Would she work with Woody Allen again? She would. I’ve been out of the loop the past few days, in recovery from having two wisdom teeth removed, but in my limited purview the best (and most controversial) thing on the internet in that time has been Vulture‘s interview with actress Anjelica Huston. In a wide-ranging interview conducted by Andrew Goldman, Huston touches on everything from her famous father to why she doesn’t like edibles, how Bill Murray snubbed her on the Life Aquatic set, Oprah’s beef with her, and Jack Nicholson’s cocaine habits.

Of course, the part that’s been generating some of the most attention is Huston saying she would work with Woody Allen again.

You were in two Woody Allen films, Crimes and Misdemeanors, alongside Mia Farrow, and then Manhattan Murder Mystery. Woody Allen is basically unable to make films now because of the outcry about the molestation allegations.

I think that’s after two states investigated him, and neither of them prosecuted him.

Well, the industry seems to be treating him as though he’s guilty. Would you work with him again? Yeah, in a second.

Huston touches on Roman Polanski, too, in what critics have been describing as a “defense” of the disgraced director. But the answer given by Huston—whose “first serious boyfriend” was 42 when she was 18, and who earlier in the interview mentions wishing she could’ve been in Romeo & Juliet as a teen so she could’ve been “off in Italy having a romance on set with Franco Zeffirelli”—is more an offering of context than absolution:

You were arrested because you happened to be in Jack’s house when Roman Polanski raped 13-year-old Samantha Geimer. How did you feel about that? Well, see, it’s a story that could’ve happened ten years before in England or France or Italy or Spain or Portugal, and no one would’ve heard anything about it. And that’s how these guys enjoy their time. It was a whole playboy movement in France when I was a young girl, 15, 16 years old, doing my first collections. You would go to Régine or Castel in Paris, and the older guys would all hit on you. Any club you cared to mention in Europe. It was de rigueur for most of those guys like Roman who had grown up with the European sensibility.

Huston situates Polanski’s attitudes and acts as products of their time period but also not all that different than the attitudes many men in Hollywood have toward women today. Far from downplaying the depravity, she refuses to simply position Polanski and/or that era as an anomaly which we can condemn from a safe and smug distance while congratulating everyone on how far they’ve come:

Among a lot of Hollywood men, it was acceptable at that time to treat women as though they were disposable.

I think they’re still doing it. I was at the hairdresser’s yesterday, and I heard tales of such horror from women. There was one other client and two girls who were working in this rather small hairdressing shop. And one of the girls had been passed a Mickey Finn in a bar and had woken up on a couch with a guy ejaculating wildly all over her face. And as she was telling the story, another girl who worked in the salon came in and said, “The weirdest thing happened to my friend last night. She was found at four in the morning in the Wilshire district, coatless, shoeless, with scratches and bruises all over her body. She doesn’t know whether she was raped. So, I’m trying to stop her from having a bath because we need to get her to the police.”

Later, Goldman asks Huston if she had any “#MeToo experiences”:

Yeah, yeah.

What happened? You’d have to ask me that on a daily basis, practically. That’s how often it happens, that you’re objectified, or misread, or put down. I think men do it a lot, and I don’t really think half the time they know what they’re doing. That’s how inured they are.

Huston goes on to describe Supreme Court Justice Brett Kavanaugh as “all that believable.”

Throughout the interview, her answers are candid and colorful while failing to fall into neat liberal/conservative (or woke/canceled) lines. Ignore the Twitter haters, and read the whole thing for yourself here.

FREE MINDS

FOSTA lawsuit update. The group challenging FOSTA, last year’s law banning prostitution ads, just got a boost from an unlikely source: 21 state attorneys general. Cathy Gellis at Techdirtexplains:

The important thing to remember about this appeal is that the question before the appeals court isn’t really about the constitutionality of FOSTA itself. What’s being appealed is the case having been dismissed for lack of standing by the plaintiffs. The district court never directly ruled on the constitutionality of the law; it only ruled that these plaintiffs had no right to complain about it to the courts. According to the district court these plaintiffs weren’t being hurt, or likely to be hurt, by FOSTA, and so it dismissed their case. What the parties are fighting about now is whether this assessment by the district court was right.

For the plaintiffs it makes sense to keep pressing the constitutional issue because shining a light on the unconstitutionality of the law illuminates the injury the unconstitutionality has already caused and will continue to cause. But the defense has a different and much simpler job. All the DOJ [Department of Justice] has to do to defend FOSTA is say is, “The district court was right. These people were not hurt by FOSTA and will not be hurt by FOSTA, so keep this case dismissed.” If the appeals court agrees that there has been no injury, and that there is unlikely to be any injury, then the case remains dismissed and this constitutional challenge goes away.

Thus, Justice Department’s defense has continued to be that the plaintiffs aren’t actually being harmed by FOSTA. And yet, Gellis writes,

that’s exactly what the amicus brief by the twenty-one state attorney generals does not do. Although it is intended to support the DOJ’s defense of the statute, rather than supporting the DOJ’s argument that the plaintiffs’ complaints are much ado about nothing, their brief instead reads as a bright flashing neon sign warning the court that there is plenty of reason for them to be worried. Because, in contrast to the DOJ’s arguments about what FOSTA does not do, this brief reads as a paean to everything FOSTA is going to let the states do, including to people just like the plaintiffs.

“Democracy Dollars.” Senator and 2020 presidential hopeful Kirsten Gillibrand (D–N.Y.) yesterday proposed a plan to give every American $600 to give to politicians. Calling them “Democracy Dollars,” Gillibrand is trying to sell this as a way to give big-money interests and Washington insiders less influence in politics.

Nicholas Clairmount at The Independent has a good piece on why this such a bad plan. A sample:

First, it would simply multiply the amount of money in politics by an order of magnitude, with effects that wouldn’t be good for the political system at large, but would be good for ad buyers and PR flacks and political operatives….

There are roughly 235 million eligible voters in the United States. Say roughly half of them bothered to use the $600 (about 60 per cent of Americans vote in presidential years and about 40 per cent in midterm years). That means, conservatively, politicians would be looking at a little more than $70bn a cycle. What Gillibrand would have accomplished, then, if her initiative to deal with money in politics were hugely successful, would be to multiply the $6.5bn cesspit of corruption and division that is the long race for the White House by more than ten. I somehow doubt Washington’s lobbyist and political operative class hates this idea.

FOLLOWUP

What I just saw from the Attorney General is unacceptable. Barr must resign now.

The fallout and fanfare continues from yesterday’s grilling of Attorney General Bob Barr by the Senate Judiciary Committee.Reason‘s Eric Boehm has torn apart Lindsey Graham’s shameful performance during it.

Republicans certainly didn’t have a monopoly on disgusting displays of self-aggrandizement and partisan hackery. Democrats have been using this as an opportunity to demand that Barr resign over the testimony he gave yesterday. Barr’s departure would make many of us libertarians happy, but the grounds offered here just doesn’t cut it, alas. Still, flimsy pretense hasn’t stopped senators who are also 2020 presidential candidates from milking the opportunity for all they can…

Attorney General Barr needs to resign. Today, he's proven once again that he's more interested in protecting the president than working for the American people. We can't trust him to tell the truth, and these embarrassing displays of propaganda have to stop.

AG Barr is a disgrace, and his alarming efforts to suppress the Mueller report show that he's not a credible head of federal law enforcement. He should resign—and based on the actual facts in the Mueller report, Congress should begin impeachment proceedings against the President.

Barr was supposed to testify before the House Judiciary Committee today, but he has decided against it “following a dispute between House Democrats and the nation’s top law enforcement officer over whether Barr would publicly face questions from committee staff attorneys,” reports CNN.

Celebs are jumping on the Equal Rights Amendment bandwagon:

If you are a man who believes women should be protected in the constitution from discrimination based on sex—retweet this tweet. #MenForTheERA#ERANow#ERAHearing

Would she work with Woody Allen again? She would. I’ve been out of the loop the past few days, in recovery from having two wisdom teeth removed, but in my limited purview the best (and most controversial) thing on the internet in that time has been Vulture‘s interview with actress Anjelica Huston. In a wide-ranging interview conducted by Andrew Goldman, Huston touches on everything from her famous father to why she doesn’t like edibles, how Bill Murray snubbed her on the Life Aquatic set, Oprah’s beef with her, and Jack Nicholson’s cocaine habits.

Of course, the part that’s been generating some of the most attention is Huston saying she would work with Woody Allen again.

You were in two Woody Allen films, Crimes and Misdemeanors, alongside Mia Farrow, and then Manhattan Murder Mystery. Woody Allen is basically unable to make films now because of the outcry about the molestation allegations.

I think that’s after two states investigated him, and neither of them prosecuted him.

Well, the industry seems to be treating him as though he’s guilty. Would you work with him again? Yeah, in a second.

Huston touches on Roman Polanski, too, in what critics have been describing as a “defense” of the disgraced director. But the answer given by Huston—whose “first serious boyfriend” was 42 when she was 18, and who earlier in the interview mentions wishing she could’ve been in Romeo & Juliet as a teen so she could’ve been “off in Italy having a romance on set with Franco Zeffirelli”—is more an offering of context than absolution:

You were arrested because you happened to be in Jack’s house when Roman Polanski raped 13-year-old Samantha Geimer. How did you feel about that? Well, see, it’s a story that could’ve happened ten years before in England or France or Italy or Spain or Portugal, and no one would’ve heard anything about it. And that’s how these guys enjoy their time. It was a whole playboy movement in France when I was a young girl, 15, 16 years old, doing my first collections. You would go to Régine or Castel in Paris, and the older guys would all hit on you. Any club you cared to mention in Europe. It was de rigueur for most of those guys like Roman who had grown up with the European sensibility.

Huston situates Polanski’s attitudes and acts as products of their time period but also not all that different than the attitudes many men in Hollywood have toward women today. Far from downplaying the depravity, she refuses to simply position Polanski and/or that era as an anomaly which we can condemn from a safe and smug distance while congratulating everyone on how far they’ve come:

Among a lot of Hollywood men, it was acceptable at that time to treat women as though they were disposable.

I think they’re still doing it. I was at the hairdresser’s yesterday, and I heard tales of such horror from women. There was one other client and two girls who were working in this rather small hairdressing shop. And one of the girls had been passed a Mickey Finn in a bar and had woken up on a couch with a guy ejaculating wildly all over her face. And as she was telling the story, another girl who worked in the salon came in and said, “The weirdest thing happened to my friend last night. She was found at four in the morning in the Wilshire district, coatless, shoeless, with scratches and bruises all over her body. She doesn’t know whether she was raped. So, I’m trying to stop her from having a bath because we need to get her to the police.”

Later, Goldman asks Huston if she had any “#MeToo experiences”:

Yeah, yeah.

What happened? You’d have to ask me that on a daily basis, practically. That’s how often it happens, that you’re objectified, or misread, or put down. I think men do it a lot, and I don’t really think half the time they know what they’re doing. That’s how inured they are.

Huston goes on to describe Supreme Court Justice Brett Kavanaugh as “all that believable.”

Throughout the interview, her answers are candid and colorful while failing to fall into neat liberal/conservative (or woke/canceled) lines. Ignore the Twitter haters, and read the whole thing for yourself here.

FREE MINDS

FOSTA lawsuit update. The group challenging FOSTA, last year’s law banning prostitution ads, just got a boost from an unlikely source: 21 state attorneys general. Cathy Gellis at Techdirtexplains:

The important thing to remember about this appeal is that the question before the appeals court isn’t really about the constitutionality of FOSTA itself. What’s being appealed is the case having been dismissed for lack of standing by the plaintiffs. The district court never directly ruled on the constitutionality of the law; it only ruled that these plaintiffs had no right to complain about it to the courts. According to the district court these plaintiffs weren’t being hurt, or likely to be hurt, by FOSTA, and so it dismissed their case. What the parties are fighting about now is whether this assessment by the district court was right.

For the plaintiffs it makes sense to keep pressing the constitutional issue because shining a light on the unconstitutionality of the law illuminates the injury the unconstitutionality has already caused and will continue to cause. But the defense has a different and much simpler job. All the DOJ [Department of Justice] has to do to defend FOSTA is say is, “The district court was right. These people were not hurt by FOSTA and will not be hurt by FOSTA, so keep this case dismissed.” If the appeals court agrees that there has been no injury, and that there is unlikely to be any injury, then the case remains dismissed and this constitutional challenge goes away.

Thus, Justice Department’s defense has continued to be that the plaintiffs aren’t actually being harmed by FOSTA. And yet, Gellis writes,

that’s exactly what the amicus brief by the twenty-one state attorney generals does not do. Although it is intended to support the DOJ’s defense of the statute, rather than supporting the DOJ’s argument that the plaintiffs’ complaints are much ado about nothing, their brief instead reads as a bright flashing neon sign warning the court that there is plenty of reason for them to be worried. Because, in contrast to the DOJ’s arguments about what FOSTA does not do, this brief reads as a paean to everything FOSTA is going to let the states do, including to people just like the plaintiffs.

“Democracy Dollars.” Senator and 2020 presidential hopeful Kirsten Gillibrand (D–N.Y.) yesterday proposed a plan to give every American $600 to give to politicians. Calling them “Democracy Dollars,” Gillibrand is trying to sell this as a way to give big-money interests and Washington insiders less influence in politics.

Nicholas Clairmount at The Independent has a good piece on why this such a bad plan. A sample:

First, it would simply multiply the amount of money in politics by an order of magnitude, with effects that wouldn’t be good for the political system at large, but would be good for ad buyers and PR flacks and political operatives….

There are roughly 235 million eligible voters in the United States. Say roughly half of them bothered to use the $600 (about 60 per cent of Americans vote in presidential years and about 40 per cent in midterm years). That means, conservatively, politicians would be looking at a little more than $70bn a cycle. What Gillibrand would have accomplished, then, if her initiative to deal with money in politics were hugely successful, would be to multiply the $6.5bn cesspit of corruption and division that is the long race for the White House by more than ten. I somehow doubt Washington’s lobbyist and political operative class hates this idea.

FOLLOWUP

What I just saw from the Attorney General is unacceptable. Barr must resign now.

The fallout and fanfare continues from yesterday’s grilling of Attorney General Bob Barr by the Senate Judiciary Committee.Reason‘s Eric Boehm has torn apart Lindsey Graham’s shameful performance during it.

Republicans certainly didn’t have a monopoly on disgusting displays of self-aggrandizement and partisan hackery. Democrats have been using this as an opportunity to demand that Barr resign over the testimony he gave yesterday. Barr’s departure would make many of us libertarians happy, but the grounds offered here just doesn’t cut it, alas. Still, flimsy pretense hasn’t stopped senators who are also 2020 presidential candidates from milking the opportunity for all they can…

Attorney General Barr needs to resign. Today, he's proven once again that he's more interested in protecting the president than working for the American people. We can't trust him to tell the truth, and these embarrassing displays of propaganda have to stop.

AG Barr is a disgrace, and his alarming efforts to suppress the Mueller report show that he's not a credible head of federal law enforcement. He should resign—and based on the actual facts in the Mueller report, Congress should begin impeachment proceedings against the President.

Barr was supposed to testify before the House Judiciary Committee today, but he has decided against it “following a dispute between House Democrats and the nation’s top law enforcement officer over whether Barr would publicly face questions from committee staff attorneys,” reports CNN.

Celebs are jumping on the Equal Rights Amendment bandwagon:

If you are a man who believes women should be protected in the constitution from discrimination based on sex—retweet this tweet. #MenForTheERA#ERANow#ERAHearing

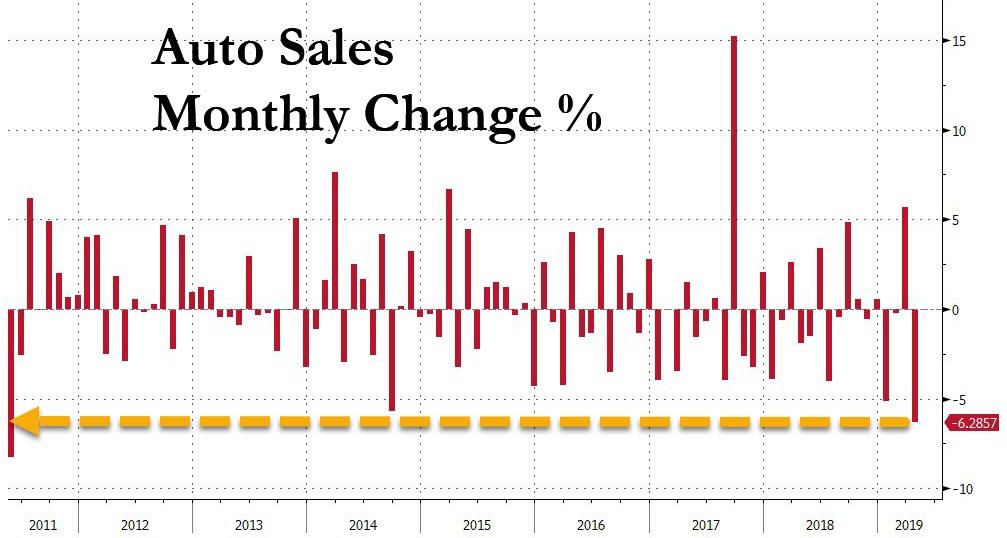

It was yet another dismal month for US auto sales in April, continuing a recessionary trend that has been in place not only in the US, but globally, for the better part of the last 12 months and certainly since the beginning of 2019. The nonsense-excuse-du jour for this month’s disappointing numbers is being placed on the weatheron seasonality on rising car prices, which easily pushed away an overextended, broke and debt-laden U.S. consumer.

In a nutshell, US auto sales in April tumbled by 6.1% – the biggest monthly drop since May 2011 – to just 16.4 million units, the lowest since October 2014. Aside for an incentive-boost driven rebound in March, every month of 2019 has seen a decline in the number of annualized auto sales. Furthermore, as David Rosenberg notes, the -4.3% Y/Y trend is the weakest it has been for the past 8 years.

Adding “fuel to the fire”, the average price of a new car in April came in at $36,720, the highest ASP so far this year, according to The Detroit News. It comes at a time where interest rates remain above 6% on average, further pressuring sales.

Edmunds analyst Jessica Caldwell said: “April sales were a bit dampened by the harsh financing conditions we’ve been seeing in the new-car market. Shoppers are really starting to feel the pinch as prices continue to creep up and interest rates loom at post-recession highs.”

Brian Irwin, Accenture Plc’s managing director for North American automotive, said simply: “We are disappointed with how sales turned out.”

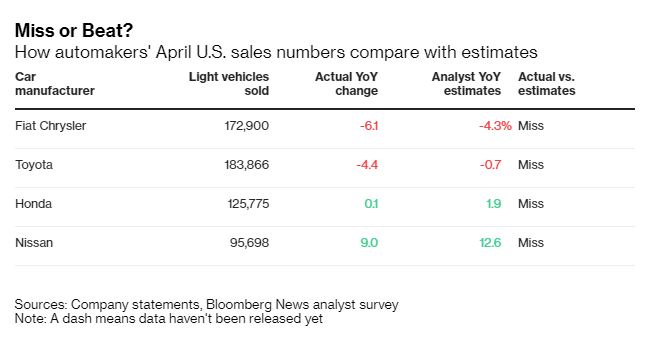

Across the board, almost all major names missed estimates, especially as passenger vehicle sales continued to collapse. Nissan was the one manufacturer that was able to buck the trend for the month. Some additional details, according to Bloomberg:

Ford’s U.S. sales fell 4.7 percent, according to Automotive News. That was steeper than the 4 percent drop predicted by analysts. The Ford brand fell 4.7 percent, while Lincoln dropped 6.2 percent, the publication reported.

Fiat Chrysler deliveries fell 6.1 percent, its third straight monthly U.S. sales decline. Chrysler sales fell 37% while Dodge slipped 24%. FCA’s Fiat brand saw a 34% dip in sales last month while Alfa Romeo was down 14%.

Honda eked out a gain of 0.1 percent, as the new Passport sport utility vehicle helps offset declines for cars including the Accord sedan. Honda’s passenger car sales fell 2.4%, driven down by an 11.5% drop in Accord deliveries.

Toyota sales fell 4.4 percent, while the Corolla sedan saw a 32.8% drop in deliveries and its Camry fell 2.1%.

Nissan, whose total sales rose 9 percent, credited cut-rate financing offers with helping boost its redesigned Altima sedan in April, and the automaker is expanding that program to its Rogue SUV this month.

Nissan’s success came from offering a better rate, proving that much of what is keeping the consumer away has been a financial burden. Billy Hayes, a division vice president for Nissan North America, said: “Offering a special rate has done well for us.”

On top those poor results, another one of Detroit’s “Big Three” has said that it will no longer be reporting sales on a monthly basis. FCA said Wednesday it will switch to quarterly sales reports, following the lead of both Ford and General Motors. It said it would begin quarterly reports on October 1 and will provide monthly reports up until that time.

FCA’s Chief Communications Officer Niel Golightly said: “A quarterly sales reporting cadence will continue to provide transparency of our sales results while at the same time aligning with where industry practice is heading.”

More transparency from less reporting – got it. We’re sure it has nothing to do with the fact that FCA’s year-to-date sales are down 4%.

FCA’s U.S Head of Sales Reid Bigland, who has been making excuses for the automaker’s sluggish sales all year, said: “April marks the start of the spring selling season and we anticipate strong consumer spending as we move through May. The industry may be shaking off the first-quarter sluggishness, but shoppers are coming into showrooms and buying.”

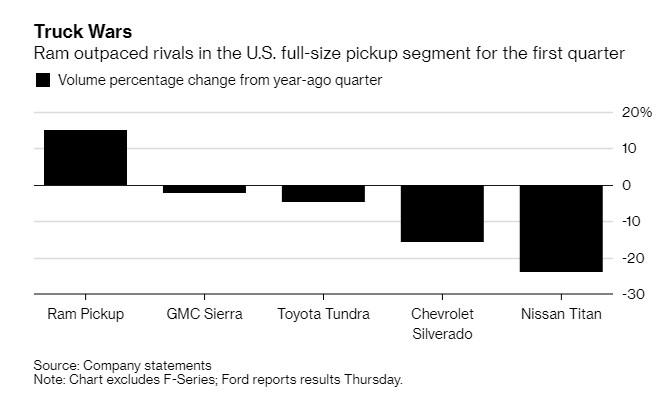

FCA’s Ram truck brand was one of the only six brands to post an increase in sales last month, up 25%. The Ram pickup posted a 25% gain with 49,106 units sold and is up 22% for the year. Jeep sales were lower by 8% in April, catalyzed by a 25% drop in Wrangler sales and a 13% drop in Cherokee sales. Ram had also bucked the trend last month:

And it’s no coincidence that the biggest failsafe for auto sellers – fleet sales – which can sometimes allow sellers to stuff the channel to meet numbers, have finally cooled.

Zo Rahim, an analyst for Cox Automotive said: “Fleet sales in April appear to have cooled from their impressive run in the first quarter. With overall sales down and fleet moderating, softness in vehicle sales still stems from weakness in the retail market. Affordability concerns coupled with attractive supply in the used-vehicle market might suggest retail sales might not bottom out for the foreseeable future.”

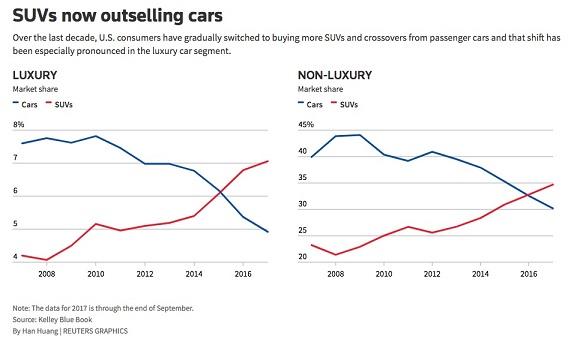

In February, auto sales plunged to 18 month lows as SUV demand hit a brick wall. SUVs were, until this February, one of the sole remaining bright spots in the rapidly slowing U.S. auto market. Despite the fact that they were crippling traditional sedan sales, Americans’ transition to SUVs was seen as a silver lining, prompting many automakers to make infrastructure changes to account for the change in demand. That silver lining looks to have all but completely disappeared at this point.

In January, auto companies set the tone for the year, starting 2019 just as miserably as 2018 ended, with major double digit plunges in sales from manufacturers like Nissan and Daimler.

via ZeroHedge News http://bit.ly/2DLi0J4 Tyler Durden

The further we get from her historic electoral defeat at the hands of President Trump, the more unhinged Hillary Clinton becomes.

Case it point: it appears the former secretary of state has moved on from endlessly blaming everybody but herself and her campaign staff for the many miscalculations made along the way (many have joked that Clinton probably couldn’t point out Wisconsin on a map), to actively soliciting enemies of the US to interfere on behalf of the Democrats in 2020.

Of course, there’s still plenty of evidence that Russia did exactly that back in 2016 (this thread was explored in more detail during AG Barr’s Wednesday hearing before the Senate Judiciary Committee).

But that didn’t stop Clinton from publicly asking China to step in and give the Democrats a boost against Trump during the 2020 race during an appearance on – where else? – the Rachel Maddow Show. Specifically, she asked the Chinese to steal Trump’s tax returns, which the Democrats have been having more trouble obtaining than they had probably expected.

“Imagine, Rachel, that you had one of the Democratic nominees for 2020 on your show, and that person said, you know, the only other adversary of ours who is anywhere near as good as the Russians is China,” Clinton told Maddow. “So why should Russia have all the fun? And since Russia is clearly backing Republicans, why don’t we ask China to back us?”

“And not only that, China, if you’re listening, why don’t you get Trump’s tax returns?” I’m sure our media would richly reward you.”

Clinton, clearly sore about Mueller’s findings, said China’s interference (which, according to the Trump administration, is already happening) could be part of a ‘great power contest’.

“Let’s have a great power contest, and let’s get the Chinese in on the side of somebody else,” she added. “Just saying, that shows how absurd the situation we find ourselves in.”

She added that the No. 1 thing she learned from reading the Mueller report was that the Russians interfered in the 2016 race to boost Trump, and that they haven’t been held accountable (that is, except for all the sanctions, and the indictments and the…well, you know).

Asked for her thoughts on the Barr hearing, Clinton said she thought Democrats on the Senate Judiciary Committee did a “good job” exposing Barr as “the president’s defense lawyer” (note: WSJ’s editorial board has offered plenty of evidence to the contrary).

“I think that the Democrats on the committee did a good job today in exposing that he is the president’s defense lawyer,” Clinton said. “He is not the attorney general of the United States in the way that he has conducted himself.”

Of course, Clinton’s comments were intentionally meant to mimic Trump’s now-famous campaign-era ‘joke’ that Russia steal Clinton’s missing emails and hand them over to the Republicans.

We now wait for Clinton to clarify that she, too, was ‘just kidding.’

via ZeroHedge News http://bit.ly/2Ja322P Tyler Durden

“If you can walk away, it’s a good landing. If you can use the airplane the next day, it’s an outstanding landing!”

What’s not to like about current markets?

A strong US economy – the strength of last week’s 3.2% growth rate data will likely be bolstered by a strong Jobs number tomorrow and ongoing solid economic releases through this month.

A US President determined to pump-prime an economic boom ahead of election year – who will do anything to avoid a downturn.

Theresa May finally doing something decisive and sacking a minster for indiscipline might suggest political firmness on the way, and maybe even a deal with Labour on Brexit?

A compliant(ish) Fed showing no sign of tightening policy. (Some analysts put it another way – the Fed rejecting Trump by not cutting rates…)

The same Fed perceiving no concerns on inflation, painting a picture of a US economy on a “healthy path”.

Signals Trump wants the China Trade deal signed asap – and even prepared to “compromise” on the key content – could provide another market booster.

US Oil production reaching record levels.

Apple surging 5% – despite falling sales – because it announced another stock buyback. (See link to a very interesting Bloomberg note on Apple’s failure to fill the looming iPhone “crater”.)

Maybe global trade is not a bad as we feared – has anyone noticed the Baltic Dry Index (an index showing global shipping costs) is up 54% in the last month?

Second quarter corporate results were expected to be poor – lower because of the global trade fracas and overstretched. Instead they’d generally been stronger than expected, hinting at a much firmer base.

Q2 Reporting across the Tech sector – the sector many think most vulnerable to a correction – has been solid. Aside from Alphabet’s lacklustre numbers, most Tech did well. Facebook was supposed to be the one that would cost us all dear because of on-going privacy issues and regulation. Nope. FB has seen a massive gain!

All in all, its not a bad picture. Economic growth, low rates, strong corporate performance, global trade not dead, and smiles all round. Or is it a bit complacent? I reckon the rosy picture I’ve painted above is somewhat distorted – it’s a dangerous reflection of deeper underlying issues with markets.

I am concerned about the bond market. Why? Because in the bond market lies the truth.

It’s very difficult to invest sensibly in the bond market at present. Rates remain distortedly low. Much of Europe is back in negative yield territory. US rates have not normalised either. Its an investment truth you can’t survive on 2.5% 10-year Treasury Yields, and corporate bond yields at spreads so tight they don’t properly reflect risk. Treasuries are supposed to be the zero-risk rate – but when the discount rate they provide is simply wrong, then it effects every other investment – distorting the risk/return equation.

Fixed Income Investors are left with the option of idiosyncratic plays – looking for value in thin illiquid markets. Over the past few days I’ve been speaking to clients about a whole raft of bond ideas to generate above market returns, but it’s difficult to focus on making 6% by taking extremely clever and complex synthetic European Sov risk when the stock market is touching new highs each and every day.

There are smart bond market plays out there – but overall markets seem focused on yield tourism again. When bond rates are too low to care about, money is looking for unconstrained returns that can’t be found in the dull boring predictable bond markets. When bond yields are so artificially low and stock prices look to have another leg up, then it difficult to ignore them!

Remember Blain’s Market Mantra no 1: “The Markets only objective is to inflict the maximum amount of pain on the maximum amount of participants.” Feels to me its setting itself up to catch as many bond market refugees as possible, and fleece them in stocks…

Call me Cassandra, but I don’t think this ends well..

One interesting snippet to note.. I note Warren Buffet has made a big bet on Dubai property (which is down 25% in last few years..) What does he know that we don’t? We’ve been talking about the likelihood of increased volatility and potential instability in the region, rather than it finding a firm base.. Hmmm. Must consider foundations in sand.

via ZeroHedge News http://bit.ly/2GXbqzY Tyler Durden

Good news America – productivity is surging at its fastest rate in nine years

Bad news America – it’s on the back of lower labor costs

Theoretically, they are close to the mirror of one another in a stable world (a rise in one necessarily means the inverse in another) and US productivity in Q1 soared 3.6% QoQ – the biggest QoQ rise since Q3 2014

Driven by the fact that Unit labor costs fell 0.9% in 1Q vs. up 2.5% prior quarter (Output rose 4.1% in 1Q vs. up 2.6% prior quarter, Employee hours rose 0.5% in 1Q vs. up 1.3% prior quarter, and nominal compensation rose 2.6 percent, the least in three quarters).

On a year-over-year basis, productivity rose 2.4% – the largest rise since Q3 2010…

…While labor costs advanced 0.1%, the least since 2013.

Blooomberg notes that it will still probably take more time to determine whether productivity is enjoying persistent increases after relatively slow gains throughout the current expansion, with an average of 1.3 percent from 2007 to 2018. Fed Chairman Jerome Powell on Wednesday brushed aside pressure for an interest-rate cut and said productivity is partly driven by technology developments and very hard to predict.

Today’s report showed output rose at a 4.1 percent pace, while hours worked increased 0.5 percent; that gain was last slower in 2015.

via ZeroHedge News http://bit.ly/2VaOUxt Tyler Durden

Joe Biden became the latest presidential contender to demand that AG Barr resign following a 5-hour-plus hearing on Wednesday where Democratic members of the Senate Judiciary Committee howled, mostly without evidence, that Barr was improperly trying to cover for President Trump, that he had deliberately watered down Mueller’s findings and that he was, in effect, acting as a mole within the DOJ feeding information on the 14 ongoing investigations to the White House.

Given his treatment at the hands of the Senate, it’s hardly a surprise that Barr declined to appear before the House Judiciary Committee on Thursday, which is stocked with even more bloodthirsty Democrats who will all need to defend their seats in 18 months time. And while Democrats will inevitably portray this as Barr shirking responsibility, as WSJ points out in an editorial published in Thursday’s paper, Barr’s treatment at the hands of the Judiciary’s Democrats was nothing short of reprehensible – and the coordinated ‘leak’ of the Mueller letter on the eve of the hearing was a blatant attempt to discredit an Attorney General who had done nothing wrong.

As WSJ explains, Mueller’s complaint that Barr’s summary of the 448-page report’s findings “lacked context” was likely an exercise in ass-covering. How could Barr be expected to distill the full sweep and scope of such a lengthy report’s findings in just four pages. In the same letter, Mueller affirmed that Barr’s summary was accurate – and, more tellingly, that he had been moved to write the letter following “public confusion” about his findings (i.e. Republicans’ trumpeting of ‘no collusion, no obstruction’, which probably angered Mueller’s many fanboys and fangirls in the #resistance).

As Lindsey Graham interjected following Marie Hirono’s bombastic questioning, where she effectively labeled Barr a liar and a traitor, the AG has been subjected to vicious slander at the hands of the Democrats simply for doing his job honestly and properly.

And the calls for his resignation are merely the cherry on top.

If Barr’s actions should be contrasted with anyone’s, the most fitting example would be former AG Loretta Lynch. Lynch “cowered” before James Comey and bowed to partisan interests by refusing to make a prosecutorial judgment after the Clinton investigation.

Did the Democrats demand that she resign?

Read the full editorial below:

Washington pile-ons are never pretty, but this week’s political setup of Attorney General William Barr is disreputable even by Beltway standards. Democrats and the media are turning the AG into a villain for doing his duty and making the hard decisions that special counsel Robert Mueller abdicated.

Mr. Barr’s Wednesday testimony to the Senate Judiciary Committee was preceded late Tuesday by the leak of a letter Mr. Mueller had sent the AG on March 27. Mr. Mueller griped in the letter that Mr. Barr’s four-page explanation to Congress of the principal conclusions of the Mueller report on March 24 “did not fully capture the context, nature, and substance” of the Mueller team’s “work and conclusions.” Only in Washington could this exercise in posterior covering be puffed into a mini-outrage.

Democrats leapt on the letter as proof that Mr. Barr was somehow covering for Donald Trump when he has covered up nothing. Hawaii Sen. Mazie Hirono, the Democratic answer to Rep. Louie Gohmert, accused Mr. Barr of abusing his office and lying to Congress, and demanded that he resign. The only thing she lacked was evidence.

Mr. Barr’s four-page letter couldn’t possibly have covered all the nuances of a 448-page report. It was an attempt to provide Mr. Mueller’s conclusions to Congress and the public as quickly as possible, while he took the time to work through the entire document to make redactions required by law and Justice Department rules.

This is exactly what he promised to do in his confirmation hearing.Even Mr. Mueller’s complaining letter admits that Mr. Barr’s letter wasn’t inaccurate, a fact Mr. Barr says Mr. Mueller also conceded in a subsequent phone call. The Mueller complaint, rather, was that there was “public confusion about critical aspects” of his investigation. Translation: Republicans were claiming vindication for Donald Trump, and Mr. Mueller was taking hits in the press for not nailing the worst President in history. Having been hailed for months as a combination of Eliot Ness and St. Thomas More, Mr. Mueller and his team of prosecutors seem to have been unnerved by some bad press clips.

Mr. Barr told the Senate Wednesday that he offered Mr. Mueller the chance to review his four-page letter before sending it to Congress, but the special counsel declined. Mr. Mueller worked for Mr. Barr, and that was the proper time to offer suggestions or disagree. Instead, Mr. Mueller ducked that responsibility and then griped in an ex-post-facto letter that was conveniently leaked on the eve of Mr. Barr’s testimony. Quite the stand-up guy.

Mr. Barr has since released the full Mueller report with minor redactions, as he promised, and with the “context” intact. Keep in mind Mr. Barr was under no legal obligation to release anything at all. Mr. Mueller reports only to Mr. Barr, not to the country or Congress.

Mr. Barr has also made nearly all of the redactions in the report available to senior Members of Congress to inspect at Justice. Yet as of this writing, only three Members have bothered—Senate Judiciary Chairman Lindsey Graham, Senate Majority Leader Mitch McConnell and ranking House Republican on Judiciary Doug Collins. Not one Democrat howling about Mr. Barr’s lack of transparency has examined the outrages they claim are hidden.

Democrats are also upset that Mr. Barr concluded that Mr. Trump did not obstruct justice regarding the Russia probe. But in that decision too Mr. Barr was behaving as an Attorney General should. Mr. Mueller compiled a factual record but shrank from a “prosecutorial judgment.” Mr. Barr then stepped up and made the call, however unpopular with Democrats and the press.

* * *

Contrast that to the abdication of Loretta Lynch, who failed as Barack Obama’s last Attorney General to make a prosecutorial judgment about Hillary Clinton’s misuse of classified information. Ms. Lynch cowered before the bullying of then FBI director James Comey, who absolved Mrs. Clinton of wrongdoing while publicly scolding her. That egregious break with Justice policy eventually led Mr. Comey to re-open the Clinton probe in late October 2016, which helped to elect Mr. Trump.

All of this shows again the risks of appointing special counsels. They lack the political accountability that the Founders built into the separation of powers. Mr. Mueller, in his March 27 letter, revealed again that like Mr. Comey at the FBI he viewed himself as accountable only to himself.

This trashing of Bill Barr shows how frustrated and angry Democrats continue to be that the special counsel came up empty in his Russia collusion probe. He was supposed to be their fast-track to impeachment. Now they’re left trying to gin up an obstruction tale, but the probe wasn’t obstructed and there was no underlying crime. So they’re shouting and pounding the table against Bill Barr for acting like a real Attorney General.

via ZeroHedge News http://bit.ly/2JicNML Tyler Durden

During the first hearing in what’s expected to be a protracted legal battle over the US’s extradition request, Wikileaks’ founder Julian Assange told a British judge that he wished to fight extradition, and the hearing was concluded with the next court date set for May 30.

Assange, whom the US has charged with conspiring with Chelsea Manning to break into a government computer, a charge that carries a maximum prison term of 5.5 years, appeared on screen wearing a sports jacket. He wasn’t handcuffed. And when asked if he would consent to surrender to the US, he replied that he did not wish to do so, according to CNN.

Assange, speaking from Belmarsh prison, was wearing a sports jacket and was not handcuffed.

Asked by Judge Michael Snow if he wished to consent to surrender himself for extradition, Assange said: “I do not wish to surrender myself for extradition for doing journalism that’s won many, many awards and affected many people.”

His appearance came a day after another judge slapped him with a 50-week sentence for skipping bail back in 2012.

As we previewed last night, Wikileaks editor-in-chief Kristinn Hrafnsson said Wednesday that the extradition process is where ‘the real battle begins’ for Assange.

Speaking to CNN after Assange’s bail violation sentencing on Wednesday, WikiLeaks’ Editor-in-Chief Kristinn Hrafnsson said he was “shocked and appalled by this decision to sentence Julian to two weeks short of the maximum sentence for not showing up in court.”

He added that the US extradition claim is “where the real battle begins.”

Assange’s legal team has yet to publicize its defense strategy, but most expect them to argue that the request is politically motivated. Meanwhile, Hrafnsson declared that it’s Wikileaks’ view that the charges cited by the US in the extradition request are merely a ruse, and that Assange will be charged with violating the 1970 Espionage Act once he’s safely on American soil – a charge that could carry the death penalt.

“Everything in this case seems to indicate that what is being established is a violation of the espionage act of 1970 which carries the death penalty,” Hrafnsson explained. “Although the extradition is based on a lower level of offenses, we think that is basically a snaring strategy to get him to United States where additional charges will be added.”

As CNN explained, to extradite Assange, a court must agree that his alleged violations would also constitute criminal conduct in the UK. Afterward, the UK’s home secretary would still have final say on whether Assange is handed over.

Extradition requests to the UK from outside the European Union are governed by Part 2 of the Extradition Act 2003. When reviewing the US extradition claim, it will not be for the UK courts to determine culpability. A judge only determines whether the US request satisfies the “dual criminality” legal requirement – meaning that the alleged crime is illegal in both countries. The judge would also consider if granting extradition would breach his human rights.

If satisfied that the claim meets procedural conditions, the case would be sent to the British home secretary for a final decision on ordering the extradition.

Protesters gathered outside the courthouse before the hearing (during which Assange participated by video link; he was being held in a high-security prison).

Supporters of WikiLeaks founder Julian #Assange protesting outside Westminster Magistrates Court at US extradition hearing: “US, UK – Hands off Assange!” pic.twitter.com/x0Ros0OuCs

— Socialist Equality Party (Britain) (@SEP_Britain) May 2, 2019

And crowds waited to hear from Assange’s lawyers after the hearing had concluded. Some even blocked a nearby road in a gesture of protest.

Outside the court waiting for Assange legal team to speak. Extradition matter back in court again May 30. pic.twitter.com/9oypAJs3MY

Tesla’s need for cash has finally slipped beyond the point where CEO Elon Musk can continue to pretend to ignore it, and instead has been given a violent thrust into urgent, as the company filed this morning to offer about 2.7 million shares (~$650 million in stock) and $1.35 billion in convertible notes one week after Musk said there was merit to the cash-crunched company raising more capital. Shares popped on the news in the pre-market session on news Musk would participate in the offering:

The entire financing seeks to raise about $2. The converts will add another maturity to the company’s nearly $11 billion in debt it already carries and, by our back of the envelope calculations, the equity issuance will dilute current shareholders by approximately 1.25%. The senior convertible notes will be due in 2024.

To put a lipstick on the dilution pig, CEO Elon Musk has indicated his “interest” in purchasing up to about 42,000 shares, or a paltry $10 million of the offering. This equates to about 0.045% of Musk’s reported $22 billion net worth. According to FinTwit regular @bgrahamdisciple, Elon Musk is the only executive officer or director who has purchased shares in the last 12 months. Other executive officers and directors have executed 41 sales in the past 12 months.

Goldman Sachs, Citigroup, BofA, Deutsche Bank, Morgan Stanley, Credit Suisse, Soc Gen and Wells Fargo will be handling the offering. As Mark Spiegel points out, the lead underwriter on the stock has a “sell” rating on the name and a $200 price target.

With key Asian markets (China and Japan) closed for the second day in a row, Europe’s share markets struggled early on even as US equity futures levitated form session lows…

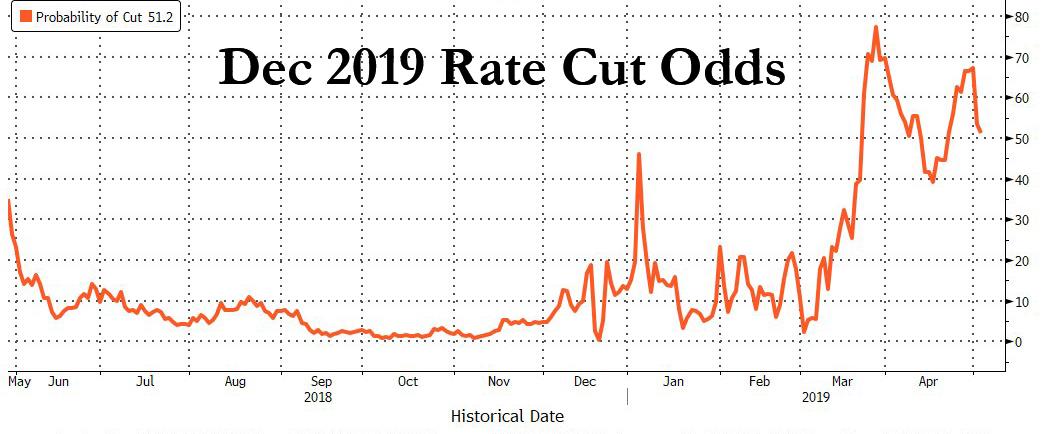

… after the Fed crushed hopes that it is preparing its first interest rate cut in years, as Powell said inflationary pressures were “transitory”, sending 2019 rate cut odds sliding.

As a result, stocks were mixed on Thursday as, in Bloomberg’s words “investors switched their focus from monetary policy back to company earnings and the outlook for global trade”. The dollar was little changed, while treasury yields continued their ascent.

Starting off the overnight session, Asian trading was thinned by holidays in Japan and China but Hong Kong and Korea’s stocks gained after CNBC reported the U.S. and China could announce a long-awaited trade deal by May 10, as Chinese Vice Premier Liu He heads to Washington. Though now expected by markets if confirmed, it would remove significant uncertainty that has weighed on markets and global data for a year now.

“I would still expect some relief rally once the deal gets done. The question is how big that move might be,” State Street GM’s Metcalfe added.

Following the subdued Asian action, Europe’s basic resource stocks led the downward shift in equities with a 1.4 percent drop to their lowest since late March. Continental Europe was also trying to get back up to speed having been shut for holidays on Wednesday. Oil and metals markets added to the pressure on stocks on Thursday with traders sending copper to a 2-month low while news of record US production sent the price of oil sliding after a 33% rise this year.

Elsewhere Turkey’s lira remained under pressure near the 6 per dollar mark after data there had showed manufacturing activity contracting for the 13th month in a row. Euro zone factory activity also contracted for a third straight month. “Demand shortages were again evident in the Turkish manufacturing sector in April, while currency weakness led to inflationary pressures building again,” said Andrew Harker, associate director of IHS Markit.

But the biggest driver of risk on Thursday was the reaction to the Fed, where for all the intense political pressure to ease policy and the mixed growth/inflation data, the central bank held the line on Wednesday and refused to signal anything other than it was still on pause as Reuters put it.

Although the Fed made the predicted 5 basis point cut to the interest it pays on banks’ excess reserves – a technical move to ease money market tightness as it runs down its balance sheet – chair Powell was unwavering on the rate outlook and said the recent relapse in inflation rates was likely temporary.

“The market has gotten perhaps ahead of itself in quite confidently pricing in (U.S) interest rate cuts,” said Michael Metcalfe, head of global macro strategy at State Street Global Markets. “Powell was quite dismissive of the latest downturn in inflation… which I think has caused the market to reassess that a little bit.”

Emerging markets steadied from Wednesday’s knee-jerk sell-off as the US spike slowed down, and investors weighed the Fed’s comments for clues on the global-growth outlook. The EM benchmark index rose for a second day, while an index developing-nation currencies was little changed, as the focus turned to the next big catalyst for risk sentiment – the U.S. jobs report due Friday.

In rates, most government bonds in Europe initially tracked the slide in Treasuries, though they reversed declines to edge higher after data showed the euro area’s manufacturing slump extended into a third month. Dollar bonds of shorter tenors from Ukraine to Turkey advanced, with money managers saying the asset class has received a new lease of life from the Fed’s pause on rate moves.

The Bloomberg Dollar Index was little changed after rising 0.1 percent on Wednesday; the dollar index drifted around 97.600 against its set of major currency peers after going as high as 97.728 and hovering around $1.1211 to the euro and $1.305 to Britain’s pound after the Bank of England kept its rates on hold. An increase in Treasury yields helped to narrow the premium on emerging-market sovereign bonds. Manufacturing data from Asia suggested the worst may be over for the region. “Emerging-market credit is holding up reasonably well,” BlueBay strategist Tim Ash told Bloomberg. “It is emerging as the asset of choice in the EM space as people feel nervous about investing in local currencies and local markets given enduring dollar strength and the U.S.-EM growth differential.”

In commodities, the drop in oil prices came after US crude production output set a new record, though the losses were capped by the intensifying crisis in Venezuela and the stopping of Iranian oil sanction waivers by Washington. US crude was last off 27 cents at $63.32 a barrel while Brent slipped 33 cents to $71.86. Copper was at a two month low after a heavy tumble on Wednesday, while spot gold was marginally weaker at $1,271.55 an ounce.

Looking at today’s calendar, durable goods orders, factory orders and initial jobless claims are due. Scheduled earnings include DowDuPont, Gilead Sciences and Cigna.

Market Snapshot

S&P 500 futures up 0.2% to 2,927.25

STOXX Europe 600 down 0.3% to 389.82

MXAP down 0.02% to 162.64

MXAPJ up 0.1% to 540.16

Nikkei down 0.2% to 22,258.73

Topix down 0.2% to 1,617.93

Hang Seng Index up 0.8% to 29,944.18

Shanghai Composite up 0.5% to 3,078.34

Sensex up 0.2% to 39,093.26

Australia S&P/ASX 200 down 0.6% to 6,338.41

Kospi up 0.4% to 2,212.75

German 10Y yield rose 1.9 bps to 0.032%

Euro up 0.2% to $1.1215

Brent Futures down 0.8% to $71.59/bbl

Italian 10Y yield fell 2.9 bps to 2.184%

Spanish 10Y yield rose 0.8 bps to 1.009%

Brent Futures down 0.8% to $71.59/bbl

Gold spot down 0.5% to $1,270.65

U.S. Dollar Index down 0.1% to 97.55

Top Overnight Headlines from Bloomberg

It’s possible for U.S. and China to announce a trade deal by May 10 as Chinese Vice Premier Liu heads to Washington for further talks next week, CNBC reported, citing people familiar with matter

Theresa May and her arch political rival Jeremy Corbyn are both signaling they may be edging closer to a Brexit deal after a month of talks between their teams that seemed to be going nowhere

U.K. Prime Minister May fired her defense secretary for revealing secret discussions about Huawei Technologies’s role in Britain, as she attempted to assert control over a government that has become dominated by the battle to succeed her

BOC Governor Stephen Poloz said he still believes policy interest rates would likely need to rise if the slew of factors slowing the expansion vanish

European Union warned about greater transatlantic political tensions after President Trump decided to let U.S. citizens file lawsuits over property confiscated in Cuba during the 1959 revolution

Federal Reserve Chairman Jerome Powell pushed back against pressure for interest-rate cuts from traders and President Donald Trump, saying inflation will rebound and the economy will stay healthy without fresh help from the central bank

The Federal Reserve’s message of patience this week further relieves pressure on “resilient” economies across Asia, said a regional body

The euro area’s manufacturing slump showed tentative improvement in April as Italy’s contraction slowed markedly and French industry stopped shrinking

Asian equity markets were mixed as the region partially shrugged off the negative lead from US where all major indices were pressured, and the S&P 500 snapped a 3-day streak of record closes after Fed Chair Powell downplayed prospects for looser policy at the post-FOMC presser. ASX 200 (-0.6%) traded negative with the index led lower by financials after AMP Capital reported net cash outflows widened in Q1 and with ‘Big 4’ bank NAB also weighed after it lowered its interim dividend by 16%. Elsewhere, both KOSPI (+0.4%) and Hang Seng (+0.8%) recovered from early losses on return from Labour Day holidays amid US-China trade optimism as reports suggested a trade deal could be possible by the end of next week, while China also recently announced several measures to open up its financial sector to foreign companies in a concession to the US. As a reminder, Japan and mainland China remained closed for holidays.

Top Asian News

Huawei is Said to Hold Fixed-Income Investor Meetings in Asia

Naval Ships Deployed as India Braces for Worst Storm Since 2014

AIA Hits High After China Plan to Open Up Financial Industry

Major European indices have traded indecisively this morning [Euro Stoxx 50 -0.3%], as the region struggles to find direction post-FOMC where US indices were subdued but Asia did manage to somewhat shrug off the negativity. It is also worth bearing in mind that markets are playing catchup due to yesterday Labour Day holiday for much of Europe which may account for some of the volatility. Sectors are subdued this morning, although there was some mild outperformance in Healthcare and utility names at the open. This morning’s notable earnings release came from Shell (+2.3%) who beat on their Q1 adj. profit and have begun the next tranche of their share buyback programme, with the heavyweight lifting energy names higher in-spite of lower oil prices. Separately, Volkswagen (+4.5%) are towards the top of the Stoxx 600 after beating on Q1 revenue and confirming their FY outlook for car sales. Also of note are Bayer (+3.3%) whose share prices are supported this morning by the US Environmental Protections agency stating that glyphosate is not a carcinogen. Elsewhere Lloyds (-1.0%) are in the red post-earnings as the Co’s Q1 statutory pre-tax profit missed on Co. complied estimates, Lloyds have also made an additional PPI provision of GBP 100mln.

Top European News

Volkswagen Gains After Profit Rises, Confirms Annual Targets

Watches of Switzerland Considers IPO as Apollo Reduces Stake

Deutsche Bank Said to Have Virtually No New Plan for What’s Next

In FX, although the Greenback has a lost a degree of its post-Powell recovery momentum, the index remains above 97.500 and on a more stable footing as the Fed chair refrained from flagging any shift towards a rate cut or even a hint that soft inflation could tip the policy balance from neutral to dovish. In fact, after the 5 bp IOER reduction he stressed that the move was technical rather than fundamental and repeatedly downplayed slowing price developments as transitory. Hence, the DXY has rebounded from sub-97.200 lows and just above a Fib support level (97.121), albeit with the Buck now mixed vs G10 peers.

EUR – The single currency has drawn a bit more encouragement from the run of Eurozone manufacturing PMIs, as all bar Germany posted better than expected headlines, including Italy that rebounded relatively firmly following a return to GDP growth in Q1. Eur/Usd is back above 1.1200 as a result having probed a few pips below the 200 HMA at 1.1194, but the headline pair may be hampered by heavy option expiry interest stretching from 1.1200-10 through 1.1225-40 and up to 1.1250 (1.5 bn, 2 bn and 1.1 bn respectively). Moreover, chart resistance could cap the upside given the 30 DMA at 1.1236 and a Fib at 1.1242.

NZD/AUD – The Kiwi and Aussie are marginally outperforming vs major counterparts amidst reports that a US-China trade accord may be in the offing as soon as next week and at the end of the next talks to take place in Washington, with Beijing said to be offering concessions in return for a recent olive branch from the US. Nzd/Usd is hovering between 0.6620-39 and Aud/Usd within a 0.7012-29 range as the Aud/Nzd cross sits just under 1.0600 and attention down under turns towards next week’s RBNZ and RBA policy meetings (notwithstanding NFP tomorrow of course). Both rate calls are seen tight with swap pricing not far from evens for easing, but as NAB contends that it may be to early for the RBA options are indicating higher break-evens as a result (circa 80 pips).

GBP/CAD/CHF/JPY – All on a more even keel vs the Greenback, with Cable straddling 1.3050 and braced for BoE super Thursday after only deriving modest support from a return to growth in the UK construction sector. However, the Pound is consolidating gains relative to the Euro over 0.8600 amidst some talk that 1 MPC voter could break ranks and switch into hike mode – full preview on the headline feed and via the Research Suite. Conversely, the Loonie is struggling to hold above 1.3450 against the backdrop of ongoing weakness in oil prices, while the Franc is back down near 1.0200 and sub-1.1400 against the Euro in wake of weak Swiss retail sales and a contractionary manufacturing PMI. The Yen has also retreated from Wednesday’s pre-FOMC peaks through 111.50 and the 30 DMA (111.42) into decent option expiries (1.2 bn between 111.50-55).

NOK/SEK – Disappointing Scandi manufacturing PMIs vs consensus and previous readings have soured sentiment to a degree, but Eur/Nok has also been driven higher by the aforementioned crude retracement, to 9.7400+ at one stage vs Eur/Sek topping out just shy of 10.7050.

In commodities, Brent (-1.0%) and WTI (-0.9%) prices are lower, with oil prices subdued as this week’s large crude stockpile builds overshadows Iranian waiver woes and Venezuela concerns, although some of downside in the complex could be attributed to a firmer post-FOMC Dollar. In terms of recent newsflow Russia’s April oil production stood at 11.23mln BPD vs. 11.3mln in March, with these levels being relatively in-fitting with recent IFX reports. Additionally, the Russian Energy Ministry have stated that they are to keep May’s production in-line with the prior agreements; which was agreed at a reduction of 228k BPD (from the October baselines of 11.4mln BPD) in the OPEC pact. Gold (-0.5%) was also afflicted by the surge in the Dollar, with the yellow metal unable to recover from this downside, in spite of the Buck easing off highs, and is currently trading firmly at the bottom of its USD 7/oz range. While copper prices are still around 2-month lows as the red metal is missing the support of its largest buyer China which is on Labour Day holiday for the remainder of the week.

US Event Calendar

7:30am: Challenger Job Cuts YoY, prior 0.4%

8:30am: Initial Jobless Claims, est. 215,000, prior 230,000; Continuing Claims, est. 1.66m, prior 1.66m

8:30am: Nonfarm Productivity, est. 2.2%, prior 1.9%; Unit Labor Costs, est. 1.5%, prior 2.0%

9:45am: Bloomberg Consumer Comfort, prior 60.8

10am: Factory Orders, est. 1.5%, prior -0.5%; Factory Orders Ex Trans, prior 0.3%

10am: Cap Goods Orders Nondef Ex Air, prior 1.3%; Cap Goods Ship Nondef Ex Air, prior -0.2%

DB’s Jim Reid concludes the overnight wrap

Needless to say, the focus yesterday in markets was on the Fed meeting, and though the eventual outcome was broadly in line with expectations, we did finally see a return of some volatility after the statement’s release and subsequent press conference. The only change in policy was a 5bps cut to the IOER, though that was just a technical adjustment and not a monetary policy signal. The S&P 500 initially rallied on dovish expectations, but then retraced to end the day -0.75% lower for the biggest decline since March as Powell spoke hawkishly about the inflation and growth outlook at his press conference.

Indeed, markets made a bit of a u-turn between the statement and press conference. First, Treasury yields fell as much as -4.9bps to touch 2.453% and the S&P 500 advanced as much as +0.29% to a new intraday all-time high. The reason for the rally was the initially dovish Fed statement, which contained few changes but did change the assessment on inflation from “near 2%” to “have declined and are running below 2%.” That was interpreted as a signal that the committee is more concerned about weak inflation data, which could be a catalyst to justify a rate cut in the near or medium term. However, in his press conference, Powell emphasized that recent inflation weakness is expected to be “transient or idiosyncratic” and that he doesn’t see a strong case for a move in either direction.Even when prompted about how he would respond to a downside surprise, he explicitly stopped short of endorsing a rate cut. He also spoke positively about the growth outlook in China and Europe, and said that financial conditions are accommodative. All in all, he sounded more optimistic about the economy than expected. Our US economists last night reiterated their view that they expect the Fed to remain patient and keep rates steady for the foreseeable future. See their note here .

Powell’s comments caused markets to promptly reprice, with bond yields completely reversing their moves. 10y yields ended the session flat at 2.501%, though they had already fallen earlier in the session after the weak ISM report – more on that below – so they ended net higher after all the Fed drama was done. 2y yields rose +3.8bps and the 2s10s curve, which had steepened over one basis point after the Fed’s statement, retraced to end -4.0bps flatter at 19.3bps. Along with the S&P 500’s retreat, the NASDAQ and DOW ended -0.56% and -0.61%, with losses fairly widespread. In fact, 83% of S&P 500 companies ended lower, the highest ratio in over five weeks and third worst day of the year. The dollar rallied +0.21%, which was +0.53% off its intraday lows, with losses spread evenly between the euro (-0.17%) and a basket of EM currencies (-0.17%). WTI oil prices mirrored the dollar’s move, falling -0.49%, though the big driver was data that showed another large build in US inventories.

This morning Asia has followed in a slightly more mixed fashion, however the various holidays in Japan and China have sapped some liquidity out of the market. Of those open, the Hang Seng (+0.63%) and Kospi (+0.41%) are both up, however the ASX (-0.67%) has retreated. US futures are also slightly positive. The gains in Hong Kong and Korea seem to have got a boost from news out of CNBC that a US-China trade deal is “possible” by next Friday. Politico is also reporting that the two sides are close to an agreement and that the plan being put forward is for the US to remove a 10% tariff on a portion of the $200bn of Chinese imports hit by tariffs, before lifting the rest not long after. However, the article also suggests that a 25% tariff on $50bn of Chinese goods would stay in place longer and possibly until after the 2020 election.

That story comes as US-China trade talks wrapped up in Beijing yesterday. Treasury Secretary Mnuchin confirmed in a tweet that the meetings had been “productive” and that talks between both sides will continue in Washington DC next week. So, we’re nearing the business end of talks at last it seems.

The other highlight for markets yesterday was the US data and most notably that much softer than expected ISM manufacturing report. The 52.8 reading for April came in well below expectations for 55.0 and represented a drop of 2.5pts from March. It was also the lowest reading since October 2016 and it means that the current level is now 8pts below the August 2018 peak. The breakdown was also soft with the employment component dropping over 5pts to 52.4, new orders also down over 5pts to 51.7 and most notably the prices paid component falling over 4pts to 50.0. The associated statement highlighted Mexico/US border crossing delays on numerous occasions as slowing supplier deliveries.

Prior to this and in contrast to the ISM data, we got a much stronger than expected April ADP employment change print (275k vs. 180k expected) which also included upward revisions to the March data. In fact, it was the strongest monthly reading since July 2018 and continues the theme of the labour market still being incredibly strong. A reminder that we’ve got the April employment report tomorrow. The only other notable US data yesterday was the April vehicle sales figures, which fell to 16.4mn, the lowest level since August 2017. That’s still higher than every month from mid-2007 through early 2014, so not a cause for alarm yet.

In Europe, it was only the UK that was open of the main markets, with the FTSE 100 closing -0.44% and Gilt yields falling -3.4bps. Sterling also ended +0.14%, despite the dollar’s broad strength, after the April manufacturing PMI was confirmed at 53.1 – matching the consensus – and therefore down 2pts from March. In addition, mortgage approvals in March were confirmed as declining to 62.3k and the least since 2017. Consumer credit was also the weakest since 2013 at just £0.5bn and therefore continues a declining trend for consumer lending in the UK. All-in-all this just means more confusing data to untangle for the BoE – which as a reminder meet today at lunchtime.

Staying with the UK, the Brexit newsflow is starting to slowly creep back onto our screens. The last couple of days have seen both the Conservatives and Labour talk up recent progress and especially compromise on a customs union, with PM May seen to be pushing for a deal being reached next week and ahead of the EU elections in just three weeks now. It’s worth flagging that the UK local elections are today, where an expected bad result for May will only increase pressure to a reach a deal sooner rather than later.

In other news, the ECB’s Guindos said yesterday that the ECB is “open-minded” to discussions around changing the inflation target, but haven’t yet discussed anything. This is similar to recent comments fellow policy maker Rehn made. This morning we’ve got the final April manufacturing PMIs in Europe where the consensus is for no change in the 47.8 flash reading for the Euro Area. A reminder that this included sub-50 readings for Germany (44.5) and France (49.6) while Italy is forecast to print at 47.8 which is only a marginal improvement on the very soft March reading. Spain is forecast to improve to 51.2. Those readings will be drip fed from 8am BST.

To the day ahead now, where this morning the focus is on those aforementioned final April PMIs in Europe. The focus after that turns to the BoE meeting where no policy change announcement is expected, however our UK economists expect the tone to be marginally hawkish given stronger than expected growth a tight labour market coupled with weaker rate expectations. This afternoon in the US we’ve got another busy slate of data releases with claims, preliminary Q1 nonfarm productivity and unit labour costs, and final March durable, capital and factory orders data all due. We’ve also got comments due from the ECB’s Hansson this morning and then Praet this evening, while from today US waivers on purchases of Iranian oil officially expire. The earnings highlights today include Shell, Volkswagen, DowDupont, BNP and Lloyds.

via ZeroHedge News http://bit.ly/2IUlNrL Tyler Durden