For a few hours it seemed like we could even stabilize, if only a bit, ahead of today’s scheduled main event: the March jobs report at 8:30am ET. And then all hell broke loose at 6:08am when this Bloomberg headline hit:

- *CHINA ANNOUNCES EXTRA 34% TARIFFS ON US GOODS

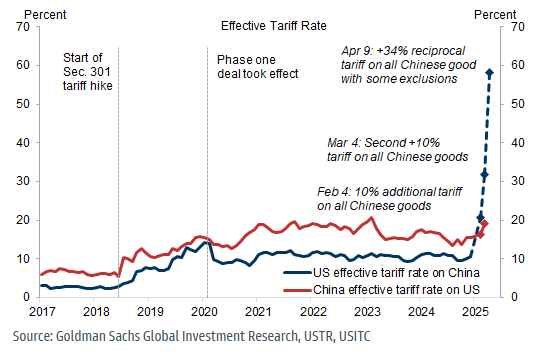

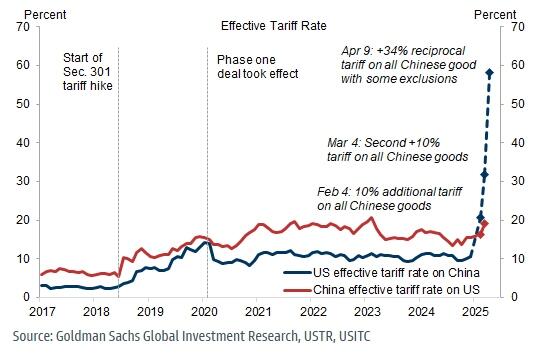

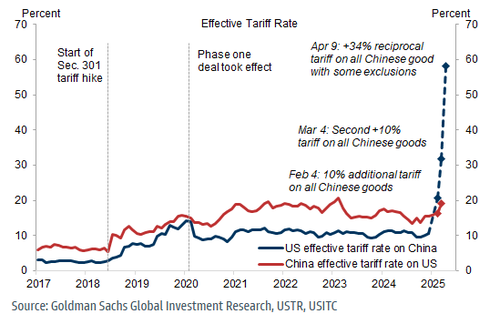

In other words, far from seeking concessions, Beijing is now looking to escalate the trade war further, and forcing Trump to double down with even harsher retaliatory tariffs on China of his own, which at this point may push the blended tariff rate on Chinese goods above 100%.

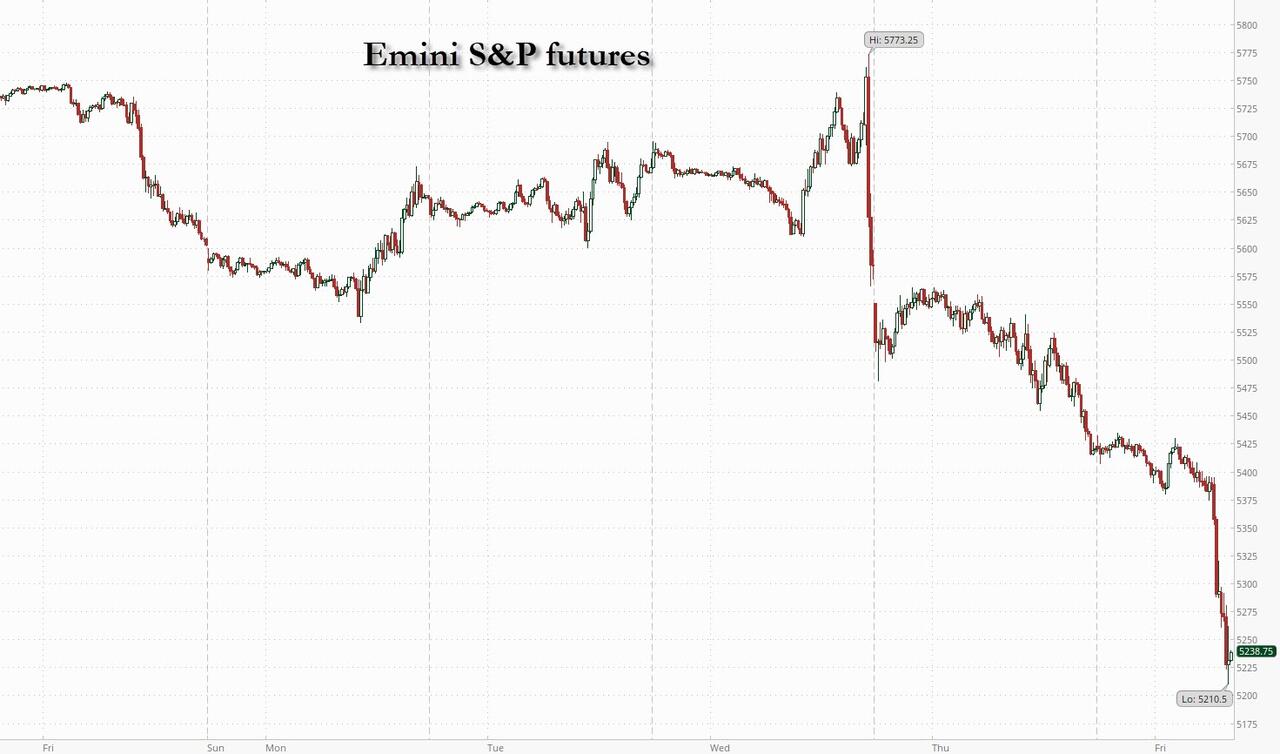

What followed instantly was sheer, unadulterated liquidation panic:

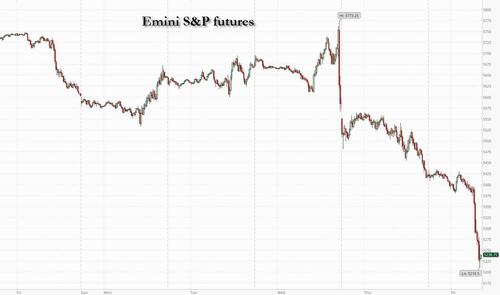

- *S&P 500 FUTURES DECLINE 4.1%, NASDAQ 100 FUTURES DOWN 4.6%

- *COPPER PLUNGES MORE THAN 5%, BIGGEST LOSS SINCE JULY 2022

- *US 2-YEAR YIELD FALLS TO 3.498%, LOWEST SINCE SEPTEMBER 2022

- *BRENT OIL DROPS BELOW $65 FOR FIRST TIME SINCE AUGUST 2021

- *US CREDIT RISK GAUGE JUMPS MOST SINCE REGIONAL BANKING CRISIS

- *STOXX EUROPE 600 INDEX FALLS 5.2%, MOST SINCE MARCH 2020

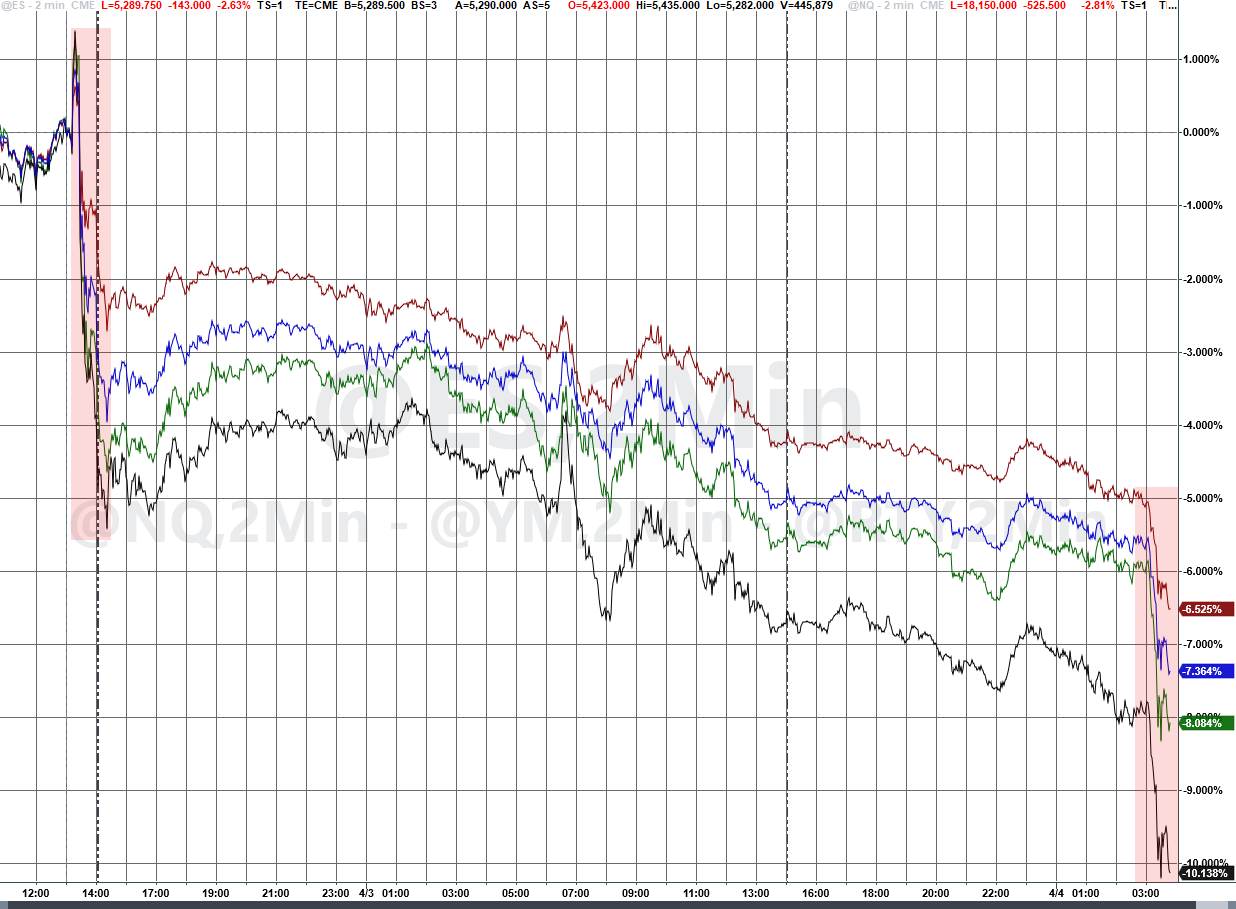

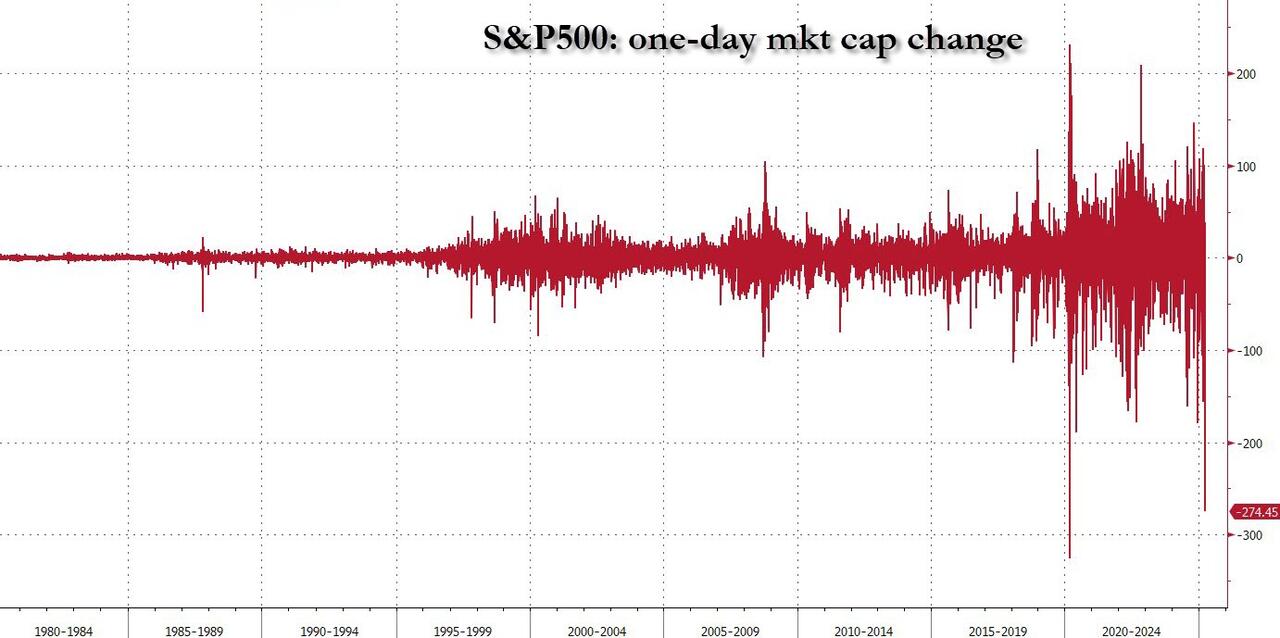

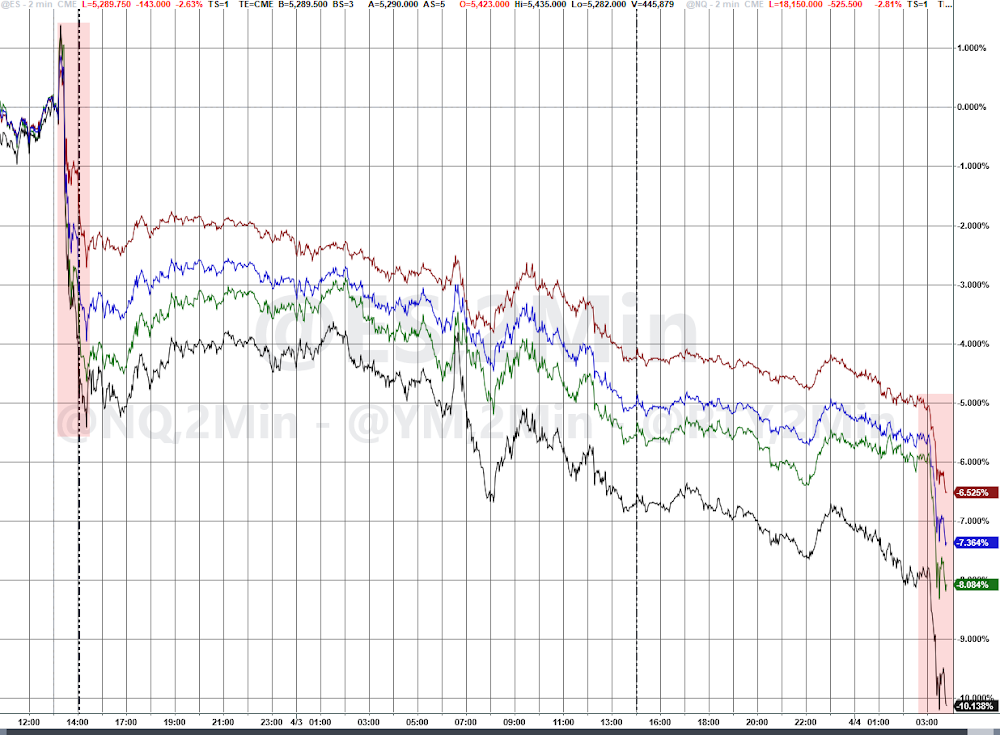

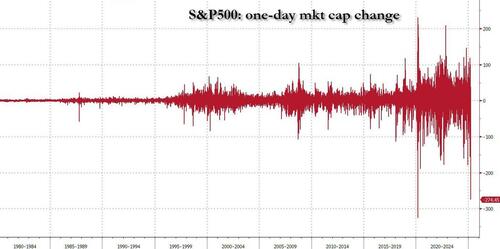

Instead of writing, we’ll let the charts do the talking, summarizing the bloodbath so far. The S&P is set to record losses on six of the past seven weeks.

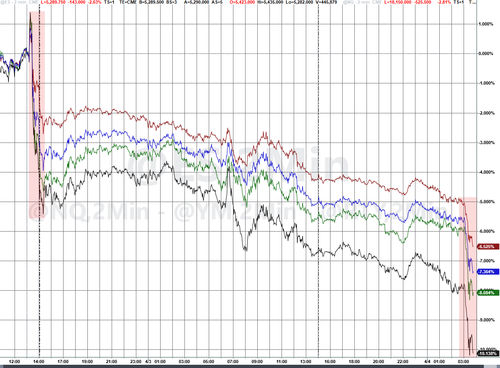

Volatility has come roaring back as VIX explodes above 45. A continuation of the selloff on Friday — when the government’s jobs report for March is released — threatens to extend Fund managers yanked $4.7 billion out of US stocks in the week through April 2 in the second week of outflows, data compiled by EPFR Global and Bank of America show.

The post-liberation day market has been a historic bloodbath

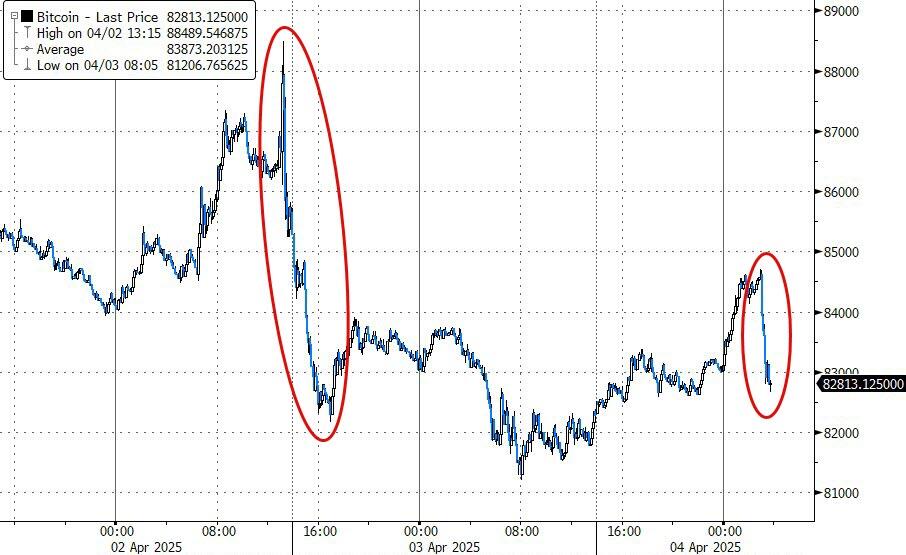

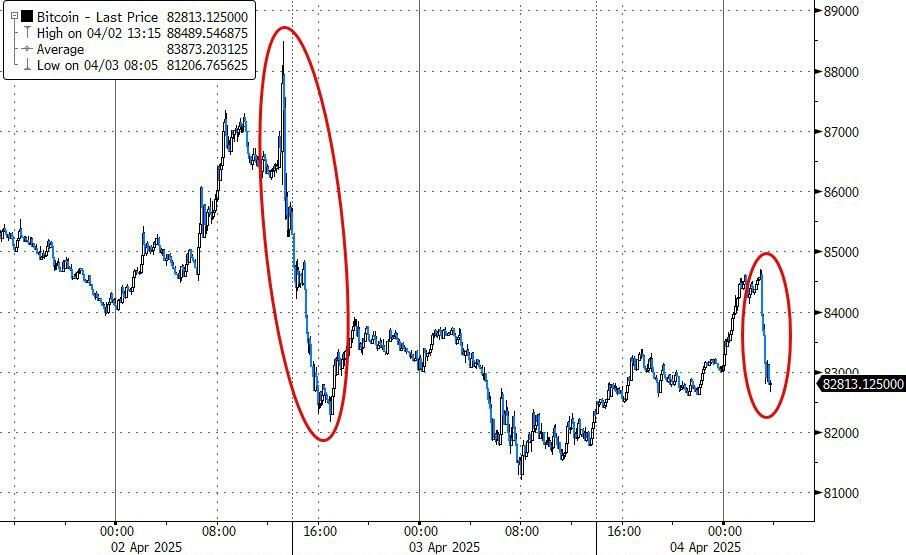

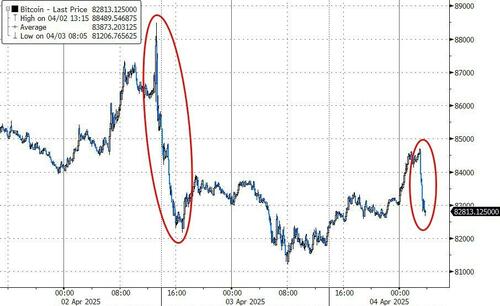

Bitcoin reversed all modest overnight gains, but remains surprisingly resilient.

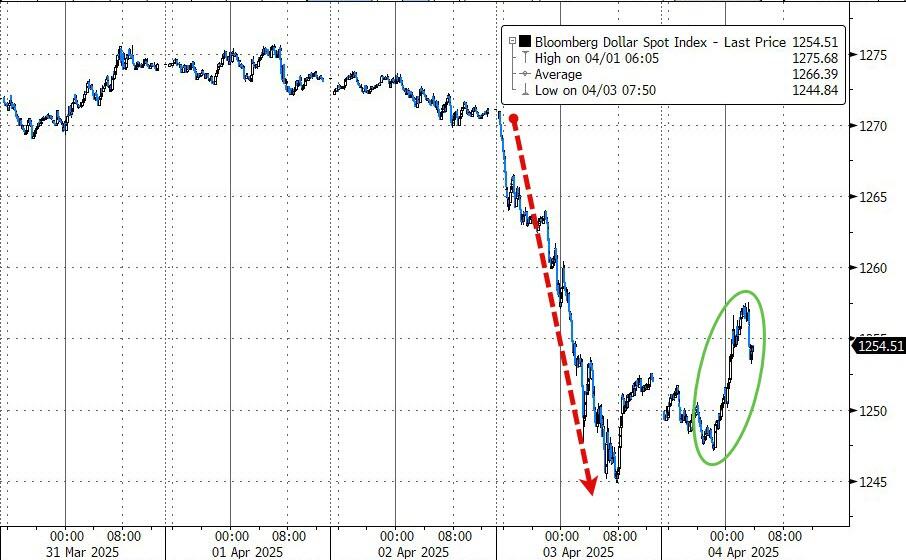

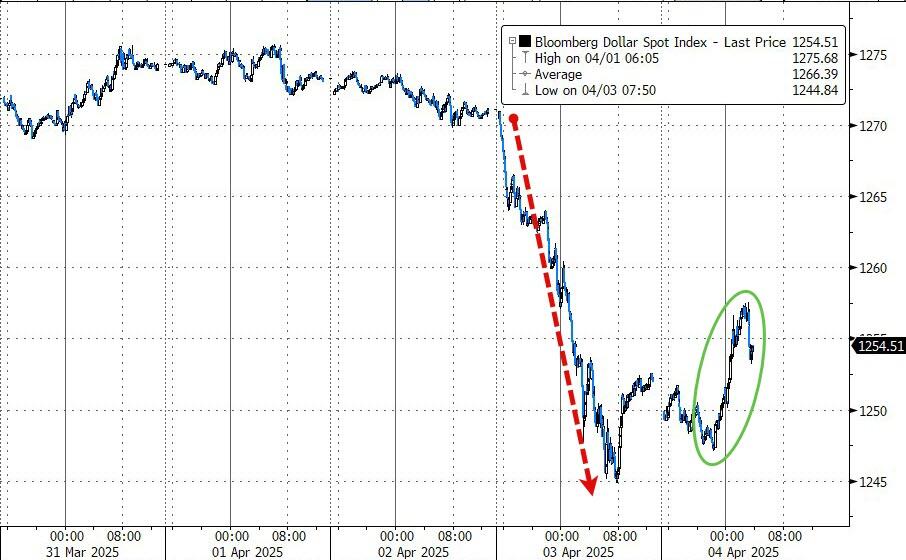

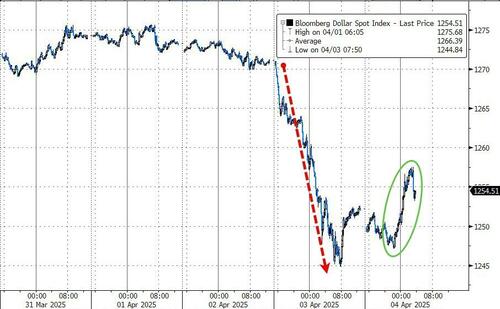

The dollar’s modest reversal higher was promptly halted, and the greenback reversed just as it was gaining.

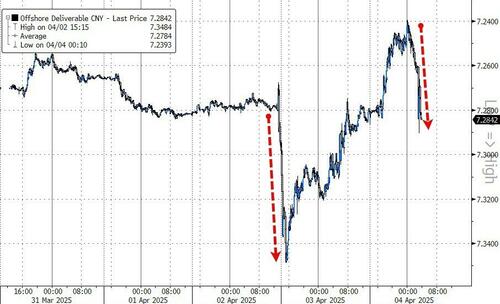

It wasn’t just the dollar: the yuan also tumbled, reversing its bizarre gains since Trump declared trade war on China.

“The market is bleeding and more pain is clearly coming as this escalating trade war risks pushing the US economy into a recession,” Luca Paolini, chief strategist at Pictet Asset Management said over the phone. “It’s not a surprise China would retaliate. But this will inevitably cause a recession because the damage is done — unless Trump backs off.”

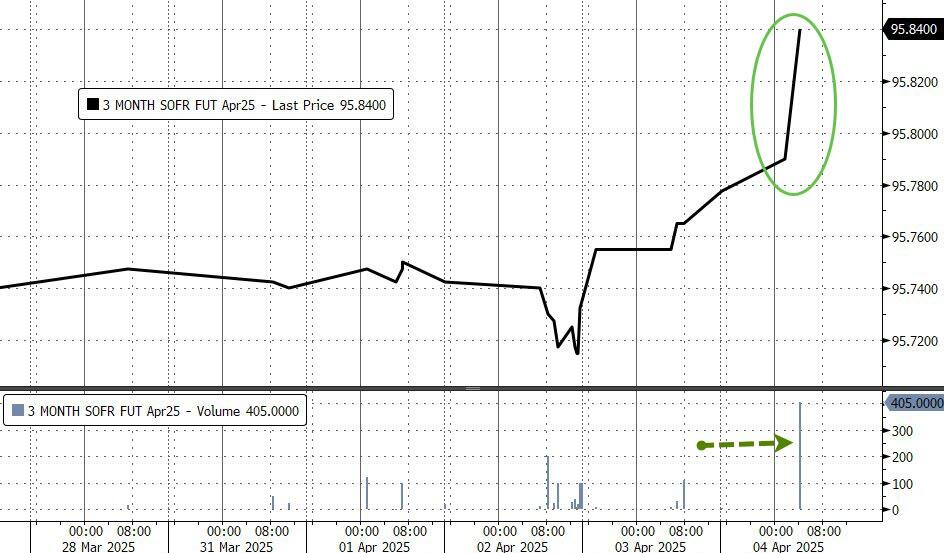

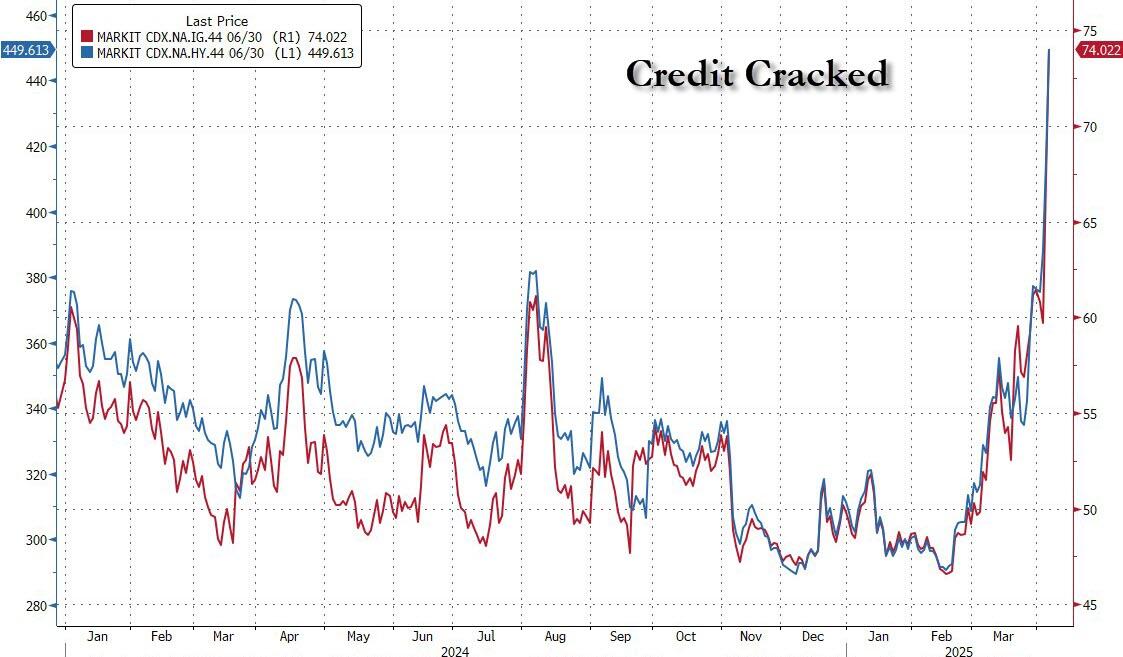

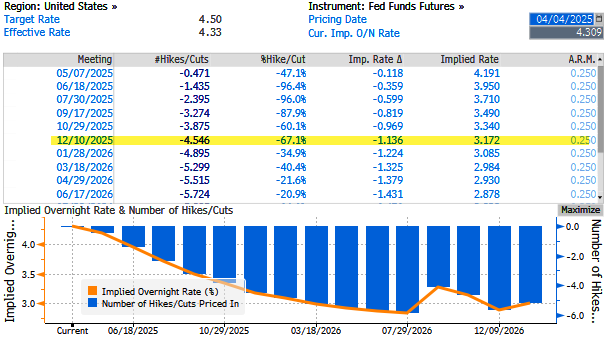

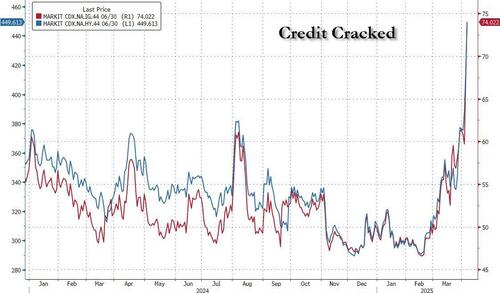

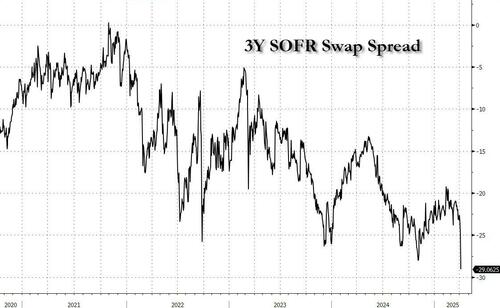

Well, there is an alternative: an emergency rate cut by the Fed, which now looks increasingly likely, because credit has officially cracked..

… but worse, the 3Y SOFR swap spread, a metric of Treasury market stress is the lowest on record.

Friday’s losses follow a massive wipe out by US stocks on Thursday that erased $2.7 trillion in value – the second biggest one day loss in history – in the wake of Trump’s drastic new trade tariffs which ignited widespread recession fears.

In a few minutes, investors will get a look at the latest monthly jobs print — the first major piece of data for the quarter — which could have wide-ranging implications for bond, stock and currency markets as well as the Fed’s next moves. Jerome Powell is scheduled to deliver remarks at 11:25 a.m. in Arlington, Virginia, which will be parsed for signs of weakness spreading to the workforce.

The derivatives market is pricing in more volatility ahead. Options traders are betting that the S&P 500 will move roughly 1.6% in either direction after the jobs print today, based on the price of at-the-money straddles, according to Citigroup Inc. That’s well above the average straddle price for a 0.9% swing in either direction over the past 12 months. It’s also well below what the market has already swung!

“How bad will it get for the economy? With so much uncertainty swirling, stocks are selling off and that’s signaling that investors see both economic and profit growth slowing because of the trade war,” Adam Sarhan, founder of 50 Park Investments said by phone.

Bloomberg reports that the equity rout now has Wall Street’s biggest stock bull, Oppenheimer’s John Stoltzfus, rethinking his 7,100 price target on the S&P 500, which is among the highest on Wall Street tracked by Bloomberg and would imply a 25% gain through Thursday’s close. That comes as RBC Capital Markets’s Lori Calvasina cut her price target on the index for a second time this year to 5,550 from 6,200, given a dimmer outlook for economic and profit growth.

“Without a doubt, where we’re sitting here it is under review and has been under review for awhile,” John Stoltzfus said on Bloomberg Television Friday. “The reality has been until we got these rather surprising unpleasant levels of tariffs and the market’s reaction, we’re naturally going to have to take a look and sharpen our pencils, so to speak.”

Treasuries added to steep weekly gains unleashed by unfolding trade war, sending 2-year yields to lowest level since September 2022, after China retaliated against US tariffs with measures including a 34% levy on all American imports. Yields across maturities are lower by at least 11bp led by the 2-year, down nearly 19bp and below 3.5%. Fed-dated OIS contracts price in additional easing, with 115bp anticipated by year-end and about 50% odds of move in May. US session includes March jobs report and a speech by Fed Chair Powell at 11:25am New York time. US 10-year yield, around 3.89% near session low, is richer by 15bp on the day, more than 40bp on the week, and 100bps since January; bunds outperform by an additional 2bp in the sector while gilts trade broadly in line. Front-end-led gains — as more Fed easing is priced in — extend the steepening in 2s10s and 5s30s curves by nearly 3bp and 6bp on the day

More stuff is happening, but honestly it is meaningless to go over everything since prices are moving at a furious pace and everything will be stale as soon as we write about it, and certainly after the jobs report is published.

US economic calendar includes March jobs report at 8:30am. Fed speaker slate includes Chair Powell at 11:25am on the economic outlook, with text release and Q&A expected. Barr (12pm) and Waller (12:45pm) also speak

Market Snapshot

- S&P 500 mini -2.9%

- Nasdaq 100 mini -3.1%

- Russell 2000 mini -4.1%

- Stoxx Europe 600 -5%

- 10-year Treasury yield -12 basis points at 3.91%

- VIX +14 points at 44

- Bloomberg Dollar Index +0.2% at 1254.8,

- Euro +0.1% at $1.1055

- WTI crude -4% at $64.15/barrel

Top Overnight News

- Trump administration officials are assuring farm-state Republicans they will funnel billions of taxpayer dollars to farmers who are hit by Trump’s intensifying trade war. But it may be some time before any money is released. The administration wants to take stock of the economic fallout of the tariffs in the agriculture sector before rolling out aid, which will likely take several more months. Politico

- While there have been expressions of displeasure, Republicans (who could use their own votes to stop the new tariffs cold) made clear they had no intention of acting anytime soon. “I think most members on our side are very willing to give the president time,” Arkansas Sen. John Boozman said, summing up the view of many GOP lawmakers who might have qualms about Trump’s massive new levies but showed little interest — at least for now and the near future — in doing anything concrete to restrain him. Politico

- President Donald Trump on Thursday contradicted his top aides on the purpose of his sprawling new global tariff regime, adding to the uncertainty over the trade war that has sent markets reeling. Earlier in the day, top Trump aide Peter Navarro and Commerce Secretary Howard Lutnick said the president was not looking to strike deals over the tariffs. “This is not a negotiation,” Navarro told CNBC. But after markets closed down sharply, Trump told reporters on Air Force One that he would be open to striking deals with individual countries. WaPo

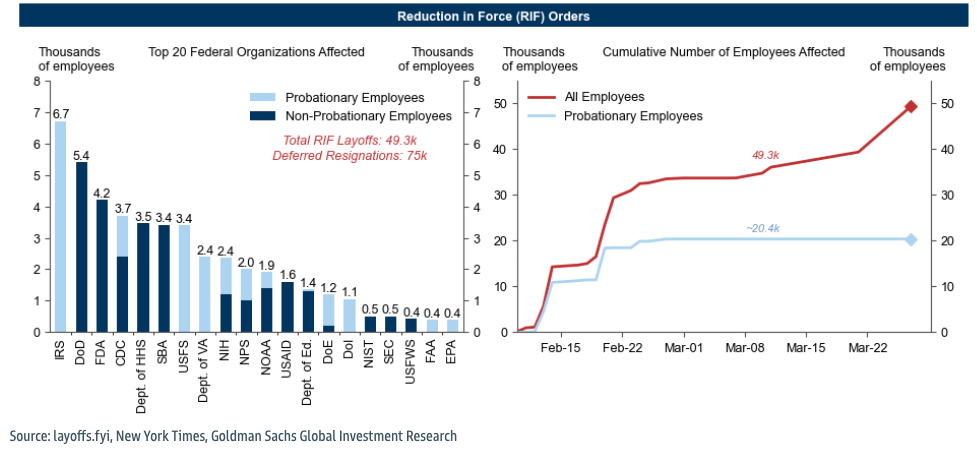

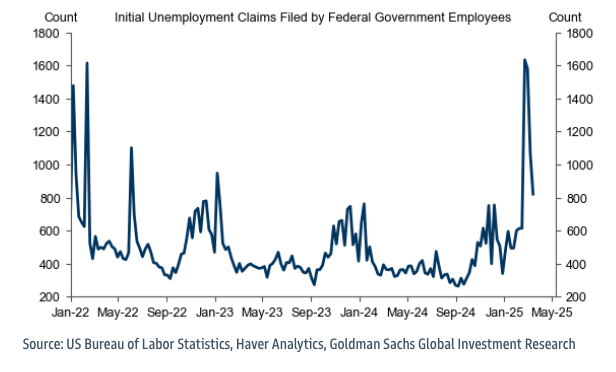

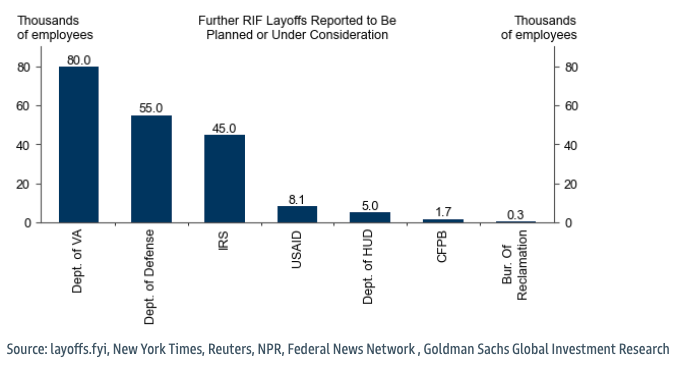

- US Social Security faces thousands more job cuts. The Social Security Administration is drafting plans to begin layoffs of potentially thousands more employees as soon as next week: WaPo

- Republicans are weighing the creation of a new bracket for those earning $1 million or more to offset some of the costs of their tax bill, a stark departure from decades of GOP opposition to tax increases. BBG

- China retaliated against the new US tariffs, announcing a 34% levy on all American imports starting April 10. Earlier, Donald Trump said he’s open to negotiations if other nations can offer something “phenomenal.” BBG

- President Trump’s jumbo tariffs on China threaten to create a new problem for a global economy already stressed over trade: a $400 billion deluge of Chinese goods looking for new markets. WSJ

- Japanese PM Shigeru Ishiba will meet opposition leaders today to discuss responses to the tariffs, which he said should be called a “national crisis.” BOJ Governor Kazuo Ueda said the US’s move will weigh on growth. BBG

- Traders now see the Fed cutting 100 bps by year-end, with a 50% chance of a cut in May. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks resumed the post-Liberation Day selling after Wall St suffered its worst loss since 2020, while fresh drivers are light amid the Greater China holiday closures and with participants now awaiting US jobs data. ASX 200 re-entered correction territory with the declines led by heavy losses in tech and energy in which the latter was pressured after oil prices fell by around 7% amid tariff turmoil and news that OPEC+ decided to increase output by a larger-than-scheduled 411k barrels per day in May. Nikkei 225 sold off again and fell below the USD 34,000 level with better-than-expected Household Spending data doing little to spur a recovery. KOSPI was initially choppy but ultimately weakened after the Constitutional Court upheld President Yoon’s impeachment which sparked some angry protests and triggered an election to be held within 60 days.

Top Asian News

- BoJ Governor Ueda said US tariffs are likely to exert downward pressure on Japan and global economies, while he added it is hard to say now how US tariffs will affect Japan’s price moves and they will closely monitor US tariff impact on Japan, overseas economic and price developments in deciding monetary policy. Ueda said they will scrutinise data, including from hearings, available at the time of each policy meeting to gauge the US tariff impact on Japan’s economy and prices.

- BoJ Deputy Governor Uchida said they will raise interest rates if underlying inflation heightens against the background of continued improvements in the economy. Uchida said they will examine, without any preset idea if economic and price forecasts laid out in the quarterly report will be achieved, as well as scrutinise at each meeting economic, and price developments and risks including the impact from US tariffs.

- South Korean Constitutional Court ruled to oust impeached President Yoon with the decision made unanimously.

European bourses (STOXX 600 -2.1%) are entirely in the red, in a continuation of the Trump-tariff induced slump seen on Thursday. Price action has only really been downwards today, given the lack of fresh catalysts and with traders mindful of the key NFP report ahead. European sectors hold a strong negative bias, with only a couple of sectors managing to hold in positive territory. Food Beverage & Tobacco outperforms today, largely thanks to the defensive bias in the markets today. Banks continue to underperform, extending on the prior day’s losses; yields continue to drive lower, and fears of an economic slowdown continue to increase.

Top European News

- UK government said almost GBP 14bln of R&D funding is allocated to bolster life sciences, green energy, space and beyond to improve lives and grow the economy.

- Goldman Sachs cuts the UK’s 2025 GDP growth forecast to 0.7% (prev. 0.8%).

- Deutsche Bank says the latest US tariffs could hit Europe and the UK’s GDP by 0.4-0.7% percentage points and 0.3-0.6 percentage points respectively.

DXY

- DXY is on a firmer footing, after initially edging lower in overnight/early European trade. Yesterday was a woeful session for the USD on account of concerns over the US’ growth outlook post-tariffs with the DXY falling from an opening level at 103.37 to a trough at 101.26. Trade specific updates since have been relatively light, so focus today will be on US NFP and then Fed Chair Powell thereafter.

- EUR/USD has been weighed on in recent trade by the pickup in the USD but is still firmly above yesterday’s opening level @ 1.0848. Analysts at ING attribute the recent resilience in the EUR not to a positive reappraisal of the Eurozone’s growth outlook but more as a result of the “alternative liquidity offered by the euro”.

- JPY is marginally softer vs. the USD and faring better than peers on account of the JPY’s safe-haven appeal. BoJ speak overnight saw Governor Ueda remark that US tariffs are likely to exert downward pressure on Japan and global economies, however, it is hard to say now how US tariffs will affect Japan’s price moves. Elsewhere, Deputy Governor Uchida noted that rates will be raised if underlying inflation heightens against the background of continued improvements in the economy. USD/JPY has made its way back onto a 146 handle but is still far away from yesterday’s opening level at 149.21.

- After a solid showing vs. the USD yesterday which sent Cable from a 1.2968 base to a 1.3207 peak, the recent resurgence of the Dollar briefly sent the pair back onto a 1.29 handle with a session low at 1.2976.

- Antipodeans underperform today after seeing slight gains in the prior session. Gains yesterday were limited by the high-beta status of both currencies, which is the main driver of today’s underperformance as internal macro drivers for Australia and New Zealand remain light.

Fixed Income

- USTs continue to advance as the risk tone remains downbeat and has deteriorated further in the European morning. Bringing USTs to a 113-12+ peak, weighing on yields across the curve with the belly/10yr once again lagging. Trade updates have been relatively light since “Liberation Day”, but President Trump suggested that the onus is on partners to bring him something “phenomenal”. US NFP is on the docket and then focus turns to Fed Chair Powell thereafter.

- Bunds are already getting on for gains of 100 ticks on the day with Payrolls and Powell yet to print. Initial action was modest in nature, with overnight focus primarily on Japan as JGBs played catchup to Thursday’s moves and BoJ bets were altered to show just 13bps of tightening implied for the rest of 2025. Peaked at 130.75 thus far with gains of 163 ticks WTD.

- Gilts are also moving higher alongside peers. Upside of 104 ticks at most so far, higher by over 230 ticks on the week and around 350 above the low from last Wednesday’s Spring Statement.

Commodities

- Crude continues its recent slump with WTI and Brent currently down by around USD 2.60/bbl and USD 2.50/bbl respectively. There has been little fresh fundamental in today’s trade, but pressure is ultimately a factor of a) negative risk tone. b) fears of slowing economic growth. c) OPEC+ decided to increase output by a larger-than-scheduled 411k barrels per day in May. Brent Jun’25 currently at the lower end of a USD 67.53-70.11/bbl range.

- Precious metals are on the backfoot today, with spot silver underperforming vs gold. Specifically for the yellow-metal, price action was rangebound overnight and remained within overnight ranges for most of the European morning, before then succumbing to some modest selling pressure alongside a broader pick-up in the Dollar. Currently trading around USD 3,090/oz in a USD 3,078.60-3,116.67/oz range.

- Base metals are entirely in the red, given the risk tone and in a continuation of the recent slump across the commodity complex; a holiday in China, is also a factor for the downside today.

Geopolitics: Middle East

- Israeli military say they have “eliminated” Hassan Farhat, a Hamas commander in Lebanon

- Israeli media reported that the Israeli army launched raids on large areas in the Gaza Strip, according to Al Jazeera

- Houthi-affiliated media reports US aggression on the Kahlan area, east of Saada city, northern Yemen, according to Al Jazeera.

- Iran reportedly abandons Houthis under relentless US bombardment and ordered its military personnel to leave Yemen, according to The Telegraph.

- US President Trump said he spoke with Israeli PM Netanyahu on Thursday who may visit the US next week, although it was separately reported that Israeli PM Netanyahu’s visit to the White House will likely take place in a few weeks.

- Turkey said Israel’s attacks on regional countries have made Israel the biggest threat to regional security, while it added that Israel is a regional destabiliser and is feeding chaos and terror.

- Saudi Crown Prince received a phone call from Iran’s President during which they discussed developments in the region and issues of common interest.

Geopolitics: Ukraine

- US President Trump’s inner circle advises against a call with Russian President Putin until he commits to a full ceasefire.

- Russian envoy Dmitriev said lots of differences remain, but a diplomatic solution is possible and there is already some progress on trust-building measures, while he sees a positive dynamic in US-Russian relations and said Several meetings are needed to sort out differences. Dmitriev also stated that a long-term solution that takes into account Russian security concerns is what is needed, as well as commented that they are not asking for a lifting of sanctions and that they can do a deal with the US on rare earths.

- Moscow’s mayor said Russian air defences repelled drones approaching Moscow and specialists are examining fallen fragments.

US Event Calendar

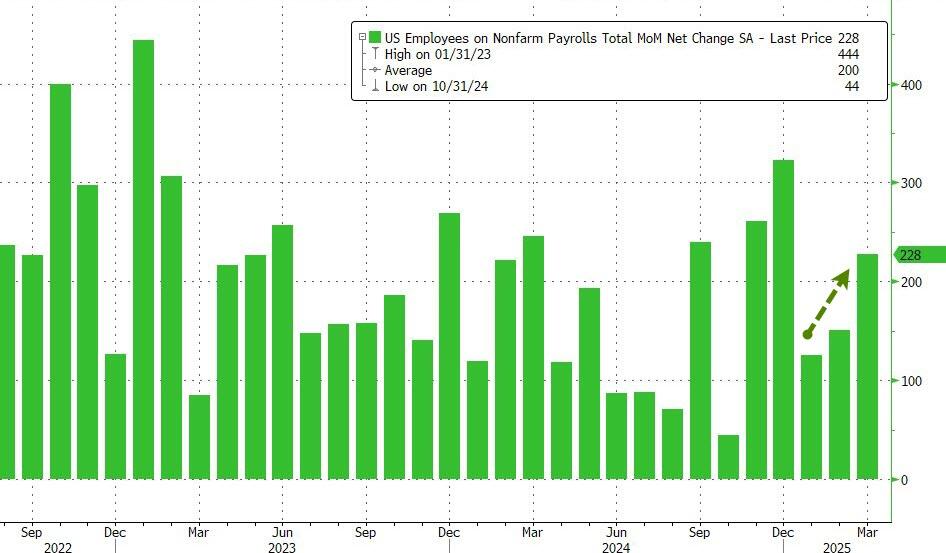

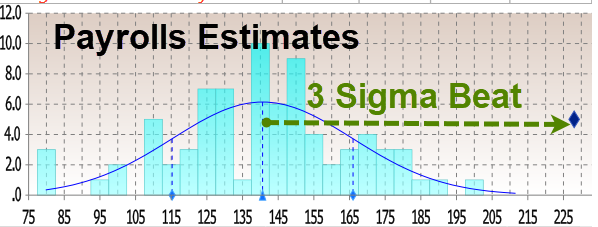

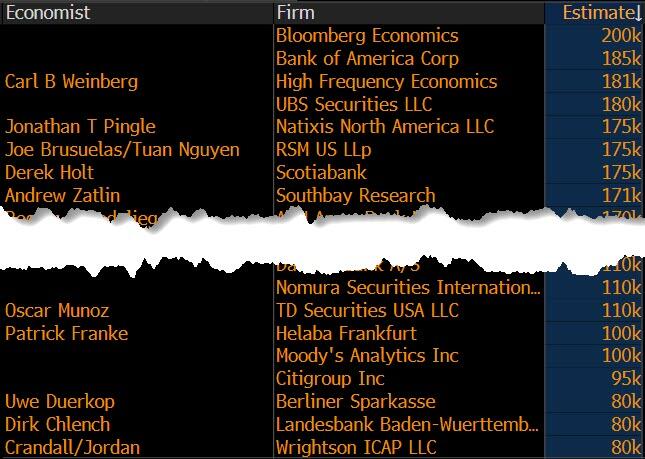

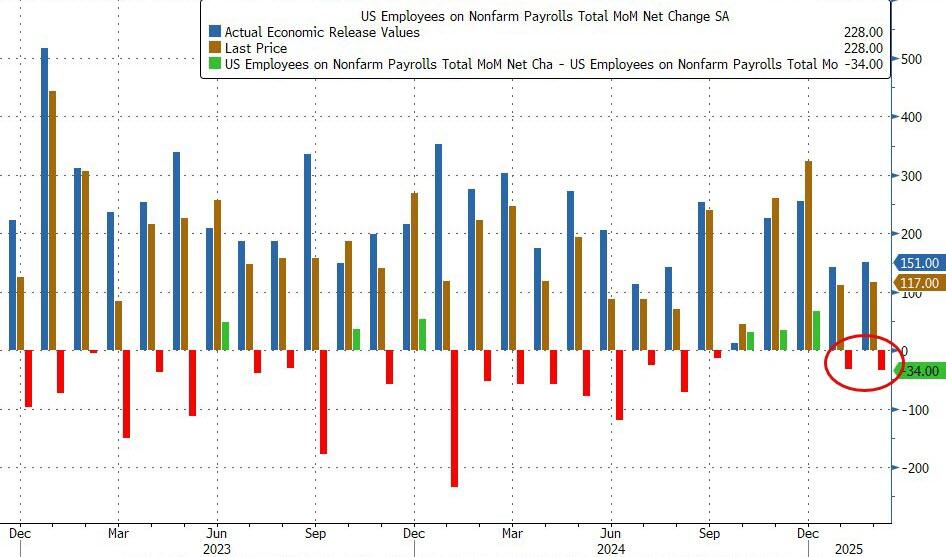

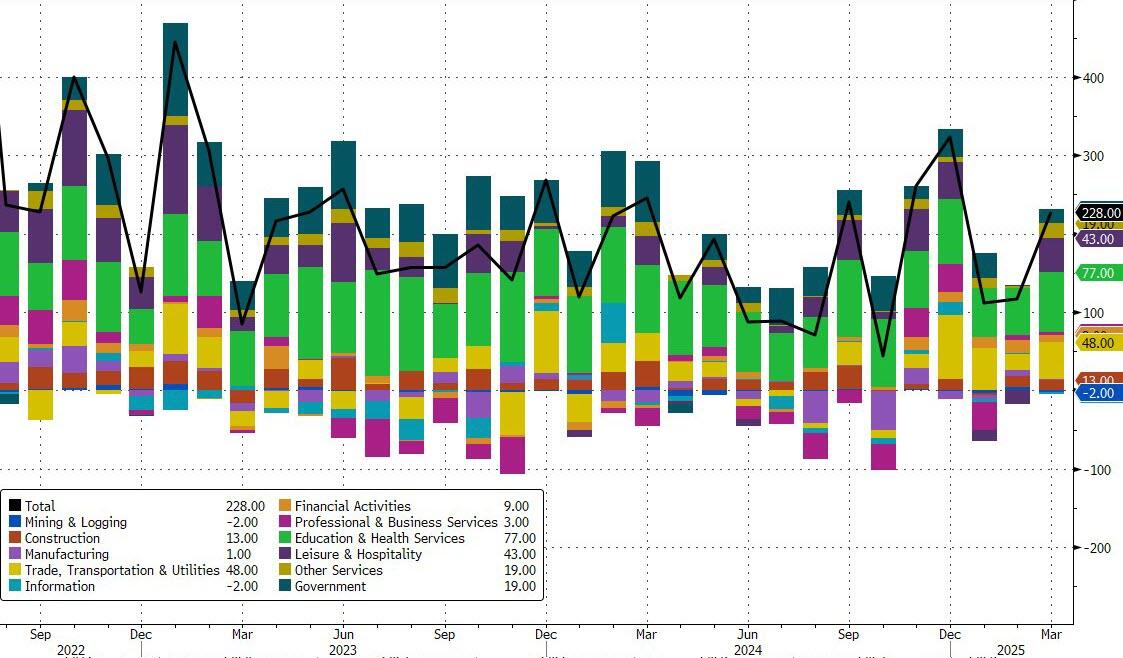

- 8:30 am: Mar Change in Nonfarm Payrolls, est. 140k, prior 151k

- 8:30 am: Mar Change in Manufact. Payrolls, est. -1k, prior 10k

- 8:30 am: Mar Unemployment Rate, est. 4.1%, prior 4.1%

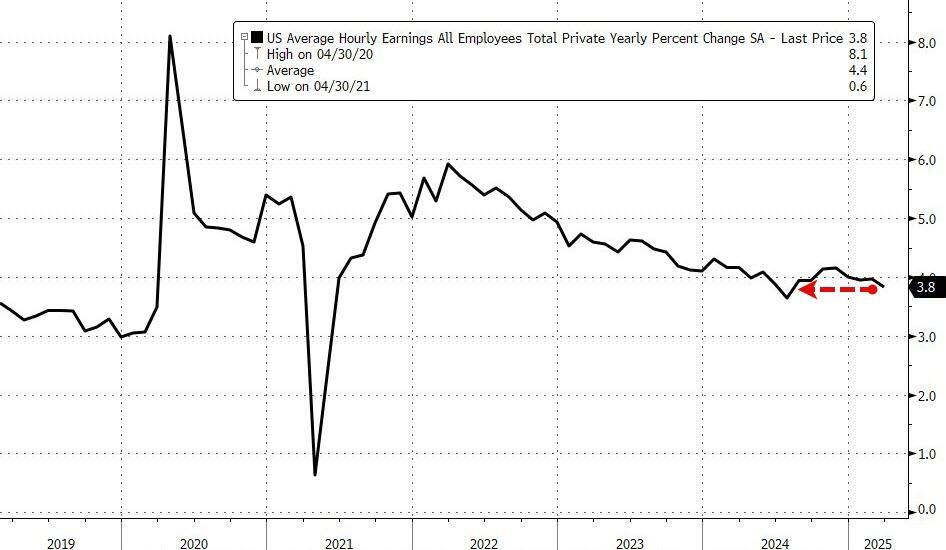

- 8:30 am: Mar Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

- 8:30 am: Mar Average Hourly Earnings YoY, est. 4%, prior 4%

DB’s Jim Reid concludes the overnight wrap

The last 24 hours have been truly historic for markets, as the impact of the US reciprocal tariffs cascaded across different asset classes, with no sign of letting up overnight. We’ll dive into more depth shortly, but just to run through some of the moves, yesterday saw the S&P 500 fall -4.84%, marking its biggest daily decline since June 2020, with futures down another -0.74% this morning. In turn, that took the peak-to-trough decline for the S&P 500 beyond 12%, meaning it’s now the biggest overall decline since the 2022 bear market. Otherwise, US HY spreads widened by +53bps yesterday, the biggest move wider since March 2020 at the height of the pandemic turmoil. The 10yr Treasury yield has fallen beneath 4% again, with futures fully pricing in a Fed rate cut by the June meeting. Both the dollar index (-1.67%) and Brent crude oil (-6.42%) suffered their worst days since 2022. And overnight, the 10yr Japanese government bond yield (-16.8bps) is on track for its biggest decline since 2003. So we’re currently experiencing some of the biggest moves in years right across the major asset classes.

Given the significance of the tariff announcement, here at Deutsche Bank Research we’ve been thinking through what this means for our global forecasts. Yesterday we provided an initial guide (link here) on how they’ll shift if the tariffs do hold, although clearly there’s still a lot up in the air, including the extent of any retaliation. For the US, the movement is stagflationary, and our economists think these could reduce the 2025 GDP forecast (Q4/Q4) from 2.2% to around or under 1%, with core PCE up from 2.7% to around 4%. So recession risks will likely rise materially if these tariffs are sustained. And when it comes to the Fed, they think the latest moves make them more likely to cut, even though the direction of travel is highly stagflationary, with the bias now towards up to four cuts this year if this tariff policy holds.

Meanwhile in Europe, our economists’ discuss their latest estimates in a report yesterday (link here). They estimate that the increase in US tariffs could knock 0.4-0.7pp off EU GDP, and that the EU will likely retaliate. Although the tariffs could complicate the easing trajectory for the ECB, they think they’re likely to continue cutting, and hold their terminal rate forecast of 1.50% at end-2025, with further rate cuts in April, June, September and December. They think the hit to growth will increase pressure on the ECB to cut rates, especially as the euro moved above $1.11 intraday yesterday for the first time in over 6 months.

In terms of what happens now, the big question is how the US’s trading partners might retaliate, as that will play a huge role in determining what the overall economic and market impact will be. For instance, French President Macron said yesterday that companies should pause their US investments, saying “What would be the message of having big European players that invest billions in the American economy at the same time they are hitting us”. Separately, it was announced by Canadian PM Market Carney that Canada would put 25% tariffs on US-made autos that don’t comply with the USMCA deal. At the same time, investors will be watchful of any potential deals to reduce tariffs, with Trump saying yesterday evening that “The tariffs give us great power to negotiate” but that other countries would have to offer something “phenomenal” in negotiations for him to relent. So no signs of any immediate relief.

On the back of all this, investors grew increasingly fearful about a potential US recession, with US equities seeing their sharpest decline in years. The S&P 500 (-4.84%) , the NASDAQ (-5.97%) and the small cap Russell 2000 (-6.59%) all saw their worst days since 2020, and there were as many as 74 companies in the S&P that fell by at least 10% yesterday. All that meant measures of volatility continued to spike, with the VIX index (+8.51pts) moving up to 30.02pts, its highest level since the turmoil last summer. And given mounting fears of a downturn, the more cyclical sectors drove the underperformance, with the Magnificent 7 (-6.67%) posting its worst day since July and extending the decline from its December peak to -24%. Meanwhile in Europe, the declines weren’t quite as bad, but even there the STOXX 600 (-2.57%) saw its biggest move lower since August.

Whilst growth fears were at the forefront yesterday, investors were also becoming a lot more concerned about inflation. In fact, the US 1yr inflation swap (+8.3bps) rose for a ninth session in a row to close at its highest level since 2022, back when the Fed were still hiking by 75bps per meeting to get inflation under control again. However, because of the growth fears, investors also priced in that the Fed would cut rates more aggressively over the months ahead. In fact as we go to press this morning, futures are now pricing over 100bps of rate cuts by the December meeting, and are fully pricing in an initial cut by the June meeting. They even see a 34% probability of a cut at the next meeting in May, so all eyes will be on Fed Chair Powell’s comments today to see his reaction.

With investors worried about the growth shock and pricing in more rate cuts, that helped sovereign bond yields to move lower across the curve, albeit with a very sharp steepening. For instance, the 2y Treasury yield (-17.8bps) fell back to 3.68%, and the 10yr yield (-10.1bps) fell to 4.03%, yet the 30yr yield (-3.0bps) saw a smaller decline to 4.47%. And over in Europe, there were also declines as investors priced in more ECB rate cuts, with yields on 10yr bunds (-7.0bps), OATs (-5.0bps) and BTPs (-4.3bps) all moving lower.

Over in the FX space, there was a huge depreciation in the US Dollar yesterday, with the dollar index (-1.67%) posting its biggest daily decline since 2022. That included a +1.83% move for the Euro, which closed at $1.1052, which is the first time it’s closed above $1.10 in six months. More broadly, our FX strategists are maintaining their bullish EUR/USD view, and George Saravelos warned yesterday (link here) that there’s an increasing concern that the dollar is at risk of a broader confidence crisis.

Amidst the huge market moves, sentiment wasn’t helped by the latest ISM services data, which came in beneath expectations in March. The headline index was down to a 9-month low of 50.8 (vs. 52.9 expected), and the employment component (46.2) slumped to its lowest since December 2023. That said, for now at least, the labour market hasn’t shown an obvious sign of deterioration, with the weekly initial jobless claims at 219k over the week ending March 29 (vs. 225k expected), which pushed the 4-week average down to 223k.

That focus on US data will continue today, as we’ve got the March jobs report coming out at 13:30 London time. Clearly it won’t account for the full impact of these reciprocal tariffs that are now coming, but it will be an important test as it’s one of the first hard data prints we have for the month of March. In terms of what to expect, our US economists are looking for nonfarm payrolls to come in at +150k, with the unemployment rate rounding up to 4.2%. You can see their full preview and register for their post-release webinar here. Later on today, we’ll then hear from Fed Chair Powell, who’s giving a speech on the economic outlook, so that will be heavily in focus to hear about how the Fed are thinking about tariffs and their reaction function. Ahead of that, we did hear from Fed Vice Chair Jefferson yesterday, who said “there is no need to be in a hurry to make further policy rate adjustments.

Overnight, this direction of travel has continued in markets, with sharp losses in Asia that built on yesterday’s moves. For instance, Japan’s Nikkei is down another -3.74%, on top of its -2.77% move yesterday. So as it stands, the index is down -9.93% for the week, which would be its worst weekly performance since the pandemic turmoil of March 2020. That comes amidst a sharp appreciation in the Japanese yen, which is currently at 145.62 per US dollar this morning.

Moreover, there’s been an astonishing move in Japan’s government bond yields, with the 10yr yield (-16.8bps) on track for its biggest daily decline since 2003. Meanwhile in Australia, the S&P/ASX 200 (-2.24%) has also built on its Thursday losses, leaving it on track for its worst weekly performance since 2022. And in South Korea, the KOSPI is down -1.71%. Equity markets in China are closed for a holiday.

To the day ahead now, and the main highlight will be the US jobs report for March. Other data includes German factory orders and French industrial production for February, along with the construction PMIs for March in Germany and the UK. Elsewhere, central bank speakers include Fed Chair Powell, along with the Fed’s Barr and Waller.