Many top Democrats now favor decriminalizing “illegal entry.” During the second night of the second round of Democratic Party 2020 debates, former Vice President Joe Biden was asked to answer for immigration policy under former President Barack Obama.

Moderator Don Lemon asked, “Vice President Biden, in the first two years of the Obama administration, nearly 800,000 immigrants were deported, far more than during President Trump’s first two years. Would the higher deportation rates resume if you were president?”

Biden said “absolutely not” to that. But he also disagreed with many of his rivals about decriminalizing undocumented border crossings. “The fact of the matter is that, in fact, when people cross the border illegally, it is illegal to do it unless they’re seeking asylum,” said Biden. “People should have to get in line.”

Democrats overall have come a long way from Obama’s immigration policy since he left office. Both this round of debates and the first featured questions about whether unauthorized border crossings should be criminalized. And both times, former Housing Secretary Julián Castro has called for the repeal of Section 1325 of the Immigration Nationality Act. Last night, Castro also chastised Biden for not having “learned the lessons of the past.”

Section 1325 is what makes entering the U.S. without permission a federal crime, rather than merely a civil infraction. As immigration reporter Dara Lind explained after the first 2020 debate,

Castro wants to get rid of it—so that being an unauthorized immigrant in the US would still be a civil offense but no longer a federal crime.

And he’s pushing the rest of the Democratic field to join him.

In that first debate in June, only Beto O’Rouke opposed the repeal of Section 1325 among that night’s debaters. “In a Democratic primary that has shown the party has shifted leftward on several issues since the Obama administration, this exchange was still remarkable,” Lind commented. “In fiscal year 2016, immigration offenses—illegal entry and reentry chief among them—made up a majority of federal criminal prosecutions.” (Emphasis mine.)

Last night, several candidates agreed with Castro, several candidates were unclear, and Biden and Michael Bennett emphatically disagreed. Here are the most relevant portions of their statements:

Joe Biden: “If you cross the border illegally, you should be able to be sent back. It’s a crime.”

Michael Bennett: “I disagree that we should decriminalize our border.”

Cory Booker: “An unlawful crossing is an unlawful crossing, if you do it in the civil courts or if you do in the criminal courts. But the criminal courts is what is giving Donald Trump the ability to truly violate the human rights of people coming to our country….Doing it through the civil courts means that you won’t need these awful detention facilities that I have been to.”

Julian Castro: “The only way that we’re going to guarantee that these kinds of family separations don’t happen in the future is that we need to repeal this law. There’s still going to be consequences if somebody crosses the border. It’s a civil action. Also, we have 654 miles of fencing. We have thousands of personnel at the border. We have planes; we have boats; we have helicopters; we have security cameras….What we need are politicians that actually…have some guts on this issue.”

Bill de Blasio: “Why are we even discussing on one level whether it’s a civil penalty or a criminal penalty, when it’s an American reality? And what we need is comprehensive immigration [reform], once and for all, to fix it.”

Tulsi Gabbard: “We will have to stop separating children from their parents, make it so that it’s easier for people to seek asylum in this country, make sure that we are securing our borders and making it so that people are able to use our legal immigration system by reforming those laws.”

Kirsten Gillibrand: “I don’t think we should have a law on the books that can be so misused. It should be a civil violation and we should make sure that we treat people humanely.”

Kamala Harris: [At border detention facilities] “I saw children lined up single file based on gender being walked into barracks. The policies of this administration have been facilitated by laws on the books…that allow them to be incarcerated as though they’ve committed crimes. These children have not committed crimes…and should be not treated like criminals.”

Jay Inslee: “We have to make America what it’s always been, a place of refuge. We got to boost the number of people we accept. I’m proud of being the first governor saying, ‘Send us your Syrian refugees.'”

Andrew Yang: “We can’t always be focusing on some of the distressed stories. And if you go to a factory here in Michigan, you will not find wall-to-wall immigrants; you will find wall-to-wall robots and machines. Immigrants are being scapegoated for issues they have nothing to do with in our economy.”

Kirsten Gillibrand tried to have her Biden-attack moment during Wednesday night’s debate, criticizing the former vice president’s record on women’s issues. Biden looked baffled, saying she had always championed his work with women and been part of his efforts in the past. Indeed, in old tweets, Gillibrand praised Biden for things like his “unwavering commitment to combating violence against women.”

Bill de Blasio took his closing speech time last night as an opportunity to promote taxthehell.com, a site that announces de Blasio’s plan to “tax the hell out of the super rich.”

Columbus, Ohio, police “brought departmental charges on Wednesday against five officers who were involved in the arrest of Stormy Daniels at a strip club last year.”

from Latest – Reason.com https://ift.tt/2Kg6TdM

via IFTTT

Blain’s Morning Porridge, submitted by Bill Blain of Shard Capital

With one hand the Fed giveth, a 25 bp basis point cut, but on the other it taketh – Powell’s “mid-cycle adjustment” left markets confused.

Where is the easing to negative-infinity they’d been promised? The yield curve inverted (spawning a host of headlines about how the bond market again predicts a recession), the dollar strengthened (well, of course it would), and stocks did nothing till they stumbled and fell a bit – a toddler screaming that “insuring against downside risks” should mean a promise of another cut, stunned when Powell said “it’s not the beginning of a long series of rate cuts.”

Thus occurred the most pointless rate cut in Fed history – easing rates in a “healthy” economy pretty much at full employment with a “favourable” outlook, where the only real problem is massively inflated financial asset bubbles. The effect will be to juice already distorted financial assets higher. Marvellous (US readers – sarcasm alert).

Two Fed Voting governors dissented – give them medals.

Trump tweeted: “As usual, Powell let us down.” Helpful. Donald wants a “lengthy and aggressive rate cut cycle which will keep pace with China, The European Union and other countries…” Predictable.

Blain’s Brexit Watch

As Boris plans to pour billions into No-Deal Preparations, the Irish accuse him of Bullying tactics, and Labour gets ready to offer a second referendum as their response, it’s all get terribly exciting. (It also deeply depressing – just writing this makes me wonder if I am suffering PTSD?) The feelgood Boris engendered just a week ago is already wearing thin. All the bluff and bluster needs balanced by something tangible. As yet, we aren’t seeing it. This is leading to lots of questions – does Boris need to engage with Brussels and go visit.

The Answer from Downing Street will be no. Dominic Cummings will insist. Let others respond to the challenge of an agreement that Boris has laid down. No Engagement. Europe will come to us. (Seriously?)

The result is going to be further uncertainty, confustion and opportunities for Project Fear Remoaners to snipe and moan.

Pundits now see the likelihood of a No-Deal at 30% and rising, with Sterling heading lower to $1.15.

Hold onto your seats boys and girls. This is going to get rough before we land.

via ZeroHedge News https://ift.tt/336gts2 Tyler Durden

As if to underscore the latter notion, Sanford’s name was included in a national presidential poll for the first time in a July 23–28 McLaughlin & Associates survey released Wednesday. The results were grim for the South Carolinian—just 4 percent of 415 likely voters preferred Sanford, compared to 81 percent for Trump. The only candidate with worse polling day yesterday was former Massachusetts governor and 2016 Libertarian Party vice presidential nominee Bill Weld, who limped home with 2 percent.

Sanford said he will make a decision about whether to run over the next two weeks, but it’s hard to imagine the math getting any better. Trump’s approval rating among Republicans has been between 87 percent and 91 percent all year, and it’s been resting comfortably at 90 percent since mid-June. That 81 percent is the highest he has scored in the monthly McLaughlin poll since it began last year. He is outfundraising Weld by a ratio of 150 to 1, and he has rigged the Republican National Committee to an extent that would make Hillary Clinton jealous.

The former Freedom Caucus congressman, who was bounced as an incumbent in a primary last year by an opponent Trump backed at the last minute (who in turn got beaten by a Democrat), has maintained that the central premise of his candidacy is to foreground discussions of debt and deficits at a time when Republicans in power no longer want to hear about the subject. “Fiscal conservatism may be on life support,” he told Real Clear Politicsthis week, “but I don’t believe the patient is dead.”

Fiscal sobriety is also a core Bill Weld concern, and it’s earned him consistent 75-percentage-point deficits in national polls. Gary Johnson made debt/deficits his number-one issue running for Senate in his home state of New Mexico, and it got him just 15.4 percent of the vote, half as much as his unknown Republican opponent. The GOP is the party of trillion-dollar deficits, and fiscal hawks who remain in office are rapidly becoming an endangered species.

“We’re the only party that cares about [debt],” Libertarian Party National Committee Chair Nicholas Sarwark told me at Freedom Fest last month. “Do you want to bankrupt your children and grandchildren or not? With issues like this, where neither of the two old party nominees are going to even address the issue, we can unite the country…around the idea of fixing problems and dealing with the issues that Americans have that have been ignored for too long.”

Asked to explain why Weld is getting thumped running on that issue, Sarwark quipped, “He picked the wrong team.” Asked whether Sanford is making the same mistake, Sarwark said, “Probably.” But then Sarwark argued that having libertarian-leaners compete for the GOP nomination is a good thing.

“I wish Bill Weld all the success in the world for the Republican primary,” he said. “I think the vehicle can’t be saved, but he’s doing what he can to save something that he knew. I think that that’s noble. I think that to the extent that he can hurt a bad president, I think that’s noble. It’s a good fight, but it’s not our fight….

“The work that Bill Weld is doing is a good step for some people, because if he’s speaking libertarian language to Republican primary voters, and he doesn’t win that primary, those people are going to have to go somewhere; they’re not going to go for the president. They’re either going to go for whoever the Democratic nominee is, or they’re going to go for the Libertarian nominee. And that creates opportunities for us.”

It remains to be seen whether those opportunities will be leveraged by a high-profile contender such as Rep. Justin Amash (I–Mich.), by one of the lower-profile candidates who have already declared, or by some as-yet-undeclared pretender to the third-party throne (maybe even Mark Sanford!). Whoever it is, he or she will be swimming against currents much less favorable than in 2016.

from Latest – Reason.com https://ift.tt/2LUIZYl

via IFTTT

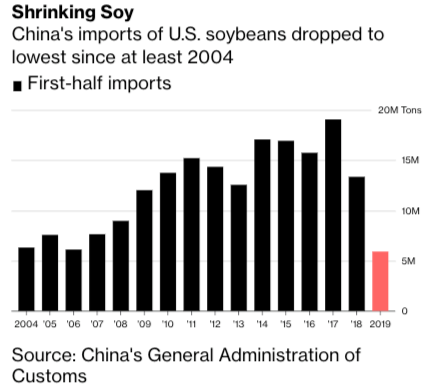

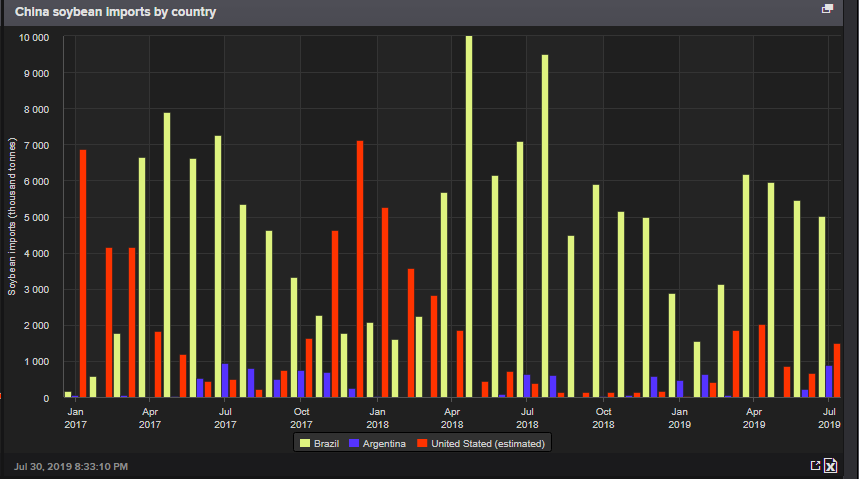

A new report from Bloomberg shows US soybean exports to China collapsed in 1H19 to the lowest level in more than a decade.

The US exported 614,806 tons of soybeans to China in June, according to US customs data. That brought 1H19 China imports of soybeans from the US to 5.9 million tons, the lowest level since 2004, according to Bloomberg calculations.

US farmers, who harvest soybeans from September to November, have been some of the hardest hit in the trade war as Chinese buyers shift to Latin American markets for agricultural products.

Senior US officials met in China on Wednesday with the hopes of resolving trade disputes that could result in more agriculture trade between the two countries.

But the US trade delegation broke off discussions with its Chinese counterparts on early Wednesday morning and is already on its way back to Washington, a sign that no new progress was made, and that China is not likely to buy significant amounts of US agriculture products this summer.

According to Bloomberg, US delegates including Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer wrapped up talks with Vice Premier Liu He and their other Chinese counterparts on Wednesday afternoon at the Xijiao State Guest Hotel in Shanghai, according to a pool report.

The latest round of talks took place against a jarring backdrop following a fresh outburst by Trump on Twitter, who, as delegates gathered Tuesday, slammed China’s unwillingness to buy American agricultural products and said it continues to “rip off” the US.

…to ripoff the USA, even bigger and better than ever before. The problem with them waiting, however, is that if & when I win, the deal that they get will be much tougher than what we are negotiating now…or no deal at all. We have all the cards, our past leaders never got it!

What’s worse, the talks were supposed to focus on “goodwill” gestures, like the agricultural purchases promised by China, and the rollback of sanctions on Huawei promised by Trump. This could be devastating for US farmers as China is going to continue sourcing soybeans from Latin America, not the US, in 2H19.

Since the start of the trade war, most of China’s soybeans have come from Brazil. Last year, the bulk of the country’s 80 million ton export went to China, replacing market share that was once controlled by US farmers.

The Global Times on Wednesday morning said if Washington still holds the illusion that Beijing will somehow cave in and compromise on issues concerning sovereignty, “then no deal is fine.”

The Trump administration prepared for a no-deal week with the unveiling of a $16 billion farm bailout several weeks ago, that is expected to greatly benefit the wealthiest of US farmers while not providing adequate financial support for smaller ones.

With the election coming up, there’s a high probability since the trade talks collapsed Wednesday that China could abandon US agriculture markets for Brazil, Argentina, and Paraguay, which could certainly lead to increased financial hardships for President Trump’s base, the American farmer, located across the Midwest US.

via ZeroHedge News https://ift.tt/317hK0n Tyler Durden

As if to underscore the latter notion, Sanford’s name was included in a national presidential poll for the first time in a July 23–28 McLaughlin & Associates survey released Wednesday. The results were grim for the South Carolinian—just 4 percent of 415 likely voters preferred Sanford, compared to 81 percent for Trump. The only candidate with worse polling day yesterday was former Massachusetts governor and 2016 Libertarian Party vice presidential nominee Bill Weld, who limped home with 2 percent.

Sanford said he will make a decision about whether to run over the next two weeks, but it’s hard to imagine the math getting any better. Trump’s approval rating among Republicans has been between 87 percent and 91 percent all year, and it’s been resting comfortably at 90 percent since mid-June. That 81 percent is the highest he has scored in the monthly McLaughlin poll since it began last year. He is outfundraising Weld by a ratio of 150 to 1, and he has rigged the Republican National Committee to an extent that would make Hillary Clinton jealous.

The former Freedom Caucus congressman, who was bounced as an incumbent in a primary last year by an opponent Trump backed at the last minute (who in turn got beaten by a Democrat), has maintained that the central premise of his candidacy is to foreground discussions of debt and deficits at a time when Republicans in power no longer want to hear about the subject. “Fiscal conservatism may be on life support,” he told Real Clear Politicsthis week, “but I don’t believe the patient is dead.”

Fiscal sobriety is also a core Bill Weld concern, and it’s earned him consistent 75-percentage-point deficits in national polls. Gary Johnson made debt/deficits his number-one issue running for Senate in his home state of New Mexico, and it got him just 15.4 percent of the vote, half as much as his unknown Republican opponent. The GOP is the party of trillion-dollar deficits, and fiscal hawks who remain in office are rapidly becoming an endangered species.

“We’re the only party that cares about [debt],” Libertarian Party National Committee Chair Nicholas Sarwark told me at Freedom Fest last month. “Do you want to bankrupt your children and grandchildren or not? With issues like this, where neither of the two old party nominees are going to even address the issue, we can unite the country…around the idea of fixing problems and dealing with the issues that Americans have that have been ignored for too long.”

Asked to explain why Weld is getting thumped running on that issue, Sarwark quipped, “He picked the wrong team.” Asked whether Sanford is making the same mistake, Sarwark said, “Probably.” But then Sarwark argued that having libertarian-leaners compete for the GOP nomination is a good thing.

“I wish Bill Weld all the success in the world for the Republican primary,” he said. “I think the vehicle can’t be saved, but he’s doing what he can to save something that he knew. I think that that’s noble. I think that to the extent that he can hurt a bad president, I think that’s noble. It’s a good fight, but it’s not our fight….

“The work that Bill Weld is doing is a good step for some people, because if he’s speaking libertarian language to Republican primary voters, and he doesn’t win that primary, those people are going to have to go somewhere; they’re not going to go for the president. They’re either going to go for whoever the Democratic nominee is, or they’re going to go for the Libertarian nominee. And that creates opportunities for us.”

It remains to be seen whether those opportunities will be leveraged by a high-profile contender such as Rep. Justin Amash (I–Mich.), by one of the lower-profile candidates who have already declared, or by some as-yet-undeclared pretender to the third-party throne (maybe even Mark Sanford!). Whoever it is, he or she will be swimming against currents much less favorable than in 2016.

from Latest – Reason.com https://ift.tt/2LUIZYl

via IFTTT

The phrase “mid-cycle adjustment” sent shudders through risk markets yesterday, during Powell’s press conference. Mid cycle! When corporate debt to GDP is at extremes, earnings growth slowing, and the US manufacturing sector close to contraction, this really does not look mid-cycle to us.

By delivering a 25bp insurance cut, the Fed actually tightened financial conditions for Main Street US, making subsequent easing more likely. The march higher of the USD is the main problem the Fed has to deal with. This has pushed our estimate of the neutral nominal Fed Funds rate much lower this year to under 1.4% and, with yesterday’s move, it could well fall further.

The Fed had many opportunities to reduce market expectations for an easing cycle, but did not take them. In so doing they have repeated the December 2018 hike error, wasting ammunition, and long term US rates will rightly continue to fall from here. For the first time under Trump’s leadership, we see value in long end Treasuries here, as a Fed policy-error trade (for example as a 2s30s flattener).

2s10s seems likely to invert in the near term, as the market digests the implications of a Fed which cut rates while simultaneously tightening financial conditions. Such a poor delivery of a cut puts the Fed closer to the zero lower bound, and therefore a liquidity trap. Inflation expectations should continue to fall in the US, and we would expect US corporate spreads and equities to see more selling flows.

Our conclusion is that the market will be proven correct- to prolong the cycle as the Fed is seeking, the Fed will need to ease further, by around 75bp from here just to reach neutral. Until then, expect long end Treasuries to be well bid, particularly as long-end carry just became a bit more favorable.

via ZeroHedge News https://ift.tt/2KeKEF0 Tyler Durden

MSNBC Host Joe Scarborough of MSNBC’s ‘Morning Joe’ complained in a tweet last night that the Democratic contenders onstage last night for Pt. 2 of the second Democratic debate spent more time attacking President Barack Obama’s policies than they spent attacking President Donald Trump.

He added that this is “politically stupid and crazy.”

These candidates are attacking Barack Obama’s policy positions more than Donald Trump. That is politically stupid and crazy.

Though Scarborough also inadvertently admitted something important: The Democratic Party of today isn’t the same party from 2016. Instead, even candidates who once believed themselves to be part of the mainstream have embraced policies that are much further to the left, largely thanks to the influence of “the Squad” and their fellow progressives, who have been gaining influence in Washington since the mid-terms.

Scarborough is probably also referring to the fact that Biden and Harris, the two front runners who participated in Wednesday night’s debate, were lightning rods for criticism. Bill de Blasio and others got into a huge debate with Biden over health-care reform, even prompting Biden to declare these criticisms of Obamacare “malarky”.

Biden was also attacked over the 800,000 deportations that occurred during the Obama Administration, which seemed to support the Trump Administration’s argument that Trump’s supposedly “draconian” border policies are merely a continuation of the Obama years.

While the “you’re playing into Republicans’ hands!” argument is certainly compelling to some, they should probably tell Scarborough not to say the quiet part out loud.

via ZeroHedge News https://ift.tt/2YAAUhs Tyler Durden

The Federal Reserve cut interest rates for the first time in over a decade Wednesday. And Jerome Powell left the door open for future cuts.

Peter Schiff broke it all down on his most recent podcast, saying this is the first interest rate cut on the short road to zero.

During his press conference after the FOMC meeting, Fed Chairman Jerome Power tried to straddle the fence. In the process, he ended up mixing his messages.

Powell called the 25 basis point cut a “mid-cycle adjustment.” When asked about future cuts, the Fed chair left that door propped open, saying “As the committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion.”

About midway through the Q&A session, Powell said the Fed wasn’t embarking on a long rate-cutting cycle like it would during a recession. But then he backtracked and sounded a little more dovish later on.

Let me be clear: what I said was it’s not the beginning of a long series of rate cuts. I didn’t say it’s just one or anything like that. When you think about rate-cutting cycles, they go on for a long time and the committee’s not seeing that.”

Of course, when the Fed pivoted to the “Powell Pause” last December, most analysts weren’t expecting a rate cut down the road. And here we are.

Peter Schiff predicted all of this. During his podcast, Peter called this the first step on the road to zero. And he said it was going to be a pretty short road.

Powell claimed the Fed was cutting rates as an insurance policy to ensure problems in the global economy don’t spill over into a healthy US economy. Peter called this a load of BS.

Either he is lying, or he’s a complete idiot. And I tend to believe its the former. And the reason he is lying is because if he told the truth, he would scare the sh** out of the markets.”

Peter reiterated something he’s been saying all along — a 25-basis point cut isn’t going to cut it. To underscore this point, he noted that the Dow fell over 300 points after the announcement. But Peter said Powell was right when he said this wasn’t the beginning of a long easing cycle. That’s because it won’t take long to get to zero.

It doesn’t have a lot of ammunition to cut rates, and so I think we’ll get to zero relatively quickly. And we’ll stay there until the Fed completely loses control of this thing.”

Keep in mind the last two times the Fed started cutting rates a recession quickly followed.

Peter said he thinks the stock market will continue to trend downward until the Fed significantly softens the position that it took yesterday.

He reiterated that it’s clear Powell is lying about this just being a temporary measure in a good economy.

The fact that there was so much contradictory statements made by Powell during this conference, I mean, it’s obvious that he’s lying, he’s making up excuses because he’s trying to pretend the economy is great, but he’s cutting rates anyway. So, he’s trying to defend, really, a ridiculous story. He contradicts himself. If you’re being honest, it’s easy not to contradict yourself because you just tell the truth. But when you’re lying, you weave a very tangled web. One lie contradicts another lie because you can’t keep your story straight. And that is the position he was in.”

Listen to the whole podcast for more analysis on the Fed’s latest move and what may lie ahead.

via ZeroHedge News https://ift.tt/2YgPdIJ Tyler Durden

World stocks and US index futures rebounded, even as the dollar charged to its highest in more than two years on Thursday after the Federal Reserve spoiled hopes of a run of U.S. interest rate cuts when Fed Chair Powell shocked when he said that the rate cut is a “mid-cycle adjustment” indicating it’s not the start of an extended series of cuts.

After the rate cut on Wednesday, Powell said in a press conference that the Fed’s quarter-point reduction amounted to a “mid-term policy adjustment.” Two Fed officials dissented to the decision, favoring no change. President Donald Trump said in a tweet “Powell let us down” with the size of the move.

While there was already a blizzard of global data and events going on, it was Fed Chair Jerome Powell’s remarks on Wednesday that set the markets running – literally – with the hour that contained Powell’s press conference seeing trading volumes explode to the highest level of the year; this is when Powell said the first U.S. rate cut in over a decade was “not the beginning of a long series of rate cuts” and the market tumbled.

Analyst hot takes on the Fed’s decision came hot and heavy: “That’s what a hawkish cut looks like,’’ Morgan Stanley analysts including Ellen Zentner wrote in a note to clients. “The minimal size of the cut, the dissents, and Powell’s press conference disappointed markets, and undercut our expectation.”

“We believe the Fed is trying to thread the needle, balancing market jitters about slowing global growth with robust consumer spending and a strong job market in the U.S.,” said Nick Maroutsos, co-head of global bonds at Janus Henderson. In other words, by cutting just 25 bps, the Fed is trying to bolster market confidence while also keeping some dry powder in reserve in case of an economic shock.”

But it was the dollar’s reaction said it all: the DXY index surged to the highest in more than two years, euro/dollar dropped below $1.11 for the first time since May 2017, and Brexit-hobbled sterling hit 30-month lows just above $1.21. The Bloomberg dollar index jumped to the highest since 2018 as all bank clients who had been following short dollar trade recos were carted out feet first.

Ten-year Treasuries had rallied on Wednesday after the cut and when policy makers brought forward their plan to abandon the run-down in the bond portfolio.

“Markets interpreted the Fed’s communication as slightly hawkish and therefore further rate cuts in the immediate future were somewhat priced out,” said David Milleker, senior economic advisor at Union Investment. “And the dollar strengthened. All in all, the Fed did not achieve what it presumably wanted.” However, perhaps sensing that they had overreacted, world stocks rebounded modestly overnight as futures for all three main U.S. stock gauges nudged higher.

In Europe, the Stoxx Europe 600 Index rose 0.4% following a weak start, with financial services shares leading the rebound and banks also rising after upbeat results from the likes of Societe Generale and Barclays. Other top-performing European sectors included retail and telecom, while British American Tobacco, the top contributor in terms of index points, also extended its gain on better-than-expected earnings.

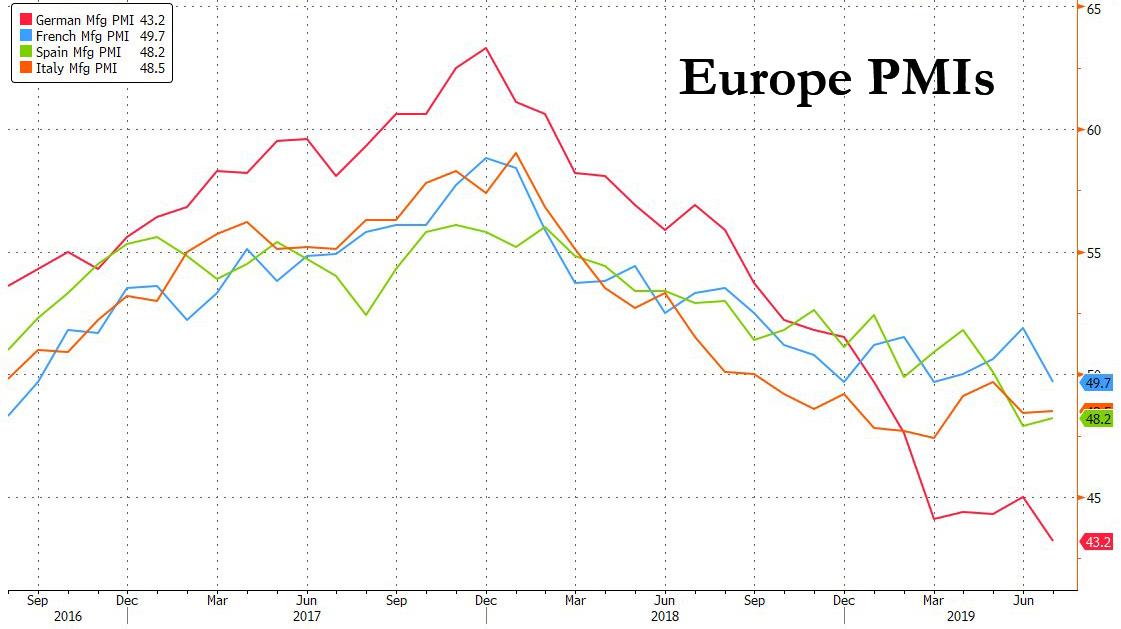

Most Asian equity gauges dropped earlier, though Japan’s benchmark recouped early losses as the yen slid. European bullishness was reinforced by disappointing European data, which saw the French manufacturing PMI slide back into contraction, while German Mfg PMI tumbled to a fresh multi-year low.

Europe reversed earlier losses in Asia where the MSCI index of Asian shares ex-Japan fell 0.8%, extending losses for a fifth day to the lowest since mid-June and posting its biggest one-day percentage drop in a month. The S&P BSE Sensex Index fell the most in the region, headed for its lowest level in five months on Thursday after completing its worst July in 17 years. Australian shares declined 0.4%. Losses by Chinese shares ended down 0.8%. Taiwan shares extended their losing streak to a fifth day as China imposed a ban on travel to the island. Japan stocks rebounded from early losses, helped by strong earnings at the country’s largest financial firms and a weakening in the yen. The nation’s banks and brokerages surged after Nomura and Mitsubishi UFJ reported large increases in quarterly profit.

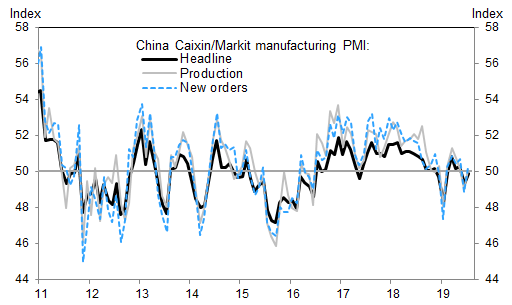

Downbeat data and factory surveys on Thursday had also pointed to further weakness for Asia’s trade-reliant economies. South Korea’s exports fell for an eighth straight month in July amid weak global demand and a dispute with Japan. New export orders shrank the most in about six years. South Korea, the world’s sixth-largest exporter, is the first major industrial economy to release trade data each month, providing an early assessment on the health of global demand. Pressure on Chinese factories eased slightly, but manufacturing activity continued to shrink according to the Caixin PMI which printed in contraction if modestly better than expected.

Specifically, China’s Caixin manufacturing PMI came in at 49.9 in July, above market expectations and also higher than June’s reading. The production sub-index increased by 1.1pp to 50.1, and the new orders sub-index went up to 50.2 from 48.8. Inventory indicators suggest a destocking trend — the raw material inventories sub-index was 0.4pp lower at 49.8, and the finished goods inventory index fell 0.7pp to 48.5. Employment growth deteriorated further — the employment sub-index was 0.3pp lower at 48.7, the lowest reading since February 2019.

“The broader global trade dynamic remains a challenge,” Morgan Stanley strategist Michael Zezas said. “Trade should continue to drag on corporate confidence, capex and global growth in the near term.”

U.S. Treasuries were sold off as investors scaled back their pre-Fed expectations for at least 100 basis points of cuts in the near term. Yields on 10-year notes climbed as high as 2.058% in Europe from a U.S. close of 2.007%, before recovering some of the losses. Core euro zone bond yields were rising, too, although -0.428% German Bund levels were still extraordinary.

Elsewhere in FX, as noted earlier the pound weakened, dropping below 1.21 and resuming its recent losing streak and staying lower as the Bank of England kept interest rates unchanged. Gilts pared a small gain. “Sterling remains vulnerable to a further escalation in Brexit tensions and we anticipate the market will likely discount higher risks of a ‘no deal’ outcome in the weeks ahead,” said Roger Hallam, currency chief investment officer at J.P. Morgan Asset Management.

Elsewhere, the Aussie dollar slipped below key chart support of $0.6832 to as low as $0.6828, a level not seen since an early January “flash crash”. The kiwi hit a six-week trough of $0.6535 on expectations the Reserve Bank of New Zealand will cut rates next week.

The Chinese yuan weakened to its lowest level in six weeks, slipping below 6.9 against a strengthening greenback. The onshore yuan fell to as low as 6.9150 per dollar on Thursday, the lowest since June 18, before paring the decline. “The Fed was less dovish than expected, so the dollar rebounded strongly across the board and against the yuan,” said Stephen Chiu, FX and rates strategist at Bloomberg Intelligence, adding that the yuan was expected to remain steady against the greenback in the near term while advancing against a basket of trading partners’ currencies. The People’s Bank of China set its daily yuan fix 0.14% weaker than Wednesday, but at a level stronger than 6.9 per dollar, which was considered its line in the sand for the currency. “I think the yuan will hover around the current level for a while, 6.85 to 6.95 for now,” said Tommy Xie, an economist at Oversea-Chinese Banking Corp. in Singapore. The PBOC is not likely to follow the Fed with a cut of its own, he added.

In commodities, U.S. crude futures fell 76 cents to $57.82 per barrel after comments on the rate outlook. Brent was down 71 cents at $64.34. Spot gold also fell, to $1,405.26.

With the Fed out of the way, and with traders now departing for their summer vacations, investors will continue to keep an eye on the ongoing earnings season amid even more abysmal liquidity, as well as Friday’s U.S. jobs data and trade developments. American and Chinese negotiators plan to meet again in early September, after the latest round of talks ended with few signs of concrete progress.

Expected data include jobless claims and PMI readings. Verizon, Veon and U.S. Steel are among companies reporting earnings

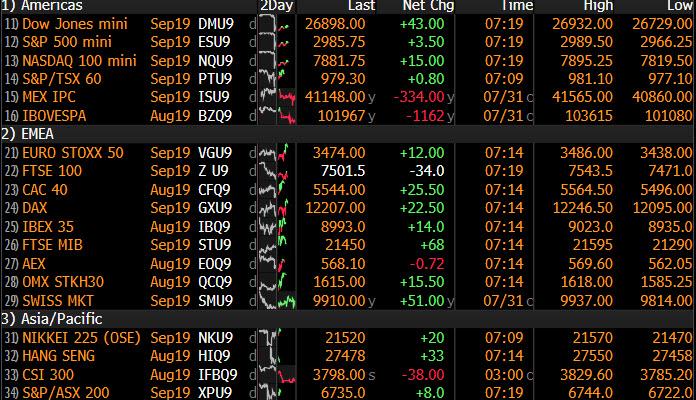

Market Snapshot

S&P 500 futures up little changed at 2,982.75

STOXX Europe 600 up 0.02% to 385.85

MXAP down 0.6% to 157.47

MXAPJ down 0.8% to 514.77

Nikkei up 0.09% to 21,540.99

Topix up 0.1% to 1,567.35

Hang Seng Index down 0.8% to 27,565.70

Shanghai Composite down 0.8% to 2,908.77

Sensex down 1.5% to 36,904.26

Australia S&P/ASX 200 down 0.4% to 6,788.93

Kospi down 0.4% to 2,017.34

German 10Y yield rose 2.1 bps to -0.419%

Euro down 0.3% to $1.1045

Brent Futures down 1.2% to $64.26/bbl

Italian 10Y yield fell 11.8 bps to 1.19%

Spanish 10Y yield rose 3.7 bps to 0.321%

Brent Futures down 1.1% to $64.45/bbl

Gold spot down 0.6% to $1,405.70

U.S. Dollar Index up 0.3% to 98.82

Top Overnight News from Bloomberg

Fed’s Powell hearkened back to the central bank’s 1990’s policy successes by suggesting he can sustain the record long U.S. economic expansion with just a modest reduction in interest rates. He said the cut this week shouldn’t be seen as a signal for extended easing

Manufacturing in the euro area shrank for a sixth month at the start of the third quarter, dragged down by Germany’s worst slump in seven years. The downbeat figures come in the wake of reports showing slower economic growth in France, Spain and the euro area, with Italy stagnating

China’s central bank refrained from immediately following the U.S. Federal Reserve in cutting borrowing costs, signaling its preference to continue with the current targeted easing approach for now.

President Donald Trump said Federal Reserve Chairman Jerome Powell “let us down” by delivering an interest-rate cut that’s not aggressive enough to fight the trade and currency battles his administration is waging

U.S. and Chinese trade negotiators plan to meet again in early September, as the latest round of negotiations ended with few signs of concrete progress. Chinese State media hails ‘transition’ role of Shanghai talks

The Trump administration on Wednesday imposed sanctions against Iranian Foreign Minister Javad Zarif in a provocative move that diminishes the prospects for a diplomatic solution to rising tensions that have brought the U.S. and Tehran to the brink of war

Joe Biden faced an onslaught from across the Democratic debate stage as his opponents sought to cut down the party’s front-runner on health care, immigration, women’s issues and criminal justice

Barclays Plc Chief Executive Officer Jes Staley said the bank cut 3,000 jobs in the second quarter as the firm sought to keep a tight grip on expenses and counter criticism over its ability to reach profitability targets

London Stock Exchange Group Plc agreed to snap up Refinitiv in a $27 billion blockbuster deal, betting on a future dominated by data that will extend its reach beyond Europe

Asian stocks traded lacklustre as the region reacted to the FOMC meeting. ASX 200 (-0.3%) and Nikkei 225 (U/C) were lower with notable weakness seen in gold miners after the precious metal slumped post-FOMC, although downside in Australia’s broader market was limited by resilience in its largest weighted financials sector, while the Japanese benchmark briefly turned positive as it found solace from a weaker currency and amid a heavy slate of earnings. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (-0.8%) conformed to the downbeat picture after the PBoC skipped liquidity operations again and participants digested more PMI data in which Chinese Caixin Manufacturing PMI topped estimates but remained below the 50 benchmark level, while there was also increasing concerns regarding the Chinese military intervening in Hong Kong. Conversely, participants had their first opportunity to react to the more constructive tone struck between US and China in trade talks. Finally, 10yr JGBs were lower and tracked the weakness seen in USTs following the less dovish than expected Fed, with further pressure seen after the 10yr auction results which attracted weaker demand.

Top Asian News

Tax Haven Crackdown Catches Asia Hedge Funds in Its Crosshairs

China Encourages Tencent to Boost Cooperation with SOEs

Iron Ore Falls as Samarco Close to Regaining License

Betting Like SoftBank Drives Toyota’s Value Up by $19 Billion

European stocks have nursed the losses seen at the open [Eurostoxx 50 +0.4%] and are somewhat consolidating following the downside seen post-FOMC. Major bourses are mixed with the FTSE 100 (Unch) faring slightly worse as its oil giant Shell (-4.6%) fell to the foot of the Stoxx 600 as the Co’s profits plunged on lower oil prices. This, coupled with an uninspiring energy complex sees the EU energy sector significantly underperforming, whilst other sectors (ex-materials) are broadly in positive territory. Notable movers today are largely on the back of earnings, with Altice (+23.7%), Capita (+21.0%), SocGen (+4.5%) and Standard Chartered (+4.5%) all bolstered by optimistic numbers. On the flip side, Barclays (-3.2%) is hit on a profit miss, while Siemens (-4.3%) narrowed its EBITA forecast and now sees it at the lower end of the previously guided range. Miners also took a hit from the FOMC-triggered downside in the metals complex. Finally, a special dividend announcement from Rio Tinto (-2.4%) did little to support their share price this morning.

Top European News

European Manufacturing Slump Keeps Economy Under Pressure

U.K. Allocates Extra $2.6 Billion to Prepare for No-Deal Brexit

Polish Central Bank Boss Signals No Response to Inflation Shock

Russia to Grant Some Visas to U.S.-Embassy Backed Moscow School

In FX, the Dollar is broadly firmer in wake of the FOMC and relatively hawkish guidance to accompany the 25 bp ease. The decision to cut rates was not unanimous and Fed Chair Powell stressed that the move was different to previous policy loosening heralding the start of a lengthy cycle by framing the reduction as a mid-cycle adjustment, albeit adding that it is not necessarily a case of ‘one and done’. Nevertheless, the markets were hoping for more and the index rallied to a new 2019 peak at 98.941 before losing momentum ahead of Friday’s NFP that may be pivotal for the rest of the year in terms of policy action.

AUD/NZD/NOK/SEK – Relative outperformers or at least recovering some lost ground, as the Aussie found support near early Feb 2016 lows around 0.6827 vs its US counterpart and has subsequently bounced to 0.6850+, while the Kiwi rebounded from 0.6535 to reclaim 0.6560+ status. Elsewhere, the Scandi Crowns are both benefiting from technical retracements against the Euro and seemingly independent of contrasting manufacturing PMIs given a bad Norwegian miss and sub-50 print vs firmer than forecast Swedish headline that was only partly offset by less upbeat components. Indeed, Eur/Nok is back down below 9.8000 and Eur/Sek under 10.7000.

GBP/EUR/JPY/CAD/CHF – The Pound has also largely shrugged off a better than expected UK manufacturing PMI amidst ongoing and increasing no deal Brexit risk as output hit circa 7 year lows and attention shifts to BoE super Thursday and the prospect of a more dovish/downbeat tone to the MPC minutes, QIR and Governor Carney presser. Indeed, Cable has now lost grip of the 1.2100 handle and Eur/Gbp is eyeing 0.9130 ahead of high noon and the 12.30BST news conference – full preview available via the Research Suite and Headline Feed. Mixed Eurozone manufacturing surveys have not really impacted the single currency either as Eur/Usd hovers towards the base of a 1.1080-33 range, while the Yen has regrouped from 109.30 lows to probe resistance at 109.00 and hefty option expiry interest from the big figure to 109.10 in 2 bn. Elsewhere, the Loonie has handed back all and more of its post-Canadian GDP data gains and is looking at offers said to be stacked between 1.3230-40, with the Franc pivoting 0.9950 and 1.1000 against the Euro.

EM – Amidst pronounced depreciation vs the Greenback, Turkey’s Lira has bucked the trend on further positive follow through from the latest CBRT inflation report and outlook, with Usd/Try remaining south of 5.6000 and hardly reacting to a more contractionary manufacturing PMI. However, the Real may underperform after a bigger than anticipated 50 bp BCB rate cut from a 3.8130 close post-FOMC.

In commodities, the energy complex remains subdued in the after-math of the disappointing FOMC forward guidance issued yesterday. WTI and Brent futures have since traded sideways below 58.00/bbl and 64.50/bbl respectively with little by way of fresh catalysts. Looking at technical levels to the upside, WTI sees the psychological 58/bbl mark ahead of its 200 DMA at 58.09/bbl, meanwhile its Brent counterpart sees clean air (ex-psych levels) between 63.50-65.00/bbl. In terms of geopolitics, US announced sanctions on Iranian Foreign Minister Zarif during the back-end of the US session, albeit the news did little to sway oil prices. Elsewhere, the metal market remains under pressure from the FOMC fallout in which gold plummeted over 20/oz since the release. The yellow metal remains under pressure (albeit above the 1400/oz level) as the Dollar index hovers near YTD highs. Meanwhile, copper remains lacklustre and firmly below the 2.7/lb as the red metal holds onto the Powell-induced losses.

US Event Calendar

8:30am: Initial Jobless Claims, est. 214,000, prior 206,000; Continuing Claims, est. 1.67m, prior 1.68m

9:45am: Bloomberg Consumer Comfort, prior 63.7

9:45am: Markit US Manufacturing PMI, est. 50, prior 50

10am: ISM Manufacturing, est. 52, prior 51.7

10am: Construction Spending MoM, est. 0.3%, prior -0.8%

Wards Total Vehicle Sales, est. 16.9m, prior 17.3m

DB’s Jim Reid concludes the overnight wrap

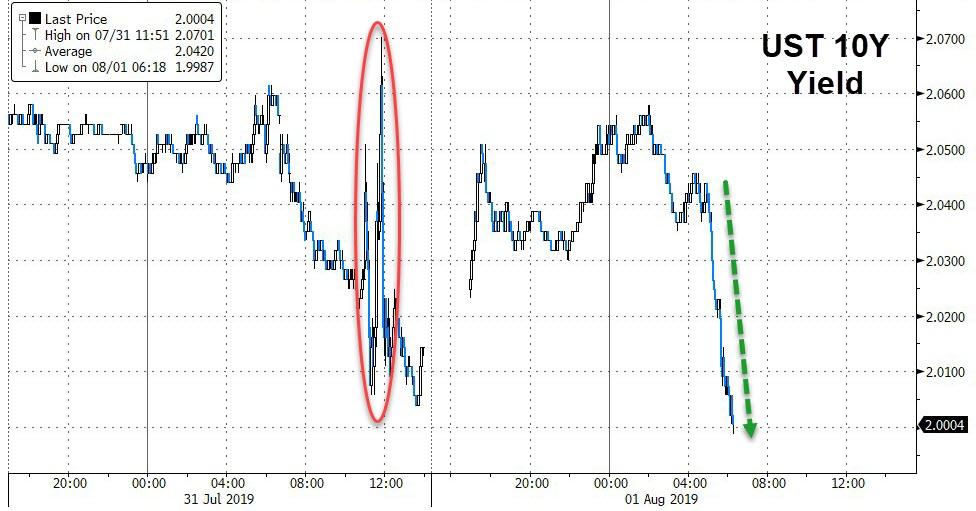

So welcome to August with July ending with a bit of a bang for markets. Indeed yesterday’s Fed meeting was the obvious main event, and it certainly did not disappoint even if Mr Powell did for many. As we discussed yesterday the risk/reward set up isn’t great ahead of this easing cycle and last night showed us how difficult it’s going to be for central banks to keep up with market expectations.

The Fed did cut interest rates by 25bps as broadly expected, albeit with two dissents from regional Fed presidents. Equities fell, the yield curve flattened worryingly and the dollar strengthened. Initially the moves seemed to just be a mechanical reaction to the fact that the interest rate cut was 25bps instead of 50bps, given the market had priced in around a 16% chance for a larger move. However, the adverse moves accelerated during Chair Powell’s press conference after he characterised the move as “a mid-cycle adjustment to policy” and said it was not “the beginning of a lengthy cutting cycle.”

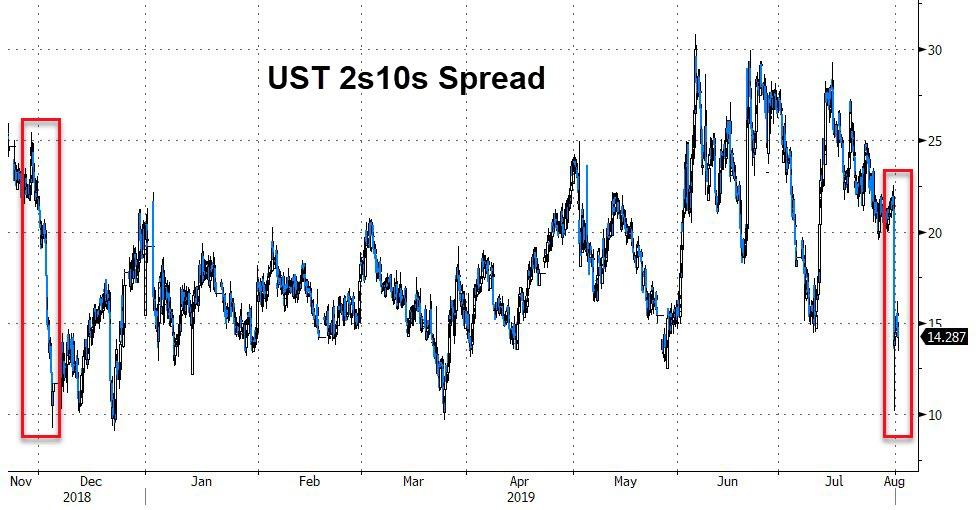

The market certainly interpreted that as a signal of a hawkish cut, possibly with Powell signaling reduced odds for further cuts. The price moves across asset classes certainly seemed to be consistent with higher odds of a policy mistake. At one point during the presser, the S&P 500 and NASDAQ were down as much as -1.83% and -1.98%, respectively, while two-year yields rose as much as +11.5bps (+15bps from just before the announcement), taking the 2y10y yield curve -10.8bps flatter to 10.2bps at one point.

The curve ultimately ended -7.1bps flatter at 13.9bps (14.9bps this morning), the lowest level since May and towards to bottom of the YTD range. Ten-year yields rallied to end -4.7bps lower (but are up +2.1bps this morning), while two-year yields moderated to close +2.2bps higher (are up a further +1.4bps this morning). This flattening was in contrast to the +9.1bps of steepening that occurred after the June Fed meeting, when the FOMC signaled the impending rate cut with the curve hitting a seven month high of around +29bps. As a reminder I place a high degree of weight on the 2s10s curve when trying to work out where in the US cycle we are. With us almost getting back into single digits at one point last night we’re no more than a few bad days away from inverting. This for me is the biggest worry from last night.

In the end, the S&P 500 declined -1.10%, which was the worst day for the index since 31 May. The NASDAQ and DOW ultimately closed -1.19% and -1.23%, respectively, as well. The dollar rallied +0.58% to its strongest level in over two years. President Trump tweeted after markets closed that “Powell let us down” because “what the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle.” There was no immediate reaction to the tweet, but is certainly raises the political heat on the Fed.

Even before that tweet, Powell seemed to be feeling the heat and used his final comments to specifically address and reframe his earlier remarks which had driven the selloff. He clarified that “I didn’t say it’s just one (cut) or anything like that (…) what I said was it’s not a long cutting cycle, in other words, referring to what we do when there’s a recession or a very severe downturn. That’s really what I was ruling out.” So he tried to emphasize that the FOMC does not expect a recession or a downturn, but that they are ready to cut rates more than once as needed. He also referred one reporter to look at history for prior examples of “mid-cycle adjustments,” tacitly signaling that he views the current environment as similar to the 1995 and 1998 episodes, when the Fed cut rates 75bps each time. So a bit of a mixed message with the market a bit confused. However the reality is that it had probably gone over its skis a bit in expectations.

To recap the Fed’s actual policy statement, which came with two dissents from Kansas City’s George and Boston’s Rosengren, the only major additions were a reference to “global developments” and a new comment saying that the Committee will “contemplate the future path of the target range for the federal funds rate.” The statement still said that they “will act as appropriate to sustain the expansion.” The Fed also opted to end its balance sheet runoff effective today, rather than the end of September as originally planned, though this move will have only a marginal impact on markets.

Before the Fed decision, a pretty bad MNI Chicago PMI for July did help to justify the Fed’s decision to cut. The index fell to 44.4 (vs. 51.0 expected), the lowest reading since December 2015. Before that, every single one of the 68 instances of a Chicago PMI at or below the 44.4 level over the last 50 years has been associated with a recession. The index was this low in mid-1967 without prompting a recession, however. On an ISM-adjusted basis, the index fell -4.5pts to 47.5, and the details were broadly weak as well. The production and employment components were both the weakest since 2009 at 41.4 and 42.9, respectively. The print presents downside risks to today’s ISM manufacturing report, as well as tomorrow’s jobs report.

With the ongoing uncertainty over global trade being a major factor behind yesterday’s rate cut, it’s worth noting that the latest round of trade talks between the US and China finished yesterday. A White House statement following the talks described the meetings as “constructive”, and said that the discussions included “forced technology transfer, intellectual property rights, services, non-tariff barriers, and agriculture.” Regarding future talks, it said they “expect negotiations on an enforceable trade deal to continue in Washington, D.C., in early September,” though staff-level discussions will continue in August. So this won’t get resolved soon but at this stage it’s a positive that they’ve agreed to meet again. In the meantime we are obviously susceptible to a Trump tweet on the matter.

Again on the theme of the lower interest rate world, it was interesting that the FT reported yesterday that UBS have decided to pass on negative interest rates to its wealthy clients as banks start to appreciate that low or negative rates are not going to be the temporary phenomenon they had previously thought. In itself, it might not be a big deal but it may mark the start of a period where banks try to pass on more of the cost of central bank’s policies. What depositors do on this will be interesting. To exaggerate, if I have 100 units with a bank and I’m going to see this erode in value now I can either hoard cash (after recent building works I won’t need a big mattress), buy assets (risky), spend more as why bother to save (a bit extreme), or accept a steady reduction in my wealth, be grumpy and maybe save more to compensate. I haven’t got my head around which theme will dominate if this practise become more widespread.

Overnight in Asia markets are following Wall Street’s lead with the exception of Japan which is making modest gains (after paring early losses) on a weaker Japanese yen (-0.39% this morning). Other than that, the Hang Seng (-0.68%), Shanghai Comp (-0.78%) and Kospi (-0.18%) are all down. Elsewhere, futures on the S&P 500 are up a marginal +0.04%. The US dollar has continued to strengthen with the index being up +0.33% this morning after advancing +0.48% yesterday. In terms of overnight data releases, China’s Caixin manufacturing PMI surprised on the upside at 49.9 (vs. 49.5 expected). The accompanying statement suggested that new export orders stayed in contractionary territory but saw a rise while components of output and new orders returned to expansion. A slightly better message than yesterday’s official PMIs. Elsewhere Japan’s final July manufacturing PMI came in two-tenths lower than the initial read at 49.4 (vs. 49.3 last month).

In other overnight news, Bloomberg has reported that the Bank of Korea Governor Lee Ju-yeol considers “Japan’s recent export restrictions against South Korea are a big risk,” while adding that Japan may decide as early as this week to take South Korea off the “white list” of nations it deems to be safe buyers of sensitive materials. If Japan goes ahead with the move then it is likely to affect South Korea’s automobile, steel, aviation and electronics industries. The foreign ministers of both nations are meeting today in Bangkok after the US urged them to calm rising trade tensions that are threatening global supply lines. Meanwhile, here in the UK, the government has doubled spending to £4.2bn on no-deal Brexit preparations this financial year while bringing the total cash allocated to £6.3bn. For this, the Chancellor of the Exchequer Sajid Javid has set aside £2.1 bn of new cash including an immediate £1.1bn pounds to improve key border and customs infrastructure and ensure access to critical medical supplies. The remainder will be made available to government departments if needed.

Ahead of the Fed, the main story in European markets yesterday were the new record lows for sovereign bond yields. 10-year bunds fell -4.0bps to an all-time closing low of -0.440%, and now comfortably below the ECB’s deposit rate of -40bps. It was the same direction for French 10-year debt, down -4.3bps to close at -0.184%. And perhaps most eye watering of all, Swiss 10-year yields fell -3.0bps to close at -0.805%. Even 30-year Swiss debt now trades at a yield of -0.186bps and the longest bond, maturing in 2064, now yields -0.081%. Equities were mixed, with the STOXX 600 up +0.17%, with the DAX (+0.34%), CAC 40 (+0.14%) and the FTSE MIB (+0.56%) all making gains before the FOMC. Once again the FTSE 100 was the outlier, falling -0.78%, as it traded inversely to a rallying sterling.

The moves in Europe came as GDP figures confirmed the ongoing slowdown in the Eurozone economy, with Q2 growth of +0.2% (as expected), down from +0.4% in Q1. The decline in Q2 growth brings the yoy growth rate to +1.1%, the lowest since Q4 2013. Separately, inflation readings showed Eurozone CPI fell to +1.1% in July, the lowest since February 2018, while core inflation fell to +0.9% (vs. +1.0% expected). In terms of the country details we got yesterday, growth in Spain was at +0.5% (vs. +0.6% expected), which was the slowest quarterly growth there since Q2 2014. Italy saw growth come in above expectations however, with a flat 0.0% reading in Q2 (vs. -0.1% contraction expected), and unemployment in the country fell to 9.7%, the lowest since January 2012. Nevertheless, Italian inflation data showed HICP at +0.4% in July (vs. +0.5% expected), the lowest since November 2016. In spite of the lower than expected inflation readings, Euro five-year forward five-year inflation swaps ended the session up +2.5bps.

Continuing the big week for central banks, having already heard from the BoJ and the Fed, the Bank of England’s MPC will be making their latest policy decision today, and we’ll also have the release of the Bank’s quarterly inflation report and a press conference from Governor Carney. In their preview last Friday (link here ) our UK economists wrote that although they expect the MPC will vote to keep Bank Rate on hold, they think that they will drop their tightening bias, “with the MPC becoming more sensitive to a deteriorating economic outlook vis-à-vis the ongoing trade wars and an increasing risk of a no deal Brexit.” Since the MPC’s last meeting of course, sterling has weakened noticeably, although yesterday it was the best-performing G10 currency versus the dollar, trading flat despite broad strength for the greenback.

Wrapping up, in terms of other data yesterday in the US, the ADP Employment Change said that 156k jobs had been added in July (vs. 150k expected), while June’s reading was revised up by +10k. Although better than expected, this brought the 3-month moving average down to its lowest level since 2010. Elsewhere, the employment cost index for Q2 was +0.6% (vs. 0.7% expected).

Looking to the day ahead, the Bank of England will be announcing its latest monetary policy decision, with Governor Carney giving a press conference afterwards. In terms of data, the manufacturing PMIs will be the highlights, with Italy, France, Germany, the Eurozone and the UK all reporting this morning, before the US in the afternoon. From the US, there’ll also be the July ISM manufacturing data as well as June construction spending. Earnings releases today include Royal Dutch Shell, Barclays, Verizon Communications, General Motors, Rio Tinto and Siemens, and in the UK, there’s a parliamentary by-election taking place which will have implications for the new PM with his majority at risk of dropping to two.

via ZeroHedge News https://ift.tt/2ZmLyWt Tyler Durden