Carl Menger, father of the Austrian School of Economics, showed the world that money is not the product of the state. He did not mean that government is intrinsically incapable of decreeing something to be money while other groups, organized for different purposes, could do it. He described how money emerges as the commodity which is most marketable (“absatzfähigkeit” in German).

He discusses factors that limit marketability including to whom you can sell a particular good, where you can sell it, when you can sell it, etc. The most marketable is the one anyone can buy or sell anywhere at any time, with no limitations on quantity.

Picture the problems with fresh oysters, crude oil, winter woolens, and iron ingots. Oysters spoil very quickly, crude oil has to be stored in a specialized tank, no one wants wool mittens in the summer, and iron is heavy. Only a dealer in seafood could buy oysters. Oil can only be bought up to the buyer’s storage capacity. No clothing retailer wants to buy merchandise that will sit in a warehouse for a year until next winter. Moving iron any great distance is expensive.

At one time, cattle was money. A big cause of this is that cattle move under their own power. For nomadic societies, everyone thought of livestock as wealth and pastureland was not a limitation. However, as people settled into cities and agriculture, animals didn’t work so well any more. What would a blacksmith or weaver do with a few cows in the workshop? And what will it cost to feed them? They needed something more convenient.

Gold emerged as the most marketable commodity. It does not have any of the above problems. Anyone can accept gold anywhere at any time, and bring it anywhere else to anyone else.

It is important to ask why a commodity. Why not love? “I will trade you two acres of farmlands for love (or a kiss)” Why not chiseled carvings on a stone at the city temple, kept in absolute trust by the priests? Why not pieces of paper? The first is a frivolous question to make a point. Love or a kiss cannot be exchanged with a third party.

But the other two are nontrivial, and deserve a serious answer. The answer is not: because price inflation. Or, at least, that is only one potential risk among others that lead to a more general problem and the full answer. Nor is it about collapse and the end of the world, what will people barter with (e.g. bullets, cigarettes, or dried food). It is about a universal concern in the human condition.

Trust.

Obviously if you think someone is a cheat, then you will not extend him credit. Or if you don’t like the balance of risk and reward, you will want to withdraw credit. But the issue is much broader than these two simple cases. In the market, it is not usually black and white. There are degrees. In other words, you may want to keep a certain fraction of your wealth in the system, where it earns a return and is easy to use in exchange.

At the same time, you may also want to keep some portion at home in the sock draw or under the floor boards. Everyone must decide for himself what portion to hoard. Yes, we use the word hoarding, though we know that most economists were dismissive of it if not derisive. In his book Human Action, economist Ludwig von Mises called it, “…a deus ex machina, the much talked about hoards…” (though in other places, he treated hoarding more dispassionately).

In fact, there is an arbitrage between hoarding and—to coin a verb word here—crediting. Hoarding is less convenient. Handling and trading physical pieces of metal such as coins has a cost in time spent and often a wider bid-ask spread. However, crediting incurs the risks of default, fraud, and even honest error.

Spread is always a motivator. In this case, there are two spreads. One is convenience, ease of use, time saved. The other is interest. The higher the yield on gold that one can earn, the greater the incentive to dishoard and put one’s money to work. The lower the return, or the higher the risk, the greater the incentive to hoard.

Hoarding is the only alternative to crediting. Whether you put the gold in your pocket, store it in a safe, or contract with a professional vaulting service, you are withdrawing your gold, refusing to grant credit, not allowing your gold to be used by anyone for any reason, and not being in a position to depend on a third party to return your gold (which is somewhat ambiguous in the case of a depository).

This illustrates why money is a physical commodity. Everything else is a form of credit. With any other monetary asset, you are granting credit to someone. Your asset is represented by a number on a ledger of a debtor, or at least an issuer. For purposes of extricating yourself from risk, for purposes of having something in hand, only taking home a physical commodity will do.

Note that not just any commodity suffices. If you buy a warehouse full of lumber, palettes full of copper bars, or a tank full of crude, these have storage costs. And you are speculating. You cannot rest easy so long as you have these goods, because the prices are always moving either up or down. If up, then you are getting richer. If down, then you are getting sweatier.

All the discussion of price in the gold community aside, this is not true for gold. People put gold into intergenerational trusts, with good reason. When you hold the monetary commodity, you are safe. The purpose is not to sell it for a higher price, but to hold it for its own sake, for the reasons we cited for hoarding earlier.

Leaving aside the question of whether price is determined subjectively, we now raise the following question. Is the definition of commodity subjective? Is a thing a commodity, or not a commodity, based on personal preference? Can one person just say that a number on a ledger is a commodity, while it is equally true for another to say no, that only a thing you can hold in your hand is a commodity?

This is no mere argument over what to include in a word’s definition. This is an argument over what sort of thing serves for that portion of one’s wealth that one does not wish to be crediting.

Where one needs hoarding, a number on someone else’s ledger will not do.

We began with Menger. Above we discussed the properties of the monetary commodity and hoarding vs. crediting. Now our discussion of money-is-commodity inevitably leads to Mises’ famous regression theorem.

Mises argues:

“Thus the demand for a medium of exchange is the composite of two partial demands: the demand displayed by the intention to use it in consumption and production and that displayed by the intention to use it as a medium of exchange. With regard to modern metallic money one speaks of the industrial demand and of the monetary demand. The value in exchange (purchasing power) of a medium of exchange is the resultant of the cumulative effect of both partial demands.”

Regression refers to the fact that the monetary demand of today is based on the monetary demand of yesterday. But yesterday’s monetary demands only existed because of last week’s monetary demand, and so on. Is this an infinite regression, or does it go back only so far and end at some point?

Mises argues it’s not infinite. Demand for the monetary good consists of two components, but only one of them depends on yesterday’s demand. Therefore, if you go back far enough, you will find a day when the good was not a monetary good—when its demand was exclusively for consumption and production.

One is, of course, free to argue that Mises was wrong. In such view, money does not have its origin as a good used in production and consumption. And money could be whatever anyone says it is. Or perhaps not just anyone has the power to deem something money, only a government has that power.

However, if one accepts Mises’ argument, then one has to address bitcoin. We have seen many papers contending that bitcoin meets the requirements of Mises’ regression theorem. Without singling anyone out for our scathing argument, let us just summarize them as: bitcoin has utility apart from its use in exchange. The bitcoin network solves certain problems, the blockchain is elegant and scalable, etc.

Our criticism of this logic is that bitcoin, the monetary thing itself, is demanded for some reason. Bitcoin proponents will tell you why. Its purchasing power is rising. One needs no abstract thought experiment to trace back to the origins of bitcoin in the mists of antiquity. It began ex nihilo in 2009.

Since then, its demand for use as a medium of exchange—we will be generous and concede for purposes of this argument that its speculative demand is merely demand for medium of exchange—has risen. However, what is its use—and by this we mean a bitcoin as such—for any kind of consumption or production?

Mises was clear in referring to a thing’s use “in consumption and production.” One cannot change the context and say the bitcoin blockchain, technology, network, or ecosystem have value. They do, but that does not change the nature of the value of a bitcoin. One does not buy a bitcoin to eat, nor to melt and combine with bytecoins and kilocoins, and manufacture into candlesticks, mirrors, electrical conductors.

Bitcoin is no commodity. Bitcoin does not pass Mises’ regression test. Bitcoin has no demand other than demand for medium of exchange.

However, for now it does substitute for gold in one important regard. It meets the need for speculation, for capital gains.

The price of gold dropped $24, and that of silver 60 cents this week. This is a far cry from Sep 8, when the price of silver hit $18.21. Since then, it’s been almost all downhill. What happened? Since the beginning of last month, the price of silver had been rising and at the basis along with it. Basis is future price minus spot price. A rising price and basis is telling us that buyers are pushing up the price—of futures. By arbitrage, the price of the metal is pulled up too, but it trails.

Another way to describe this is to say that the marginal buyer of silver metal is the market maker, who warehouses it for the futures buyer. If this is the marginal demand, then it’s a bearish indicator because it could disappear and become the marginal supply.

That is what has happened for the last two weeks. The closing price peaked on Sep 7, and has been dropping since then. Along with it, the basis has been falling. Both the August through Sep 7 trend of rising price and basis, and the Sep 8 through present trend of falling price and basis show us something clearly that cannot be seen on other graphs. These moves are caused by speculators positioning and then depositioning themselves.

Two facts in this round trip are unfortunate for silver speculators. One, when the price was rising, the basis was rising. Real demand dropped off while speculative demand is only temporary. Two, when the price came back down the basis did not fall that much. The fundamental silver price that we calculate daily began falling after 8 September.

One might wish for the price to skyrocket, but one must respect the data. The data does not guarantee that the price could not hit $20 or $22 perhaps. But it shows that there is no reason for it, and the more the price rises, the stronger are the forces pulling it down.

We are not in the same short-term interest environment that existed during most of the last 9 years. This is reflected in the cost of carry for all trades. In the case of silver, the silver forward rate shows that the offered rate (what a trader would pay to carry silver for 6 months) was around 0.5% at the end of 2015, but has since gone up to about 2%.

We assume that silver speculators are more mindful of the cost, and likely to close positions sooner at this higher rate. If that is so, then expect speculative moves to end sooner and maybe even silver to spend more time trading below its fundamentals than previously.

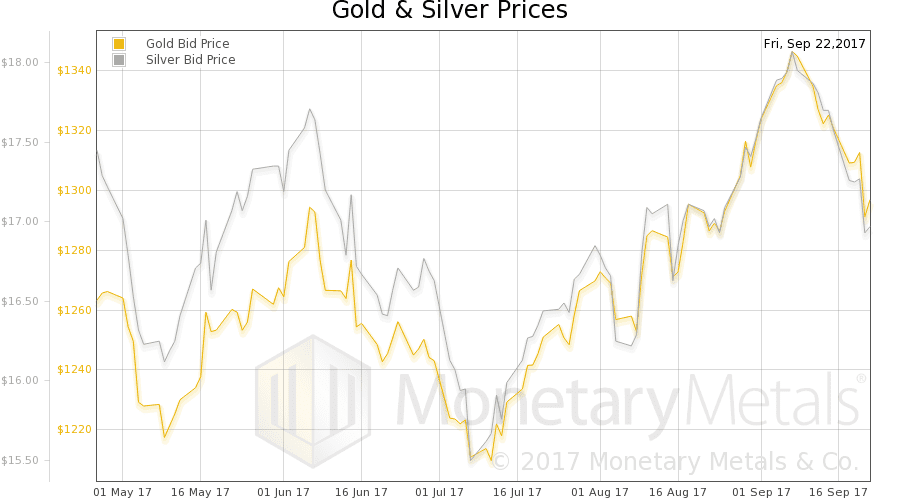

We will look at an updated picture of the fundamentals of supply and demand of both metals. But first, here are the charts of the prices of gold and silver, and the gold-silver ratio.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio rose.

In this graph, we show both bid and offer prices for the gold-silver ratio. If you were to sell gold on the bid and buy silver at the ask, that is the lower bid price. Conversely, if you sold silver on the bid and bought gold at the offer, that is the higher offer price.

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The dollar is up some more (the inverse of the falling price of gold). The cobasis (red line, scarcity) is up a bit.

Our calculated Monetary Metals gold fundamental price actually increased $8 to $1,378.

Now let’s look at silver.

This is the time of year when both metals have the same active contract month, December. This means the near contract basis has the same duration, and we can make a direct comparison. The gold cobasis is -0.88%, and for silver it is -0.82%.

This would paint a picture of silver being the scarcer metal. However, with silver’s poorer liquidity, we generally see a lower basis / higher cobasis in the near contract. The fact that they are so close actually indicates that gold is likely to be scarcer.

This is why we calculate a continuous basis, to take out the propensity to fall inherent in the near contract. The continuous gold cobasis is -1.24% and for silver it is -1.38%.

Our calculated Monetary Metals silver fundamental price fell $0.06 to $17.32 (recall from gold above, the fundamental price is up $8).

For whatever reason, call it “risk off”, call it “no one wants silver in a potential war with a nuclear power”, call it “soft industrial demand for metals”, silver is weaker than gold at this time.

We calculate a fundamental gold-silver ratio of around 79.5

© 2017 Monetary Metals

via http://ift.tt/2y3A7sC Monetary Metals