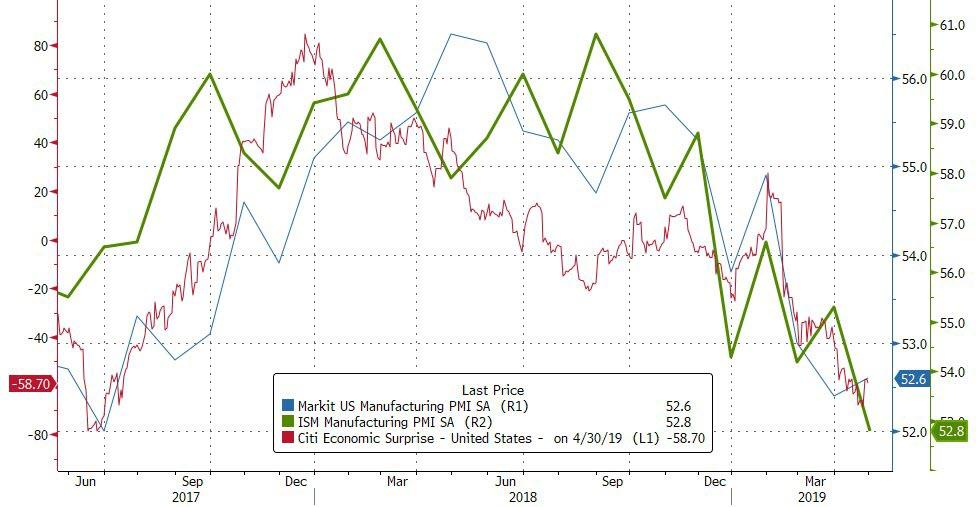

Following Canada’s Manufacturing PMI plunge into contraction in April, Markit reported US Manufacturing saw a very modest rebound in April (from 52.4 to 52.6) despite the slowest growth in employment in two years.

ISM was considerably worse, plunging to its weakest since October 2016

The gauge for export orders fell below 50 for the first time in three years while imports missed the threshold for the first time in two years, the latest evidence President Donald Trump’s trade wars are weighing on factories.

The measure for new orders also slipped to near the weakest since 2016, indicating softer demand. At the same time, the inventoriesgauge increased, suggesting stockpiles continue to expand, a trend that will likely eventually reverse and be a drag on growth.

ISM’s employment gauge fell to near a two-year low, signaling weakness ahead of Friday’s U.S. jobs report.

The index of prices paid dropped to 50, a signal that inflation pressures are likely to remain muted.

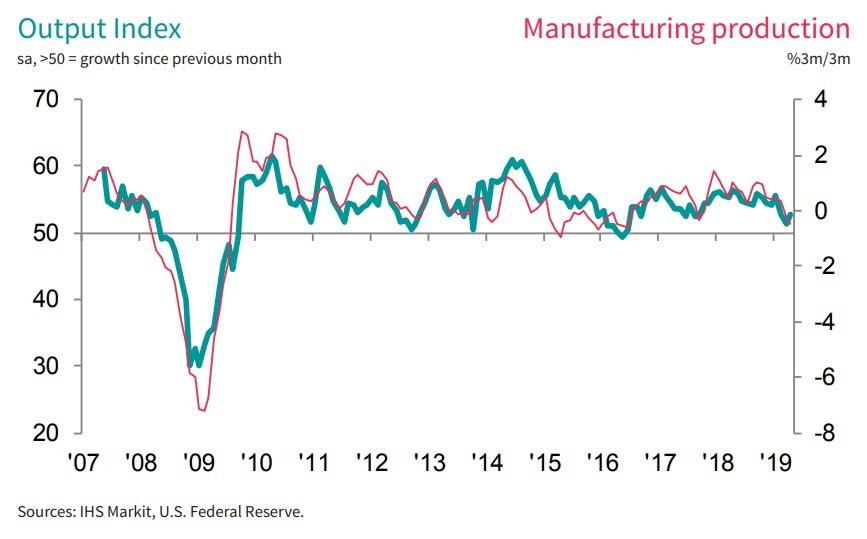

“Although the PMI ticked higher in April, the survey remains consistent with manufacturing acting as a drag on the economy at the start of the second quarter, albeit with the rate of contraction easing. Historical comparisons indicate that the survey’s output gauge needs to rise above 53.5 to signal growth of factory production. As such, the data add to signs that the economy looks set to slow after the stronger than expected start to the year.

“Employment growth also disappointed as hiring slipped to the lowest for nearly two years, albeit in part due to firms reporting difficulties finding staff amid the current tight labour market.

“There was better news on the order book front, however, with inflows of new business rising and firms signalling an improved export performance. Unfortunately, on balance, manufacturers seem sceptical that the rise in demand will persist, with future expectations of output growth slumping lower in April.

“Both input cost and factory gate price inflation rates meanwhile eased further, down to the lowest for over one and a half years, hinting that consumer price inflation rates will have continued to cool in April.”

So, probably best for Jay Powell to ignore the hard data and focus on the weak surveys to provide cover for his dovishness.

via ZeroHedge News http://bit.ly/2GP0eFK Tyler Durden

Last night’s deep-state ‘leak’ of a letter penned by Robert Mueller to AG (and longtime friend and colleague) William Barr complaining that Barr’s summary of Mueller’s findings, released several weeks before the redacted report, didn’t capture the full “context, nature and substance” of the report was of course conveniently timed to hand Democrats plenty of ammunition to tear into Barr during Wednesday morning’s hearing before the Senate Judiciary Committee.

(Of course, as we’ve pointed out, when Barr pressed Mueller about whether Barr’s summary was inaccurate, the special counsel demurred, and affirmed that he didn’t think it was. Mueller’s letter was reportedly dated March 27. Barr released the summary on March 24.)

But the fact Barr insisted during back-to-back Congressional testimony on April 9 & April 10 that he didn’t know where the special counsel stood regarding the AG’s characterization of the report has already prompted some Democratic senators to demand Barr’s resignation, per the Washington Post.

Chris Van Hollen, the Senator who asked Barr about what he knew about Mueller’s feelings about the summary, demanded Barr resign and once again accused him of being a ‘propaganda chief’ for the president.

He labeled his position “the most recent example of the attorney general acting as the chief propagandist for the Trump administration instead of answering questions in a straightforward and objective manner.”

In a prepared statement for the committee, Barr defended his handling of the special counsel’s investigation.

“As Attorney General, I serve as the chief law-enforcement officer of the United States, and it is my responsibility to ensure that the Department carries out its law-enforcement functions appropriately. The Special Counsel’s investigation was no exception.”

Pelosi seized on the reports about the Mueller letter to demand that Barr release the full Mueller report and all the underlying docs that the Demos have subpoenaed.

Attorney General Barr misled the public and owes the American people answers. It’s time for DOJ to release the full report & all underlying docs — and finally allow Mueller to testify. Americans deserve the facts. Barr must stop standing in the way. https://t.co/9mfIaKSOSj

House Judiciary Chairman Jerry Nadler demanded that Barr appear before the House Judiciary Committee on Thursday for another hearing, as the Dems have requested.

This is why it is so critical for AG Barr to appear before @HouseJudiciary on Thursday so that we can ask him about the reported letter from Special Counsel Mueller over the AG’s misleading summary of Mueller report. https://t.co/2xstNNOBoPpic.twitter.com/xBV0w65TAq

And Chuck Schumer demanded that Barr bring the full Mueller letter with him to Wednesday’s hearing, and also demanded that Mueller appear before Congress to testify.

In light of Mueller’s letter, the misleading nature of Barr’s 4/10 testimony & 4/18 press conference is even more glaring.

Barr must bring the letter with him when he testifies in the Senate tomorrow.

The Dems lapdogs in the press have also piled on, with CNN’s Chris Cilizza warning that “William Barr is in deep trouble” in an editorial published Wednesday morning shortly before the hearing was set to begin.

With all the drama, Wednesday’s hearing is bound to be a lively one. Watch live below:

Dissatisfied with media coverage of the results of his investigation into possible collusion between the Trump campaign and the Russian government, Special Counsel Robert Mueller wrote a letter to Attorney General William Barr in late March expressing frustration that Barr’s four-page memo to Congress summarizing Mueller’s findings “did not fully capture [their] context, nature, and substance.”

That’s according to The Washington Post, which obtained a copy of the letter on Tuesday. The Post did not publish the letter in full, which means we are relying here on their interpretation of a letter that supposedly complains about Barr’s interpretation of Mueller’s report. From The Post:

The letter and a subsequent phone call between the two men reveal the degree to which the longtime colleagues and friends disagreed as they handled the legally and politically fraught task of investigating the president. Democrats in Congress are likely to scrutinize Mueller’s complaints to Barr as they contemplate the prospect of opening impeachment proceedings and mull how hard to press for Mueller himself to testify publicly.

At the time Mueller’s letter was sent to Barr on March 27, Barr had days prior announced that Mueller did not find a conspiracy between the Trump campaign and Russian officials seeking to interfere in the 2016 presidential election. In his memo to Congress, Barr also said that Mueller had not reached a conclusion about whether Trump had tried to obstruct justice, but that Barr reviewed the evidence and found it insufficient to support such a charge.

Days after Barr’s announcement, Mueller wrote the previously undisclosed private letter to the Justice Department, laying out his concerns in stark terms that shocked senior Justice Department officials, according to people familiar with the discussions.

“The summary letter the Department sent to Congress and released to the public late in the afternoon of March 24 did not fully capture the context, nature, and substance of this office’s work and conclusions,” Mueller wrote. “There is now public confusion about critical aspects of the results of our investigation. This threatens to undermine a central purpose for which the Department appointed the Special Counsel: to assure full public confidence in the outcome of the investigations.”

According to The Post, the two men talked on the phone after Barr received the letter, and this conversation was friendlier in nature.

Barr is scheduled to testify before the Senate Judiciary Committee on Wednesday and the House Judiciary Committee on Thursday. Barr previously testified that he didn’t know whether Mueller supported his conclusions.

FREE MINDS

“Camille Paglia should be removed from UArts faculty and replaced by a queer person of color,” reads a recent student-created petition calling for the firing of the legendary art critic whose views on gender and sex have occasionally offended the modern progressive left. “UArts: you are disrespecting your students and putting them in danger. Do better.”

This is hardly the first time Paglia has endured such calls. When her first book, Sexual Personae, was published in 1990, faculty members at Connecticut College compared it to Mein Kampf. At the time, it was intellectually curious students who defended the book.

The situation in Venezuela may be reaching a climax: Embattled dictator Nicolas Maduro had plans to flee the country but was convinced by Russian forces to stay, U.S. Secretary of State Mike Pompeo claimed on Tuesday. Maduro disputes this. According to NPR:

U.S. officials have been characterizing the situation in Venezuela as nearing its endgame, and opposition leader Juan Guaidó called for the “final phase” of the uprising Tuesday in his attempt to remove Maduro from power. But Venezuela’s military handily stamped out pockets of resistance, and despite word from American officials that key Maduro allies are abandoning him, the country’s defense minister proclaimed his continuing loyalty. More than 50 countries support Guaidó’s claim to power.

QUICK HITS

Islamic State leader Abu Bakr al-Baghdadi has appeared on video for the first time since 2014. The self-proclaimed caliph acknowledged ISIS’s loss of territory in Iraq and Syria but promised “there will be more to come after this battle.”

Dissatisfied with media coverage of the results of his investigation into possible collusion between the Trump campaign and the Russian government, Special Counsel Robert Mueller wrote a letter to Attorney General William Barr in late March expressing frustration that Barr’s four-page memo to Congress summarizing Mueller’s findings “did not fully capture [their] context, nature, and substance.”

That’s according to The Washington Post, which obtained a copy of the letter on Tuesday. The Post did not publish the letter in full, which means we are relying here on their interpretation of a letter that supposedly complains about Barr’s interpretation of Mueller’s report. From The Post:

The letter and a subsequent phone call between the two men reveal the degree to which the longtime colleagues and friends disagreed as they handled the legally and politically fraught task of investigating the president. Democrats in Congress are likely to scrutinize Mueller’s complaints to Barr as they contemplate the prospect of opening impeachment proceedings and mull how hard to press for Mueller himself to testify publicly.

At the time Mueller’s letter was sent to Barr on March 27, Barr had days prior announced that Mueller did not find a conspiracy between the Trump campaign and Russian officials seeking to interfere in the 2016 presidential election. In his memo to Congress, Barr also said that Mueller had not reached a conclusion about whether Trump had tried to obstruct justice, but that Barr reviewed the evidence and found it insufficient to support such a charge.

Days after Barr’s announcement, Mueller wrote the previously undisclosed private letter to the Justice Department, laying out his concerns in stark terms that shocked senior Justice Department officials, according to people familiar with the discussions.

“The summary letter the Department sent to Congress and released to the public late in the afternoon of March 24 did not fully capture the context, nature, and substance of this office’s work and conclusions,” Mueller wrote. “There is now public confusion about critical aspects of the results of our investigation. This threatens to undermine a central purpose for which the Department appointed the Special Counsel: to assure full public confidence in the outcome of the investigations.”

According to The Post, the two men talked on the phone after Barr received the letter, and this conversation was friendlier in nature.

Barr is scheduled to testify before the Senate Judiciary Committee on Wednesday and the House Judiciary Committee on Thursday. Barr previously testified that he didn’t know whether Mueller supported his conclusions.

FREE MINDS

“Camille Paglia should be removed from UArts faculty and replaced by a queer person of color,” reads a recent student-created petition calling for the firing of the legendary art critic whose views on gender and sex have occasionally offended the modern progressive left. “UArts: you are disrespecting your students and putting them in danger. Do better.”

This is hardly the first time Paglia has endured such calls. When her first book, Sexual Personae, was published in 1990, faculty members at Connecticut College compared it to Mein Kampf. At the time, it was intellectually curious students who defended the book.

The situation in Venezuela may be reaching a climax: Embattled dictator Nicolas Maduro had plans to flee the country but was convinced by Russian forces to stay, U.S. Secretary of State Mike Pompeo claimed on Tuesday. Maduro disputes this. According to NPR:

U.S. officials have been characterizing the situation in Venezuela as nearing its endgame, and opposition leader Juan Guaidó called for the “final phase” of the uprising Tuesday in his attempt to remove Maduro from power. But Venezuela’s military handily stamped out pockets of resistance, and despite word from American officials that key Maduro allies are abandoning him, the country’s defense minister proclaimed his continuing loyalty. More than 50 countries support Guaidó’s claim to power.

QUICK HITS

Islamic State leader Abu Bakr al-Baghdadi has appeared on video for the first time since 2014. The self-proclaimed caliph acknowledged ISIS’s loss of territory in Iraq and Syria but promised “there will be more to come after this battle.”

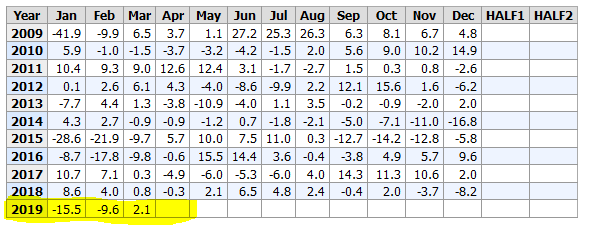

On Friday, April 26, 2019, the market was stunned with a much stronger than expected 3.2% rate of first-quarter economic growth. Wall Street expectations were clearly off the mark, ranging from 1.3-2.3%. The media took this as a sign the economy is roaring. To wit, a headline from the Washington Post started “US Economy Feels Like the 1990s.”

Upon first seeing the GDP report, we immediately looked with suspicion at the surprisingly low GDP price deflator. The GDP price deflator is an inflation measure used to normalize GDP so that prior periods are comparable to each other without the effects of inflation.

The Bureau of Economic Analysis (BEA) reports nominal and real GDP. Real GDP is the closely followed number that is reported by the media and quoted by the Fed and politicians. Since the GDP price deflator is subtracted from the nominal GDP number, the larger the deflator, the smaller the difference between real and nominal GDP.

The BEA reported that the first quarter GDP price deflator was 0.9%, well below expectations of 1.7%. Had the deflator met expectations, the real GDP number would have been about 2.4%, still high but closer to the upper range of economists’ expectations.

Fueling the Deflator

Like Wall Street, we were expecting a deflator that was in line or possibly higher than its recent average. The average deflator over the last two years is 2.05%, and it is running slightly higher at 2.125% over the last four quarters. Our expectation for an average or above average deflator in Q1 2019 were in large part driven by oil prices which rose by 32% over the entire first quarter. Due to the price move and the contribution of crude oil effects on inflation, oil prices should have had an unusually high impact on inflation measures in the first quarter of 2019.

Per the American Automobile Association (AAA), gas prices in the United States rose from $2.25 per gallon in January to $2.75 by the end of March, a gain of 22%. Gasoline RBOB futures, the most commonly quoted contract for wholesale gasoline prices, tell a similar story, rising from $1.30 per gallon to $1.83 over the quarter, for a gain of 41%.

With a good amount of digging through the BEA website, we learned that despite the substantial rise in the price of oil and gasoline in the first quarter, the BEA actually reported a decline in fuel prices. The BEA, which uses data from the Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) report, reported that fuel prices fell on average by 7.8% during the quarter. The table below for fuel prices (BLS code CUSR0000SETB) from the BLS is the direct input used to account for energy prices within the GDP deflator.

The BLS is not wrong; they are just using a three-month average, and therefore their data lags by three months. Essentially, the fuel price data feeding the first quarter GDP deflator is from the fourth quarter of 2018. During this period, the price of oil and gas fell precipitously.

With a little back of the envelope math, we conclude that had the price of oil been unchanged the deflator would have been approximately 1.45%, and Real GDP growth would have been 2.75%. Had the price risen, instead of fallen, by 7.8% the deflator would have been 1.99%, and GDP would have been 2.20% and on par with expectations. Had it risen more than 7.8%, Real GDP would have been even lower.

Implications

The BEA is not cooking the books. However, by this methodology using old data, sharp changes in fuel prices will result in flawed quarterly data. This problem is self-correcting. For instance, the sharp decline in oil prices in the fourth quarter which helped lower the deflator in the first quarter will be offset when the surge in first quarter oil prices weigh on second-quarter GDP. The graph below shows Gasoline RBOB futures to highlight the recent volatility in gasoline prices.

It is not just the deflator that concerns us about second-quarter GDP. In this weekend’s newsletter, The Bull Is Back… But Will It Stay? we stated the following:

“Almost 50% of the increase in GDP came from slower imports and a massive surge in inventories which suggests slower consumer consumption which comprises roughly 70% of economic growth. In other words, future GDP reports will also likely be weaker. (Net Trade and Inventories was 1.68% of the 3.2% rise.)”

The ratio of inventory to sales has steadily climbed over the last 12 months. If consumption stays weak, we should see companies backing off on inventory stocking. Rising inventories increase GDP and falling inventories have the opposite effect. As a result and as stated above “future GDP reports will also likely be weaker.”

Looking ahead, we are confident that the second quarter GDP deflator will be 2% or higher. We also believe that if consumption remains frail, companies will slow their inventory growth. While difficult to predict as we are only a month into the quarter, these two important factors are likely to weigh on second-quarter GDP. Keep in mind, these are only two of thousands of factors, but they play an outsized role in determining GDP.

Currently, and subject to change as more economic data is released, we have a strong suspicion that the positive surprise in the Q1 report will be followed with an equally surprising weak Q2 report. As stock markets probe new record highs, the question for investors is, will the market care?

via ZeroHedge News http://bit.ly/2ISakJg Tyler Durden

Over the weekend, the late Friday headline snuck through that the SEC and Elon Musk had once again agreed to a settlement over Musk’s use of Twitter, and the subsequent allegation that Musk should be held in contempt of court for violating a previous settlement. Now, despite Judge Allison Nathan signing off on a second settlement, one voice out of the SEC is speaking out against what he sees as a “bizarre series of events”.

The news of the second settlement being reached over the weekend went relatively unnoticed, with it again being perceived by many as letting Musk off easy, despite being far more detailed in defining what he is and is not allowed to do on Twitter going forward.

While many skeptics and Musk critics derided the second settlement, a more prominent voice has emerged from the criticism: a commissioner at the SEC, Robert Jackson. Jackson, the sole Democrat at the SEC, issued a dissenting statement on Tuesday evening after Judge Nathan approved the deal that resolved the new settlement between Musk and the SEC, according to FT.

Jackson had sharp tongued criticism toward the settlement, stating: “Given Mr. Musk’s conduct, I cannot support a settlement in which he does not admit what is crystal clear to anyone who has followed this bizarre series of events: Mr. Musk breached the agreement he made last year with the Commission—and with American investors.”

Musk had been accused of violating a previous settlement last year that required him to get his tweets pre-approved. The new agreement outlines additional information that requires advanced approval. Musk has denied breaking his initial settlement, an almost laughable defensive posture that ultimately wound up working.

The comment is a relatively rare dissent at the SEC, who has been united for the most part, at least in public, on enforcement actions under Jay Clayton. Two Republican commissioners had privately objected to the initial settlement with Mr. Musk last year. And when you can make a point clear to both sides of the aisle – namely that Mr. Musk might be getting special treatment from the SEC – why wouldn’t it warrant a further look and additional scrutiny from the public?

via ZeroHedge News http://bit.ly/2GR1s36 Tyler Durden

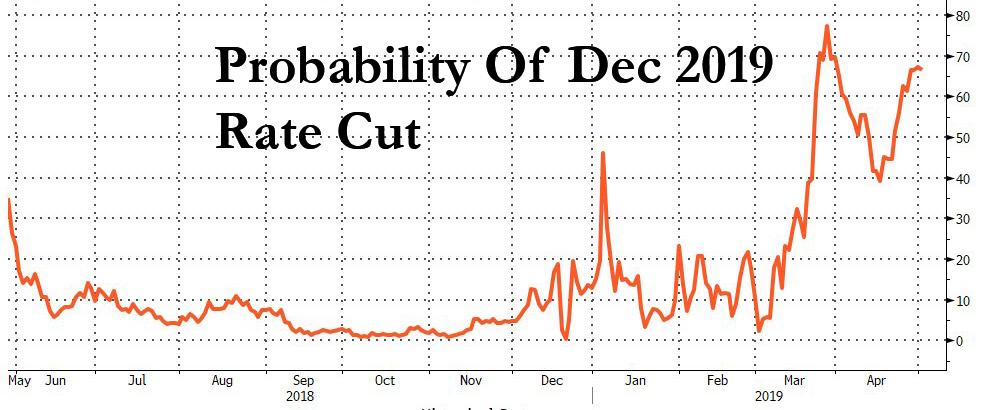

With the Fed set to announce its rate decision in under 6 hours, markets are confident that the non-data dependent Fed will cut rates by the end of 2019, despite continued strength in GDP and payrolls, in line with president Trump’s demands for a 1.00% rate cut and/or QE, and will provide further tailwind for risk assets.

But what if the market – whose discounting capacity has been destroyed by a decade of central planning – is wrong? That’s the thesis of Bloomberg macro commentator Garfield Reynolds, who writes overnight that this year’s “goldilocks” rally in stocks and bonds will likely be derailed by a far more hawkish than expected Fed.

Here are his arguments:

Rates markets have taken Fed Governor Jerome Powell’s dovish inch and mistakenly run a mile. The FOMC isn’t likely to deliver any rate cuts in the next year.

The U.S. economy isn’t in distress. Unemployment has barely ticked up from the half- century low touched in September, and 1Q GDP beat forecasts handily. Yes, inflation is nowhere to be seen, and there were plenty of devils lurking in the details of those national accounts, but a 2019 growth forecast of 2.4% is far short of a “break the emergency glass” situation.

Stocks at record highs are helping to boost financial conditions to their easiest since September and levels more often associated with robust economic expansion.

It’s fair to argue that there’s no present justification for further Fed hikes, but rate cuts have usually only come when the outlook was much darker. And yet, eurodollar futures and Fed fund futures suggest traders are convinced cuts are coming.

A shift in perceived policy bias toward easing has made bets on cuts a good reward-to-risk proposition that feeds on itself. Look at Australia where money poured in to RBA futures as markets anticipated its switch to a neutral bias — regardless of the fact it was crystal clear no move was coming for months.

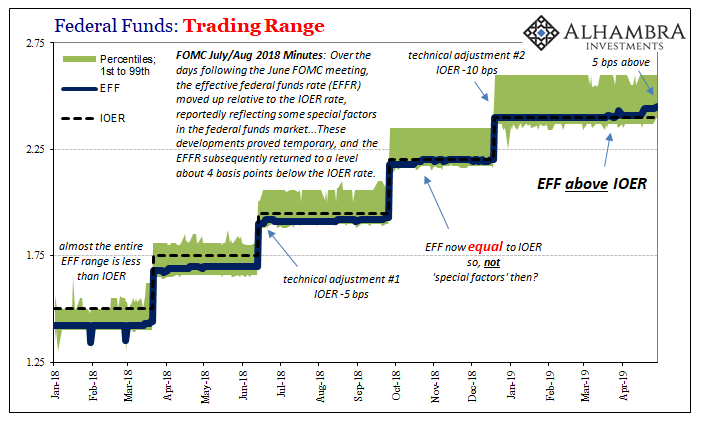

What adds to the danger for stocks and bonds — which have each benefited from expectations for easing — are money- market quirks that exacerbate the message from those rate cut bets. Due to the impact of balance sheet reduction, the effective Fed funds (EFF) rate has climbed 5 basis points above its supposed policy-set ceiling of the interest on excess reserves (IOER). That’s potentially a 20% head-fake for anyone looking to gauge market expectations for rate moves.

Usually, 60% odds at the very least should be needed before investors can bank on a move coming. If we price off the IOER “ceiling” instead of the “rogue” EFF level, the odds for a cut this year drop from 67% to just under 50%.

That’s still too high a probability given the economic reality, but it at least favors Powell’s wait-and-see rhetoric instead of the perception that one-or-more cuts are priced.

Unfortunately, stocks and bonds both appear ripe for disappointment from an overly aggressive front-end rates market, potentially setting off fresh volatility spikes and a stocks meltdown.

via ZeroHedge News http://bit.ly/2GNKxP1 Tyler Durden

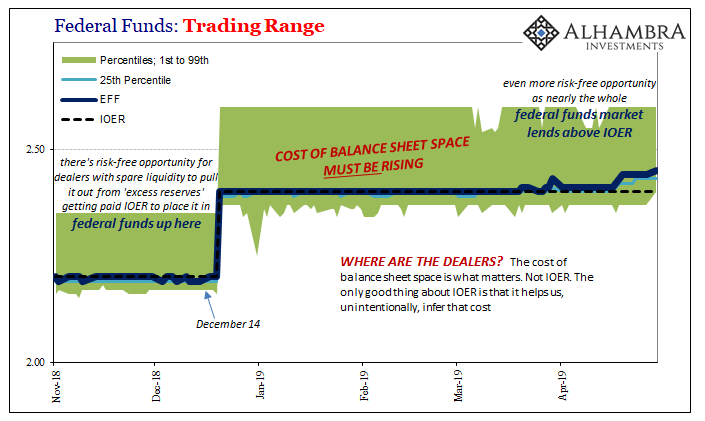

Federal funds is up again. As of yesterday, the 29th, the effective rate (EFF) is now 5 bps above IOER. That takes it to within 5 bps below the top of the Federal Reserve’s policy range. According to FRBNY, the 1st percentile in yesterday’s session was 2.40%, meaning that almost the entire federal funds market is paying more than IOER. Where are the dealers?

If a scramble for liquidity shows up here, what is it like everywhere else where it does matter? The federal funds market is nothing more than leftover pocket change of the FHLB’s. But with these rates, there should be more than that going on. There is opportunity for any enterprising dealer to take advantage of risk-free spreads, to make something more than what it is.

And the profit opportunities just sit there.

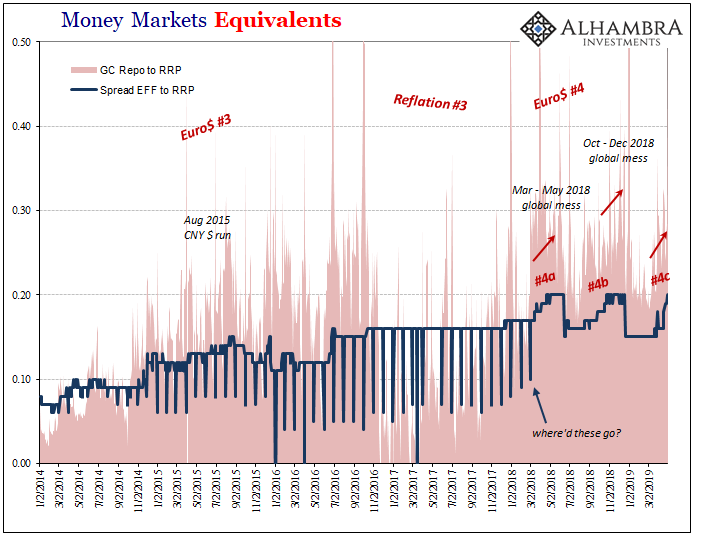

It’s not just here where the dealers publicly demonstrate their hoarding. If EFF is up you pretty much know what’s going on in the repo market. There is no obvious reason why month-end in repo should be so dry. We’ve become accustomed (though only during these Euro$ squeeze periods) to quarter-end runups in the GC rates. Month-end is something else.

That’s just what happened yesterday. The final trading day of a middle month in Q2 2019 for some reason became extra special hard in terms of repo market liquidity. It’s not nearly the insanity experienced at the very end of 2018, but the GC rate for UST collateral was fixed today at 2.807% (DTCC). That’s nearly 56 bps above RRP (literally off the chart below), and a lot more than yesterday’s 2.534%. The GC rate for MBS was even higher, 2.915%.

The few who do notice these vitally important indications will keep talking about T-bills or some other technical-sounding excuse. Meanwhile, going back to the original outbreak last year, the world keeps coming apart. The global economy’s minus signs keep piling up and proliferating.

If you are a big leveraged player, meaning just about every large financial entity on the planet, you can’t afford to be so sanguine or to keep your head stored so firmly, deeply in the sand. As illiquidity escalates with these warnings, the chance of the most dreaded phone call in finance rises.

The collateral call creeps ever closer, the one that can terminate your career and your firm if due care is not exercised. The lingering lesson of Bear.

Given this situation, it doesn’t matter one bit that you might agree with Economists. Let’s say you are ultra-positive on the economy. The unemployment rate in the US is the true picture of the domestic situation, inflation has to therefore rise. The world isn’t going to keep buying all the US federal debt, not with the economy on the rise and demand for UST’s dropping against that rising supply.

It’s going to be really bad for especially duration (meaning long end UST holders) – at some point.

Those factors, however, don’t mean a damn thing today. All that does matter is EFF and repo (and interest rate swaps, as well as FX). Liquidity is primary over everything. The more these “benign” problems continue forward and intensify, the less relevant those other parameters will be. The bond market massacre can easily wait. A long time.

And that’s if you actually believe Economists.

They are thinking something else because they don’t get bonds. CNBC’s chief Economist Steve Liesman sent out a survey to a lot of others like him. Guess what? Surprise of all surprises, the Economists almost uniformly believe that Economists are right and the bond market must be wrong.

Almost two-thirds of them. 63% are still forecasting another Fed rate hike by the end of this year. Whereas bond and money markets continue to betting trillions on a cut perhaps more, not these guys. They are sticking with their econometric models where the unemployment rate cannot possibly be so faulty (again).

“The markets are irrationally pessimistic about the future. There is no recession coming,” wrote Chris Rupkey, chief financial economist at MUFG. “Cutting rates for low inflation at this time is ill-advised…The Fed should restart its gradual pace of rate hikes later on this year.” [emphasis added]

For them, green shoots and an overblown growth scare. It doesn’t matter that, according to the same survey, these same Economists had last year expected the 10-year UST yield to rise to 3.5% or more but now only expect 2.75% by the end of 2019. The difference is just transitory stuff. China trade tensions that will go away when a trade deal is done.

But that’s the thing. Here we are one-third of 2019 in the books already and EFF keeps showing up Jay Powell; repo keeps doing remarkably disruptive things. And the economic data continues to follow the obviously illiquid nature of global money – as do bond yields. Even the US economy’s biggest (purported) boom in a long time has proved vulnerable, pulling up especially lame recently in all the key components (income most of all).

We’ve been here before, of course. What I wrote in May 2014could’ve easily been written today:

That sets up another “titanic” struggle between economists and money markets – academic models against those with actual money positions. The economist side sees taper as a signal that the economy is going to take off (as intended under the Bernanke scenario of influencing expectations), whereas the credit and dollar markets may be coming around to taper as optimal control, preserving policy margins ahead of economic turbulence.

We know which side stocks are betting on.

Stocks didn’t care, outside of seven months starting August 2015, that Economists got it wrong for the third time in the last almost twelve years dating back to Bill Dudley’s first ugly encounter with the curves in 2007. There was no recovery and acceleration in 2015, no big liftoff as had been planned by Economists and central bankers in 2014.

Bonds were right. Euro$ #3 pushed the US economy very, very close to recession while the rest of the world suffered a variably intense nightmare. The way the markets are positioned now, that’s actually the upside to today’s confirmed Euro$ #4, the least worst case. If bonds are specifically right about rate cuts, that’s more of a downside still.

Then again, Economists and their models could just get lucky for once. That’s about all they have going for them at this point. When does it ever just work out great once all the biggest financial institutions in the world, despite what the Economists working for them say, all pile in on liquidity preferences? Pretty much never, especially when the reasons they are and have been are right there in front of everyone.

via ZeroHedge News http://bit.ly/2DJ2EEW Tyler Durden

After March’s gravely disappointing miss (well below the March rebound in non-farm payrolls), ADP employment was expected to rebound to its somewhat flat forecast of 180k in April.

After last month’s +129k miss, ADP played catch up this month with a massive +275k (and upward revision to +151k for March) with Services adding 223k and Goods producers up 52k

“April posted an uptick in growth after the first quarter appeared to signal a moderation following a strong 2018,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute.

“The bulk of the overall growth is with service providers, adding the strongest gain in more than two years.”

Information and Natural Resource jobs declined…

Mark Zandi, chief economist of Moody’s Analytics, said,

“The job market is holding firm, as businesses work hard to fill open positions. The economic soft patch at the start of the year has not materially impacted hiring. April’s job gains overstate the economy’s strength, but they make the case that expansion continues on.”

Soaring GDP and employment data – and yet the market still expected 30bps of rate cuts in 2019? Something is wrong here!

via ZeroHedge News http://bit.ly/2WpBxpG Tyler Durden

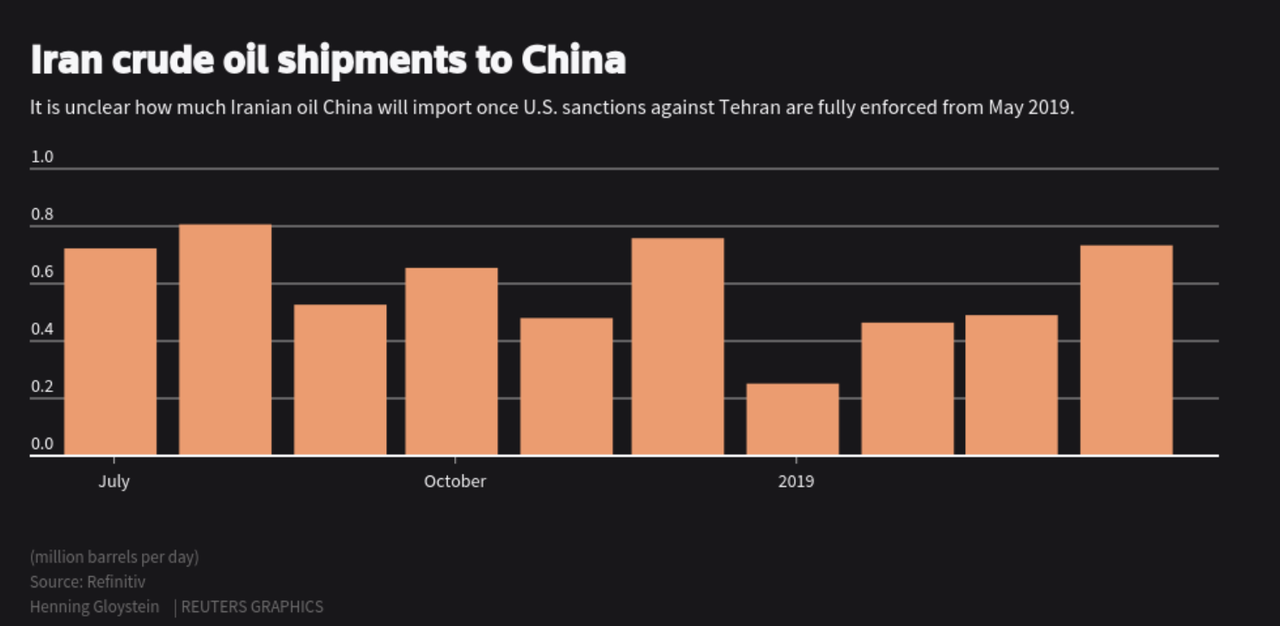

It’s no secret that Beijing has chafed at American audacity to try and dictate whom Chinese refineries can and can’t buy oil from. And in the latest example of just how aggravating the decision to end waivers for Iranian crude imports has been for the world’s second-largest economy, Reuters reported that some 20 million barrels of Iranian crude have been languishing at the northeastern port of Dalian for months, but because of the US’s decision to re-impose sanctions on Iran back in November, nobody wants to touch the oil.

Even when the waivers were in effect, Chinese refineries couldn’t secure financing and insurance that would allow them to purchase the oil because of the uncertainty surrounding the future of the waivers.

Iran sent the oil to China via the National Iranian Tanker Company before the sanctions were imposed as Iran struggled with a backlog of oil that had exhausted the country’s domestic storage capacity. So Beijing, the largest buyer of Iranian oil, allowed the NTCC to store some oil in so-called bonded storage tanks situated in the Dalian port. The oil has yet to go through Chinese customs.

China filed a formal complaint with the US over its decision to end the waivers, but the US has refused to consider any exceptions to its plans to reimpose full sanctions.

As one analyst told Reuters, no Chinese company will touch the oil unless specifically instructed to do so by the Chinese government.

The oil is being held in so-called bonded storage tanks at the port, which means it has yet to clear Chinese customs. Despite a six-month waiver to the start of May that allowed China to continue some Iranian imports, shipping data shows little of this oil has been moved.

Traders and refinery sources pointed to uncertainty over the terms of the waiver and said independent refiners had been unable to secure payment or insurance channels, while state refiners struggled to find vessels.

The future of the crude, worth well over $1 billion at current prices, has become even more unclear after Washington last week increased its pressure on Iran, saying it would end all sanction exemptions at the start of May.

“No responsible Chinese company with any international exposure will have anything to do with Iran oil unless they are specifically told by the Chinese government to do so,” said Tilak Doshi of oil and gas consultancy Muse, Stancil & Co in Singapore.

To be sure, Reuters says, some of the oil was apparently purchased by a Sinopec refinery. But the bulk of the stock remains untouched.

Some Iranian oil sent to Dalian has moved, according to a ship tracking analyst at Refinitiv.

Dan, a supertanker owned by NITC moved 2 million barrels of oil from Dalian more than 1,000 km (620 miles) to the south to the Ningbo Shi Hua crude oil terminal in March, according to Refinitiv data.

Ningbo is home to Sinopec’s Zhenhai refinery, one of the country’s largest oil plants with a capacity of 500,000 barrels a day and a top processor of Iranian oil.

The headache for Beijing will likely only get worse, because shipping data show more Iranian crude is heading for Chinese ports.

For now, more Iranian oil is heading to China, with the supertankers Stream and Dream II due to arrive in eastern China from Iran on May 5 and May 7, respectively, Refinitiv data showed.

Some of this crude may be from Chinese investments into Iranian oilfields, a sanctions grey area.

Eventually, this could create incentives for non-compliance that are just too powerful for Chinese companies to ignore, particularly companies that have investments in Iranian oilfields. Some companies might try bartering for the oil, while others resort to illegally forged documents.

Whether China will keep buying oil from Iran remains unclear, but analysts at Fitch Solutions said in a note “there may be scope for imports via barter or non-compliance from … China.”

Muse, Stancil & Co’s Doshi said the only way to get the Iranian oil out of Dalian now was by cheating.

“Only rogue parties might try to cheat the system and try to pass the Iranian oil at Dalian as something else via fraudulent docs. But I doubt this is easy or can amount to much in terms of volume.”

Regardless of what happens to the oil, the incident serves as a reminder of the many annoyances that US sanctions create for its geopolitical rivals. Every barrel of China has sitting offshore that its refineries can’t touch is one more reason for Beijing to pursue the creation of an alternative payments channel that’s outside of American control…and more incentive for Chinese refineries, at the government’s behest, to push exporters to accept payment in yuan, something that the Shanghai-traded, yuan-denominated oil futures have already incentivized.

The US should acknowledge the perverse incentives for de-dollarization that its own policies have created – something that one of America’s favorite boogeyman has labeled a “colossal strategic mistake.”

via ZeroHedge News http://bit.ly/2GUMNp5 Tyler Durden