We’re gonna need a dovish-er Fed…

Bonds and bullion remain bid as the dollar skids but stocks rolled over dramatically, not helped by DowDupont and European banks.

via ZeroHedge News http://bit.ly/2SldDgk Tyler Durden

another site

We’re gonna need a dovish-er Fed…

Bonds and bullion remain bid as the dollar skids but stocks rolled over dramatically, not helped by DowDupont and European banks.

via ZeroHedge News http://bit.ly/2SldDgk Tyler Durden

Federal agents are going to dramatic lengths to find immigrants trying to game the student visa system. “For years, the Department of Homeland Security has operated a fake university in the Detroit suburbs as part of an undercover operation that lured undocumented immigrants,” The Daily Beast reports.

Federal agents are going to dramatic lengths to find immigrants trying to game the student visa system. “For years, the Department of Homeland Security has operated a fake university in the Detroit suburbs as part of an undercover operation that lured undocumented immigrants,” The Daily Beast reports.

The Homeland Security-run “University of Farmington”—first revealed by The Detroit News—ran from 2015 until recently and “intensified one month into President Donald Trump’s tenure as part of a broader crackdown on illegal immigration,” the News says. The school offered immigrants on student visas a way to maintain their student status (and associated work permit) without actually doing any coursework.

As a result, eight people were indicted for “conspiracy to commit visa fraud” and “dozens” of University of Farmington students were arrested by Immigration and Customs Enforcement (ICE) agents. Most of those arrested are from India and now face deportation.

As with FBI-led terror and drug plots, the scheme raises questions. The fake school gave legal immigrants with expiring student visas a simple way to stay here, by paying tuition at what was listed as an accredited university. It’s not at all clear that those scammed knew the school was a total sham, knew that enrolling there wasn’t legitimate for visa purposes, or would have engaged in any fraud had the feds not provided the opportunity.

“The university had a professional website, a red-and-blue coat of arms, a Latin slogan meaning ‘knowledge and work’ and a physical location at a commercial building on Northwestern Highway,” The Detroit News reports.

Federal agents deployed several tactics to make the University of Farmington appear to be a legitimate school. The main photo of University of Farmington students on the school’s website is nearly identical to a commercially available picture on the stock photograph website Shutterstock.

The University of Farmington has its own Facebook page, too, with a calendar of events, including one scheduled for next week with non-existent university officials.

ICE has also been telling immigrants to show up for court hearings or risk being deported. But the alleged hearings aren’t actually scheduled. “Immigrants were instructed to appear on weekends, midnight, and dates that just didn’t exist, like Sept. 31,” reports CBS News.

I’m about as pro-life as it gets, you guys all know I am.

But it seems to me there’s a far more charitable interpretation of Northam’s comments here. https://t.co/FKyoG7Yw1w

— (Stephanie) Slade (@sladesr) January 30, 2019

Should we legalize prostitution? What would Norman Rockwell do? I talk to @reason‘s @ENBrown about the upshot of decriminalizing sex work on today’s show. https://t.co/XXYiZe1v4j

— Andrew Heaton

from Hit & Run http://bit.ly/2UvDhMK

via IFTTT

Authored by Kevin Muir via The Macro Tourist blog,

If you read only one MacroTourist post all year, this is the one I want you to read. I think it’s that important.

Today’s topic is sure to incite some pretty strong reactions. There will be cries of “no! that’s just wrong!” from the hard-money advocates. The cynics will proclaim “that’s going to end in disaster” and the pessimists will shake their head in disbelief while muttering something about “the follies of the ivory tower academics” as they walk away.

For some of you, the topic of Modern Monetary Theory (MMT) will be old hat. For others, this will be a new term. For those who are not familiar, I suggest you take some time to learn about this new branch of economic thinking as it is coming to a screen near you.

Although I have an opinion about what is best for our economy and society, I am not here to convince you of anything except the fact that MMT is gaining traction, and to remind you that spending time arguing about its relative merits/detriments will not help your trading or investing one iota.

You see, I try to be like that joke; “Dear Optimist and Pessimist, while you were busy debating over whether the glass was half-full or half-empty, I drank it. Signed the Opportunist.”

I know I am nowhere near smart enough to influence policy. So why even try? Nor do I have any desire. So why bother debating it? Yet I love trying to figure out this great big game we call investing. In that vein, putting your head in the sand regarding MMT would definitely be a mistake.

Let me take you through my journey of trying to understand MMT, and along the way, I hope to maybe help a little with your navigating the coming changes in economic thinking.

It was about a year ago when MMT started popping up on my radar. Realizing that all I knew was what the acronym stood for (Modern Monetary Theory), I reached out to Bespoke’s George Pearkeswho is a wealth of knowledge when it comes to economic thinking. You see, I am basically a markets guy. George is a markets guy, but there is also a big part of him that is more pure “economist”.

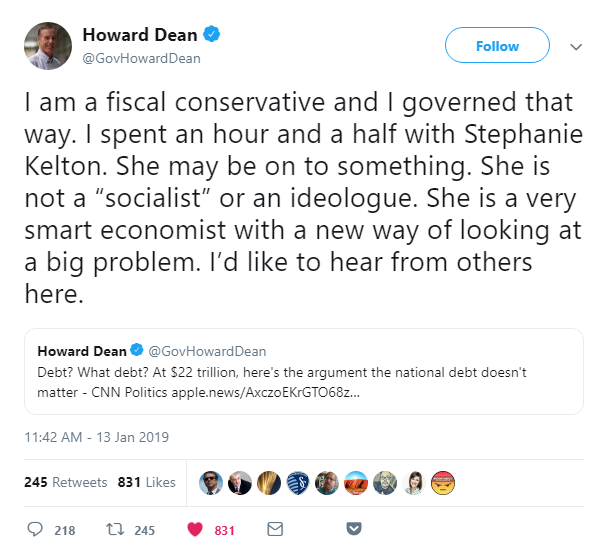

And George was his typical super-nice-guy self. He guided me to some great resources, but ultimately pointed me in the direction of the face of MMT – Professor Stephanie Kelton from Stony Brook University.

Last autumn Professor Kelton gave a speech at Stony Brook University titled “But How Will We Pay for It? If you have an hour to spare, this is probably the best introduction to MMT out there.

[As an aside, George and I recently had a chat about MMT on his podcast BespokeCast. Fast-forward to about half-way to get to the MMT stuff.]

Back to my journey of learning about MMT. Apart from being a professor, Stephanie was also the economic advisor for Bernie Sanders’ campaign.

Given the general more right-leaning bias of people in the finance arena, I can already hear the groans and the clicking to the next article. But wait! Before you go and listen to what Alex Jones is screaming about, remember that your job as an investor is not to forecast what should be but rather focus on what will be.

So let’s get to it. What exactly is MMT?

Modern Monetary Theory is a macroeconomic theory that contends that a country that operates with a sovereign currency has a degree of freedom in their fiscal and monetary policy which means government spending is never revenue constrained, but rather only limited by inflation.

This is my layman’s version after reading and listening to everything I could on the subject, but I think I got the gist of it.

MMT’ers believe that government’s red ink is someone else’s black ink. Sure, the government owes dollars, but they have a monopoly of creating those dollars, and not only that, the creation of more and more dollars is essential to the functioning of the economy.

Here are the policy implications of accepting MMT:

governments cannot go bankrupt as long as it doesn’t borrow in another currency

it can issue more dollars through a simple keystroke in the ledger (much like the Fed did in the Great Financial Crisis)

it can always make all payments

the government can always afford to buy anything for sale

the government can always afford to get people jobs and pay wages

government only faces two different kinds of limitations; political restraint and full employment (which causes inflation)

The government can keep spending until they begin to crowd out the private sector and compete for resources.

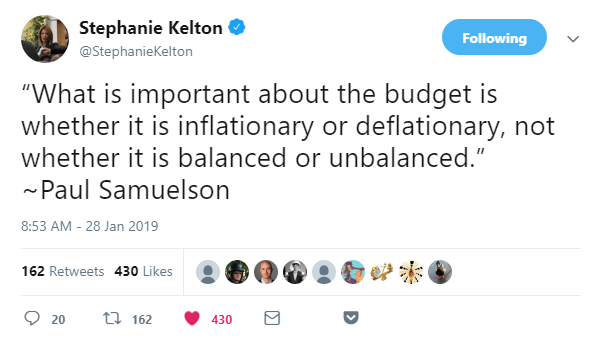

And in fact, Stephanie Kelton argues it is immoral to not utilize this power to fix problems in our society. From an interview she gave,

“if you think you can’t repair crumbling infrastructure or feed hungry kids, unless and until you find some money somewhere, it’s actually pretty cruel because you leave people who are struggling in a position where there are still struggling and they are hurting, and they are not properly taken care of…”

I know what you are thinking. Sure sounds like socialism.

But MMT is not socialism. Not by a long shot.

MMT’ers don’t necessarily believe in taxing the wealthy and redistributing it to the poor. Though they do believe the way conventional economics and politicians think about money is wrong.

I know it seems insane to think about the government as not having to worry about deficits and debts. It doesn’t seem to make sense. How can a government just spend money without having to worry about paying it back?

It’s like when Kramer got lost downtown. Remember the terror in his voice when he realized he was at 1st and 1st – where the same street intersects with itself at the nexus of the universe?

But here is another way to think about it. If you have an economy with underused capacity, having the government spend on infrastructure or other societal useful endeavors is actually raising the total GDP of the country.

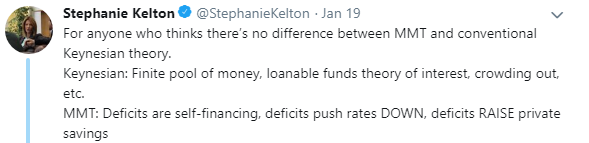

Yet isn’t that just Keynes theory? Yeah, trying to wrap my head around the difference between Keynes and MMT took me a while, but I think I got it.

Keynesians are still tied to the idea that we are bound by fiscal constraints whereas MMT’ers believe that the only real restraint is inflation.

I heard an economist the other day on Bloomberg say something about the dire state of the global economy because of the stretched balance sheets of the various sovereigns. He said something to the effect of spending will collapse because “who has the capacity for fiscal spending?”

And this is the conventional thinking that prevails almost everywhere.

But MMT’ers would argue that by not spending now, we will be harming our productive capacity in the future. Ultimately it makes no sense to have economic capacity sitting fallow because of a self-imposed worry about paying back a debt that is denominated in an asset that only the government can create.

But, but, but… won’t that create inflation? Yup! Darn right it will, and that’s the point. MMT’ers believe that inflation is the only true constraint a government faces.

As I was learning about MMT it made me wonder if Richard Koo (balance sheet recession fame) was also an MMT’er. After all his belief in the paradox of thrift causing a self-defeating vicious circle seems straight out of MMT’s theories.

So far I have named all these rather left-wing proponents of MMT, but is it truly the domain of the far left? Well, interestingly, former hedge fund manager Warren Mosler has run for office numerous times as a MMT advocate. I dug up this interesting debate between Warren and this Austrian economist.

And while doing my research, I stumbled on this great interview with Professor Steve Keen titled, “Does Modern Monetary Theory make sense?”

I have greatly simplified MMT – no denying that. There were points when I was reading about the relative slope of the IS curve of Keynesians versus MMT’ers and I had a slight moment of panic that I was back in my third-year Economics class after having missed the past two weeks of classes.

How about I try to explain MMT in contrast to the policies of the past decade?

Let’s step back and think about what’s happened in our economy since the Great Financial Crisis and then think about how MMT changes the equation.

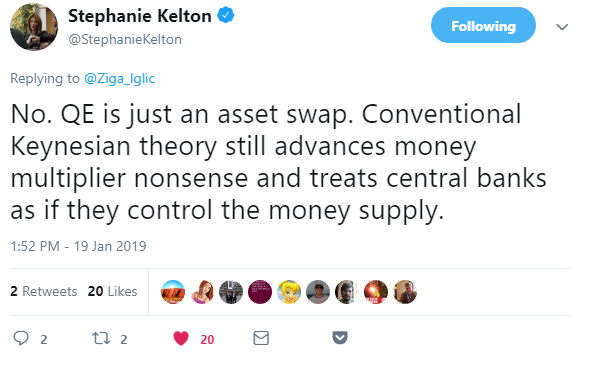

There can be no denying that the grand credit super-cycle has seen more and more debt being piled on to an ever growing mound. In 2007 it looked like we had hit the Minsky moment when no more debt could be balanced on the teetering edifice, and when the final piece of the Jenga puzzle was removed, it started to come tumbling down. At this point private credit had entered into a deflationary self-reinforcing credit destruction loop which would have resulted in a cleansing reset of the entire system. Yet this would have been extremely painful and it soon became clear that the government didn’t have the stomach to live through this sort of reset. So they flooded the system with money through quantitative easing – much to the howls of protest from the economic and Wall Street elite who insisted this would cause inflation. But much to almost everyone’s surprise, there was almost no inflation – at least little inflation as we generally think about it. There was plenty of financial asset inflation as all that new money pushed down interest rates and caused asset prices to lift, but the average worker saw little benefit from the Fed’s largess. You see, even though the Fed was busy buying everything with a CUSIP, the Federal Government was in the midst of one of the biggest cuts in discretionary spending in the history of the United States.

I try to keep my politics to myself, but I can’t hide my feeling that socialism for the rich is not a fair way to run a society. You can’t have a heads-I-win-tails-you-lose situation for banksters and other well-connected parties, but the moment that the economy starts to gain traction, the Fed needs to tamp down on the brakes for fear of inflation.

Regardless of whether you agree with my view or not, it doesn’t matter.

The public has woken up to the fact that supply-side-trickle-down economics is not helping them anywhere near as much as promised.

You might think these sorts of tax-cutting pro-business policies are the best thing for our economy. So be it. Reasonable people can have differing opinions. But the tide is shifting away from this belief, so it really doesn’t matter what you, or I, or even the smartest economist in the world believes.

Society’s mood has changed and Stephanie Kelton’s concepts will continue to gain supporters.

If I had told you four years ago that the following picture wasn’t a photoshop, you would have probably told me I was nuts.

Trump was elected due to a profound disappointment with the status quo. It’s easy to forget but even Obama was elected on a platform of hope and change.

Don’t underestimate how pissed off the average American is (and Canadian, Frenchman, Englishman, etc… for that matter). Monetary stimulus with fiscal austerity doesn’t do anything except make the rich richer.

MMT is novel, ambitious, and a little bit scary. I get it. But let me let you in on a little bit of a secret – young people aren’t afraid of trying something new. They know the system isn’t working and are desperately looking for an alternative. I think they found it in MMT…

If I am correct, I suspect we will see many Democrat candidates (perhaps all?) adopt MMT as a tenant of their platform. And here is a crazy thought for you – what if Trump beats them to it?

I have long argued that eventually we will hit a period where governments will spend and Central Banks will facilitate their deficits. MMT provides academic justification of where we all know we are headed anyway.

In one of the interviews I watched with Professor Kelton, she said that the idea of deficits being funded with bond issuance is purely a self-imposed limitation. It’s required by law, but in reality, it doesn’t need to be done. The law can be changed. The government could simply spend $100 while only taking in $90 and directly writing cheques against the Federal Reserve to pay for the $10.

Think about how inflationary this will be! But isn’t that the whole goal?

I have always chuckled at the idea that governments were powerless to create inflation. If they want to create inflation – they can. There just needs to be the political will. And it looks like that will has finally arrived.

So what does this mean for your portfolio?

Although I don’t have any concern about the government funding itself, I do have lots of worry that inflation would quickly rise and before too long, the government would be forced to cut back its spending, and that typical of governments, it would prove much more difficult than instituting spending. Therefore I would expect fixed-income to be a terrible investment under MMT. Even if the government pegs rates low, inflation will be the real risk. It would make little sense to sit in an asset that pays fixed.

To me, MMT would scream that the best course would be to buy real productive assets hand over fist.

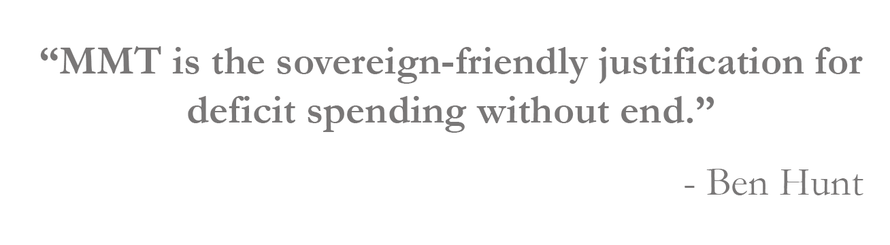

Ben Hunt had an interesting piece in his excellent blog Espilon Theory titled, “Modern Monetary Theory or: How I Learned to Stop Worrying and Love the National Debt”. I would argue that he represents conventional Wall Street thinking in terms of his pessimism regarding MMT, but I would like to highlight two terrific points from his writing.

Ben believes MMT will gain traction in the coming years; “Like I said, you may not have heard about MMT yet. But you will. You won’t be able to avoid it. Why? Because MMT is the post hoc justification of both easy fiscal policy and easy monetary policy. As such, it is the new intellectual darling of every political and market Missionary of the Left AND the Right.”

He also contends that MMT will switch QE’s inflation in financial assets to inflation in the real world.

I agree with Ben that MMT will change the type of inflation the economy experiences. I will leave it to much smarter people than I to decide if this is a good or bad thing.

In the meantime, in the coming months, quarters and years, watch for MMT to become a much larger source of change for your portfolio and trading. You might think it’s great and that the financial world could use a change. Or you might think it’s terrible and will be a disaster. Doesn’t matter what you or I think. MMT is coming. Ignoring it would be foolish.

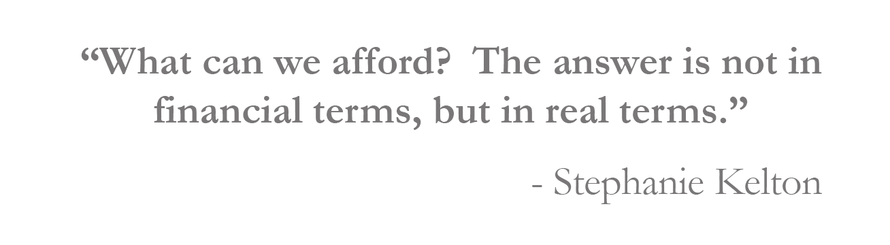

I will leave you with two quotes. One from Ben Hunt and one from Stephanie Kelton. They sum up the battle that will soon envelop the political and financial landscape.

Thanks for reading.

via ZeroHedge News http://bit.ly/2sWowXT Tyler Durden

It has been more than a year since Saudi Crown Prince Mohammad bin Salman ordered a sweeping “corruption crackdown” that involved arresting dozens of the kingdom’s wealthiest and most well-connected businessmen and political elites and locking them up in an ad hoc prison inside the Riyadh Ritz-Carlton, according to the Financial Times.

Almost immediately after news of the arrests crossed into Western media, rumors that the detainees were being abused and tortured started filtering through as well. Images of dirty mattresses splayed across the floor of the same ballroom where MbS had only weeks earlier held his “Davos in the Desert” investment forum shocked viewers, as did reports that one detainee – reportedly a Saudi military officer – died during a particularly grueling interrogation session.

After dozens of detainees – a group that reportedly included Saudi Prince Alwaleed bin Talal – agreed to surrender billions of dollars in assets and cash, most were let go; others were moved to a more traditional prison where, according to the Financial Times, some are being held on corruption charges to this day. Others, including Mohammed al-Amoudi, a Saudi-Ethiopian businessman, and Amr al-Dabbagh, a senior executive, have only just been released as the crackdown officially came to a close.

In recognition of the end of the probe, the Saudi government has finally confirmed that, all told, the Saudi state yielded more than $100 billion during the crackdown.

And for the first time, the kingdom also released official numbers about the number of people who were detained, the number who settled and the number who have been referred for further prosecution after the kingdom “refused to settle” because of “existing corruption charges,” per the FT.

Here’s a quick rundown of the most salient details from the FT report:

Of course, thanks to the killing of Jamal Khashoggi and Saudi’s involvement in the ongoing conflict in Yemen, the ruthlessness that MbS exercised during the crackdown has been largely overshadowed.

But if Saudi’s oil production cuts fail to sustain the January rally in oil, and the kingdom is once again presented with the logistical challenge of filling a massive budget hole, we wouldn’t be surprised to see MbS order another round.

via ZeroHedge News http://bit.ly/2MJHjyo Tyler Durden

Authored by Lance Roberts via RealInvestmentAdvice.com,

“What scares me the most longer term is that we have limitations to monetary policy — which is our most valuable tool — at the same time we have greater political and social antagonism.” – Ray Dalio, Bridgewater Associates

Dalio made the remarks in a panel discussion at the World Economic Forum’s annual meeting in Davos on Tuesday where he reiterated that a limited monetary policy toolbox, rising populist pressures and other issues, including rising global trade tensions, are similar to the backdrop present in the latter part of the Great Depression in the late 1930s.

Before you dismiss Dalio’s view Bridgewater’s Pure Alpha Strategy Fund posted a gain of 14.6% in 2018, while the average hedge fund dropped 6.7% in 2018 and the S&P 500 lost 4.4%.

The comments come at a time when a brief market correction has turned monetary and fiscal policy concerns on a dime. As noted by Michael Lebowitz yesterday afternoon at RIA PRO

“In our opinion, the Fed’s new warm and cuddly tone is all about supporting the stock market. The market fell nearly 20% from record highs in the fourth quarter and fear set in. There is no doubt President Trump’s tweets along with strong advisement from the shareholders of the Fed, the large banks, certainly played an influential role in persuading Powell to pivot.

Speaking on CNBC shortly after the Powell press conference, James Grant stated the current situation well.

“Jerome Powell is a prisoner of the institutions and the history that he has inherited. Among this inheritance is a $4 trillion balance sheet under which the Fed has $39 billon of capital representing 100-to-1 leverage. That’s a symptom of the overstretched state of our debts and the dollar as an institution.”

As Mike correctly notes, all it took for Jerome Powell to completely abandon any facsimile of “independence” was a rough December, pressure from Wall Street’s member banks, and a disgruntled White House to completely flip their thinking.

In other words, the Federal Reserve is now the “market’s bitch.”

However, while the markets are celebrating the very clear confirmation that the “Fed Put” is alive and well, it should be remembered these “emergency measures” are coming at a time when we are told the economy is booming.

“We’re the hottest economy in the world. Trillions of dollars are flowing here and building new plants and equipment. Almost every other data point suggests, that the economy is very strong. We will beat 3% economic growth in the fourth quarter when the Commerce Department reopens.

We are seeing very strong chain sales. We don’t get the retail sales report right now and we see very strong manufacturing production. And in particular, this is my favorite with our corporate tax cuts and deregulation, we’re seeing a seven-month run-up of the production of business equipment, which is, you know, one way of saying business investment, which is another way of saying the kind of competitive business boom we expected to happen is happening.” – Larry Kudlow, Jan 24, 2019.

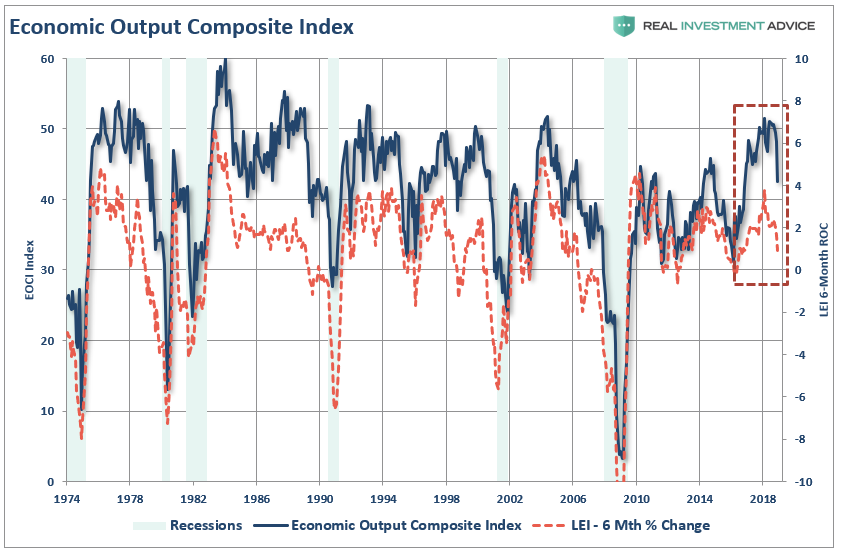

Of course, the reality is that while he is certainly “spinning the yarn” for the media, the Fed is likely more concerned about “reality” which, as the data through the end of December shows, the U.S. economy is beginning to slow.

“As shown, over the last six months, the decline in the LEI has actually been sharper than originally anticipated. Importantly, there is a strong historical correlation between the 6-month rate of change in the LEI and the EOCI index. As shown, the downturn in the LEI predicted the current economic weakness and suggests the data is likely to continue to weaken in the months ahead.”

As Dalio noted, one of the biggest issues facing global Central Banks is the ongoing effectiveness of “Quantitative Easing” programs. As previously discussed:

“Of course, after a decade of Central Bank interventions, it has become a commonly held belief the Fed will quickly jump in to forestall a market decline at every turn. While such may have indeed been the case previously, the problem for the Fed is their ability to ‘bail out’ markets in the event of a ‘credit-related’ crisis.”

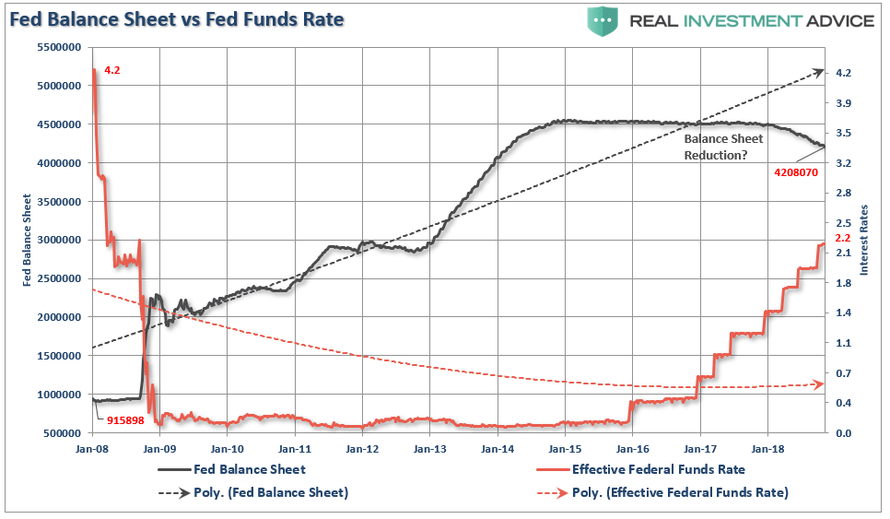

“In 2008, when the Fed launched into their “accommodative policy” emergency strategy to bail out the financial markets, the Fed’s balance sheet was only about $915 Billion. The Fed Funds rate was at 4.2%.

If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion dollar balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bail out’ the markets today, is much more limited than it was in 2008.”

But it isn’t just the issue of the Fed’s limited toolbox, but the combination of other issues, outside of those noted by Dalio, which have the ability to spur a much larger.

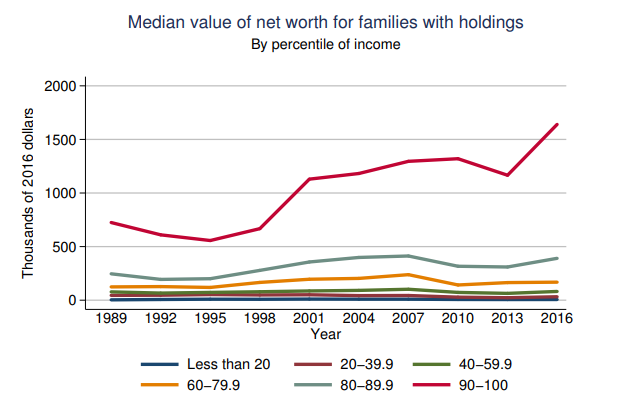

The nonprofit National Institute on Retirement Security released a study in March stating that nearly 40 million working-age households (about 45 percent of the U.S. total) have no retirement savings at all. And those that do have retirement savings don’t have enough. As I discussed recently, the Federal Reserve’s 2016 Survey of consumer finances found that the mean holdings for the bottom 80% of families with holdings was only $199,750.

Such levels of financial “savings” are hardly sufficient to support individuals through retirement. This is particularly the case as life expectancy has grown, and healthcare costs skyrocket in the latter stages of life due historically high levels of obesity and poor physical health. The lack of financial stability will ultimately shift almost entirely onto the already grossly underfunded welfare system.

However, that is for those with financial assets heading into retirement. After two major bear markets since the turn of the century, weak employment and wage growth, and an inability to expand debt levels, the majority of American families are financially barren. Here are some recent statistics:

78 million Americans are participating in the “gig economy” because full-time jobs just don’t pay enough to make ends meet these days.

In 2011, the average home price was 3.56 times the average yearly salary in the United States. But by the time 2017 was finished, the average home price was 4.73 times the average yearly salary in the United States.

In 1980, the average American worker’s debt was 1.96 times larger than his or her monthly salary. Today, that number has ballooned to 5.00.

In the United States today, 66 percent of all jobs pay less than 20 dollars an hour.

102 million working age Americans do not have a job right now. That number is higher than it was at any point during the last recession.

Earnings for low-skill jobs have stayed very flat for the last 40 years.

Americans have been spending more money than they make for 28 months in a row.

In the United States today, the average young adult with student loan debt has a negative net worth.

At this point, the average American household is nearly $140,000 in debt.

Poverty rates in U.S. suburbs “have increased by 50 percent since 1990”.

Almost 51 million U.S. households “can’t afford basics like rent and food”.

The bottom 40 percent of all U.S. households bring home just 11.4 percent of all income.

According to the Federal Reserve, 4 out of 10 Americans do not have enough money to cover an unexpected $400 expense without borrowing the money or selling something they own.

22 percent of all Americans cannot pay all of their bills in a typical month.

Today, U.S. households are collectively 13.15 trillion dollars in debt. That is a new all-time record.

Here is the problem with all of this.

Despite Central Bank’s best efforts globally to stoke economic growth by pushing asset prices higher, the effect is nearly entirely mitigated when only a very small percentage of the population actually benefit from rising asset prices. The problem for the Federal Reserve is in an economy that is roughly 70% based on consumption, when the vast majority of American’s are living paycheck-to-paycheck, the aggregate end demand is not sufficient to push economic growth higher.

While monetary policies increased the wealth of those that already have wealth, the Fed has been misguided in believing that the “trickle down” effect would be enough to stimulate the entire economy. It hasn’t. The sad reality is that these policies have only acted as a transfer of wealth from the middle class to the wealthy and created one of the largest “wealth gaps” in human history.

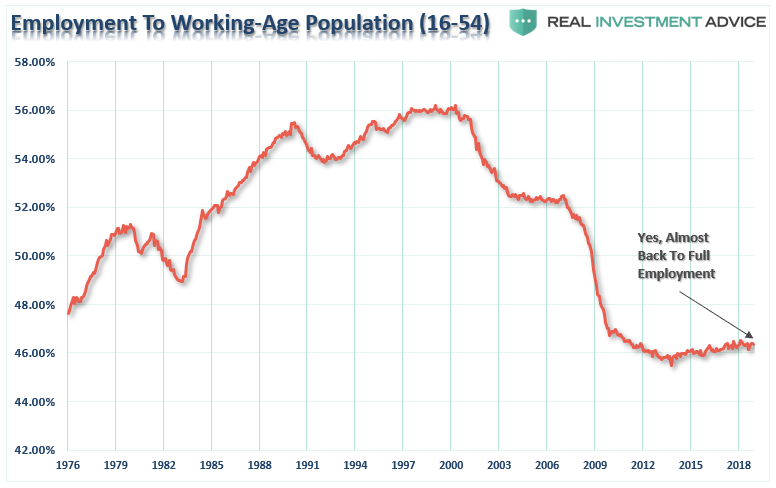

The real problem for the economy, wage growth and the future of the economy is clearly seen in the employment-to-population ratio of 16-54-year-olds. This is the group that SHOULD be working and saving for their retirement years.

The current economic expansion is already set to become the longest post-WWII expansion on record. Of course, that expansion was supported by repeated artificial interventions rather than stable organic economic growth. As noted, while the financial markets have soared higher in recent years, it has bypassed a large portion of Americans NOT because they were afraid to invest, but because they have NO CAPITAL to invest with.

To Dalio’s point, the real crisis will come during the next economic recession.

While the decline in asset prices, which are normally associated with recessions, will have the majority of its impact at the upper end of the income scale, it will be the job losses through the economy that will further damage and already ill-equipped population in their prime saving and retirement years.

Furthermore, the already grossly underfunded pension system will implode.

An April 2016 Moody’s analysis pegged the total 75-year unfunded liability for all state and local pension plans at $3.5 trillion. That’s the amount not covered by current fund assets, future expected contributions, and investment returns at assumed rates ranging from 3.7% to 4.1%. Another calculation from the American Enterprise Institute comes up with $5.2 trillion, presuming that long-term bond yields average 2.6%.

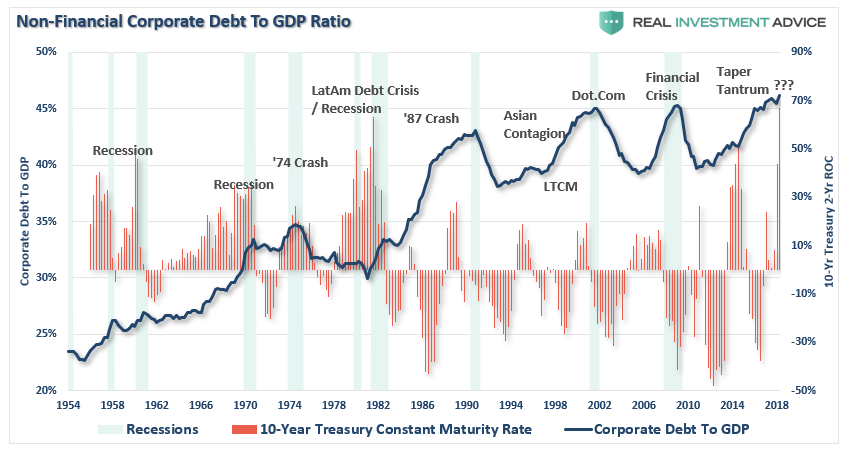

The massive amount of corporate debt, when it begins to default, will trigger further strains on the financial and credit systems of the economy.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping will cause a debacle of mass proportions. It will require a massive government bailout to resolve it.

But it doesn’t end there. Consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt. When the recession hits, the reduction in employment will further damage what remains of personal savings and consumption ability. The downturn will increase the strain on an already burdened government welfare system as an insufficient number of individuals paying into the scheme is being absorbed by a swelling pool of aging baby-boomers now forced to draw on it. Yes, more Government funding will be required to solve that problem as well.

As debts and deficits swell in the coming years, the negative impact to economic growth will continue. At some point, there will be a realization of the real crisis. It isn’t a crash in the financial markets that is the real problem, but the ongoing structural shift in the economy that is depressing the living standards of the average American family. There has indeed been a redistribution of wealth in America since the turn of the century. Unfortunately, it has been in the wrong direction as the U.S. has created its own class of royalty and serfdom.

The issue for future politicians won’t be the “breadlines” of the 30’s, but rather the number of individuals collecting benefit checks and the dilemma of how to pay for it all.

The good news, if you want to call it that, is that the next “crisis,” will be the “great reset” which will also make it the “last crisis.”

via ZeroHedge News http://bit.ly/2RYCd7u Tyler Durden

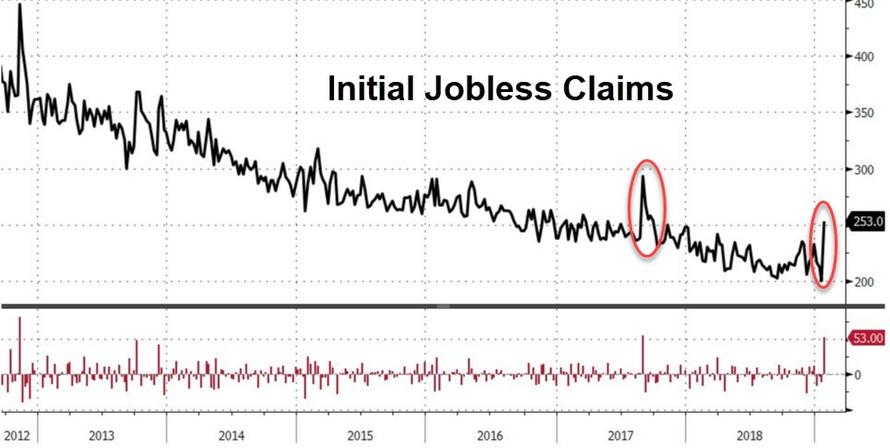

Initial jobless claims exploded higher by 53,000 last week to 253,000 – the highest since Sept 2017 (from the lowest in 50 years).

This is the biggest weekly spike since the Hurricane season chaos of September 2017 (Harvey, Irma, Jose, and Maria)…

Presumably most if not all of this surge will be erased over the nest week or two as the shutdown is now over.

via ZeroHedge News http://bit.ly/2UvEbZP Tyler Durden

Submitted by Rabobank strategist Michael Every

The ECB: a legend in its own mind. Draghi recently emphasized that although GDP growth was not looking good now, better times lay ahead – because Chinese fiscal and monetary stimulus will kick in. I know the neoliberal Davos consensus Draghi champions is a big fan of outsourcing, but isn’t it taking things a bit too far when the central bank of the world’s richest region leaves much-needed stimulus to a far poorer country with a political-economy anathema to it? If Brexit goes badly wrong will Draghi be on the phone to the PBOC straight away in that case?

Yesterday the ECB also proudly Tweeted its own economic research showing **drumroll** that QE helped reduce inequality.

ECB asset purchases have reduced inequality in the eurozone, our research shows. They have especially benefited low-income households, which suffer the most from unemployment. Full Research Bulletin here https://t.co/MlMQO2BXxK pic.twitter.com/4DtpcOsqms

— European Central Bank (@ecb) January 30, 2019

That’s right, reduce. The central claims are: (1) by lowering unemployment at the lower end of the socio-economic ladder, QE put money in people’s pockets; (2) higher stock prices didn’t have any influence on wealth inequality; and (3) higher house prices helped to reduce inequality.

I can hear the stunned silence. That’s wonderfully convenient for the ECB, and for Davos Man, as the 2019 WEF started by warning of the need to look after “the losers of globalisation” and to refocus its moral mission – and then failed to provide a single proposal for how we do that, again, switching the topic to climate change and hoping we wouldn’t notice because it’s so serious a topic. Yet now there is a cure for global inequality – more QE!

At first reading I thought that these ECB results were the kind of start-with-your-conclusion-and-work-backwards, pick-and-mix, pseudo-scientific gibberish that I have come to expect from the same central bank economic research teams who didn’t see the GFC coming, expect to have to do QE after the GFC, didn’t see the new normal coming, didn’t see populism coming, and now don’t understand that QT (in the US) causes a market meltdown. However, I was too generous.

It’s not that the ECB can’t prove QE helped reduce unemployment; or that the jobs created are widely accepted as being low paid; or that the ECB’s survey data covers just four of the Eurozone’s diverse members; or that it is insane to argue nobody gets richer from rising equities; or that rising house prices, and rents, must mean inequality for those who don’t own houses. It’s because on closer examination, the authors are not Useful Idiots. They are shills.

The give-away is that at the end of the accompanying video explaining why the ECB has reduced inequality there are two piles of graphic money. The smaller one, lower-income households, grows. (Yay!) The larger one, richer households, shrinks as if the rich are getting less money in some kind of tax redistribution mechanism. (Yay!) That is objectively not true. Yet it’s what they want viewers to see. That is the kind of spin you’d associate with a populist politician. As my colleague Christian Lawrence quipped after I shared the video with him, “Next the ECB will be telling us negative interest rates help the homeless.”

We were not the only ones to feel that way. The responses on Twitter were a flood of very angry rebuttals. Indeed, I don’t think the ECB realises just what a stupid mistake it has made. It is never a good thing to be spotted as a shill: crowds tend to get angry. Worse, the ECB have made a (false) economic case that QE helps inequality, when actually it exacerbates it. That means when we do more QE people will be expecting to see greater equality and will get the opposite – again, the crowd will get nasty. The ECB have also opened the door to those same angry populists to say “If your QE can reduce inequality slightly, imagine what our kind of QE could do!” – and what intellectual defence could the ECB mount? “You can’t do that – it’s…too effective(?)”

* * *

Meanwhile, the Fed did what every cynic must have known in their heart of hearts that the Fed would do: totally capitulate. Not only is it now “patient” whereas in October the economy was overheating –and unemployment is lower now than it was then, and wage growth higher– but it is willing to be “flexible“ over the pace at which is reduces its balance sheet, and to expand the same balance sheet if things go wrong. Considering that our house view is that we are likely to see a US recession in 2020, we can start the clock until rate cuts, not rate hikes, and towards more QE and a larger Fed balance sheet, not a smaller one. Luckily, of course, the ECB have just laid out the intellectual ground for the Fed to claim that they will be reducing inequality by doing so. I can smell the pitchforks and burning torches from here.

In short, our global institutions, like central banks, are in serious trouble even before we have to deal with a trade war, Hard Brexit, geopolitical risk, the May EU elections, or the next US recession, any of which could happen. Populism is rising, and the Establishment has no idea what to do. Epic market volatility is assured.

Naturally, markets love it today though. More drugs, what’s not to like! Stocks up, bond yields down, and the USD down – for now. Because don’t think this means good things for the rest of the world. That Chinese stimulus had better arrive soon. What used to be capitalism is waiting patiently for what is still closer to communism than the used-to-be capitalists will admit.

via ZeroHedge News http://bit.ly/2sZBnbA Tyler Durden

Wisconsin Republican congressman Sean Duffy recently introduced a bill to give President Trump new powers to raise tariffs in response to actions taken by other individual countries on American goods. This effort to expand the president’s power should make the White House happy, since Trump is eager to see his trade efforts bear fruit. We’ll likely hear about that during his State of the Union address. But as Veronique de Rugy observes, this bill will also move our nation back to the days of the infamous Smoot-Hawley Tariff Act of 1930. In other words, nonsensical protectionist policies won’t make America great again.

Wisconsin Republican congressman Sean Duffy recently introduced a bill to give President Trump new powers to raise tariffs in response to actions taken by other individual countries on American goods. This effort to expand the president’s power should make the White House happy, since Trump is eager to see his trade efforts bear fruit. We’ll likely hear about that during his State of the Union address. But as Veronique de Rugy observes, this bill will also move our nation back to the days of the infamous Smoot-Hawley Tariff Act of 1930. In other words, nonsensical protectionist policies won’t make America great again.

from Hit & Run http://bit.ly/2Gc4Fvr

via IFTTT

As talks in Washington between a delegation of senior US officials led by Trade Representative Robert Lighthizer and a delegation from Beijing led by Vice Premier Liu He enter their second day, President Trump conclusively ruled out the possibility that a deal could be announced by the end of the week in a series of early morning tweets.

The president said that while the negotiations are going “very well,” he said that “no final deal will be made until my friend President Xi, and I, meet in the near future to discuss and agree on some of the long standing and more difficult points.”

China’s top trade negotiators are in the U.S. meeting with our representatives. Meetings are going well with good intent and spirit on both sides. China does not want an increase in Tariffs and feels they will do much better if they make a deal. They are correct. I will be……

— Donald J. Trump (@realDonaldTrump) January 31, 2019

….meeting with their top leaders and representatives today in the Oval Office. No final deal will be made until my friend President Xi, and I, meet in the near future to discuss and agree on some of the long standing and more difficult points. Very comprehensive transaction….

— Donald J. Trump (@realDonaldTrump) January 31, 2019

According to the president, the two sides are seeking a “comprehensive deal” that will leave “NOTHING unresolved”…suggesting that even the more controversial issues like US demands that China end its policy of institutionalized IP theft and cyberespionage activities will be addressed in any final deal.

….China’s representatives and I are trying to do a complete deal, leaving NOTHING unresolved on the table. All of the many problems are being discussed and will be hopefully resolved. Tariffs on China increase to 25% on March 1st, so all working hard to complete by that date!

— Donald J. Trump (@realDonaldTrump) January 31, 2019

Trump is expected to meet with Liu and his delegation at the White House on Thursday afternoon.

via ZeroHedge News http://bit.ly/2GaTrY8 Tyler Durden

In a bid to solidify his legitimacy, Venezuela’s self-proclaimed interim president Juan Guaido has claimed in a New York Times Op-Ed that he and his advisers have “had clandestine meetings with members of the armed forces and the security forces” in Venezuela, offering amnesty to all who are not found guilty of crimes against humanity.

Guaido declared himself interim president of Venezuela last week. Backed by the United States and most of Latin America – and with US-based Venezuelan bank accounts turned over to him, the 35-year-old opposition leader writes that “Maduro no longer has support of the people,” and that his “time is running out.”

“In order to manage his exit with the minimum of bloodshed, all of Venezuela must unite in pushing for a definitive end to his regime.”

Read Guaido’s Op-Ed below:

***

Juan Guaidó Via the New York Times

Juan Guaidó: Venezuelans, Strength Is in Unity

To end the Maduro regime with the minimum of bloodshed, we need the support of pro-democratic governments, institutions and individuals the world over.

CARACAS, Venezuela — On Jan. 23, 61 years after the vicious dictator Marcos Pérez Jiménez was ousted, Venezuelans once again gathered for a day of democratic celebration.

Pérez Jiménez was fraudulently elected by a Constituent Assembly in 1953. His term of office was scheduled to expire in 1958. But rather than calling for free and transparent presidential elections, he was undemocratically re-elected after holding a plebiscite on his administration late in 1957. Following widespread protests and a rupture within the military establishment, the dictator left the country and Venezuela regained its freedom on Jan. 23, 1958.

Once again we face the challenge of restoring our democracy and rebuilding the country, this time amid a humanitarian crisis and the illegal retention of the presidency by Nicolás Maduro. There are severe medicine and food shortages, essential infrastructure and health systems have collapsed, a growing number of children are suffering from malnutrition, and previously eradicated illnesses have re-emerged.

We have one of the highest homicide rates in the world, which is aggravated by the government’s brutal crackdown on protesters. This tragedy has prompted the largest exodus in Latin American history, with three million Venezuelans now living abroad.

I would like to be clear about the situation in Venezuela: Mr. Maduro’s re-election on May 20, 2018, was illegitimate, as has since been acknowledged by a large part of the international community. His original six-year term was set to end on Jan. 10. By continuing to stay in office, Nicolás Maduro is usurping the presidency.

My ascension as interim president is based on Article 233 of the Venezuelan Constitution, according to which, if at the outset of a new term there is no elected head of state, power is vested in the president of the National Assembly until free and transparent elections take place. This is why the oath I took on Jan. 23 cannot be considered a “self-proclamation.” It was not of my own accord that I assumed the function of president that day, but in adherence to the Constitution.

I was 15 when Hugo Chávez came to power in 1998. At the time I lived in Vargas State, which borders the Caribbean. In 1999 torrential rains caused flash floods that left thousands of people dead. I lost several friends, and my school was buried in the mudslide.

The importance of resilience has been etched into my soul ever since. Both of my grandfathers served in the armed forces and they instilled a strong work ethic in their children that helped my family recover from those devastating floods. I saw that if I wanted a better future for my country I had to roll up my sleeves and give my life to public service.

When it became clear that under Chávez the country was drifting toward totalitarianism, I joined the student movement, which played a crucial role in delivering him a decisive loss on a referendum in 2007 that would have granted him sweeping powers. I became involved in local politics and was elected to serve as a deputy representing Vargas State in the National Assembly in 2015.

Editors’ Picks

Can a Church Founded in 1677 Survive the 21st Century?

‘I Feel Invisible’: Native Students Languish in Public Schools

The Insect Apocalypse Is Here

That same generation of brothers and sisters from my student movement days stands alongside me today, as Venezuelans from across the political spectrum are joining in an effort to re-establish democracy. It is incumbent on us to reinstate normality, in order to build the advanced and prosperous country of which we all dream.

But first we must recover our freedom.

The struggle for freedom has been part of our DNA ever since independence was achieved in Latin America 200 years ago. In this century we have taken to the streets repeatedly, knowing that not only is the survival of our democracy at stake, but the very fate of our nation.

A pattern has developed under the Maduro regime. When pressure builds, the first recourse is to repress and persecute. I know this because buckshot pellets fired by members of the armed forces — at peaceful protesters in 2017 — remain lodged in my own body. A minor price to pay compared to the sacrifices made by some of my compatriots.

Under Mr. Maduro at least 240 Venezuelans have been murdered at marches, and there are 600 political prisoners, including the founder of my party, Leopoldo López, who has been a prisoner for five years. When repressive tactics prove futile, Mr. Maduro and his henchmen disingenuously propose “dialogue.” But we have become immune to such manipulation. There are no more stunts left for them to pull. The usurpation of power was their only remaining option.

Given that the Maduro regime cannot legitimately retain power, our response is threefold: First, to shore up the National Assembly as the last bastion of democracy; second, to consolidate the support of the international community, especially the Lima Group, the Organization of American States, the United States and the European Union; and third, to address the people, on the basis that they have a right to self-determination.

Over 50 countries have recognized either me as interim president or the National Assembly as the legitimate authority in Venezuela. I have appealed to António Guterres, the United Nations Secretary General, as well as to several humanitarian agencies, for support in easing the humanitarian crisis. I have begun the process of appointing ambassadors and locating and recovering national assets tied up abroad.

There is a broad consensus among Venezuelans in favor of change: 84 percent of our people reject Mr. Maduro’s rule. We have, therefore, been holding town halls across the country so people can talk openly about the moment in which we find ourselves, and about our future.

The transition will require support from key military contingents. We have had clandestine meetings with members of the armed forces and the security forces. We have offered amnesty to all those who are found not guilty of crimes against humanity. The military’s withdrawal of support from Mr. Maduro is crucial to enabling a change in government, and the majority of those in service agree that the country’s recent travails are untenable.

Mr. Maduro no longer has the support of the people. Last week in Caracas, citizens from the poorest neighborhoods that had been Chavista strongholds in the past took to the streets in unprecedented protests. They went out again on Jan. 23 with the full knowledge that they might be brutally repressed, and they continue to attend town hall meetings.

Mr. Maduro’s time is running out, but in order to manage his exit with the minimum of bloodshed, all of Venezuela must unite in pushing for a definitive end to his regime. For that, we need the support of pro-democratic governments, institutions and individuals the world over. It is imperative that we find effective solutions for the grave humanitarian crisis we are suffering, just as it is to go on building a path toward understanding and reconciliation.

Our strength, and the salvation of all Venezuela, is in unity.

Juan Guaidó is the president of the Venezuelan National Assembly and an opposition leader. This essay was translated from the Spanish by Thomas Bunstead.

via ZeroHedge News http://bit.ly/2UrNzxy Tyler Durden