The World’s Economic Myths Are Hitting Their Limits

Authored by Gail Tverberg via Our Finite World blog,

There are many myths about energy and the economy. In this post I explore the situation surrounding some of these myths.

My analysis strongly suggests that the transition to a new Green Economy is not progressing as well as hoped.

Green energy planners have missed the point that our physics-based economy favors low-cost producers.

In fact, the US and EU may not be far from an economic downturn because subsidized green approaches are not truly low-cost.

[1] The Chinese people have long believed that the safest place to store savings is in empty condominium apartments, but this approach is no longer working.

The focus on ownership of condominium homes is beginning to unwind, with huge repercussions for the Chinese economy. In March, new home prices in China declined by 2.2%, compared to a year earlier. Property sales fell by 20.5% in the first quarter of 2024 compared to the same period a year ago, and new construction starts measured by floor area fell by 27.8%. Overall property investment in China fell by 9.5% in the first quarter of 2024. No one is expecting a fast rebound. The Chinese seem to be shifting their workforce from construction to manufacturing, but this creates different issues for the world economy, which I describe in Section [6].

[2] We have been told that Electric Vehicles (EVs) are the way of the future, but the rate of growth is slowing.

In the US, the rate of growth was only 3.3% in the first quarter of 2024, compared to 47% one year ago. Tesla has made headlines, saying that it is laying off 10% of its staff. It also recently reported that it is delaying deliveries of its cybertruck. A big issue is the high prices of EVs; another is the lack of charging infrastructure. If EV sales are to truly expand, they will need both lower prices and much better charging infrastructure.

[3] Many people have assumed that home solar panel sales would rise forever, but now US home solar panel sales are shrinking.

A forecast made by the trade group Solar Energy Industries Association and consulting firm Wood Mackenzie indicates that US solar panel installations by homeowners are expected to fall by 13% in 2024. There are many issues involved: higher interest rates, less generous subsidies to homeowners, not enough grid capacity for new generation, and too much overproduction of electricity by solar panels in the spring and fall, when heating and air conditioning demand is low. The overproduction issue is particularly acute in California.

For each individual 24-hour day, the timing of solar energy production does not match up well with when it is needed. With sufficient batteries, solar electricity produced in the morning can help run air conditioners in the evening. But storage from summer to winter is still not feasible, and batteries for short-term storage are expensive.

[4] It is a myth that wind and solar truly add to electricity supplies for the US and the countries in the EU. Instead, their pricing seems to lead to tighter electricity supplies.

Strangely enough, in the US and the EU, when wind and solar are added to the electric grid, electricity supplies seem to get tighter. For example, one article says, Most of US electric grid faces risk of resource shortfall through 2027, NERC [regulatory group] says.

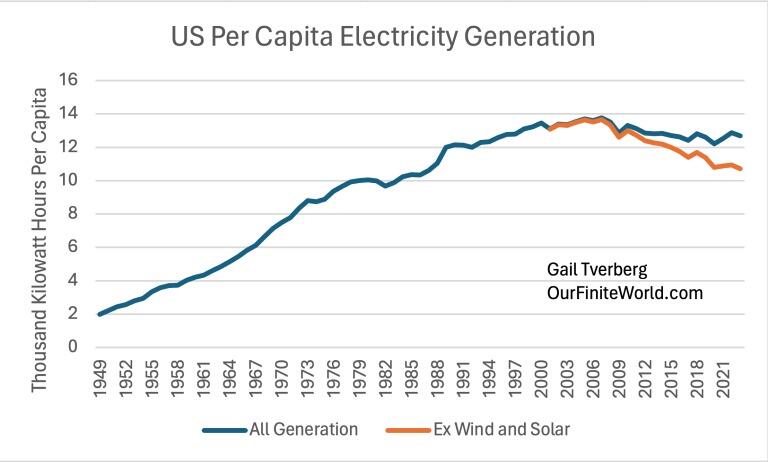

Charts of electricity supply per capita show an unusual trend when wind and solar are added. Figure 1 shows that, in the US, once wind and solar are added, total electricity generation per capita falls, rather than rises!

Figure 1. US per capita electricity generation based on data of the US Energy Information Administration. (Data is through 2023, even though this is not easy to see from the labels.)

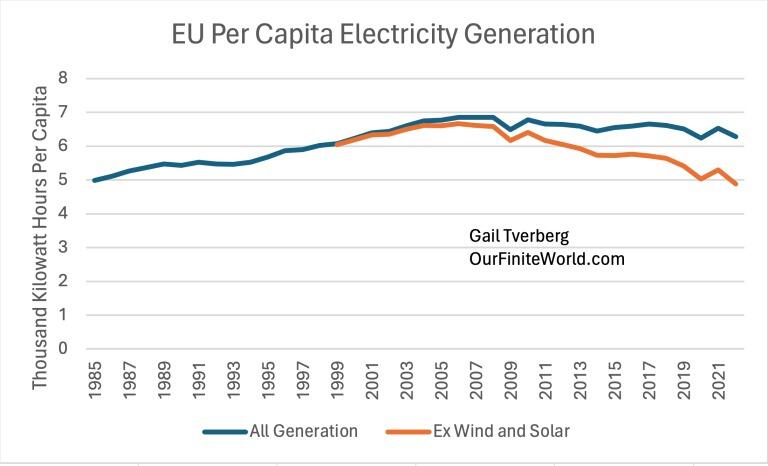

The EU, using a somewhat shorter history period, shows a similar pattern of declining total electricity generation per capita, even when wind and solar are added (Figure 2).

Figure 2. Electricity generation per capita for the European Union based on data of the 2023 Statistical Review of World Energy, prepared by the Energy Institute. Amounts are through 2022.

I believe that the strange pricing systems used for wind and solar in the US and EU are driving out other electricity suppliers, especially nuclear. With this system, intermittent electricity enjoys the subsidy of going first at the regular wholesale market rate. Other providers find themselves with very low or negative wholesale rates in the spring and fall of the year and on weekends and holidays. As a result, their overall return falls too low. Nuclear is particularly affected because it requires a huge, fixed investment, and it cannot be ramped up and down easily.

Besides the foregoing issues affecting the supply of electricity generated, there are also factors affecting the demand for electricity. Electricity generation using wind and solar tends to be high priced when all costs are included. The US and EU are already high-cost areas for businesses to operate. High electricity rates further add to the impetus to move manufacturing and other industry to lower-cost countries if businesses desire to be competitive in the world market.

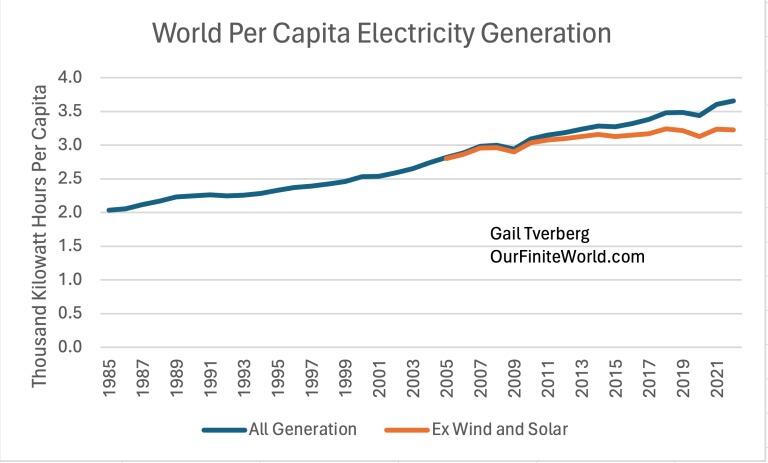

On a world basis, in 2022, wind and solar added about 13% to total world electricity generation (Figure 3).

Figure 3. Electricity generation per capita for the World based on data of the 2023 Statistical Review of World Energy, prepared by the Energy Institute. Amounts are through 2022.

Based on Figure 3, with the addition of wind and solar, the upward slope of the world per capita electricity generation has been able to remain pretty much constant from 1985 to 2022, at about 1.6% per year. But the US and the EU, as high-cost producers of goods and services, haven’t been able to participate in this per capita growth of electricity.

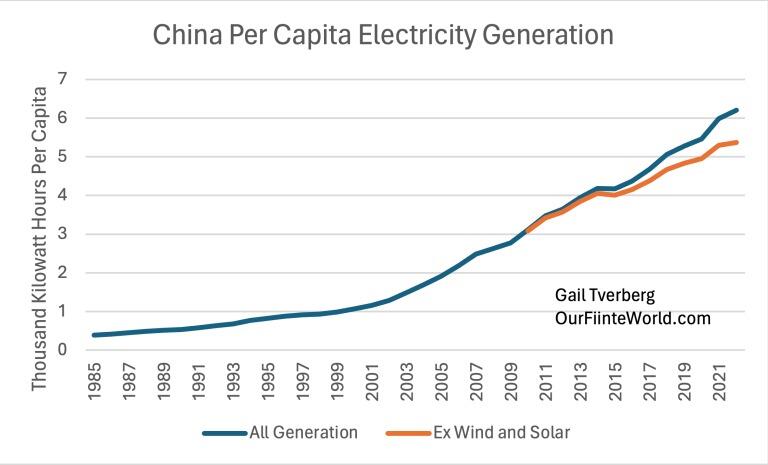

Instead, China has been a major beneficiary of the shift of manufacturing overseas from the US and EU. It has been able to rapidly increase its electricity supply per capita, even with wind and solar. It has also been adding both nuclear and coal-fired electricity generation capacity.

Figure 4. Electricity generation per capita for China based on data of the 2023 Statistical Review of World Energy, prepared by the Energy Institute. Amounts are through 2022.

Thus, this analysis produces the result a person would expect if the physics of the world economy favors efficient (low-cost) producers.

[5] It is a myth that the US and EU can greatly ramp up the use of EVs or greatly increase the use of Artificial Intelligence (AI) without relying on fossil fuels.

Both EV production and AI are heavy users of electricity supply. We have seen that the US and the EU no longer have growing per-capita electricity supplies. Ramping up electricity generation would require a long lead time (10 years or more), a major increase in fossil fuel consumption, and an increase in electricity transmission lines.

The State of Georgia, in the United States, is already running into this issue, with planned data centers (related to AI) and EV manufacturing plants. The state plans to add new gas-fired electricity generation. It will also import more electricity from Mississippi Power, where the retirement of a coal-fired plant is being delayed to provide the necessary additional electricity. Eventually, more solar panels are planned, as well.

[6] It is a myth that the world economy can continue as usual, whatever happens to energy supply and growing debt. China’s homebuilding problems could, in theory, lead to debt bubbles crashing around the world.

The world economy depends upon a growing bubble of debt. It also depends on an ever-increasing supply of goods and services. In fact, the two are closely interrelated. As long as a growing supply of low-priced energy of the types used by built infrastructure is available, the economy tends to sail along.

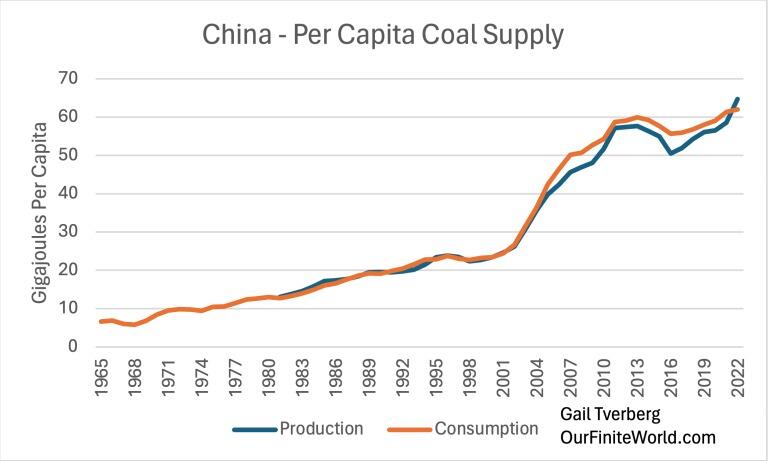

China, with problems in its property business, is an example of what can go wrong when energy supplies (coal in China) become expensive, as supply becomes increasingly constrained. Figure 5 shows that China’s per-capita coal supply became constrained in about 2013. China’s per capita coal extraction had been rising, but then it dipped. This made it more difficult for builders to construct the homes planned for would-be homeowners. This is part of what got home builders in China into financial difficulty.

Figure 5. Per capita coal supply in China based on data of the 2023 Statistical Review of World Energy, prepared by the Energy Institute. Amounts are through 2022.

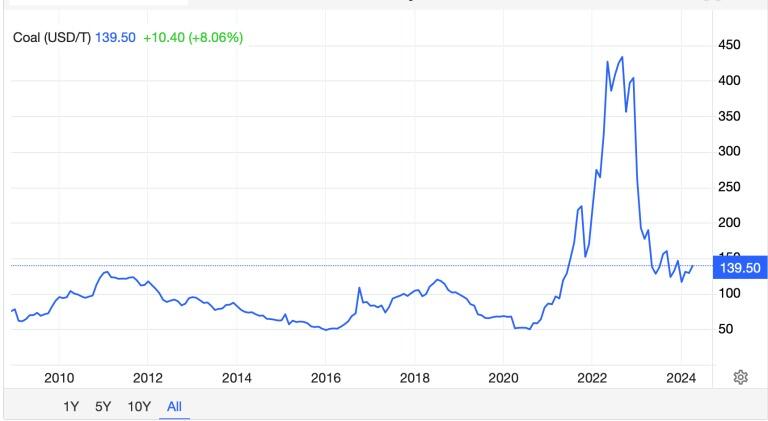

Finally, in 2022, China was able to get coal production up. But the way this was done was through very high coal prices (Figure 6). (The prices shown are for Australian coal, but Chinese coal prices seem to be similar.)

Figure 6. Newcastle Coal (Australia) prices in chart prepared by Trading Economics.

Building concrete homes at such high coal prices would have resulted in new homes that were far too expensive for most Chinese citizens to afford. If builders were not already in difficulty from low supply, adding high coal prices, as well, would be a second blow. Furthermore, all the workers formerly engaged in home building needed new places to earn a living; the current approach seems to be to move many of these workers to manufacturing, so that the popping of the home building bubble will have less of an impact on the overall economy of China.

There is now concern that China is ramping up its manufacturing, particularly for exports, at a time when China’s jobs in the property sector are disappearing. The problem, however, is that ramping up exports of manufactured goods creates a new bubble. This huge added supply of manufactured goods can only be sold at low prices. This new low-priced competition seems likely to lead to manufacturers, around the world, obtaining too-low prices for their manufactured products.

If other economies around the world are forced to compete with even lower-cost goods from China, it could have an adverse impact on manufacturing around the world. With low prices, manufacturers are likely to lay off workers, or give them excessively low wages. If wages and prices are inadequate, debt bubbles in other parts of the world are likely to collapse. This will happen because many borrowers will become unable to repay their debt. This is the reason that we have been hearing a great deal recently about raising tariffs on Chinese exports.

[7] The world’s biggest myth is that the world economy can continue to grow forever.

I have pointed out previously that based on physics considerations, economies cannot be expected to be permanent structures. Economies and humans are both self-organizing systems that grow. Humans get their energy from food. Economies are powered by the types of energy products that our built infrastructure uses. Neither can grow forever. Neither can get along without energy products of the right types, in the right quantities.

We become so accustomed to the narratives we hear that we tend to assume that what we are told must be right. These narratives could be based on wishful thinking, or on inadequate models, or on a sour grapes view that says, “We don’t want fossil fuels anyhow.” We know that humans need food, and that economies will continue to require fossil fuels. We can’t make wind turbines or solar panels without fossil fuels. What do we plan to do for energy without fossil fuels?

In a finite world, economies cannot continue forever. We don’t know precisely what will go wrong or when it will go wrong, but we can get a hint from the recent failures of myths that our economy may change dramatically in the not-too-distant future.

Tyler Durden

Fri, 04/19/2024 – 18:00

via ZeroHedge News https://ift.tt/w2RFQge Tyler Durden