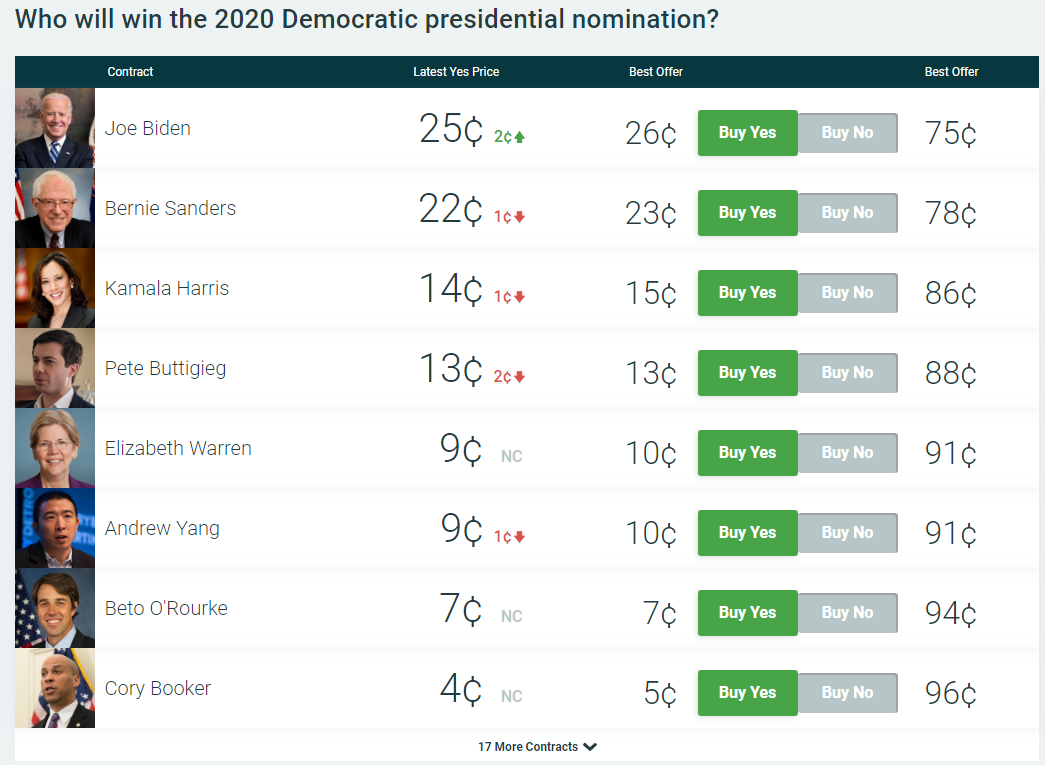

Former Vice President Joe Biden is mopping up at the polls since launching his bid for the Democratic presidential nomination – enjoying a double-digit lead over the rest of the field, according to The Hill, which cites two new national surveys.

A CNN-SRSS poll released early Tuesday reveals that Biden leads Vermont independent Bernie Sanders by 24 points, with 39% of the Democratic electorate vs. 15%. The poll reveals an 11-point surge for Biden over last month, when 28% of Democrats said they would vote for him in the primary.

That said, only 36% of Democrats said they were dead-set on their choice for president, though of those who say they’ve made up their mind, 50% are voting for Biden.

Biden’s lead extends across most every major demographic or political group, though it shrinks some among younger voters (31% Biden to 19% Sanders among those under age 45), liberals (32% Biden to 19% Sanders) and whites (29% Biden to 15% Sanders among white voters).

Still, only about a third of potential Democratic voters with a preference in the race (36%) say they will definitely back the candidate they currently support, 64% say they could still change their minds. Those who say they are locked in are more apt to back Biden: 50% in that group support him, 21% Sanders, 8% Warren. –CNN

A Morning Consult survey, meanwhile, places Biden at 36% vs. 22% for Sanders, a less impressive gain, yet still placing the former VP firmly ahead of the Vermont Senator.

According to online prediction website PredictIt, however, the gap between Biden and Sanders is much narrower.

The next bombshell report to drop from the Justice Department likely will earn none of the breathless fanfare and media coverage that Special Counsel Robert Mueller’s report received, but it could be far more incriminating.

In the next several weeks, Inspector General Michael Horowitz is expected to issue his summation of the potential abuse of the Foreign Intelligence Surveillance Act by top officials in the Obama Administration and holdovers in the early Trump Administration who were overseeing the investigation of Donald Trump’s presidential campaign.

And the perpetrators of the so-called FISAgate scandal now are scrambling for cover as the bad news looms.

Horowitz announced last March that his office would examine the Justice Department’s conduct “in applications filed with the U.S. Foreign Intelligence Surveillance Court (FISC) relating to a certain U.S. person.” That U.S. person is Trump campaign associate Carter Page. In October 2016, just two weeks before the presidential election, the Justice Department submitted an application to the FISC seeking authorization to wiretap Page. The court filing accused Page, a Naval Academy graduate and unpaid campaign advisor, of being an agent of Russia.

The application cited the infamous Steele dossier—unsubstantiated political propaganda that had been funded by the Hillary Clinton campaign and Democratic National Committee—as its primary source of evidence. But the specific political origin of the dossier intentionally was omitted in the court filing. (Robert Mueller similarly tap danced around the role of Fusion GPS, the political consulting firm that hired Christopher Steele to create the dossier. Mueller never mentioned the name “Fusion GPS” in the 448-page document, referring to it only vaguely as “the firm that produced the Steele reporting.”)

Former FBI Director James Comey and former Deputy Attorney General Sally Yates signed the original FISA application. It was renewed three times; subsequent signers included former acting FBI Director Andrew McCabe and Deputy Attorney General Rod Rosenstein. If there’s one document that represents the malevolence, chicanery and arrogance of the original Trump-Russia collusion fraudsters, it’s the Page FISA application.

But—to borrow a favorite term of the collusion truthers—the “walls are closing in” on the FISA abusers.

Representative Mark Meadows (R-N.C.) and James Jordan (R-Ohio) recently met with Horowitz and offered some ominous news for Comey and company: “We anticipate the IG’s report will come out . . . in the next four to six weeks and I think it’s highly likely that we’ll see criminal referrals coming from them,” Meadows told Fox Business host Maria Bartiromo on April 14.

President Trump also speculated that the inspector general’s report would contain damning allegations against former top officials for the world’s most powerful law enforcement agency.

“I think he [Horowitz] knows how big this is,” Trump told Sean Hannity in an interview last week. “The IG report coming out in three or four weeks, from what I hear, is going to be…a blockbuster because he has access to information that most people don’t.” If anyone misled the FISA court, including Comey and Yates, Trump suggested that “they’ll all be in a pile of trouble.”

Since last fall, Trump has threatened to declassify the entire application, much of which is still concealed behind redactions, but that has presumably been delayed to protect the integrity of the investigation. Once the inspector general’s report comes out, however, Trump would be free to unredact crucial portions of the application.

So the targets of the inspector general’s probe and their media pals now are spinning hard in preparation of the report’s release.

Natasha Bertrand, a reliable mouthpiece for Fusion GPS, is smearing Horowitz and raising questions about his investigation. “Former U.S. officials interviewed by the inspector general were skeptical about the quality of his probe,” she wrote in an April 17 piece for Politico. “The inspector general seemed neither well-versed in the FISA process nor receptive to the explanations, the officials said.”

Comey unconvincingly is rejecting accusations by Attorney General William Barr and others that there was “spying” on the Trump campaign. “When I hear that kind of language used, it’s concerning,” serial uptalker Comey said in an April 11 interview. “The FBI and the Department of Justice conduct court-ordered electronic surveillance. I have never thought of that as spying. I don’t know of any court-ordered electronic surveillance aimed at the Trump campaign (emphasis added).”

Yates appeared on Sunday for a softball interview with NBC’s “Meet The Press” host Andrea Mitchell. Without any sense of irony, Mitchell introduced Yates as “someone who seems to show up at key moments in the Trump presidency,” including her central role in the set-up, laughable Logan Act inquiry, and subsequent firing of former National Security Advisor Michael Flynn. (Yates served as acting attorney general for 10 days before Trump fired her for insubordination.)

Yates, much like Comey, has a flair for the dramatic, often using hushed tones, theatrical facial expressions, and overwrought rhetoric to make her point: “When the Russians came knocking at their door, you would think a man who likes to make a show of hugging the flag would have done the patriotic thing and would have notified law enforcement.” (Hard eye roll.)

Yates referred to Trump campaign objections about Russian collusion as “a lie” and (falsely) lamented that “now we have devolved to ‘there’s nothing wrong with taking help,’ illegal help, from a foreign adversary. Surely that’s not where we’ve come to.”

But Yates’ own words might come back to haunt her, and soon.

An April 19 article in the New York Times, which now is backpedaling on the legimitacy of the Steele dossier in advance of the Horowitz report, speculated that the dossier was part of a Russian propaganda campaign targeting the Trump team.

“There has been much chatter among intelligence experts that Steele’s Russian informants could have been pressured to feed him disinformation,” the Times reported. Further, at the time Steele was working for Fusion GPS on Russian-sourced dirt against Trump, he also was lobbying on behalf of Oleg Deripaska, a Russian oligarch with ties to the Kremlin.

So if Yates signed a court document that heavily relied on shady sources and a lobbyist (Steele) for a Putin-connected billionaire, who would be guilty of relying on help from a foreign adversary for political purposes? Not Donald Trump.

The imperious Yates and her accomplices might have a chance to answer that question—and others—in front of Congress in the very near future.

In response to her “Meet the Press” interview, Senator John Cornyn (R-Texas) tweeted that Yates’ actions “will certainly be part of forthcoming Senate Judiciary Committee oversight hearings on FBI/DOJ during Obama years in which she served as Deputy AG under Loretta Lynch.”

The Horowitz report could do what the Mueller report could not: Find legitimate evidence of conspiracies between political operatives, Russian interests, and top government officials; uncover attempts to obstruct justice as the various investigations into misconduct proceeded; and expose rank corruption at the highest levels of a presidential administration.

It just won’t be the presidential administration that Mueller and his colleagues were targeting.

Content created by the Center for American Greatness, Inc. is available without charge to any eligible news publisher that can provide a significant audience. For licensing opportunities for our original content, please contact licensing@centerforamericangreatness.com.

Photo Credit: Thos Robinson/Getty Images for The New Yorker

via ZeroHedge News http://bit.ly/2GS4hSS Tyler Durden

Today is #NationalAdoptAShelterPetDay, so I thought I’d post my own pet proposal for the tax code: a deduction for adopting shelter pets. Right now, many animal shelters are 501(c)(3) charitable organizations, a category that includes corporations or foundations “organized and operated exclusively . . . for the prevention of cruelty to children or animals.” In other words, if dogs or cats are kept in a shelter, the government won’t tax the donations that keep them fed and cared for.

But as soon as those dogs or cats are adopted and go home, the government’s help ends. That doesn’t make much sense, because adoption and home life are much better ways of preventing cruelty than keeping the same animals in shelters forever. And while adopting a pet isn’t purely self-sacrificing—just look at them!—it still performs a service to the pets themselves and to society at large, which the government ought to encourage. (People also love their adopted children, but they still perform a great service by adopting them, which is why the tax code supports adoptions as well as foster homes.)

So my proposal is to amend the Internal Revenue Code to provide a deduction for the ordinary and necessary expenses of caring for a pet adopted from a 501(c)(3)-qualifying shelter. (The deduction could be capped at some predetermined limit, perhaps based on an IRS estimate of the national average.)

Because it would only apply to charitable shelters, the deduction wouldn’t encourage “puppy mills” or breeding for sale. And because it only reduces, rather than eliminates, the expenses of caring for a pet, it wouldn’t be a money-maker for animal hoarders. Instead, it would simply take the support we already give to shelter pets and extend just as much incentive to get them out of the shelters and into loving homes.

Best of all, the proposal has a perfect cringe-inducing and Congress-ready acronym: the “Pet Adoption, Welfare, and Support (PAWS) Act of 2019.” (Attention Hill staffers: imagine your boss’s free local-news airtime for endorsing the PAWS Act from the neighborhood shelter!)

And if any of you do decide to adopt a shelter pet sometime soon, you might be lucky enough to find some like these.

from Latest – Reason.com http://bit.ly/2GK0x4r

via IFTTT

Today is #NationalAdoptAShelterPetDay, so I thought I’d post my own pet proposal for the tax code: a deduction for adopting shelter pets. Right now, many animal shelters are 501(c)(3) charitable organizations, a category that includes corporations or foundations “organized and operated exclusively . . . for the prevention of cruelty to children or animals.” In other words, if dogs or cats are kept in a shelter, the government won’t tax the donations that keep them fed and cared for.

But as soon as those dogs or cats are adopted and go home, the government’s help ends. That doesn’t make much sense, because adoption and home life are much better ways of preventing cruelty than keeping the same animals in shelters forever. And while adopting a pet isn’t purely self-sacrificing—just look at them!—it still performs a service to the pets themselves and to society at large, which the government ought to encourage. (People also love their adopted children, but they still perform a great service by adopting them, which is why the tax code supports adoptions as well as foster homes.)

So my proposal is to amend the Internal Revenue Code to provide a deduction for the ordinary and necessary expenses of caring for a pet adopted from a 501(c)(3)-qualifying shelter. (The deduction could be capped at some predetermined limit, perhaps based on an IRS estimate of the national average.)

Because it would only apply to charitable shelters, the deduction wouldn’t encourage “puppy mills” or breeding for sale. And because it only reduces, rather than eliminates, the expenses of caring for a pet, it wouldn’t be a money-maker for animal hoarders. Instead, it would simply take the support we already give to shelter pets and extend just as much incentive to get them out of the shelters and into loving homes.

Best of all, the proposal has a perfect cringe-inducing and Congress-ready acronym: the “Pet Adoption, Welfare, and Support (PAWS) Act of 2019.” (Attention Hill staffers: imagine your boss’s free local-news airtime for endorsing the PAWS Act from the neighborhood shelter!)

And if any of you do decide to adopt a shelter pet sometime soon, you might be lucky enough to find some like these.

from Latest – Reason.com http://bit.ly/2GK0x4r

via IFTTT

Two weeks ago, Blackrock’s Larry Fink reincarnated the ghost of January 2018 past, when the CEO of the world’s largest manager told CNBC that “we have risk of a melt up.” While it wasn’t quite clear why to Fink a melt up is risky, the last time the US stock market experienced the sheer, unbridled euphoria of price indiscriminate buying was January 2018 when just days later the S&P tumbled by 10% in the aftermath of the infamous Volmageddon blow up of levered inverse VIX ETNs.

So what is Fink is right and a melt up, similar to the one observed for much of 2016 in the aftermath of the first Shanghai Accord, is on deck? The problem, at least optically, is that active asset managers, virtually all of whom have boycotted the rally ever since last December, will almost certainly not jump into stocks at all time highs, with most of them expecting at least a modest pullback as JPM’s Marko Kolanovic believes. And yet, by definition a melt-up does not end until there is bear capitulation and everyone jumps into the pool.

So there is a bit of a paradox as on one hand buybacks, gamma-imbalanced dealer desks and shorts keep pushing stocks higher even as active investors keep pulling money out of stocks.

This also brings up the question of what is the best way to trade a meltup if one can’t fully allocate capital at all time highs?

One answer to this question comes from Bank of America’s derivatives strategist, Benjamin Bowler, who recommends a trade that generated a 10x return during the last market meltup, back in 10x.

As Bowler writes in a note published overnight, as the S&P 500 enjoys its best start of the year since 1975, investors (many of whom have missed most of the gains) are wondering whether to hop on for the ride or avoid adding risk in case the end of the rally is near. Indeed, the recent “green shoots” in the global economy (not to be confused with the latest batch of distinctly adverse data, including China’s latest PMIs and today’s Chicago PMI in the US) and a benign positioning picture “suggest there may be room for US equities to run further”, according to the BofA strategist.

For instance, Bowler notes that the latest update of BofAML’s Library of Proprietary Indicators shows a bullish shift, led by the recovery/stabilization of global growth indicators. Meanwhile, as BofA’s CIO Michael Hartnett noted last Friday, equity positioning has not kept up with the rally; he argues that “greedy” flows could propel the S&P much beyond 3000, echoing the thesis that Marko Kolanovic has held ever since last October. Furthermore, adding to the “meltup risk”, “Fed tightening seems a thing of the past ‘even against soaring asset prices”, and Brexit and US-China tariffs have loosened their grip on markets for now, essentially minimizing three of last year’s main sources of risk.

The question therefore is simple: can positioning and “less bad” global economic conditions alone continue to push the S&P well past all-time highs? The answer, according to Bowler is that “today’s low volatility backdrop makes hedging upside risk easier, as options are inexpensive and can help avoid having to time the top of the market.”

How? By using short-dated S&P calls to “capture a melt-up without having to time a melt-down.“

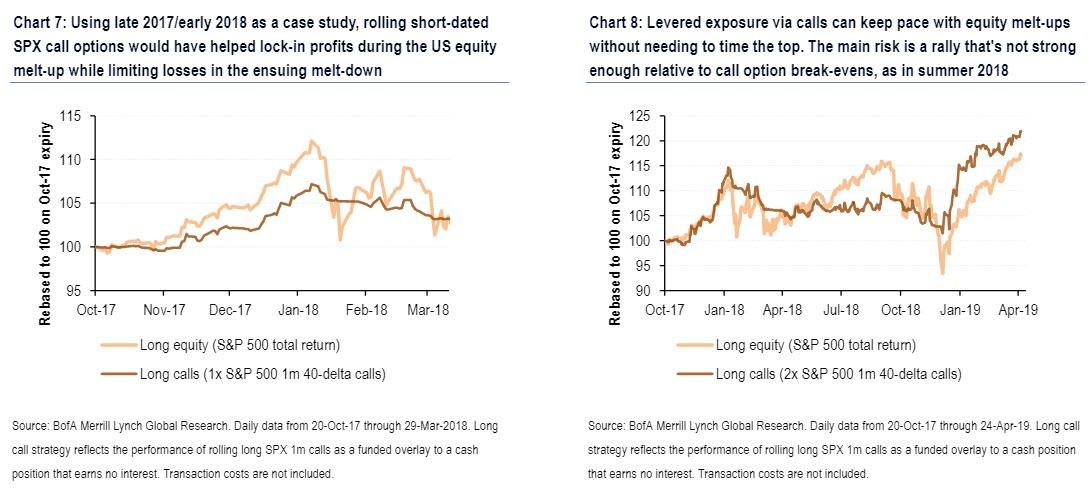

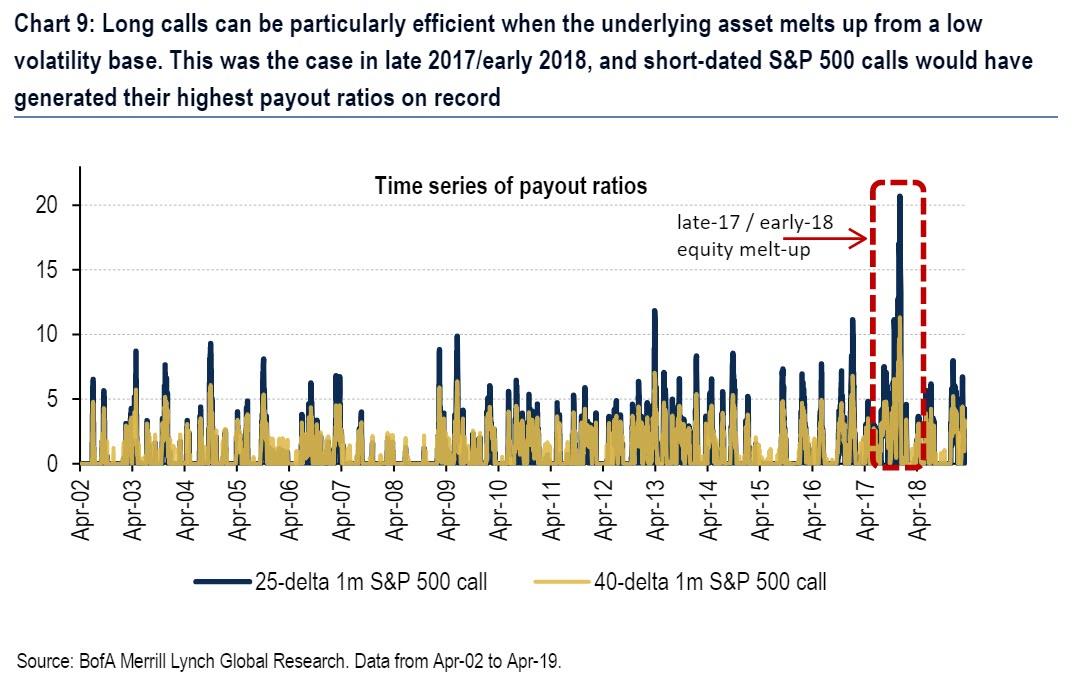

Referring to the behavior of the S&P 500 in late 2017/early 2018 as a case study, Bowler illustrates how “rolling short-dated SPX call options would have helped lock-in profits during the US equity melt-up while limiting losses in the ensuing melt-down.“

Indeed, in what may be the perfect high upside beta, low downside beta hedge, BofA notes that acquiring US equity exposure synthetically via long SPX 1m 40-delta calls would have gained ~7% from Oct-17 through the Jan-18 peak in equities (vs. ~12% for an S&P 500 total return investment) while losing less than 2% during the Feb-18 VIXplosion (as the S&P fell 10% – see Chart 7).

As another example discussed by Bowler and his team, twice the equity exposure via calls (as in Chart 8) would have enabled investors to more than keep pace with the equity melt-up while outperforming delta-one exposure in the Feb-18 and Mar-18 sell-offs. Such a strategy would have again outperformed in the Dec-18 correction and in the ensuing V-shaped recovery in markets in 2019. The main risk as seen from Chart 8 is a period like summer 2018 in which the S&P doesn’t rally strongly enough relative to call option break-evens.

There is an additional kicker that makes this strategy especially lucrative: the recent collapse in the VIX.

Indeed, as shown in Chart 9, readers can see the efficacy of using calls to hedge the risk of an equity melt-up that starts from a low volatility base. What a backtest of this trade shows is that long SPX 1m calls achieved their highest payout ratios on record (data since Apr-02) in the Dec-17/Jan-18 “blow-off top” in US equities, returning between 10x to 20x depending on the exact parametrization.

Not bad for a trade which captures all the upside and is virtually not hurt by the resulting downside. Now the only question is “how can this trade blow up spectacularly.” Unfortunately, on that Bowler had nothing to share.

via ZeroHedge News http://bit.ly/2J2jq5o Tyler Durden

University presses periodically face threats to the financial support they receive from their universities. Such support is crucial, leaders of academic publishing say, because university presses publish work with scholarly significance, knowing that impact must be measured in ideas shared or conventional wisdom challenged, not commercial standards on book sales.

But even if such threats occur periodically, many academics were stunned and angry to learn that Stanford University has announced that it will no longer provide any financial support for its press. Professors at Stanford are pushing back, but there are no signs that the university will reconsider.

Without support from the university, dozens of books released by the press each year would no longer be published.

“At first glance the proposition that a university of Stanford’s stature would voluntarily inflict damage upon an asset like the Stanford University Press seems shockingly improbable. The press is a world-class scholarly publisher with a 125-plus-year history—a global ambassador of the university’s brand,” said Peter Berkery, executive director of the Association of University Presses, via email.

“It appears the Stanford administration is proceeding from the misperception that university presses are self-funding—which, with only a handful of highly circumstantial exceptions, is demonstrably not the case.”

As the Chronicle of Higher Educationexplains (article unfortunately behind paywall), Stanford University Press brings in some $5 million in annual revenue from its books and other publications, but nonetheless depends on the approximately $1.7 million in annual subsidies from the university in order to make ends meet. The article also notes that SUP’s need for subsidies is in part driven by the University’s refusal to allow the Press to raise money from major donors.

The Chronicle reports that Stanford Provost Persis Drell suggested that the money could instead be spent on graduate fellowships. But it also notes that it would in fact fund only about three such fellowships per year. That seems like a small price to pay for continuing one of the world’s leading academic publishers.

The sum of $1.7 million is a lot of money to you and me. But it’s actually a fairly small amount for a university with a massive endowment and a $6.3 billion annual budget. Unlike commercial publishers, academic presses are not intended to make a profit. There task is to publish works that contribute to our knowledge of important issues, but don’t necessarily attract a large readership.

Stanford UP has a well-deserved reputation for being one of the top handful of academic in several fields, including my own fields of law and political economy. Among my favorite significant Stanford UP books are Martin Redish’s Judicial Independence and the American Constitution and Terry Anderson and Peter Hill’s The Not So Wild, Wild West: Property Rights on the Frontier. The latter book reshapes our understanding of both the “Wild West” (showing it was a lot more orderly than its image suggests) and the creation of property rights (which is far less dependent on government than usually thought). We need more works like these, not fewer.

Admittedly, I am not a completely disinterested observer. My first book as a law professor, Democracy and Political Ignorance: Why Smaller Government is Smarter, was published by Stanford UP in 2013, and has since been widely reviewed, published in a revised second edition, and translated into Italian and Japanese. Stanford took a risk on an ambitious proposal by an academic with little track record for writing books. Importantly, they also agreed to set a relatively low price for the book (going against the standard practice of many other academic publishers), which made it accessible to buyers other than libraries and academics with substantial expense accounts.

Thanks in part to the pricing decision, Democracy and Political Ignorance sold thousands of copies and attracting attention in media outlets around the world. It’s an example of SUP’s willingness to proceed with projects that might otherwise have been overlooked. It is also, of course, an example of their laudable willingness to publish books that advocate positions at odds with prevailing political opinion in the academic world, and among most of the Press’s own editorial staff. Anderson and Hill’s excellent book, mentioned above, is another example of SUP’s commitment to ideological diversity.

While my SUP book had the good fortune to turn a profit, many worthwhile academic books, however, are unlikely to be profitable in the same way. Their audiences may be unavoidably limited to experts in the relevant field.

I should add, also, that SUP’s editorial and production work on my book—led by law and anthropology editor Michelle Lipinski—was exemplary. Since 2013, I have had the opportunity to work with several other leading academic publishers, and I know whereof I speak on this point. I have heard similar praise from other SUP authors.

Stanford is a private organization and has the right to set spending priorities as it wishes. Reasonable people can disagree about the value of some of SUP’s specific expenditures and publication decisions. But largely gutting Stanford University Press would be a major mistake.

from Latest – Reason.com http://bit.ly/2Lfy1NO

via IFTTT

University presses periodically face threats to the financial support they receive from their universities. Such support is crucial, leaders of academic publishing say, because university presses publish work with scholarly significance, knowing that impact must be measured in ideas shared or conventional wisdom challenged, not commercial standards on book sales.

But even if such threats occur periodically, many academics were stunned and angry to learn that Stanford University has announced that it will no longer provide any financial support for its press. Professors at Stanford are pushing back, but there are no signs that the university will reconsider.

Without support from the university, dozens of books released by the press each year would no longer be published.

“At first glance the proposition that a university of Stanford’s stature would voluntarily inflict damage upon an asset like the Stanford University Press seems shockingly improbable. The press is a world-class scholarly publisher with a 125-plus-year history—a global ambassador of the university’s brand,” said Peter Berkery, executive director of the Association of University Presses, via email.

“It appears the Stanford administration is proceeding from the misperception that university presses are self-funding—which, with only a handful of highly circumstantial exceptions, is demonstrably not the case.”

As the Chronicle of Higher Educationexplains (article unfortunately behind paywall), Stanford University Press brings in some $5 million in annual revenue from its books and other publications, but nonetheless depends on the approximately $1.7 million in annual subsidies from the university in order to make ends meet. The article also notes that SUP’s need for subsidies is in part driven by the University’s refusal to allow the Press to raise money from major donors.

The Chronicle reports that Stanford Provost Persis Drell suggested that the money could instead be spent on graduate fellowships. But it also notes that it would in fact fund only about three such fellowships per year. That seems like a small price to pay for continuing one of the world’s leading academic publishers.

The sum of $1.7 million is a lot of money to you and me. But it’s actually a fairly small amount for a university with a massive endowment and a $6.3 billion annual budget. Unlike commercial publishers, academic presses are not intended to make a profit. There task is to publish works that contribute to our knowledge of important issues, but don’t necessarily attract a large readership.

Stanford UP has a well-deserved reputation for being one of the top handful of academic in several fields, including my own fields of law and political economy. Among my favorite significant Stanford UP books are Martin Redish’s Judicial Independence and the American Constitution and Terry Anderson and Peter Hill’s The Not So Wild, Wild West: Property Rights on the Frontier. The latter book reshapes our understanding of both the “Wild West” (showing it was a lot more orderly than its image suggests) and the creation of property rights (which is far less dependent on government than usually thought). We need more works like these, not fewer.

Admittedly, I am not a completely disinterested observer. My first book as a law professor, Democracy and Political Ignorance: Why Smaller Government is Smarter, was published by Stanford UP in 2013, and has since been widely reviewed, published in a revised second edition, and translated into Italian and Japanese. Stanford took a risk on an ambitious proposal by an academic with little track record for writing books. Importantly, they also agreed to set a relatively low price for the book (going against the standard practice of many other academic publishers), which made it accessible to buyers other than libraries and academics with substantial expense accounts.

Thanks in part to the pricing decision, Democracy and Political Ignorance sold thousands of copies and attracting attention in media outlets around the world. It’s an example of SUP’s willingness to proceed with projects that might otherwise have been overlooked. It is also, of course, an example of their laudable willingness to publish books that advocate positions at odds with prevailing political opinion in the academic world, and among most of the Press’s own editorial staff. Anderson and Hill’s excellent book, mentioned above, is another example of SUP’s commitment to ideological diversity.

While my SUP book had the good fortune to turn a profit, many worthwhile academic books, however, are unlikely to be profitable in the same way. Their audiences may be unavoidably limited to experts in the relevant field.

I should add, also, that SUP’s editorial and production work on my book—led by law and anthropology editor Michelle Lipinski—was exemplary. Since 2013, I have had the opportunity to work with several other leading academic publishers, and I know whereof I speak on this point. I have heard similar praise from other SUP authors.

Stanford is a private organization and has the right to set spending priorities as it wishes. Reasonable people can disagree about the value of some of SUP’s specific expenditures and publication decisions. But largely gutting Stanford University Press would be a major mistake.

from Latest – Reason.com http://bit.ly/2Lfy1NO

via IFTTT

Just in case he hadn’t already made his position re: interest rates clear to the FOMC, President Trump apparently wanted to make sure policy makers knew their place shortly after the beginning of their two-day policy meeting on Tuesday.

After calling for QE4 and rate cuts earlier this month, Trump is now calling on the central bank to slash interest rates by a full percentage point, which would bring the Fed funds target rate back to 1.25%-1.5%, a level it hasn’t seen in more than a year.

Trump also praised Beijing’s latest massive credit injection (which apparently wasn’t enough to stave, and despite surprisingly strong Q1 GDP growth, “with our wonderfully low inflation, we could be setting major records and at the same time make our national debt start to look small.”

Of course, during its last meeting, Jerome Powell made clear that the central bank would ‘pause’ its rate-hike plans for at least the duration of this year.

China is adding great stimulus to its economy while at the same time keeping interest rates low. Our Federal Reserve has incessantly lifted interest rates, even though inflation is very low, and instituted a very big dose of quantitative tightening. We have the potential to go…

….up like a rocket if we did some lowering of rates, like one point, and some quantitative easing. Yes, we are doing very well at 3.2% GDP, but with our wonderfully low inflation, we could be setting major records &, at the same time, make our National Debt start to look small!

Surprisingly, stocks haven’t ramped despite the president moving the goal posts on his rate-cut demands to call for even steeper cuts as US data has at least nominally improved and US stocks have soared to all time highs. A clear pattern has emerged: The higher the highs in stocks, the steeper the cuts in rates.

via ZeroHedge News http://bit.ly/2GUKmCT Tyler Durden

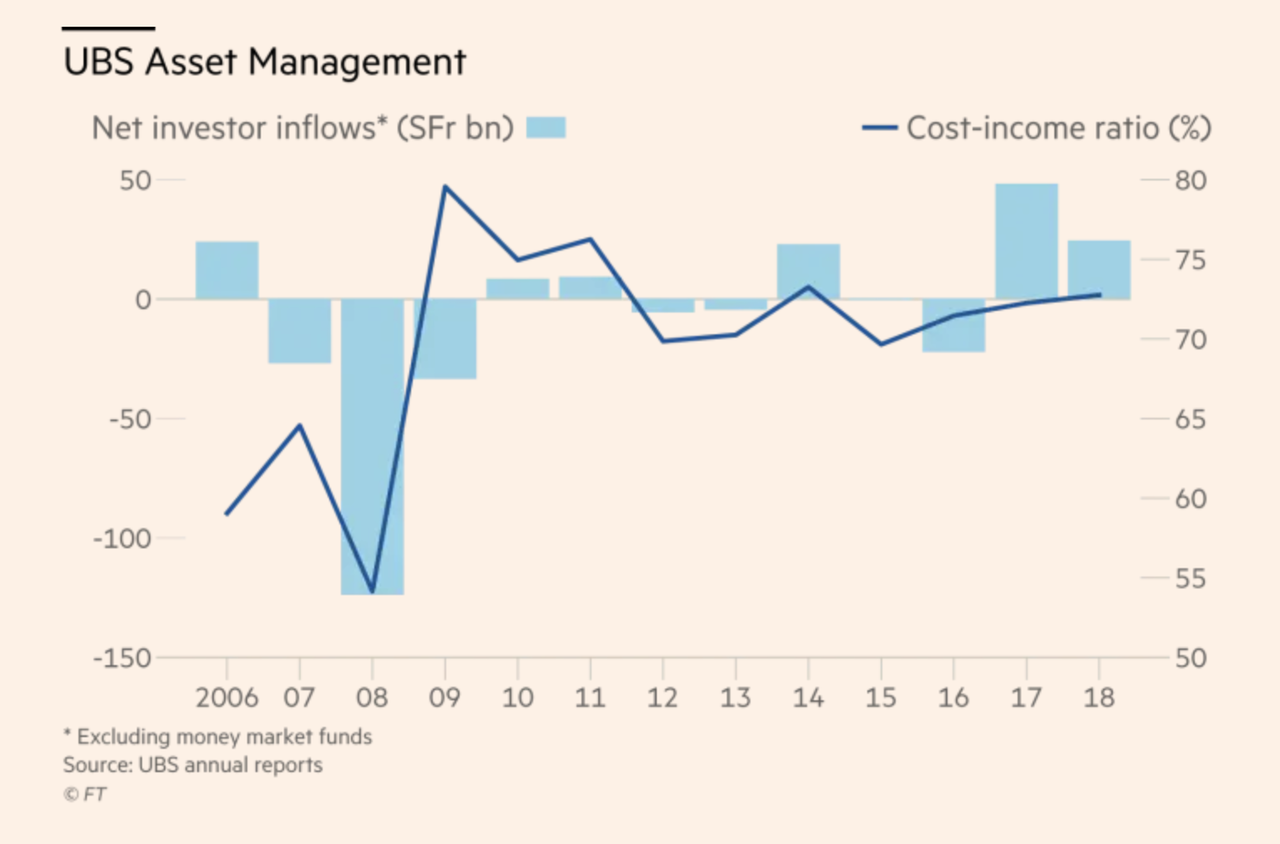

Like the other lagging European investment banks (Deutsche and SocGen immediately spring to mind), UBS is resorting to the last resort of the embattled megabank CEO when shareholders are demanding higher profits ‘or else’.

After a decade where UBS cut thousands of jobs in its investment bank unit, Sergio Ermotti is turning to one of the few business lines where fat can feasibly be cut: UBS’s once legendary asset-management business.

Before the crisis, the Swiss bank held the title of world’s largest asset manager. But it has seen its stature diminish during the intervening years, largely thanks to rise of passive managers like BlackRock (the current title-holder). Though the number of employees at UBS’s asset-management business have declined by one-third since 2006, the cost-to-income ratio has remained stuck at 72.7%, acccording to the FT.

According to Bloomberg, most of these cuts will focus on the unit’s back office, where managers are being told that for ever five employees who leave, they can only hire one to replace them. That’s now an informal rule at the bank, according to BBG’s sources.

For the client-facing employees, the rule is less strict: Managers can hire one employee for every two who leave.

UBS Group AG is telling executives in its large wealth management business to be more selective when hiring bankers as it seeks to cut costs following a challenging first quarter, according to people familiar with the matter.

The bank has introduced an informal rule to allow hiring of one back-office employee only if five are leaving, the people said, asking not to be identified because the matter is private. For client-facing staff, the rule is less strict: Managers can hire one banker for two departing ones, the people said.

Like other banks (for example, State Street), we imagine UBS will try and compensate for the back-office cuts by using automation to streamline workflow.

The bank said earlier this year that it would slow hiring and cut costs as Ermotti warned that this year saw one of the worst first quarter environments in history. When the bank reported earnings, its investment banking revenue took a hit from weak trading revenues, while its asset-management business outperformed thanks to a surprisingly strong pickup in its client business.

However, this hasn’t stopped Ermotti from seeking a tie-up with DWS, the Deutsche Bank-controlled asset manager, which would create, as the FT described it, a new “European champion” better equipped to compete with BlackRock and Vanguard.

via ZeroHedge News http://bit.ly/2GT2RHQ Tyler Durden

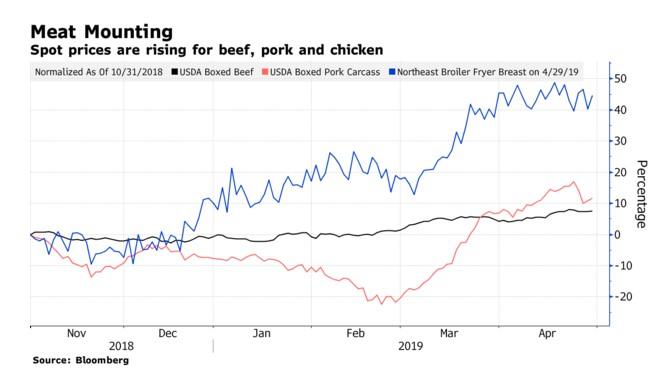

Just hours after IMF Director Christine Lagarde got done telling the world that “everybody” would like a little more inflation, McDonald’s warned investors on Tuesday that it could be under pressure from commodity costs in the U.S. rising as much as 3% – higher than the 1% to 2% inflation that it had forecast just three months ago. In fact, the dining industry as a whole is reeling under the same pricing pressure, according to Bloomberg.

BJ’s Restaurants Inc. is expecting higher pork prices and Yum China Holdings Inc. told investors that rising poultry costs will hit their margins for the rest of the year. These worries come on top of a cost concerns about a rise in the minimum wage.

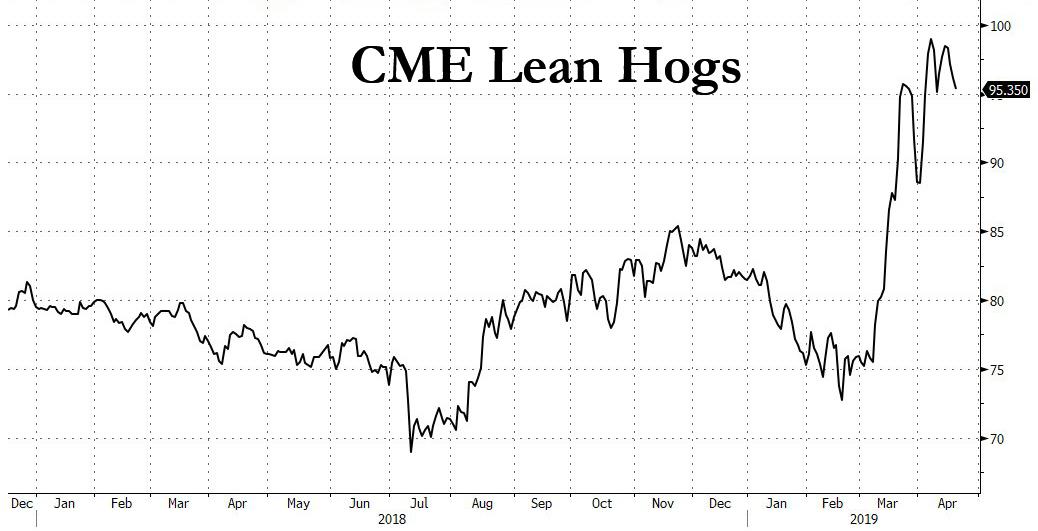

The rise in meat prices has been largely driven by the swine fever that is decimating China’s hog population. Processors around the world have been trying to make up for the shortages caused by the outbreak, but prices have spiked nonetheless. As companies look to substitute pork with more chicken and beef, those prices have also risen.

At Texas Roadhouse Inc., the price hikes have already hit the menu, with customers paying as much as 3% more to help the company try to offset its costs. President Scott Colosi said: “That’s going to go a long ways on margins.”

And so it seems that just about “everybody” in the industry is recognizing these signs of inflation – except, of course, for people like Jerome Powell, Christine Lagarde and other central bankers.

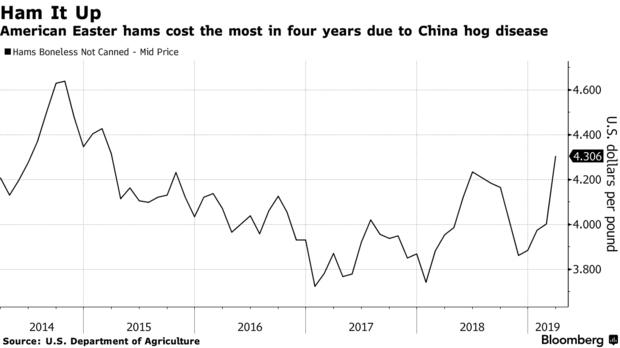

We reported back in mid April that pork prices were starting to rise as a result of the swine flu in China. Six weeks ago we reported that US federal agents seized 1 million pounds, or 454 metric tons, of pork smuggled from China to the same port amid growing fears the meat could contain traces of the African swine fever virus that has ravaged the Asian country’s hog herd.

As the disease continued to spread throughout China – the world’s largest producer and consumer – we predicted the trend would only get worse, which it has. US retail prices for boneless hams hit $4.31 per pound in March, the highest since 2015.

In the European Union, wholesale pig prices have climbed 16% in two months, while lean hog futures traded on the CME are higher by 32% since the February lows.

This is on top of the fact that Americans are already paying more for everyday items like beverages and diapers, according to a recent analysis In our prior note about Lagarde’s comments, we noted that most working people are already struggling to process the inflation in health-care costs, tuition, rent and other necessities that have hammered the standard of living in the developed world.

But as we know, inflation, like every other basic economic “mystery” that the Fed tries fruitlessly to understand, will only wind up being an issue after it’s too late to correct the problem.

via ZeroHedge News http://bit.ly/2GVzPYa Tyler Durden