.

.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/pjKmzgkmaLs/story01.htm williambanzai7

another site

.

.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/pjKmzgkmaLs/story01.htm williambanzai7

Submitted by John Rubino of The Dollar Collapse blog,

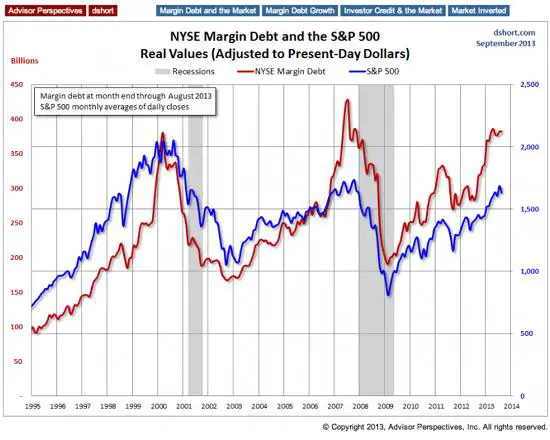

The US equity markets are back in record territory, at least in nominal terms.

The last two times they spiked this way, the following year was pretty brutal. See the next chart, which tracks the S&P 500 and margin debt, the amount of money investors are borrowing against their shares of stock to buy more stock. The chart seems to show that when investors are optimistic enough to use leverage to invest in already-risky stocks, then the good times have pretty much run their course and something nasty is imminent. If recent history is our guide, it is now time to either take some money off the table or short the hell out of the big indexes – or whatever else you like to do when the market looks overbought.

But this conclusion is only valid if we’re in the same stage of the credit bubble as during those two previous sentiment peaks. In 2000 and 2007, to take just one measure of financial stability, the federal government’s debt was $6 trillion and $8 trillion, respectively, versus $17 trillion today. Plenty of other leverage metrics are also way up, indicating that the US is much further down the path of currency debasement than it was just a few years ago. So the question becomes: at what point does a quantitative difference become qualitative? When does the phase change occur? The next chart shows why this question is more than academic. In the early stages of Zimbabwe’s epic hyperinflation its stock market rose from 2,000 to over 40,000 in one year. Presumably a lot of indicators similar to margin debt were by then pointing to a blow-off top and screaming “sell” to students of history.

Then the market proceeded to run up to 4,000,000. What happened? The country ran its printing press flat-out and inflated away its currency, so the price of pretty much every tangible asset, when measured in Zimbabwean dollars, went parabolic. Since equities represent part ownership of companies, and most non-financial companies own tangible assets, their value went up as well. Not enough to increase in real terms (versus gold, for instance) but enough to make shorting that market a really bad idea.

So are we 2007 America or 2006 Zimbabwe? A lot is riding on the answer.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/5idBs8UmrW8/story01.htm Tyler Durden

As the 'diplomatic' debacle continues to rage between the US and Europe (most loudly France and Germany) over the Obama administration's ongoing eavesdropping on its allies' cell phones, Reuters reports that (state-backed) Deutsche Telekom is calling for German comms companies to cooperate to shield local internet traffic from foreign intelligence services. "It is internationally without precedent that the internet traffic of a developed country bypasses the servers of another country," notes one academic, warning that if more countries wall themselves off, it could lead to a troubling "Balkanisation" of the Internet, crippling the openness and efficiency that have made the web a source of economic growth. Despite Obama's denials, the situation is not fading away, and Germany and France continue to demand a "no spying" agreement.

As a diplomatic row rages between the United States and Europe over spying accusations, state-backed Deutsche Telekom wants German communications companies to cooperate to shield local internet traffic from foreign intelligence services.

…

More fundamentally, the initiative runs counter to how the Internet works today – global traffic is passed from network to network under free or paid-for agreements with no thought for national borders.

If more countries wall themselves off, it could lead to a troubling "Balkanisation" of the Internet, crippling the openness and efficiency that have made the web a source of economic growth, said Dan Kaminsky, a U.S. security researcher.

Controls over internet traffic are more commonly seen in countries such as China and Iran where governments seek to limit the content their people can access by erecting firewalls and blocking Facebook and Twitter.

"It is internationally without precedent that the internet traffic of a developed country bypasses the servers of another country," said Torsten Gerpott, a professor of business and telecoms at the University of Duisburg-Essen.

"The push of Deutsche Telekom is laudable, but it's also a public relations move."

…

Government snooping is a sensitive subject in Germany, which has among the strictest privacy laws in the world, since it dredges up memories of eavesdropping by the Stasi secret police in the former East Germany, where Merkel grew up.

The issue dominated discussions at a European summit on Thursday, prompting Merkel to demand that the U.S. strike a "no-spying" agreement with Berlin and Paris by the end of the year.

…

Brazil's President Dilma Rousseff, angered by reports that the U.S. spied on her and other Brazilians, is pushing legislation that would force Google, Facebook and other internet companies to store locally gathered or user-generated data inside the country.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/6ia7M3CZSss/story01.htm Tyler Durden

The headline September Durable Goods number was great: rising at 3.7%, this was well above the August revised 0.2% increase and far above expectations of a 2.3% increase. However, a quick glance into the reasons shows why the reality is – once again – far uglier. Actually, the reason is just one: Boeing, which reported 127 plane orders in September compared to just 16 in August. This translated into a 57.5% monthly increase in non-defense aircraft orders in September (and Syria’s contribution can’t be denied either, leading to a 15.2% increase in defense airplane orders). So what does the US capital spending climate look like when stripped away from very volatile (and very cancelable) Boeing orders? In a word ugly: Durable Goods ex transports actually declined by -0.1, on expectations of a rebound to 0.5%, following an even more downward revised August print of -0.4%.

![]()

But aside from the broader durable goods, and focusing on pure CapEx, in the form of Capital Goods Orders non-Defense Shipments (not so much order which too can be canceled), it is here that we get yet another validation of our thesis from early 2012, namely that the Fed has killed all corporate CapEx-driven growth. Cap Goods orders declined -1.1%, from a sharply downward revised 0.4% (was 1.5%) in August and wildly missing expectations of a 1.0% increase: this was the third consecutive miss in a row in this series. As for the shipments: at -0.2%, sliding from a downward revised 1.1%, and also missing expectations, this was the 6th miss in the Shipments category in the past 7 months. So much for any hopes of a recovery.

But wait until we get the October print when the government was “shut down” for more than half the month: it is here that the real plunge in Corporate CapEx will arguably be felt and the chart below will look like it suddenly had a downward facing heart attack.

Summarizing the above: with such horrible news, it is impossible for the S&P to not hit a fresh record high today. After all: not only is the Noctaper guaranteed, but the scenario of an increase in QE is becoming ever more likely…

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/p-vlxf0X6vw/story01.htm Tyler Durden

There are people in the world that go to work every day to end up stating the damn obvious. Oh! They get paid for doing that too. Heaven forbid that they should do that for free. They get paid for saying what we have all been shouting from the roof-tops for years and that has been complacently ignored, pooh-poohed, laughed at, lambasted and pulled apart. Well, now it’s our turn to do the same to the German Central Bank, the Bundesbank for stating the obvious in a report on Monday in which it has been admitted that the German housing market is ready to bust its bubble since housing is overvalued by 20%. Dankeschön Bundesbank!

What is worth celebrating is only that at last someone from a central bank has actually admitted what the rest of the world has been harping on about and griping over for years now. Do people that get appointed to central banks come from planets where they can’t see properly or where they at least see the world from that rose-colored spectacle point of view? Do they have some perception of the world that is entirely different from our own one? Up until now, it may well have been what they have been making us believe.

In a report published yesterday the Bundesbank states that house rises: “are difficult to justify based on fundamental factors”. We all saw that coming in a bis-repetita placent fashion. One housing bubble is never ever enough. It’s like a double shot of vermouth. It might hurt the next morning, but it’s a damn good feeling as it slips down the throat and then we forget and hot the bottle again when the headache has somewhat subsided. That’s what’s been happening for months now around the world in our economies; and the headache still hasn’t gone. Banks are still being injected with drip-fed cash propping them up from all sides in the hope (against hope) that the economy will be rescued and revamped.

According to some analysts, there’s yet again no need to worry and any alarm bells that are sounding are the pure fantasizing of alarmist plot theories of a growing bubble issue on the housing market. Germany isn’t in any danger according to some of an explosion since:

But, that won’t stop the bubble growing since there is a lack of available housing in German cities as well as in other major places in the world as migrationary workers and increases in population size outstrip the availability of space and building projects. In the short-term there will be a further increase in housing prices in these cities. Limited supply coupled with reduced interest rates will inevitable make demand greater than supply and prices will in back-to-basic economics increase. There should be the ‘housing bubble for dummies’ coming out in the very near future. But, even then, someone will turn around and say that they never saw it coming.

It’s not just Germany it’s all over the world from Shanghai to New York. In the UK two financial schemes set up by the government (Help to Buy and Funding for Lending) have already caused reminiscent memories of the US mortgage guarantee programs and a disguised subprime set-up. No matter. We shall just end up with the same bricks and mortar on our faces as the banks and the investors rake in the money and then end up getting propped up and injected with more greenbacks (still).

There are those out there who are still saying that the word bubble is only premature and let’s not put the cart before the horse. Only trouble is: the horse went to the knacker’s yard long ago and there really won’t be any point in bolting the financial (un-)stable door when it all happens again.

The growing bubble will explode and what’s bad enough is that the countries we live in haven’t even got governments that have been able to admit and recognize the economically blatantly obvious situation that we have been preparing for now for the past five years. Even when they have admitted it, they turn round and just like the Bundesbank say that there is no ‘macroeconomic risk to financial stability’.

Originally posted: Blatant Housing-Bubble: Stating the Obvious

You might also enjoy: Let’s Downgrade S&P, Moody’s and Fitch For Once | US Still Living on Borrowed Time | (In)Direct Slavery: We’re All Guilty | The Nobel Prize: Do We Have to Agree? |

Technical Analysis: Bear Expanding Triangle | Bull Expanding Triangle | Bull Falling Wedge | Bear Rising Wedge | High & Tight Flag

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/EnSJKcW1DPk/story01.htm Pivotfarm

As frequent readers will recall, one of our favorite series of posts describing the “Walking Dead” monetary zombie-infested continent that is Europe is the one showing the abysmal state Europe’s credit creation machinery, operated by none other than the Bank of Italy’s, Goldman’s ECB’s Mario Draghi, finds itself in. As a reminder, it was as recently as September when we found that “Mario Draghi’s Nightmare Gets Worse” because “European Loans Declined At Record Rate.” To our complete lack of surprise, when a few hours ago the ECB released the latest monetary and credit creation update for the month of September, it showed… no change. Or rather, while loans to the private sector are at all time record lows, that other metric which Draghi at least has some direct control over (since he obviously can’t control the amount of confidence in the system aside from threats of brute force), M3, just had its lowest pace of increase since January 2012.

But here’s the kicker: while the US at least has the Fed to step in and forcefully push credit into the private sector void as it has been doing every day since Lehman, in Europe, with the ECB’s balance sheet actively declining, the continent is well, on its own to fend against the monetary zombies horde shown below.

SocGen agrees:

The European Central Bank reported that money supply growth (M3) in the euro area decelerated further in September, dropping to an annual rate of 2.1% – the slowest pace of increase since January 2012 – well below the ECB’s 4.5% target. Looking at credit, the picture is once again one of fragmentation. While the French corporate sector proved rather resilient to credit crunch, the total amount of credit to corporates plunged by 4.9%yoy in Italy, 7% in Portugal, and an alarming 19.9% in Spain. Undoubtedly, this weakness in monetary and credit developments will add pressure on the ECB, which could decide to ease financial conditions further. But this will not be sufficient.

Our view is that a rate cut would require an additional weakening in either the growth or the inflation outlook.

The combination of currency in circulation and overnight deposits (M1) increased by only €6bn in September, after the average €38bn jumps recorded over the July/August time span. On an annual basis, the growth of M1 continued to slow. Indeed, the closely-followed aggregate stood 6.6% above year-ago levels in September, after 6.8% in August and 7.1% in July.

On that matter, the ECB recently communicated on the fact that the solid increase in the M1 aggregate seen since the beginning of the year would ultimately foster a recovery in credit – and Investment – even though the overall money supply growth (M3) was decelerating.

Yet, it is not clear to us how a movement in overnight deposits would be such as to stimulate investment. What we rather believe is that the flow of credit remains negative, which suggests that the strong recovery in investment everyone expects is unlikely to happen for, at least, six to nine more months.

Not only is it not clear to SocGen, worst of all it is not clear to Mario Draghi, which is why his nightmares will only get worse and worse, as loan creation collapses further, as non-performing loans accumulate, and as Europe’s credit-money zombies finally escape their cages and start biting chunks of meat off of (Europe’s unemployed) people.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/uS-EygqJ6SU/story01.htm Tyler Durden

As frequent readers will recall, one of our favorite series of posts describing the “Walking Dead” monetary zombie-infested continent that is Europe is the one showing the abysmal state Europe’s credit creation machinery, operated by none other than the Bank of Italy’s, Goldman’s ECB’s Mario Draghi, finds itself in. As a reminder, it was as recently as September when we found that “Mario Draghi’s Nightmare Gets Worse” because “European Loans Declined At Record Rate.” To our complete lack of surprise, when a few hours ago the ECB released the latest monetary and credit creation update for the month of September, it showed… no change. Or rather, while loans to the private sector are at all time record lows, that other metric which Draghi at least has some direct control over (since he obviously can’t control the amount of confidence in the system aside from threats of brute force), M3, just had its lowest pace of increase since January 2012.

But here’s the kicker: while the US at least has the Fed to step in and forcefully push credit into the private sector void as it has been doing every day since Lehman, in Europe, with the ECB’s balance sheet actively declining, the continent is well, on its own to fend against the monetary zombies horde shown below.

SocGen agrees:

The European Central Bank reported that money supply growth (M3) in the euro area decelerated further in September, dropping to an annual rate of 2.1% – the slowest pace of increase since January 2012 – well below the ECB’s 4.5% target. Looking at credit, the picture is once again one of fragmentation. While the French corporate sector proved rather resilient to credit crunch, the total amount of credit to corporates plunged by 4.9%yoy in Italy, 7% in Portugal, and an alarming 19.9% in Spain. Undoubtedly, this weakness in monetary and credit developments will add pressure on the ECB, which could decide to ease financial conditions further. But this will not be sufficient.

Our view is that a rate cut would require an additional weakening in either the growth or the inflation outlook.

The combination of currency in circulation and overnight deposits (M1) increased by only €6bn in September, after the average €38bn jumps recorded over the July/August time span. On an annual basis, the growth of M1 continued to slow. Indeed, the closely-followed aggregate stood 6.6% above year-ago levels in September, after 6.8% in August and 7.1% in July.

On that matter, the ECB recently communicated on the fact that the solid increase in the M1 aggregate seen since the beginning of the year would ultimately foster a recovery in credit – and Investment – even though the overall money supply growth (M3) was decelerating.

Yet, it is not clear to us how a movement in overnight deposits would be such as to stimulate investment. What we rather believe is that the flow of credit remains negative, which suggests that the strong recovery in investment everyone expects is unlikely to happen for, at least, six to nine more months.

Not only is it not clear to SocGen, worst of all it is not clear to Mario Draghi, which is why his nightmares will only get worse and worse, as loan creation collapses further, as non-performing loans accumulate, and as Europe’s credit-money zombies finally escape their cages and start biting chunks of meat off of (Europe’s unemployed) people.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/uS-EygqJ6SU/story01.htm Tyler Durden

Two days after Spain reported its first positive sequential GDP print (unclear just how adjusted the definition of GDP was to get to this watershed moment after 9 quarters of declines) and a day after it unemployment supposedly dropped more than expected (what was left unsaid is that the Spanish working age population dropped 85,200 in Q3 and -279,000 YoY and that of the 39,500 “jump” in Q3 employed people, virtually all were self-employed or temps while employees on permanent contracts were down by 146,300), the 5 second attention span investing herd is now convinced the housing market in Spain has dropped. This was “formalized” after billionaire Bill Gates invested $155 million, also known as pocket change, in Spain’s infrastructure group Fomento de Construcciones & Contratas. Surely, if anyone knows how to time housing market turns it is the guy who brought us MS-DOS 3.1.

Unfortunately, the mythical housing bottom may have been just that – mythical – following news that Spain’s bad bank (oh yeah – lest we forget, Spain has a wonderful rug under which it can hide all insolvent bank NPLs) failed to attract high enough bids in its first sale of commercial real estate and will cut the size of the portfolio being offered to make it easier to sell, according to Bloomberg which cited three people familiar with the matter.

Bloomberg reports why rumors of the Spanish housing market’s resurrection, may have been exagerated:

The bad bank, known as Sareb, received more than 30 offers for the portfolio that were lower than it expected, said one of the people, who declined to be named because the information isn’t public. It will reduce the number of buildings in the package known as Corona to four from seven, the person said. A spokeswoman for Madrid-based Sareb declined to comment.

Spain created Sareb last year to absorb 50 billion euros ($69 billion) of real-estate assets from lenders including Bankia group that took aid as part of the nation’s European bailout. Its failure to attract high enough bids may undermine growing optimism in Spain as the stock market has surged 21 percent this year and foreign investors including Microsoft Corp. founder Bill Gates buy into Spanish companies.

In August Sareb agreed to sell a majority stake in a group of almost 1,000 homes known as Project Bull to private-equity firm H.I.G. Capital LLC. It also sold loans advanced to Inmobiliaria Colonial SA with a nominal value of 245 million euros to Burlington Loan Management Ltd.

Also known as two greatest fools. So far, all alone.

On the bright side, this only means that the Fed will need to send out some more memos to banks (and hedge funds) warning about lax lending practices, which will remain unread until the next crash, in the meantime the same banks, and hedge funds, will scramble to pick up whatever carry trades are left in the global fungible market – if it means ultimately rushing into whatever dregs the Sareb has to sell to the greater fool, so be it.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Gxwqucf9DHs/story01.htm Tyler Durden

Two days after Spain reported its first positive sequential GDP print (unclear just how adjusted the definition of GDP was to get to this watershed moment after 9 quarters of declines) and a day after it unemployment supposedly dropped more than expected (what was left unsaid is that the Spanish working age population dropped 85,200 in Q3 and -279,000 YoY and that of the 39,500 “jump” in Q3 employed people, virtually all were self-employed or temps while employees on permanent contracts were down by 146,300), the 5 second attention span investing herd is now convinced the housing market in Spain has dropped. This was “formalized” after billionaire Bill Gates invested $155 million, also known as pocket change, in Spain’s infrastructure group Fomento de Construcciones & Contratas. Surely, if anyone knows how to time housing market turns it is the guy who brought us MS-DOS 3.1.

Unfortunately, the mythical housing bottom may have been just that – mythical – following news that Spain’s bad bank (oh yeah – lest we forget, Spain has a wonderful rug under which it can hide all insolvent bank NPLs) failed to attract high enough bids in its first sale of commercial real estate and will cut the size of the portfolio being offered to make it easier to sell, according to Bloomberg which cited three people familiar with the matter.

Bloomberg reports why rumors of the Spanish housing market’s resurrection, may have been exagerated:

The bad bank, known as Sareb, received more than 30 offers for the portfolio that were lower than it expected, said one of the people, who declined to be named because the information isn’t public. It will reduce the number of buildings in the package known as Corona to four from seven, the person said. A spokeswoman for Madrid-based Sareb declined to comment.

Spain created Sareb last year to absorb 50 billion euros ($69 billion) of real-estate assets from lenders including Bankia group that took aid as part of the nation’s European bailout. Its failure to attract high enough bids may undermine growing optimism in Spain as the stock market has surged 21 percent this year and foreign investors including Microsoft Corp. founder Bill Gates buy into Spanish companies.

In August Sareb agreed to sell a majority stake in a group of almost 1,000 homes known as Project Bull to private-equity firm H.I.G. Capital LLC. It also sold loans advanced to Inmobiliaria Colonial SA with a nominal value of 245 million euros to Burlington Loan Management Ltd.

Also known as two greatest fools. So far, all alone.

On the bright side, this only means that the Fed will need to send out some more memos to banks (and hedge funds) warning about lax lending practices, which will remain unread until the next crash, in the meantime the same banks, and hedge funds, will scramble to pick up whatever carry trades are left in the global fungible market – if it means ultimately rushing into whatever dregs the Sareb has to sell to the greater fool, so be it.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Gxwqucf9DHs/story01.htm Tyler Durden

Overnight Media Digest

WSJ

* A flurry of recent attacks by al Qaeda-linked militants in Iraq – strengthened by their alliance with jihadist fighters in Syria – is threatening to undo years of U.S. efforts to crush the group.

* Activist investor Carl Icahn boosted his investment in Apple Inc by 22 percent to 4.73 million shares, and continued to push for a massive $150 billion buyback at the company, according to a letter he sent to Apple Chief Executive Tim Cook.

* Former employees at USIS, the company that did the background check of Edward Snowden, the leaker of national-security information, say they were pushed to speed through background checks amid a corporate culture that made revenue the top priority.

* Outrage over alleged U.S. monitoring of German Chancellor Angela Merkel’s personal cellphone spread across Europe on Thursday, threatening to complicate an array of America’s trans-Atlantic interests.

* Twitter set its price range for its initial public offering at $17 to $20 a share, in a deal that values the company at up to $11.1 billion.

* Highly rated issuers sold more than $12 billion of bonds Thursday, taking advantage of robust investor demand and the latest tumble in market interest rates to stock up on cash.

* The U.S. Federal Communications Commission is considering softening the decades-old 25 percent foreign-ownership limit on TV and radio stations, paving way for new investment.

* The slowdown in mortgage-refinancing activity is hitting towns across the U.S. as banks such as Bank of America, Wells Fargo and Citigroup eliminate thousands of jobs to cope with declines in home lending.

* Amazon.com Inc shares soared Thursday in after-hours trading after the online retailer reported its third loss in the past year. Investors were focused on a big jump in quarterly sales, which exceeded analysts’ forecasts.

* The Chief Executive of Southwest Airlines Co hinted Thursday that the carrier could soon start charging for checked baggage if the flying public comes to accept the fees that other airlines charge.

FT

Micro-blogging company Twitter set a modest $17 to $20 price range per share for its initial public offering next month, anxious to avoid the runaway valuations which dogged rival Facebook’s offering.

Bank of America is planning to axe 3,000 jobs – most of which are not full-time employees – in its legacy asset servicing unit as improving credit quality reduces work on delinquent loans and foreclosures.

WPP, the world’s largest advertising company, posted better-than-expected third-quarter sales growth driven by strength from business in western Europe for the first time this year.

Royal Bank of Scotland’s “bad bank” is taking bids for its West Register internal property portfolio, which consists of a number of industrial distribution units with a guide price of 63 million pounds ($101.85 million).

G4S, the world’s biggest security services firm, said its UK chief executive had stepped down immediately after holding the position for little more than a year

NYT

* Twitter disclosed that it planned to price its eagerly awaited initial public offering in the $17 a share to $20 a share range, as it readies a road show for investors.

* The Food and Drug Administration on Thursday recommended tighter controls on how doctors prescribe the most commonly used narcotic painkillers. The move, which represents a major policy shift, follows a decade-long debate over whether the widely abused drugs, which contain the narcotic hydrocodone, should be controlled as tightly as more powerful painkillers like OxyContin.

* Fury over reports that American intelligence had monitored the cellphone of Chancellor Angela Merkel spread from Germany to much of Europe on Thursday, plunging trans-Atlantic relations to a low and threatening to recast the United States and President Obama from friend and ally to cyberbully.

* When the stock market opened on Thursday, NQ Mobile Inc , a Chinese mobile security company, had a valuation of $1.1 billion. Just hours later, half of its value was erased. Muddy Waters, a short-selling firm known for its scathing reports on Chinese companies, released a harsh assessment of NQ Mobile on Thursday, calling it a “massive fraud.”

* Federal officials did not fully test the online health insurance marketplace until two weeks before it opened to the public on Oct. 1, contractors told Congress on Thursday.

* The Federal Reserve’s rule asks banks to estimate how much cash might flee in a 30-day period, and requires them to enough assets that they could sell to cover that outflow.

* Microsoft Corp’s earnings of $5.24 billion beat expectations, and were helped in large part by a surge in the company’s corporate software business.

* On Thursday, DuPont said it would spin off its performance chemicals segment into a new publicly traded company. The unit – which makes a pigment that turns paints, paper and plastics white, as well as refrigerants and polymers for cables – generated about $7 billion in revenue in 2012.

* More than a year after

the activist investor William Ackman won a bitter battle for control of the Canadian Pacific Railway, he is cashing in part of his investment at a substantial profit.

* Many high-end brands have left behind Bal Harbour Shops, for years a magnet to the wealthy, for more breathing room in Miami’s Design District – once an enclave of furniture showrooms, low storefronts and empty streets in the shadow of two interstate highways.

Canada

THE GLOBE AND MAIL

* Canadian Prime Minister Stephen Harper insisted that “very few” people in Conservative circles knew that chief aide Nigel Wright was personally bailing out Senator Mike Duffy when the politician faced public pressure to reimburse taxpayers for questionable expense claims.

* Senators pressed the Canadian government about why a federal spy agency has been probing telecommunications in Brazil, seeking clear answers about the activities of Communications Security Establishment Canada.

Reports in the business section:

* CGI Group Inc faced the full fury of the U.S. political process on Thursday, as executives from the Canadian technology giant appeared before an angry congressional committee investigating the botched rollout of the healthcare.gov website.

* Companies operating in Canada’s oil sands are facing new pressure to assess and disclose the long-term risks to the value of their crude reserves amid a global effort to address climate change.

NATIONAL POST

* Training for front-line officers and better information sharing between police and government agencies can help protect law enforcement officials from potentially aggressive “sovereign citizens,” says a newly declassified briefing to Canadian police chiefs.

* An American who shot a Chicago police officer, and then fled to Toronto until he was caught 30 years later, was treated unfairly by Canadian immigration officials, a judge has ruled. The Federal Court of Canada said there were several problems with the way officials handled Douglas Gary Freeman’s immigration case and, as a result, he was “denied procedural fairness.”

FINANCIAL POST

* On a conference call to discuss third-quarter results, the Chief Executive of Potash Corp of Saskatchewan Inc ripped into OAO Uralkali, the Russian producer, saying its decision to collapse a cartel-like marketing company and max out production was “probably the single dumbest thing” he has ever seen in the fertilizer business.

* Pershing Square Capital Management has announced a public offering of more than 5.9 million shares of Canadian Pacific Railway Ltd that would have a value of more than $880-million at market prices.

China

CHINA SECURITIES JOURNAL

– Net profit of Chinese insurers jumped 134.9 percent in the first nine months of this year to 91.75 billion yuan ($15.09 billion), due to a low base last year and improved investment returns, according to the China Insurance Regulatory Commission.

SHANGHAI SECURITIES NEWS

– Shanghai will merge the city’s two major newspaper groups, the Jiefang Daily Group and Wenhui Xinmin United Press Group.

– Wal-Mart Stores is looking to close 15-30 underperforming stores in China.

SHANGHAI DAILY

– Competition and protectionism have caused Japanese dairy manufacturer Meiji to quit the China infant formula market. Meiji was forced to slash prices by regulators during an anti-monopoly campaign.

CHINA DAILY

– China’s industrial recovery remains weak, said an official with the Ministry of Industry and Information Technology.

– Agricultural Bank of China plans to offload non-performing assets valued 10 billion yuan ($1.64 billion) on the Beijing Financial Assets Exchange.

PEOPLE’S DAILY

– China’s urban employment increased by 10.66 million people during the first nine months, hitting the 9 million target for the year ahead of schedule.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

Advance Auto Parts (AAP) upgraded to Outperform from Sector Perform at RBC Capital

Amazon.com (AMZN) upgraded to Strong Buy from Market Perform at Raymond James

CYS Investments (CYS) upgraded to Neutral from Underperform at BofA/Merrill

Career Education (CECO) upgraded to Outperform from Market Perform at Wells Fargo

Columbia Sportswear (COLM) upgraded to Neutral from Sell at Citigroup

DuPont (DD) upgraded to Buy from Neutral at Citigroup

Forest Labs (FRX) upgraded to Market Perform from Underperform at BMO Capital

ITT Educational (ESI) upgraded to Neutral from Sell at Compass Point

ITT Educational (ESI) upgraded to Neutral from Underweight at JPMorgan

Knightsbridge Tankers (VLCCF) upgraded to Equal Weight from Underweight at Evercore

Monolithic Power (MPWR) upgraded to Outperform from Perform at Oppenheimer

Sierra Bancorp (BSRR) upgraded to Market Perform from Underperform at Raymond James

Downgrades

Caterpillar (CAT) downgraded to Neutral from Overweight at Atlantic Equities

Coca-Cola Enterprises (CCE) downgraded to Hold from Buy at Societe Generale

Credit Suisse (CS) downgraded to Neutral from Overweight at JPMorgan

Eastman Chemical (EMN) downgraded to Neutral from Conviction Buy at Goldman

Hill-Rom (HRC) downgraded to Market Perform from Outperform at Wells Fargo

ICON plc (ICLR) downgraded to Market Perform from Strong Buy at Raymond James

Landstar System (LSTR) downgraded to Neutral from Outperform at Credit Suisse

NCR Corp. (NCR) downgraded to Neutral from Buy at Compass Point

PAREXEL (PRXL) downgraded to Neutral from Outperform at RW Baird

Patterson-UTI Energy (PTEN) downgraded to Hold from Buy at Wunderlich

Plexus (PLXS) downgraded to Underperform from Neutral at BofA/Merrill

Rayonier (RYN) downgraded to Market Perform from Outperform at Raymond James

Rayonier (RYN) downgraded to Neutral from Buy at BofA/Merrill

Rayonier (RYN) downgraded to Sell from Hold at Deutsche Bank

Reliance Steel (RS) downgraded to Neutral from Outperform at Credit Suisse

STMicroelectronics (STM) downgraded to Neutral from Buy at Goldman

Sandridge Mississippian Trust (SDT) downgraded to Underperform at Raymond James

Sirius XM (SIRI) downgraded to Neutral from Buy at Goldman

Susquehanna (SUSQ) downgraded to Market Perform from Outperform at FBR Capital

Susquehanna (SUSQ) downgraded to Neutral from Outperform at Credit Suisse

Susquehanna (SUSQ) downgraded to Underperform from Market Perform at Raymond James

Taubman Centers (TCO) downgraded to Neutral from Overweight at JPMorgan

Texas Capital (TCBI) downgraded to Market Perform from Outperform at Keefe Bruyette

Timken (TKR) downgraded to Neutral from Buy at BofA/Merrill

Union First (UBSH) downgraded to Market Perform from Outperform at Keefe Bruyette

United Continental (UAL) downgraded to Underweight from Neutral at JPMorgan

Zimmer (ZMH) downgraded to Neutral from Outperform at RW Baird

Initiations

21st Century Fox (FOXA) initiated with an Outperform at FBR Capital

Actavis (ACT) initiated with a Buy at Citigroup

DISH (DISH) initiated with an Underperform at FBR Capital

DirecTV (DTV) initiated with a Market Perform at FBR Capital

Discovery (DISCA) initiated with an Outperform at FBR Capital

Disney (DIS) initiated with an Outperform at FBR Capital

Hannon Armstrong (HASI) initiated with a Sector Perform at RBC Capital

Kythera (KYTH) initiated with a Buy at BofA/Merrill

Mylan (MYL) initiated with a Neutral at Citigroup

NGL Energy Partners (NGL) initiated with an Outperform at Raymond James

Netflix (NFLX) initiated with a Market Perform at FBR Capital

Starz (STRZA) initiated with a Market Perform at FBR Capital

Teva (TEVA) initiated with a Buy at C

itigroup

TiVo (TIVO) initiated with a Market Perform at FBR Capital

Time Warner (TWX) initiated with an Outperform at FBR Capital

Vermilion Energy (VET) initiated with a Neutral at Goldman

Viacom (VIAB) initiated with an Outperform at FBR Capital

HOT STOCKS

Disney (DIS) to build its largest Disney Store in Shanghai, China

Microsoft (MSFT) CFO said corporate PC demand better than expected, Bloomberg reports

DuPont (DD) to spin-off Performance Chemicals segment

Omnicare (OCR) to pay U.S. $120M to settle False Claims Act suit

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Callaway Golf (ELY), Superior Energy (SPN), Validus (VR), Flowserve (FLS), QLogic (QLGC), KLA-Tencor (KLAC), CA Technologies (CA), NetSuite (N), Western Digital (WDC), NCR Corp. (NCR), Maxwell (MXWL), VeriSign (VRSN), Chubb (CB), Regal Entertainment (RGC), Wynn Resorts (WYNN), Zynga (ZNGA), Microsoft (MSFT), Deckers Outdoor (DECK)

Companies that missed consensus earnings expectations include:

Santander Chile (BSAC), Cliffs Natural (CLF), ResMed (RMD), KBR (KBR), Delta Apparel (DLA), DeVry (DV), BJ’s Restaurants (BJRI), Sterling Financial (STSA),

Companies that matched consensus earnings expectations include:

Cabot Oil & Gas (COG), Express Scripts (ESRX), Cerner (CERN), Amazon.com (AMZN), Netgear (NTGR)

NEWSPAPERS/WEBSITES

SYNDICATE

Aerie Pharmaceuticals (AERI) 6.72M share IPO priced at $10.00

Alcobra (ADHD) 2M share Secondary priced at $16.50

Canadian Pacific (CP) announces sale of 5.97M shares by Pershing

CommScope (COMM) 38.462M share IPO priced at $15.00

Dynavax (DVAX) to offer common stock

Endurance (EIGI) 21.051M share IPO priced at $12.00

Fidelity National (FNF) 17.25M share Secondary priced at $26.75

Horsehead Holding (ZINC) 5.5M share Secondary priced at $12.00

Institutional Financial (IFMI) files to sell 6.84M shares of common stock

Sorrento Therapeutics (SRNE) 4.15M share Secondary priced at $7.75

Sprague Resources (SRLP) 8.5M share IPO priced at $18.00

Twitter (TWTR) sees IPO price range $17-$20 on 70M shares

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Doxk1m-TfnM/story01.htm Tyler Durden