For only $19.99, you can instantly stream our 11-hour library, and learn about the 100 Supreme Court cases everyone should know. Or jump around to watch the cases you studied in class. Here is a preview of all 100 videos. Click the “playlist” feature (3rd icon from the right):

from Latest – Reason.com https://ift.tt/2rG5wza

via IFTTT

Futures Flat On Lack Of “Trade Deal Optimism”; Traders Puzzled By Sudden Hang Seng Tumble

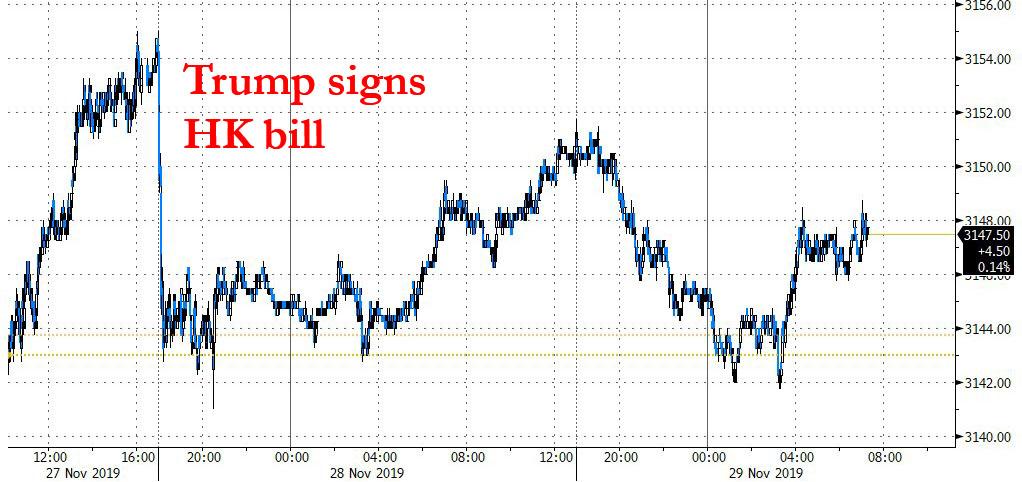

Futures were caught in the narrow range in which they traded for much of Thanksgiving Day holiday amid a lack of both trade deal optimism but more importantly, a lack of an actual retaliatory act from China which appears satisfied to jawbone in response to the passage of HK law, but is unwilling to do anything else to risk the trade deal as reported overnight.

And with the failure to break out to fresh highs, world shares also slipped on Friday as the MSCI World index strained for a record high, with investor nerves from Asia to Europe frayed over how or when the United States and China can agree a truce in their damaging trade war. The MSCI All Country world index again fell 0.2% to 548.48 points, remaining just short of the record 550.63 scaled in January 2018 before the eruption of tensions over trade between Washington and Beijing.

In Europe, the Stoxx 600 recovered from an early drop but after levitating modestly in the green, as declines in mining and construction shares offset increases in technology and travel, was back to unchanged if still near a four-year high. In holiday-thinned trade, stronger than expected eurozone inflation data was the main piece of economic data. The data showed inflation accelerated in November, comforting EcoCB policymakers, even if some factors pushing up prices may be only temporary. The ECB will next meet on Dec. 12, with its loose policy stance not expected to change for months to come. It may, however, decide to dump all bonds issued by companies that are not determined “green” by Christine Lagarde (we are only joking… we hope).

Earlier in the session, Asian stocks declined for a second day, led by tech firms, as investors awaited China’s possible retaliation against a U.S. bill supporting Hong Kong protesters. Most markets in the region were down, with Hong Kong leading losses and Indonesia rebounding. Despite Friday’s weakness, the MSCI Asia Pacific Index is heading for a third straight month of gains. The Topix fell 0.5% in thin trading, driven by Toyota Motor and Recruit Holdings. Japan looks set to re-embrace the power of public spending with one of its biggest ever stimulus packages. The Shanghai Composite Index closed 0.6% lower, capping a third week of declines, as signs of financial stress in China are putting the nation’s policy makers to the test. India’s Sensex retreated ahead of a quarterly economic report, which is expected to show the weakest growth in more than six years.

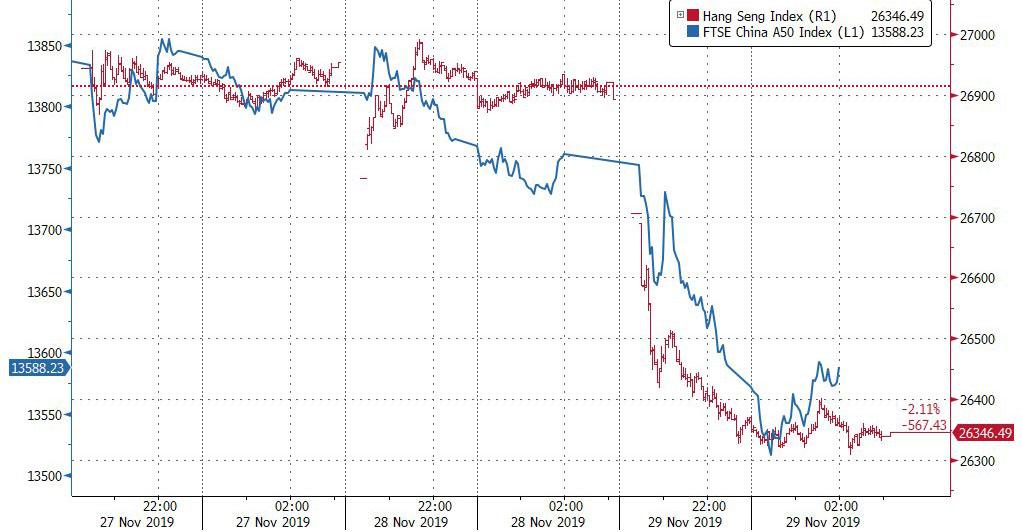

The big surprise in Asian trading was the a sudden, unexplained tumble in Hong Kong stocks which spread to the onshore market, with selling reflexively accelerating amid nervousness over a lack of clear triggers for the slump. As Bloomberg reports, the market was rife with speculation for the cause: health-care shares tumbled in Hong Kong when a document circulating on social media suggested Beijing could add dozens of new drugs to another round of procurement. Others said there was too much macro risk going into the weekend, with increasing uncertainty on the trade-war front. In onshore trading, the selling accelerated in the afternoon session as investors took profits in crowd favorites like Kweichow Moutai.

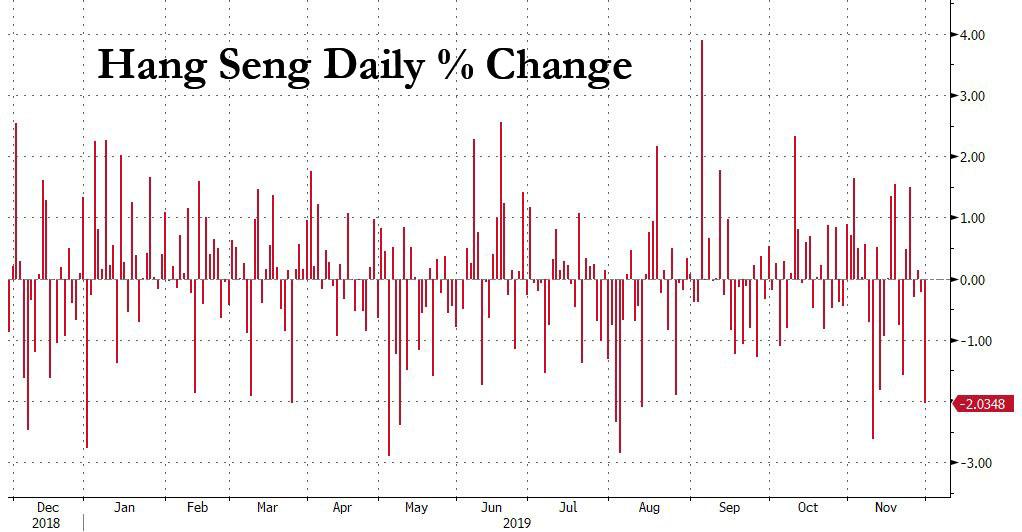

In total, Hong Kong’s Hang Seng Index tumbled 2% on volume that was 36% higher than the 30-day average. Quoted by Bloomberg, some traders said Thursday’s U.S. holiday meant investors lacked cues in Friday’s Asian session.

“There’s no obvious trigger” for the selloff according to First Shanghai Securities strategist Linus Yip who speculated that continued uncertainty over the outcome of U.S.-China trade negotiations could be one factor weighing on sentiment.

The Hong Kong sell-off came as investors grew uncertain over how U.S. markets will perceive the latest clash between Washington and Beijing over Hong Kong. “The more recent news on the trade front is how the Hong Kong situation might play into the U.S.-China trade negotiations,” said Hugh Gimber, strategist at J.P. Morgan Asset Management. “The market is now waiting on the next clear steer on when investors might be able to expect a deal to be reached.”

Meanwhile, across the Pacific, Wall Street will start the half-day session on Friday following Thanksgiving with futures gauges suggesting losses of around 0.2%, just shy of all time highs.

The lack of a more powerful selloff following Trump’s Wednesday’s night signature indicates that markets do not believe the trade deal will collapse as a result as investors bet it remains in the interest of both Washington and Beijing to move forward with talks to get a trade deal. Meanwhile, the MSCI world index climbed 2.5% this month, its third straight month of gains, helped in part by hopes the world’s two biggest economies are moving toward a resolution. The trade conflict has upset financial markets and disrupted supply chains even if stocks have continued to climb buoyed by nonstop optimism and hope that a deal is just around the corner… ever since the summer of 2018!

Meanwhile, what really matters is central bank policy and the Fed’s NOT QE: for the year, the MSCI world index is up over 20% this year, helped by a lowering of interest rates and injections of government stimulus around the world.

In rates, 10Y Treasurys were unchanged from Wednesday, trading at 1.764%; Benchmark European bonds, including Germany’s 10-year Bund yield, were also little changed, trading off one-month lows hit the previous session.

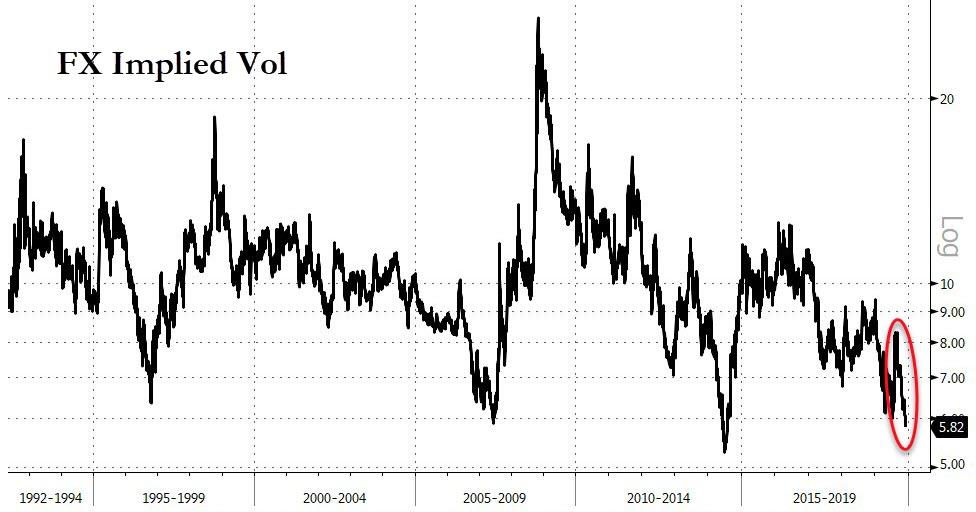

In FX, the dollar traded initially flat at 98.387, and edged up slightly against the Japanese yen. In early London trading, the greenback reached 109.55 yen, not far off a six-month peak of 109.61 set on Wednesday. The dollar then took off and the Bloomberg dollar index rose again, spiking above 1,210, headed for its biggest monthly gains since July. The pound eyed its longest monthly run of advances against the euro in more than 4.5 years, while the relative cost of hedging sterling climbed ahead of next month’s U.K. election. The euro stood at $1.1005, and has been stuck in a tight range for the past week. As trading in major currencies slumbers, their implied volatilities, key gauges of expected swings measured by their option prices, plumbed record lows this week.

Elsewhere, bitcoin gained 1.5%, with the original cryptocurrency on course for its worst month in a year. Bitcoin had been heavily sold off by investors as expectations fade that China’s embrace of blockchain would help cryptocurrencies enter the mainstream.

In commodities, oil prices dipped, with investors awaiting a meeting of OPEC and its allies next week. OPEC watchers expect an extension to a pact to throttle oil output but no deeper cuts to be agreed by the producer group and its allies next week. Brent crude futures were down 44 cents, or 0.7%, at $63.43 a barrel.

Markets Snapshot

S&P 500 futures down 0.2% to 3,147.00

STOXX Europe 600 down 0.07% to 408.97

MXAP down 0.9% to 163.88

MXAPJ down 1.1% to 524.25

Nikkei down 0.5% to 23,293.91

Topix down 0.5% to 1,699.36

Hang Seng Index down 2% to 26,346.49

Shanghai Composite down 0.6% to 2,871.98

Sensex down 0.7% to 40,839.78

Australia S&P/ASX 200 down 0.3% to 6,846.00

Kospi down 1.5% to 2,087.96

German 10Y yield fell 1.2 bps to -0.373%

Euro down 0.02% to $1.1007

Italian 10Y yield rose 2.7 bps to 0.888%

Spanish 10Y yield fell 1.4 bps to 0.397%

Brent futures down 0.6% to $63.49/bbl

Gold spot little changed at $1,456.71

U.S. Dollar Index little changed at 98.37

Top Overnight News from Bloomberg

Banks have been wrong for most of the past 10 years with their krona predictions as Sweden’s economy, often seen as a barometer for global trade, found itself battered by recessionary fears and tariff wars

The worst is over for the European economy, according to buyers of exchange-traded funds. Investors have poured $1.5 billion into U.S. ETFs focused on European assets in November, data compiled by Bloomberg show

Chancellor Angela Merkel’s government plans to tighten restrictions on foreign takeovers amid growing concerns China is scooping up Germany’s technology jewels

The ECB should integrate climate change and energy transition into its forecasting and assessment of collateral, Governing Council Member Villeroy said

For the last year, Saudi Arabia has largely turned a blind eye to cheaters within the OPEC+ alliance, cutting its own output more than agreed to offset over-production from the likes of Iraq and even Russia. Now, Riyadh’s had enough

Police said they had lifted lifted their blockade on Hong Kong Polytechnic University after officers cleared a campus that’s been besieged for nearly two weeks amid a violent standoff with demonstrators

Asian markets were mostly subdued after the holiday closure stateside for Thanksgiving Day and amid continued trade uncertainty, despite a more conciliatory tone from China’s State Council and with the retaliation so far to US President Trump’s Hong Kong bill signing seen as a mere slap on the wrist. ASX 200 (-0.3%) initially prodded record levels but with gains later reversed by underperformance in miners and the largest weighted financials sector, while the opening gains for the Nikkei 225 (-0.5%) eventually succumbed to the pressure from currency flows and substandard data in which Industrial Production matched its worst contraction since January last year. Hang Seng (-2.0%) and Shanghai Comp. (-0.6%) declined as markets second-guessed China’s retaliation measures for the HK bill and after PBoC’s inaction this week resulted to a CNY 300bln net liquidity drain, with the losses in the Hong Kong benchmark exacerbated as all its components resided in negative territory following the recent increased IPO activity and as the city braces for a resumption of protests over the weekend. Finally, 10yr JGBs weakened in an extension of yesterday’s post-2yr auction selling pressure and with demand also kept subdued by the lack of BoJ presence in the market, as well as mixed Japanese data releases.

Top Asian News

Ambani Said in Talks to Sell News Assets to Times Group

BOJ Cuts Buying Range for 10-25 Year Bonds in December Plan

India Braces for Shock GDP as Modi Scrambles to Spur Economy

Indiabulls Erases Gain as Court Allows More Time for Findings

Major European bourses (Euro Stoxx 50 +0.1%) are mixed and off of morning lows, after a broadly negative Asia-Pac session during which sentiment was undermined by the hangover from recent trade concerns. Month-end factors coupled with low liquidity also seem likely to distort the price action. Sector performance is mixed with no clear standout. In terms of individual movers; Ocado (+12.4%) shares shot higher on the news that the Co. has agreed to a partnership with Japanese grocer Aeon, the companies first partnership in the region. Elsewhere, positive broker moves for Bouygues (+1.5%) and Scout24 (+0.8%) saw their respective shares supported. In terms of the laggards; St James’ Place (-3.5%) fell to the bottom of the Stoxx 600 following a downgrade at Goldman Sachs. Elsewhere, negative broker movers put Remy Cointreau (-1.2%), Air France (-1.5%) and Royal Mail (-2.2%) shares under pressure. Separately, E.ON (+2.0%) posted strong Q3 earnings, which were roughly 20% above the prior year’s figures, while the Co. also raised the outlook on the completion of Innogy’s (-0.2%) transaction. On which note, Innogy and E.ON presented proposals for the restructuring of Innogy’s Npower unit – which could lead to 4.5k in job losses and closures of a number of call centres. Finally, Renault (+1.4%) shares are supported amid reports that the Co. is reportedly mulling a program that would boost efficiency with Nissan and Mitsubishi.

Top European News

German Unemployment Unexpectedly Drops as Optimism Edges Up

Euro- Area Inflation Quickens, But Remains Far Below ECB’s Goal

Merkel’s Fate Rests With Disgruntled Members of Battered Partner

Ocado Expands Into Asia With Japan Robot Warehouse Deal

In FX, the major outperformers and movers outside of recent ranges, as an improvement in NZ consumer confidence gives the Kiwi a further fillip following more upbeat business sentiment or less bleak to be precise on Thursday. Nzd/Usd is extending gains above 0.6400 and threatening to break free from the 0.6425 level that has been keeping the pair tethered, while Eur/Sek is now eyeing the psychological 10.5000 mark in wake of firmer than forecast Swedish Q3 GDP that has given the Swedish Krona a fundamental lift on top of renewed bullish technical impetus after the cross retreated through 10.5500 chart support more convincingly.

GBP – Far from hero to zero, but Sterling is losing more of its YouGov pre-UK election poll mojo with negative month end cross winds also weighing on the Pound via Eur/Gbp demand. Cable has now lost grip of the 1.2900 handle and briefly slipped below the 21 DMA (1.2884), while 0.8500 continues to cushion the aforementioned cross.

AUD/EUR/JPY/CAD/CHF – All narrowly mixed vs the Dollar that is still doing well if not quite defying gravity amidst rebalancing models flagging various strains of Greenback selling for month end (DXY holding ‘comfortably’ above 98.000 and towards the upper end of a 98.412-301 range). The Aussie is trying to piggy-back its Antipodean counterpart, but remains top heavy into 0.6800 and Aud/Nzd has pulled back from 1.0550 again after weaker than expected private sector credit data overnight. In similar vein, Eur/Usd seems destined to stay anchored around 1.1000 with yet more hefty option expiries hampering attempts to the upside vs decent technical support limiting losses beneath the big figure, while mixed Eurozone data is broadly being ignored. Elsewhere, Usd/Jpy, Usd/Cad and Usd/Chf are also treading familiar ground in narrow parameters of 109.60-45, 1.3292-79 and parity-0.9980 respectively, with the Yen torn between conflicting Japanese data and standard BoJ policy rhetoric from Governor Kuroda, Franc largely shrugging off a decline in the Swiss KOF indicator and Loonie awaiting Canadian GDP along with any USMCA developments for some independent direction.

In commodities, crude markets are subdued (albeit off intraday lows) amid a lack of fresh catalysts, as prices pull back slightly following a strong finish to yesterday’s session. In terms of crude specific news; OPEC’s Economic Commission Board yesterday reportedly suggested that OPEC does not need to implement deeper cuts over H1 2020, premised on the assumption that the surplus in production over the first half of the year will be later offset by a deficit in the latter part of the year. This is broadly in line with expectations for the outcome of the 5-6 December meeting, as indicated by multiple sources in recent weeks. Elsewhere, Russian oil production for the month of November stood at 11.24mln BPD, according to IFAX citing sources, which is relatively unchanged from the prior month. In terms of metals, gold prices are subdued and well within recent ranges; the precious metal managed to meander just under yesterday’s 1458.32/oz high, but has since pulled back slightly, and remains well off this week’s USD 1470/oz high. Copper prices, meanwhile, continue to slip, with poor Industrial Output/Production readings out of Japan and South Korea overnight doing little to help sentiment.

US Event Calendar

Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

Yesterday was spent mostly waiting to see if we’d get a response from China following President Trump’s signing of legislation expressing support for Hong Kong protestors. Other than a statement from the foreign ministry and a tweet from the editor-in-chief of the state run Global Times saying that China was considering putting the drafters of the law on a no-entry list, we didn’t really get any. So we’ll have to wait and see if this impedes “phase one” trade negotiations. This morning Asian markets are down again with the Nikkei (-0.38%), Hang Seng (-1.98%), Shanghai Comp (-0.64%) and Kospi (-1.32%) all in the red. The declines in Hong Kong and China are being led by drugmakers over unconfirmed reports that China will accelerate a centralized procurement program that’s driving down generic drug prices. Elsewhere, futures on the S&P 500 are down -0.28%.

The decline for the Kospi overnight follows the Bank of Korea decision to keep interest rates unchanged; however, they did cut growth forecasts in 2019 and 2020, both by 0.2pp to 2.0% and 2.3%, respectively.

In other news, BoJ governor Kuroda said that the central bank needs to pay attention to downside risks to the economy, especially stemming from overseas, while adding that, to reach its inflation target, the BoJ will continue with powerful monetary easing. He also said that it’s important to weigh costs and benefits of policy and added that Japan needs structural reforms, deregulation to boost its potential growth. Yields on 10y JGBs are up +1.6bps to -0.089%.

As for the rest of markets yesterday, in Europe we ended with modest declines across most equity markets. The STOXX 600 closed down -0.14% for its first decline in a week with volumes close to 40% below average with the auto sector (-0.78%) down notably. The DAX, CAC and FTSE MIB closed -0.31%, -0.24% and -0.61% respectively while the FTSE 100 was -0.18%. European Banks also nudged down -0.69% despite bond markets being a touch weaker. Indeed 10y Bunds were +1.3bps and BTPs +2.9bps higher in yield. The latter seemingly underperforming post a 10y auction, which saw a drop in demand. In FX, having touched a high of $1.2951 on Thursday evening following the release of the YouGov MRP mode, Sterling faded slightly through yesterday’s session and is trading at 1.2914 this morning.

Staying with FX, the rout for the Chilean Peso (-1.17%) continued yesterday and along with the Colombian Peso hit a new all-time low. The Brazilian Real (+1.17%) did manage to strengthen but also remains a shade above its own record low as political turmoil in the region continues following anti-government demonstrations. Meanwhile, Chile’s central bank said overnight that it will sell as much as $10bn on the spot market and provide an equal amount of currency hedges to arrest the currency’s decline. EM FX is now down -0.64% for the year with 4 of the biggest 6 decliners being currencies in LatAm.

Lastly, yesterday’s data included a softer-than-expected November HICP print in Germany (-0.8% mom vs. -0.7% expected) although it was noted that the year-over-year rate printed ahead of expectations (+1.2% yoy vs. +1.1% expected) seemingly due to a methodology change for package holidays. Meanwhile in Spain CPI was also a tad softer than expected (0.0% mom vs. +0.1% expected). Elsewhere the October M3 money supply reading for the Euro Area stayed put at +5.6%, which was a tenth ahead of expectations while finally November confidence indicators for the Euro Area on average improved from October.

Looking at the day ahead, with no data due out of the US the focus will be here in Europe where we’re due to get the preliminary CPI report for the Euro Area, France and Italy, October money and credit aggregates data in the UK, November unemployment and October retail sales in Germany and final Q3 GDP revisions for France. Away from that we’re expecting to get some comments out of the ECB, specifically from Hernandez de Cos, Villeroy and Guindos.

The Thrombeys are a sprawling family that’s rich in nitwits. Not so much the old man, wealthy crime novelist Harlan Thrombey (Christopher Plummer), who is in any case suddenly dead, but his heirs and in-laws, all hungry for an inheritance and just the kind of devious schemers you’d expect to find in a country manor murder mystery such as this.

Writer-director Rian Johnson, still being nerd-roasted for his smash-hit Star Wars installment, The Last Jedi, happily acknowledges his influences in constructing Knives Out—primarily Agatha Christie novels and the movies made from them (Death on the Nile, Evil Under the Sun), as well as pictures like Gosford Park and the super-tricky Deathtrap. Johnson appears to be having a lot of fun here, as does the large and star-filled cast, so it’s a shame that, despite the story’s many incidental pleasures, it never really takes off.

The plot is ridiculously complicated, of course. There are several prime suspects in the murder of Harlan Thrombey, whose throat was slit on the night of his 85th birthday party. The man assigned to crack the case (assigned by whom is another mystery) is Benoit Blanc (Daniel Craig), “the last of the gentleman sleuths,” as someone amusingly puts it. Blanc is a Poirot-like outsider, a southerner who sounds as if he’s mumbling through a mouthful of magnolias. He’s about as far removed from James Bond as Craig could possibly get, and the actor seems to be enjoying the respite (although he doesn’t do a lot of virtuoso crime-solving of the sort you might expect).

In time-honored fashion, Blanc assembles his suspects in a large drawing room filled with vast carpets and elaborate bric-a-brac. (The movie’s production design is impressively deluxe.) Among those submitting to the detective’s questioning are Harlan’s wimpy son Walt (Michael Shannon), who has a cushy sinecure running his father’s publishing house; his daughter Linda (Jamie Lee Curtis), a real-estate shark whose business has long been financed by her dad; Linda’s husband Richard (Don Johnson), a dodgy customer whose own misdeeds will eventually be made clear; Harlan’s widowed daughter-in-law Joni (Toni Collette), a “lifestyle guru” constantly in need of money; and Harlan’s smug, smirky grandson Ransome (Chris Evans, playing way against type).

Also nibbling around the edges of the plot are a pair of ineffective cops (LaKeith Stanfield and Noah Segan), the family’s sharp-eyed housekeeper (Edi Patterson), and Walt’s creepy alt-right son (Jaeden Martell).

And then there’s Marta Cabrera (Ana de Armas), Harlan’s live-in nurse, the only good-hearted person on the scene. Marta is physically incapable of deceit—she vomits if compelled to tell a lie—so Blanc recruits her to be his Watson. (“The game is afoot, eh?”)

A lot of stuff happens, Lord knows, and the story’s frenzied twists and turns never stop. There’s a secret entrance to the house, a suspiciously missing toxicology report, some lethally mixed-up meds, and a bit of rote political nudging (about illegal immigrants and children in cages) that the movie could have done without. There’s also an amusing car chase and wonderfully caustic performances by Collette and Evans. But Armas doesn’t bring a lot of spark to what is in fact the movie’s central character and Craig sometimes seems like a bystander as the action unfolds around him. His character may have a Southland drawl, but it’s so weirdly thick that you begin to wonder if he’s actually from anywhere at all.

from Latest – Reason.com https://ift.tt/2Du3HZ2

via IFTTT

Morgan Stanley Fires FX Traders Overt $140 Million Loss

2019 has been a ‘volatile’ year for traders in the foreign exchange markets, if not for actual currencies.

After early year chaos amid trade wars, global recession fears, and sanctions threats, FX volatility tumbled, spiked, and then collapsed (along with every other asset class vol) as central banks stomped their boots on the throat of uncertainty.

Source: Bloomberg

And with FX vol at or near record lows, traders have been unwilling to chase the dollar’s performance as much as they were earlier in the year…

Source: Bloomberg

But, according to Bloomberg, quite a few Morgan Stanley traders were heavily-positioned the wrong way.

According to “people with knowledge of the matter”, Morgan Stanley fired or placed on leave at least four traders amid a probe into alleged mismarking of trades linked to emerging-market currencies.

Emerging Market FX (broadly) has collapsed in 2019…

Source: Bloomberg

And along with it, EM FX vol has crashed to near record lows…

Source: Bloomberg

According to the report, the bank is investigating whether the suspected mismarking helped conceal a loss of $100 million to $140 million.

As Bloomberg details, and for those who are unfamiliar that his exact same process has been taking place in corporate bonds for decades (although woe to anyone who is caught doing it), in so-called mismarking the value placed on securities doesn’t reflect their actual worth. The probe at Morgan Stanley revolved around relatively more complex products such as FX options instead simple underlying cross, which may have given them confidence that the layer of complexity would prevent getting caught.

It did not.

Making matters worse, Morgan Stanley’s FX options desk has struggled this year amid a slump in volatility, the swings in currencies that can generate profits for traders, even across more unruly emerging markets such as Turkey:

Source: Bloomberg

Then again, who can blame them for losing money in this market as EM FX vol has collapsed irrationally amid soaring policy uncertainty. Maybe the “criminal” traders in question can cop a plea and agree to rat out the central bankers who are responsible for the current disastrous state of “markets.” Surely the associated depositions and discovery alone will be worth the price of a bid/ask spread.

Dennis Gartman To Stop Writing “The Gartman Letter”

“There was a great disturbance in the 3x inverse Gartman ETF, as if millions of human, algo, quant and HFT trader voices cried out in terror and were suddenly silenced.”

It appears that the Gartman Letter, the world’s most valuable letter for market contrarians, is sadly coming to an end.

A SPECIAL ANNOUNCEMENT REGARDING THE FUTURE OF THE GARTMAN LETTER:

After a great deal of thought and with an even greater deal of sadness, we have decided to cease producing The Gartman Letter as of December 31st of this year after three and one half wonderful decades of rising each morning at 1:00 a.m. to write and complete our duties.

During this time we have witnessed the advent and ubiquity of the fax machine; the arrival and even the greater ubiquity of the internet; the virtual demise of some of the world’s great newspapers; the wonder of Microsoft Word; of Adobe Acrobat et al. We’ve lived through the fall of the Berlin Wall; the creation of the European Union; the rise and retirements of friends and clients; hurricanes and power outages and all the while having missed less than a handful of TGLs over those decades.

But there comes a time when retirement calls. My right hand is weary and is giving me problems, making daily writing a good deal more difficult than it had been in the past. Too, the simple sums of information available to everyone have made our efforts difficult and yet easier at the same time. Add to this the increased tax and regulation requirements and we’ve chosen to stop doing business as we have in the past.

We are thinking about our future…maybe a bi-weekly bulletin or perhaps podcasts and other technologies that may be available to us in the future to try to make certain that we are not immediately forgotten by our myriad friends in the capital and commodity markets. Also we like the television, radio and print interviews that we do and wish not to give that up and won’t, if called upon. And, of course, our weakening golf game needs some far greater attention!

We want to take the time to thank everyone who has been a friend to TGL over the years and they are far, far too many to mention. This has been a truly wonderful experience over the decades and we shall always consider ourselves uncommonly fortunate. If the next decades are only half as great as the last three and one half, how lucky shall we be?

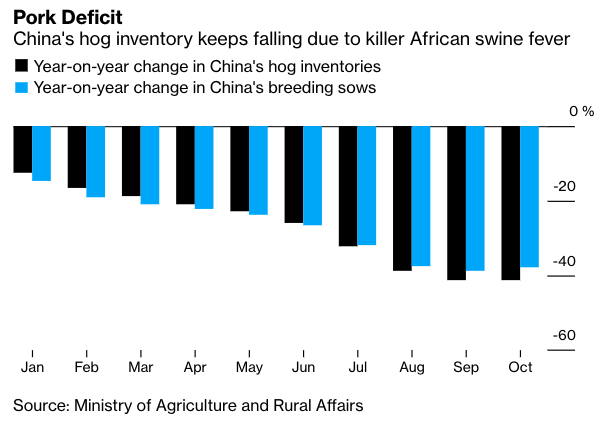

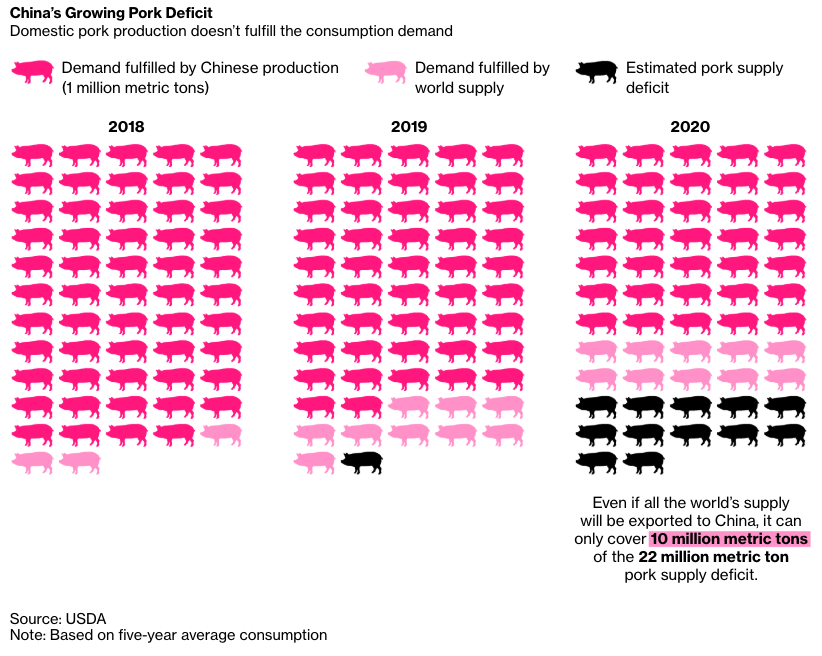

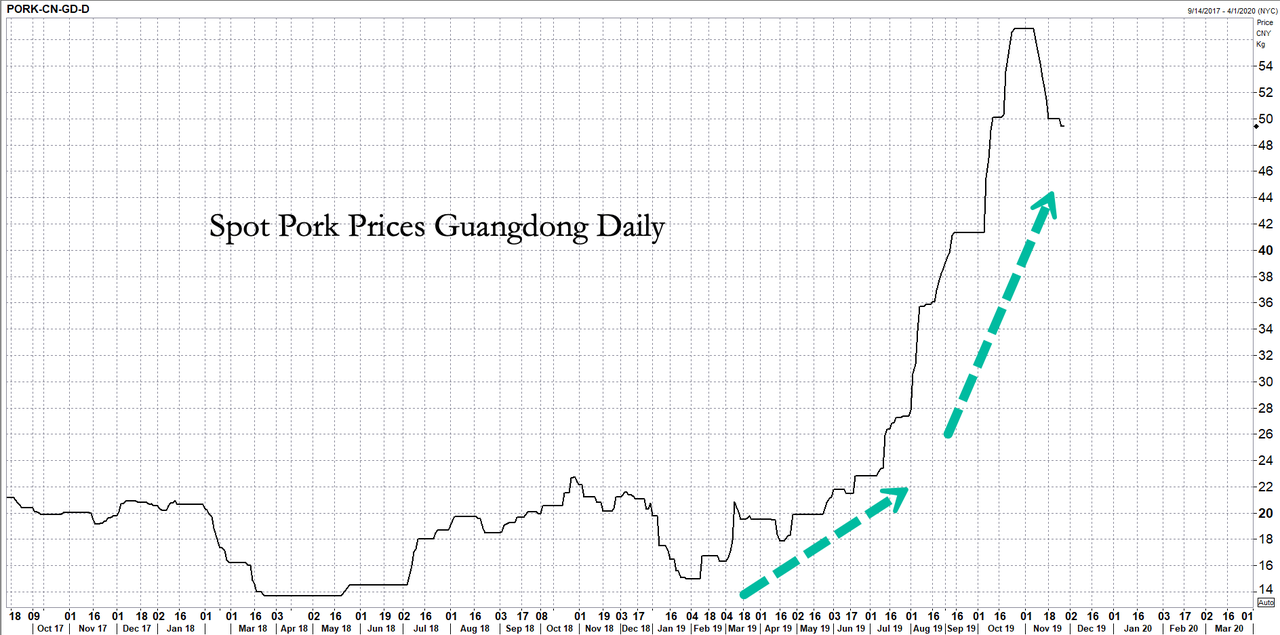

There Are Not Enough Pigs In The World To Fill China’s Pork Hole

African swine fever has wiped out herds of pigs all over China – by some estimates more than half – and it now appears the global supply of pork might not be able to satisfy the country’s demand in early 2020, reported Bloomberg.

The Ministry of Agriculture and Rural Affairs published new data on Friday that shows the number of hogs in China dropped 40% in Oct. YoY. The decline is mostly due to the African swine fever and farmers culling their herds to prevent further transmission of the dangerous disease.

The disease has spread from Africa to Europe, and currently across Asia, and are fears pork supplies around the world are dwindling and might not be able to fill China’s deficit. Just this week, the Dutch government announced plans to shrink its hog industry (why? because apparently pigs smells – the government says fewer pigs means less odor nuisance and a better living environment, as well lower emissions of ammonia, in the European country with the most cows and pigs relative to land area).

In southern China’s Guangdong province, spot prices have jumped 230% since January, with much of the gains seen in late summer as the disease gained momentum and farmers were forced by the government to cull more pigs.

The jumped in spot prices wasn’t just because domestic pork production collapsed, but the government has had difficulty sourcing products from abroad. It seems the world doesn’t have enough pork for China.

The trade war, until recently, prevented Chinese importers from souring US pork. China has found alternative sourcing in South America, signing trade deals with Argentina and Brazil for agriculture products. Though it could take months for the pork to arrive in China, the pork deficit will likely increase in early 2020, and spot prices will move higher.

Food inflation and a decelerating economy in China are a recipe for socio-economic problems in 2020.

The Thrombeys are a sprawling family that’s rich in nitwits. Not so much the old man, wealthy crime novelist Harlan Thrombey (Christopher Plummer), who is in any case suddenly dead, but his heirs and in-laws, all hungry for an inheritance and just the kind of devious schemers you’d expect to find in a country manor murder mystery such as this.

Writer-director Rian Johnson, still being nerd-roasted for his smash-hit Star Wars installment, The Last Jedi, happily acknowledges his influences in constructing Knives Out—primarily Agatha Christie novels and the movies made from them (Death on the Nile, Evil Under the Sun), as well as pictures like Gosford Park and the super-tricky Deathtrap. Johnson appears to be having a lot of fun here, as does the large and star-filled cast, so it’s a shame that, despite the story’s many incidental pleasures, it never really takes off.

The plot is ridiculously complicated, of course. There are several prime suspects in the murder of Harlan Thrombey, whose throat was slit on the night of his 85th birthday party. The man assigned to crack the case (assigned by whom is another mystery) is Benoit Blanc (Daniel Craig), “the last of the gentleman sleuths,” as someone amusingly puts it. Blanc is a Poirot-like outsider, a southerner who sounds as if he’s mumbling through a mouthful of magnolias. He’s about as far removed from James Bond as Craig could possibly get, and the actor seems to be enjoying the respite (although he doesn’t do a lot of virtuoso crime-solving of the sort you might expect).

In time-honored fashion, Blanc assembles his suspects in a large drawing room filled with vast carpets and elaborate bric-a-brac. (The movie’s production design is impressively deluxe.) Among those submitting to the detective’s questioning are Harlan’s wimpy son Walt (Michael Shannon), who has a cushy sinecure running his father’s publishing house; his daughter Linda (Jamie Lee Curtis), a real-estate shark whose business has long been financed by her dad; Linda’s husband Richard (Don Johnson), a dodgy customer whose own misdeeds will eventually be made clear; Harlan’s widowed daughter-in-law Joni (Toni Collette), a “lifestyle guru” constantly in need of money; and Harlan’s smug, smirky grandson Ransome (Chris Evans, playing way against type).

Also nibbling around the edges of the plot are a pair of ineffective cops (LaKeith Stanfield and Noah Segan), the family’s sharp-eyed housekeeper (Edi Patterson), and Walt’s creepy alt-right son (Jaeden Martell).

And then there’s Marta Cabrera (Ana de Armas), Harlan’s live-in nurse, the only good-hearted person on the scene. Marta is physically incapable of deceit—she vomits if compelled to tell a lie—so Blanc recruits her to be his Watson. (“The game is afoot, eh?”)

A lot of stuff happens, Lord knows, and the story’s frenzied twists and turns never stop. There’s a secret entrance to the house, a suspiciously missing toxicology report, some lethally mixed-up meds, and a bit of rote political nudging (about illegal immigrants and children in cages) that the movie could have done without. There’s also an amusing car chase and wonderfully caustic performances by Collette and Evans. But Armas doesn’t bring a lot of spark to what is in fact the movie’s central character and Craig sometimes seems like a bystander as the action unfolds around him. His character may have a Southland drawl, but it’s so weirdly thick that you begin to wonder if he’s actually from anywhere at all.

from Latest – Reason.com https://ift.tt/2Du3HZ2

via IFTTT

Stephen R. Platt believes that the so-called Opium War of 1839–1842 was one of the most “shockingly unjust wars in the annals of imperial history.” The central question, he writes in Imperial Twilight, is a moral one: How could Britain—a country that had just abolished slavery—so hypocritically turn around and push drugs onto “a defenceless China”?

Platt, a University of Massachusetts Amherst historian, thus joins a long list of writers who have portrayed the Opium War as one of the worst crimes of the modern era. Karl Marx, for one, believed that the slave trade was merciful compared to the opium trade. Forty years ago, John King Fairbank, doyen of modern Chinese studies, called the opium trade “the most long-continued and systematic international crime of modern times.”

If this were so, one wonders why the production, trade, and use of opium were entirely legal in such places as Turkey, Egypt, Persia, and India for decades both before and after the Opium War. One wonders why the drug’s cultivation spread in the second half of the nineteenth century to the Netherlands, France, Italy, and the Balkans. One also wonders why, as Virginia Berridge revealed in her pioneering 1981 book Opium for the People, up to 100 tons of the substance was imported every year into England, where it was readily available until the end of the 19th century, commonly administered even to children in the form of laudanum.

The author claims that opium was recreational in China but medicinal elsewhere. But this is a dubious distinction, one not even made in Britain—a country where, before 1900, alcohol, tobacco, and opium were all viewed as both palliatives and stimulants. In the absence of modern medicine, all too often pleasure meant absence of pain, especially in a poor and largely agrarian country such as China. Opium allowed ordinary people to relieve the symptoms of such endemic diseases as dysentery, cholera, and malaria and to cope with pain, fatigue, hunger, and cold.

And the vast majority of opium users in China were not the desperate addicts portrayed by proponents of prohibition. They were occasional, intermittent, light, and moderate users—a far cry from Thomas De Quincey, an English writer who famously ingested truly gargantuan quantities of the substance. Platt quotes De Quincey’s Confessions of an English Opium-Eater at length to invoke the horrors of addiction, but surely he realizes that De Quincey was one of the 19th century’s most eccentric addicts. (Then again, he appears ignorant of the fact that, despite the title of his book, De Quincey did not eat but rather drank opium, mixed with a bottle or two of strong spirits per day in his periods of heavy dependence.)

Readers, Platt tells us, have long been treated to triumphant accounts of how the West vanquished a “childish people who dared to look down on the British as barbarians,” with China appearing as no more than a caricature of “unthinking traditions and arrogant mandarins.” The author, instead, promises to “give motion and life” to the changing China of the early 19th century.

I am not sure which “triumphant accounts” he has in mind. There is no dearth of historians who have written engagingly about the events leading up to the Opium War. Dozens of titles fit the bill, some going back more than half a century. Surely Frederic Wakeman Jr.’s Strangers at the Gate (1966) is a model, in style and in substance, although the book is apparently not worthy of mention in Platt’s bibliography. Another classic is Peter Ward Fay’s well-crafted The Opium War, 1840–1842 (1975), a 500-page magnum opus with all the telling detail required to bring the era back to life.

What Platt’s book offers is a competent and entertaining, if somewhat meandering, account of British efforts to open up the Qing empire to foreign trade. Foreign merchants were confined to a small settlement in the southern port of Canton, where they had to negotiate with the government officials who maintained a virtual monopoly over the market. The import of opium, as well as saltpeter, salt, and other commodities, was forbidden, as were exports of a range of other products, from rice, copper, and iron to timber.

In consequence, there was a thriving black market from which many profited, not least the officials who used their monopoly to line their own pockets. For decades before the Opium War, foreigners tried to break through these constraints. Platt devotes several chapters to these adventurers, traders, missionaries, and diplomats: the failed Macartney embassy of 1793, the Scottish merchants William Jardine and James Matheson, the linguist and scholar George Staunton, the British superintendent Charles Elliot. This is well-trodden ground, even if Platt tells his tale ably.

The book’s subtitle is The Opium War and the End of China’s Last Golden Age. This is somewhat puzzling. China, Platt reminds us in a short paragraph, was a powerful, prosperous, dominant country in the 18th century (an empire of “almost unimaginable height”), viewed with admiration by Europeans. But the notion of a golden age rapidly disappears from view as it becomes clear that by the turn of the century, the Qing empire was racked by rebellions, piracy, and corruption on a staggering scale.

Decades of tension in Canton over issues of trade, jurisdiction, and sovereignty came to a head in 1839, after the emperor rejected a proposal from his own advisors to legalize and tax opium. His envoy seized a vast amount of the substance and trapped foreign merchants and their families in the settlement of Canton without charge or trial. Up to this point, no British official disputed the Qing empire’s right to control its borders and determine which foreign goods should be admitted. But now, even George Staunton, who opposed the opium trade and had spent his career defending the sovereignty and dignity of the Qing, believed that force was required.

Others objected to retaliation: In a well-known speech reproduced in Imperial Twilight, a young William Gladstone declared in the House of Commons that he could not think of “a war more unjust in its origins.”

A single frigate was sent to protect merchants and civilians, followed by an expeditionary force. By 1841, following more talking than fighting, both sides had negotiated a deal in Canton, which London and Beijing then rejected. Time and again, as Julia Lovell showed in her 2014 book The Opium War: Drugs, Dreams and the Making of China, the British tried to inform their adversaries of their demands, but the dispatches the emperor’s underlings in Canton sent to the court in Beijing were fictitious. Two years into the war, the emperor still thought it was a mere skirmish and wondered where exactly England was on the map.

The Treaty of Nanjing was finally signed in 1842. It did not mention opium. England had gone to war to protest the arbitrary detention of British subjects and the confiscation of their private property. By 19th century standards, this was a legitimate reason for military engagement. Not until after the fall of the Qing in 1911 did a new generation of nationalists in the Republic of China come to see the agreement as unequal.

Even before the treaty was ratified, the former president of the United States, John Quincy Adams, commented in a lecture before the Massachusetts Historical Society that opium was a “mere incident to the dispute but no more the cause of the war than the throwing overboard of the tea in Boston harbour was the cause of the North American revolution.” It is a conclusion shared by many subsequent historians, including Peter Ward Fay and Frank Welsh, but evidently not by Stephen Platt.

from Latest – Reason.com https://ift.tt/2L27hgX

via IFTTT