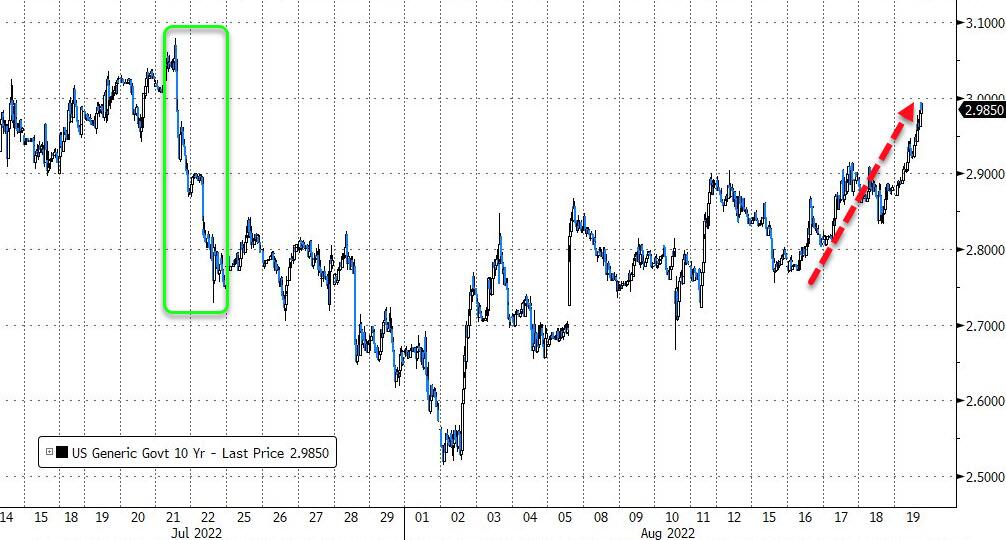

Stocks Extend Losses, Yields Spike After “Recession” Comments From Fed’s Barkin

Federal Reserve Bank of Richmond President Thomas Barkin says “getting inflation under control is going to be necessary to set up what we have the potential to do in the economy.”

Barkin warned that “The Fed must curb inflation even if this causes a recession,” adding that The Fed “needs to raise rates into restrictive territory.”

“I’ve convinced myself that not getting inflation under control is inconsistent with a thriving economy”

Barkin further added that “I’ve been supportive of front-loading.”

The Richmond Fed president’s comments echoe’d ECB’s Schnabel’s words of warning that “even if we entered a recession, it’s quite unlikely that inflationary pressures will abate by themselves,” Schnabel said.

“The growth slowdown is then probably not sufficient to dampen inflation.”

It appears the world’s central bankers are rapidly realizing that a recession is needed to tamp down inflation… and in fact even that may not do the trick – this is a supply issue, not a demand issue.

Translation: we need a depression to ‘fight’ Putin!

This prompted further weakness in stocks with Nasdaq down 2%…

And yields spiking higher with 10Y inching closer to 3.00%…

…erasing all the price gains from the ECB/US-weak-data bond rally.

Is the scene being set for Powell to steal the jam out of the ‘Fed Pivot’ bulls’ donut next week in J-Hole?

Apple Discloses New Security Flaw That Can Allow Attackers To Take “Complete Control” Over iPhones, iPads, & iMacs

Apple has disclosed what are being called “serious” security vulnerabilities with iPhones, iPads and iMacs this week. The vulnerabilities are so significant, they can potentially allow attackers to “take complete control of the devices”, according to Sky.

In a non-descript statement on Thursday, Apple said it was “aware of a report that this issue may have been actively exploited”.

Everyone that owns the affected devices, which include iPhones after the 6S, new iPads and any Mac running OS Monterey, is being encouraged to update their software as soon as possible. The hack even affects some older iPod models. Remember iPods?

Apple said on its website that means a malicious application “may be able to execute arbitrary code with kernel privileges”, which is computer lingo for taking full control over your computer, discovering your Anthony Weiner-style photo collection and (even worse) altering your recipe for chicken francese.

Rachel Tobac, the CEO of SocialProof Security, told The Guardian the flaw gives “full admin access to the device” so that anyone can “execute any code as if they are you, the user”. She said that “activists or journalists who might be the targets of sophisticated nation-state spying” should be the most concerned about the flaw.

A second flaw could be exploited if a vulnerable device accessed or processed “maliciously crafted web content [that] may lead to arbitrary code execution”, according to Sky, citing TechCrunch.

Apple was mum on further details for the time being, but we will continue keeping a close eye on the story.

By Simon White, Bloomberg Markets Live analyst and reporter

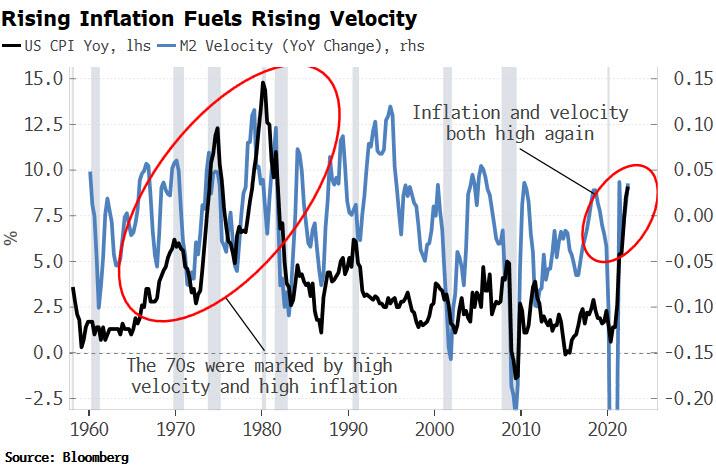

Rising velocity will keep inflation persistently elevated and at risk of becoming unanchored, leaving longer-term yields looking structurally too low.

Central bankers should be careful what they wish for. After years of trying to arrest the fall in the velocity of money, it is finally on the rise again.

Velocity is little talked about these days, but in the first throes of the financial crisis it was the center of attention. Defined here as the ratio of GDP to M2 money, velocity continued to fall no matter what the Fed threw at it in the fevered months and years after the GFC

That’s a major problem when you’re trying to resuscitate demand. Velocity is in essence the average number of times each dollar is spent in the economy, so its inexorable decline meant that, despite the Fed creating trillions of new dollars, total demand was still falling as each dollar was being spent fewer times.

The problem was not causal. Demand was collapsing as households and businesses were in the midst of a major retrenchment in the aftermath of the financial crisis.

Risk appetite was rock-bottom and the main providers of credit to the economy — banks — were pulling back from lending in order to rebuild their balance sheets, or just stay alive. The Fed was running up the down escalator as it created ever more reserves only for them to be hoarded by banks, firms and households.

That’s why the Fed was unable to create sustainable inflation despite expanding its balance sheet to unprecedented levels. But the times they are a-changing.

Velocity is related to rates, and falling rates through much of the 2010s meant it fell too. But now that rates are rising, there is a greater incentive for savers to decrease money balances and hold higher-yielding assets, which means a higher velocity of money. Velocity today is rising faster than it has done since 2010 and is set to keep advancing.

This explains why inflation — even though it is very likely to fall in the coming months — will remain persistently elevated above its long-term average and continue to be susceptible to flaring even higher later in the cycle.

Elevated inflation is the spark that lights the fire, and velocity is what fuels it. Rising velocity without high inflation is not normally a problem, but when inflation also starts rising it creates more demand for money and thus velocity rises, with a feedback loop developing. We are on the cusp of that today.

We can now see how the trillions of dollars of hitherto largely idle reserves at the Fed could rapidly become very inflationary. Prices rise, requiring more money to pay for the rising nominal cost of goods and services. Ultimately this means greater demand for reserves, i.e. the velocity of reserves increases, which soon translates into a rise in the velocity of broader money measures too. More inflation ensues. Wash, rinse, repeat.

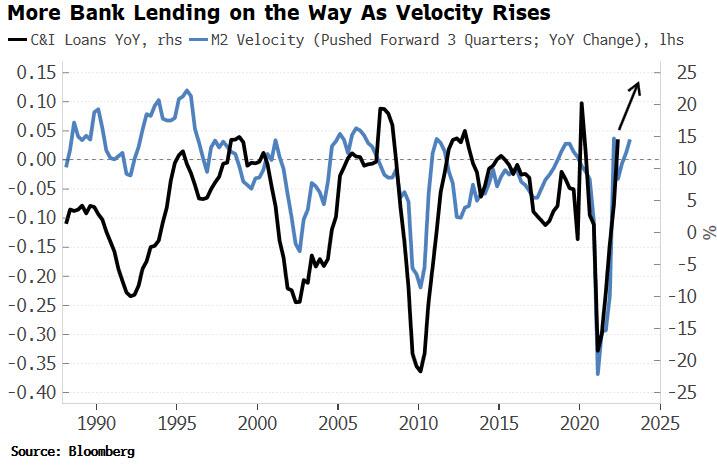

Even people without much money are experiencing an inflationary-driven increase in demand for it, which is manifesting itself through a rise in bank loans. Rising velocity typically precedes accelerating growth in commercial and industrial loans by about three quarters (C&I loans are a good proxy for loans overall given the stringent lending standards generally attached to them).

Demand for C&I loans is also rising, but banks are tightening their standards for such loans. This is unusual as demand for loans normally falls when standards are being tightened, suggesting demand for loans — to cover inflation-driven rises in costs — is overwhelming the tighter loan standards.

More loans means more money, which banks can conjure out of thin air, meaning yet more inflation potential.

QT is an attempt to mitigate the inflationary potential of Fed reserves by curtailing velocity. The reduction in reserves should lead to an even greater fall in demand, meaning velocity should fall.

Rate increases, on the other hand, are supposed to work on the demand channel as they can only affect the price of reserves while leaving the volume unchanged.

QE was supposed to work in reverse to QT, causing velocity to rise as demand increased more than the increase in money. We know it failed to achieve that aim.

If something fails one way, it’s prudent to assume it might not work in the opposite direction either. Rising velocity will keep the inflation embers alive for some time yet.

Erdogan Attempts To Play Peacemaker Between Zelensky & Putin

Turkish President Recep Tayyip Erdogan is trying his hand at being a “peace broker” upon his first visit to Ukraine since the war began. He met with Secretary-General Antonio Guterres and President Volodymr Zelensky in the western Ukrainian city of Lviv, where the Ukrainian leader hailed Erdogan’s visit as a “powerful message of support from such a powerful country.”

High on the agenda in the trilateral talks included expanding the grain export deal which has already seen at least half a dozen vessels navigate the Black Sea safety corridor under the guidance of a joint operations room in Istanbul. This been Turkey’s greatest diplomatic success over the course of the six-month long war so far.

Erdogan also said he discussed possible scenarios of ending the war between Ukraine and Russia, though without offering specifics, and it appears little progress in this area was made in terms of potential future proposals that could be offered Russia (which itself seems little interested in ending its offensive until all “objectives are met”). However, rumors are persisting – not for the first time though – that there are concrete proposals in the works.

Erdogan described that the leaders “discussed the exchange of prisoners of war between Ukraine and Russia, and that he would later raise the issue with Russian President Vladimir Putin.” So it seems Erdogan is touting is status as a past “go between” of sorts with Putin and the West.

“We attach great importance to this issue…of what happened to the exchange of these captives,” Erdogan told reporters in Lviv.

The ongoing standoff at the Zaporizhzhia nuclear power plant was also under intense discussion, with the dangerous situation among the first issues raised at an initial press briefing soon after Erdogan’s arrival.

Zelensky urged for the United Nations to ensure safety and security at Zaporizhzhia, also while demanding for the IAEA to be allowed access – a request which it appears so far the Kremlin has rejected.

Turkish President Recep Tayyip Erdoğan met with Ukrainian President Volodymyr Zelensky in Lviv on Thursday to discuss ways to expand grain exports in Ukraine. pic.twitter.com/DvnVjgpPVu

“Erdogan is known to have a certain influence with Putin, and I think Zelensky and Guterres will explore with Erdogan possible formulas for defusing the situation at the Zaporizhzhia nuclear plant,” a France24 Turkey correspondent observed.

“We do not want to experience a new Chernobyl,” Turkish President Recep Tayyip Erdogan tells reporters after his meeting with President Volodymyr Zelenskyy and U.N. Secretary-General Antonio Guterres in the Ukrainian city of Lviv. Erdogan was voicing his concern about the clashes around the Russian-occupied Zaporizhzhia nuclear power plant.

Gutteres echoes Erdogan’s warning, saying that “any potential damage to Zaporizhzhia is suicide.”

Rumors that Pres. Erdogan 🇹🇷 has arrived today to Lviv 🇺🇦 with a peace plan, already accepted by🇷🇺, to discuss with Zelensky 🇺🇦.

The fact that Zelensky drove for 7 hours (seen in video) to meet Erdogan, says a lot. Zelensky doesn’t go to Kyiv train station to meet arriving VIPs. pic.twitter.com/i5kpko3xBC

Both the Russian and Ukrainian sides continue to accuse the other of jeopardizing the safety of the power plant, with Moscow saying Ukraine forces are repeatedly shelling the complex. On Thursday each also said the other is planning a “false flag provocation”. The Kremlin has even specified it’s belief that some kind of provocation or significant incident will happen on Friday (8/19).

I cannot remember a time when I’ve had so many interesting discussions with so many smart people where there is so little overall agreement. We all agree on some things and are in complete disagreement on other things. That in itself is unusual, as narratives are generally more coherent and consistent than that. Even stranger is that what we agree and disagree on is all over the map. It’s like a bad Rorschach Test.

Not only am I trying to refine and update my view (as well as second guess myself on all of my views), but I’m also really trying to figure out how so many people that I respect and listen to are so all over the map.

Which brings me to the “Town Car vs NYC Cab” analogy.

Town Car vs NYC Cab

When you order a town car (or even an upscale Uber), you have certain expectations. Timely arrival. Probably clean. Air conditioned. Likely a fast (they are paid by the trip), but reasonably smooth ride.

When you get into a NYC cab, you hope for clean, but know there may only be a slight chance of that. If it is a hot day and the windows are up, you have at least the possibility of air conditioning (I would avoid taxis with rolled down windows on hot days, because there is almost no good explanation for that, and lots of bad ones).

From there, it is all about the ride, but more often than not, you are going to get some version of hit the gas, slam the brakes, hit the gas, swerve, brake hard, pedal to the metal, jerk the wheel, brake hard, swear at pedestrians, gas it into a yellow light, only to decide at the last minute to come to a screeching halt. It isn’t as bad as the occasional time you get a driver who uses both feet, but it’s pretty bad and pretty standard.

Right now, there are those of us who are analyzing the economy as though it is a town car and others who are viewing it as a NYC cab ride.

I don’t know which one is correct. I’m in the NYC cab camp, but it is important to understand what this analogy means for analysts and their outlooks.

Models, rate of change, historical comparisons.

For those sitting in the town car, models are extremely valid. Rates of change follow patterns and the data is expected to be “smooth” over time. There is a lot that can be learned from history since the same models, smoothness, and reaction functions exist. This can range from outlooks on jobs (optimistic), inflation (fears about the ability to lower it), and recession odds.

NYC cab riders are lurching about. The ability to get large jumps and rapid directional changes is part of the thought process. Record drops in NY State manufacturing aren’t surprising. Ongoing strength in jobs is surprising. Inflation could jump to 10% or we could be discussing deflation by the end of the year (I’m more concerned about this than I am about runaway inflation). History isn’t as applicable because the starting conditions have never been like this. Massive stimulus, supply shocks, etc., don’t lend themselves well to following historical patterns. We’ve never had significant QT and that is about to start.

Past actions have worked versus past actions keep priming the pump.

Some of this is redundant with the prior bullet point, but those riding in the town car tend to believe that prior policy was largely good. It promotes a faith in policy, which does make it easier to lean on traditional models and historical examples.

Those of us stuck in NYC cab mode see us lurching from one crisis to the next. We put on the gas, slam on the brakes, and hope for the best. For some, this balances out, and we get to the destination in one piece and in a timely fashion. For others, we can’t help but see a series of crises, where each “new” crisis follows the prior “crisis” more closely. The cycles of highs and lows are accelerating. We are basically cringing in the back seat waiting for the brakes to fail, for a tire to pop when it hits a curb, or to rear-end someone and be stuck dealing with that mess (probably too pessimistic, but it does appeal to me).

Continuous versus dislocated. Differential versus non-differential.

This is more at the extreme of both sides, but are there “triggers” that once pulled, cannot easily be fixed? Do economies and people behave in smooth, continuous patterns, which can be adjusted easily? Or are they lurching about, creating the risk of something altering course so much that it is difficult to get back to “normal”? The U.S. blocking Russia’s Central Bank from accessing their dollars may have been a necessary step in what we were doing to attempt to hurt Russia, but I don’t think any country that doesn’t behave like we would want them to will forget that action. It changes things in a way that makes it difficult to go back. If everything continues, we can nudge things along and correct things sooner rather than later. If things have the ability to “jump” and be dislocated, the effects of policy mistakes are that much greater and more difficult to fix. I think the time it took for the last stimulus bill to get approved was problematic – had it been done in February 2020, it made sense, but by the time it got passed, the “problems” it was fixing had largely dissipated.

Once I started thinking about it from this perspective, the arguments started making a lot more sense. It has become much easier for me to start to understand the views more clearly. I don’t necessarily agree with others (nor they with me), but at least I’m seeing how we might be getting there within our own logical frameworks.

Town car strategists will have smoother data and expect longer cycles. Policy will tend to work as expected in their models. Surprises are rare and are more “one-off” than indicative of anything major occurring.

NYC cab strategists are looking for faster shifts in the data. U-turns are possible. Traditional policies don’t work as smoothly as projected, and unusual policies (like QT) create unexpected problems.

I know I’ve drifted into the NYC cab side of the spectrum (anyone who has driven with me would probably agree that this is both figurative and literal). That concerns me and I may have to re-think that, but I’m stuck on a few things:

Wealth destruction, especially in crypto and disruptive companies, is going to hit the economy faster than “traditional” models predict because these things didn’t exist in prior times. Add in the evidence of a slowing housing market and we have a negative wealth effect that I think is unlike others we’ve seen.

Inventory build. I see inventory build as sowing the seeds for deflation. Not only will pricing power diminish, but manufacturing will slow. Chinese exports have slowed and I’m told by some that it is because of production problems. For me, it seems to fit the narrative that we’ve overbought and need to cut back, so manufacturing (globally) will be hurt. This inventory build is occurring in the midst of wealth destruction and rate hikes. However, maybe I’m too negative on this and things will take much longer to play out than I suspect.

Monetary Policy Fixes Everything. This probably scares me the most. It is one reason why (for the past few weeks) I’ve been advocating for buying puts and calls because it has become accepted wisdom. The “bad news” is “good” can only last so long (I think). When you go back to the GFC, monetary policy was quick to respond, yet it didn’t stop the overall decline in markets until almost two years after the policies were enacted. Yes, there were some strong rallies between the summer of 2007 and 2009, but it took a long time to bottom. Yes, the central bankers have learned to act faster and more aggressively (like they did when COVID hit), which is good, but is it sufficient?

Bottom Line

I have no idea which side is right, but I’ve found that since I started to think about people as being in town cars vs NYC cabs, I’m having a better time understanding their views, which is a big step towards making me smarter and understanding all the possible scenarios better.

In the meantime, may all your cabs, Ubers, and Lyfts be clean, air-conditioned, and with safe drivers!

Shortly before the 2016 election, Mike Pence tweeted that “@realDonaldTrump and I commend the FBI for reopening an investigation into (Hillary) Clinton’s personal server because no one is above the law.” And who can forget the GOP crowds chanting “lock her up” in regard to Clinton—a sentiment Trump supported?

I had no problem with the email investigation provided a judge had authorized it and it conformed to legal standards. Truly, no one—not even a potential or actual president—should be above the law. However, the “lock her up” mantra, which pro-Trump crowds directed at other Democrats including Michigan Gov. Gretchen Whitmer, gave me the creeps.

In banana republics, the new despot tries to lock up the old strongman and rounds up his vanquished supporters. Even accounting for emotions that politicians drum up at rallies, that line was appalling. Americans should never cheer the idea of turning federal law enforcement—whatever its many current flaws and abuses—into a version of the Praetorian Guard.

Last week’s big news is the FBI had executed a search warrant at Trump’s Mar-a-Lago estate, as it conducts an investigation into the alleged mishandling of classified documents. The former president and his minions have been all over the media describing the investigation as a political witch-hunt—a concept that, apparently, they no longer find to be entertaining.

“My beautiful home, Mar-A-Lago in Palm Beach, Florida, is currently under siege, raided, and occupied by a large group of FBI agents,” the former president said in a statement. Some of his most-agitated supporters are openly calling for civil war. They are blasting the FBI’s “tyranny.” Suddenly, people who seemed eager to sic federal agents on their political opponents are aghast that the FBI would conduct an investigation of one of their own.

Some conservative rhetoric would be laughable if it weren’t so dangerous. One popular podcaster, Steven Crowder, warned liberals: “(Y)ou think they’re not gonna come for you?” He didn’t seem concerned about turning the U.S. into a third-world hellhole: “I don’t care if we become Nicaragua at this point. You’ve already rung the bell, you can’t un-ring it.”

But the strangest response, from Rep. Marjorie Taylor Greene (R–Ga.) was to “defund the FBI.” The anti-Trump conservative website, The Bulwark, collected assorted tweets and statements from prominent Republican members of Congress and commentators who had savaged leftists for their “defund the police” rhetoric during anti-police-abuse protests—but who now are echoing Greene’s ideas.

“Man Shot in Downtown Memphis Just Off Beale Street. This is What Happens When You Elect ‘Defund the Police’ Democrats,” tweeted conservative columnist Todd Starnes in June. This week he had a somewhat different hot take: “The FBI has been weaponized. Defund and Dismantle.”

Fox News’ Dan Bognino called for widespread firings and accountability at the bureau: “I don’t buy this rank and file crap either. Throw it right in the garbage. I don’t buy it one bit. I was a Secret Service agent, and I was the rank-and-file. Me. And you know what? I saw something I didn’t like, and I left.” At this point, I should start cheering. Conservatives finally are echoing points that my fellow criminal-justice reformers have long made.

Police agencies absolutely need reform. Police unions protect bad actors. District attorneys rarely prosecute those officers even for egregious conduct. Fired cops simply get jobs at other agencies. The “thin blue line” mentality prods officers to follow orders rather than hold misbehaving colleagues accountable—as evidenced by the failure of Derek Chauvin’s three colleagues to intervene during George Floyd’s death.

Instead of walking away when their agencies carry out unconstitutional raids or abuse the power of asset forfeiture to confiscate property, police typically go along without complaint. But instead of proposing serious reforms, some progressives trotted out their “defund the police” mantra, which allowed conservatives to easily depict them as advocates for lawlessness.

It was one of the dumbest political mantras I’ve ever heard, but it was based very loosely on a sound idea. Why shouldn’t Americans use the public purse strings to force police departments to improve their operations? When government agencies abuse our constitutional rights, they will do so even more zealously if we give them more money. Ditto for federal police agencies.

Now, suddenly, the Right seems to believe progressives were right—it only took the FBI to target their beloved ex-president to open their eyes. It remains to be seen whether the raid on Trump’s estate is an abuse of power, but the FBI has a history of misusing authority. (So does the IRS, which is poised to receive a huge cash infusion.)

Frankly, it’s hard to believe conservatives who wanted to lock up their political opponents and opposed police-accountability measures are acting out of principle rather than partisanship. Their opponents on the Left are no better, but perhaps this could be a teachable moment for everyone.

This column was first published in The Orange County Register.

In 2005, President George W. Bush signed into law the Protection of Lawful Commerce in Arms Act (PLCAA), a statute designed to protect gun makers, dealers, distributors, and importers from being sued “for the harm caused by the misuse of firearms by third parties, including criminals.”

“Our laws should punish criminals who use guns to commit crimes,” Bush declared, “not law-abiding manufacturers of lawful products.” The law’s passage was widely seen as a victory for the gun rights movement. But a new case out of Pennsylvania now asks whether the same law should be shot down for violating bedrock constitutional principles of federalism.

The case is Gustafson v. Springfield, Inc. It centers on the tragic death of a 13-year-old boy who was accidentally shot and killed by his friend. The friend falsely believed that the semiautomatic handgun he was holding was unloaded because the magazine had been removed. In fact, one round was still chambered.

The dead boy’s family sued the gunmaker in state court. But the Court of Common Pleas of Westmoreland County said the lawsuit was barred by the terms of the PLCAA, which preempts state tort law in this area. In a decision issued last week, however, a majority of the Superior Court of Pennsylvania not only reversed that ruling but also held that the PLCAA itself is unconstitutional.

“I recognize that state courts do not typically resolve claims involving the constitutionality of federal statutes,” wrote Judge Deborah Kunselman. “However, that is the issue presented by the facts of the case before us. The Gustafsons filed a product-liability lawsuit under Pennsylvania common law, which, but for a federal statute, would have proceeded through our state courts like every other civil action. When their claims were abruptly dismissed under PLCAA, the question of that federal law’s constitutionality fell squarely before us, and we must answer it.”

The court’s answer was that the PLCAA must fall. “Tort law is a decidedly state issue,” Kunselman argued. “If courts allow Congress to regulate tort litigation involving these products, it could eventually regulate all litigation. This is not permitted under the Constitution of the United States’ principles of federalism. As such,” she concluded, the PLCAA “violates the Tenth Amendment.”

Writing in dissent, Judge Judith Ference Olson charged the majority with missing the relevant constitutional provisions at play. “Congress had the express authority to enact PLCAA under its enumerated powers granted by the Commerce Clause to regulate interstate and foreign commerce,” Olson argued. “Thus, the only way PLCAA could violate the Tenth Amendment is if the Act commands state legislatures to enact a particular law or state executives to administer a federal law. PLCAA does neither.”

This is a case worth watching. For one thing, the Superior Court of Pennsylvania is not likely to have the last word on the matter. Eventually, this dispute will land in federal court. There is also the unusual political angle. As the case moves forward, gun control advocates—who would love to see firearms manufacturers face more product-liability lawsuits—will be embracing the sort of 10th Amendment arguments more commonly voiced by conservatives and libertarians. There’s something here for practically everyone to argue about.

If a cryptocurrency like bitcoin were to become a commonly accepted medium of exchange—a global decentralized monetary system that no third party can stop or control—would the U.S. government attempt to make it illegal and prosecute the developers who contribute to its code base? Is software protected by the First Amendment? Will the government one day prosecute individuals who design 3D-printed guns and then make their plans downloadable on the internet? Last week brought cause for alarm that a federal crackdown on the decentralized, open-source software movement might be coming.

In the past, the U.S. government has pursued financial services companies like cryptocurrency exchanges, holding them criminally liable for mishandling other people’s money or for facilitating international payments without following Know Your Customer and other regulations.

But what happened on August 8 was different: The U.S. Treasury Department announced that its Office of Foreign Assets Control (OFAC) was adding Tornado Cash, an Ethereum-based tool for making cryptocurrency transactions anonymous, to the U.S. sanctions list. Dutch authorities arrested a suspected developer of Tornado Cash, accusing him of facilitating the laundering of billions in stolen funds.

What’s he guilty of? Writing code and making it free on the internet.

What triggered the U.S. crackdown on Tornado Cash was the allegation that North Korean hacking collective the Lazarus Group used Tornado Cash in an attempt to disguise a cryptocurrency payment worth about $455 million to North Korea’s missile program.

The Treasury Department’s action is reminiscent of the case against the software developer Phil Zimmerman, who developed and distributed software known as PGP in the early 1990s. PGP was the first widely accessible tool for sending messages over the internet with powerful encryption.

Zimmerman became the target of a three-year federal investigation on the grounds that his software was so powerful that making it possible for foreigners to download it online was the equivalent of distributing weapons to foreign countries without permission from the state department. The government ultimately dropped the investigation thanks in part to free speech activists who printed the entire PGP source code in a book published by MIT Press and sold it abroad to make the point that its creation was a form of writing protected by the First Amendment, just like any other book.

Zimmerman’s legal battle was part of what’s known as the crypto wars, which refers to the ongoing battle to keep powerful cryptography legal. The sanctioning of Tornado Cash is the latest chapter in that struggle. To better understand its implications, I reached out to attorney Jerry Brito, who’s the executive director of Coin Center, a nonprofit focused on policy issues and regulations facing bitcoin and other cryptocurrencies.

“What’s been sanctioned here is not a person. There’s a sanction on a tool. And so the sanction really is on millions of Americans who otherwise might want to use that tool for completely lawful purposes,” says Brito.

Watch the full video above.

Produced by Zach Weissmueller; edited by Danielle Thompson. graphics by Isaac Reese, Jim Epstein, and Thompson.

Photo credits: Yichuan Cao/Sipa USA/Newscom; joan slatkin; CNP/AdMedia/Newscom; Liu Jie / Xinhua News Agency/Newscom

One Market Indicator With A Perfect Track Record Says Stocks Have Bottomed… Another Says They Are About To Plunge Again

Just when you thought markets have reached peak schizophrenia – not helped by the fact that the Fed wants to have it both ways, and “on the one hand calling inflation unacceptably high and inflationary pressures broad-based, while on the other they hinting at slowing the pace of rate hikes, thus allowing financial conditions to ease, well before there is any real evidence of a meaningful move back towards there 2% target thus leaving the market confused as to whether the Fed is likely to continue to raise rates well into 2023” – we now have a Heisenberg state for markets where one flawless, 100% accurate indicator suggests i) the market is set to to tumble and hit a new bottom, while according to another ii) stocks have already bottomed and will now soar.

In other words, we are about to see at least one of two “guaranteed”, 100% correct indicators be wrong for the first time.

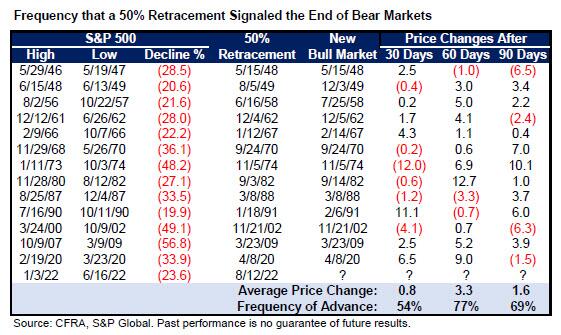

Why? Consider the following: last Thursday we first pointed out that 4220 is critical level for S&P futures: it’s the 50% Fib ES retracement. A close above it would void the bear market rally thesis as there has never been a bear market rally that exceeded the 50% fib and went on to make new cycle lows

4220 is critical level: it’s the 50% Fib ES retracement. A close above it would void the bear market rally thesis as there has never been a bear market rally that exceeded the 50% fib and went on to make new cycle lows pic.twitter.com/dZlXMi1fXG

Yesterday, CFRA’s Sam Stovall echoed what we said when it pointed out that “the S&P 500 Index closed above 4,232 on Friday, a 50% retracement of the plunge from its Jan. 3 closing high to its June 16 low. For traders who closely follow Fibonacci analysis, finishing above this level implies a bottom has already been set.”

To sound (or seem) original, CFRA showed a table confirming what we first said, namely that the S&P has never set a lower low in any of the 13 post-World War II bear markets after recovering 50% of its peak-to-trough decline. As a result, Stovall told clients that while markets may be taking a breather, investors should “look upon any possible decline as a dip that should be bought since history says the low is already in.”

So we’ve bottomed then? Well, no… not so fast, because according to another “flawless” indicator, the bottom has yet to come.

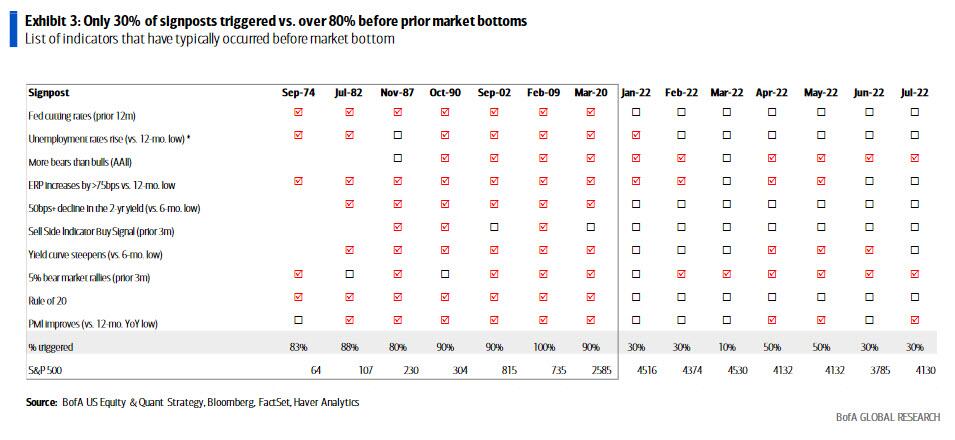

As BofA’s Savita Subramanian writes in a market note this morning (available to pro subscribers), only 30% of the bank’s bull market signposts (things that happen before a market bottom) have been triggered vs. 80%+ in prior market bottoms, suggesting that another pullback is likely.

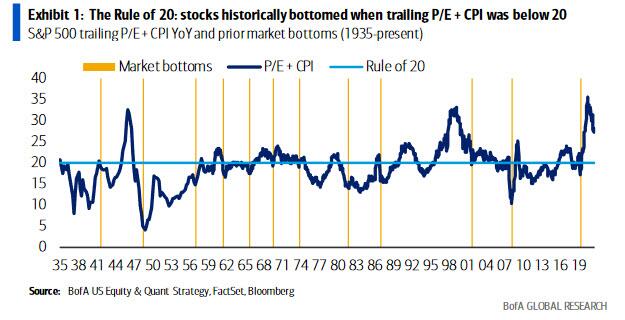

But more to the point, according to Savita, one signpost with a perfect track record is the Rule of 20, i.e., the sum of CPI y/y + trailing P/E has always been lower than 20 when the market bottomed.

What does this mean? Well, outside of inflation falling to 0%, or the S&P 500 falling to 2500, an earnings surprise of 50% would be required to satisfy the Rule of 20, while consensus is forecasting an aggressive and “unachievable” 8% growth rate in 2023 already.

In short, we have reached a perfect quantum state of a market based on flawless backward looking indicators, where one “100% accurate” market signpost predicts stocks melt up from here (or at worst, suffer a modest drop), while another sees stocks tumbling as much as 2,500 if not lower to a new, and far more painful low.

One of the two will see their perfect predictive track record crushed forever.

By Hal Press, founder of North Rock Digital, first published in Bankless

What’s Up With The Merge?

As we approach the Merge, we wanted to provide a write-up on how we are thinking about the Ethereum ecosystem and specifically Merge-related investments.

This is meant as a follow-up to the prior article we wrote on Ethereum, which can be found here.

Since I published the original article in January much has transpired, some assumptions have changed and the outlook for the future has been altered. Despite this, the core thesis remains, Ethereum is set to undergo the largest structural shift in the history of crypto. Back in January, the path to the Merge was extremely uncertain. Now, that path has crystalized.

The final testnet, Goerli, was recently completed successfully and a Mainnet target date has been set for Sep 15/16.

So where do we stand?

The Biggest Structural Shift in Crypto History

Regarding the Merge the thesis has not changed, Ethereum is set to undergo a massive structural shift as expenses will effectively be reduced to zero.

The shift will give rise to the first large-scale structural demand asset in crypto history. As we have stated in our core thesis many times, this paper will address what has changed and new topics not discussed in the prior article. First, it is useful to highlight aspects of the core Ethereum model to get a sense of some of the key fundamentals such as supply reduction and the post-Merge staking rate.

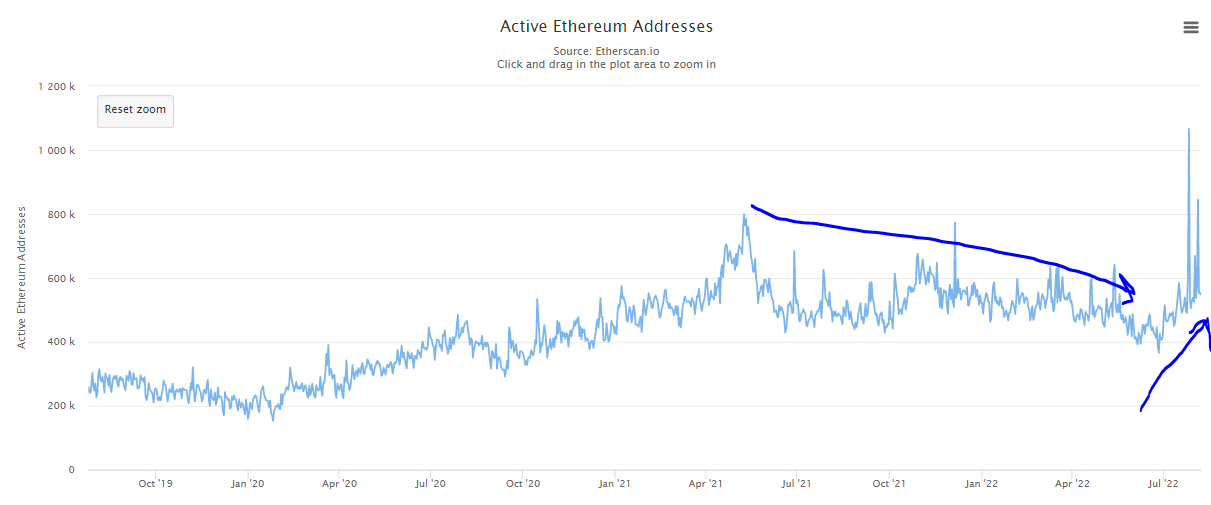

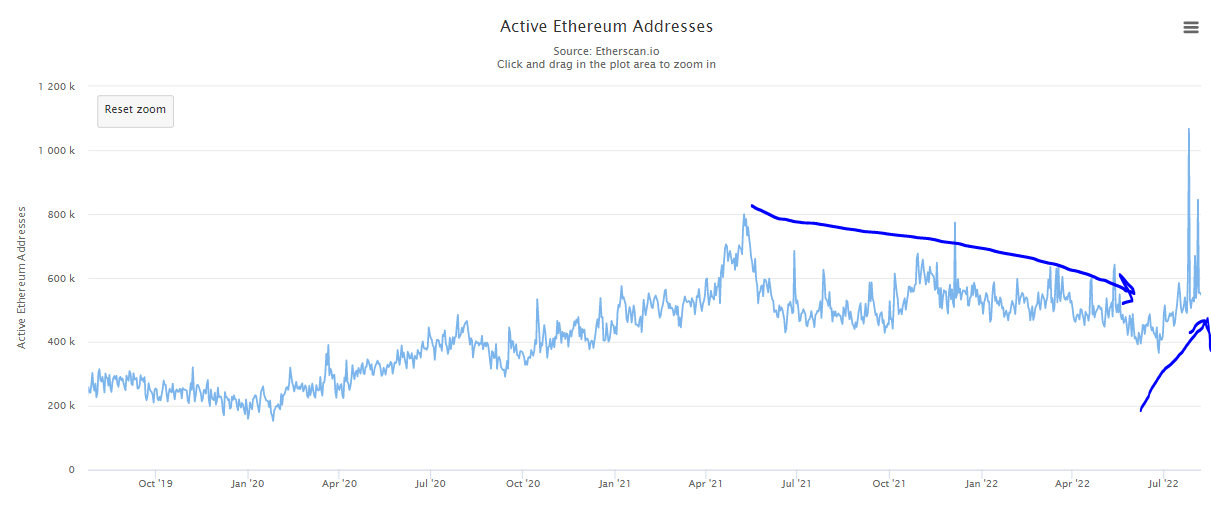

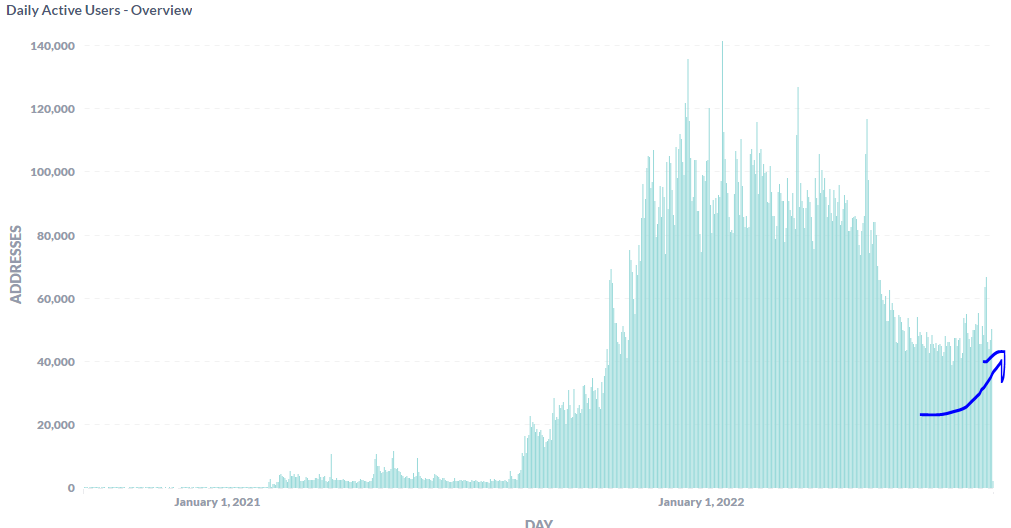

The largest shift since last December is that ETH-denominated fees have fallen significantly. However, there is an interesting dynamic at play here. Although fees have declined, active users have experienced a steady uptrend since late June.

This may seem inconsistent as more users should lead to higher gas. However, we believe this dynamic is caused by recent efficiency optimizations of various popular Ethereum applications. The best and most significant example is Opensea, which in migrating Seaport (from Wyvern) increased gas efficiency by 35%. This has led to a reduction in gas that doesn’t correlate to a decline in activity.

In fact, multiple indicators suggest that despite the low gas readings activity has been increasing recently (more on the specifics here later). This raises an interesting question: what is the optimal fee run rate for Ethereum? Higher fees mean more ETH is burned and post-Merge also correlates to a higher staking rate, but these higher fees also limit adoption.

As we saw in ’21, when fees are too high, some users get pushed to other L1 ecosystems. After roll-ups scale appropriately, Ethereum should be able to achieve both high fees and continued adoption. In the current environment though, it is interesting to think about the optimal mix. We believe the optimal point is approximately the point at which fees are high enough to burn all new issuance. This will enable ETH supply to be stable while also keeping fees low enough not to inhibit adoption. Interestingly, of late, fees have found an equilibrium near this point. Lower fees also seem to be having a positive impact on adoption as active users have begun to increase after a long downtrend.

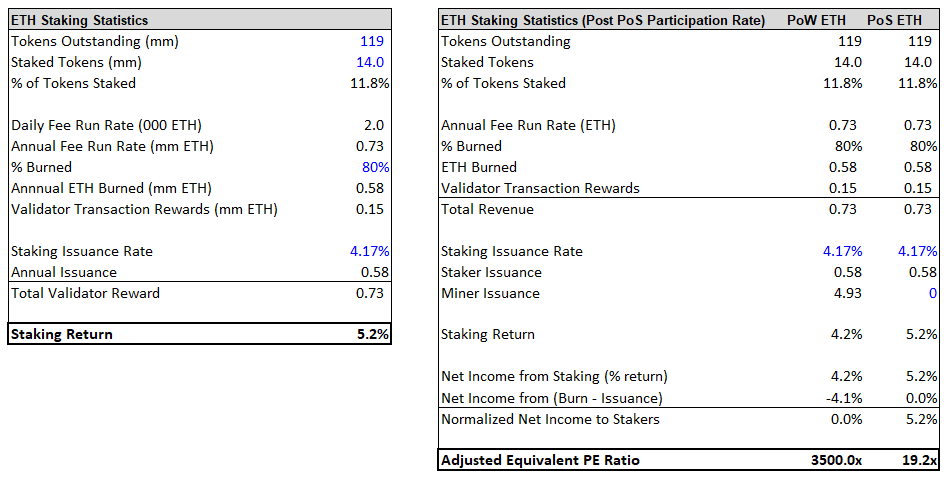

Despite the fact that we seem to be near an optimal fee run rate, the reduced fees do negatively impact various model outputs. This impact is not critical as at the current run rate the burn would still be still large enough for ETH to be slightly deflationary post-Merge. Importantly, the current run rate would continue to drive structural demand as the majority of issuance is unlikely to be sold, while fees that are used must be purchased off the open market.

The staking rate will increase post-Merge by ~100 bps from 4.2% to 5.2%. However, this does not properly illustrate the true impact. To fully appreciate the shift, we must evaluate the real yield rather than the nominal yield. While the current nominal yield is ~4.2%, the real yield is close to zero, as 4.4% of new ETH is issued every year. In this context, the real yield is currently ~0% but will increase to ~5% post-Merge. This is an enormous shift and will create the highest real yield in crypto by a large margin. The only other comparable yield is BNB with a 1% real yield. ETH’s 5% yield will be a market-leading figure. What is the significance of this yield?

Stakers will receive a net ~5% rate, which equates to 100/5= ~20x earnings. This multiple is considerably cheaper than the revenue multiple because the staking participation rate is quite low, meaning stakers receive an outsized share of total rewards. This is one of the key advantages of ETH from an investment standpoint.

As there are so many other uses for ETH, throughout the crypto ecosystem, most ETH ends up locked in those applications rather than staked. This in turn allows stakers to receive an outsized real yield.

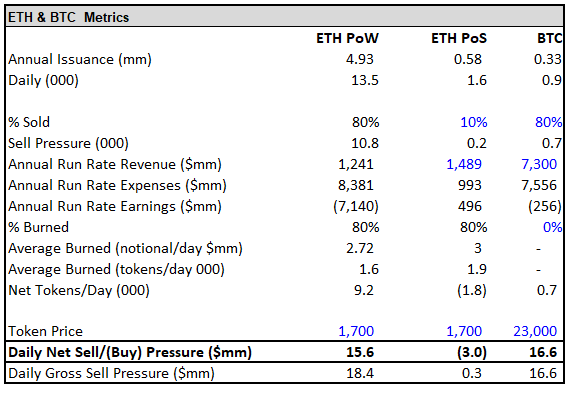

In terms of the flows, ETH will transition from enduring structural outflows of ~$18mm/day to structural inflows of ~$0.3mm/day. While the demand side of the flow equation has softened, the complete reduction of the supply side remains the most important variable. Our estimate for the ETH-denominated supply reduction is actually larger than it was previously. This is due to the fact that the price declines from the highs have not been accompanied by a corresponding hash rate reduction. As a result, miner profitability has decreased dramatically, and they are likely selling close to 100% of mined ETH.

For calculation’s sake, I have assumed 80% of miner issuance is being sold. In this context, ETH has found an equilibrium in which miners sell roughly 10.8k ETH ($18mm USD) per day. Given that fees have been averaging ~$2mm this yields a net outflow of ~$16mm. Post Merge this sell pressure will reduce to zero, and it is projected that there will be a structural inflow of ~$0.3mm/day post-Merge.

To conclude, while many of the numbers have shifted meaningfully in the last eight months, the conclusion remains roughly the same, ETH will shift from requiring ~$18mm of new money entering the asset to keep the price from declining to requiring ~$0.3mm exiting to keep the price from increasing.

To summarize, the staking rate and structural demand are lower than they were 6 months ago. However, this is to be expected in a period of slower activity, and if activity continues to rebound these rates will increase. The primary investment case remains the same, there is an enormous opportunity to front-run the largest structural shift in the history of crypto.

Another point that I think is often overlooked here is that the Merge is more than a shift in supply and demand. It is also a massive fundamental upgrade for Ethereum as the network becomes much more efficient and secure in many ways. This is part of what differentiates the Merge from prior BTC halvings.

It is 3x as large of a supply reduction combined with a massive improvement in fundamentals compared to a decline in fundamentals in the case of BTC halvings (reduced security).

Finally, there are two additional dynamics worth discussing.

1. Time Harvesting

Before addressing how this relates to ETH it is important to lay some contextual groundwork.

Why is it that the SPX (or virtually any US/Global equity index) has been such a profitable and consistent investment vehicle over the long term? Most people think this dynamic has been driven almost entirely by earnings growth and multiple expansion. They would posit that if growth slows or the multiple stops expanding these investments would be unlikely to have positive returns going forward. This is incorrect.

The primary and most reliable source of growth for the price of these indices has been the passage of time.

Here is an example to illustrate this somewhat unintuitive point. A lemonade stand, LEMON (LEMON = The Enterprise, $LEMON = LEMON shares), earns $1 each year. There are 10 shares of $LEMON outstanding. LEMON has no cash or debt on its balance sheet. The market currently values $1 of ex-growth equity earnings at a 10x multiple. What is LEMON worth today? What about each share of $LEMON?

If we assume that next year LEMON will continue to earn $1 annually while the market applies the same multiple, what will LEMON/$LEMON be worth in a year? Take a minute and come to an answer.

If you answered $10/$1 for the first pair of questions you are correct. If you answered $10/$1 for the second pair, you are not. For part 1, LEMON is worth $10 as the market applies a 10x multiple to its $1 of earnings and assigns 0 value to its balance sheet. For part 2, the market continues to apply a 10x multiple to the $1 of earnings, but importantly, it also assigns $1 to the $1 of cash that now sits on LEMON’s balance sheet. LEMON is now worth $11 and each share is worth $1.10. When companies earn money, the money doesn’t disappear, it flows to the company’s balance sheet and the value of it accrues to the owners of the business (the equity holders). $LEMON has appreciated 10% in a year due to the earnings they have generated, despite 0 growth and 0 multiple expansion.

This is the power of earnings yield paired with the passage of time.

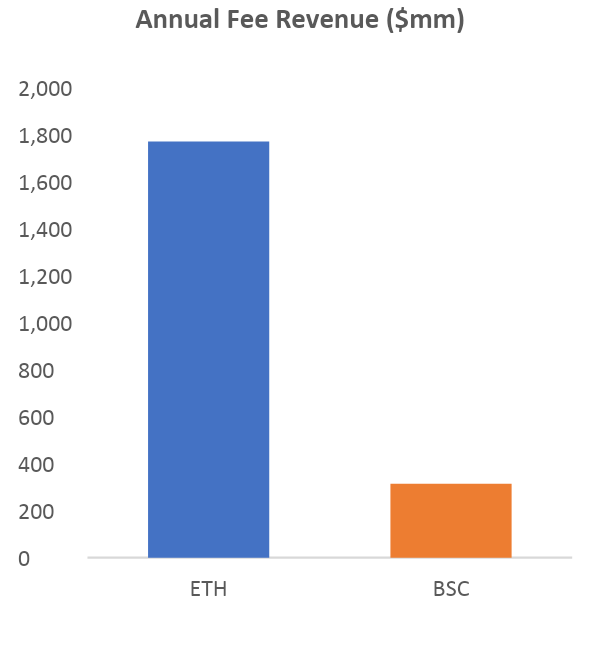

Crypto hasn’t benefited from this dynamic at all. In fact, crypto actually suffers from the reverse effect. Since almost all crypto projects’ expenses are greater than their revenues, they must dilute their holders to generate the funds necessary to cover their negative net income. As a result, unless earnings grow or their multiple expands, the price of each individual token will decline. The most notable exception I can think of is BNB, which is the sole current L1 to generate more revenue than expenses.

It is no surprise the chart of BNB/BTC is essentially up only and recently broke an ATH.

ETH will enter this exclusive class the moment it transitions to PoS. Post-merge ETH will generate a real yield of approximately 5%. This yield will be very different from virtually every other (non-BNB) L1 where the staking yield simply comes from inflation that offsets the yield. All else equal ETH holders will earn 5% each year. Time will become a tailwind rather than the headwind it is for 99.9% of other projects.

This will also change the psychology of holders and incentivize a stronger long-term buy and hold approach, effectively locking up more illiquid supply. Additionally, the “real yield” thesis and the fact that ETH will be the first large-scale real yield crypto asset will be particularly appealing to many institutions and should help accelerate institutional adoption.

2. The Wall of Worry

Throughout the last few months, investors have been extremely skeptical about technical risks, edge cases, and timing risks.

The latest edge case that has generated attention is the potential for PoW forks of Ethereum that live on after the Merge. Some PoW maximalists (miners etc.) would prefer to use PoW ETH and think that a forked version of the current ETH is superior to ETC, which already exists as a PoW alternative. We do not believe there is much value in the fork, but our opinion on this matter is not particularly relevant.

The important point is that this fork will have no impact on post-Merge PoS ETH. All of the potential risks are either easily managed or not risks in the first place. For example, replay attacks will most probably not be an issue as the PoW chain is unlikely to use the same chain ID. Furthermore, even if they maliciously choose to use the same chain ID, this can be managed by either not interacting with the PoW chain or first sending the assets to a splitter contract.

Finally, even if a user does get replay attacked, it will only impact that individual user’s assets and not the overall health of the chain. What the PoW fork does do is provide a dividend to ETH holders, further adding to the value of the Merge. If the fork has any value, ETH holders will be able to send it to an exchange and sell it for additional capital, much of which will then be recycled back into PoS ETH. While we view this as a positive for the Merge-related investment case, many are worried about the potential risks and a litany of other edge cases. We have weighed each risk and concluded the upside far outweighs the downside.

Nonetheless, these concerns are keeping many long-term believers sidelined.

As we approach the Merge many of these issues will be addressed. Eventually, many of these skeptics will be converted, creating fueling continued inflows as we approach the event and culminating with a large set of buyers who will purchase ETH the day the Merge occurs successfully. This should help offset any “sell the news” dynamic.

Just last month, less than 1/3 of people thought the Merge would occur before October. Now the date has been confirmed for mid-September and still, the market is only pricing in two-thirds chance of it occurring before October.

Given this backdrop how should we expect prices to move as we approach the Merge? This is the central question.

First, we acknowledge the reality that macro will continue to have a large impact on absolute price levels despite the Merge. However, it is still reasonable to think through how Merge related alpha will evolve over the coming weeks. In our opinion, the path gets harder to predict the further out you look but then at some point when you’ve gone far enough it starts to become easier again.

Short-Term

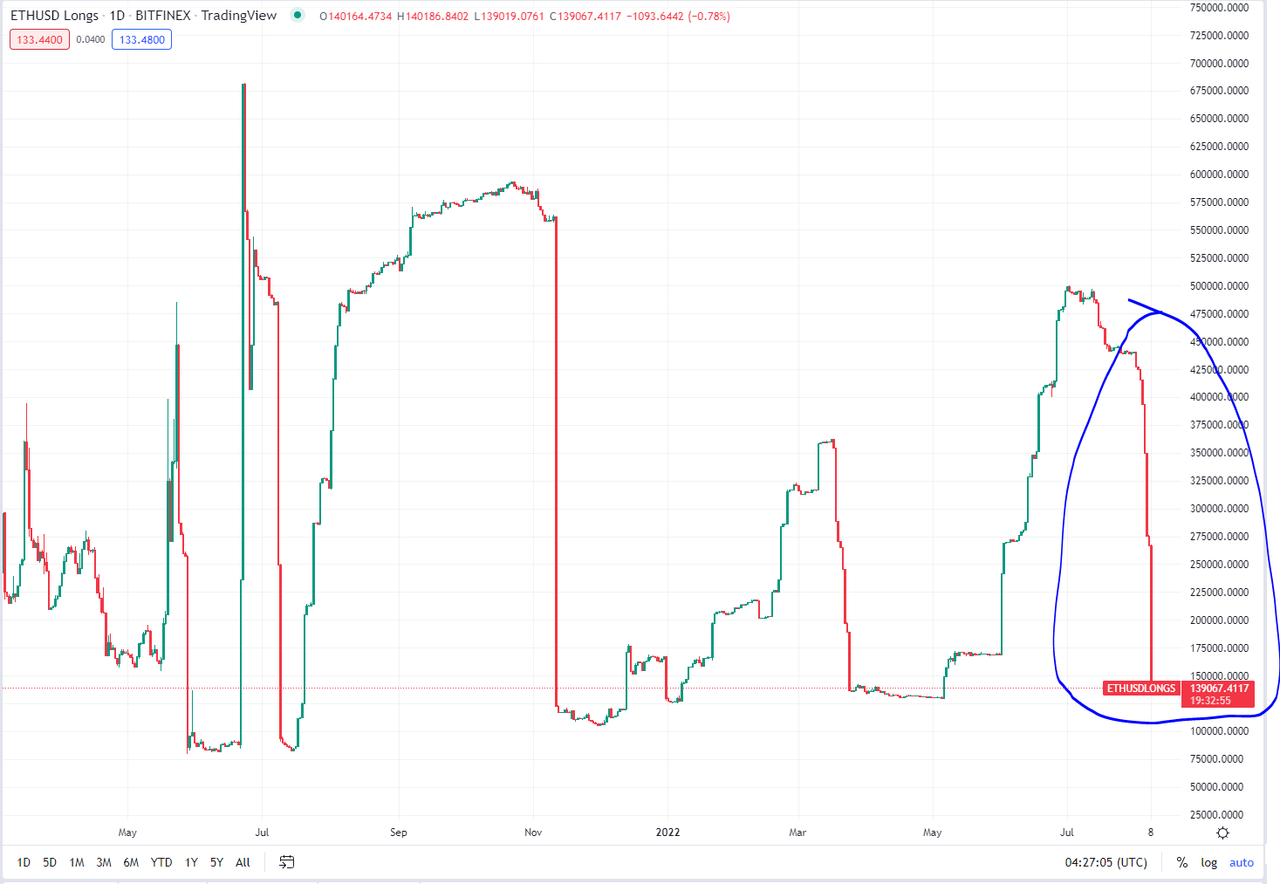

Despite the narrative that has already been building around the Merge, positioning is still quite light within the more discretionary pockets of the market. Perpetual funding has remained negative for most of the rally since June, indicating that there are more shorts than longs in the perp market.

Recently, Bitfinex longs, another notable discretionary pocket of ETH exposure, were reduced back to the lows.

IMO, this light positioning is likely due to many larger participants viewing this move as a “bear market rally” and therefore wanting to put hedges on as we have continued higher.

Historically, there is a large contingent of investors, who lean in the direction of BTC maximalism and will always look to fade the Merge narrative. Their theses primarily revolve around one of two central points.

The first is: “the Merge has been 6 months away for 6 years.” The second concern is around technical/execution risk. After evaluating the timing and execution risk, we have become comfortable with both. After the final testnet, Goerli, was successfully Merged earlier this week, the core developers set a target for the Mainnet Merge for September 15/16. All that remains is coordination.

While many are concerned about the execution risk, the upgrade has been tested extremely rigorously over the years and cross-checked by many teams. Furthermore, one of the core pillars of Ethereum is resilience. This is the reason there are so many different clients–the redundancy acts as a safety net to protect against singular edge cases or bugs. Multiple, usually well over two, unrelated fluke events occurring simultaneously would be required to affect the protocol.

This built-in resilience, the most accomplished developer team in the space, and many years of preparation have given us comfort that a technical issue, though a risk, is unlikely.

Given the cautious positioning and constant desire to “fade” the trade, I expect the next four weeks to follow a similar path as the prior four. There will be periods of pronounced fear as people overanalyze extremely unlikely edge cases. However, I expect the price declines around these periods to be shallow as there are many underexposed parties looking to add exposure on any weakness. Furthermore, almost everyone selling ETH over these next few weeks is only selling it tactically and planning to buy it back at some point before, or immediately after the Merge occurs.

This dynamic means net outflows are measured. On the flip side, I expect the hype around the Merge to magnify significantly as the date comes into focus and the narrative is picked up by the mainstream media. As I believe the thesis is extremely compelling and digestible by both institutional and retail capital, I expect inflows to accelerate as we approach the Merge creating a higher high, higher low dynamic as we approach the date.

What happens once the Merge actually occurs? Normally, you would think there would be risk of a “sell the news” reaction; many investors concerned about technical risk, plan to buy post-Merge. They believe they will capture the structural effect of the Merge without the technical risks. The post-Merge period will also depend on how much FOMO is generated as we approach the Merge and positioning when we actually get there.

We do expect significant buy flows and follow-through directly after the Merge as it is effectively “de-risked.”

Medium-Term

We expect a period of range trading as short-term traders sell, and this sell flow will be digested by the structural demand and larger slower moving institutional accounts. Price action in this period is less predictable and depends on the macro environment. As I have said previously, macro is incredibly hard to predict, but I will offer a few thoughts, nonetheless.

The crypto macro environment is driven by one core metric: whether adoption is growing, stable, or declining. This metric is somewhat impacted by the broader macro environment, but ultimately what matters most is this adoption metric. The reason this metric affects prices is because adoption also drives the long-term flow of funds into or out of the space. Simply put, when users are adopting crypto, they are generally also investing new money into the crypto ecosystem, and this is what drives the macro. When adoption is declining macro is hostile, when it is flat, macro is neutral and when it is growing, macro is accommodating. So how does the macro look today?

For the majority of the last 8-9 months, we have been in a declining adoption environment with a net outflow of users departing the ecosystem.

From May ’21 until the end of June daily active users have experienced a declining trend. Over the last ~6 weeks, we have seen a nascent recovery as users have steadily been increasing. This is a green shoot and indicates a potential thawing of the macro environment. We had been in a declining adoption phase, and we have now, at least, entered a stable adoption phase and potentially an increasing adoption phase. There are other green shoots that have been sprouting recently as well.

After many weeks of redemptions, Tether has started to slowly mint new coins. After a long period of outflows, new money has started to enter the space again.

This impact is not unique to the Ethereum ecosystem, AVAX has also recently seen daily active users increase.

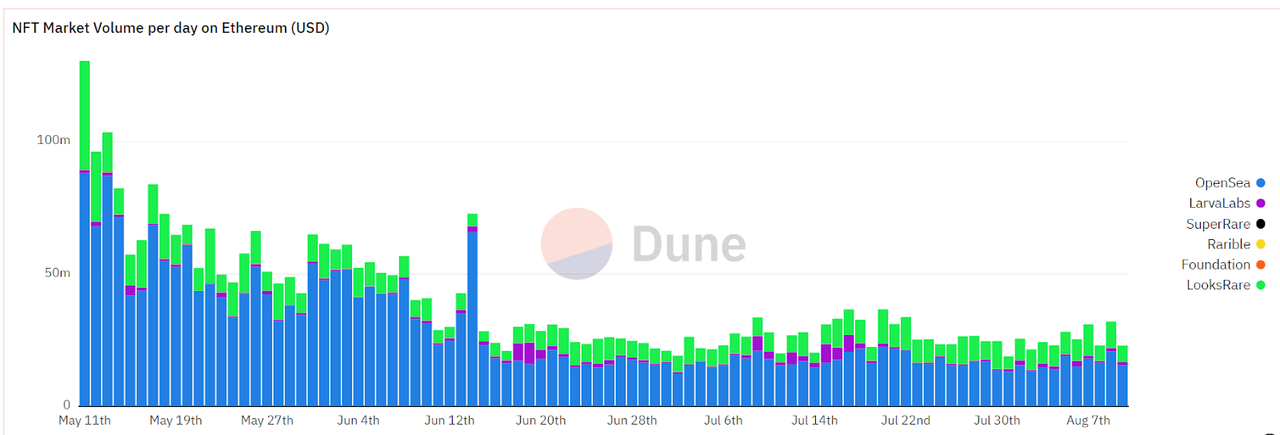

NFT users and transactions have been stable recently.

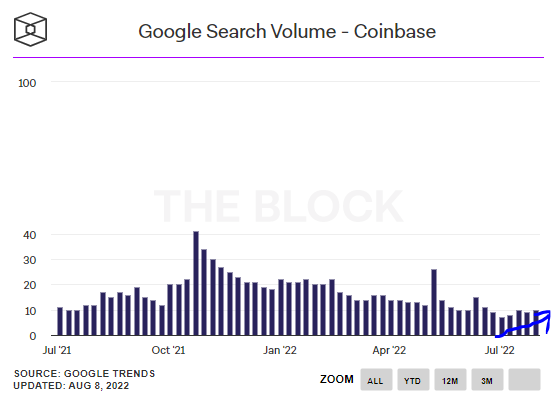

And certain web searches have started to positively inflect, while others are more stable.

These are not dramatic increases, nothing like the exponential increases we saw at the start of the ’21 bull market. This is why I label them green shoots. They are still young and fragile. If they are smothered, they will likely wither and die, but if nurtured they could grow into something material.

We think the broader macro environment will play a key role in determining whether these green shoots live or die. To us, inflation is by far the most important macroeconomic variable; therefore, we believe that if inflation moderates and allows the fed to pivot and ease monetary policy there is a good chance these green shoots will grow stronger. However, if inflation remains high and the fed is forced to continue tightening policy they will likely be smothered and die. Predicting the course of inflation is not our primary domain, however, due to its significance in markets today, we studied it closely. After review, we feel moderating inflation is the most likely outcome, which should give these green shoots a chance to blossom.

Another advantage, in favor of a more sustained bottom, is the fact that an enormous amount of vesting from project launches in the last 24 months has now been absorbed. Furthermore, as most of the projects are down 70-95%, the USD notional size of all future vesting is also vastly reduced. Together, these two dynamics help meaningfully reduce the overall daily supply the space must absorb.

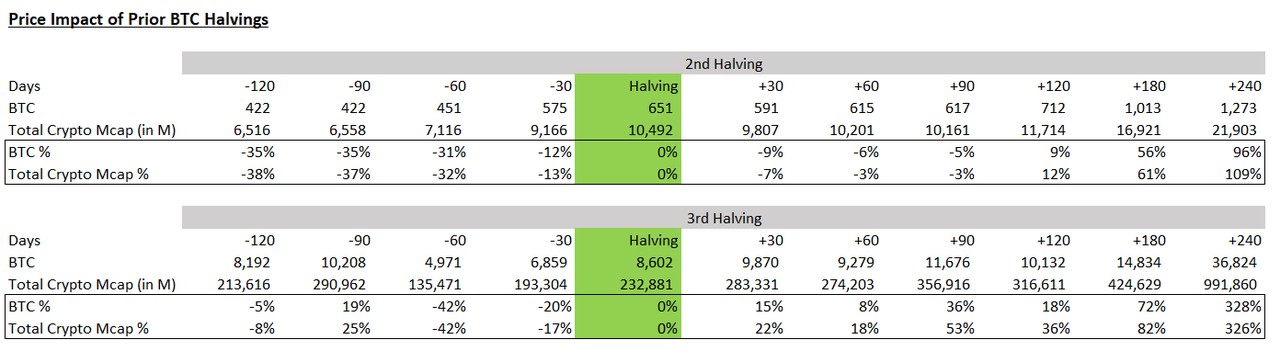

Lastly, the final variable that we think will impact this equation is none other than the Merge. Investors underestimate the impact the Merge will have on the macro environment of the entire space. There is some uncertainty about how much the supply reduction caused by prior BTC halvings has fueled the ensuing price action rather than coincidentally aligning with the natural cycles of human emotion and monetary policy. We sympathize with these uncertainties and think there has been an element of luck in the timing. However, we think the supply reductions also had an impact and the truth likely lies somewhere in the middle. Another common criticism is that supply changes don’t drive price and all that matters are demand changes. We are not in accord with this thinking. A supply reduction is not different than a demand addition.

Let’s say miners sell 10k ETH/day, and instead of getting rid of this sell pressure we simply add 10k ETH/day of buy pressure. This would have the exact same impact as eliminating the miners’ sell pressure but would be a demand change rather than a supply change. It is obvious these two options would have the same impact and it, therefore, makes no sense to us why one would matter more than another.

If we then believe that BTC halvings have impacted crypto’s macro, then it stands to reason that the Merge should do the same. While ETH dominance is significantly lower than BTC dominance at the time of the last halving, the impact from the Merge is nearly as large as the prior BTC halving as a % of total crypto market cap and significantly larger on an absolute basis.

Post-Merge crypto will be relieved of ~$16mm of daily supply. This is not an insignificant amount. To recognize this, it is useful to consider the cumulative impact.

We think a TWAP of 70k ETH per week would have a market impact. That is effectively the impact the Merge will have except it doesn’t stop after a year; it continues into perpetuity. This has the potential to positively influence the entire space as the positive flow impact trickles into other parts of the market. This should provide an added macro tailwind to help nurture the green shoots we referenced earlier and increases their odds of survival.

To conclude, if macro moderates at all, there is a real chance that what began as a bounce off of a capitulation bottom morphs into a more sustainable and organic recovery and the Merge should help aid this process.

Long-Term

In the long-term, the future becomes easier to predict, as structural flows are most important over this time horizon and easier to forecast. This is where the Merge’s impact is most pronounced. As long as Ethereum’s network adoption continues, which we deem likely, structural demand will remain and further inflows will also exist. This should result in sustainable and consistent appreciation, especially compared to other tokens, over many years (hopefully decades) to come. We expect Ethereum to surpass Bitcoin as the largest cryptocurrency within the next few years as we believe flows are the most important variable in crypto. Ethereum will forever have a flow tailwind post-Merge. Bitcoin will forever have a flow headwind. To get a sense for how things may look, the BNB/BTC chart is a good place to start.

BNB/BTC has steadily increased and made multiple new ATHs during this bear market despite little narrative momentum. We believe this is primarily due to the fact that BNB is the only L1 with structural demand. Post-Merge Ethereum will have greater structural demand than BNB both on an absolute and market cap weighted basis.

Investment Strategies to Win the Merge

1. ETH/BTC

Before evaluating the ETH/BTC trade it is necessary to provide some more general context on the PoW vs PoS debate. Much of the following is paraphrased from the appendix of the first article but it is worth reiterating. We believe PoS is a fundamentally more secure system for a variety of reasons. Firstly, each unit of security costs less with PoS. To understand why PoS provides more efficient security than PoW we first need to explore how these consensus mechanisms generate security in the first place. A consensus mechanism is as secure as the cost to 51% attack it. The efficiency of the system can then be measured by the cost (issuance) required to generate a unit amount of security.

In other words, how many dollars the network has to pay out to receive $1 of protection from a 51% attack. For PoW, the cost of a 51% attack is primarily the hardware required to obtain 51% of the hash rate. The relevant metric is how much money miners require to invest $1 in mining hardware. The math tends to work out close to 1 to 1 meaning miners require 100% annual rate of return on their investment or in other words $1 of annual issuance for each $1 they spend on hardware and utilities. In this context, the network needs to issue roughly $1 of supply each year to generate $1 of security.

In the case of PoS, stakers are not required to purchase hardware, so the question becomes what return do stakers demand to lock up their stake in the PoS consensus mechanism?

In general, stakers require a significantly lower rate of return than the 100% miners typically demand.

The primary reason for this is that there is no incremental cost outlay and their assets do not depreciate (mining hardware typically depreciates close to 0 after a few years). The required rate should generally fall in the 3-10% range. As we calculated earlier, the current estimated post-Merge staking rate of 5% falls right in the middle of this range. This means that to gain $1 of security a PoS needs to issue $0.03-$0.10 of issuance. This is 10x-33x more efficient than PoW (20x more in the case of Ethereum’s PoS).

To conclude, this means that a PoS network can issue ~1/20th the issuance of a PoW network and be just as secure. In the case of ETH, they will actually issue about 1/10th of the issuance and the network will be twice as secure as it was during PoW.

This efficiency is not the only advantage. Both consensus mechanisms share a common issue, which is that the security of the chain is correlated to the price of the token. This has the potential to create a self-reinforcing negative feedback loop whereby the reduction in token price causes a reduction in security, which therefore causes a decrease in confidence and drives a further decrease in token price and then repeats. PoS has a natural defense against this dynamic, PoW doesn’t. The attack vector for PoS is much more secure than PoW.

First, to attack a PoS system you must control a majority of the stake. To do this you must purchase at least as many tokens as are staked from the market. However, not all tokens are available for sale. In fact, much of the supply is never traded and is effectively illiquid. Furthermore, and most importantly, with each token acquired the next token becomes harder and more expensive to acquire.

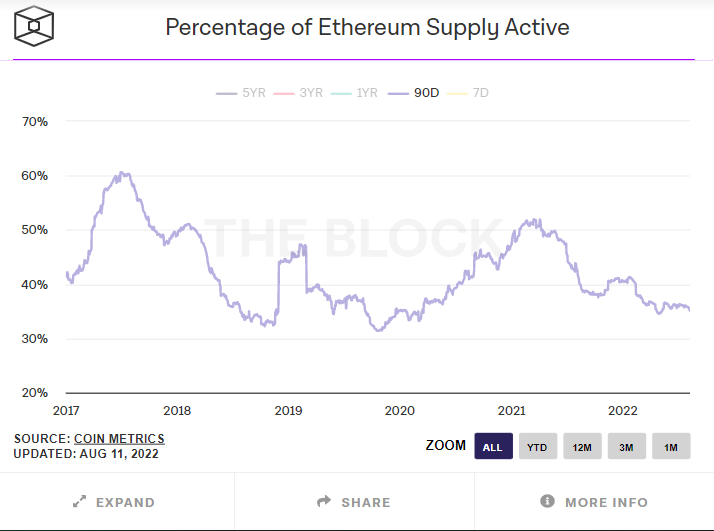

In the case of Ethereum, only ~1/3 of tokens are liquid (moved in the last 90 days). This means that once a steady state staking participation rate of closer to 30% has been reached it will be extremely difficult no matter the amount of money possessed, to attack the network. An attacker would need to purchase the entire liquid supply, which is impractical and nearly impossible.

Another important feature of this defense mechanism is that it is relatively unaffected by price. Because the limiting factor to attack is liquid supply rather than money it does not get much easier to attack the network with lower prices. If there is not enough liquid supply (measured as a % of total tokens) to purchase, it doesn’t matter how cheap each token becomes because the limiting factor is not price. This price-insensitive defense mechanism is incredibly important to deter the potential negative feedback loop that declining prices could otherwise create.

In the case of PoW, in addition to being 20x less efficient, there is no such defense mechanism. Each hardware unit may be marginally harder to acquire than the next, but there is no direct relationship, and if there is a correlation that does exist, it is weak at best. Importantly, it also becomes significantly easier to attack at lower prices as the number of hardware units required decreases linearly with price and the supply of hardware units does not change.

It is not reflexive in the manner the PoS liquid supply defense is.

Other advantages of PoS such as better energy efficiency and better healing mechanisms are articulated clearly elsewhere, therefore we will not focus on them in this piece.

Another misconception about PoS is that it drives centralization by rewarding large stakers more than small stakers. We believe this to be incorrect.

While large stakers receive more staking rewards than smaller stakers, this does not drive centralization. Centralization is the process by which large stakeholders increase their percentage of the stake over time.

This is not what occurs in the PoS system. As large stakers have a larger stake to begin with, the larger rewards do not increase their percentage of the pool. For example, if 10 ETH is staked between two counterparties, Counterparty X has 9 ETH and counterparty Z has 1 ETH. X controls 90% of the stake. A year later X will have received 0.45 ETH and Z will have received .05 ETH. X has received 9 times the amount of rewards as Z. However, X still controls 90% of the stake and Z still controls 10%. The proportions have not been altered and therefore no centralization has occurred.

These inherent differences impact the debate around ETH/BTC. Most consider ETH a totally different asset to BTC as they do think is designed to be a decentralized SoV (replace gold), while BTC is. We believe in many important ways Ethereum is better suited to be a long-term SoV than Bitcoin. Before we compare the two, it is first necessary to evaluate Bitcoin’s current security model and how it may evolve over time.

As discussed earlier, a system’s security is derived from the cost of a 51% attack. As a PoW network, this cost is determined by the amount of money it would take to purchase enough hardware rigs and other equipment/electricity necessary to control 51% of the hash power.

This is roughly equivalent to the cost necessary to recreate the current mining hash rate that exists on the network. In an efficient market (mostly an accurate assumption over the medium/long term), the total hash rate is a product of the value of the issuance that miners receive. Bitcoin is as secure as the value of its issuance. As discussed earlier, this security is both inefficient and importantly lacks the reflexive defense of a PoS system.

What happens when Bitcoin halves its issuance every four years? The system fundamentally becomes 50% less secure assuming all other variables are held constant. Historically, this has not been a large problem as the value of the issuance (and therefore the security) is a function of two variables: the number of tokens issued and the value of each token.

As the price of the tokens has more than doubled around every halving cycle, this has more than compensated for the issuance reduction on an absolute basis. The absolute security of the network has increased through each cycle despite the number of tokens being issued halving. However, this is not a sustainable dynamic long-term for multiple reasons. First, it is not realistic to expect the value of each token to continue to more than double with each cycle. An exponential price increase is mathematically impossible to sustain over long periods of time.

To illustrate this point, if BTC price doubled every halving cycle it would exceed global M2 after ~7 more halving cycles. Eventually, BTC price will stop increasing at this rate; when it does each halving cycle will drastically cut into its security.

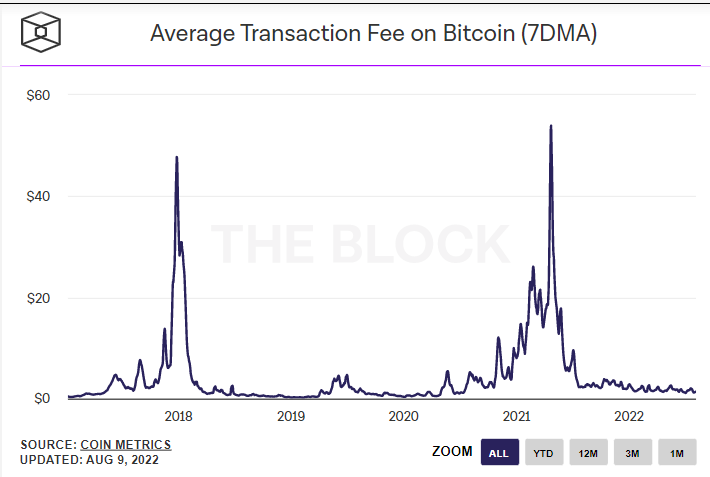

If the BTC price declines around the halving cycle, the security reduction will be even more significant and could trigger the negative feedback loop referred to earlier. This security system is fundamentally unsustainable so long as prices are capped, which they are. The only way to counter this issue is to generate meaningful fee revenue.

This fee revenue could then replace some of the issuance and continue providing an incentive for miners and therefore provide security even after issuance is reduced. The issue for Bitcoin is that fee revenue has been negligible, and also declining, over a long period of time.

In our opinion, the only practical way to generate security over the long term is through significant fee revenue. Therefore, to function as a sustainable SoV a system must generate fees. The alternative is tail emissions, which guarantees inflation compromising the SoV utility.

Long-term security represents the most important property of an SoV. For example, gold has captured the majority of the SoV market for so long as nearly all market participants are confident that it will remain legitimate long into the future.

For a crypto asset to become an adopted and successful SoV, it too must convince the market that it is extremely secure and that its legitimacy is guaranteed. This can only be possible if the protocol’s security budget is sustainable for the long term, inherently favoring a PoS system that has a large and durable fee pool. We believe the most likely candidate for this system is ETH. It is one of only two L1s with a significant fee pool. The other, BNB, is extremely centralized.

Credible neutrality is the second critically important characteristic of a successful SoV. Gold has no allegiance or reliance on anything. This independence creates its success as an SoV. For another asset to be widely adopted as an SoV it must also be credibly neutral. For a cryptocurrency credible neutrality is accomplished through decentralization. Today, the most decentralized cryptocurrency is undoubtedly Bitcoin. This is primarily because Bitcoin has very little development effort, and the protocol is mainly ossified, but nonetheless, the fact remains that it is by far the most decentralized protocol today. If you tried to kill Bitcoin today, it would be extremely hard. If you tried to kill ETH today, it would still be extremely hard, but likely easier than BTC.

However, we believe it is more important to look at the end state than the current state so long as there is a realistic path to achieve this end state. Ethereum has a clear roadmap ahead of it. We believe that while we are currently only in the middle of this roadmap, eventually (I’d estimate ~8-12 years) this roadmap will be complete, and the significance of the core developer team will fade.

At this point, ETH will have a compelling case that it is more decentralized than BTC in addition to possessing far superior long-term security.

Contrary to popular belief, PoS naturally promotes decentralization more than PoW. Larger PoW miners receive a clear benefit from economies of scale, which drives centralization. Scale is much less relevant for PoS as the cost of setting up a node is vastly lower than a PoW rig and there is no real benefit to large-scale electricity as the electricity required for PoS is 99%+ lower.

The economy of scale is a large factor for PoW but is not for PoS.

400,000 unique ETH validators exist today and the top 5 holders only control 2.33% of the stake (excluding smart contract deposit). This level of decentralization and diversity separates ETH from all other PoS L1s. Furthermore, this compares to BTC favorably as the top 5 mining pools today control 70% of the hashrate.

While some critics will point out that liquid staking providers control an overwhelming portion of Ethereum’s stake, we believe these concerns are overblown. Additionally, we expect these concerns to be addressed by the liquid staking protocols and expect additional checks to be put in place to further protect against these concerns.

In summary, PoS is a fundamentally better consensus mechanism for a crypto SoV. This is the reason the Merge will represent a major milestone on Ethereum’s roadmap, marking a critical juncture in its journey to become the most appealing cryptographic SoV.

The fundamental reasons discussed above are the reason we favor the ETH/BTC trade long-term and specifically around the Merge. However, flows, and specifically structural flows, are most important in determining price. It is the structural shift in flows that the Merge triggers that makes this trade so appealing and why the Merge is such a large catalyst for it. Historically, the structural flow for both BTC and ETH have been quite similar.

Although ETH has had a smaller market cap its issuance has been ~3x larger on a market cap weighted basis. This larger issuance has made it extremely difficult for ETH to ever surpass Bitcoin in market cap as it would require ETH to absorb 3x the daily USD denominated supply. An interesting exercise is to think about the chart above and what the inputs are as clearly there has been a strong relationship (stronger than normal correlation would imply). The charted values are a product of tokens issued and token price. What happens if you reduce the tokens issued variable but want to retain the relationship? You must increase token price.

So what should we expect to happen when we reduce the token issued variable for Ethereum by 90%? This is not to say that price should 10x to offset this reduction as the impacts are not necessarily linear, but the relationships are worth considering.

To conclude, post-Merge the passage of time will forever be a flow tailwind for Ethereum while for Bitcoin it will always be a headwind. Ultimately, this straightforward reality is what we believe will be the primary driver of the eventual flippening.

2. Staking Derivatives

As Ethereum is such a large ecosystem many other areas will be tangentially affected by the Merge. As an investor, it is often interesting (and profitable) to consider the second and third-order effects of certain catalysts to search for opportunities that may be inefficiently priced in the market. Regarding the Merge, there are many options such as L2s, DeFi, and Liquid Staking Derivative (LSD) protocols.

After a comprehensive review of the different alternatives, we have concluded that the liquid staking protocols are set to be the largest fundamental beneficiaries of the Merge (even more so than ETH).

The thesis is simple. The LSD protocols’ revenues are directly impacted by the price of ETH plus multiple other Merge related tailwinds that compound each other. Additionally, their largest expense, the cost of subsidizing the liquidity pool between their staking derivate token and native ETH, declines, effectively to zero, shortly after the Merge. At a high level, I expect a 4-7x Merge driven increase in ETH protocol revenue (assuming only modest a ETH price increase) and a 60-80% reduction in their largest expense. This is a uniquely powerful fundamental impact.

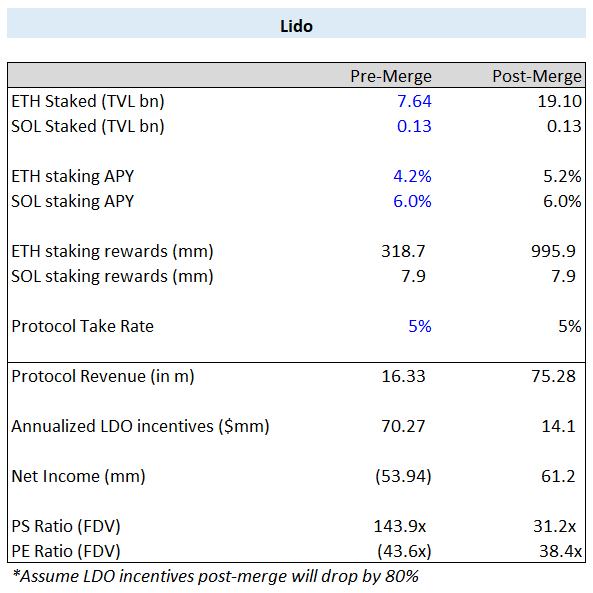

We must examine the revenue and expense model of these protocols to fully comprehend this thesis. Using Lido as an example, as it is the largest of the LSD protocols, let’s examine the model.

Note that these principles also apply to the other players as they are generally quite similar. Lido generates revenue as a percentage of the staking rewards that accrue to their liquid staking derivatives, stETH. Lido receives 5% of all staking rewards generated. If a user deposits 10 ETH for 10 stETH and generates an additional 0.4 stETH over the course of a year. The user keeps 90% of 0.4, the validator keeps 5% and Lido keeps the other 5%. As can be seen, Lido’s revenue is purely a function of the staking rewards generated on its LSD.

These staking rewards are a function of four separate variables: total ETH staked, ETH staking rate, LSD market share, and ETH price.

Importantly, the staking rewards are the product of all four variables. If multiple variables are impacted their effect on the output compounds. In other words, if you double one and triple the other the impact on the staking rewards is 600%. All the variables, except market share, are directly impacted by the Merge.

Total ETH staked will likely increase dramatically from the current 12% to closer to ~30% a 150% increase. As discussed earlier, the staking rate is likely to increase from 4% to ~5%, a 25% increase. There is no reason to think the Merge will significantly impact LSD market share so we can assume this is held constant and has no impact. Lastly, for the sake of this exercise let’s assume a 50% increase in the price of ETH. The aggregate effect of these different variables is 250%*118%*150%= 444% or a ~4.4x increase in revenue.

Expenses also meaningfully drop. The largest expense of these LSD protocols is incentivizing the liquidity pools between their LSD and native ETH. Given there are no withdrawals yet, it is extremely important to create deep liquidity to manage large flows between the LSD and native ETH.

However, once withdrawals are enabled these incentives will no longer be required. As there will then be an arbitrage if the two ever differ materially, natural market forces will keep them relatively pegged as arbitrageurs buy the LSD on any dips. This will allow the LSD protocols to drastically reduce their issuance (expenses), which will also materially reduce the sell pressure on the tokens.

LDO is trading at ~144x revenue on a pre-Merge number but this declines to ~31x when you look at it on a post-Merge number. While not overly cheap by traditional measures, this is attractive for a high-growth strategic asset in the crypto space where valuations are typically elevated. Importantly, this is real revenue that will accrue to the protocol.

A common concern among LDO critics is that this revenue does not get returned to holders. They often compare the protocol to Uniswap for this reason.

While it is true the revenue is not passed through to token holders at current, we do not think this is a legitimate concern nor do we think the Uniswap comparison is correct—just because token holders do not receive cash flow today does not mean they will not in the future.

We believe there will be a time when these returns are enabled. We also know that multiple large stakeholders agree on this issue. Furthermore, we do not think Lido should return cash today and would actually be very concerned with management’s competence if they did. This is an extremely early-stage business (~1.5 years old) that is still in its infancy growth phase. They require regular cash raises and are burning cash on a run rate basis today (this will change post-Merge).

It would not be sensible to raise money from investors to cover the burn and then distribute protocol revenue to token holders, in turn increasing the burn. This would be akin to a startup paying out investor distributions with early revenue despite not generating enough revenue to cover expenses. This would never happen in the traditional capital markets because it is not rational.