Elizabeth Warren likes to say she’s a champion of the little guy. But she recently announced a major policy proposal to provide more than a trillion dollars in aid. Much of that money would disproportionately benefit the relatively well off and well connected.

The idea is to eliminate student debt up to $50,000 for people with households incomes under $100,000, and more limited debt cancellation for households between $100,000 and $250,000 a year. By her own estimates, the full plan, which also includes funds for Pell Grants and historically black colleges, would cost about $1.25 trillion.

But the nature of college attendance and student loans means that Warren’s loan forgiveness plan is actually a massive giveaway to the relatively well-off.

Only about a third of people over 25 have a college degree, making them a comparatively elite group, whose elite status is reinforced by, among other things, the connections they make while at college.

College graduates earn about $1 million more during their lifetimes than non-college graduates, according to a Georgetown University study. A separate study from Pew found college graduates typically earn about $17,500 more annually than people who only had high school degrees.

College graduates aren’t, for the most part, super rich. But generally speaking, they are far more comfortable than the majority who lack such degrees. And while many of the people who would benefit from the plan currently have modest incomes, that’s partly because many of them are young people with relatively high future earnings potential. This is a plan that would spend taxpayer money to benefit them.

Warren’s defendersmight respond that it’s still a downward transfer, since the whole thing will be paid for by a new tax on the super wealthy.

There are, however, a few problems with using a wealth tax as a financing mechanism.

The first is that the tax might not be constitutional. Even if it is, another problem is that it’s likely to raise far less money than projected. That’s why most countries that have tried wealth taxes over the last two decades have abandoned them.

The third, as the The Washington Examiner‘s Philip Klein points out that, is that Warren has also suggested that this same revenue tax could be used to help pay for a whole slew of other progressive policy ideas. Those include Medicare for All, the Green New Deal, and subsidized child care, which, all together, would cost tens of trillions of dollars—far more than even the most generous wealth tax would raise.

Ultimately, what Warren wants to do is tax the wealthy to help the merely well off, rather than prioritize programs that help the truly needy. Warren isn’t helping the little guy—she’s helping the folks already on top stay that way.

Music: Pomp and Circumstance, by Edward Elgar. Performed by Eastern Wind Symphony. Path to Follow—Jingle Punks https://youtu.be/CEek1N4wSHA

Produced by Todd Krainin. Written and narrated by Peter Suderman.

In most ways, yesterday’s Congressional Budget Office (CBO) report on single-payer health care looks scrupulously neutral. It takes no position on the merits of single payer, which is often popularly referred to as Medicare for All. It does not estimate the costs or budgetary effects of the single payer plans proposed by liberal lawmakers like Sen. Bernie Sanders (I–Vt.) and Rep. Pramila Jayapal (D–Wash.).

Instead, the CBO report acts as an introduction to the many questions that would need to be resolved in order for such a system to be put in place. It highlights the obstacles standing between where we are now and a single-payer system, and the potential consequences—to both individual patients and taxpayers writ large—of the various tradeoffs required to get there.

By simply raising these questions, the CBO report serves as a sober and practical guide to single-payer skepticism.

The report portrays any potential move to single-payer health care—in which the federal government would run a national health plan that acts as the primary financier of most health care services in the country—as a huge and difficult undertaking. “The transition toward a single-payer system could be complicated, challenging, and potentially disruptive,” it says, before laying out several of the major decisions that would have to be made, such as the speed at which individuals would be expected to move to the new government-run plan (a recent plan backed by Democrats in the House called for a two-year transition), and what to do about job losses in the health insurance industry.

The transition process, however, is not the primary focus of the report, most of which is devoted to laying out the various policy considerations and specific choices that would be involved in designing a single-payer system. These questions can seem wonky and bureaucratic. But what the report drives home is that the dry, wonky stuff would have significant effects on the quality, value, and availability of care that patients could expect to receive.

For example, what would happen when the expansion of health coverage inevitably increased the demand for health care? More people with insurance would invariably mean more people trying to access medical services, posing a challenge to the system. “Whether the supply of providers would be adequate to meet the greater demand would depend on various components of the system, such as provider payment rates,” the report says. “If the number of providers was not sufficient to meet demand, patients might face increased wait times and reduced access to care.”

Single payer plans like the one proposed by Bernie Sanders typically assume that the new system would pay something like today’s Medicare rates, which are often quite a bit lower than those paid by private coverage. So the delivery infrastructure, from hospitals to doctors offices to emergency rooms, would face a dual shock—lower rates to providers on the one hand, greater demand on the other—that would likely result in longer waits for care. That’s hardly surprising, given that long wait times are a frequent complaint in countries like Canada, which has single-payer, and Britain, which runs a fully socialized health care system.

Moving to a single-payer system would also risk depriving patients of choice and individual customization. Compared with today’s arrangement, “the benefits provided by the public plan might not address the needs of some people,” and a “public plan might not be as quick to meet patients’ needs, such as covering new treatments.”

Questions about what is covered, and how much the government pays for particular products and services, would, in a government-run, taxpayer-financed system, inevitably become political, which is to say politicized, decisions: “A single-payer system would also need a way to decide which new treatments and technologies it would cover.”

These decisions would necessarily become political decisions in part because they would have implications for the program’s overall cost. Covering more services would be more expensive; covering fewer would place limits on the types of care people receive.

Policymakers might respond by, say, requiring no cost sharing for some types of treatments deemed better values, while requiring patients to contribute out of pocket for others. But that, in itself, is a judgment call, and would have consequences of its own, pushing people into one type of care that bureaucrats and politicians view as preferable. Or, as CBO puts it, “because some judgment would be required to determine the value of services, some of those determinations would be imperfect, and the use of value-based insurance design would increase the administrative complexity and costs of the single-payer system.” No doubt the lobbying surrounding these judgments would be intense, as health providers jockeyed for bureaucratic favoritism.

Cost, of course, would be a major point of contention for any single payer system, and the Medicare for All plans have so far largely avoided the question, issuing lists of “pay-fors” without specifying exactly how (or if) the enormous price tag would be offset. Multiple estimates have put the additional cost to the government at around $32 trillion, which would require more than doubling federal corporate and individual taxes to pay for. Single-payer advocates tend to argue that this actually represents a savings, since although government spending would increase, total national spending on health care would be somewhat lower.

But CBO’s report casts doubt on whether those savings would actually occur. “Total national health care spending under a single-payer system might be higher or lower than under the current system,” it says, “depending on the key features of the new system, such as the services covered, the provider payment rates, and patient cost-sharing requirements.” Some of the ideas favored by single-payer supporters, like negotiating for prescription drugs, might not pay off, because in a nationwide system, it would be difficult for policymakers to refuse to cover certain drugs. “It is uncertain whether the single-payer plan could use the threat of excluding certain drugs from the formulary as a negotiating strategy,” the report says. “It is also unclear whether a single-payer system could withstand the political pressure that might result from excluding some drugs. By contrast, private insurers can threaten to exclude drugs from their formularies and can follow through on that threat.” Without competition from private plans, drugmakers might have the upper hand in negotiations.

Other countries with single-payer systems allow for private health insurance that works alongside or on top of the government-run plan. Yet the high-profile plans from lawmakers like Sanders and Jayapal would virtually wipe out private health insurance in the space of just a few years.

The CBO report offers an overview of numerous other, often technical questions, from who owns hospitals to what sort of payment scheme—global budgets? Fee for service? Capitated payments?—would be used to pay providers. It lays out, in some detail, what international single-payer systems cover, and what they don’t, highlighting the various trade-offs they entail, few if any of which are part of Bernie Sanders’ Medicare for All plan. Certainly, these trade-offs are not part of the way he advertises it.

What the CBO report shows, in other words, is that designing and implementing a single-payer health care system would be enormously difficult as both a pragmatic and political matter. It’s a warning, in a way, about the scale, scope, and likely consequences of the challenge.

If anything, the report, which at just 34 pages is more of an overview than a deep dive, probably understates the challenge. But it asks many of the right questions, and in doing so, makes clear that there are no easy answers.

from Latest – Reason.com http://bit.ly/2vAasV6

via IFTTT

Watching US equities drop after Chair Powell’s press conference today, I could not help but think back almost 19 years, to 2 separate interactions I had in 2000 with my former employer Steve Cohen and equally famous hedge fund manager Lee Cooperman. The turn of the millennium was a watershed year for domestic stocks. The dot com bubble was starting to burst, but Fed Funds sat at 6.5% from June to December, the highest levels since 1991. Markets wanted either a cut or at least some reassurance the Fed Put was still in place.

On one FOMC meeting day that year, Steve had set up very short. Since everyone in the room got to see his positions, we all knew that and almost everyone was therefore short as well. The old trading room at SAC was quite small, so the energy going into the day was palpable. The best trader in the world had a point of view, and we were all going to end the day with a nice gain by piggybacking on his insight.

Except the day didn’t start off as expected. Stocks rallied at the open and all morning long. By 11am the room was sitting on a major loss. Steve was quiet – he usually was – but he knew if he just sat around waiting until 2pm he would be tempted to change his mind.

So Steve left the desk, something that rarely happened, and went downstairs to the cafeteria to have lunch with his family. I can still remember catching a glimpse of him at a large table with his wife and children, happily distracted by their presence and munching on some fish sticks. Yes, billionaires eat fish sticks…

As 2pm neared and with Steve back on the desk, things still weren’t going well. The market had continued its ascent. The Fed decision crossed the tape – no rate cut – but stocks rose further still. If you’ve never seen 30 traders anxiously trying not to stare at their P&Ls and wondering if their leader has lost his edge, I don’t recommend the experience. The only sound was Steve’s trading assistant calling out ever-higher S&P levels.

But then, around 230pm stocks stopped going up. And then it started to drop. At first just a little, and then more of a plummet. Everyone started to breath again. Steve, of course, looked exactly the same. Aside from needing a little lunchtime breather, things had worked out the way he thought.

As he left the room at 4pm, all he said to us was “That’s how you do it, boys… Have a good night.” We gave him a standing ovation. He waved on his way out the door.

The setting for the other story was an idea dinner at a steak place in Manhattan. The attendees were a bunch of hedge fund analysts and PMs, and for whatever reason Lee Cooperman – famous in NY hedge fund circles even then – thought this event was the best use of early evening hours.

Most of the conversation revolved around how much the Fed could actually do to stabilize the stock market and US economy. The consensus among the attendees – none over 40 years old save Lee – was that the Fed was powerless. The bubble was too big, animal spirits too lofty, and the US economy too exposed to the equity wealth effect.

Cooperman was quiet through this debate, but as he stood up to go he said to the table “All very interesting, but you don’t want to live in a world where the Fed can’t impact stock prices. Good night.” And with that, he was gone.

It has been a long time since those two events, but for me they bookend how I think about the role of the Fed in setting asset prices:

For a trader, the Fed is a catalyst like any other. You analyze the prevailing market narrative and decide if the event (an FOMC meeting) will live up to expectations.

Today was a perfect example of that. As we outlined last night, everything from 2-year yields to Fed Funds Futures were signaling a more dovish Fed anxious to spur inflation. Chair Powell isn’t ready to go there, so markets dropped after the press conference.

Investors are more concerned with how the Fed sees the general level of stock prices and, just as importantly, the volatility of those prices. The Fed Put is more about the CBOE VIX Index than whether the S&P is at 2500 or 3000. We saw that well enough in December/January.

Summing up: when it comes to how one should “trade the Fed”, perspective and conviction are everything. The trader will see today’s action as a sign markets were overconfident in a dovish Fed. The investor will look at Fed Funds Futures still putting +50% odds on a rate cut this year and 10-year Treasuries at 2.5% and see indications that the Fed is still in their corner.

via ZeroHedge News http://bit.ly/2VDKrmx Tyler Durden

In most ways, yesterday’s Congressional Budget Office (CBO) report on single-payer health care looks scrupulously neutral. It takes no position on the merits of single payer, which is often popularly referred to as Medicare for All. It does not estimate the costs or budgetary effects of the single payer plans proposed by liberal lawmakers like Sen. Bernie Sanders (I–Vt.) and Rep. Pramila Jayapal (D–Wash.).

Instead, the CBO report acts as an introduction to the many questions that would need to be resolved in order for such a system to be put in place. It highlights the obstacles standing between where we are now and a single-payer system, and the potential consequences—to both individual patients and taxpayers writ large—of the various tradeoffs required to get there.

By simply raising these questions, the CBO report serves as a sober and practical guide to single-payer skepticism.

The report portrays any potential move to single-payer health care—in which the federal government would run a national health plan that acts as the primary financier of most health care services in the country—as a huge and difficult undertaking. “The transition toward a single-payer system could be complicated, challenging, and potentially disruptive,” it says, before laying out several of the major decisions that would have to be made, such as the speed at which individuals would be expected to move to the new government-run plan (a recent plan backed by Democrats in the House called for a two-year transition), and what to do about job losses in the health insurance industry.

The transition process, however, is not the primary focus of the report, most of which is devoted to laying out the various policy considerations and specific choices that would be involved in designing a single-payer system. These questions can seem wonky and bureaucratic. But what the report drives home is that the dry, wonky stuff would have significant effects on the quality, value, and availability of care that patients could expect to receive.

For example, what would happen when the expansion of health coverage inevitably increased the demand for health care? More people with insurance would invariably mean more people trying to access medical services, posing a challenge to the system. “Whether the supply of providers would be adequate to meet the greater demand would depend on various components of the system, such as provider payment rates,” the report says. “If the number of providers was not sufficient to meet demand, patients might face increased wait times and reduced access to care.”

Single payer plans like the one proposed by Bernie Sanders typically assume that the new system would pay something like today’s Medicare rates, which are often quite a bit lower than those paid by private coverage. So the delivery infrastructure, from hospitals to doctors offices to emergency rooms, would face a dual shock—lower rates to providers on the one hand, greater demand on the other—that would likely result in longer waits for care. That’s hardly surprising, given that long wait times are a frequent complaint in countries like Canada, which has single-payer, and Britain, which runs a fully socialized health care system.

Moving to a single-payer system would also risk depriving patients of choice and individual customization. Compared with today’s arrangement, “the benefits provided by the public plan might not address the needs of some people,” and a “public plan might not be as quick to meet patients’ needs, such as covering new treatments.”

Questions about what is covered, and how much the government pays for particular products and services, would, in a government-run, taxpayer-financed system, inevitably become political, which is to say politicized, decisions: “A single-payer system would also need a way to decide which new treatments and technologies it would cover.”

These decisions would necessarily become political decisions in part because they would have implications for the program’s overall cost. Covering more services would be more expensive; covering fewer would place limits on the types of care people receive.

Policymakers might respond by, say, requiring no cost sharing for some types of treatments deemed better values, while requiring patients to contribute out of pocket for others. But that, in itself, is a judgment call, and would have consequences of its own, pushing people into one type of care that bureaucrats and politicians view as preferable. Or, as CBO puts it, “because some judgment would be required to determine the value of services, some of those determinations would be imperfect, and the use of value-based insurance design would increase the administrative complexity and costs of the single-payer system.” No doubt the lobbying surrounding these judgments would be intense, as health providers jockeyed for bureaucratic favoritism.

Cost, of course, would be a major point of contention for any single payer system, and the Medicare for All plans have so far largely avoided the question, issuing lists of “pay-fors” without specifying exactly how (or if) the enormous price tag would be offset. Multiple estimates have put the additional cost to the government at around $32 trillion, which would require more than doubling federal corporate and individual taxes to pay for. Single-payer advocates tend to argue that this actually represents a savings, since although government spending would increase, total national spending on health care would be somewhat lower.

But CBO’s report casts doubt on whether those savings would actually occur. “Total national health care spending under a single-payer system might be higher or lower than under the current system,” it says, “depending on the key features of the new system, such as the services covered, the provider payment rates, and patient cost-sharing requirements.” Some of the ideas favored by single-payer supporters, like negotiating for prescription drugs, might not pay off, because in a nationwide system, it would be difficult for policymakers to refuse to cover certain drugs. “It is uncertain whether the single-payer plan could use the threat of excluding certain drugs from the formulary as a negotiating strategy,” the report says. “It is also unclear whether a single-payer system could withstand the political pressure that might result from excluding some drugs. By contrast, private insurers can threaten to exclude drugs from their formularies and can follow through on that threat.” Without competition from private plans, drugmakers might have the upper hand in negotiations.

Other countries with single-payer systems allow for private health insurance that works alongside or on top of the government-run plan. Yet the high-profile plans from lawmakers like Sanders and Jayapal would virtually wipe out private health insurance in the space of just a few years.

The CBO report offers an overview of numerous other, often technical questions, from who owns hospitals to what sort of payment scheme—global budgets? Fee for service? Capitated payments?—would be used to pay providers. It lays out, in some detail, what international single-payer systems cover, and what they don’t, highlighting the various trade-offs they entail, few if any of which are part of Bernie Sanders’ Medicare for All plan. Certainly, these trade-offs are not part of the way he advertises it.

What the CBO report shows, in other words, is that designing and implementing a single-payer health care system would be enormously difficult as both a pragmatic and political matter. It’s a warning, in a way, about the scale, scope, and likely consequences of the challenge.

If anything, the report, which at just 34 pages is more of an overview than a deep dive, probably understates the challenge. But it asks many of the right questions, and in doing so, makes clear that there are no easy answers.

from Latest – Reason.com http://bit.ly/2vAasV6

via IFTTT

Despite another domestic abuse incident, Officer Darren Cachola might once again get to keep his job at the Honolulu Police Department (HPD).

Cachola was arrested Tuesday for felony abuse of an unspecified member in his house. Following his arrest, the Star Adviser revealed a long history of brutality both in Cachola’s professional and personal lives. He once kicked a motorcyclist and broke their ribs during a traffic stop. He was also caught on camera hitting his former girlfriend in the restaurant where she worked at the time.

In 2017, Cachola’s wife told a 911 dispatcher that Cachola was choking her. Police saw red marks around his wife’s neck, but she told the officers that she was not injured and Cachola was never arrested or charged. Instead, he was told to stay away from his wife for 48 hours. The wife later filed a lawsuit alleging that the responding officers discouraged her from filing charges, and instead told her to give a statement that said she merely got into an argument with her husband.

The HPD has attempted to reprimand Cachola for his behavior. The department even fired him in 2015 following the on-camera fight with his girlfriend.

But a union arbitrator fought for Cachola’s reinstatement, which was granted last year. The State of Hawaii Organization of Police Officers filed a complaint with the Hawaii Labor Relations Board to prohibit the details of the decision from becoming public. The board then issued a temporary order against the police chief and city officials to keep the details from being released.

HPD is hardly the first department that’s struggled to get rid of an officer.

In 2018, a magistrate ruled that “Florida’s Worst Cop,” Opa-locka police sergeant German Bosque, was free to return to the police force despite three arrests and six firings over the course of 20 years. Bosque has been accused of “stealing drugs, possessing counterfeit cash, brutalizing suspects and bystanders, lying, insubordination, sexual assault.”

from Latest – Reason.com http://bit.ly/2UUVl31

via IFTTT

Last week, when we showed the latest fund flow data confirming that active, mutual funds have now experienced a virtually non-stop torrent of capital outflows for the past 14 months, with the redeemed funds used to fund ETFs and various other passive, “robotic” investments, we had one piece of simple advice: “learn to code.”

Well, as it so often happens these days, what we thought was sarcastic humor turned out to be the bitter truth just days later, and as Bloomberg reported this morning, two Janues Henderson fund managers, Thomas Hanson and Hartej Singh, have requested to leave the company which until recently employed Bill Gross. They will be replaced by a new quantitative team of four, who will be recruited by the asset manager.

The hiring will “reflect the changing nature of fund management and how greater use of technology, statistical techniques and data management will augment our fundamental processes,” she said.

In short: the hiring will reflect that active, fundamental managers should, well, learn to code, as the only “managers” that matter in this broken, centrally-planned market are those who trade not on fundamentals but on big data, trends, and fund flows, especially that of the Fed.

As a result, Janus Henderson’s global credit team will go to six from eight fund managers (after losing its most notable credit manager, Bill Gross several months earlier). Thomas Hanson, who co-managed the European high-yield and “Credit Alpha” strategies, joined from Legal & General Investment Management in 2015. Hartej Singh has joined Pension Insurance Corporation as a portfolio manager, according to his LinkedIn profile. He was previously co-manager of Janus Henderson’s sterling-denominated credit funds.

As for the real reason why the asset manager is scrambling, Janus Henderson, which was created in the merger between Janus Capital and Henderson Group, suffered its sixth quarter of investor withdrawals in the first three months of this year. Which is why the fund will try anything just to stop the bleeding.

via ZeroHedge News http://bit.ly/300nbi2 Tyler Durden

Despite another domestic abuse incident, Officer Darren Cachola might once again get to keep his job at the Honolulu Police Department (HPD).

Cachola was arrested Tuesday for felony abuse of an unspecified member in his house. Following his arrest, the Star Adviser revealed a long history of brutality both in Cachola’s professional and personal lives. He once kicked a motorcyclist and broke their ribs during a traffic stop. He was also caught on camera hitting his former girlfriend in the restaurant where she worked at the time.

In 2017, Cachola’s wife told a 911 dispatcher that Cachola was choking her. Police saw red marks around his wife’s neck, but she told the officers that she was not injured and Cachola was never arrested or charged. Instead, he was told to stay away from his wife for 48 hours. The wife later filed a lawsuit alleging that the responding officers discouraged her from filing charges, and instead told her to give a statement that said she merely got into an argument with her husband.

The HPD has attempted to reprimand Cachola for his behavior. The department even fired him in 2015 following the on-camera fight with his girlfriend.

But a union arbitrator fought for Cachola’s reinstatement, which was granted last year. The State of Hawaii Organization of Police Officers filed a complaint with the Hawaii Labor Relations Board to prohibit the details of the decision from becoming public. The board then issued a temporary order against the police chief and city officials to keep the details from being released.

HPD is hardly the first department that’s struggled to get rid of an officer.

In 2018, a magistrate ruled that “Florida’s Worst Cop,” Opa-locka police sergeant German Bosque, was free to return to the police force despite three arrests and six firings over the course of 20 years. Bosque has been accused of “stealing drugs, possessing counterfeit cash, brutalizing suspects and bystanders, lying, insubordination, sexual assault.”

from Latest – Reason.com http://bit.ly/2UUVl31

via IFTTT

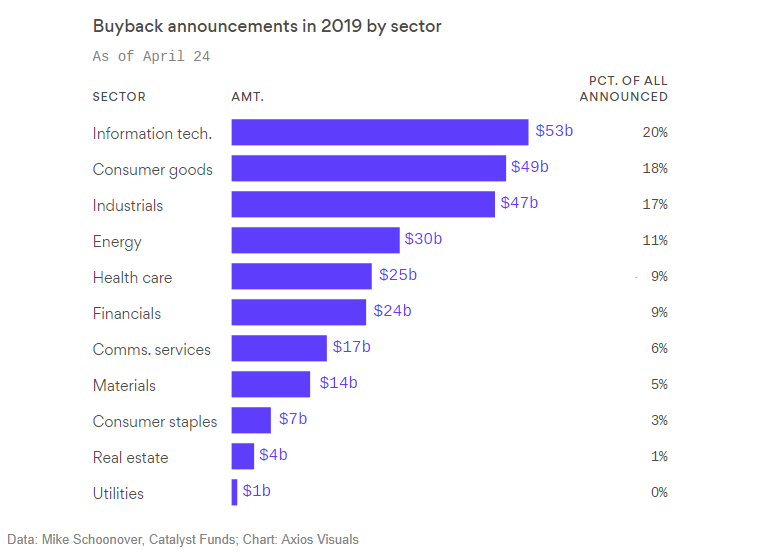

I recently wrote about stock buybacks in our weekly newsletter. However, a recent report from Axios noted that for 2019, IT companies are again on pace to spend the most on stock buybacks this year, as the total looks set to pass 2018’s $1.085 trillion record total.

“By the numbers: Companies so far have spent $272 billion on buybacks, data compiled by Mike Schoonover, COO of Catalyst Funds, for Axios shows.

Between the lines: The amount of spending on buybacks announced by companies in the IT sector has fallen significantly this year as other industries, particularly energy and industrials, have picked up the slack. Companies in those sectors have about doubled their percentage of announced buybacks.

The top 5 sectors for buybacks this year accounted for 76% of the total. Last year, the top 5 sectors accounted for 82%, led by IT, financials, health care, consumer discretionary and industrials, respectively.

Interestingly, buyback spending has not coincided with market performance for most sectors.

As I have shown previously, the runoff in shares outstanding since the financial crisis lows have been nothing short of stunning.

It has been the magnitude of buybacks which have now brought it to the attention of politicians. It is a “political football” perfectly suited for the 2019 primaries as the “wealth gap” in America has become a visible chasm. Debates around share repurchases invoke themes for everyone: shades of corporate greed, historic income inequality, images of populism, and the idea that they’ve propped up the most-hated bull market of all time.

“Politicians like Sens. Elizabeth Warren, Bernie Sanders, Chuck Schumer, and Marco Rubio have derided buybacks’ explosive rise due in large part to the Trump administration’s tax cuts, demanding Congress more fairly regulate what public companies can do with their cash.

“Corporate self-indulgence has become an enormous problem for workers and for the long-term strength of the economy,” Sens. Sanders and Schumer wrote in a New York Times op-ed in February, which was met the following month with an opposing piece in the paper.

The pressure on buybacks, which hit a record $806.4 billion in 2018 according to an estimate from S&P Dow Jones Indices, isn’t expected to let up.”

Where’s The Beef

The buyback boom can be traced back to Bill Clinton’s 1993 attempt to reign in CEO pay. Clinton thought, incorrectly, that by restricting corporations to expensing only the first $1 million in CEO compensation for corporate tax purposes, corporate boards would limit the amount of money they doled out to CEO’s.

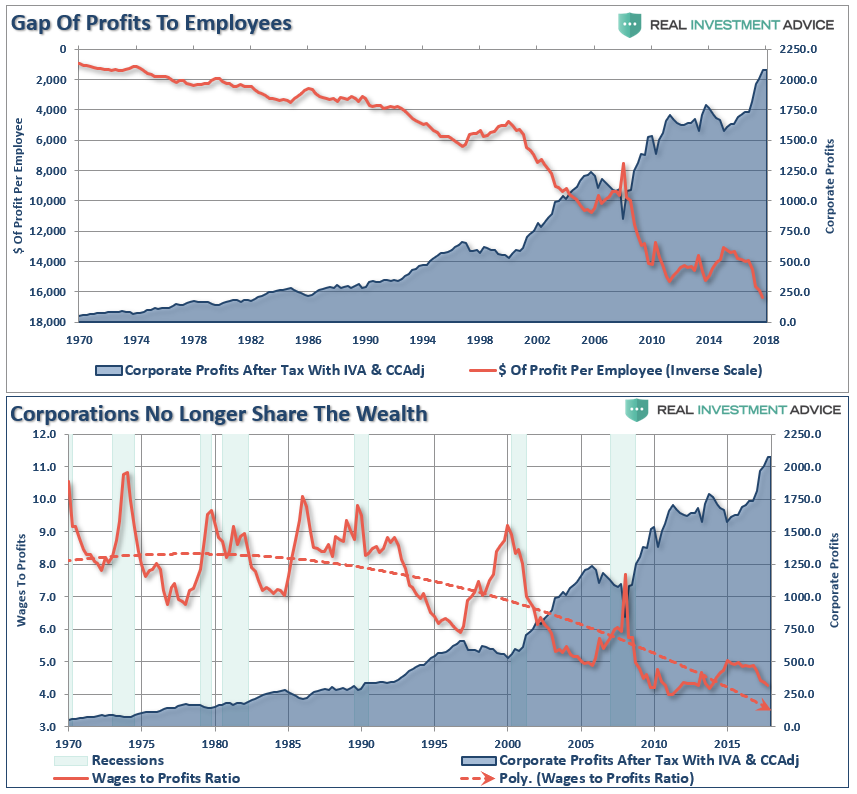

To Bill’s chagrin, corporations quickly shifted compensation schemes for their executives to stock-based compensation. Subsequently, CEO pay rose even higher, and as I showed previously, the gap between profits and wages has become vastly distorted. Rising profitability, fewer employees, and increased productivity per employee has all contributed to the surging “wealth gap” between the rich and the poor.

In 1982, according to the Economic Policy Institute, the average CEO earned 50 times the average production worker.Today, the CEO Pay Ratio’s increased to 144 times the average workerwith most of the gains a result of stock options and awards.

You can understand why it is a political “hot topic” for 2020.

The arguments in support of corporate share buybacks are relatively “thin” in terms of substance.

Limited potential to reinvest for growth. (Least favorable use of cash.)

Management feels the stock is undervalued. (Rarely a consideration)

Buybacks can make earnings and growth look stronger. (Main reason given by firms)

Buybacks are easier to cut during tough times. (Easy to deploy and controlled by the board)

Buybacks can be more tax-friendly for investors. (Rarely a consideration)

Buybacks can help offset stock-based compensation. (Primary use in many cases)

Of the reasons given, the ones which support executive compensation are the most valid.

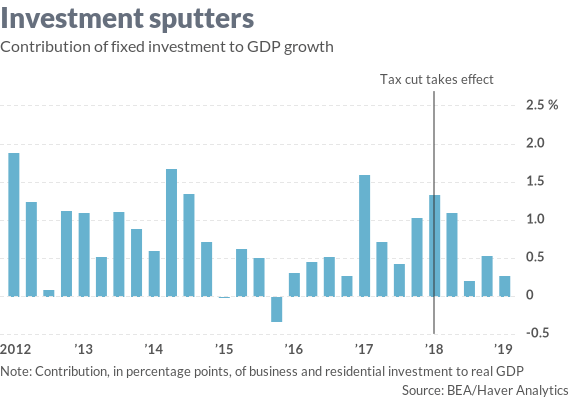

The debate over share repurchases came to the fore following the tax cuts in December of 2017. The bill was targeted at corporations and lowered the tax rate from 35% to 21%. The tax cut plan was “sold” the the American public as a “trickle down” plan and by giving money back to corporations; they would in turn hire more workers, increase wages, and invest in America.

“Kevin Hassett, chairman of the White House Council of Economic Advisers said ‘the gross domestic product report confirms our view that the momentum from last year was not a sugar high but a serious response to long-run policies that have made the U.S. a more attractive place for business.’

There’s just one problem with Hassett’s assessment.

The unexpected strength in the GDP report came from inventories, trade, and state and local government spending, not from business investment, which is where one would expect to see the response to the kind of long-run, supply-side policies Hassett implied.”

Where did the money primarily go? Just one place; share repurchases.

The problem with the surge in share repurchases is that such actions divert ever-increasing amounts of cash from productive investments which ultimately impairs longer-term profit and growth.

“But, corporate profits have been surging.”

Not so much.

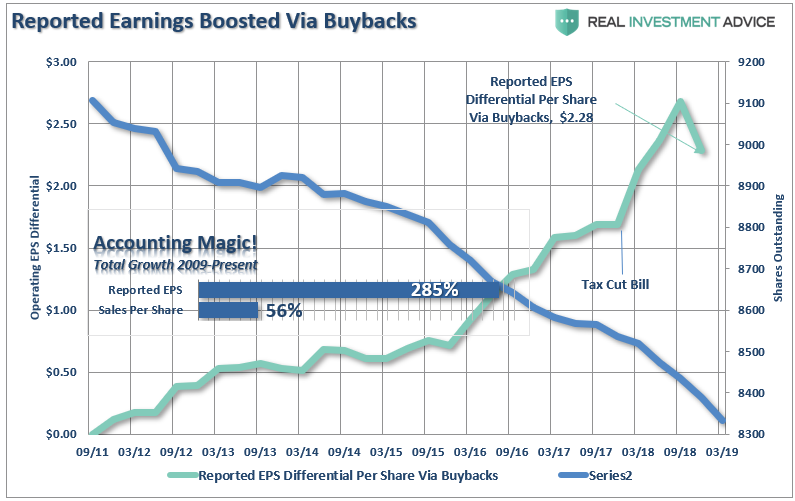

The reality is that stock buybacks create an illusion of profitability. Such activities do not spur economic growth or generate real wealth for shareholders, but it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.

Let’s clear up a myth used to support the benefit of stock buybacks:

“Share repurchases aren’t bad. It is simply the company returning money to shareholders.”

Not really.

Share buybacks only return money to those individuals who sell their stock. This is an open market transaction. For example, Apple (AAPL) just announced they plan to buy $75 billion of their stock back. Via NY Times,

“Apple’s record buybacks should be welcome news to shareholders, as the stock price is likely to climb. But the buybacks could also expose the company to more criticism that the tax cuts it received have mostly benefited investors and executives.”

Let’s clear something up. Buybacks do not RETURN money to shareholders. A dividend does.

The only people who receive any capital from the buyback are those who opt to sell their shares. They have their capital back, but they no longer have the shares. Also, while it is believed that buybacks ALWAYS increase share price, that is not necessarily the case. Apple bought a vast amount of shares back in 2018, the stock lost 15% of its value.

So, who are the ones mostly selling their shares?

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.” – Financial Times

A recent report on a study by the Securities & Exchange Commission found the same:

SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

“The real problem is that buybacks, unlike dividends, can be used to systematically transfer value from shareholders to executives. Researchers have shown that executives opportunistically use repurchases to shrink the share count and thereby trigger earnings-per-share-based bonuses.

Executives also use buybacks to create temporary additional demand for shares, nudging up the short-term stock price as executives unload equity.”

What is clear is that the misuse and abuse of share buybacks to manipulate earnings and reward insiders has become problematic.

Ending The Addiction

Now that you understand the background, and who share buybacks actually benefit, you can understand the reason why this debate has become a much more visible topic heading into the 2020 election cycle.

Most people have forgotten that share repurchases were banned in 1933 following the “Crash of 1929,” until the ban was repealed during the Reagan Administration in 1982.

“Buybacks were illegal throughout most of the 20th century because they were considered a form of stock market manipulation. But in 1982, the Securities and Exchange Commission passed rule 10b-18, which created a legal process for buybacks and opened the floodgates for companies to start repurchasing their stock en masse.”

But more importantly, they are obfuscating the normal functioning of the market relative to price discovery. As John Authers recently pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

The other problem with the share repurchases is that is has increasingly been done with the use of leverage. The explosion of corporate debt in recent years will become problematic during the next recession particularly as the proliferation of sub-investment grade issuers are locked out of the bond market for refinancing activities. As noted by the Bank of International Settlements.

“If, on the heels of economic weakness, enough issuers were abruptly downgraded from BBB to junk status, mutual funds and, more broadly, other market participants with investment grade mandates could be forced to offload large amounts of bonds quickly. While attractive to investors that seek a targeted risk exposure, rating-based investment mandates can lead to fire sales.”

With 62% of investment grade debt maturing over the next five years, there are a lot of companies that are going to wish they didn’t buy back so much stock.

“The corporate resource allocation process is America’s source of economic security or insecurity, as the case may be. If Americans want an economy in which corporate profits result in a shared prosperity, the buyback and executive compensation binges will have to end. As with any addiction, there will be withdrawal pains.”

There aren’t any easy fixes and banning them altogether is probably a “horse that is long gone.”

However, an honest assessment of the abuses, some rule changes in both reporting requirements and timing of sales, as well as potentially some limits on the amounts of annual repurchases could provide a start.

Just like any addiction, it is always better to ween the subject off of the addiction than just going “cold turkey.”

But, like 1929, it will likely be the next major market crash which solves the problem.

via ZeroHedge News http://bit.ly/2UV1NXD Tyler Durden

French protesters, many donning yellow vests, took a bus across the English Channel to protest outside of Julian Assange’s Thursday extradition hearing in London, according to Bloomberg.

Arriving just one day after chaotic May Day clashes with Paris police, the protesters highlighted the growing movement of activists who voicing concern as UK courts gear up to consider a US extradition request for the WikiLeaks founder.

“We came here to show support because Assange represents

part of the information revolution,” said 39-year-old French protester Alice Eff, who said she arrived on an 80-seat bus with other Assange supporters.

WikiLeaks’ release of hundreds of thousands of classified

cables, and war logs from Afghanistan and Iraq had struck a

chord with the movement, she said outside Westminster

Magistrates Court, though there was no formal connection with

the WikiLeaks organization.

American authorities are pursuing extradition so Assange

can face trial on accusations that he conspired with ex-Army

analyst Chelsea Manning to illegally download classified

government material. Eff said she was concerned that the

existing U.S. charge against Assange could be further broadened. –Bloomberg

“We are protesting in France in order to have more democracy and to have more transparency from the government. And that’s what Julian Assange has been fighting for,” one yellow vest protester named Vincent told Sputnik News. “So for us it was obvious to come here and to support him to, just tell him that he is not alone, that there are like hundred thousands of people in France at least and I guess all [over] the world, probably millions, that consider him as a hero for doing what he has done, to sacrifice his own life and his own freedom in order to put out in the public confidential information that… yeah, release critical information that is important for the public to know.”

Assange was arrested by UK authorities on April 11th after Ecuador revoked his political asylum of nearly seven years. He now faces charges in the United States of conspiring with whistleblower Chelsea Manning to break into a Pentagon computer in order to leak classified information. He faces up to 5.5 years in prison if convicted.

The WikiLeaks founder faces another extradition hearing on May 30, and has told the London court that he does not want to be sent to the United States as we reported earlier on Thursday.

Assange, speaking from Belmarsh prison, was wearing a sports jacket and was not handcuffed.

Asked by Judge Michael Snow if he wished to consent to surrender himself for extradition, Assange said: “I do not wish to surrender myself for extradition for doing journalism that’s won many, many awards and affected many people.” -CNN

His appearance came a day after another judge slapped him with a 50-week sentence for skipping bail back in 2012.

As we previewed last night, Wikileaks editor-in-chief Kristinn Hrafnsson said Wednesday that the extradition process is where ‘the real battle begins’ for Assange.

Speaking to CNN after Assange’s bail violation sentencing on Wednesday, WikiLeaks’ Editor-in-Chief Kristinn Hrafnsson said he was “shocked and appalled by this decision to sentence Julian to two weeks short of the maximum sentence for not showing up in court.”

He added that the US extradition claim is “where the real battle begins.”

Assange’s legal team has yet to publicize its defense strategy, but most expect them to argue that the request is politically motivated. Meanwhile, Hrafnsson declared that it’s Wikileaks’ view that the charges cited by the US in the extradition request are merely a ruse, and that Assange will be charged with violating the 1970 Espionage Act once he’s safely on American soil – a charge that could carry the death penalty.

via ZeroHedge News http://bit.ly/2J82RFi Tyler Durden

Just a few short hours after Stephen Moore assured Bloomberg reporters during an interview that “I’m all in” despite the Senate pushback to his Federal Reserve nomination (and notably disagreeing with Trump that a 1% rate-cut was needed), President Trump has just confirmed that Moore has withdrawn his nomination:

Steve Moore, a great pro-growth economist and a truly fine person, has decided to withdraw from the Fed process. Steve won the battle of ideas including Tax Cuts….

….and deregulation which have produced non-inflationary prosperity for all Americans. I’ve asked Steve to work with me toward future economic growth in our Country.

As Jim Rickards previously noted, that if Moore withdraws next or if his nomination is defeated, no worries. There’s some indication that Trump’s next nominee will be Judy Shelton.

She does have a Ph.D. and is a well-known advocate of a new gold standard. Just this Sunday she wrote an article in The Wall Street Journal, “The Case for Monetary Regime Change,” that challenged the current system and defended the classical gold standard.

She has also defended Trump’s trade policies, arguing that those who embrace unfettered free trade dogma “disregard the fact that the ‘rules’ are not working for many American workers and companies.”

For those who wanted Moore to step aside next, the best advice may be “Be careful what you wish for.”

via ZeroHedge News http://bit.ly/2Y0l8Zj Tyler Durden