Biden Considers New ‘Wall Street’ Tax To Match Warren, Bernie

With Elizabeth Warren surpassing him in a national poll for the first time, Joe Biden is finally acquiescing to the pressure from his party’s increasingly left-wing voters and exploring more ‘progressive’ tax policies, including a ‘wealth tax’ like the plans proposed by both Warren and Bernie Sanders, and a ‘financial transaction’ tax on Wall Street that would increase the costs of stock, bond and derivative trades, the Washington Post reports.

Currently alone among the three highest polling polling Democrats, Biden is finding that his more centrist policies aren’t stirring up much excitement among his voters.

Meanwhile, Sanders released a wealth-tax plan earlier this week that imposes such high rates on billionaires that it virtually guarantees that their wealth will eventually be siphoned off by the IRS. The Democratic Socialist has also released a plan to make college free by taxing stock, bond and derivative trades. Biden has endorsed similar plans in the past, and according to WaPo, a financial transaction tax might end up being a major part of his new tax policy.

Of course, as we’ve pointed out in the past, slapping a tax on stock and bond trades would not only hurt Wall Street trading desks, it would probably cause liquidity to dry up, ensuring that even the smallest drop in stocks would be magnified by the total collapse in liquidity, and result in a crash that wipes out trillions in value. We once joked that this seems less like a plan to make college free, and more like a plan to reset the system.

WaPo reports that a Biden aide confirmed that the campaign is working on a new tax policy proposal, but that he couldn’t say anything about what specific proposals are in the mix. Biden has said that he will soon introduce new tax policies designed to show how he will pay for expanding government.

Biden “has and will continue to put forward details regarding how he will finance his biggest plans, because the stakes are too high not to be straightforward with the American people about how much they will cost and who will pay for them,” said Andrew Bates, a campaign spokesman.

Toward the end of the Obama years, Biden had expressed interest in a financial transaction tax after advisors showed the Vice President how much money could be raised by taxing Wall Street. But Biden coming out in favor of such a plan would mark a major departure from the Democrats’ typical platform.

“To have a leading presidential candidate, who is considered a moderate, take a position so counter to Wall Street – that would be a big step, no question about it,” said Frank Clemente, executive director of Americans for Tax Fairness, a liberal group focused on tax equity. “The vast majority of revenue it generates is from the wealthiest Americans, who have the most amount of money to contribute.”

Biden’s tax proposals already call for corporate taxes to be raised from 21% to 28% (the Trump tax law cut it down from 35%) as well as increasing the rate paid by the richest taxpayers. And his agenda, from health care to climate change to criminal justice, has been criticized by conservatives as even further left than Hillary Clinton’s in 2016.

But if Biden does move his tax policies sharply to the left, how much longer will it be before he embraces “Medicare For All.”

Oil Erases All Saudi-Attack Gains After Iran Sanctions Report

Already helped by reports of apartial Saudi cease-fire with Yemen, oil prices have legged lower – erasing all the price gains since the Saudi-attack – on the back on a Reuters report saying that US offered to remove all Iranian sanctions in exchange for talks.

That’s not going to help the value of the Aramco IPO.

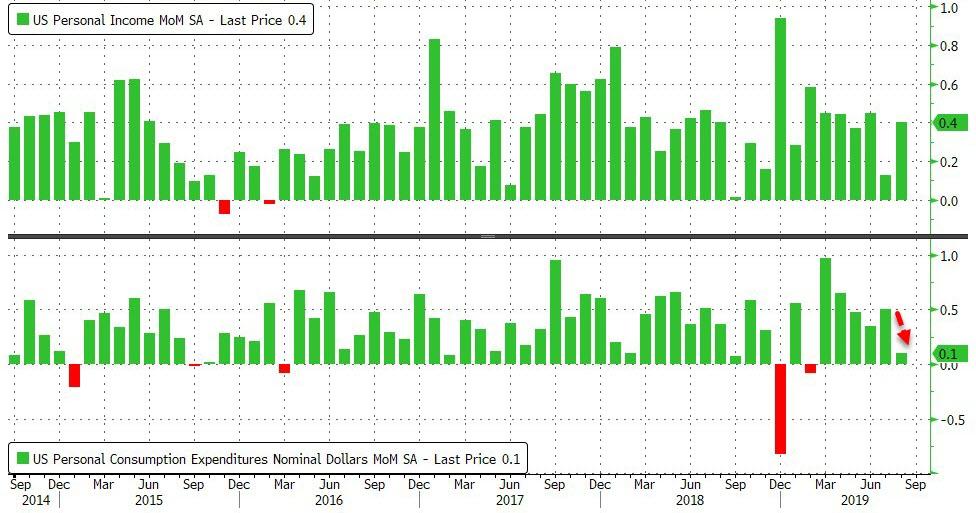

US Spending Growth Weakest In Six Months, Core Capex Tumbles

Americans’ personal income and spending growth in August was expected to reverse some of the moves seen in July (income slowed, spending accelerated) and it did with incomes up 0.4% MoM (as expected) accelerating over July’s 0.1% rise, but spending growth was only 0.1% (well below July’s and expectations).

This is the weakest MoM gain in six months…

Source: Bloomberg

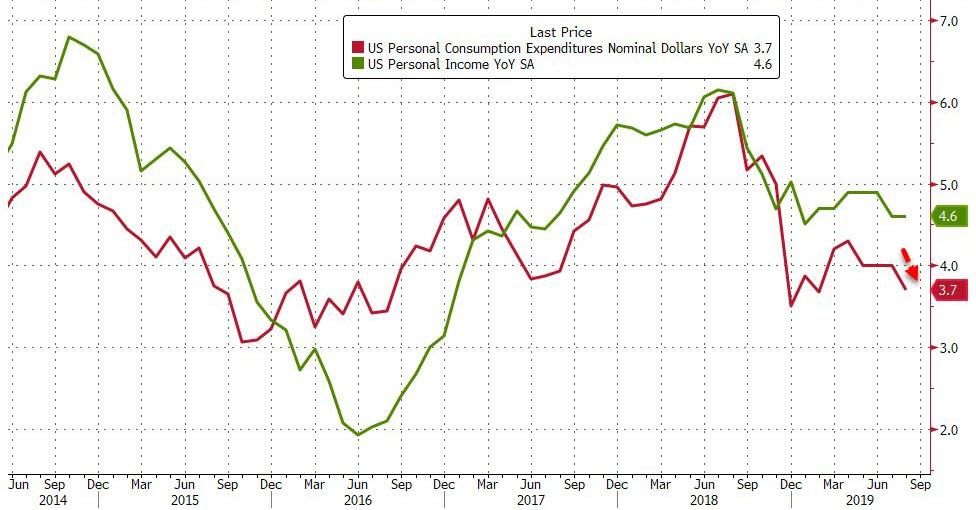

Which sparked a slowdown in income and spending growth year-over-year (weakest annual gains in spending in six months)…

Source: Bloomberg

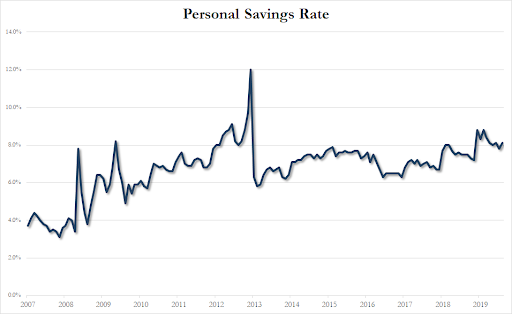

Which prompted a rise in the savings rate (to highest since March 2019)

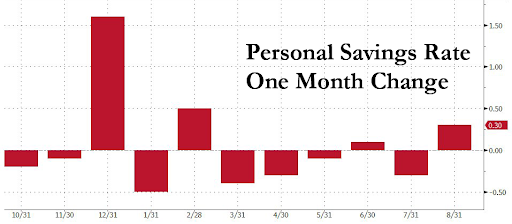

This is the biggest MoM jump in the savings rate since Feb 2019…

The Fed’s favorite inflation indicator accelerated but remains well below the 2.00% mandate…

Source: Bloomberg

A separate Commerce Department report showed bookings for non-military capital goods excluding aircraft — a proxy for business investment — fell 0.2%, the weakest performance in four months, compared with forecasts for no change; and the biggest annual contraction in core capex since Nov 2016

Source: Bloomberg

The data suggest growth continued to cool in the third quarter, adding focus to next week’s September jobs report to show whether the labor-market slowdown is deepening.

Liquidity Shortage Eases: Fed Accepts Only $49BN In Final, Underscubscribed Term Repo

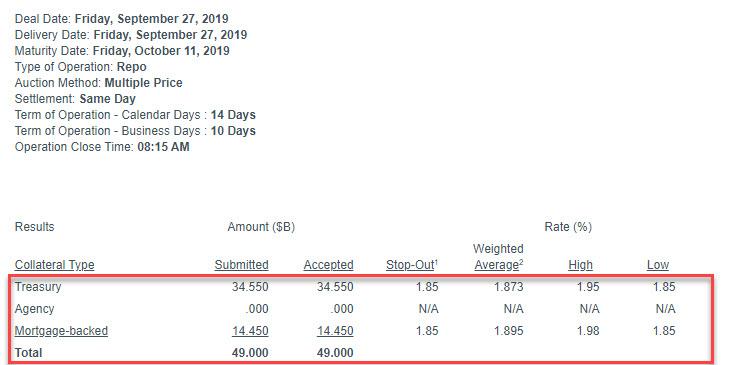

One day after the Fed concluded its 2nd upsized, $60BN term repo on Thursday and which was notably oversubscribed – which sparked fresh concerns about dealer funding needs heading into quarter end – moments ago the Fed released the results of the final, third term repo which indicated that while funding tensions remain, they appear to have eased as the Fed accepted “only” $49 billion in the undersubscribed operation, which accepted all $34.55BN in Treasuries and $14.450BN in MBS that were tendered.

Why is this good news? Because some had feared that the third repo would also be oversubscribed, hinting that some dealers would not be able to find all the liquidity they need into quarter end. That, however, did not happen and instead as of this moment, all dealers who were concerned about their quarter-end funding needs should have the appropriate liquidity needed.

Now the only question is what the results for today’s overnight repo operation will show. If funding stress is indeed easing this too should be well below the full $100BN allotment.

Every time we walk past lumber racks in a home-improvement store my wife or daughters start giggling about all the “fine pieces of wood.”

It’s an inside joke that goes back to my first rental property in a small Mojave Desert town. I bought it “as is” in an online auction (although I saw it in person first), and remember the horrified look on the faces of my family when I took them to see it. Think of the term “uneasy silence.”

Half of the roof had blown off from vicious desert winds. The house had broken windows, broken everything, trash strewn everywhere. It looked like something out of the movie “Road Warrior,” given that it sat amid tumbleweeds, sand and cactus. Anyway, I lovingly fixed it up on a shoestring budget. When it was done, I popped for a pricey but fine piece of wood to create the mantelpiece. I was proud of it—and still get teased.

This is not the newspaper version of “Fixer Upper,” but a look at rent control. Gov. Gavin Newsom is likely to sign an anti-rent-gouging bill that caps annual rent increases at 5 percent plus inflation and limits the ability of landlords to evict tenants.

The debate has centered on the plight of tenants, who face soaring rents as California’s self-imposed housing crisis deepens. Opponents note that landlords will exit the market, builders will stop building apartments or turn rentals into condos, and owners will defer maintenance. Owners and renters will become adversaries as regulators and tenant boards turn a simple market transaction into an us-versus-them situation. Rent control obliterates housing markets wherever it is imposed.

Personal stories trump economic arguments, so today’s column offers my perspective as a small-time landlord. It’s a story other investors share, and sheds light on why government caps will make the housing situation worse. They’re not looking for sympathy, even when tenants mistreat the property, don’t pay their rent, or when unexpected things happen. In my case, a small earthquake cracked the toilet line and flooded my Mojave Desert house the day tenants were supposed to move in. It’s a business with costs, risks, and rewards.

But here’s a clue of what’s going to happen. I’ve rarely raised rent or charged late fees and am lackadaisical about rules. Now the state is going to tell me how much I can charge and make it tough to evict any bad tenants. Most landlords will now raise rents to the maximum allowable limits every year and strictly enforce the terms of the lease. Many will sell their houses to single-family owners, which will take them off the rental market.

Currently, I’m under market rate with most rents because I rather keep good tenants than risk finding new ones. With rent control, landlords lose the ability to raise rents when they choose, so we need to be diligent to keep rents at their peak given that the previous year becomes the baseline. If we are lax on enforcing the lease, then it’s hard to suddenly declare that to be a “just cause” for eviction. Since the state will control our profits, we’ll need to maximize profits wherever we can.

I’ll probably turn management over to management companies, which are far less lenient when a tenant has a tough month or less likely to authorize what I did recently—insulate a house and install new ductwork to help a tenant get utility bills to an affordable spot.

This is a side business. It’s partly a labor of love. Most of my homes are historic properties in working-class communities. After I renovated an Art Deco mansion on a city park, neighbors hugged me because turning an eyesore into a professional office building helped upgrade the surrounding block. As an aside, a 2020 ballot initiative would remove Proposition 13’s property-tax limits from most commercial buildings, which could obliterate my earnings on that property. California gets you coming and going.

At what point does it make more sense to stick one’s money in a mutual fund? That fund doesn’t call you at 2 am when the toilet is overflowing. When small landlords leave the market that means fewer single-family homes for rent. It makes renters more dependent on big apartment companies, who can afford the staff to manage the regulatory hassles. It also means fewer opportunities for middle-class people to buy and rent out real estate, which remains a great path to wealth creation. Not everyone has a government pension, you know.

It’s about incentives. You get more of what you encourage and less of what you punish. California’s rent crisis is caused by insufficient supply, which is the result of a system that imposes a punishing level of regulation and fees on builders and developers—and now on landlords. It will mean fewer properties for rent and fewer landlords who proudly design the fireplace mantle.

Just like in 2008, most Americans are living right on the edge financially, and so any sort of an economic downturn is going to be extremely painful for tens of millions of American families. When you have not built up a financial cushion, any sort of a setback can be absolutely disastrous. During the last recession, millions of Americans suddenly lost their jobs, and because most of them were living paycheck to paycheck a lot of them suddenly couldn’t pay their mortgages. In the end, millions of Americans lost their homes during the “subprime mortgage meltdown”, and today the housing bubble is even larger than it was back then. Sadly, the reality of the matter is that many of us are just barely scraping by from month to month, and that is a very dangerous position to be in.

A new survey that was just released shows just how vulnerable American consumers have become at this point in time. According to the survey, the top financial priority for 38 percent of all Americans is just trying to pay the bills, and for 19 percent of all Americans it is dealing with credit card debt. The following comes from Fox Business…

Among survey respondents in the nationally representative poll, 38 percent said their top financial priority is “just staying current on living expenses or getting caught up on all the bills.” Almost 3 in 10 respondents (29 percent) said their chief priority was “saving more money,” and 19 percent indicated they were mainly working on paying down debt from products like credit cards and student loans.

So that means that for nearly 60 percent of all Americans, the top financial priority each month is either finding a way to pay the bills or dealing with credit card debt.

And if you are struggling to pay the bills each month or you are drowning in credit card debt, the truth is that you are definitely not ready for the next recession.

More than a decade into the longest economic expansion on record, almost two-fifths of people said in a new Bankrate poll that their main financial priority was just keeping their heads above water on living expenses rather than saving money.

Nearly as many of those surveyed said that they’re not following financial budgets, according to Bankrate’s September Financial Security Poll.

So many people out there spend money whenever they feel like it and they don’t have any sort of a plan for their finances.

And then when they get deep into debt they wonder how that could have possibly happened.

It is so important to take charge of your money and to have a plan for where you want to go financially. Because if you don’t have a plan for your money, I promise you that somebody else does. As many of us have learned the hard way, it is all too easy to fall victim to all of the financial predators that are constantly circling these days. The big financial institutions want to get Americans into as much debt as possible, because the deeper we are in debt the more money they make.

In our society, everything has become all about extracting as much money out of you as possible. Even when we are at the checkout counter at the supermarket we are asked if we want to get some “cash back” so that they can charge us a “convenience fee” and make even more money. And of course most of the money that is extracted out of us ultimately ends up at the very top of the financial pyramid, and as a result the gap between the “haves” and the “have nots” continues to grow.

In fact, the U.S. Census Bureau is telling us that the gap between the rich and the poor is now “greater than it has ever been”…

In the midst of the longest economic expansion the United States has ever seen, with poverty and unemployment rates at historic lows, the separation between rich and poor from 2017 and 2018 was greater than it has ever been, federal data show.

To be fair, the U.S. Census Bureau has only been measuring this since 1967, and so it is entirely possible that things could have been even worse earlier in our history.

But the numbers do clearly show that the gap has been steadily widening for years, and at this point wealth inequality in the U.S. is far greater than it is in any country in Europe…

The Gini index measures wealth distribution across a population, with zero representing total equality and 1 representing total inequality, where all wealth is concentrated in a single household. The indicator has been rising steadily during the past several decades. When the Census Bureau began studying income inequality more than 50 years ago, the Gini index was 0.397. In 2018, the Gini index rose to 0.485.

By comparison, no European country had a Gini index greater than 0.38 between 2017 and 2018.

So what this means is that we have a small group of people at the top of the pyramid doing really, really well, but meanwhile most of the rest of us are deeply struggling.

The way that our entire system is structured greatly favors Wall Street, the big banks, the largest corporations and those with enormous amounts of money. And they are able to maintain control of the system by literally buying elections and controlling public opinion through their control of the mainstream media. Our founders were deeply suspicious of large concentrations of power, and we need to return to the values that our nation was founded upon if we ever hope to turn things around.

Unfortunately, more Americans that ever are convinced that socialism is the answer to the problems that I just discussed, and this is fueling the rise of politicians such as Bernie Sanders and Elizabeth Warren.

But socialist experiments have failed all throughout human history, and socialism would fail here too.

Big government is never the answer. Sadly, we already have the biggest government in the history of the world, and many Americans seem absolutely determined to make it even bigger.

Every time we walk past lumber racks in a home-improvement store my wife or daughters start giggling about all the “fine pieces of wood.”

It’s an inside joke that goes back to my first rental property in a small Mojave Desert town. I bought it “as is” in an online auction (although I saw it in person first), and remember the horrified look on the faces of my family when I took them to see it. Think of the term “uneasy silence.”

Half of the roof had blown off from vicious desert winds. The house had broken windows, broken everything, trash strewn everywhere. It looked like something out of the movie “Road Warrior,” given that it sat amid tumbleweeds, sand and cactus. Anyway, I lovingly fixed it up on a shoestring budget. When it was done, I popped for a pricey but fine piece of wood to create the mantelpiece. I was proud of it—and still get teased.

This is not the newspaper version of “Fixer Upper,” but a look at rent control. Gov. Gavin Newsom is likely to sign an anti-rent-gouging bill that caps annual rent increases at 5 percent plus inflation and limits the ability of landlords to evict tenants.

The debate has centered on the plight of tenants, who face soaring rents as California’s self-imposed housing crisis deepens. Opponents note that landlords will exit the market, builders will stop building apartments or turn rentals into condos, and owners will defer maintenance. Owners and renters will become adversaries as regulators and tenant boards turn a simple market transaction into an us-versus-them situation. Rent control obliterates housing markets wherever it is imposed.

Personal stories trump economic arguments, so today’s column offers my perspective as a small-time landlord. It’s a story other investors share, and sheds light on why government caps will make the housing situation worse. They’re not looking for sympathy, even when tenants mistreat the property, don’t pay their rent, or when unexpected things happen. In my case, a small earthquake cracked the toilet line and flooded my Mojave Desert house the day tenants were supposed to move in. It’s a business with costs, risks, and rewards.

But here’s a clue of what’s going to happen. I’ve rarely raised rent or charged late fees and am lackadaisical about rules. Now the state is going to tell me how much I can charge and make it tough to evict any bad tenants. Most landlords will now raise rents to the maximum allowable limits every year and strictly enforce the terms of the lease. Many will sell their houses to single-family owners, which will take them off the rental market.

Currently, I’m under market rate with most rents because I rather keep good tenants than risk finding new ones. With rent control, landlords lose the ability to raise rents when they choose, so we need to be diligent to keep rents at their peak given that the previous year becomes the baseline. If we are lax on enforcing the lease, then it’s hard to suddenly declare that to be a “just cause” for eviction. Since the state will control our profits, we’ll need to maximize profits wherever we can.

I’ll probably turn management over to management companies, which are far less lenient when a tenant has a tough month or less likely to authorize what I did recently—insulate a house and install new ductwork to help a tenant get utility bills to an affordable spot.

This is a side business. It’s partly a labor of love. Most of my homes are historic properties in working-class communities. After I renovated an Art Deco mansion on a city park, neighbors hugged me because turning an eyesore into a professional office building helped upgrade the surrounding block. As an aside, a 2020 ballot initiative would remove Proposition 13’s property-tax limits from most commercial buildings, which could obliterate my earnings on that property. California gets you coming and going.

At what point does it make more sense to stick one’s money in a mutual fund? That fund doesn’t call you at 2 am when the toilet is overflowing. When small landlords leave the market that means fewer single-family homes for rent. It makes renters more dependent on big apartment companies, who can afford the staff to manage the regulatory hassles. It also means fewer opportunities for middle-class people to buy and rent out real estate, which remains a great path to wealth creation. Not everyone has a government pension, you know.

It’s about incentives. You get more of what you encourage and less of what you punish. California’s rent crisis is caused by insufficient supply, which is the result of a system that imposes a punishing level of regulation and fees on builders and developers—and now on landlords. It will mean fewer properties for rent and fewer landlords who proudly design the fireplace mantle.

SSDD: Global Markets Rise On “Wave Of Trade Optimism”

It’s groundhog day, again.

World shares erased losses and US equity futures traded at yesterday’s high on the last day of the week, buoyed by what Reuters described was “a wave of optimism that U.S.-China trade tensions might be easing” as markets continued to brush off concerns about possible impeachment moves against U.S. President Donald Trump

MSCI’s world index reversed earlier losses and was trading flat as US traders walked into their desks, even as it was still heading toward its worst weekly performance since mid-August, though Europe’s STOXX 600 index fared better, adding 0.5% as London’s bourse outperformed on a weaker pound and hopes grew of progress toward resolving the trade war.

Wall Street futures signaled a firm opening in New York, gaining around 0.3% and reversing all of yesterday’s late losses.

Mining and car-maker shares led Europe’s Stoxx 600 higher, along with U.K. stocks while chipmakers Infineon and Siltronic both fell around 1.5%, mirroring losses for Asian chip-related shares Samsung Electronics and SK Hynix after major Huawei supplier Micron Technology tumbled 7% in after-hours trade after it forecast first-quarter profit below Wall Street targets. Britain’s exporter-heavy FTSE 100 rose along with gilts and the pound fell after Bank of England’s most hawkish policymaker, Michael Saunders, said rate cuts may be needed even if there is a Brexit deal.

Earlier in the session, Asian stocks fell, heading for a weekly loss, as investors assessed new revelations surrounding an impeachment inquiry of U.S. President Donald Trump. Most markets in the region were down, with Japan and South Korea leading declines. The Topix dropped 1.2%, dragged by a slew of Japanese companies trading ex-dividend. The Shanghai Composite Index closed 0.1% higher after fluctuating for most of the day, with Kweichow Moutai rising and China Shenhua Energy retreating. The U.S. probably won’t renew a temporary waiver that lets American companies do business with telecommunications giant Huawei. India’s Sensex inched 0.1% lower, dragged by Tata Consultancy Services and IndusInd Bank. The country is upgraded to neutral on expectation that recent tax changes will lift earnings, UBS analysts wrote in a note today

On Thursday, investors focused on a whistleblower report that said Trump abused his office in trying to solicit Ukraine’s interference in the 2020 U.S. election for his political benefit, and that the White House tried to “lock down” evidence about that conduct. The report came after the speaker of the U.S. House of Representatives Nancy Pelosi this week launched an impeachment inquiry into Trump, who has denied wrongdoing. However, chances of his being removed from office look slim given that the Republicans control the Senate, where any impeachment trial would be held.

“What we are waiting to see is how this might impact the U.S.-China trade negotiations,” said Hugh Gimber, global market strategist at J.P. Morgan Asset Management. “It’s that combination this week of weakening economic data and rising political uncertainty that has caused some tricky periods in markets.”

And speaking of the biggest source of overnight market “optimism”, Washington and China are preparing for another round of trade talks scheduled for Oct. 10 and 11, but investors voiced scepticism at prospects of a major breakthrough then.

“There is still a huge gulf,” said Eoin Murray, head of investment at Hermes Investment Management, adding that prospects for a deal had receded from earlier in the year. “Around April, May time, the main sticking point was the enforcement mechanism – but we have retreated miles from that at this point.”

Tech remains a sticking point, with reports on Thursday that the United States is unlikely to allow American firms to supply China’s Huawei Technologies undermining hopes of a broad bilateral deal.

Offsetting lingering doubts, China’s top diplomat said on Thursday that China was willing to buy more U.S. products and that trade talks would yield results. Those comments fueled the positive mood after Trump on Wednesday praised the Chinese purchases, saying a trade deal could come sooner than people thought.

“Trade… remains the most important issue for markets, and the news that we have had over the last couple of weeks I would see as gestures of goodwill from both sides – trying to set up a more constructive negotiation in a couple of weeks’ time,” Gimber added.

In FX, the dollar headed for a second week of gains amid supportive quarter-end flows and a pound under pressure. The pound tumbled to a two week low and gilts rallied after otherwise hawkish BOE policymaker Michael Saunders said the central bank may have to cut interest rates even in the event of an orderly Brexit. Treasuries slipped while euro-area bonds traded mixed and stocks edged higher. The New Zealand dollar was one of the few currencies to appreciate against the dollar this week, boosted by the central bank’s comments Thursday indicating interest rate cuts were working.

The offshore yuan was set for its most serene week in two months as a week-long holiday to celebrate the 70th anniversary of the People’s Republic of China approaches. The currency was poised for a 0.09% move this week, its smallest weekly move since July 26. Meanwhile, the onshore yuan has continued to fall even as the central bank has set its daily reference rate stronger than expected for an eighth day. Its set for a weekly drop of 0.45%. “The fixing has been pretty stable, sending the signal that China wants to slow down the pace of depreciation,“ said Tommy Xie, an economist at Oversea-Chinese Banking Corp. However, onshore traders remain “jittery” and they are still buying the greenback on dips, he said, adding that the next catalysts to watch out for are the trade talks with the U.S. due in October, and the fourth plenary session of the 19th People’s Congress.

In rates, moves in European bond markets Friday were limited, with Treasuries underperforming German bunds; gilts led gains. 10Y Treasurys dipped modestly, with the yield on benchmark US paper rising from 1.69% to 1.71%. China’s 10-year government bonds slipped, with the yield headed for a 5-basis-point weekly advance.

Oil fell after a report that Saudi Arabia had moved to impose a partial cease-fire in Yemen. Treasury 10-year note yields ticked above 1.71% while the dollar was steady against its biggest counterparts.

Market Snapshot

S&P 500 futures up 0.2% to 2,986.75

STOXX Europe 600 up 0.4% to 391.57

MXAP down 0.6% to 157.43

MXAPJ down 0.2% to 503.69

Nikkei down 0.8% to 21,878.90

Topix down 1.2% to 1,604.25

Hang Seng Index down 0.3% to 25,954.81

Shanghai Composite up 0.1% to 2,932.17

Sensex down 0.1% to 38,936.80

Australia S&P/ASX 200 up 0.6% to 6,716.12

Kospi down 1.2% to 2,049.93

German 10Y yield rose 0.3 bps to -0.579%

Euro up 0.07% to $1.0929

Italian 10Y yield fell 1.9 bps to 0.485%

Spanish 10Y yield fell 0.6 bps to 0.143%

Brent futures down 0.1% to $62.67/bbl

Gold spot down 0.5% to $1,497.54

U.S. Dollar Index up 0.1% to 99.22

Top Overnight News from Bloomberg

Revelations about Donald Trump’s interactions with Ukraine’s president are shaping up to be the most serious threat to his presidency so far, surpassing even the special counsel investigation into Russian election interference that dogged the first two years of his administration

The Bank of England may have to cut interest rates even if the U.K. avoids a no-deal Brexit, according to policy maker Michael Saunders. His remarks are a sharp departure for someone who was previously considered the most hawkish member of the Monetary Policy Committee

The EU is rapidly losing faith that U.K. Prime Minister Boris Johnson can deliver a divorce deal by the Oct. 31 deadline, as Brexit talks stumble. EU officials view Johnson’s inflammatory rhetoric against his opponents as a hindrance and have all but given up on a breakthrough over the next five weeks

Brexit anxiety might be high, but that hasn’t stopped European corporate bond issuers from selling a record amount of sterling-denominated debt this month. It makes perfect sense when cross-currency basis swaps can leave them borrowing for less than at home

Chinese industrial companies’ profits fell in August, with the 2% drop from a year ago another sign of how the slowing economy is hurting business and increasing problems for the government

Asian equity markets were mostly subdued following the weak lead from Wall St where all major indices finished negative on what was a choppy session due to trade uncertainty and as political concerns regarding the whistleblower complaint lingered. ASX 200 (+0.6%) and Nikkei 225 (-0.8%) were mixed in which Australia bucked the overall downbeat trend in the region ahead of next week’s anticipated RBA rate cut although metal names and gold miners lagged as the precious metal eyed the USD 1500/oz level to the downside, while the Japanese benchmark was led lower by losses in Kansai Electric after reports of illicit payoffs and with notable declines in SoftBank due to the ongoing WeWork woes. Hang Seng (-0.3%) and Shanghai Comp. (Unch.) trades lacklustre as participants mulled over the latest trade rhetoric in which an official stated the US is unlikely to extend temporary waivers to supply Huawei although reports later noted no decision has been made and US-China talks are to resume on October 10th-11th, while the latest data provided no comfort as Chinese Industrial Profits contracted by 2%. Finally, 10yr JGBs were higher with mild support seen amid underperformance of stocks in Tokyo but with the gains in bonds capped by predominantly weaker results at the 2yr JGB auction.

Top Asian News

China Misses Out on Entering FTSE Russell Global Bond Index

China Markets May Benefit From Latest Rules on Wealth Products

Bond Stress Mounts in China’s Qinghai Province as Sale Fails

Two Emerging Markets Are Ready for the Next Global Recession

Major European indices are firmer this morning, with the FTSE 100 (+1.2%) leading the way after dovish comments from BoE Hawk Saunders caused Sterling to slip. Sectors are all in the green bar IT, which is hampered by broad-based downside in European chip names following Micron’s earnings last night where their EPS guidance missed exp. and they noted near term macro and trade uncertainties. Elsewhere, Commerzbank (+1.5%) are subdued as the Co. state they no-longer anticipate an increase in underlying revenue for 2019; although, they have launched a public acquisition offer for Comdirect Bank at EUR 11.44/shr. Sticking with Germany but moving into the DAX (+0.9%) where BASF (+3.0%) have confirmed their mid-term outlook and the additional EUR 2bln in savings by 2021; additionally, the CEO anticipates an Oil and Gas IPO in H2 2020. Separately, Rheinmetall (-2.3%) are weaker after reporting that production in the US, Mexico and Brazil has been severely impacted by a malware attack. Today’s notable in-hours story is from AMS (-7.5%) who have submitted their final offer for Osram Licht (+3.3%) in which they have increased their offer by EUR 2.50/shr for the Co.

Top European News

U.K. May Need Rate Cuts Even If It Avoids No-Deal, Saunders Says

Imperial Brands Prepares Strategy to Deal With Investors

Funding Blow Deepens Pain for Ukraine Leader Reeling From Trump

Italy Weighs VAT Changes, Penalty on Cash as Conte Seeks Revenue

In FX, the Pound is the marked G10 laggard after BOE MPC-hawk Saunders surprisingly took a more dovish stance as he stated that looser monetary policy could be warranted amid “prolonged high Brexit uncertainty” coupled with disappointing global growth and as the adverse effects of high uncertainty is becoming clearer in domestic macro data. Saunders also noted that in the even the UK avoids a no-deal, rates could go either way, i.e. a rate cut is still on the table in the event a no-deal Brexit is averted. Cable gave up the 1.2300 handle (from around 1.2330) to an intraday low of 1.2270 ahead of its 50 DMA at 1.2262. Meanwhile the EUR is flat on the day after the earlier softness in the single currency was countered by an even softer Sterling post-Saunders. Meanwhile, the EUR initially felt pressure amid an interview by ECB-dove Lane who stated the ECB has further room to ease and that the stimulus package announced was a relatively smaller one in his opinion. EUR/USD resides around 1.0925 having visited a low of 1.0905 ahead of reported bids at the psychological 1.0900 level, 1.0880-90 and a Fib at 1.0864. EUR/GBP remains firm just under 0.8900 having hit an intraday high of 0.8896.

DXY – Firmer on the day with the index eyeing YTD highs of 99.37 having already reached an intraday peak at 99.31. The Dollar gains seen recently are in the absence of clear catalysts, although market participants point to month and quarter-end as a potential factor. UBS notes that foreign equities, particularly Japanese, have outperformed US stocks in September, which “implies that hedge rebalancing pressures could favor the US dollar”. Meanwhile, the weakening Euro amid further deterioration in the EZ may also be underpinning the Greenback. DXY currently resides just below 99.25 ahead of the YTD peak. USD/JPY meanwhile has breached 108.00 to the upside amid the strength in the Buck (ahead of the September high at 108.48 and the psychological 108.50). Looking ahead, the State-side docket sees the release of the Core PCE metrics alongside Durable Goods with Fed’s Quarles (voter) and Harker (non-voter) due to speak later.

AUD, NZD – The Aussie bucks the trends and remains firm ahead of next week’s RBA rate decision. Money markets are currently pricing in around a 78% chance of a 25bps cut, although support for the currency could be derived from Morgan Stanley’s call for the RBA to stand pat until further economic data is available, whilst firmer copper prices also underpin the currency. AUD/USD is back above the 0.6750 level whilst AUD/NZD tested 1.0750 to the upside (vs. low of 1.0720), in turn pressuring NZD/USD back below 0.6300.

SEK – The Scandi Crown remains weaker against the Euro amid disappointing retail sales which saw the MM and YY figures miss forecasts. EUR/SEK breached its 50 DMA at 10.6898 and now eyes 10.6900 to the upside having printed an intraday low at 10.6520.

In commodities, WTI and Brent futures fell deeper into negative territory as the geopolitical risk premium unwound further amid reports that Saudi Arabia has agreed to establish a partial ceasefire in Yemen which follows reports of US aiding Saudi Arabia bolster its defences. The WSJ article took WTI below the 56.00/bbl mark and under the cluster of DMAs including its 50 DMA (56.02/bbl), 100 DMA (56.63/bbl) and 200 DMA (56.66/bbl), whilst Brent lost the USD 62.00 handle. Elsewhere, gold prices are on the backfoot amid a firmer Greenback as the yellow metal dips below the 1500/oz mark to a current low of 1491/oz. Meanwhile copper prices are firmer with upside attributed to signs of progress in US/China trade talks with a date now set for principal level talks, according to sources. Copper is back above USD 2.58/lb ahead with the next level to the upside the psychological 2.60/lb mark.

US Event Calendar

8:30am: Durables Ex Transportation, est. 0.2%, prior -0.4%

8:30am: Personal Income, est. 0.4%, prior 0.1%

8:30am: Real Personal Spending, est. 0.2%, prior 0.4%

8:30am: PCE Deflator MoM, est. 0.1%, prior 0.2%; PCE Deflator YoY, est. 1.4%, prior 1.4%

8:30am: PCE Core Deflator MoM, est. 0.2%, prior 0.2%; PCE Core Deflator YoY, est. 1.8%, prior 1.6%

8:30am: Durable Goods Orders, est. -1.0%, prior 2.0%

8:30am: Personal Spending, est. 0.3%, prior 0.6%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.0%, prior 0.2%; Cap Goods Ship Nondef Ex Air, est. 0.25%, prior -0.6%

10am: U. of Mich. Sentiment, est. 92.1, prior 92; Current Conditions, prior 106.9; Expectations, prior 82.4

10am: U. of Mich. 1 Yr Inflation, prior 2.8%; 5-10 Yr Inflation, prior 2.3%

DB’s Jim Reid concludes the overnight wrap

I had a day trip to Germany yesterday and it was pouring with rain when I boarded the plane and it started again as I landed and didn’t stop all day. Basically since Sunday all I’ve known is rain. It makes a mockery of the decision I made on Saturday when after scattering a garden ruined by builders with grass seeds, I slowly and meticulously sprayed it with water. A few hours later it hardly stopped raining for four days. That’s 90 minutes of my life I won’t get back.

I feel the same about politics at the moment. I’m glued to the political machinations on both sides of the Atlantic even if I know it’s not going to progress my understanding of life and markets very much. Indeed the direction in markets at the moment is either dictated by trade, the impeachment drama or a combination of both. Well yesterday the impeachment news won out initially after the whistle-blower complaint was released before headlines suggesting that the US is unlikely to extend a temporary waiver for US companies to continue supplying Huawei then took over.

The end result was a slide for US equity markets with the S&P 500 closing down -0.23% (but off its lows) and the NASDAQ down a slightly heavier -0.58%. That’s four down days out of the last five for the S&P 500 although to be fair the magnitude hasn’t been all that impressive with the index still within just 1.58% of the all-time highs. Both indexes closed above their lows after an afternoon rally which briefly sent the S&P 500 into positive territory, boosted by optimistic trade comments from Chinese Foreign Minister Wang who said that the US has shown good will and that he hopes “talks will not only resume but will proceed and yield results.” There were further positive indications from top US economic advisor Kudlow, who spoke positively about the scope for passing the USMCA this year despite the impeachment diversion. As for the substance of the impeachment issue, the main headlines which came out of the public release of the whistle-blower’s complaint was the reference to “lock down” records of the interaction and that White House officials were “deeply disturbed” by Trump’s call with the Ukrainian president. Overnight the Los Angeles Times published a private recording where Mr Trump has been accused of intimidation towards the whistleblower by saying that he was “almost a spy” and added “You know what we used to do in the old days when we were smart with spies and treason, right? We used to handle it a little differently than we do now.” Expect this story to go on for a while.

Back to markets, and there was some attention on the recent softness of IPOs after Peleton had the third-worst trading debut in ten years, according to Bloomberg. Despite selling shares at $29, they traded as low as $24.75 and closed -11.17% at 25.76. New equity issuance has decelerated to the slowest pace since 2016 so far in 2019, the FT reported. Further, with the reported delay in Saudi Aramco’s listing, attention is focusing more and more on pre- and post-IPO companies. An ETF of IPOs has underperformed the broader market by 12.89% since its July peak. It’s notable that the last time this index of new issuances lagged by such a margin, it was just before the Oct-Dec sell-off last year. Overnight, Micron Technology gave a disappointing quarterly profit forecast and warned that global trade tensions may prolong a memory-chip industry slump. Shares were down c. -7% in after hours trading.

Despite the softness in equities, volatility remained muted with the VIX ending at 16.1 (+0.1pts), though the risk off sentiment did drive a steady bid for safe havens with 2y and 10y treasury yields rallying -2.2bps and -4.2bps respectively. The USD (+0.17%) gained slightly, while EM currencies struggled, especially the Mexican peso (-0.52%) after Banxico cut rates and gave more dovish than expected policy guidance. There was some action later in the day following a number of Fedspeakers, and thankfully a distraction from the politics. Front and centre was Clarida who, speaking at a Fed Listens event, said that inflation is running close to the 2% target and that inflation expectations are a level consistent with price stability. He also spoke about the potential outcomes of the Fed’s policy review, saying that “make-up strategies lead to better average performance” in models, but it’s not clear if those outcomes would carry over to the real world. After the US markets closed, Richmond Fed President Barkin, a known hawk, said that the recent rate cuts don’t “mean a recession is imminent, nor that we are in a prolonged period of easing.”

Overnight, Asian markets are trading largely lower with the Nikkei (-1.30%) leading the declines as a large number of companies are trading ex-dividend while the Hang Seng (-0.30%) and Kospi (-1.15%) are also down. The Shanghai Comp and CSI 300 are trading flat. The above mentioned overnight report from the LA Times is helping to slightly dampen sentiment this morning.

In other overnight news, the Sun has reported that three UK cabinet ministers are preparing to push for Boris Johnson to lower his demands over Brexit talks after the Tories’ annual conference in Manchester next week. The report added that they will demand that he abandons senior aide Dominic Cummings’s aggressive strategy and accept any last-minute offer from the EU. Meanwhile, the FTSE Russell index decided not to include China’s domestic debt in its flagship World Government Bond Index, citing concerns including liquidity and settlement of trading, and added that China will remain on the FTSE Russell’s watchlist. The company said in its statement that further updates will come “as appropriate after the interim review in March 2020.” The decision comes as a bit of surprise after the Bloomberg Barclays Global Aggregate bond index decided to include Chinese debt in April and JPMorgan earlier this month decided it will start a phased inclusion of Chinese sovereign debt into its emerging-market indexes from the end of February. Elsewhere, Turkish President Tayyip Erdogan said that it was impossible for Turkey to stop buying oil and natural gas from Iran, despite the threat of US sanctions, and added that trade between the two countries would continue. The Turkish lira is trading (-0.11%) down this morning.

Back to yesterday and the third Q2 GDP reading in the US was unrevised at +2.0% qoq however there was a surprising upward revision to Q2 core PCE to +1.9% qoq from the previous forecast of +1.7%. With that in mind it’s worth noting that we get the August PCE data this afternoon where the consensus expects a +0.2% mom core reading, which would push the annual rate up two-tenths to +1.8% yoy. Yesterday’s data could provide some upside risks to that though. It would be ironic if inflation started to come through just as everyone has given up on it.

As for the other data yesterday, the August advance goods trade balance showed a deficit of $72.8bn which was a tad smaller than expected. Wholesale inventories rose a better than expected +0.4% mom (vs. +0.1% expected), jobless claims remained at a lowly 213k, August pending home sales rose +1.6% mom (vs. +1.0% expected) and the September Kansas City Fed manufacturing survey was a bit better than expected having risen 4pts to -2 (vs. -4 expected).

In Europe, and specifically over at the ECB, Reuters reported that Lautenschlaeger sent an internal email to ECB staff suggesting that her decision to resign early from the board “was probably the result of professional, rather than personal, considerations”, which as expected more than likely reflects an opposition to the September stimulus programme. Data showed a 5.7% yoy increase in the M3 money supply, better than expected, which pointed to another healthy expansion in bank credit flows. The credit impulse rose 0.6pp to the highest level in four months. European equities finished onside yesterday with the STOXX 600 up +0.61% while 10y Bunds were little changed.

Looking at the day ahead, data due this morning in Europe includes the preliminary September CPI report in France and September confidence indicators for the Euro Area. In the US the focus will be on the aforementioned August PCE report, while preliminary August durable and capital goods orders data will also be important to watch. The August personal income and spending prints are also due along with the final September University of Michigan consumer sentiment survey revisions. Away from that, the Fed’s Quarles and Harker will speak along with the ECB’s Guindos, Knot and Lane.

UK Tanker Seized By Iran Released After Two Months In Captivity

The British-flagged Stena Impero tanker was released Friday after more than two months of being moored outside Iran’s Bandar Abbas port.

Footage showing #British oil tanker Stena Impero starting to move from Bandar Abbas port of #Iran for international corridor of Persian Gulf on Friday morning. pic.twitter.com/3rIIQUZkwo

Stena Impero was seized in July by Iran in the Strait of Hormuz for alleged marine violations two weeks after British naval forces detained an Iranian tanker off the territory of Gibraltar.

“The ship is on the move,” Erik Hanell, the chief executive of the ship’s owner, Sweden’s Stena Bulk, told Reuters in a text message. “We will comment further when the ship reaches international waters.”

According to Refinitiv tracking data, the vessel is heading for Dubai’s Port Rashid in the United Arab Emirates. The automatic identification system, an automated tracking system that uses transponders on the ship, indicates the vessel is “underway using the engine,” traveling at 12 knots, and about 155 miles from Port Rashid.

The vessel is likely to reach its destination in about a day, is expected to make more headlines when the vessel hits international waters and arrives at Port Rashid.

The Ports and Maritime Organization of Iran in Hormozgan Province said in a statement the vessel left the Bandar Abbas port early Friday and was heading towards international waters. The statement added that a judicial file was still open on the ship.

Iranian President Hassan Rouhani, at a news conference Thursday in New York during the United Nations’ annual gathering of world leaders, told reporters he expected Stena Impero to be released after the completion of legal procedures.

“The tanker is going through the final court proceedings. I predict that it will be released,” Rouhani said at the UN on Thursday.

Stena Bulk said Wednesday there were zero negotiations with Iran and wasn’t informed of any formal charges against the crew.

“We haven’t been accused of anything,” Stena Bulk Chief Executive Erik Hanell said in a telephone interview. “Not through any formal letter or anything else to the company.”

Relations between the US and Iran have become tenser since Washington withdrew from the Joint Comprehensive Plan of Action, also known as the “Iran deal,” in May 2018.

The abandoning of the Iran deal resulted in the Trump administration imposing heavy economic sanctions on Tehran, a move that has paralyzed the country’s economy.

Earlier this week we reported how the US had imposed new sanctions on Chinese entities for “knowingly engaging” in transporting Iranian oil – the move is part of the Trump administration’s “maximum economic pressure campaign against the Iranian regime and those who enable its destabilizing behavior,” said Secretary of State Mike Pompeo in a press release on Wednesday.

Takashi Miike is possibly the last director—well, Rob Zombie and the sadly retired Uwe Boll might also spring to mind—whom you’d expect to find dabbling in true romance. It’s taken him a while to reach this breakthrough, but hey, he’s been busy. (As required by movie-reviewing law, I must here point out that, although he’s only 59 years old, Miike is credited with directing more than 100 films, many of them released theatrically, others made for the straight-to-video market or for TV.) Since his trademark is a species of fierce, sadistic violence that’s so over-the-top it’s often funny (well, to a certain kind of viewer), the appearance of a new Miike movie called First Love might incline fans to fear that he’s going soft on them.

But no. Or not really. This being a Miike film, the young canoodlers at the heart of the story are a boxer with a brain tumor (Masataka Kuboat) and a drug-addicted call girl (Sakurako Konishi). And the Tokyo that they flee through over the course of one long, frantic night is a place where severed heads come rolling out of doorways, a woman expends a lot of energy kicking a man to death (“You don’t get out of this by dying,” she screams at his lifeless body), and an angry yakuza carefully drives his van over an unconscious bad guy’s head (cue sound of melons being crushed).

One drawback of Miike’s madly prolific approach to filmmaking is that it sometimes leaves him scrambling for good scripts, which he isn’t always able to find, if he even bothers looking. (On the other hand, his 1999 needle-torture classic Audition is a picture not an awful lot like any other, and so is his spectacularly brutal 2001 gang flick, Ichi the Killer.) With First Love, the director has said that he wanted to get back to a classic yakuza crime film, and he’s certainly done that—the picture is filled with tough guys (and very tough women), scuzzy drug dealers and crooked cops, all doing pretty much what you’d expect. What makes the movie compelling is the tireless energy and choreographic clarity that Miike brings to his action sequences, of which there are, of course, many.

The story gets underway in a boxing ring, where Leo, a well-regarded up-and-comer, is losing a match for reasons he can’t understand. (Miiki renders his fight scenes with nimble camera strategies and very tight editing, and you can almost feel the sweat spraying your face with each punch.) After Leo gets the news that he has a possibly inoperable brain tumor, we move along to make the acquaintance of Monica, who’s turning tricks to pay off a debt owed by her abusive father to a yakuza bigwig. Monica is kept a virtual hostage by a drug dealer who has gotten her addicted to heroin, and she’s also mercilessly berated by the dealer’s unhinged girlfriend Julie (pop singer and TV star Becky, taking a step up in the biz).

Fuurther enlivening the story is a treacherous yakuza youth called Kase (Shôta Sometani) who’s scheming with a corrupt police detective (Nao Ohmori, a veteran of Ichi the Killer) to hijack a big drug shipment and blame it on the Chinese mob. Also on hand, at first as a subject of nervous discussion and later as a fearsome presence, is a hitman called One-Armed Wang (a name I take to be a shout-out to the 1967 martial arts movie of that title), who has been able to continue pursuing his chosen profession, despite his handicap, by acquiring a pump-action shotgun. (If only the actor who plays him could acquire a name in the movie’s English-language credits.)

First Love isn’t great Miike, but it’s fun, despite the fact that—spoiler—love conquers all (or at least a lot) in the end. Fans should find quite a bit to like—there’s a quick, funny bit, for example, in which a gunman has his shooting arm hacked off with a sword and then finds it hard to pry his pistol back out of his former fingers.)

Miike remains a meticulous action filmmaker; if only he hadn’t always been in such a hurry. And now he faces a serious challenge in the ultra-violence department: the John Wick movies. These are also deliriously brutal (although not as sadistically twisted as some of Miiki’s films), but they’re also set in a world with a rich pulp mythology unlike anything Miike has come up with (as far as I’m aware). Our man might want to give this some thought, maybe take a year off.

from Latest – Reason.com https://ift.tt/2mfCLqM

via IFTTT