremlin said that talks with Ukraine in Istanbul Tuesday yielded no breakthroughs and refused to discuss the status of Crimea as part of a peace deal, as the Russian constitution prohibits anyone discussing the fate of Russian regions. The S&P futures were 0.3% lower while Nasdaq futures declined 0.4%. Commodities climbed, fueling renewed concerns about inflation’s impact on profits and economic growth while the inversion of the 2s10s yield curve that started the clock on the next recession did not help investor mood. Europe’s Stoxx 600 snapped a three-day winning streak after surging to the highest level in five weeks and oil futures gained over 2%. The dollar slipped, the euro climbed and the yen bounced from a six-year low after the Bank of Japan pledged to buy more securities than planned and include longer-dated debt.

“The yield curve inversion needs to be sustained before it’s a predictor of anything,” Mariann Montagne, senior portfolio manager at Gradient Investments , said on Bloomberg Television. “We’ll have volatility both in the stock and the bond markets but we think that progression” on the cease-fire talks will lead to upward earnings revisions.

Apple shares were slightly lower in premarket trading, set to end their longest winning streak since 2003 after the iPhone maker surged nearly 20% over the past 11 days. Chinese live-streaming platforms fell in U.S. premarket trading after Chinese government agencies vowed to crack down on any tax-related crimes in the sector. Bilibili (BILI US) falls 3.8%, HUYA (HUYA US) -4.4%. Other notable premarket movers:

- BioNTech (BNTX US) rises 3% premarket as the Covid-19 vaccine- maker says it’s planning a share buyback of as much as $1.5 billion and will propose a special dividend.

- Chewy (CHWY US) slumps 14% in premarket trading after the online pet products retailer’s results missed estimates and it forecast slower-than- anticipated sales growth.

- Microvast (MVST US) slumps 14% in premarket after the battery solutions provider reported 2021 results, with the company’s CEO flagging “many headwinds” in the release.

- RH (RH US) falls 14% premarket after the furniture retailer’s fourth-quarter results missed expectations amid “softening” demand in the current quarter.

- Romeo Power (RMO US) shares jump 7.1% in premarket after the battery-products maker said it has started shipping its first production pedigree packs to a key customer.

On Tuesday, the S&P 500 rallied to the highest level since mid-January. Skeptical NATO allies are evaluating whether Russia’s promise to scale back military operations in Ukraine marks a turning point in the conflict or simply a tactical shift as attacks were still reported near Kiev. Here are some of the latest developments involving the Ukraine war courtesy of Newsquawk:

- Ukrainian President Zelenskiy said they are not reducing defensive efforts as the Russian army still has significant potential to carry out attacks, according to Reuters.

- Ukraine Deputy PM says three humanitarian corridors have been agreed for evacuations on Wednesday; said Ukraine had requested 97 corridors to be opened in the worst-hit areas. Ukraine Forces warn of danger of Russian ammunition exploding at Chernobyl.

- Ukraine Presidential Adviser says on negotiations, Ukraine has improved its position in all respects.

- Russian Kremlin says Ukraine has begun to put demands down on paper and be more specific which is a positive thing. Not seen anything really promising that looks like a breakthrough, there is a lot of work ahead

- Governor of Donestsk region says situation is difficult, shelling is continuing in nearly all cities around the demarcation line.

Germany triggered an emergency plan to brace for a potential Russian gas cut-off, as President Vladimir Putin steps up demands that the fuel should be paid for in rubles. Russia may expand the list of commodities for which it demands payment in rubles to include grain, oil, metals and others.

Meanwhile, as reported last night, BofA analysts echoed Goldman and warned that the 11% surge in U.S. stocks in the past two weeks has the hallmarks of a bear-market rally that might give way to deeper losses. Philadelphia Fed Bank President Patrick Harker said Tuesday he expects a series of “deliberate, methodical” rate increases this year, but said he is open to a half-point move in May if near-term data shows more inflation. Economic data releases Wednesday include U.S. GDP.

“While the Fed faces considerable challenges in pulling off an economic soft landing, the central bank did manage to do so in 1965, 1984, and 1994; thus, we think it is too soon to write off their chances of doing so again, said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We believe investors should brace for higher rates, without overreacting by neglecting areas of value in equity markets.”

Europe’s Stoxx 600 was down 0.6%, but traded off worst levels; sentiment was dented after Kremlin comments that there has been no breakthrough in Ukraine talks. Travel, retail and media names lag; energy and miners outperform. European stocks exposed to Russia and Ukraine slipped in early trading as optimism about a de-escalation of the war in Ukraine faded. The skepticism over Russia’s promise to scale back military operations in Ukraine has dented global stocks and boosted oil prices. Nokian Renkaat, which has a large factory near St. Petersburg, is down more than 7%, among top decliners on Stoxx 600. Here are some of the most notable premarket movers:

- Equinor, Shell, BP and other energy peers lead gains on the Stoxx 600, with the energy subindex its best performer, with basic resources gaining too: Glencore +2.5%, Boliden +4.7%

- Bachem rises as much as 4.1%, the best performer on the Stoxx 600 Health Care index, after Credit Suisse upgraded the company to outperform on its strength in peptides manufacturing

- Bloomsbury Publishing climbs as much as 8.8% after the company best known for the Harry Potter series said the new fantasy novel series ‘Crescent City’ had driven “exceptional” sales in February

- Encavis shares gain as much as 9.3% as Warburg sees an “upbeat outlook” that should “trigger earnings revisions,” after the company reported earnings late Tuesday

- Pearson shares fall as much as 11% after Apollo said it does not intend to make an offer for the firm after being unable to reach agreement over the terms with Pearson’s board

- Nokian Renkaat slides as much as 7.5% after JPMorgan and SEB cut their ratings for the Finnish tire maker due to its exposure to Russia, bringing its YTD loss to over 50%

- Other Russia-exposed peers also fall as optimism about a de-escalation of the war in Ukraine fades: Wizz Air drops as much as 5.5%, Faurecia as much as 7.5%

- Atlas Copco, SKF and Sandvik all fall after after reports emerged in Swedish media that its equipment and service contracts in Russia may have been been used by the military

Earlier in the session, Asian equities advanced for a second day as traders remained cautiously optimistic over Russia’s offer to scale back military operations in Ukraine. The MSCI Asia Pacific Index climbed as much as 0.9%, with Taiwan Semiconductor Manufacturing the biggest contributor following Micron’s strong forecast. Equities in mainland China outperformed, led by gains in brokerages and developers. Japanese stocks retreated as the yen strengthened. Inflation Trade Is Key to Everything in Global Markets Right Now Investors are hoping for a de-escalation in the war in Ukraine, though progress in cease fire talks has been met with some skepticism. Also on traders’ radar are Chinese firms’ earnings results and the risk of trading halts, and the impact from the yield-curve inversion in U.S. treasuries that are typically seen as a sign of future recession.

“With talk of de-escalation in Ukraine, volatility is easing off and that’s a positive for global equities – the benefits of which ought to flow through to an Asian region that’s very sensitive to the economic cycle and commodity prices,” said Kyle Rodda, analyst at IG Markets Ltd. While the yield curve’s inversion is another factor to consider, a recession typically comes anywhere between 12 and 24 months following an inversion implying “there’s no major reason why sentiment can’t remain well supported,” he added. Elsewhere in Asia, stocks in Australia rose for a seven-day winning streak following a stimulatory federal budget package. China tech stocks traded in Hong Kong trimmed earlier advance amid fresh regulatory crackdown worries.

Japanese equities fell as the yen strengthened amid concerns it had weakened too much. More than 1,500 Topix stocks traded without rights to the next dividend, shaving 22.4 points off the benchmark. Banks and automakers were the biggest drags the Topix, which fell 1.2%. KDDI and Tokyo Electron were the largest contributors to a 0.3% loss in the Nikkei 225. The yen strengthened 0.7% against the dollar, extending its 0.8% rally on Tuesday. The yen is still down more than 6% against the greenback since March 4 amid the Bank of Japan’s determination to continue easing. Perceived benefits of the weaker currency have helped boost the Nikkei 5.7% this month, its best since November 2020. “There’s much talk about the yen weakening further but it seems like it has gone too far,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management. The level of products exported from Japan is actually low, so “the image is a little different from reality.”

Australia’s stocks climbed, with the S&P/ASX 200 index rising 0.7% to close at 7,514.50, gaining for a seventh day, its longest win streak since December 2020. The rally followed a stimulatory federal budget package unveiled late Tuesday. Hopes for talks between Russia and Ukraine also helped investor sentiment. Life360 gained the most, rising for a second day, while Telix Pharmaceuticals led decliners. In New Zealand, the S&P/NZX 50 index rose 1.5% to 12,098.80.

In FX, the Bloomberg dollar spot index fell 0.4% as the greenback was steady to weaker against all its Group-of-10 peers; short-dated Treasury yields fell by around 4bps while longer dated ones were steady. European bonds slid, led by shorter maturities, as traders bet hotter-than-expected inflation readings will force the ECB to end its era of negative rates sooner than previously anticipated. Traders are wagering the ECB will raise its key interest rate to zero two months earlier than expected after Spain’s statistics service said EU-harmonized CPI jumped 9.8% from a year ago in March, topping all 15 estimates in a Bloomberg survey of economists. The yen outperformed all its G-10 peers as the options market signaled that a short-term top has been established in spot dollar-yen. The Bank of Japan ramped up efforts to rein in rising yields by offering to buy more debt across maturities. Bank of Japan Governor Haruhiko Kuroda gave another strong indication that the central bank will continue capping long-term bond yields after holding his first meeting with Prime Minister Fumio Kishida since the yen touched its lowest level since 2015

In rates, Treasuries were mixed with the curve steepening, pivoting around a little changed 7-year sector as 2s10s spread continues to widen away from the brief inversion that took place Tuesday. 2-year TSY yields are richer by ~3bp on the day while long-end of the curve cheapens almost 3bp — 2s10s spread steeper by 5bp; wides of the day more than 8bp. U.S. 10-year yields around 2.41%, with bunds and gilts trading 4bp and 1bp cheaper in the sector. Long-end Treasuries underperformed, cheaper on the day and following wider losses across bunds and gilts. Early gains in Asia spurred by Bank of Japan bond-buying operations, especially at long end of the curve which pushed Japanese government bond yields lower. IG dollar issuance slate includes three SOFR deals and a Misc Bhd 3Y/5Y; four issuers priced $5.1b Tuesday, takes weekly total to around $9b vs. $20b to $25b projected

European bonds slid, led by shorter maturities as traders bet higher inflation will force the European Central Bank to end its era of negative rates sooner than previously anticipated. German two-year yields, among the most sensitive to changes in the key policy rate, are on course for their first close above zero since 2014. The German curve bear-flattens, cheapening ~7bps across the short end. ECB-dated OIS rates point to a zero percent depo rate by the October meeting, red pack Euribor drops up to 9.5 ticks. USTs bull steepen, with 2y yields up 5bps. Gilts are comparatively quiet. Peripheral spreads tighten to core.

In commodities, crude futures advanced with WTI adding ~2% near $106.25. Base metals trade in the green; LME aluminum rises over 3%. Spot gold is little changed at $1,919/oz. European natural gas surges as much as 15% after Germany triggered an emergency plan to brace for a potential Russian gas cut-off.

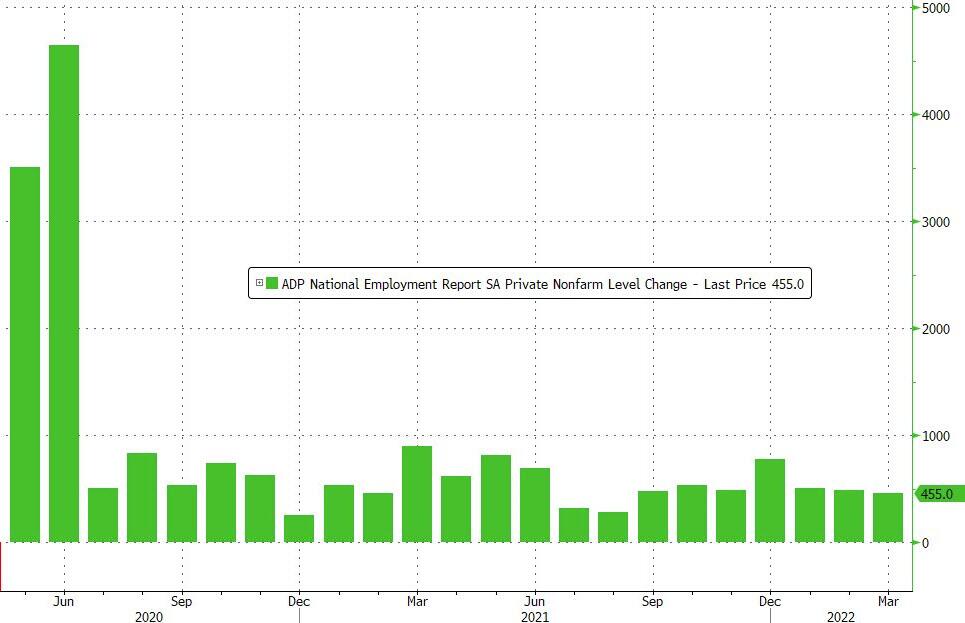

Looking at the day ahead now, and data releases include German CPI for March and Italian PPI for February, whilst in the US there’s the ADP’s report of private payrolls for March and the third estimate of Q4 GDP. Otherwise, central bank speakers include ECB President Lagarde, and the ECB’s Holzmann, Wunsch, Makhlouf and Panetta, along with the Fed’s Barkin and George, and BoE Deputy Governor Broadbent.

Market Snapshot

- S&P 500 futures down 0.3% to 4,609.50

- STOXX Europe 600 down 0.7% to 458.63

- German 10Y yield little changed at 0.64%

- Euro up 0.4% to $1.1131

- Brent Futures up 1.8% to $112.22/bbl

- Gold spot up 0.2% to $1,922.70

-

- U.S. Dollar Index down 0.41% to 98.00

- MXAP up 0.7% to 181.73

- MXAPJ up 1.3% to 595.64

- Nikkei down 0.8% to 28,027.25

- Topix down 1.2% to 1,967.60

- Hang Seng Index up 1.4% to 22,232.03

- Shanghai Composite up 2.0% to 3,266.60

- Sensex up 0.9% to 58,467.18

- Australia S&P/ASX 200 up 0.7% to 7,514.52

- Kospi up 0.2% to 2,746.74

Top Overnight News from Bloomberg

- Skeptical NATO allies are evaluating whether Russia’s promise to scale back military operations in Ukraine marks a turning point in the conflict or simply a tactical shift as attacks were still reported near Kyiv

- ECB President Christine Lagarde said Russia’s invasion poses “significant risks to growth” and has introduced “considerable uncertainty” into the economic outlook. At the same time, sticky energy costs, increasing food prices and persistent bottlenecks “are likely to take inflation higher,” she said

- The initial reaction to the prospect of a peace deal in Ukraine shows how the most important trades in markets are now all about inflation. Equities, Treasuries and the yen all rallied, underscoring how investing is being filtered through an inflation-driven prism rather than by a peace dividend, according to strategists

- In the third week of March, redemptions from China equity funds were the highest since early 2021, while outflows from Chinese bond funds exceeded $1 billion for the first time ever, according to data provider EPFR Global. That’s after regulators made promises this month to ensure policies are more transparent and predictable

- U.S. trade chief Katherine Tai said it’s time to forget about changing China’s behavior and instead take a more defensive posture toward the world’s second- biggest economy

- Germany triggered an emergency plan to brace for a potential Russian gas cut-off, as President Vladimir Putin steps up demands that the crucial fuel should be paid for in rubles

- Germany faces a “considerable risk” of lower output and possibly even a recession because of its high dependency on Russian energy, according to a panel of advisers to Chancellor Olaf Scholz. Even without a gas-supply shutoff, the Council of Economic Experts prediction is that gross domestic product will rise just 1.8% this year, down from a November projection of 4.6%

- BOE’s Broadbent sees an unprecedented external hit to the U.K.’s national income as Russia’s invasion of Ukraine “has led to substantial rises in the cost of energy and other commodities”

- India’s government is considering a proposal from Russia to use a system developed by the Russian central bank for bilateral payments, according to people with knowledge of the matter, as the Asian nation seeks to buy oil and weapons from the sanctions-hit country

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly positive amid optimism from Russia-Ukraine talks in which negotiators discussed a ceasefire and with Russia to scale down military activity in Kyiv and Chernihiv, although the US was unconvinced. ASX 200 gained on continued tech strength and with consumer stocks helped on Budget support measures. Nikkei 225 fell beneath the 28,000 level after weaker than expected Retail Sales and as the Yen nursed losses. Hang Seng and were underpinned after continued PBoC liquidity efforts and amid a deluge ofShanghai Comp. earnings including from large banks in which Bank of China and China Construction Bank both topped estimates

Top Asian News

- China’s Growth Outlook Worsens as Lockdown Fears Escalate

- U.S., India Officials Set to Hold Security Meetings in April

- Logan Unit Warns About Ability to Meet Bond-Repayment Demands

- China Tech Stocks Pare Gains After Reports on Online Video Curbs

European equities (Eurostoxx 50 -0.8%) are mostly lower as optimism from Ukraine/Russia updates yesterday fades and inflation concerns were further bolstered by regional German CPIs. FTSE 100 (+0.1%) remains afloat following gains in Energy and Basic Resources names

Top European News

- BOE’s Broadbent Sees Unprecented External Hit to National Income

- ECB’s Lagarde Says Costs of War Increase the Longer It Lasts

- Spanish Inflation Unexpectedly Soars to Almost 10% on War

- Citi Workers Stay Home as London Power Cut Disrupts Canary Wharf

In FX, Yen repatriation offsets BoJ yield intervention to keep recovery intact – Usd/Jpy extends sharp retreat to circa 121.31 from 125.10 on Monday. Euro inflated by significantly stronger than expected preliminary CPI prints and further EGB/UST yield convergence – Eur Usd takes out recent peak and probes Fib retracement in decent option expiry zone before fading around 1.1160.

Kiwi rebounds on strong building approvals and improvements in NBNZ survey readings – NzdUsd firmly above 0.6950 and AudNzd back under 1.0800. Dollar drifts ahead of ADP and more Fed commentary, with under 98.000.

In commodities, WTI and Brent have continued to pare back some of the aggressive selling pressure seen during yesterday’s

session. From a technical standpoint, May’22 WTI has made it back up to USD 107.30 vs. yesterday’s peak of USD 107.84, whilst June’22 Brent sits at 113.05 vs. yesterday’s peak of USD 114.83. US Energy Inventory Data (bbls): Crude -3.0mln (exp. -1.0mln), Gasoline -1.4mln (exp. -1.7mln), Distillate -0.2 (exp. -1.6mln), Cushing -1.1mln. US House Energy and Commerce Committee is to hold a hearing next week with six oil company executives regarding rising gas prices, according to Reuters. Germany declares “Early Warning” stage of gas supply emergency to prepare for possible escalation by Russia; says no current gas supply shortages. India is to increase natural gas prices for April-Sept to USD 6.10/mmbtu from USD 2.90mmbtu currently, according to Reuters sources.

Spot gold traded sideways and only marginally benefitted from the weaker greenback.

US Event Calendar

- 07:00: March MBA Mortgage Applications, prior -8.1%

- 08:15: March ADP Employment Change, est. 450,000, prior 475,000

- 08:30: 4Q PCE Core QoQ, est. 5.0%, prior 5.0%

- 08:30: 4Q GDP Price Index, est. 7.1%, prior 7.1%

- 08:30: 4Q Personal Consumption, est. 3.1%, prior 3.1%

- 08:30: 4Q GDP Annualized QoQ, est. 7.0%, prior 7.0%

DB’s Jim Reid concludes the overnight wrap

The last two times that the 2s10s first inverted during the cycle occurred when I was on holiday (August 22nd 2019 and way back on December 27th 2005). Proving that the yield curve is no respecter of my two-week holiday starting tomorrow, 2s10s teasingly dipped its toes into negative territory after Europe closed yesterday before discretely re-steepening into the US close (at 2.4bps). Nevertheless, the headline damage was done. The momentum has been toward flatter curves for a while, so this moment has felt inevitable even if it happened quicker than we expected. It is surely only a matter of time before we close inverted. I’ll likely be on holiday when it does so see you in a couple of weeks. First stop a diagnostic and steroid injection today in my back. Henry and Tim will be taking care of the EMR in my absence. First stop LEGOLAND and the Natural History Museum at the end of this week. The latter to see some dinosaurs that aren’t Daddy. See you on the other side.

Back to the curve and 2s10s has now flattened -75.0bps YTD, -17.4bps of which have come over the last two days amidst heightened bond market volatility, which showed no signs of calming yesterday with 2yr and 10yr Treasuries again trading in a wide range. 2yr yields were +12.3bps higher as New York walked in before finishing the day up +3.7bps, while 10yr yields went from +7.4bps higher early in the day to as low as -8.2bps, before closing down -6.4bps. US yields are another -5 to -6bps lower in Asia as I type so 15 to 20bps off the highs 18 hours ago. Yields hit their intraday peaks at this point alongside the peak in optimism around potential peace talks covered in more detail below.

Having said that there were other important bond milestones yesterday. 2yr German debt moved into positive territory in trading for the first time since 2014, although by the close it was “only” up +6.2bps at -0.07%. Note German inflation is coming out later today and the NRW region has just come out at a very high 7.6% which likely means the 6.2% national average expected is going to be beaten. So maybe more grounds for bond volatility today. Also Italian PPI is out. Remember last month this hit an astonishing 41.8% YoY.

This all comes as the Ukraine developments yesterday led to growing conviction that the ECB would commence liftoff in its policy rates this calendar year, and the amount of ECB tightening priced for 2022 went all the way up to +62.1bps by the close, surpassing their previous peak prior to the invasion. At the same time, yields on 10yr bunds (+5.3bps), OATs (+4.9bps) and BTPs (+0.9bps) all hit multi-year highs of their own even if 10yr bunds closed at 0.63, -10bps below its intraday highs of 0.73%.

As discussed near the top, the last leg of the global yield spike higher came as peace hopes exploded in the middle of the European session. However the spike in nominal yields was very short lived as commodities fell back following the positive news, dragging breakevens down with them. This followed some of the most optimistic headlines we’ve seen since the conflict began. In particular, Russia said it would “dramatically reduce” its military operations around Kyiv, and their chief negotiator Vladimir Medinsky said that Ukraine’s proposals would be passed onto President Putin for a response. Meanwhile Ukraine’s negotiator Mykhailo Podolyak said that the agreement offered would see both sides “resolve issues linked to Crimea and the city of Sevastopol though bilateral negotiations”, which Russia has occupied since 2014. So although it’s worth pointing out that we don’t even have a ceasefire yet, the fact that both sides might be edging closer towards one another has seen markets reduce the perceived likelihood of further escalation scenarios. The alternative view is that the Russians are simply diverting resources to other areas and this is purely tactical. So it’s still a long way from being over but the tail risks seem to be reducing.

This growing optimism was evident across multiple asset classes, with European equities moving back up to levels not seen since the conflict began. Indeed, the STOXX 600 (+1.74%) closed at its highest level since February 17, having now recovered by +13.85% since its closing low just 3 weeks earlier. The S&P 500 (+1.23%) also advanced, which reduced its YTD losses to just -2.82%, whilst the NASDAQ was up +1.84%. While fixed income volatility has taken off, equity volatility continues to fall as indices rally and risk sentiment improves. The VIX fell another -0.73ppts yesterday to 18.9ppts, having fallen 13 of the last 16 days after reaching its highest level in over a year earlier in the month.

Oil prices had a significant reaction as well, with Brent Crude falling by about $10/bbl between its intraday high and low just a couple of hours apart, before settling -0.94% lower at $111.42/bbl. And the euro itself strengthened by +0.92% to move just shy of $1.11.

When it comes to the Fed, the added optimism did not do much to alter pricing this year, as it seems markets have already internalised that the Fed is now less inclined to let war get in the way of the hiking cycle. Expectations for a 50bp hike at the May meeting remain high, having oscillated between 65% and 80% since last Monday, finishing yesterday near the upper end of that range at 75%. The only speaker of note was Philadelphia Fed President Harker, who said that he wouldn’t take 50bps off the table for May, but expected “a series of deliberate, methodical hikes as the year continues”. The jobs report on Friday as well as the CPI report on April 12 will be very important ahead of the Fed’s decision in early May.

Asian stock markets are mostly trading in positive territory. The Hang Seng (+1.15%) is up after shares of Chinese tech giant Tencent rose more than +2%. Meanwhile, shares of China Evergrande Group will “remain suspended until further notice” as per yesterday’s announcement by the firm. Chinese stocks opened higher with the Shanghai Composite (+1.28%) and CSI (+1.40%) leading gains across the region. Elsewhere, the Kospi (+0.25%) is trading up, building on gains in the previous session. Bucking the trend is the Nikkei (-1.27%) after giving up its earlier session gains as the Japanese Yen strengthened (~1.0%) against the US Dollar. Data showed that Japan’s retail sales (-0.8% m/m) fell for the third straight month in February, exceeding market expectations for a -0.3% loss and after falling -0.9% last month. Moving on, the S&P 500 (-0.12%), Nasdaq (-0.11%) and DAX (-0.15%) futures are all slightly down.

On the data side yesterday, there were a number of interesting releases from the US, which collectively pointed to inflationary pressures still in the pipeline. In particular, the total number of job openings in February came in at 11.266m (vs. 11m expected), which means that the number of job openings per unemployed moved back up to its second highest ever level, at 1.80 openings per unemployed person. Furthermore, the quits rate also ticked back up to 2.9%, just shy of its record 3.0% back in November and December. Otherwise, the FHFA house price index was up +1.6% in January (vs. +1.2% expected), and that was the fastest monthly gain in 7 months. Meanwhile, the Conference Board’s consumer confidence measure ticked up slightly to 107.2 (vs. 107.0 expected), but there was a growing divergence between the present situation reading, which rose to 153.0, unlike the expectations measure at 76.6, which hit its lowest level since February 2014.

To the day ahead now, and data releases include German CPI for March and Italian PPI for February, whilst in the US there’s the ADP’s report of private payrolls for March and the third estimate of Q4 GDP. Otherwise, central bank speakers include ECB President Lagarde, and the ECB’s Holzmann, Wunsch, Makhlouf and Panetta, along with the Fed’s Barkin and George, and BoE Deputy Governor Broadbent.