Law-abiding gun owners who complied with New Zealand’s mandatory gun buyback program and surrendered their assault weapons to the government discovered Monday that their privacy had been compromised by poor website security.

This week, the police website for New Zealand’s mandatory military-style semi-automatic assault weapons (MSSA) buyback was taken offline after a gun dealer told law enforcement that he was able to access users’ personal information through the site. This info included the names, addresses, dates of birth, gun license numbers, and bank account details of users. As many as 38,000 site users may have been affected, and the website will remain shut down until police can guarantee that the information is secure. Law enforcement currently believes that only dealer users had access to the sensitive information, not the public.

New Zealand implemented its gun buyback program after a March 15 attack on two mosques in Christchurch left 51 people dead. Six days after the attack, Prime Minister Jacinda Ardern announced that all military-style firearms, like the ones the killer had used, would be banned, in addition to large-capacity magazines and any parts that would make a gun readily convertible into an MSSA (such as telescoping stocks). The ban passed through New Zealand’s parliament, 119-1, in April. Those who owned these guns or accessories were ordered to surrender them to the government.

The Guardianreported that the security breach was made public when the Council of Licensed Firearms Owners (COLFO), a gun lobby group, revealed that 15 people had reached out to them claiming that they were able to access users’ personal information through the buyback portal. The group posted screenshots of the information one of the users had shared with COLFO (the identifying information has been redacted).

COLFO tells Reason that the organization is currently in the process of contacting the 19 individuals who claim to have been able to access sensitive information on the buyback website to “ascertain the extent of the access” each individual had.

New Zealand’s deputy police commissioner, Mike Clement, placed the blame for the breach on SAP, the German company that custom-built the website for the buyback. Clement said that SAP had unintentionally provided some users with greater access to other users’ personal data than should have been possible when it updated the site and that he could not “offer an absolute ironclad” assurance that users’ information had not been abused.

SAP has since claimed responsibility, stating that 66 gun dealer users had accidentally been given access to other users’ private information as a result of human error last week.

New Zealand’s buyback program gives citizens the option to surrender their weapons to gun dealers after they fill out an online form with details about their firearms. New Zealand has no reliable registration records of MSSAs because previous laws made the country’s registration process relatively easy to skirt, so the form helps fill in those gaps. The individual then surrenders their arms to a dealer, who turns the surrendered items over to law enforcement. Dealers are not supposed to have access to individuals’ personal information. In other words, law enforcement betrayed the trust of gun owners who were doing their best to comply with a government-mandated confiscation program.

Roughly 43,000 weapons had been turned in through the buyback so far. The program seeks to completely eradicate the estimated 175,000 MSSAs in private hands by December 20, after which police will begin prosecuting people who have not surrendered their weapons. With only 18 days of the buyback left, only about 25 percent of the guns estimated to be in private hands have been voluntarily surrendered. The owners of the other 75 percent of New Zealand’s MSSAs could face up to three years in prison or a $4,000 fine if they fail to meet the deadline.

The police already think that many people will refuse to surrender their newly-banned firearms. A data breach compromising the personal information of gun owners who complied with the law will surely encourage further noncompliance from those who were already resistant to the idea of turning in their guns.

from Latest – Reason.com https://ift.tt/34KJWZb

via IFTTT

“Don’t Panic”: CRE Crisis Hits The UK As Largest Property Fund Suddenly Halts Redemptions

Earlier this week, ECB vice president Luis De Guindos, speaking in an interview with El Mundo, offered a surprisingly candid take on how the ECB is distorting capital market, saying that while “we can still increase bond purchases or lower interest rates further, which means that we still have the same tools available” he added that “what is happening is that the secondary effects are becoming more tangible.”

Specifically, De Guindos said he is “worried by risk taking in the asset management sector against the background of low interest rates.” According to the ECB VP, the risk is that “supervision in this sector is not comparable with that in the banking sector. There is a risk. If they are asked for units to be paid out they have to do so within two or three days. I see a potential risk of liquidity imbalance. That is what worries me the most at the moment.”

De Guindos’ warning was spot on, because just a few hours earlier, UK fund manager M&G announced it had suspended redemptions and trading in its £2.5 billion Property Portfolio, which is marketed to retail investors, after it was unable to sell properties fast enough, particularly given its concentration on the retail sector, to meet the demands of investors, and was facing “unusually high and sustained outflows” it blamed on Brexit and the retail downturn.

As the FT reported, the M&G fund was the first major open-ended property fund to halt redemptions in this way since the crisis in the sector that caused seven funds to “gate” in 2016 following the Brexit referendum — which we profiled three years ago as one of the most high-profile market consequences of the vote to leave the EU.

First, a little history: first it was the shocking junk bond fiasco at Third Avenue which led to a premature end for the asset manager, then the three largest UK property funds suddenly froze over $12 billion in assets in the aftermath of the Brexit vote; two years later the Swiss multi-billion fund manager GAM blocked redemptions, followed by iconic UK investor Neil Woodford also suddenly gating investors despite representations of solid returns and liquid assets, then it was the ill-named, Nataxis-owned H20 Asset Management decided to freeze redemptions; finally Arrowgrass joined the list when it wrote down the value of an illiquid investment (the Dramland amusement park) by a whopping 70% overnight.

By this point, a pattern had emerged, one which Bank of England Governor Mark Carney described best when he said that investment funds that promise to allow customers to withdraw their money on a daily basis are “built on a lie.” At roughly the same time, the chief investment officer of Europe’s biggest independent asset manager agreed with him, because while for much of 2019 the biggest risk bogeymen were corporate credit, leveraged loans, and trillions in negative yielding debt, gradually consensus emerged that investment funds themselves – and specifically their illiquid investments- gradually emerged as the basis for the next financial crisis.

“There is no point denying we are faced with a looming liquidity mismatch problem,” said Pascal Blanque, who oversees more than 1.4 trillion euros ($1.6 trillion) as the CIO of Amundi SA, adding that the prospect of melting liquidity is one of “various things keeping me awake at night.”

* * *

Fast forward to today, when in what may be the first harbinger of a UK commercial real estate crisis, M&G, a London-listed asset manager, said it has been unable to sell properties fast enough, particularly given its concentration on the retail sector, to meet the demands of investors who wanted to cash out. The investor “run” led the fund to suspend any redemption requests in its £2.5 billion ($3.2 billion) Property Portfolio arriving after midday on Wednesday.

“In recent months, unusually high and sustained outflows from the M&G Property Portfolio have coincided with a period where continued Brexit-related political uncertainty and ongoing structural shifts in the UK retail sector have made it difficult for us to sell commercial property,” M&G said in a statement.

“Given these circumstances, we have now reached a point where M&G believes it will best protect the interests of the Funds’ customers by applying a temporary suspension in dealing.”

In addition to Brexit worries, M&G’s fund has been hit by its large holdings in retail property, a sector hit by retailer failures and value drops. According to the FT, the fund – which shrunk by £1.1 billion so far this year – holds 37.5% of its portfolio in retail warehouses, shopping centres, designer outlets and standard retail, based on its latest fact sheet, plus another 2.5% in supermarkets, a more stable part of the sector. The same fund was suspended in July 2016 for four months following the UK’s EU referendum when money flooded out of such funds.

Shares in the company dropped 2.6 per cent to 227.8p following the news, while the value of the property portfolio fund tumbled to the lowest level in 6 years.

Investors in the fund range from armchair, retail investors to institutional investors, dealing with millions of pounds according to the BBC. The fund waived 30% of its annual charge to investors, as they were unable to access their money, although some have called for action from the regulator on such charges.

The decision to suspend the fund, and its feeder fund, was taken by its official monitor – its authorised corporate director – and the City watchdog has been informed.

“The FCA is working closely with the firms involved to ensure that timely actions are undertaken in the best interests of all the fund’s investors,” a spokesman for the Financial Conduct Authority (FCA) said.

M&G said the suspension would be monitored daily, formally reviewed every 28 days, and would only continue “as long as it is in the best interests of our customers”. This will allow assets to be sold over time, rather than as a fire sale, in order to meet investors’ withdrawal demands. The firm has written to investors to explain the current situation.

UK investors had been shaken in recent months by the demise of previously lauded fund manager Neil Woodford. Woodford Investment Management is in the process of shuttering after Woodford, one of the UK’s most iconic investors, was fired from its flagship fund in October. The case raised questions regarding the oversight of funds which invest in assets that take a long time to sell, but from which investors can withdraw their money from at any time.

The M&G case will make the case stronger for regulators to take a tougher stance on these types of investments.

Meanwhile, investors in the UK have been pulling their money out of other large so-called open-ended property funds, and the FCA has recently introduced daily monitoring of property funds. Yet financial planners have mixed views on whether the M&G suspension could be matched by other funds in the sector.

“Property is a long-term investment and we urge investors not to panic,” said Patrick Connolly of financial advisers Chase de Vere; of course the only word that investors would hear in that sentence is “panic” and there will be a flood of redemptions across the entire investing universe, potentially starting a domino-like freeze up of property funds, similar to that seen in 2016 in the days following Brexit.

“While the M&G fund is suspended, most other providers have far greater liquidity, and less exposure to retail properties, and so are better placed to meet redemptions, as long as there isn’t a mad rush to the exit door.

“Property still remains an asset class which can play an important role in investment portfolios and, when we have some real clarity on Brexit, the prospects for this asset class will hopefully improve.”

However, Ryan Hughes, from AJ Bell, said investors would review their interest in other funds which could lead to “a rush for the exits”. “We could see a wave of suspensions now – several that offer daily redemptions are at risk,” he said.

* * *

Ryan, is of course, right and whether he knows it or not he just described what we previously called a $1.6 trillion ticking time bomb in the market. While we previously discussed “The $1.6 Trillion Ticking Time Bomb In The Market“, the M&G fiasco is merely the latest example of how pervasive investment in hard-to-mark illqiuid assets have become in Europe where money managers from Neil Woodford to H2O Asset Management have come under fire from politicians, regulators and investors. But really it’s the central bankers’ fault: having injected trillions in the market to crush yields and push investors into the riskiest assets, investment firms have had no choice but to venture into harder-to-sell assets such as real estate in a search for yield.

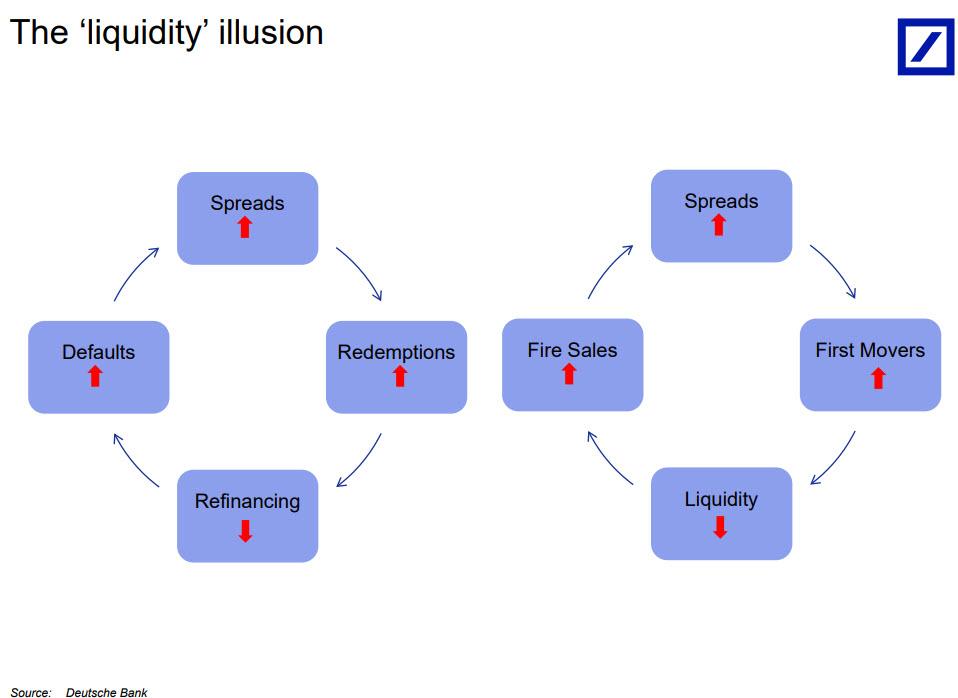

Incidentally, for those wondering if liquidity remains an illusion – a test that can only be confirmed when there is a crash and the market is indefinitely halted, an outcome that is now virtually inevitable – Deutsche Bank has a simple test: it all has to do with the sequence of events unleashed by widening spreads, where redemptions and first movers rush to sell, collapsing the market’s liquidity, freezing refinancings, and resulting in a surge in defaults and firesales, which in turn leads to even wider spreads and so on, until central banks have to step in to short circuit this toxic loop.

This also explains why GAM, Woodford, H20, Arrowgrass and many more funds (in the near future), will be similarly gated once their investors discover there is no liquidity to sell into and the only “real time” liquidity is offered to those who have a “first seller mover advantage”, to wit:

If investors anticipate severe losses on the fund’s investments, they could be incentivised to “run for the exit” to be the first to redeem their shares.

The first-mover advantage in open-ended funds arises because losses on asset sales to meet redemptions are incurred by investors which remain in the fund.

As in a ‘bank run’, the asset manager is, in principle, forced to sell assets in a fire sale in order to meet its short-dated liabilities

This dramatic imbalance of asset holdings at market making banks and buyside “bagholders” of illiquid securities, is now posing a major problem for regulators, something the Bank of England acknowledged in a working paper published earlier this month, and highlighted by Mark Gilbert, to wit: “as the funds industry has supplanted banks as a source of credit in the past decade, households and companies have benefited from a useful alternative source of financing. But, the report warned, we don’t know how this market-based system will respond under stress.”

Modelling such a scenario “can generate an adverse feedback loop in which lower asset prices cause solvency/liquidity constraints to bind, pushing asset prices lower still,” the BOE found. In other words, the new market structure may be worse than the old.

The feedback loop discussed by the BOE is the one we showed in the chart above.

And, as recent notable fund “gates” and/or collapses have shown, the difficulty for asset managers in such an eventuality is finding sufficient cash to repay exiting investors while preserving the structure of the portfolio without distorting market prices, according to Amundi’s Blanque.

According to Bloomberg, part of Amundi’s response to this seemingly intractable issue is to include liquidity buffers in its portfolios, which may mean holding securities such as German bunds and U.S. Treasuries, which should always trade freely. But the industry needs to come up with a common definition so that liquidity is included along with risk and return when assessing a portfolio’s robustness, Blanque says. Additionally, this band aid only works for modest redemptions. A wholesale liquidation would crush even the most “buffered” up fund.

For now, asset managers have to cope with what Blanque called “the sacred cow” – although a better phrase would be “constant risk” of allowing clients to withdraw funds on a daily basis.

“It is a bomb, given the risks of liquidity mismatch,” he warns. “We don’t know if what is sellable today will be sellable in six months’ time.”

That’s not the only we don’t know. As Blanque concluded, “we don’t know the channels of transmission, we don’t know how the actors will act. It is uncharted territory.”

And that, precisely, is why central banks can never again allow risk asset prices to drop: the alternative means gating not one, or two, or a hundred funds, but halting the entire market, because once everyone start selling and price discovery finally returns to a market that has been dominated by central banks for the past decade, several generations of traders and investors who have grown up without price discovery will be shocked to discover just where “fair” market prices reside.

A veteran officer with the Los Angeles Police Department (LAPD) captured himself fondling a corpse on his own body camera.

The Los Angeles Timesreports that an unnamed officer in the Central Division responded to a call about a dead woman in a residential apartment. After arriving, the officer and his partner concluded that the woman was in fact deceased. When the unnamed officer’s partner returned to the patrol car to retrieve something, the disturbing incident occurred.

The offending officer turned his body camera off and fondled the dead woman’s breasts. When he turned the camera on again, a portion of his actions were captured. When an LAPD body camera is activated, a two-minute buffer saves any audio and visual that occurred prior.

LAPD officials found the footage in a random inspection. Last month, Chief Michel Moore announced that the department would review footage to identify instances of poor policing training and bias.

Josh Rubenstein, a spokesperson for the LAPD, told the Times that an administrative investigation was “immediately launched” and the unnamed officer was placed on leave.

from Latest – Reason.com https://ift.tt/2LoFHe7

via IFTTT

Hunter Biden’s Lawyer Abruptly Quits After ‘Father-Of-The-Year’ Blows Off Child Support Hearing

Hunter Biden’s lawyer abruptly quit on Monday after the former Vice President’s son and Ukraine energy expert failed to show up for a child support hearing regarding his out-of-wedlock child with a D.C. stripper from Arkansas.

According to the Daily Mail, lawyer Dustin McDaniel – the former Attorney General for Arkansas, filed a motion to withdraw after he says Biden’s personal lawyer ‘advised’ him that he was being discharged.

“(C)ounsel will take all steps reasonably practical to protect defendant’s interests and make every effort to ensure an efficient and judicious transition for new counsel,” wrote McDaniel.

Lunden Roberts, 28, is suing Biden for $11,000 in legal fees, plus child support payments after a DNA test revealed he was the father. Biden, meanwhile, says he’s broke an has requested that the judge seal his financial records due to “significant debts” despite having been paid vast sums of money while sitting on the board of Ukrainian gas company Burisma.

Hunter was ordered by Judge Don McSpadden to provide at least three years of tax returns before he could reach a decision on monetary support for the child, whose name and gender have not been revealed. Biden has requested that his financial records be sealed to avoid public ’embarrassment’ over claims of ‘significant debts,’ according to the Mail.

In addition to preventing the disclosure of Biden’s alleged debts, it is thought information on his business ventures, investments, expenses, taxes and personal property valuations would also be included in the documents. –Daily Mail

Of course, Hunter’s financial records could also reveal the extent of payments received while sitting on the board of Burisma, which paid his consulting firm $83,333 per month.

Biden filed a motion for a Protective Order of his financial records in the Arkansas Circuit Court of Independence [last] Wednesday, citing fears that such information would be used ‘maliciously’ by the media if disclosed publicly.

‘The likelihood that [Biden’s] private records will be used in an inappropriate or malicious manner for reasons that have absolutely nothing to do with these proceedings is exceedingly high and should not be tolerated by the court,’ the filing reads.

Any such disclosures, Biden’s attorneys claim, would furthermore cause their client ‘undue prejudice, annoyance, embarrassment, and/or oppression.’

‘Due to the extraordinary circumstances surrounding the parties involved in this matter, it is in the interest of justice and necessary for a Protective Order to be in place,’ Biden’s attorney Dustin McDaniel stated.

Joe Biden is accused of abusing his position as then-Vice President to have Ukraine’s top prosecutor fired while he was conducting a wide-ranging investigation of Burisma and its owner, Mykola Zlochevsky – the country’s former minister of ecology who is accused of tax violations, money laundering, and self-dealing. His investigation was closed after 10 months, with the fired prosecutor – Viktor Shokin, claiming it was because he was investigating Biden.

President Trump’s request that Ukraine investigate is currently at the heart of US impeachment proceedings led by House Democrats.

Hunter’s child support case, meanwhile, has been adjourned until January 7.

“Whatever you think – he got elected because he pointed out huge troubles in our economy and democracy!”

No one should be in the least little bit surprised at yesterday’s market tremblor following Trump’s big reveal – he might not make a trade deal this side of the election! Quel Horror. (Sarcasm Alert) Stocks gapped down, and bonds rallied strongly – a knee jerk reaction. But it is more than that. No one should be particularly surprised a China deal is off the table. (Bloomberg seem to think it is already back on). If you had been watching closely, it should have been obvious the “we’re going to get a deal” story could only be extended so long. The question is how deep will this current wobble go? Could it become a correction? Or even a full Christmas crash?

Speaking to investors yesterday, it definitely felt like something is breaking. It’s not about the China/US spat – that is well understood. My clients are not stupid and understand how the mood in Beijing has changed – they see the Chinese don’t trust Trump and they are increasingly confident of their perception that although he barks and blusters, he is unlikely to act or bite. That will inform their political choices – including responses to Hong Kong and Taiwan.

What’s breaking is confidence in the current Trump narrative. The market’s concern is that the market narrative that’s driven stocks and bonds higher through the year is played out. It was based around two factors:

That Trump will remain disruptive, but a positive market force, juicing prices via tweets, tax cuts and short-term fixes because his re-election depends on the perception of economic strength, and

Central Banks will continue to positively distort markets via accommodative policy and monetary experimentation because they can’t face the prospect of market weakness.

It’s worked wonderfully well right through 2019 – thus far. But now the narrative is breaking down, and the next thread is becoming increasingly important. Trump’s credibility with markets could be waning. Central banks are more focused on fiscal policy, and the market is becoming blasé about the Orange Being…

The bottom line is we may be past Peak-Trump. For the last three years, markets have been collectively happy to coat-tail his actions. I don’t believe many market participants ever had much time for him – at a personal level, (and the views I hear on his personality, or his actions as a blusterer, a finagler, a bully, and much much worse are more polarised than on any other politician – even Boris isn’t so divisive.) The collective market views was that as long as he kept delivering, fine… the market could put up with him.

Although we’re all privately concerned about the ongoing White House Shenanigans and Impeachment, you’d have been foolish not to follow Trump’s market higher. What’s not to like about a US president willing to juice the market with tax cuts and calls for the Fed to ease? If the president says a Trade deal is about to happen, then why not follow the market higher? And you do.. till it stops..

Now every trader who played that game is looking around to see what the rest of the market still believes. It’s like an Emperor’s new clothes moment – you knew the fat orange guy was stark-b*ll*x naked, but while everyone else said he was wearing clothes, you went along with it. If everyone walks away at the same time, then the market is potentially in trouble.

A trade deal with China is highly unlikely – it hasn’t been likely for months. Trump pretends it doesn’t matter, and has opened new fronts against South America on Steel and Yoorp on Digital Taxes. The reality is the Great Negotiator looks to have misjudged China – rather than the Chinese being intimidated by his deal making brilliance, they don’t trust him as far as they can throw him. When the market loses confidence in his ability to keep delivering upside, then he’s in real trouble.

What’s the new narrative?

Fiscal policy is nailed on. There is the possibility of a rising inflationary threat as the credibility of the Government is roiled. And its now about corrections and the impact of new sustainability themes as the overriding investment story.

This throws a new spin into the market. Market participants are not stupid – they follow the trade war narrative closely, they’ve been analyzing China, US and Global Trade for signs of deeper weakness. What worries them is confidence. The market has been trading higher and higher on the back of a strong belief. Now it is breaking and none of them are that surprised. Clearly Trump will be the major driver next year ahead of election, but at the moment the market is trying to figure out where we’ve gone…

NATO

NATO is 70 years old today. It appears weak and fractured – with the main players driven apart as the result of a host of factors: Trump’s undiplomatic calls for greater spending, a newly resurgent France bidding for the power under Macron as Germany heads into introspection as Merkel dithers into retirement, and the unsinkable aircraft carrier of the UK disengaging from Europe following Brexit. Does it matter? Are the Ruskies really a threat?

Don’t bet against it. They have signalled they are. In October the Russian “surged” 10 attack submarines into the Atlantic. It might have been 8 because I’m told Nato’s ultra-sophisticated SOSUS line lost 2 of the brand new and ultra-silent Russian hunters. Nato’s response was poor – aircraft from around the alliance were gathered and a few old frigates sent out. The once mighty ASW capabilities of the Royal Navy are tied up protecting its two new aircraft carriers, and the fleet is short of manpower and assets.

The Russians are sending a clear message: 10 subs in the Atlantic could stop all Trade. Absolutely. What is Nato going to do about it?

The Lech house after it was destroyed by police seeking to apprehend a suspected shoplifter (court exhibit).

The Institute for Justice, a prominent libertarian public interest firm, has taken up case of Lech v. City of Greenwood Village, the recent decision in which a federal appellate court ruled that the Takings Clause of the Fifth Amendment does not require the government to compensate an innocent property owner whose house was destroyed by police seeking to apprehend a suspected shoplifter. I analyzed the issues at stake in the case here. As I explained in that post, the ruling by the US Court of Appeals for the Tenth Circuit has considerable backing from precedent, but is nonetheless seriously flawed. I also, in that post, address the pragmatic argument that we must deny compensation in such cases in order to avoid unduly burdening law enforcement operations.

Andrew Wimer of the Institute for Justice has a good discussion of the case in an article in Forbes, which also describes what IJ hopes to achieve:

Leo Lech’s home was destroyed. The windows and doors were all blown out, glass strewn inside and outside. But it wasn’t an act of God, it was an act of the local police department.

Mind you, no one in the household had committed a crime. Instead, a suspect on the run fled there randomly. He’d been chased by police for miles after stealing a shirt and two belts from a local Walmart.

With the suspect armed and ignoring police communications, the SWAT team of the Greenwood Village Police Department in Colorado started systematically taking out windows and doors using explosives and an armored vehicle. They fired tear gas canisters into the home….

The occupants of the home were Leo Lech’s son, the son’s girlfriend, and her 9-year old son, who now found themselves homeless. In apprehending a suspect wanted for a few dollars’ worth of goods, the police did damage costing Lech $400,000. While insurance covered some of the home repairs, it didn’t cover the full amount of the value of the home or personal possessions…. And just recently, a federal appeals court ruled that he couldn’t be compensated for his loss under the Fifth Amendment’s takings clause: “nor shall private property be taken for public use, without just compensation….”

Lech’s loss in court is an outrageous story…, but Lech isn’t alone. For decades, innocent property owners have struggled to receive compensation when law enforcement agencies damage their property. It is an uphill climb even in states like Colorado, where the constitution specifically says that government should pay when property is damaged….

The Institute for Justice is now taking up Lech’s case and has asked the entire 10th Circuit Court of Appeals to reconsider the decision of the three-judge panel. Regardless of whether the appeals court reverses the decision, it is likely that the U.S. Supreme Court will be asked to consider whether the U.S. Constitution protects property owners. Leo Lech’s house was destroyed and there was no compensation.

IJ has litigated (and often prevailed) in numerous other constitutional property rights cases, including a recent Supreme Court victory in Timbs v. Indiana, which ruled that the Excessive Fines Clause of the Eighth Amendment applies to state governments, and constrains civil asset forfeitures. Hopefully, their involvement will increase the likelihood of getting this decision reversed, though I fear it may be an uphill struggle. At the very least, IJ will ensure that the Lech family has topnotch pro bono representation.

NOTE: I have worked with the Institute for Justice on a variety of previous property rights cases, always on a pro bono basis. I do not have any involvement in this one, though it is possible I will write an amicus brief at some point (which would also be a pro bono project).

from Latest – Reason.com https://ift.tt/2LmfexH

via IFTTT

WTI Hovers Above $58 After Bigger-Than-Expected Crude Draw

Oil prices, led by hope-ridden trade-deal headlines and OPEC+ chatter, have soared back above $58, erasing Friday’s losses…

But, after API’s reporting a bigger than expected crude draw, all eyes are on the official government data this morning…

API

Crude -3.72mm (-1.5mm exp) – biggest draw since September

Cushing -251k

Gasoline +2.931mm

Distillates +794k

DOE

Crude -4.856mm (-1.5mm exp) – biggest draw since August

Cushing -302k

Gasoline +3.385mm

Distillates +3.063m – biggest build since July

DOE data shows an even bigger crude draw than API reported (and an even bigger build in gasoline stocks)…

Source: Bloomberg

US crude production held at record highs…

Source: Bloomberg

And WTI was unsure where to go now that the algos ran the stops…

Bloomberg Intelligence Senior Energy Analyst Vince Piazza concludes: “Increasing demands among OPEC+ participants for deeper supply curbs confirm our concern about slowing demand. Additional cuts of 400,000 barrels a day would raise reductions to 1.6 million, while stronger compliance would further aid sentiment. Extending the deal for six months into 2H20 would provide the market with greater clarity.”

The Lech house after it was destroyed by police seeking to apprehend a suspected shoplifter (court exhibit).

The Institute for Justice, a prominent libertarian public interest firm, has taken up case of Lech v. City of Greenwood Village, the recent decision in which a federal appellate court ruled that the Takings Clause of the Fifth Amendment does not require the government to compensate an innocent property owner whose house was destroyed by police seeking to apprehend a suspected shoplifter. I analyzed the issues at stake in the case here. As I explained in that post, the ruling by the US Court of Appeals for the Tenth Circuit has considerable backing from precedent, but is nonetheless seriously flawed. I also, in that post, address the pragmatic argument that we must deny compensation in such cases in order to avoid unduly burdening law enforcement operations.

Andrew Wimer of the Institute for Justice has a good discussion of the case in an article in Forbes, which also describes what IJ hopes to achieve:

Leo Lech’s home was destroyed. The windows and doors were all blown out, glass strewn inside and outside. But it wasn’t an act of God, it was an act of the local police department.

Mind you, no one in the household had committed a crime. Instead, a suspect on the run fled there randomly. He’d been chased by police for miles after stealing a shirt and two belts from a local Walmart.

With the suspect armed and ignoring police communications, the SWAT team of the Greenwood Village Police Department in Colorado started systematically taking out windows and doors using explosives and an armored vehicle. They fired tear gas canisters into the home….

The occupants of the home were Leo Lech’s son, the son’s girlfriend, and her 9-year old son, who now found themselves homeless. In apprehending a suspect wanted for a few dollars’ worth of goods, the police did damage costing Lech $400,000. While insurance covered some of the home repairs, it didn’t cover the full amount of the value of the home or personal possessions…. And just recently, a federal appeals court ruled that he couldn’t be compensated for his loss under the Fifth Amendment’s takings clause: “nor shall private property be taken for public use, without just compensation….”

Lech’s loss in court is an outrageous story…, but Lech isn’t alone. For decades, innocent property owners have struggled to receive compensation when law enforcement agencies damage their property. It is an uphill climb even in states like Colorado, where the constitution specifically says that government should pay when property is damaged….

The Institute for Justice is now taking up Lech’s case and has asked the entire 10th Circuit Court of Appeals to reconsider the decision of the three-judge panel. Regardless of whether the appeals court reverses the decision, it is likely that the U.S. Supreme Court will be asked to consider whether the U.S. Constitution protects property owners. Leo Lech’s house was destroyed and there was no compensation.

IJ has litigated (and often prevailed) in numerous other constitutional property rights cases, including a recent Supreme Court victory in Timbs v. Indiana, which ruled that the Excessive Fines Clause of the Eighth Amendment applies to state governments, and constrains civil asset forfeitures. Hopefully, their involvement will increase the likelihood of getting this decision reversed, though I fear it may be an uphill struggle. At the very least, IJ will ensure that the Lech family has topnotch pro bono representation.

NOTE: I have worked with the Institute for Justice on a variety of previous property rights cases, always on a pro bono basis. I do not have any involvement in this one, though it is possible I will write an amicus brief at some point (which would also be a pro bono project).

from Latest – Reason.com https://ift.tt/2LmfexH

via IFTTT

Musk On Trial, Day 1: “He Didn’t Literally Mean To Sodomize Me With A Submarine”

Elon Musk had his first day on the stand yesterday as part of his defamation trial for calling British cave diving hero Vern Unsworth “pedo guy”.

Based on live running commentary from various Twitter sources that were at the trial, including BuzzFeed’s Ryan Mac, The Verge’s Elizabeth Lopatto and $TSLAQ’s very own @TeslaCharts, the day lacked a lot of the fireworks that many expected, with even some Tesla skeptics even starting to speculate that Musk may be able to walk.

After jury selection, Musk was the first person to take the stand. He told the jury that the comments he made about Unsworth were “wrong and insulting” and that he didn’t know who Unsworth was at the time, according to Bloomberg. Musk claimed that Unsworth’s critical comments about Musk were “an unprovoked attack on what was a good-natured attempt to help the kids.”

Musk continued by saying: “I thought he was just some random, creepy guy that the media interviewed. So, I insulted him back.”

Musk claimed his statement of “pedo guy” wasn’t meant to be taken literally, telling the jury while on the stand: “I knew he didn’t literally mean to sodomize me with a submarine, just as I didn’t literally mean he was a pedophile.”

Musk also briefly engaged in a small spat with Unsworth’s attorney, L. Lin Wood, before the judge directed the two sides to cut it out.

Unsworth’s attorneys focused on subsequent statements made by Musk. “Bet ya a signed dollar it’s true,” Musk said, re-upping the insult a month later before asking someone on Twitter, “You don’t think it’s strange he hasn’t sued me?”

Musk then claimed Unsworth traveled “to Chiang Rai for a child bride who was about 12 years old at the time”, before calling him a “child rapist”.

Regardless of this line of questioning, Tesla skeptic @TeslaCharts did not seem impressed with Wood’s job of examining Musk. He tweeted live from the courtroom:

After today I’m considering sitting for the LSAT. I’d make a killing as an attorney if this is the benchmark.

One of Unsworth’s attorneys, Taylor Wilson, said in his opening statement that Musk’s Tweets caused Unsworth “tremendous shame”.

Wilson said: “Mr. Unsworth did the only thing he could. He filed a lawsuit against Musk for accusing him of being a pedophile in what should have been the proudest moment of his life.”

Musk’s lawyer, Alex Spiro, claimed Unsworth can’t prove damages. “This case is about an argument between two men exchanging insults,” Spiro said during his opening remarks. He also claimed that Unsworth was at court to “milk his 15 minutes of fame”.

After the day came to a close, Musk used a decoy car to escape the courtroom proceedings and avoid the media.

Unsworth helped play a key role in saving 12 boys and their soccer coach who were trapped in the Tham Luang Nang Non cave in Thailand in July 2018.

Musk had proposed his own solution for the rescue, embarking on a boastful public quest to construct a device that could help rescue the trapped children. But, ultimately, the rescue was done by actual professionals and without the help of Musk.

Musk’s submarine

In a post-rescue interview with CNN, Unsworth laughed off Musk’s proposed solution and told the billionaire he could “stick it where it hurts”, disregarding Musk’s effort as a “PR stunt”.

Musk, like a child who had just been bested on an elementary school playground, fired back by calling Unsworth names and insisting that he was a pedophile both on Twitter, and in communications with a reporter at BuzzFeed.

Unsworth obviously contends that Musk’s statements are false and that he should pay punitive and other damages for harming his reputation.

The trial is expected to last another 4 to 5 days.

Blaming everyone but Kamala Harris for her presidential campaign’s collapse. The conversation surrounding Kamala Harris’ exit from the 2020 presidential race has been reaching some ridiculous places since the California senator announced she was dropping out yesterday. Harris herself blamed billionaires, basically, while supporters and pundits expanded the blame to also include sexism, racism, biased media coverage, and other issues beyond the candidate or her campaign’s control.

If you’re wondering whether Democrats picked up any introspection since Hillary Clinton’s 2016 loss was chalked up to sexism, racism, third parties, Bernie bros, and such…the signs aren’t looking so good.

On social media and cable news, commentators keep coming back to alleged advantages enjoyed by other candidates—personal wealth, less scrutiny of their criminal justice records, etc.—to supposedly explain why Harris was forced to exit early (and to complain how unfair it is that folks like Michael Bloomberg, Pete Buttigieg, and Sen. Amy Klobuchar remain in the race).

Watching Kamala Harris drop out of the presidential race to avoid going into debt the same month Michael Bloomberg shoved his way into the competition with his billions means we should probably have a conversation about money in politics. But we probably won’t.

But all of these explanations fall apart with the slightest scrutiny. Whatever setbacks Harris may have faced based on her race and sex, they pale in comparison to the challenges she and her campaign staffers brought upon themselves.

Staff and supporters have cited the senator’s strategy, debate performances, and the flaws of her top advisors for why the campaign failed to sustain either popular or establishment liberal support.

The campaign certainly got its share of support from corporations and rich donors to start with, sustaining Harris through several Democratic debate cycles. So, the fact that former New York City Mayor Michael Bloomberg may be able to “buy his way in” to the upcoming debate by blasting the nation with a concentrated bout of self-funded campaign ads hardly seems like the stinging indictment that some want it to be.

Get back to me if Bloomberg and all his cash have any shot at getting near the White House—or even a second debate stage. But for now, Bloomberg’s brief moment in the spotlight means nothing, and it’s especially absurd to suggest he somehow knocked Harris out of the polls. Her numbers had been steadily declining for months before Bloomberg entered the race.

Some people have taken to blaming the “Kamala Harris is a cop” meme and any criticism of the former prosecutor and state attorney general’s criminal justice record, while positioning these things as unfair gotchas, and maybe even racist. The Independent offers a particularly bad example of this, one that characterizes “Kamala is a cop” criticisms as springing forth in response to her surging popularity and not something that many leftists and libertarians had been saying for a long time.

Others complain that Harris isn’t the only former drug warrior and tough-on-crime politician and yet, for instance, Amy Klobuchar, the senator from Minnesota, hasn’t seen the same level of scrutiny over her prosecutor past. Former Vice President Joe Biden hasn’t been hit constantly for the 1994 Crime Bill (though he has been hit some).

For all the (justified) critique of Kamala Harris record, Klobuchar was also a prosecutor who hasn’t faced a fraction of that scrutiny, Biden still leading despite writing the Crime Bill and Pete is up in the polls after his police force killed a black man during the campaign. https://t.co/jpp04C8f2s

Most of the candidates have some bad criminal justice points on their records, of course. Klobuchar, Biden, and others should have to answer for their carceral ways (with Biden’s burden bearing more recent examples than the crime bill, for what it’s worth). But Harris is the only candidate who explicitly positioned her campaign around law-and-order themes, running with the tagline “Kamala Harris, For the People” (a callback to her time as a district attorney) and repeatedly emphasizing her “progressive” prosecutor past.

Harris all but wore a big sandwich board sign saying “ASK ME ABOUT MY HISTORY AS A COP” and then was completely unprepared when anyone did, with the campaign blaming bigotry for folks noticing the very things Harris herself kept harping on.

A lot of Harris fans are holding out hope that she’ll find a spot on someone’s ticket as a vice president. But this may be a bit delusional, considering the spectacular flaming out of her campaign and the fact that both Harris and her people seem to divide more than they unite.

Harris allies have told me that they’re worried about her viability as a VP pick because her sister seems to control so much of her operation and that’s led to bad decision-making and that won’t fly on the bottom of the ticket https://t.co/kyKjcswpVg

Harris could have technically held on a little longer—as Anna Massoglia of Open Secrets points out, she had more than $10 million in funds left. There’s still time for her to qualify for the next debate. A candidate with her credentials and hype could, with the right messaging, still outlast the likes of Tom Steyer and exit respectably closer to the top of the tier.

Choosing to leave now is a strategic decision—no more need to attack potential future allies, no need to fumble around with wishy-washy messaging any longer—since all those excess campaign donations can now go to Harris’ next senate race.

Dropping out of 2020, Kamala Harris says "I’m not a billionaire. I can’t fund my own campaign."

FEC filings show her presidential campaign had $10.5M left on hand, which she can use for her next Senate election.

Financial disclosure puts her net worth at $1.89 MILLION to $6M+

Biden said he had “mixed feelings” about Harris’ campaign ending. “Sheisa first-rate intellect, a first-rate candidateandarealcompetitor,” he told ABC News.

FREE MINDS

Twitter’s new Terms of Service contain some cause for worry. “The changes amount to about 10 lines scattered through the 12-page document,” notes XBIZ. “While some of them are mere clarifications from the previous TOS, and one paragraph concerns the Twitter Vulnerability Reporting Program, there’s one change in the terms of service that should concern those interested in the company’s control over the content that one’s followers see. In a nutshell: Twitter has explicitly reserved the right to shadowban, under the legalese of ‘limit distribution or visibility of any Content on the service.'”

In the current TOS, Twitter reserves the right “to create limits on use and storage at our sole discretion at any time” and to “remove or refuse to distribute any Content on the Services, suspend or terminate users, and reclaim usernames without liability to you.”

The new TOS adds to this the right to “limit distribution or visibility of any Content on the service.”

FREE MARKETS

The economic case for sex work decriminalization. As the debate over decriminalizing prostitution becomes louder and “part of a broader rethinking of the criminal justice system,” opponents still worry “that prostitution is inherently violent and decriminalization would worsen the exploitation of women.” But “economic evidence—and theory” says otherwise, writes Karl Smith at Bloomberg Opinion. Smith looks at a study from economists Scott Cunningham, Gregory DeAngelo, and John Tripp:

Economists studied Craigslist, which from 2002 to 2010 gradually introduced an “erotic services” section that allowed sex workers to advertise directly and anonymously on the internet. The staggered rollout allowed the economists to measure the impact on each market as the service expanded. As expected, the market for sex workers expanded rapidly. More important, according to the 2019 paper, the expansion of Craigslist into a market “led to a 10% to 17% reduction in female homicides.” To be clear, that figure is not homicides among sex workers — which are difficult to measure in real time — but homicides among all women in the area.

This result so astounded the economists that they performed some tests to validate it. It passed them all. Moreover, effects have been demonstrated in other studies. Decriminalization in even parts of a city is associated with double-digit declines in sexual assault. A 2014 study of an inadvertent decriminalization of indoor sex work in Rhode Island from 2003 to 2009 found it resulted in a 30% drop in rapes. This isn’t mere correlation: Both the Rhode Island and Craigslist studies use several methods designed to identify causation.

Today, the House Judiciary Committee considering President Donald Trump’s impeachment “plans to hear from four constitutional scholars about the historical underpinnings of the process,” according toThe Washington Post.

The long tail of responsibility for sex trafficking continues to grow, with a new lawsuit attempting to hold the email marketing service Mailchimp legally responsible for exploitation because it sent an email about a website where an alleged trafficker would later post.

“More than two dozen correctional officers in Baltimore were charged Tuesday with using excessive force on prisoners at state-operated jails,” the Associated Press reports.

from Latest – Reason.com https://ift.tt/33Jspze

via IFTTT

{kind=link}