Submitted by Charles Hugh-Smith of OfTwoMinds blog,

Longtime correspondent Jeff W. succinctly explains the difference between metallic money (gold and silver) and credit money.

You've probably read many articles about money–what it is (store of value and means of exchange) and its many variations (metal, paper, etc.). But perhaps the most important distinction to be made in our era is between metallic money and credit money.

Longtime correspondent Jeff W. succinctly explains the difference between metallic money (gold and silver) and credit money:

We use credit money every day. It’s the only kind of money we have. But because people in Europe and America have historically used metallic money for over 2,500 years, we still have cultural habits that come from the gold money era.

When the U.S. removed gold and silver coins from circulation in the 1930’s and 1960’s and replaced paper gold certificates and silver certificates with Federal Reserve notes, the paper money looked very much the same. But the thing that the paper money represented changed dramatically. The paper money now represents units of credit money that have no guaranteed relationship with the prices of gold or silve r or anything else.

Because the nature of credit money and metallic money are not well understood, and because money is so important in our lives, it is worthwhile to examine and discuss how these two kinds of money are different.

1. Tangible vs. intangible. A gold or silver coin is a physical object that has weight, volume and physical characteristics. Credit money is a record of the existence of a debt. Credit money exists in the intangible world of information and human relationships. Where Mr. A owes Mr. B a specified unit of money, and where that debt is recorded on paper or another recording medium, and where the record of that debt passes from one person’s possession to another as a medium of exchange, you have credit money.

Gold coins are minted; debts are recorded. The two forms of money could hardly be more dissimilar.

2. Old vs. oldest. Metallic money has been used by people for about 2,600 years. It has been used sporadically and in certain places. Credit money has been used for at least 5,000 years, when people first started recording debts on clay tablets, pieces of wood or ivory, etc., and trading those IOU’s as money. Before debts were recorded in writing, they were, in prehistoric times, discussed verbally, remembered, and sometimes traded in verbal transactions. This is how very primitive people still trade using debt today.

3. Persistent vs. ephemeral. Some gold coins more than 2,000 years old are still in existence today. But it would be very rare for any performing loans to be more than 100 years old, and many loans are of very short duration. Much of the U.S. Treasury’s debt issue is very short term, lasting only 90 days or one year. Where gold coins can last for thousands of years, debts are constantly coming into existence and going out of existence.

The U.S. debt holdings of the Federal Reserve are constantly churning and rolling over, whereas gold holdings in vaults can lie stationary and do not need to be replaced or rolled over.

4. Hard to create vs. easy to create. To create a gold coin, someone has to first mine the gold from the earth, refine it, mill it, stamp it into circular shapes and then stamp the governmental pattern on it. To create a piece of credit money, a debt has to be created and then a piece of paper printed or a record created on a computer. Anyone who has no intention of paying back his debt, such as the Federal government, can potentially issue debt in infinite amounts. There is an issue of whether that debt is worth anything, however.

5. Always good vs. sometimes good. A gold coin that is legal tender will always be accepted as money. With credit money, some of it is good and some of it is bad. In recent years Zimbabwe’s credit money went bad. Before that, the Weimar Republic’s credit money became worthless. All circulating debt has a mixture of good and bad. When a lot of it goes bad at the same time, it causes a crisis, where the “toxic debt” must be guaranteed or purchased by government or else banks and other financial institutions will go bankrupt.

6. Non-interest bearing vs. interest bearing. Most debt specifies interest payments as part of the loan agreement. The Federal Reserve notes we use as money are claims on interest-bearing debt owned by the Federal Reserve. Credit money has the quality that there is a continuing flow of interest payments away from the users of money in the general population and toward creditors. There is no such continued flow of wealth from debtors to creditors in a gold money system.

7. Does not need money supply expansion vs. needs expansion. Because interest payments are constantly flowing out from families, businesses and communities to financial centers and wealthy creditors, credit money results in economic sluggishness unless there is a constant expansion of the supply of credit money. Under a gold money system, people can function much better with a constant money supply because there is no leakage of interest payments. Each community can continue to circulate its own holdings of gold money without having to pay any of it out in the form of interest payments.

8. Government does not need to enable creating more debt vs. government must enable debt creation. In order to keep a credit money economy going, more debt must be continually created. Government and financial leaders who do not want to be blamed for a downward spiral of slowing economic activity must see to it that more debt is constantly being created. Under a gold money system, there is no pressure to constantly increase the burden of debt.

9. Not as bubble prone vs. more bubble prone. The fractional reserve method of banking encourages asset bubbles because new money is created as borrowers take out new loans. When people borrow money to buy bubble assets (e.g., houses 1981-2006), it creates enormous amounts of new money to feed the asset bubble. Many asset bubbles were also created during the gold money era due to fractional reserve banking, but where the unit of currency is guaranteed by government to be equal to a fixed weight in gold, the inflation threat is taken out of the picture and that restrains bubble creation somewhat.

To support the value of their currencies under a gold money system, governments must also often raise interest rates in order to encourage investors to sell gold in exchange for bonds paying good interest. Higher interest rates also discourage the formation of asset bubbles.

10. Does not enable ZIRP vs. enables ZIRP. A zero interest rate policy is impossibl e under a gold money system. The demand for gold would soon deplete government’s gold holdings to zero. Under a credit money system a policy of low interest rates and financial repression can be imposed for an indefinite period of time.

11. Does not increase lending activity vs. increases lending activity. Low interest rates and the ease with which credit money is created lead to increased lending activity and higher debt loads. Under a gold money system, debt will necessarily be created at a slower rate. By stepping up the pace of debt creation, a credit money system serves the interests of the banks.

12. Has no problem with debt saturation vs. has serious problems with debt saturation. Continually increasing debt leads ultimately to debt saturation. When a country’s people and businesses are saturated with debt, it makes it much more diffic

ult to continue to increase the debt load. That leads to stagnation and slowing economic activity in a credit money system. A gold money system does not tend to lead to debt saturation and has no similar problems with debt saturation.

13. Increases wealth disparities vs. does not increase wealth disparities. The higher debt load facilitated by a credit money system results in greater flows of wealth from the debtor class to the creditor class. The higher debt load leads to increased disparities in income, more very poor and very rich and fewer of the middle class.

14. Holds its value vs. does not hold its value. Gold-backed currencies have an excellent track record of holding their value. Credit money tends to inflation, the rate of which largely depends on how fast new debt is being created.

15. Government as a guarantor of savings vs. government provides no guarantee. One of the three functions of money is as a store of value. (The others are a medium of exchange and a unit of account.) When the U.S. government guarantees that 35 U.S. dollars will buy an ounce of gold, as it did in the years 1934-67, government aid savers by acting as a guarantor of that store of value.

When the U.S. went off the gold standard in 1971, it changed the relationship between citizens and their government when government no longer provided that guarantee.

16. Defaulters are bad vs. defaulters are only partly bad. In a gold money system, a person who takes out a loan and does not repay it is considered a bad person, almost a thief. He has robbed his creditors of the money they were rightfully owed. In a credit money system, however, the creation of new debt is so important that anyone who goes into debt is a hero of the economy.

That is why under a debt money system, it is considered more important that new debt be created (e.g., as student loans) than to worry about whether they will ever be paid back or to pin blame and guilt on loan defaulters.

Conclusion: As we see, it is no exaggeration to say that the transition from gold money to credit money changes everything. It changes every individual’s relationship with his own money, with government, and with banks. It changes the power relationships within society. It changes the patterns of ownership and wealth accumulation.

It is very important that citizens and investors understand the credit money system that they are trying to operate within. For people with over 2,500 years of experience with gold money, it is difficult to understand it and get used to it. But anyone who does understand it will be better off because of making better-informed decisions. We might as well get used to it because we shall likely have to live with a credit money system for a very long time.

Thank you, Jeff, for an insightful and extremely important overview of the critical differences between credit money and gold/silver. The key distinction of all these important distinctions is the ephemeral nature of credit-money (and any form of fiat currency). History teaches us that a financial-political crisis of sufficient magnitude reveals the underlying value of credit-money–i.e. zero–in a brief but cataclysmic loss of faith/trust.

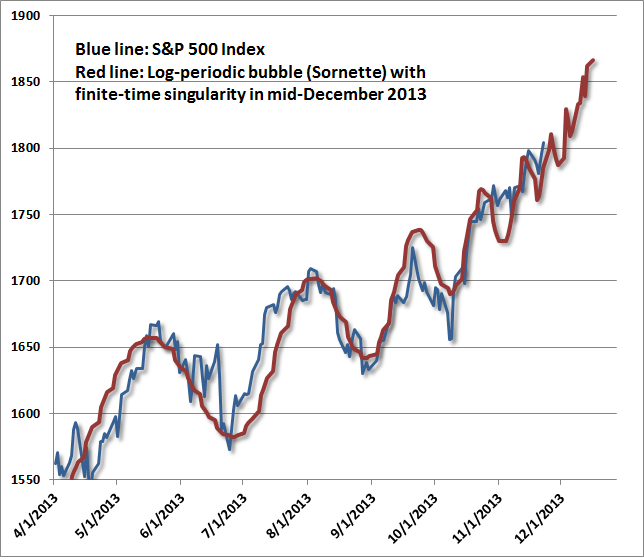

As correspondent Harun I. observed in Why Is Debt the Source of Income Inequality and Serfdom? It's the Interest, Baby: "Governments cannot reduce their debt or deficits and central banks cannot taper. Equally, they cannot perpetually borrow exponentially more. This one last bubble cannot end (but it must)."

When the current bubble bursts, the difference between metallic money and credit money will be starkly visible: no one will trade gold or silver for any amount of paper/credit money, and the ephemeral financial instruments ("assets") that dominate today's financial system will be revealed for what they are: phantom promises of value.

Of related interest:

Gold: The Once and Future Money by Nathan Lewis

Could Bitcoin (or equivalent) Become a Global Reserve Currency?

November 7, 2013

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/UZmRcPmV2NU/story01.htm Tyler Durden