Yen’s Resilience Shows Bank Of Japan Is No Longer The Driver

By Ven Ram, Bloomberg markets live reporter and strategist

The yen’s recent resilience even with evidence of cooling domestic inflation is a sign of things to come: the currency can do well even without the Bank of Japan having to come to its rescue.

Not in 16 months has Tokyo seen a lower inflation reading than what we got Tuesday. Another day, another time, the yen would have gone perhaps screamingly lower, for the outcome flies in the face of expectations that the Bank of Japan will exit negative interest rates soon. But the yen is holding its poise fine, thank you — underscoring how what is happening in the US economy may still offer the beleaguered currency some salve regardless of what the BOJ does or doesn’t do.

Suddenly, the lay of the land is looking a lot different for policymakers than the previous time they met on Oct. 31: that is when the 10-year JGB yield was hovering menacingly around 1%, forcing it to abandon its 1% yield cap and instead use it as just a “reference.” Yet, just weeks later, the yield is holding below 0.70% — meaning, even without an abandoning of the cap, there would have been little pressure on the BOJ to defend the curve.

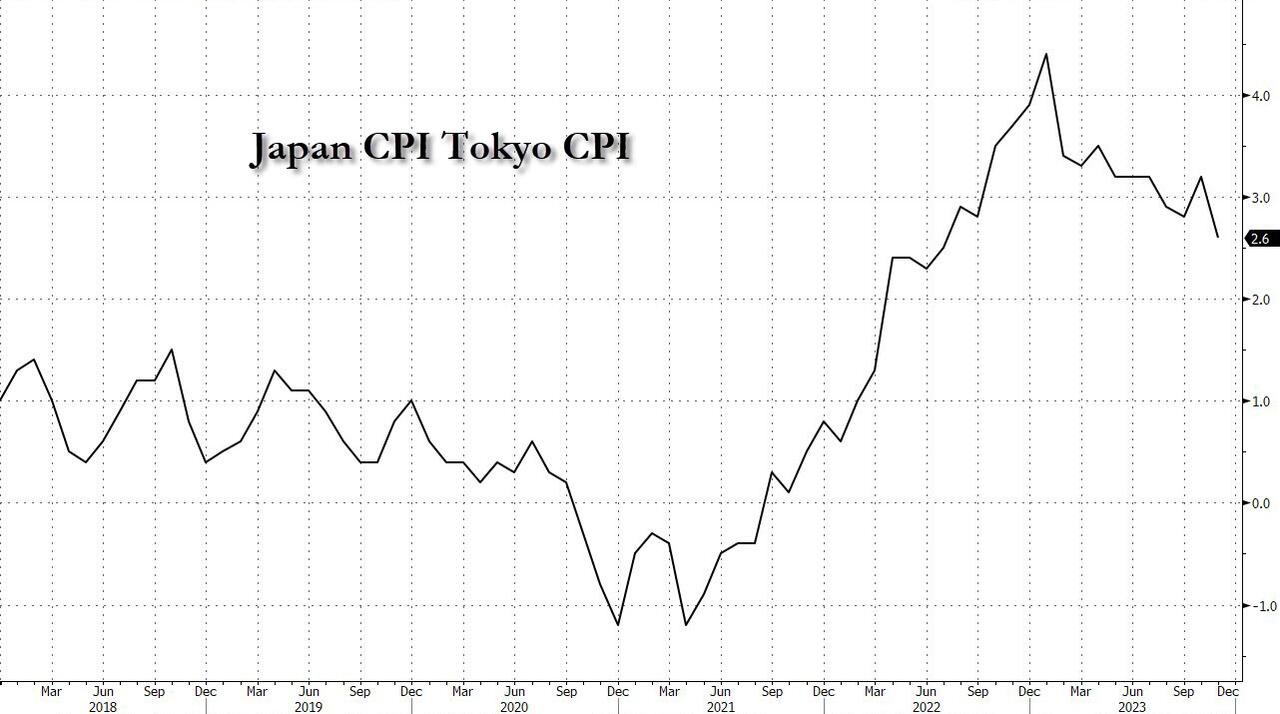

In the real economy, too, there is little sign that the central bank should act when it meets in just two weeks. Consumer prices in Japan’s capital were forecast to have risen 3% in November, a reading that would have kept up the pressure on the BOJ to end almost eight years of dalliance with a sub-zero policy rate. Yet, prices rose just 2.6% — slow enough to cause policymakers to doubt whether they have found sustainable inflation after decades of trying. Agreed, it’s not the national CPI, but as colleague Erica Yokoyama points out, Tokyo’s figures offer a leading indication of the national trend

Ironically, the yen can still find respite against the dollar, what with inflation in the US slowing faster than estimated and obviating the need for the Federal Reserve to tighten more in this cycle. That may herald a period where nominal and inflation-adjusted yield differentials start to narrow meaningfully in favor of the yen for the first time since the Fed started pushing rates higher, putting a floor on a currency that has slumped a stunning 30% since the end of 2020.

Tyler Durden

Tue, 12/05/2023 – 12:45

via ZeroHedge News https://ift.tt/FMmRXu4 Tyler Durden