“Worst Since Lehman”: Banks Break The World Again

Last week we detailed BofA’s Michael Hartnett’s warning that “The Fed will tighten until something breaks”.

Well, something just broke…

SVB’s collapse – the second biggest US bank failure in history – dominated any reaction to this morning’s mixed bag from the BLS (hotter than expected earnings growth, rising unemployment (especially for Latinos), better than expected payrolls gains).

Things started off badly as SVB crashed 65% in the pre-market before being halted. SVB bonds were puking hard and when the FDIC headline hit, the bonds collapsed further…

Source: Bloomberg

A number of small/medium sized banks were clubbed like a baby seal…

Source: Bloomberg

And the KBW regional bank index crashed (down 9 of the last 10 days and 20% in that period). The 18% drop this week was the index’s worst drop since Lehman (Sept 2008)…

Source: Bloomberg

And as you’ll see below, that started to have some notable impacts on the most arcane of global systemic risk red flag signals…

-

TED Spread at YTD highs (systemic risk rising)

-

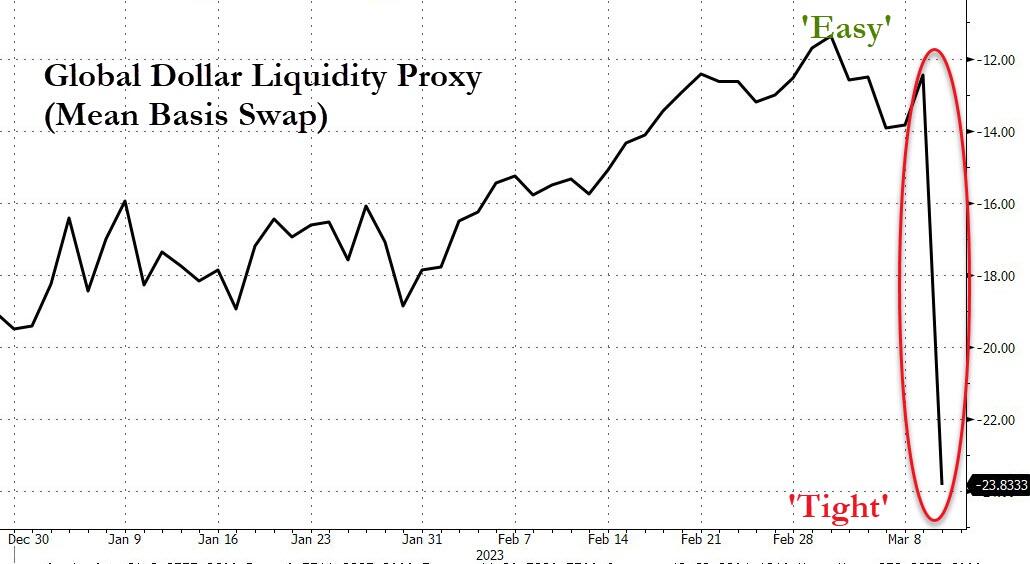

Global USD Liquidity tightest in 2023 (foreigners paying up for USDollars)

-

Global Bank Credit Risk rising

The worst week for stocks in 2023… On the week, all the US majors were down hard with Small Caps crashing 9%, S&P, Dow, and Nasdaq over 4% lower…

The Dow has been underwater on the year for over a week and is now down 4% in 2023. Today’s ugliness smashed the S&P 500 and Russell 2000 down to unchanged on the year…

Source: Bloomberg

All the US Majors are now back below their 200DMAs…

Unsurprisingly, financials were the week’s biggest sector laggards but all were red on the week…

VIX exploded higher on the day, back above 28 and recoupling with equity weakness…

Source: Bloomberg

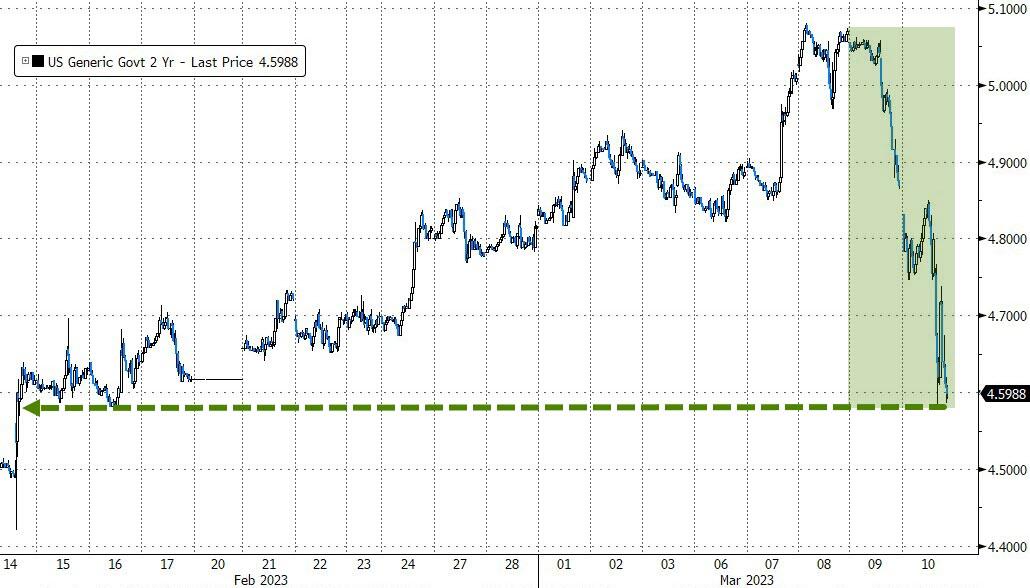

On the week, Treasuries saw a wild ride but yields ended dramatically lower across the curve with the shorter-end outperforming (down almost 30bps on the week)…

Source: Bloomberg

The 2Y yield is down over 50bps in the last two days, the biggest 2-day drop since Lehman (Sept 2008)…

Source: Bloomberg

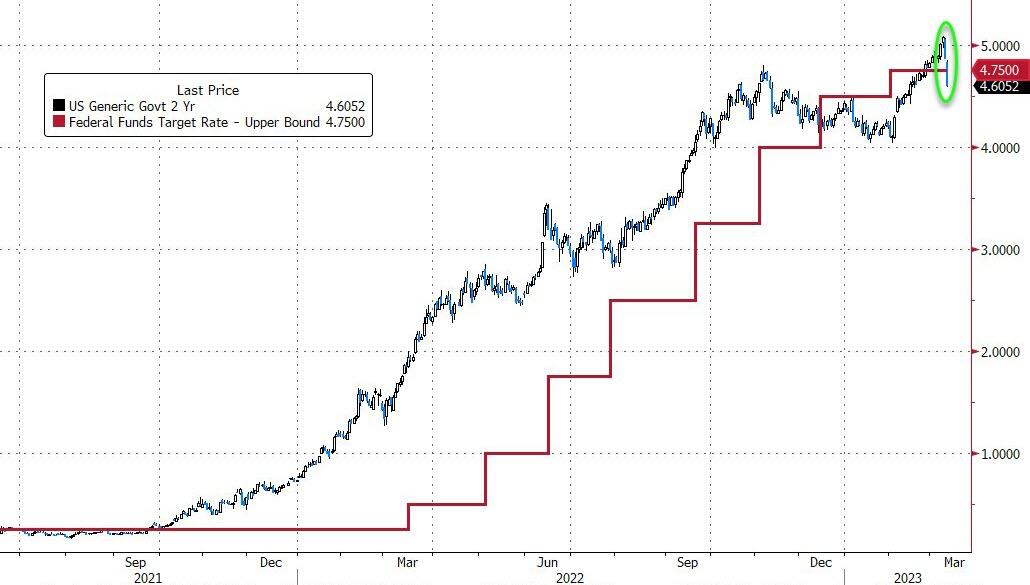

The 2Y Yield is back below the Fed Funds rate once again, and will likely be considerably further below it after the next Fed meeting…

Source: Bloomberg

The 10Y yield puked back to 3.70% – one month lows – after testing 4.00% for two weeks…

Source: Bloomberg

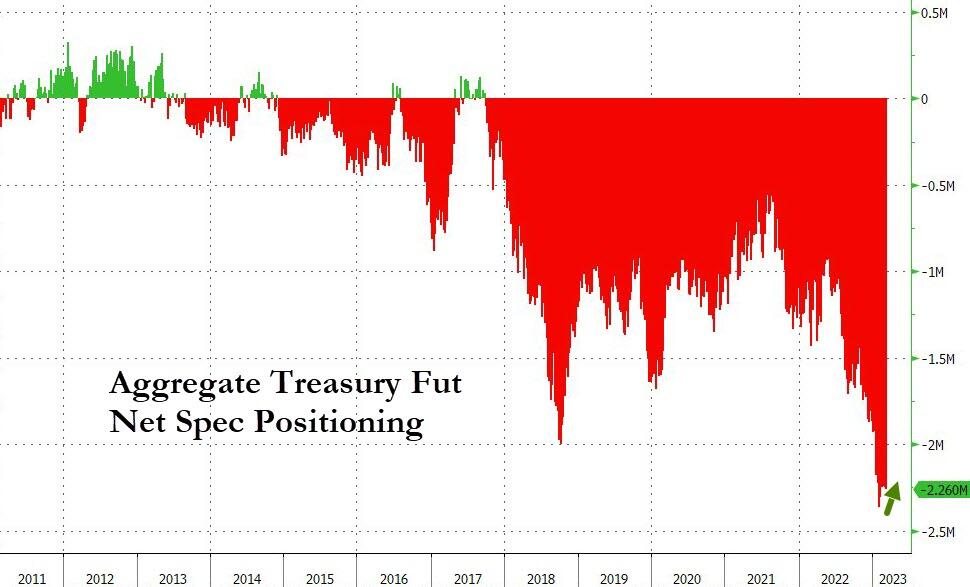

Notably, Specs are practically still at their most short ever in bonds – so this week’s plunge in yields was hurting a lot of people…

Source: Bloomberg

No extreme moves in the TED spread yet (although its back YTD highs as systemic risk increases)…

Source: Bloomberg

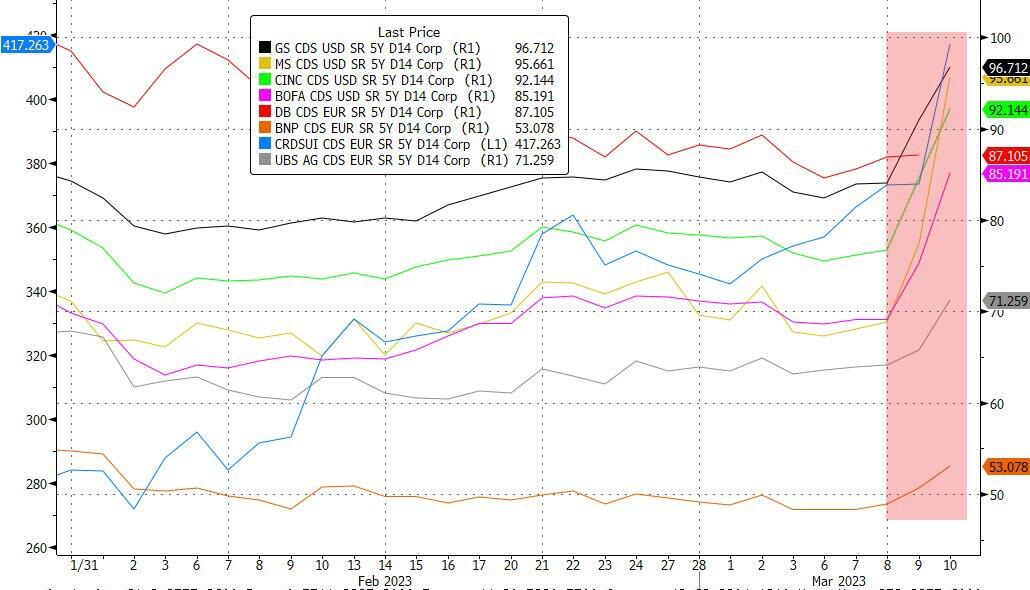

Global bank credit risk is on the rise too…

Source: Bloomberg

The dollar ended higher against its fist peers on the week – after major ups (hawkish Powell) and downs (SVB sparking dovishness)…

Source: Bloomberg

Global dollar liquidity tightened dramatically this week as the world reached for USDs at much more aggressive costs…

Source: Bloomberg

Bitcoin puked back down to $20,000 – 2 month lows – and found support…

Source: Bloomberg

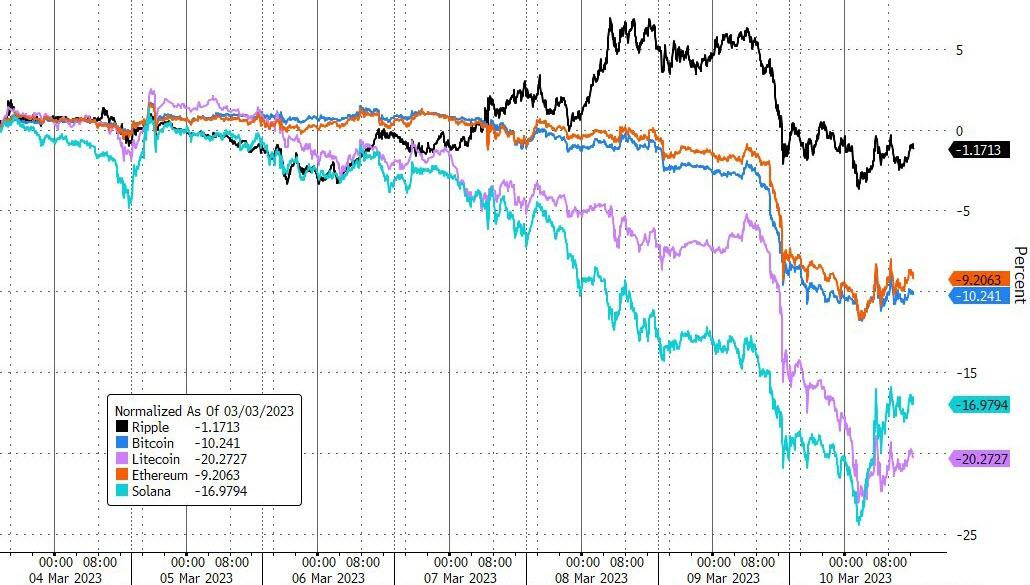

Solana and Litecoin were hit really hard this week with BTC and ETH down about 10% and Ripple holding close to unch…

Source: Bloomberg

Against all the carnage, bullion joined bonds in the safe-haven camp, with gold spiking back above $1870 – one month highs…

While oil was up today, WTI ended lower on the week back to a $76 handle…

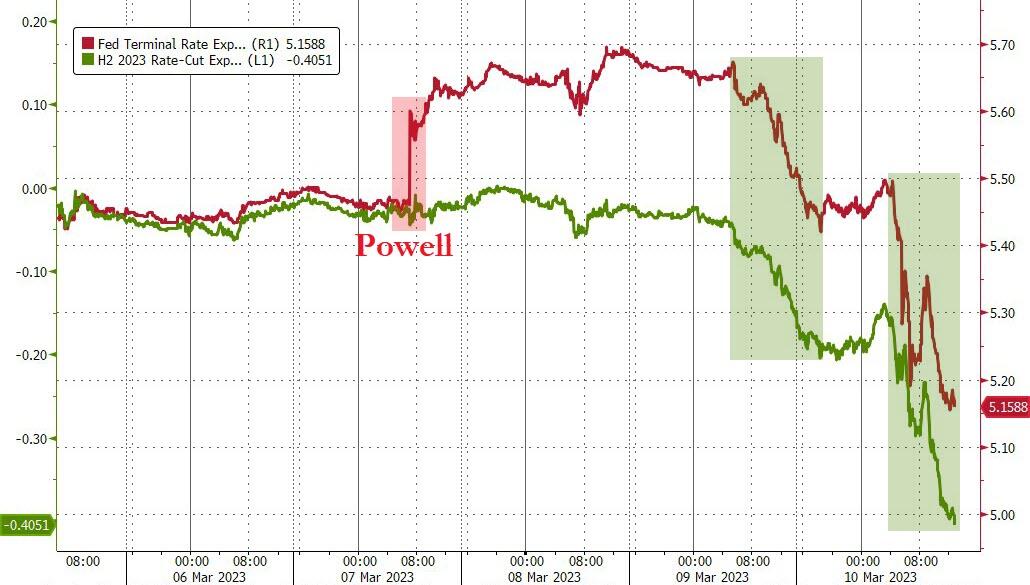

The ‘panic’ across markets had a dramatic effect on Fed rate trajectory expectations with the Fed’s terminal rate expectations plunging over 55bps since the post-Powell spike earlier in the week, and 40bps of rate-cuts are now priced-in by year-end…

Source: Bloomberg

Additionally, expectations for The Fed’s action in March are hawkishly higher on the week (but down today) with around a 40-50% chance of 50bps hike priced in…

Source: Bloomberg

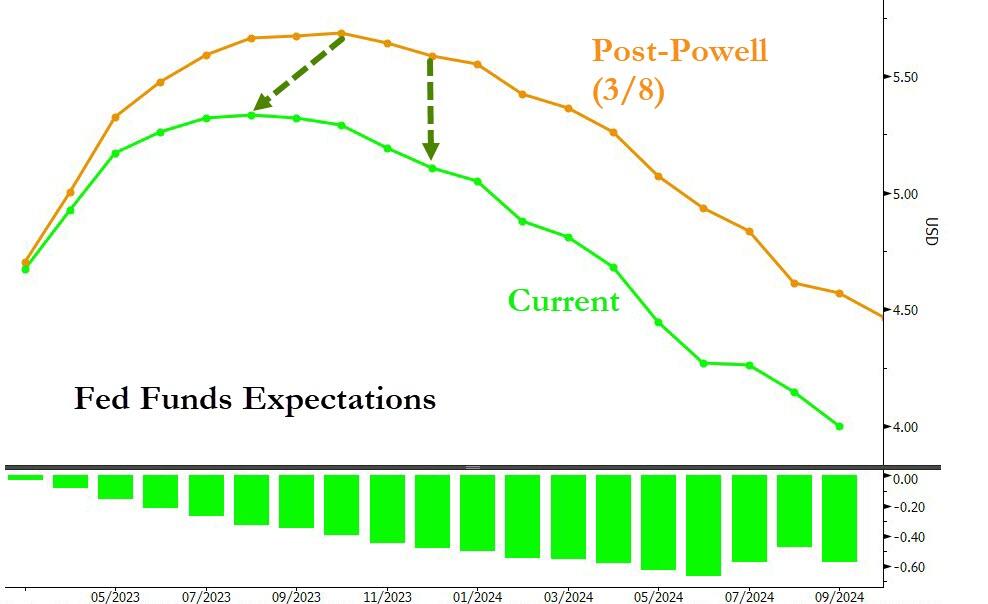

To put that shift in context, the term structure has dropped and twisted significantly since Wednesday…

Source: Bloomberg

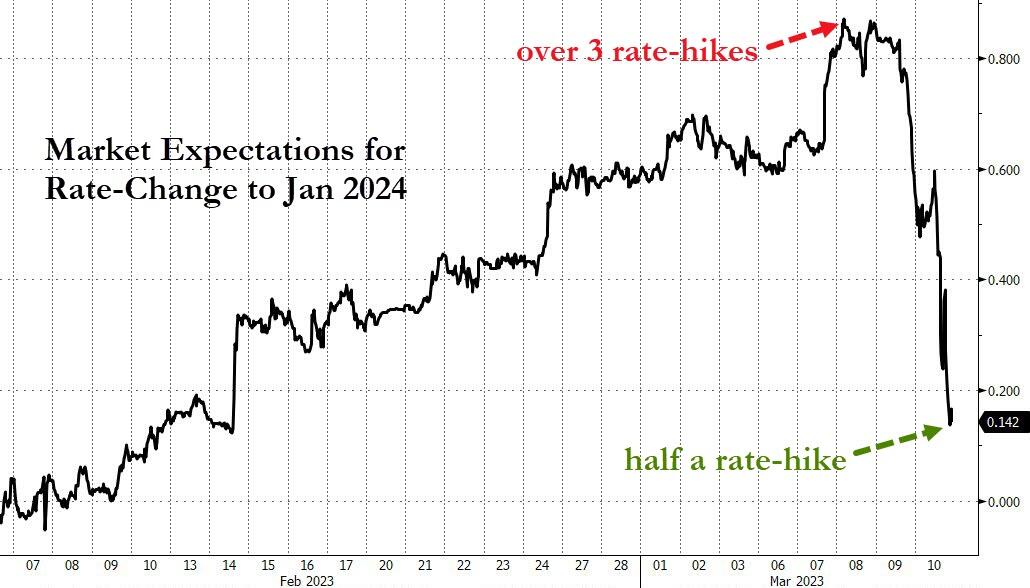

Just to really rub in what the fuck just happened… the market was pricing in over 3 25bps rate-hikes to Jan 2024 on Wednesday… and now its pricing in around half of one rate-hike…

Source: Bloomberg

Finally, we give the last word to Eric Johnston at Cantor Fitzgerald:

“Three days ago the view in the market was that economy was teflon vs the rate hikes and that there were not going to be any financial accidents because we have made it this far without much damage,” he wrote.

“What has now changed is that people now realize that we are not teflon and there can be impact and very negative impact at that from these hikes. It is not about which bank is next, or who has similar exposure, or will depositors be made whole. It is about there likely being more time bombs out there that we have no idea about right now. That is what has changed, people no longer believe we are teflon…finally.”

Maybe keep your eyes out for other bank CEOs dumping millions in their own stock…

Makes you wonder eh?

Returning full circle to the start of today’s market summary, we are reminded of Michael Hartnett’s closing remarks: “The market stops panicking when central banks start panicking.”

Tyler Durden

Fri, 03/10/2023 – 16:01

via ZeroHedge News https://ift.tt/27fhueJ Tyler Durden