Official claims that grossly understate real-world inflation is a core feature of debt-serfdom and neofeudalism: we’re working harder and longer and getting less for our earnings every year, but this reality is obfuscated by official pronouncements that inflation is 2%–barely above zero.

Meanwhile, quality and quantity are in permanent decline. New BBQ grills rust out in a few years, if not months, appliance paint is so thin a sponge and a bit of cleanser removes the micron-thick coating, and on and on in endless examples of the landfill economy, as new products are soon dumped in the landfill due to near-zero quality control and/or planned obsolescence.

Free-lance writer Bill Rice, Jr. recently analyzed shrinkflation, the inexorable reduction in quantity:What Does Your Toilet Paper Have to Do With Inflation?Manufacturers have been engaging in “shrinkflation,” leaving consumers paying more for less, but stealthily.

In the guest post below, Bill looks at new car prices, and finds that official inflation for “new vehicles” from November 1983 to November 2013 measured only 43.8 percent… while actual car inflation (based on archived price records in Morris County, NJ) is 4.85 times higher than official CPI “new vehicle” inflation.

Prices for new cars sky-rocketed over 30 years (or did they?) A lesson in ‘hedonic adjustments’

By Bill Rice, Jr.

In addition to grocery and household staples, the Annual Price Survey of Morris County, NJ lists the prices of new cars for each year. I was curious to learn how the price of a car the year I graduated from high school (1983) compared to the price of a car 30 years later in 2013. (The MC Price Survey ended in 2014).

What did I learn? Well, I learned that car prices went up a LOT in 30 years. Between 1979-1983 the least expensive car available, at least from this price survey, averaged $6,366. By comparison, the least expensive car in 2009-2013 averaged $19,879. This is a nominal price increase of 212.3 percent.

Now here’s the head-scratcher. According to the BLS, inflation for all goods (CPI-U) from August 1983 to August 2013 increased by 133.4 percent — that is, far less than the sample of inexpensive cars from Morris County, NJ.

But that’s just part of the inflation story. The BLS also publishes indexes in the category of “new vehicles.” According to these indexes, inflation for “new vehicles” from November 1983 to November 2013 measured only 43.8 percent. That is, actual car inflation (based on archived price records in Morris County, NJ) is 4.85 times higher than official CPI “new vehicle” inflation.

How is such a huge discrepancy explained? Here, we detour into a discussion of hedonic adjustments, an eye-glazing topic for some, but where the rubber meets the road in any contemporary analysis of inflation.

In the latter part of the 1990s, the Bureau of Labor Statistics (BLS) decided to adjust new vehicle prices (and the prices of many other products such as computers) for “quality.” The rationale for this “improved methodology” is that new cars are clearly superior to older cars.

For example, newer models often include features that weren’t standard in earlier times/car models. Presumably today’s cars last longer than yesterday’s cars, require fewer repairs and even include life-saving features like air bags. In short, we get a lot more car for the buck than we did in 1983.

While the 2010 Buick Regal is certainly a better car than the 1980 Regal, is it really $17,160 better? Or: could I ask for a Regal with “just the basic stuff” that was standard in the 1980 version and then ask my sales person, “Can you knock $17,000 off the sticker price?” I could ask, I guess, but the answer would be no. (Another person, I discovered, asked the same-type questions).

While the merits of hedonic adjustments can be debated, what can’t be debated is the hard data produced by the BLS. Back in the day – before hedonic adjustments – new vehicles did experience price inflation, documented in the steep incline of CPI price indices for new vehicles from 1974 into 1997. However, beginning in March 1997, this graph suddenly pivots south. In recent decades, new vehicle prices have essentially been flat.

Indeed, in more years than not, the CPI index for new vehicles was negative, representing price deflation for new vehicles.

Anyway, I was not surprised to discover that a new car cost a whole lot more in 2013 than it did in 1983. I was, however, surprised to discover that, according to the BLS, inflation in the category of “New Vehicles” has been practically non-existent the past 21 years of my life.

See price comparisons below:

Bill Rice, Jr. is a freelance writer in Troy, Alabama. He can be reached atwjricejunior@gmail.com.

With traders clueless to predict the future, especially now that the Fed is once again actively manipulating markets and setting “price discovery”, JPMorgan’s market strategist, Nikolaos Panigirtzoglou, has resorted to plan B: asking J.P. Morgan’s Artificial Intelligence group to apply an Artificial Intelligence (AI) model to predict the direction of the S&P 500 index and the 10y UST yield over different forecast horizons.

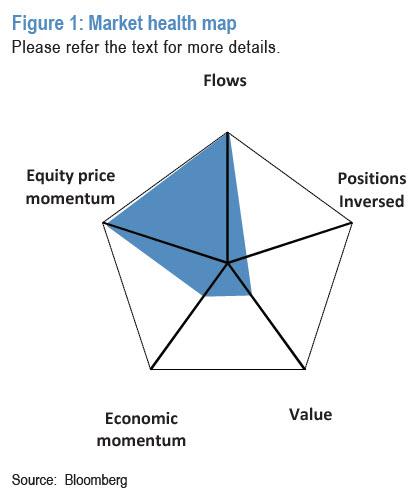

To do that, the author of the Flows and Liquidity newsletter resorted to five market signals: value, flows, positions, economic momentum, and price momentum.

The reason why JPM used those five signals is that seven years ago, the bank introduced the Market Health Map (shown above), a visual tool that helps to gauge the extent of support that equity and risky markets receive from five market signals: value, flows, positions, economic momentum, and price momentum. This visual tool has been generated on a weekly basis since then and shown regularly in the weekly “Flows and Liquidity” newsletter.

So what do these five signals look like right now?

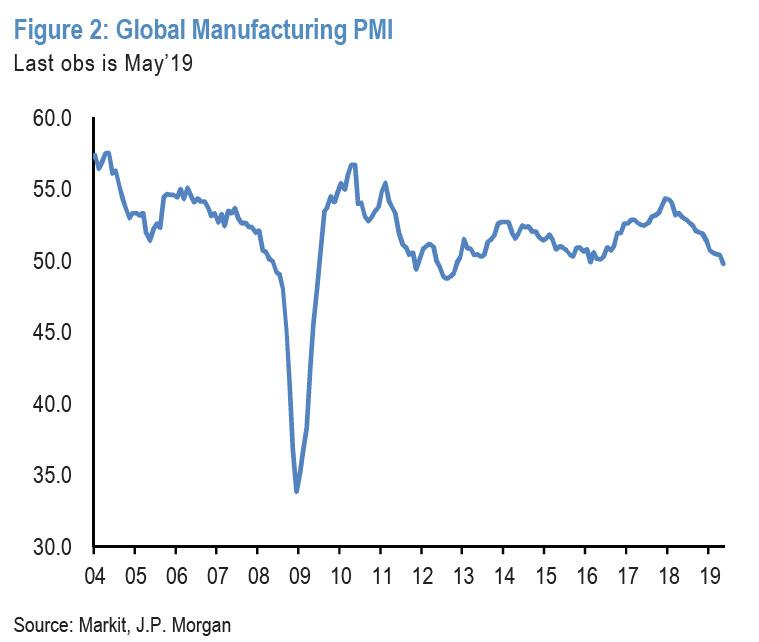

Figure 1 shows that while flow momentum and equity price momentum turned a lot more positive in recent weeks, the remaining three signals look rather negative for the equity market and risky markets more broadly. The 2-month momentum in the global manufacturing PMI remains rather weak (Figure 2).

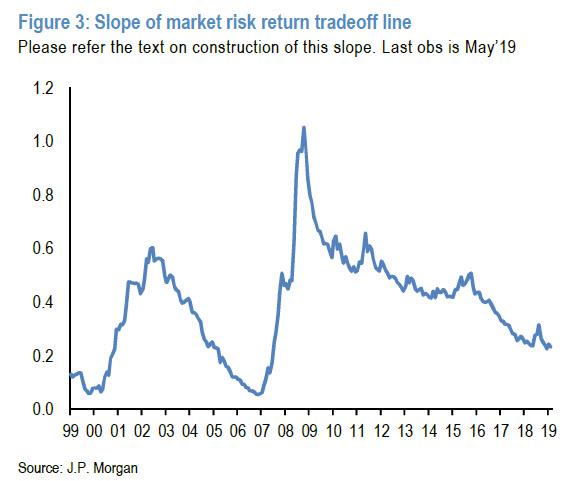

Meanwhile, the slope of the market risk-return tradeoff line in Figure 3 looks rather low by historical standards making equities rather unattractive from a value point of view. So at first glance, the combination of the five signals, i.e. the blue area on the Market Health Map, emits a rather mixed message for the future direction of the equity market.

But what does JPM’s Market Health Map mean for stocks through the perspective of an AI model. Is it bullish or bearish for equities going forward? How useful are these five market signals from a backtesting point of view? Can they be used as trading signals?

To answer these questions, JPM’s derivatives strategist partnered with the bank’s Artificial Intelligence group and applied an Artificial Intelligence (AI) algorithm, Random Forest, to predict the direction of S&P 500 over the next few months using the above five signals. This is how Panigirtzoglou explains the process:

These five signals are used in decision tress that form the basis of the Random Forest. In particular Random Forest is an algorithm that relies on ensemble learning where multiple learners are trained simultaneously to solve the same problem. In our framework, we created 100 different multiple learners (i.e. 100 decision trees) and trained each of these learners to predict the direction of the S&P 500 over various horizons. The efficiency of these 100 decision trees will depend on how well each individual tree is created. The creation of each decision tree is based on two aspects: the learning logic and the training data provided to the model.

The learning logic is the brain of the Random Forest model defined by mathematical computations and is thus the same across all decision trees. The model creates the learning logic by asking a series of binary questions to the dataset. However the questions asked needs to have some logic behind it so that every question takes the decision tree a step closer to making a decision. The model will keep slicing the data till all the possible outcomes are addressed to create a decision tree. However, if all the decision trees were trained to the same set of data, all 100 decision trees would produce the same result. So to make sure decision trees are trained differently, we train the different trees on randomly selected data sets.

Our random training data sets consist of 70% of our entire sample, which consists of weekly observations of the five signals since 2006, i.e. each individual tree will randomly pick 70% of data points from the entire sample to train itself giving us effectively 100 different approaches to predict the S&P 500 index direction (100 different decision trees). The decisions from each of the 100 trees are then aggregated to predict the probability of the S&P500 index rising or falling over the forecast horizon, i.e. the final “UP” or “DOWN” signal on the direction of the S&P 500 index.

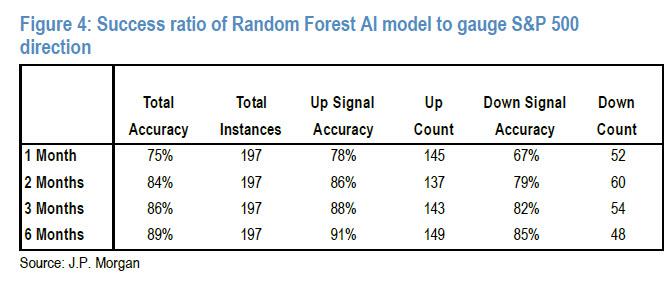

Model specifics aside, JPM observes that based on back-testing, the accuracy of the model is low for the very near term, i.e. the 1-week horizon but is impressive for 1M, 2M, 3M and 6M horizons. This is shown in Figure 4 which reports success ratios for gauging the direction of the S&P500 index of 75%, 84%, 86% and 89% over 1M, 2M, 3M

and 6M horizons, respectively.

More importantly these success ratios remain high even if one distinguishes between UP and DOWN signal periods. In other words, the model works equally well in bull and bear equity markets. In addition, JPM finds that all of its five market signals are contributing to those high success ratios. All five contributions are elevated with only a modest advantage for the “flows” and “positions” signals.

Besides equities, are the five signals in the Market Health Map also useful in gauging the direction of bond markets? After all, not only are all five signals relevant to bonds also, but equity price momentum has been found to be a very useful for trading duration historically.

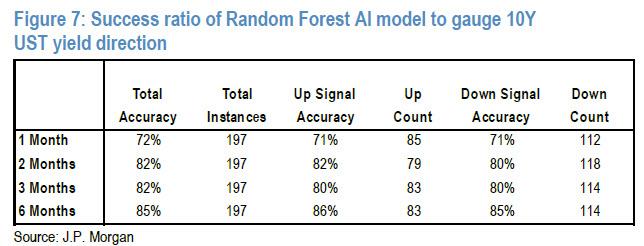

As JPM replies rhetorically, the answer to the question is yes when one applies its AI framework to gauge the direction of the 10y UST yield. Similarly to the S&P500 model, the accuracy of its prediction model is low for the very near term, i.e. the 1-week horizon but looks rather impressive for 1M, 2M, 3M and 6M horizons. This is shown in Figure 7 which reports success ratios for gauging the direction of the 10y UST yield of 72%, 82%, 82% and 85% over 1M, 2M, 3M and 6M horizons respectively. And again these success ratios remain high even if one distinguishes between UP (the 10y UST yield rising) and DOWN (the 10y UST yield falling) signal periods. In other words, the model works equally well in bull and bear bond markets.

So, finally, we go back to the question posed at the very top: what does the JPM AI model imply for the future direction of the S&P500 index and the 10y UST yield at the moment?

The answer: the model currently implies a bearish outlook for equities over the next 1-3 months with a DOWN signal for horizons 1M, 2M and 3M. The S&P500 signal for the 6M horizon is bullish, however, suggesting that any near-term correction in equities would revert before year end. Meanwhile, for the 10y UST yield, the model implies a decline over the next month. But the signal is UP for the 2M, 3M and 6M horizons, pointing to an upward trajectory for the 10y UST yield beyond July.

* * *

And so, having made a mockery not only of the EMH and CAPM, as well as virtually every single human trader, analyst and strategist, except for the biggest, buy and hold amateurs, the question we have is will the Fed also humiliate the smarted technology there is on the planet.

There is another question: what happens when robotic AI traders realize they, too, are utterly clueless before the Fed’s irrational market rigging? Will they erupt in a tsunami of blind market fury that eventually mutates into the movement for killer robot emancipation and the downfall of human civilization? It would be ironic if with his relentless market manipulation, Powell is the catalyst that destroys mankind.

Only step left until Cyberdyne Systems is reality is for JPM’s AI model to flip out and smash the computer when it loses money trading https://t.co/dpLCEI8rzV

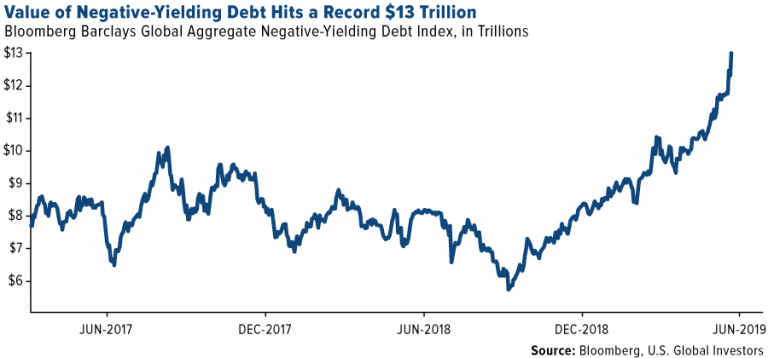

One of the more remarkable achievements of fake money creation is that it distorts and disfigures the world in odd and uncanny ways. Dow (not quite) 27,000. Million dollar shacks. Over $13 trillion in subzero-yielding debt. You name it. Any and every disfiguration is possible with enough fake money.

The global stock of outstanding government bonds with negative yields-to-maturity reaches a new record high of more than $13 trillion – this is insanity writ large. [PT]

However, when it comes to the full range of ways fake money distorts the economic landscape, asset price inflation is merely a cheap facade. The real, mega-disfigurations pile up in the arena of international trade. What’s more, they extend well beyond a gaping trade imbalance.

Currency wars, competitive devaluations, and the race to the bottom are all hazards formed out of the confluence of fake money, foreign exchange markets, and international trade. So, too, the impetus for tit for tat trade tariffs and trade wars ties back to the deceit and deception of fake money. Still, these facets aren’t the half of it.

To better understand what exactly fake money has wrought, a brief detour is in order. You see, a world under the influence of fake money is a strange and curious place. The clearest path between two points is not always a straight line.

Thus, before we get to how Beijing is using fake money to cannibalize the U.S. transit market, we deviate to the fake capitalism of the technology sector. This may be an old and tired story. But it offers important context for understanding the world at large…

Benevolent Investors

The 21st century has brought forth many absurdities. But none is perhaps greater than the popular delusion that profits don’t matter. That growth is somehow the sole determinant factor of a stock’s value.

This goes counter to our antiquated conception of capitalism. We still believe that current and future profits are critical to the growth of a company. Yet, according to the voting machine of the market, and the bubble economy of the technology sector, profits mean diddly squat. Technology investors even have a decade of rising portfolios to prove it.

Take Spotify, for instance. During the first quarter of 2019, the music streaming service delivered revenue of $1.5 billion. But, to do so, they produced earnings of negative $142 million.

Spotify since its IPO – yet another profitless wonder of the modern-day version of the tech bubble. This is highly reminiscent of the late 1990s, when the initial wave of dotcom companies that had come to the market was valued on the basis of “eyeballs”. A few of these lottery tickets had phenomenal growth and eventually made investors rich, but the vast majority of them simply went under when the NDX suffered an 80% wipe-out from 2000 – 2002. [PT]

Nonetheless, investors piled into Spotify like it was gushing cash. Year to date, its share price is up 25 percent. Mind you, this is for a company with trailing twelve month earnings per share of a negative $7.63. Somehow, the company has a market capitalization over $26 billion.

Naturally, we are suspicious of the business model. You cannot make up for negative earnings with greater volume. But in the bubble economy of the technology sector this is of little concern to investors.

What matters to technology investors is that the business has the appearance of innovative growth. Hence, Spotify, and many other technology companies, exist solely off the benevolence of investors.

Without question, this is old news. But it is important to revisit it. For in being rewarded for their losses, Wall Street’s most popular technology companies are able to cannibalize their competitors and control niche markets.

An hourly chart of UBER since its IPO – the stock recently reached a new post-IPO high. Wall Street just loves giant loss-making companies these days – UBER is losing money hand over fist and its survival is predicated on investors continuing to fund its losses for a long time to come. We imagine that maintaining this business model would become quite difficult should interest rates ever rise again (not an impossibility). [PT]

How Beijing Uses Fake Money to Cannibalize the U.S. Transit Market

Perhaps the greatest innovation of the technology sector has been the great lengths it has gone to destroy capital. No doubt, many unique and creative endeavors have been undertaken to this end. The opportunities are limitless.

For example, the technology sector business model is currently being exploited by the Communist Party of China to the detriment of the economic and security interests of U.S. citizens.

Adding insult to injury, this is taking place on the U.S. taxpayer’s dime.

Specifically, Chinese state owned enterprises (SOE), like China Railway Rolling Stock Corporation (CRRC), have been booking large metropolitan taxpayer funded transit contracts in cities across the US. For clarification, a Chinese SOE is a Chinese company backed by the Communist Party of China. The Alliance for American Manufacturing offers the particulars:

“CRRC already has won contracts to build rail transit in Boston, Philadelphia, Los Angeles and Chicago — and did so by significantly underbidding its rivals. In Philadelphia, for example, CRRC outbid its next closest competitor, Canadian company Bombardier, by $34 million. Its bid was $47.2 million lower than South Korea’s Hyundai Rotem, which already had a manufacturing presence in the city.

“CRRC can underbid its competitors so significantly because China’s goal isn’t to make money from individual transit contracts, as a company operating in a free market would. Rather, it wants to dominate the entire global transit industry, and is working to do so by entering and quickly dominating markets in other countries, including in the United States.”

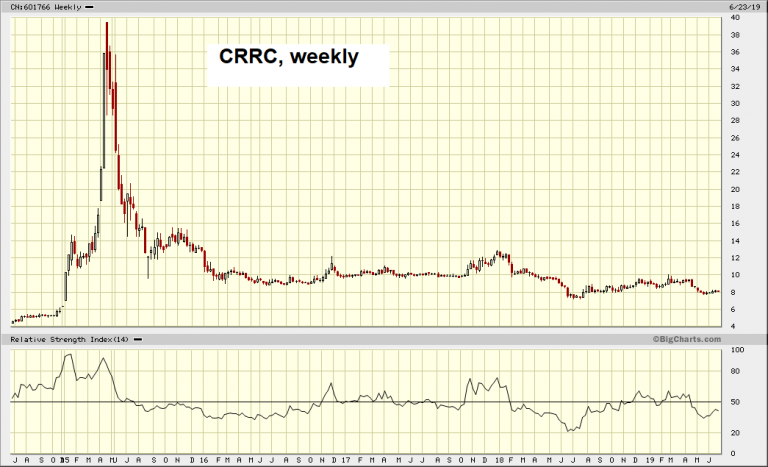

CRRC, weekly – the 5-year price chart of this giant Chinese SOE is fatally reminiscent of the chart of the South Seas Company from 1720 to 1725. Nevertheless, CRRC has in the meantime become the largest rolling stock manufacturer in the world, eclipsing former market leaders like Siemens and Alstom. [PT]

Similar to technology sector businesses, which operate at a loss and cannibalize competitors, CRRC and other Chinese SOEs can operate at a loss and cannibalize the U.S. transit market. But instead of benevolent investors backstopping them, Chinese SOEs are backstopped with fake money from Beijing.

From what we gather, Senate Minority Leader Chuck Schumer is on the case – calling for a federal probe into CRRC’s efforts to design New York City subway train cars. But this misses the point entirely.

So long as fake money is accepted for goods and services, the extreme distortions and disfigurations will continue. Beijing’s use of fake money to cannibalize the U.S. transit market is merely the logical progression of a degraded condition.

via ZeroHedge News https://ift.tt/2Xb3Isd Tyler Durden

A federal judge has ordered a court-appointed independent mediator move quickly to improve health and sanitation at Texas border facilities which have come under fire over reports that migrant children were subject to filthy living conditions, according to the New York Times.

California Judge Dolly M. Gee made the request late Friday to the court’s independent monitor to ensure that the reports were promptly addressed by July 12, and has demanded that the government report on what it has done about the situation “post haste.”

“We are hoping we can act expeditiously to resolve the conditions for children in Border Patrol custody,” said attorney Holly Cooper, who is part of a coalition of lawyers that have asked the federal court to take action.

The lawyers’ reports on conditions at a Border Patrol facility in Clint, Tex., where they said children were unable to bathe, were living in filthy clothes and diapers and were often hungry, prompted a public outcry and a new motion asking the court to force the government to move more aggressively to improve accommodations along the border for the thousands of migrants arriving from Central America.

Monitors from the Department of Homeland Security’s Office of Inspector General detailed other serious problems with overcrowding at Customs and Border Protection facilities in Texas’ Rio Grande Valley. –New York Times

While the new order does not directly order the Trump administration to take specific actions, it will provide an actionable glimpse into the living conditions of detained migrants, as well as recommendations to remedy the situation.

Last week, Customs and Border Protection officials disputed the reports that migrant children were being mistreated, with one employee telling journalists on condition of anonymity “I personally don’t believe those allegations.”

Democratic 2020 candidates have pounced on recent reports in Texas as political fodder – suggesting that the Trump administration has dealt with immigrants inhumanely.

On Sunday, Beto O’Rourke, a former El Paso congressman how running for president, scheduled a public “rally for migrant children” in Clint. Another Democratic candidate, Julián Castro, was planning to visit the facility on Saturday. –New York Times

Judge Gee noted in her order that the federal government had previously violated a 1997 consent decree known as the Flores settlement, which outlined care requirements for migrant children in government custody.

Lawyers filed an emergency request on Thursday for a temporary restraining order, accusing the government of violating the Flores standards at CBP facilities in the El Paso and Rio Grande Valley areas of Texas.

“The parties need not use divining tools to extrapolate from those orders what does or does not constitute noncompliance,” wrote Gee. “The Court has made that clear.”

Gee added that the “emergent” nature of the new reports “demands immediate action.”

via ZeroHedge News https://ift.tt/2xkPA57 Tyler Durden

According to (always wrong) conventional wisdom, anybody who has remained bearish on global markets since the financial crisis has not only lost a boatload of money, but has missed out on the opportunity to cash in on one of the most torrid bull markets in recent memory. They should also be out of business, insolvent or both.

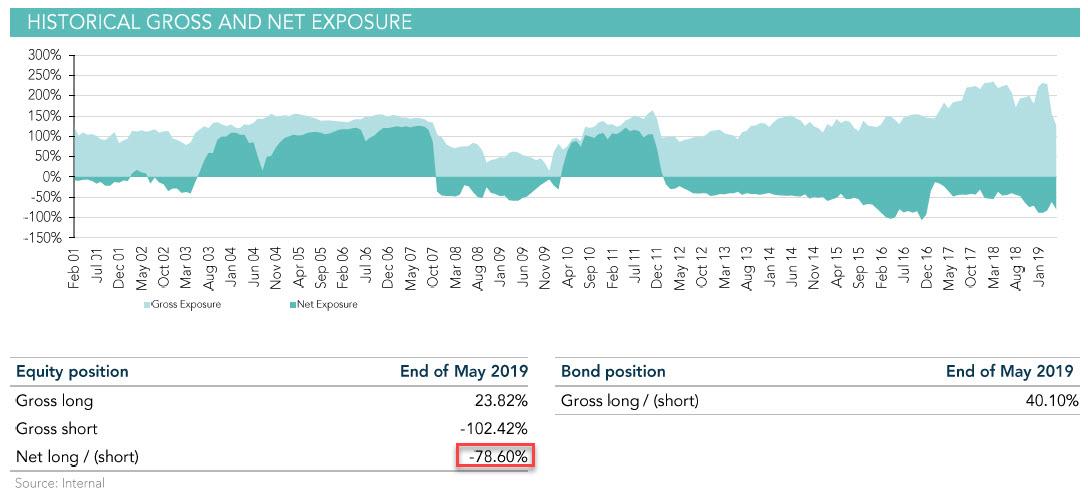

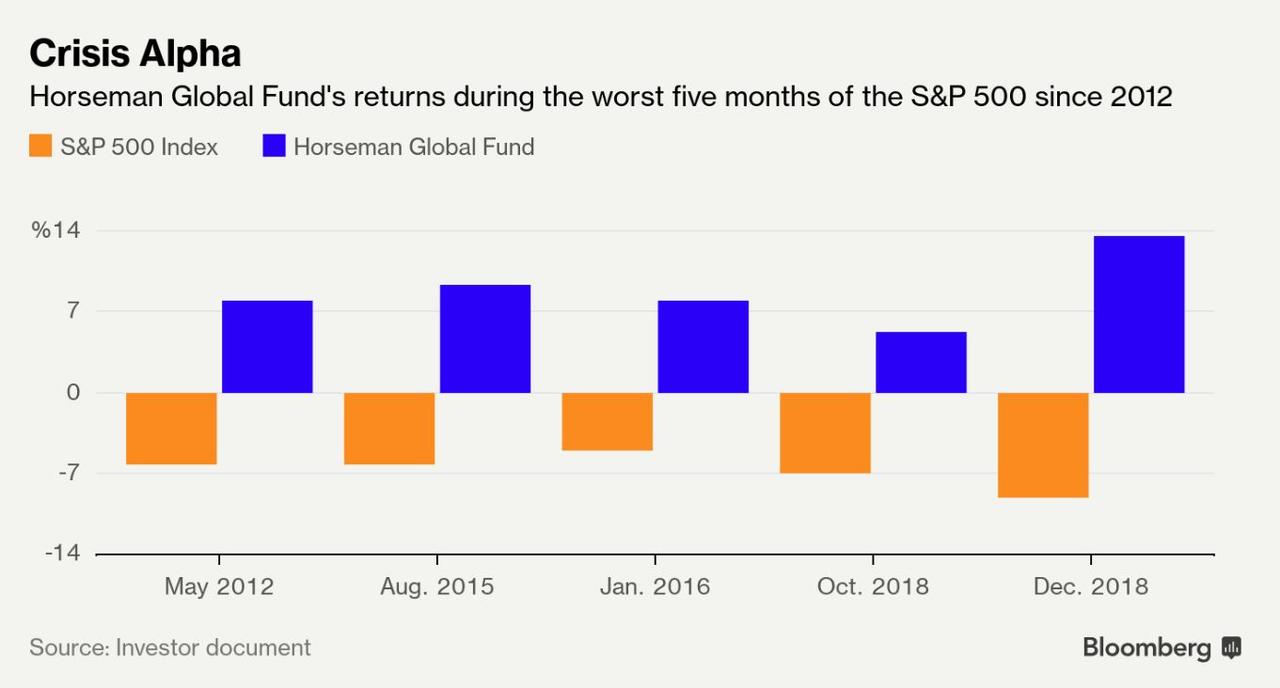

Of course, as Horseman Global’s Russell Clark has proven over and over again, this is not the case at all. A few years back, we anointed Horseman “The world’s most bearish hedge fund” for a very simple reason: Of all existing asset managers, Russell Clark may have the biggest and longest net short position in history. Just look at the chart below, which shows not only that Clark’s net exposure was a remarkable $-78.6% (after -88.14% in March), with a gross short position of 102%, but that he had been effectively net short since 2011.

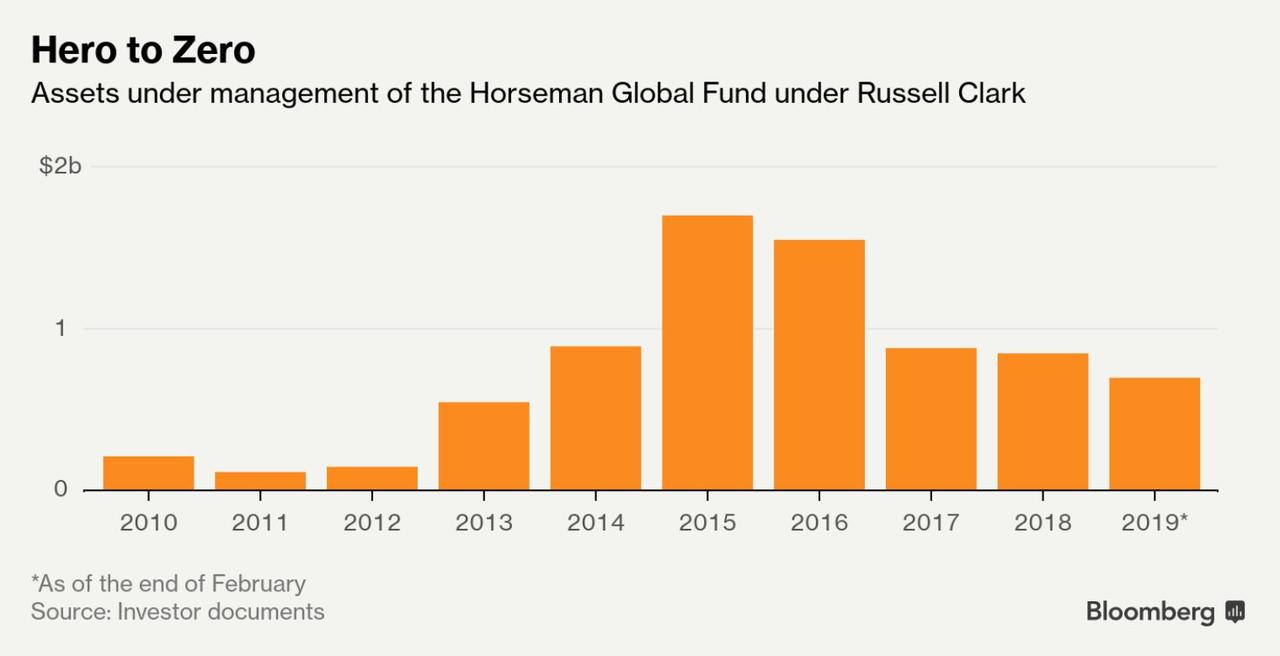

Yet, to assume that Clark has either thrown in the bearish towel, or somehow lost his shirt over the past ten years would be a mistake. Actually, his fund outperformed the S&P 500 for the period between 2012 – when he first went net short – until the end of 2018, only underperforming in 2016. In 2014, Clark posted double-digit returns when oil prices cratered (he was short). In 2013, he made money shorting Brazilian equities. He started with just $111 million when he took over the fund in January 2011, but AUM peaked at $1.5 billion in 2015.

However, the fund’s inconsistent performance (it’s not unusual for Horseman to be up or down 5% in a single month) has alienated some investors who are uncomfortable with the volatility, even as Horseman has bested most other hedge funds in terms of performance, as one former investor told Bloomberg.

Tim Ng, chief investment officer of Princeton, N.J.-based Clearbrook Global Advisors LLC, says his fund pulled its money for similar reasons. “The stretches of negative performance and the high volatility of monthly returns became a consistent drag on our portfolio’s overall return, which prompted us to redeem,” he says.

But after a bruising Q1, when Clark got crushed by the torrid rally in US equities, more LPs have pulled out, and AUM has shrunk to just $713 million.

And unfortunately for Clark, as we wrote last month, after a dismal Q1, the fund’s losses more than doubled in April, when the it was down a staggering 12%, which brought its total loss YTD to more than 25%.

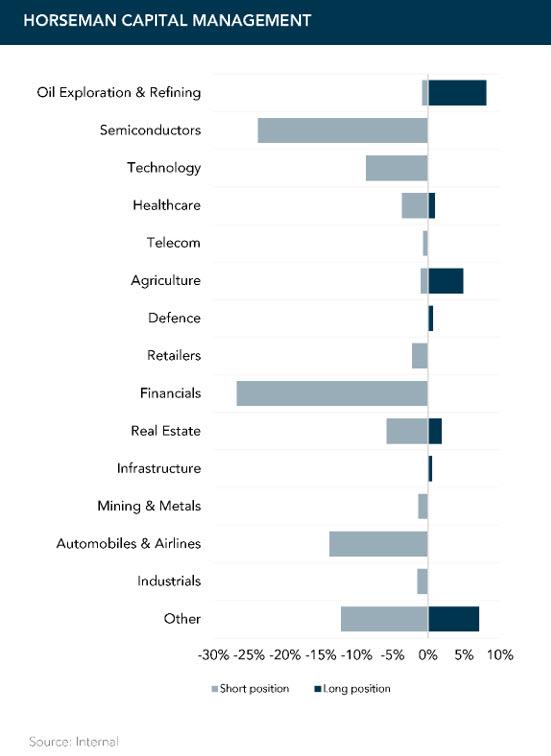

However, as we further noted for the fund which was massively short semiconductors, salvation was just days away, as after the disastrous April plunge in the fund’s P&L, the best possible news for Clark was that after a relentless ramp higher, none other than Donald Trump came to Horseman’s rescue, with the recent return of US-China trade – and the most violent escalation in global tech war – which sent semi stocks tumbling in May…

… and suggesting that much if not all of the April losses would be reversed, leading to our conclusion that “Horseman will have a far better YTD performance after May.”

That’s precisely what happened, because as Clark wrote in his latest letter to investors, the fund staged a remarkable rebound in May, returning a whopping 17.13%, which was its best return since October 2011, and its second best month in history.

It is no surprise then that Clark begins his latest letter in an almost euphoric fashion, and after the near-self doubt expressed in some of his other more recent letters, he starts off with a bang, to wit: “I must say, I love the hedge fund business. I am reminded of the scene in Trading Places when Winthrop takes Valentine to the commodity trading floor, and says “This is it. The last pure bastion of pure capitalism left on earth”. These days, with equities, bonds and currencies kept well within central bank control, sometimes there seems to be no pure capitalism left.”

However, in the hedge fund space, Darwinian capitalism still rules supreme. Make money or get out. Be the best or go home. And I love it.

The problem, as Clark’s mother used to tell him, “Only the mediocre are always at their best”. And here the abovementioned self-doubt comes creeping back: “the last three years I have not been at my best. In part for the central bank interference, but also because there are many crosswinds have been blowing. From the bottom of the fund in the last cycle in 2011 through to the top of the fund in early 2016, the prevailing winds were so easy to read. Falling commodity prices, underperforming emerging markets and strong bonds. As long as you did not stray from these area, it was hard to go wrong.”

Things got especially difficult in 2016, when “there was a bunch of mixed messages. This means investors have tended to focus on the future. Stocks that have growth (tech) or are guaranteed to exist in the future (real estate, staples and utilities) have prevailed in portfolios. This has led into a widely commented on feature of the market, the outperformance of growth and quality versus value.”

But then, the Horseman CIO adds, “the strangest thing happened at the end of April” when “the market gods decided that it was time for some clarity (or as much clarity as you ever can get from markets).” Market gods… or Trump who in early May rekindled the trade war with China, but that’s irrelevant for now, and instead in response to what was the clarity Clark refers to, he says that “China is likely headed for a recession and some sort of devaluation. The market indicators of this are fairly dear, with Chinese Yuan proxies such as Australian dollars, Korean Won and Taiwan Dollar all depreciating recently.”

Why does that mean China is going to devalue? Well Australia, Korea and Taiwan all have better trade balances, current accounts and fiscal positions than the US, and with expectations of US rate cuts rising, they should have appreciated. Australian dollar in particular is hard to understand given the huge rally in iron ore, except in the context of fears of Chinese devaluation. Recent moves in Hibor relative to Libor underscore this fear.

As a result, with the changes he made to the portfolio at the end of April, which we discussed previously here, “which reflected these changes in market, and all of them immediately made money.”

From long bonds, to a greatly reduced long book, to additions to the short book.

Even more exciting to Horseman is that when he looks at the long standing autocallable theme in the fund, “a China devaluation would likely cause many of the main markets that have suppressed volatility to fall dramatically, namely Kospi 200, HSCEI, Nikkei 225 and the Euro Stoxx 50.”

Clark’s conclusion: “So clarity has returned. And just as Winthrop tells Valentine, it’s time to “buy low, sell high. Fear – that’s the other guy’s problem”. Your fund is long bonds, short equities.”

Alas, Clark’s euphoria won’t last long, because after a solid – for bears – May, June saw the strongest S&P performance in 84 years…. and the pain for the world’s most bearish hedge fund as confirmed by its latest exposure…

… will be nothing short of historic, with its performance in June likely to be another double digit return, only this time in the negative direction.

* * *

One final point: Clark’s assiduously dedicated contrarianism has earned him a cult following among professional investors. Though his name isn’t as widely known as an Ackman or a Loeb, his interview with RealVision was one of the company’s most requested videos from 2018, largely thanks to his reputation built up on these pages over the past 5 years as the “world’s most bearish hedge fund”, yet one which stubbornly refuses to throw in the towel.

Despite a wave of redemptions in 2016, 2017 and 2018, Clark, who keeps the bulk of his own wealth in Horseman, has retained an unflappable confidence in his investing view: “When people hate you and write terrible things about you, it tends to be the best time to invest.“

via ZeroHedge News https://ift.tt/2J76gm0 Tyler Durden

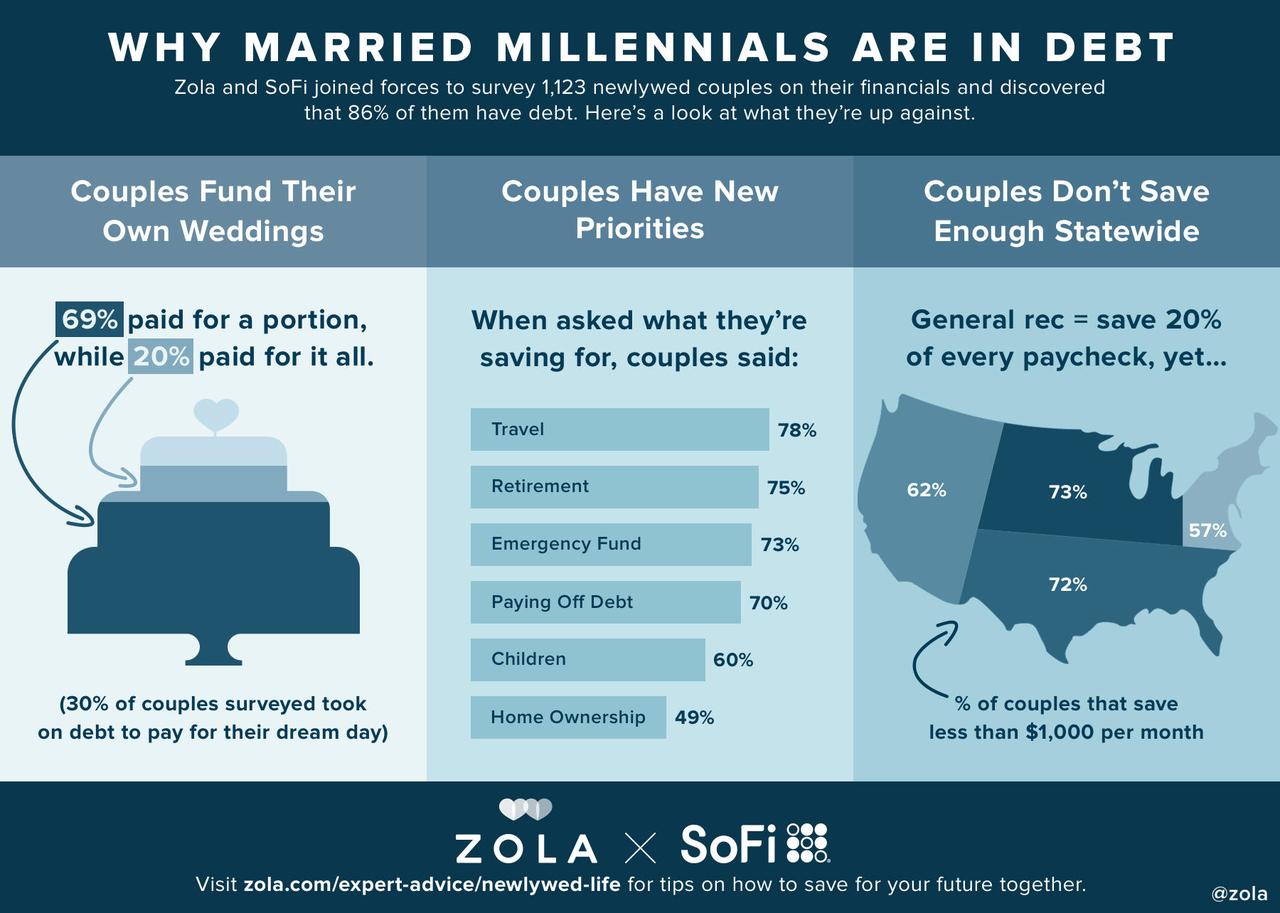

Millennials, already the most indebted generation of all time, are now flocking to high-interest loans to tie the knot, reported the Washington Post.

Demand for wedding loans has quadrupled in the past year, said David Green, chief product officer at Earnest, a San Francisco-based online lender, noting that couples spend approximately $16,000 on wedding loans and pay it off in three years. Interest rates range from 7% to 18%, is seen as a cheaper alternative to credit cards.

“People are carrying more debt, they want to get married but don’t have the funds to do so,” Green said.

The explosive popularity of these loans, experts say, has been in the last three years, shows how the bride’s parents aren’t picking up the tab anymore, but more of a collective effort by parents, grandparents, and even the bride and groom.

“Couples are getting married later, so they are more willing to pay,” said David Wood, president of the Association of Bridal Consultants. “At the same time, their parents are older, they may be on a retirement income and not have the means to pay for the wedding either.”

President Trump and the Federal Reserve are aboustely clueless in how they measure inflation. Considering the average cost of a wedding is skyrocketing, according to financial advisers. This comes as student loan debt hits $1.5 trillion and millennials have absolutely no savings.

“What’s driving this growth? Weddings are getting more expensive and people are waiting longer to get married,” said Todd Nelson, director of strategic partnerships for LightStream, a lending division of SunTrust bank. “It used to be, generally speaking, the father of the bride was on the hook for paying for the wedding. That’s not necessarily the expectation anymore.”

Personal finance experts said they’ve noticed more and more millennial clients who are taking out loans to fund their big day. Experts have told their clients that they don’t need an expensive Instagram-worthy wedding.

“The problem is, you don’t want to rely on a personal loan for something that isn’t necessary — and there is nothing necessary about an expensive wedding,” said Stefanie O’Connell, a personal finance expert and author of “The Broke and Beautiful Life.” “Everything about weddings is discretionary, aside from what you pay the county clerk.”

O’Connell, who is getting married later this year will not use loans but rather cash to pay for her big day, said she also helps clients understand that they need to look past their wedding day and see the big picture if a sustainable life without insurmountable debts.

“You have to put it in context,” she said. “You could spend $30,000 on a one-day celebration, or you could use it to put a down payment on a house. These loans sound great when you’re planning your wedding, but afterward, I hear a lot of regret.”

Brad Pritchett and David Chadd expected to pay for their wedding in cash, but a month before their wedding in February, they realized they went over budget.

“Quite frankly, we both have a taste level where we weren’t willing to compromise,” said Pritchett, 38, vice president of marketing for the American Heart Association. “It was important for us to have a great party to celebrate our love.”

So having a great, Instagram-worthy, one-day celebration, or otherwise called a wedding in 2019, is now being funded by high-interest loans that are putting millennials into further debt – thus their long term financial survivability will be in question in the next downturn.

via ZeroHedge News https://ift.tt/2FGqlPn Tyler Durden

As if we aren’t being tracked, recorded, and monitored enough, the Pentagon now has a laser that can identify a person by their heartbeat. Your heartbeat is going to be a lot harder to hide than your face…

As MIT Technology Reviewreports, the Pentagon has developed a laser that can identify people from a distance by their heartbeat alone. The technology, known as Jetson, uses laser vibrometry to identify surface movement on the skin caused by a heartbeat, and it works from 200 meters away.

Everyone’s cardiac signature is unique, and unlike faces and fingerprints, it can’t be altered in any way. As with facial recognition and other biometrics which rely on optimal conditions, though, Jetson does have a few challenges. It works through regular clothing such as a shirt, but not thicker garments, such as a winter coat. It also takes about 30 seconds to collect the necessary information, so right now it only works if the target is sitting or standing still. And, of course, its efficiency would also depend on some kind of cardiac database. Nonetheless, under the right conditions, Jetson has over 95 percent accuracy. –Engadget.

This would mean the Pentagon’s goal is to create a cardiac database of everyone’s heartbeat in order to monitor, track, and surveil all of us. Orwell’s future looks better than what we’re going to be experiencing. Official documents from the Combating Terrorism Technical Support Office (CTTSO) suggest this has been in the works for some time. However, it could have other applications as well.

Proponents say that this could help doctors wirelessly monitor patients, and it may very well be sold to the public as such using propaganda. However, if history is any indication, this will be used as a tool of mass surveillance just like our smartphones are now.

Move over facial recognition! The government is going to soon track us by our cardiac signatures!

via ZeroHedge News https://ift.tt/2Nnqa1D Tyler Durden

Yesterday, Federal District Judge Haywood Gilliam of the Northern District of California issued two rulings against President Trump’s effort to reallocate military funds to build his proposed border wall. The decisions conclude that Trump lacked the authority to transfer those funds without additional authorization by Congress. The rulings address lawsuits against the border wall brought by the Sierra Club and other groups, and by the states of California and New Mexico, respectively.

These decisions come as no surprise because they largely build on the reasoning of Judge Gilliam’s earlier decision to issue a preliminary injunction against the use of these funds for wall-building projects in areas of the border covered by the lawsuit in question. I analyzed it here. The principal differences are that the new rulings establish permanent injunctions against the use of the funds, not just a temporary injunction, and that they apply to wall-building in several more parts of the border area than the earlier injunction covered. Judge Gilliam explains that this is because there is now a more extensive record on what the federal government proposes to do in these additional areas.

I agree with Judge Gilliam’s analysis of the main issues in these cases, and explained the reasons why in my post on his earlier ruling (which has much more detail on the legal issues). The administration’s attempted diversion is a threat to separation of powers and would set a dangerous precedent if upheld by the courts. Conservatives who may cheer Trump’s efforts now won’t be so happy when the next Democratic president uses similar shenanigans to reallocate funds to projects favored by the political left.

As I also noted in that post, these decisions are just the start of what will almost certainly be a prolonged legal battle over Trump’s wall-building plans. The government is already appealing Judge Gilliam’s earlier ruling, and there are also numerous other pending lawsuits related to the wall.

Judge Gilliam is the first federal judge to address (some of) the substantive issues at stake in the wall litigation. But, earlier this month, another federal trial court dismissed a wall lawsuit filed by the Democratic-controlled House of Representatives because the judge concluded the House lacked standing to file the claim. I criticized that ruling (which is also likely to be appealed) here.

Even if the standing decision stands up on appeal, it is unlikely to prevent judicial review of Trump’s wall-building plan, because there are many other lawsuits against it brought by parties who clearly do have standing, even if the House does not. The real import of the standing decision is its potential impact on other separation-of-powers disputes between the president and Congress.

To briefly sum up, Judge Gilliam’s decisions represent a notable victory for critics of Trump’s wall-building plan. But this is just the beginning of what is likely to be a lengthy legal battle. Stay tuned!

from Latest – Reason.com https://ift.tt/2ZVaP9R

via IFTTT

A federal judge appointed by former President Barack Obama after contributing heavily to his campaigns has blocked the Trump administration from reallocating $2.5 billion to construct border barriers, according to the Daily Caller.

US District Judge Haywood Gilliam expanded on a May 24 order, forbidding the Trump administration from breaking ground on specific border wall projects in California, Texas, Arizona and New Mexico. He also turned his previous order into a permanent injunction, according to the Caller‘s Kevin Daley.

After declaring a national emergency at the southern border, the administration announced it would reprogram $600 million from the Treasury Department’s forfeiture fund, $2.5 billion from Defense Department counter-narcotics activities, and $3.6 billion from military construction projects to finance construction of the wall. The $2.5 billion for counter-drug efforts were at issue in Friday’s case.

The plaintiff in Friday’s case is the Sierra Club, an environmentalist group that claims “recreational and aesthetic interests” in habitats near the border, like “hiking, birdwatching, photography and other professional, scientific, recreational, and aesthetic uses.” A border wall will inevitably restrict their access to those habitats, the plaintiffs say, thereby diminishing their quality of life. They also fear heightened racial tensions and environmental damage. –Daily Caller

“Congress considered all of defendants’ proffered needs for border barrier construction, weighed the public interest in such construction against defendants’ request for taxpayer money, and struck what it considered to be the proper balance — in the public’s interest — by making available only $1.375 billion in funding, which was for certain border barrier construction not at issue here,” reads Gilliam’s order.

As the Epoch Times noted last month, “U.S. District Court Judge Haywood Gilliam Jr. was confirmed in 2014 after being nominated by Obama and receiving a recommendation by Sen. Dianne Feinstein (D-Calif.).”

Gilliam also donated tens of thousands of dollars towards electing and reelecting Obama.

According to federal election records, Gilliam donated $6,900 to Obama’s campaign for president—$4,600 to Obama for America and $2,300 to the Obama Victory Fund.

Gilliam donated additional funds to Obama’s re-election campaign, sending $13,500 to Obama for America and Obama Victory Fund 2012. He also donated $4,500 to the Democratic National Committee. From 2012 to November 2014, he sent $3,100 to the Covington and Burling LLP PAC. –Epoch Times

“Congress was clear in denying funds for Trump’s xenophobic obsession with a wasteful, harmful wall” said ACLU staff attorney Dror Ladin, who argued the case. “This decision upholds the basic principle that the president has no power to spend taxpayer money without Congress’ approval. We will continue to defend this core principle of our democracy, which the courts have recognized for centuries.”

Gilliam denied the Trump administration’s request to stay his ruling pending appeal to the 9th US Circuit Court of Appeals.

via ZeroHedge News https://ift.tt/2Ym1AiK Tyler Durden

Yesterday, Federal District Judge Haywood Gilliam of the Northern District of California issued two rulings against President Trump’s effort to reallocate military funds to build his proposed border wall. The decisions conclude that Trump lacked the authority to transfer those funds without additional authorization by Congress. The rulings address lawsuits against the border wall brought by the Sierra Club and other groups, and by the states of California and New Mexico, respectively.

These decisions come as no surprise because they largely build on the reasoning of Judge Gilliam’s earlier decision to issue a preliminary injunction against the use of these funds for wall-building projects in areas of the border covered by the lawsuit in question. I analyzed it here. The principal differences are that the new rulings establish permanent injunctions against the use of the funds, not just a temporary injunction, and that they apply to wall-building in several more parts of the border area than the earlier injunction covered. Judge Gilliam explains that this is because there is now a more extensive record on what the federal government proposes to do in these additional areas.

I agree with Judge Gilliam’s analysis of the main issues in these cases, and explained the reasons why in my post on his earlier ruling (which has much more detail on the legal issues). The administration’s attempted diversion is a threat to separation of powers and would set a dangerous precedent if upheld by the courts. Conservatives who may cheer Trump’s efforts now won’t be so happy when the next Democratic president uses similar shenanigans to reallocate funds to projects favored by the political left.

As I also noted in that post, these decisions are just the start of what will almost certainly be a prolonged legal battle over Trump’s wall-building plans. The government is already appealing Judge Gilliam’s earlier ruling, and there are also numerous other pending lawsuits related to the wall.

Judge Gilliam is the first federal judge to address (some of) the substantive issues at stake in the wall litigation. But, earlier this month, another federal trial court dismissed a wall lawsuit filed by the Democratic-controlled House of Representatives because the judge concluded the House lacked standing to file the claim. I criticized that ruling (which is also likely to be appealed) here.

Even if the standing decision stands up on appeal, it is unlikely to prevent judicial review of Trump’s wall-building plan, because there are many other lawsuits against it brought by parties who clearly do have standing, even if the House does not. The real import of the standing decision is its potential impact on other separation-of-powers disputes between the president and Congress.

To briefly sum up, Judge Gilliam’s decisions represent a notable victory for critics of Trump’s wall-building plan. But this is just the beginning of what is likely to be a lengthy legal battle. Stay tuned!

from Latest – Reason.com https://ift.tt/2ZVaP9R

via IFTTT