Earlier this week the State Department released its latest statistics for people who have renounced their US citizenship.

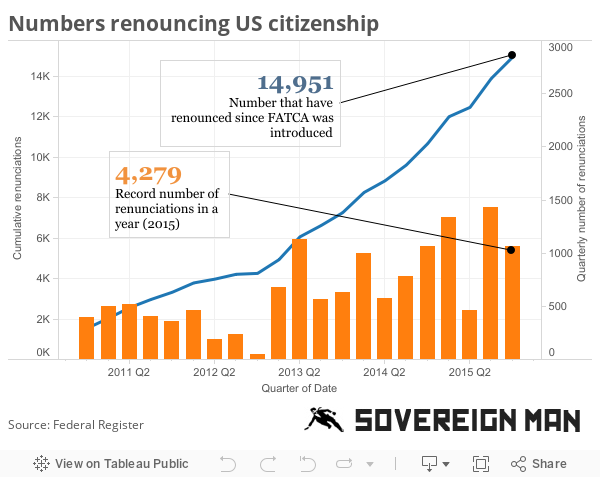

2015 was another record year, with 4,279 people divorcing themselves from the US government and heading to greener pastures elsewhere.

This was the third year in a row that broke the previous year’s record, showing that this is obviously a growing trend. The number one reason for which is quite simple: tax.

Many of these individuals were Americans already living overseas who are still subject to the pay taxes to the IRS on their worldwide income.

For 2015, the first $100,800 in earned income for Americans living abroad is generally tax free. However, higher income earners are still forced to pay their “fair share” of all the bombs, drones, and federal folly even though they don’t live in the United States.

Most countries don’t do this. If you’re Canadian, or French, or even Chinese and you move abroad you’re no longer subject to taxation in your home country presuming you earn your income overseas.

Americans living overseas are also subject to additional reporting requirements and IRS scrutiny due to the Foreign Account Tax Compliance Act (FATCA).

FATCA is an insane, extraordinarily narcissistic law that requires reporting both from individuals with foreign assets as well as from every financial institution on the planet.

Individuals living abroad are more likely to have foreign assets, so they’re disproportionately affected by the additional compliance.

For financial institutions abroad, the cost of implementing FATCA has been estimated by various foreign governments, banks, chambers of commerce, and financial media, at anywhere between $200 billion and more than $1 trillion.

Yet despite FATCA’s trillion-dollar price tag, the Wall Street Journal reports that the US government has taken in just $13.5 billion in revenue from hidden foreign accounts that FATCA is supposed to eliminate.

Obviously the cost vastly exceeds the benefit. It’s insane. Plus FATCA has driven nearly 15,000 Americans to renounce the citizenship since President Obama signed it into law in 2010.

These former Americans are often criticized for taking such a controversial step, one that is derided as being “unpatriotic”.

This criticism makes no sense when you take a larger view of history.

The State Department estimates that there are up to 6 million Americans living abroad.

Given the average size of a Congressional district at roughly 700,000 citizens, there should theoretically be eight members of Congress representing the interests of Americans living abroad.

Yet expats have no representation. There is not a single person in Congress fighting for expats, even though they are still subject to pay tax.

More than 240 years ago, residents of the colonies had a term for this. They called it “Taxation without Representation”. This idea is as old as America itself.

And in 1776, American colonists divorced themselves from the British government. Much of this was tax motivated.

In the Declaration of Independence, Thomas Jefferson expressly writes that among the reasons for independence is “imposing taxes on us without our consent.”

Former US citizens are following in these footsteps.

This is appropriate to point out, especially this year as voters in the Land of the Free delude themselves into believing that they’re going to choose their next leader.

This is total nonsense. As we discussed in this week’s podcast, the US electoral system is completely anachronistic, just like the monetary system, the banking system, etc.

This idea of having delegates, super-delegates, and the electoral college probably made sense in the election of 1788, when less than 2% of the US population was able to vote.

Today it no longer makes sense. It is an illusion of Republican Democracy. In reality your vote doesn’t count.

Let’s be honest about the world we’re living in. Particularly in politics, money counts more than anything.

If you really want to change anything, the most important ballots you can cast are with your money and with your feet.

By divorcing yourself from a government bent on indebting future generations in order to drop bombs by remote control on brown people across the world, you’re taking a conscious step to reduce their resources.

Your hard work and sweat no longer support debt, war, and freedom-killing regulations.

Renunciation is one step that many former Americans have taken to affect this change.

Understandably the idea is far too radical for most people. But there are still many completely legitimate steps that anyone can take to reduce the amount that you owe and starve the beast.

It’s a far more powerful option than punching a chad in a voting booth.

It’s a far more effective way to create “real change” than punching a chad in a voting booth.

from Sovereign Man http://ift.tt/20OqLJA

via IFTTT