“Psychology is probably the most important factor in the markets, and one that is least understood.”

– David Dreman

A motive of the financial industry is to blur the lines between investor and trader. I’m convinced it’s to make investors feel guilty for taking control of their portfolios. After all, Wall Street firms ares the experts with YOUR money.

How dare you question them?

Sell to take profits, sell to minimize losses, purchase an investment that fits into your risk parameters and asset allocations; it’s all enough to brand one as ‘trader’ in the buy & forget circles that are paid to push the narrative that markets are on a permanent trek higher and bears are mere speed bumps. Wall Street has forgotten the financial crisis. You can’t afford such a luxury.

And, if you’re a reader of RIA, you’re astute enough to know better.

“You’re a trader now?”

Broker at a big box financial shop.

A planning client called his financial partner to complete two trades. Mind you, the only trades he’s made this year. His request was to sell an investment that hit his loss rule and purchase a stock (after homework completed on riapro.net). His broker was dismayed and asked the question outlined above.

Investors are advised – Be like Warren Buffett and his crew: You know, he’s buy and hold, he never sells! Oh, please.

From The Motley Fool:

Here’s what Berkshire sold in the third quarter:

During the third quarter, Berkshire sold some or all of five stock positions in its portfolio:

750,650 shares of Apple.

31,434,755 shares of Wells Fargo.

1,640,000 shares of Sirius XM.

370,078 shares of Phillips 66.

5,171,890 shares of Red Hat.

What Do Paul Tudor Jones, Ray Dalio, Ben Graham, and even Warren Buffett have in common?

A strict investment discipline.

Despite mainstream media to the contrary, all great investors have a process to “buy” and “sell” investments.

Investment rules keep “emotions” from ruling investment decisions:

Rule #1: Cut Losers Short & Let Winners Run.

While this seems logical, it is one of the toughest tenets to follow.

“I’ll wait until it comes back, then I’ll sell.”

“If you liked it at price X, you have to love it at Y.”

It takes tremendous humility to successfully navigate markets. There can be no such thing as hubris when investments go the way you want them; there’s absolutely no room in your brain or portfolio for denial when they don’t. Investors who are plagued with big egos cannot admit mistakes; or they believe they’re the greatest stock pickers who ever lived. To survive markets, one must avoid overconfidence.

Many investors tend to sell their winners too soon and let losers hemorrhage. Selling is a dilemma. First, because as humans we despise losses twice as much as we relish gains. Second, years of financial dogma have taken a toll on consumer psyche where those who sell are made to feel guilty for doing so.

It’s acceptable to limit losses. Just because you sell an investment that isn’t working doesn’t mean you can’t purchase it again. That’s the danger and beauty of markets. In other words, a stock sold today may be a jewel years from now. I find that once an investor sells an investment, it’s rarely considered again. Remember, it’s not an item sold on eBay. The beauty of market cycles is the multiple chances investors receive to examine prior holdings with fresh perspective.

Rule #2: Investing Without Specific End Goals Is A Big Mistake.

I understand the Wall Street mantra is “never sell,” and as an individual investor you’re a pariah if you do. However, investments are supposed to be harvested to fund specific goals. Perhaps it’s a college goal, or retirement. To purchase a stock because a friend shares a tip on a ‘sure winner,’ (right), or on a belief that an investment is going to make you wealthy in a short period of time, will only set you up for disappointment.

Also, before investing, you should already know the answer to the following two questions:

At what price will I sell or take profits if I’m correct?

–Where will I sell it if I am wrong?

Hope and greed are not investment processes.

Rule #3: Emotional & Cognitive Biases Are Not Part Of The Process.

If your investment (and financial) decisions start with:

–I feel that…

–I was told…

–I heard…

–My buddy says…

You are setting yourself up for a bad experience.

In his latest tome, Narrative Economics, Yale Professor Robert J. Shiller makes a formidable case for how specific points of view which go viral have the power to affect or create economic conditions as well as generate tailwinds or headwinds to the values of risk assets like stocks and speculative ventures such as Bitcoin. Simply put: We are suckers for narratives. They possess the power to fuel fear, greed and our overall emotional state. Unfortunately, stories or the seductive elements of them that spread throughout society can lead to disastrous conclusions.

Rule #4: Follow The Trend.

80% of portfolio performance is determined by the underlying trend.

Astute investors peruse the 52-week high list for ideas. Novices tend to consider stocks that make 52-week highs the ones that need to be avoided or sold. Per a white paper by Justin Birru at The Ohio State University titled “Psychological Barriers, Expectational Errors and Underreaction to News,” he posits how investors are overly pessimistic for stocks near 52-week highs although stocks which hit 52-week highs tend to go higher.

Thomas J. George and Chuan-Yang Hwang penned “The 52-Week High and Momentum Investing,” for The Journal of Finance. The authors discovered purchasing stocks near 52-week highs coupled with a short position in stocks far from a 52-week high, generated abnormal future returns. Now, I don’t expect anyone to invest solely based on studies such as these. However, investors should understand how important an underlying trend is to the generation of returns.

Rule #5: Don’t Turn A Profit Into A Loss.

I don’t want to pay taxes is the worst excuse ever to not fully liquidate or trim an investment.

If you don’t sell at a gain – you don’t make any money. Simpler said than done. Investors usually suffer from an ailment hardcore traders usually don’t – “Can’t-sell-taxes-due” itis.

An investor which allows a gain to deteriorate to loss has now begun a long-term financial rinse cycle. In other words, the emotional whipsaw that comes from watching a profit turn to loss and then hoping for profit again, isn’t for the weak of mind. I’ve witnessed investors who suffer with this affliction for years, sometimes decades.

Rule #6: Odds Of Success Improve Greatly When Fundamental Analysis is Supported By Technical Analysis.

Fundamentals can be ignored by the market for a long-time.

After all, the markets can remain irrational longer than you can remain solvent.

The RIA Investment Team monitors investments for future portfolio inclusion. The ones that meet our fundamental criteria – cash flows, growth of organic earnings (excluding buybacks), and other metrics, are sometimes not ready to be free of “incubation,” which I call it; where from a technical perspective, these prospective holdings are not in a favorable trend for purchase.

It’s a challenge for investors to wait. It’s a discipline that comes with experience and a commitment to be patient or allocate capital over time.

Rule #7: Try To Avoid Adding To Losing Positions.

Paul Tudor Jones once said “only losers add to losers.”

The dilemma with ‘averaging down’ is that it reduces the return on invested capital trying to recover a loss than redeploying capital to more profitable investments.

Cutting losers short, like pruning a tree, allows for greater growth and production over time.

Years ago, close to 30, when I was starting out at a brokerage firm, we were instructed to use ‘averaging down’ as a sales tactic. First it was an emotional salve for investors who felt regret over a loss. It inspired false confidence backed up by additional dollars as it manipulated or lowered the cost basis; adding to a loser made the financial injury appear healthier than it actually was. Second, it was an easy way for novice investors to generate more commissions for the broker and feel better at the same time.

My rule was to have clients average in to investments that were going up, reaching new highs. Needless to say, I wasn’t very popular with the bosses. It’s a trait, good or bad, I carry today. Not being popular with the cool admin kids by doing what’s right for clients has always been my path.

Rule #8: In Bull Markets You Should be “Long.” In Bear Markets – “Neutral” or “Short.”

Whew. A lot there to ponder.

To invest against the major “trend” of the market is generally a fruitless and frustrating effort.

I know ‘going the grain’ sounds like a great contrarian move. However, retail investors do not have unlimited capital to invest in counter-trends. For example, there are institutional short investors who will continue to commit jaw-dropping capital to fund their beliefs and not blink an eye. We unfortunately, cannot afford such a luxury.

So, during secular bull markets – remain invested in risk assets like stocks, or initiate an ongoing process of trimming winners.

During strong-trending bears – investors can look to reduce risk asset holdings overall back to their target asset allocations and build cash. An attempt to buy dips believing you’ve discovered the bottom or “stocks can’t go any lower,” is overconfidence bias and potentially dangerous to long-term financial goals.

I’ve learned that when it comes to markets, fighting the overall tide is a fruitless endeavor. It smacks of overconfidence. And overconfidence and finances are a lethal mix.

We can agree on extended valuations; or how future returns on risk assets may be lower because of them. However, valuation metrics alone are not catalysts for turning points in markets. With global central banks including the Federal Reserve hesitant to increase rates and clear about their intentions not to do so anytime in the near future, expect further ‘head scratching’ and astonishment by how long the current bullish trend may continue.

Rule #9: Invest First with Risk in Mind, Not Returns.

Investors who focus on risk first are less likely to fall prey to greed. We tend to focus on the potential return of an investment and treat the risk taken to achieve it as an afterthought.

Years ago, an investor friend was excited to share with me how he made over 100% return on his portfolio and asked me to examine his investments. I indeed validated his assessment. When I went on to explain how he should be disappointed, my friend was clearly puzzled.

I went on to explain how based on the risk, his returns should have been closer to 200%! In other words, my friend was so taken with the achievement of big returns that he went on to take dangerous speculation with his money and frankly, just got lucky. It was a good lesson about the danger of hubris. He now has an established rule which specifies how much speculation he’s willing to accept within the context of his overall portfolio.

The objective of responsible portfolio management is to grow money over the long-term to reach specific financial milestones and to consider the risk taken to achieve those goals. Managing to prevent major draw downs in portfolios means giving up SOME upside to prevent capture of MOST of the downside. As many readers of RIA know from their own experiences, while portfolios may return to even after a catastrophic loss, the precious TIME lost while “getting back to even” can never be regained.

To understand how much risk to consider to achieve returns, it’s best to begin your investor journey with a holistic financial plan. A plan should help formulate a specific risk-adjusted rate of return or hurdle rate required to reach the needs, wants and wishes that are important to you. and your family.

Rule #10: The Goal Of Portfolio Management Is A 70% Success Rate.

Think about it – Major League batters go to the “Hall Of Fame” with a 40% success rate at the plate.

Portfolio management is not about ALWAYS being right. It is about consistently getting “on base” that wins the long game. There isn’t a strategy, discipline or style that will work 100% of the time.

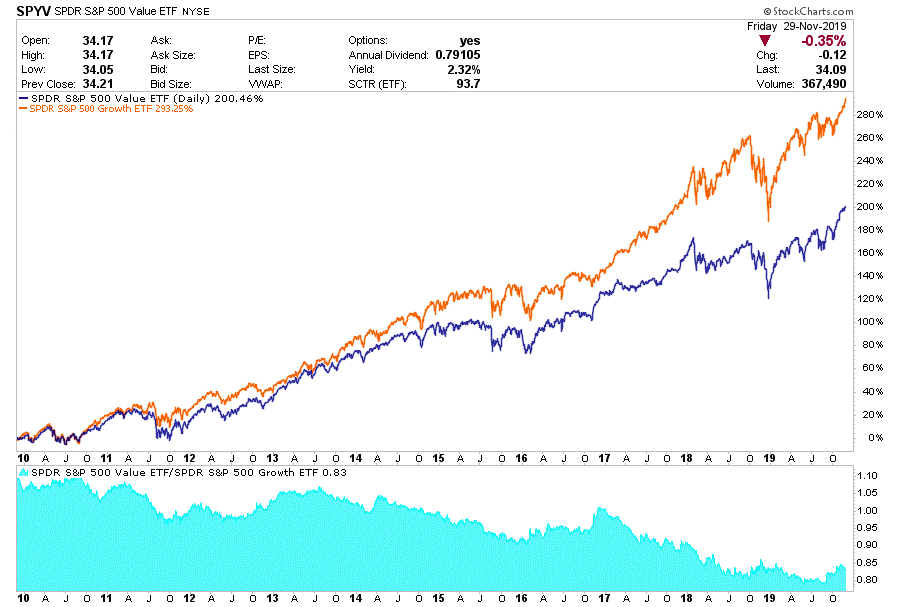

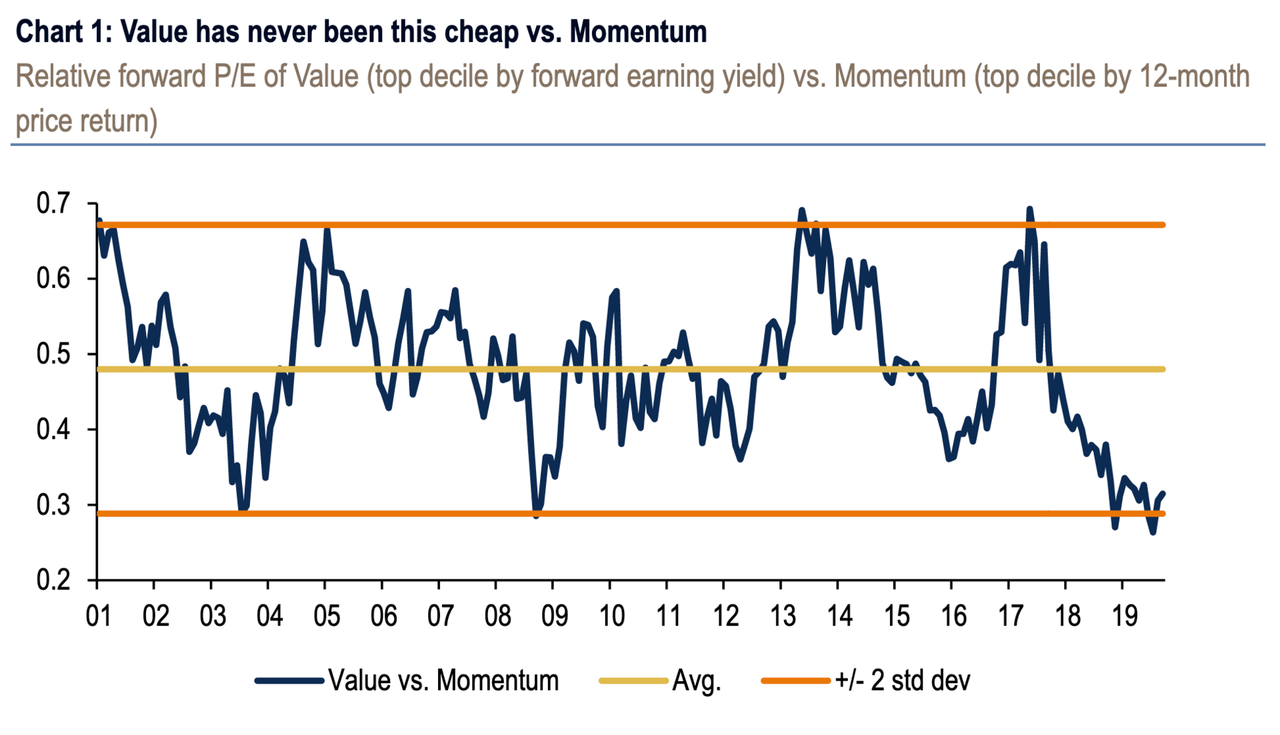

As an example, the value style of investing has been out of favor for a decade. Value investors have found themselves frustrated. That doesn’t mean they should have decided to alter their philosophy, methods of analysis or throw in the towel about what they believe. It does showcase however, that even the most thorough of research isn’t always going to be successful.

Those investors who strayed from the momentum stocks such as Facebook, Amazon, Netflix and Google have paid the price. Although there’s been a resurgence in value investing since October, it’s too early to determine whether the trend is sustainable. Early signs are encouraging.

Chart: BofA Merrill Lynch US Equity & Quant Strategy, FactSet.

A trusted financial professional doesn’t push a “one-size-fits-all,” product, but offers a process and philosophy. An ongoing method to manage risk, monitor trends and discover opportunities.

Even then, even with the best of intentions, a financial expert isn’t going to get it right every time as I outlined previously. The key is the consistency to meet or exceed your personalized rate of return.

And that return is only discovered through holistic financial planning.

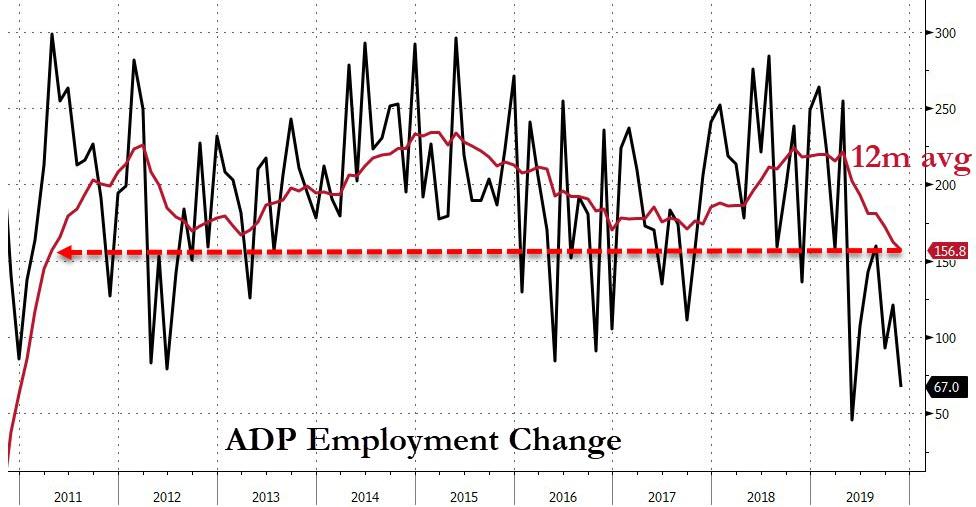

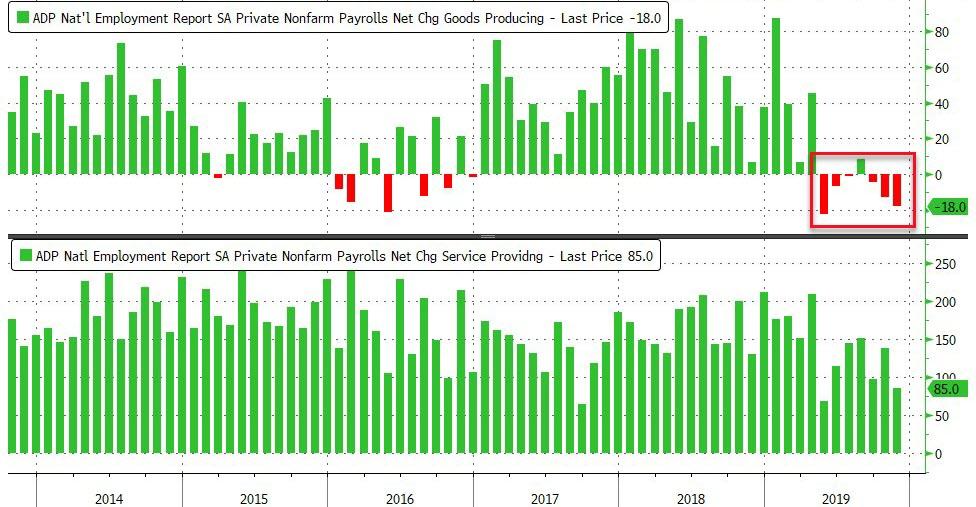

ADP Employment Data Disappoints, Second Lowest Print In A Decade

The last few months have seen ADP employment gains trending lower, alongside the plunge in ISM/PMI survey data (driven by job losses in the goods manufacturing sector), and November’s data confirms that slowdown (just as we warned here).

ADP National Employment Report prints +67k (drastically below expectations of +135k and October’s +121k)

Source: Bloomberg

The Goods-producing sector lost 18k jobs (as services added 85k)…

Source: Bloomberg

“In November, the labor market showed signs of slowing,” said Ahu Yildirmaz, vice president and co-head

of the ADP Research Institute.

“The goods producers still struggled; whereas, the service providers remained in positive territory driven by healthcare and professional services. Job creation slowed across all company sizes; however, the pattern remained largely the same, as small companies continued to face more pressure than their larger competitors.”

Full Breakdown highlights the job losses in Mining, Manufacturing, and Construction…

Mark Zandi, chief economist of Moody’s Analytics, said:

“The job market is losing its shine. Manufacturers, commodity producers, and retailers are shedding jobs. Job openings are declining and if job growth slows any further unemployment will increase.”

On 29 November 2018, defendant Davin Eldridge, a frequent publisher for a Facebook page called “Trappalachia,” entered the Macon County Courthouse. The officer working the metal detector saw defendant had a small tape recorder and “advised [defendant that] he [could] not record inside the courtroom.[“] Defendant acknowledged the officer’s instruction and entered a courtroom. As he did so, defendant bypassed signs posted on the entranceways stating: “BY ORDER OF THE SENIOR RESIDENT SUPERIOR COURT JUDGE: DO NOT use or open cell phones, cameras, or any other recording devices inside the courtrooms. Violations of this order will be contempt of court, subjecting you to jail and/or a fine. Your phone may be subject to seizure and search.”

While in the courtroom, defendant was observed sitting on the second row with a cell phone, holding it “shoulder-chest level” towards the front of the courtroom. The officer went over to defendant and instructed him to put his phone away. Defendant replied, “I’m not doing anything.” The Honorable William H. Coward, Superior Court Judge of Macon County, was presiding over a criminal matter at that time. Judge Coward was informed that a live posting of the hearing in session was streaming from a Facebook page. Based on that information, Judge Coward interrupted the hearing to issue a reminder that recordings of courtroom proceedings were prohibited by law. At the conclusion of the hearing, Judge Coward viewed the Facebook postings by defendant, which included footage of the inside of the courtroom and the prosecutor presenting his closing argument.

Judge Coward then held Eldridge in criminal contempt for violating the restrictions, and the court unanimously upheld the punishment. But, more controversially,

[T]he trial court sentenced defendant to be confined in the Macon County Detention Center for thirty days. Defendant’s sentence was suspended for twelve months, upon six specific conditions for him to meet during his probationary sentence: 1) serve an active sentence of 96 hours; 2) pay the costs of the action; 3) pay a fine of $500.00; 4) draft a 2,000-3,000 word essay on the following subject: “Respect for the Court System is Essential to the Fair Administration of Justice,” forward the essay to Judge Coward for approval, and following approval, post the essay on all social media or internet accounts that defendant owns or controls or acquires hereafter during his period of probation and attributed to defendant, without negative comment or other negative criticism by defendant or others, during said period of probation; 5) not violate any order of Court or otherwise engage in further contemptuous behavior; and, 6) not attend “any court session in Judicial District 30A unless and until his essay has been approved and posted as required herein and he has fully complied with all other provisions of this order.”

The majority, in an opinion by Judge Wanda Bryant, joined by Judge John M. Tyson, upheld this:

Given defendant’s questionable and intentional conduct, his frequent visits to the courtroom, and his direct willingness to disobey courtroom policies, we discern no abuse of discretion in the trial court’s decision to impose conditions on defendant’s probationary sentence. Such conditions are reasonably related to the necessity of preventing further disruptions of the court by defendant’s conduct, and the need to provide accountability without unduly infringing on his rights.

Judge Christopher Brook dissented as to the delete-negative-comments portion of the sentence:

While I agree with the majority that the sentencing judge’s decision to require Defendant, who violated multiple court orders by recording and livestreaming courtroom proceedings on social media, to write an essay about respect for the courtroom and publish this essay on his social media and internet accounts bears a reasonable relationship to Defendant’s criminal contempt of court, and to his rehabilitation for this crime, I do not agree that requiring Defendant to monitor comments made on this essay by third-parties and delete any comments the court might consider critical bears a reasonable relationship to Defendant’s crime or to his rehabilitation, as N.C. Gen. Stat. § 15A-1343 requires….

The [comment-monitoring] condition … holds Defendant responsible for what is essentially the behavior of others; and while there is some truth to the adage that we are only as good as the company we keep, the relevant community in this context is incredibly diffuse, extending through cyberspace….

Our Court has a “settled policy” of avoiding constitutional questions “when a case can be disposed of on appeal without reaching the constitutional issue[.]” Because I vote to vacate the condition of probation requiring Defendant to delete negative comments on the essay [on statutory grounds], I do not delve deeply into what I consider deeply troubling constitutional problems with this condition of probation. Although we generally do not review constitutional questions that have not first been raised in the trial court, suffice it to say that the sentencing judge has not only compelled Defendant to speak within the meaning of the First Amendment, he has compelled Defendant to then continue speaking by censoring the viewpoints of others expressed in response to speech compelled by the court. This compelled speech silencing third-party viewpoints expressed in response to compelled speech raises serious First Amendment concerns.

Note that, under First Amendment precedents, conditions on criminal sentences can indeed restrict or compel speech, though only so long as the conditions are “reasonably related to legitimate penological objectives,” a pretty vague standard under which the government often wins, but sometimes loses.

from Latest – Reason.com https://ift.tt/2r4bvhF

via IFTTT

It’s Day Two of Reason’s annual webathon—and before I ask you for money, I want to thank you.

Over the past 12 months, Reason TV generated a record 29.5 million views at our YouTube channel. Holy hell, that is simply amazing and humbling! That’s more views than Texas has people. And dig this: Viewers watched our documentaries, interviews, and viral videos for a combined 2.7 million hours! If you contributed even a little to those gargantuan totals, I want to thank you personally for watching.

I also want to ask you to make a (tax-deductible!) donation to Reason Foundation, the nonprofit that publishes this website. Go here to donate and see the great swag associated with different giving levels.

Your generous support is the reason we can make amazing videos such as last year’s single biggest hit, “The Insane Battle To Sabotage a New Apartment Building Explains San Francisco’s Housing Crisis,” by Justin Monticello. Justin’s film, which has pulled nearly 900,000 views at YouTube, documents the insanity gauntlet run by Bob Tilman, who spent five years and $1.4 million to earn the right to turn his coin-operated laundromat into an apartment building in one of the most over-zoned, hyper-expensive cities on the planet. It’s got a happy ending—he did eventually get the OK to move forward with his project—but the documentary will make your blood boil. Nobody should have to go through what he did, especially with his own goddamned property!

These pieces exemplify what we set out to do a dozen years ago when longtime Reason reader, sitcom legend, and The Price Is Right host Drew Carey came to us with the visionary idea of making online videos. Virtually nobody in the magazine space was thinking that way at the time, and even though we have a track record of adopting new technologies with gusto, Drew had to sell us on the idea. Video, said Drew, would allow us to reach whole new audiences and connect with them emotionally—to win hearts along with minds.

In October 2007, Reason TV went live with a video hosted by Drew, called “Gridlock.” It documented how awful traffic in Los Angeles and other cities is, explained how to fix traffic jams with free-market solutions courtesy of the transportation policy wonks at Reason Foundation, and threw in a free helicopter ride for the poor schmo with the worst commute in the City of Angels.

Since then, the folks at Reason TV, now led by Meredith Bragg, have released over 1,900 documentaries, interviews, and viral comedy hits; snagged a basketful of awards, including two prestigious nominations for National Magazine Awards (for the series Reason Saves Cleveland with Drew Carey and for “UPS vs. FEDEX“); partnered with the musical-comic genius Remy, future Fox Business host Kennedy, and journalistic giant John Stossel; and produced no fewer than 17 videos that have each yielded more than 1 million views at YouTube.

Drew was right. Video has allowed us to reach new and different audiences, especially younger people who are searching for information and analysis they’re not getting in high school and college or from ideologically rancid cable networks. Last year, fully 56 percent of our YouTube audience was under 35 years old.

As a viewer of Reason TV, I know how invaluable these videos are in the fight for a freer, fairer, and more fun world. As the former editor in chief of Reason TV, I also know how hard it is to put together a video that pulls 1,000 views, much less 1 million. Your donations—which are tax deductible!—are what makes it all happen. So please give what you can.

Here’s another big hit from last year. Enjoy Remy’s parody of Post Malone’s “Better Now?” And again, thanks.

from Latest – Reason.com https://ift.tt/2LnmIkb

via IFTTT

New York’s uniquely onerous restrictions on transporting guns were so hard to justify that the city stopped trying. Instead it rewrote the rules after the Supreme Court agreed to consider a constitutional challenge to them, and now it argues that the case is moot.

Despite the obvious vulnerability of New York’s regulations, the city successfully defended them for five years, obtaining favorable rulings from a federal judge and the U.S. Court of Appeals for the 2nd Circuit. That track record highlights a glaring problem the Supreme Court could address if it rejects the city’s mootness claim: More than a decade after the justices recognized that the Second Amendment imposes limits on gun control, lower courts routinely treat the right to keep and bear arms as a minor hindrance that can be overcome by the slightest excuse.

Under New York’s rules, licensed pistol and revolver owners were not allowed to leave home with their handguns, even if they were unloaded and stored in a locked container separate from the ammunition, unless they were traveling to or from one of seven gun ranges in the city. If a New Yorker wanted to practice at a range, participate in a competition, or defend himself at a second home outside the five boroughs, the only legal option was to buy (or rent) additional handguns.

The justification for those seemingly arbitrary restrictions was always hard to fathom, as Justice Ruth Bader Ginsburg, no one’s idea of a Second Amendment fanatic, noted during oral arguments on Monday. “What public safety or any other reasonable end is served by saying you have to have two guns instead of one,” she wondered, “and one of those guns has to be maintained in a place that is often unoccupied and that therefore [is] more vulnerable to theft?”

Richard Dearing, the attorney representing New York City, was stumped. “Petitioners have identified a difficult application of our former rule that wasn’t really contemplated when the rule was adopted,” he said.

Justice Samuel Alito asked Dearing if New Yorkers are “less safe” now that the city has loosened its restrictions. “No, I don’t think so,” Dearing replied. “We made a judgment, expressed by our police commissioner, that it was consistent with public safety to repeal the prior rule.”

In that case, Alito wondered, “what possible justification could there have been for the old rule, which you have abandoned?” Dearing again had no good answer, except to say that it was a bit easier for police to verify that a gun owner was on his way to or from a range on Staten Island, as opposed to a range in Yonkers or New Jersey.

Restrictions on fundamental rights usually pass muster only if they are narrowly tailored to further a compelling government interest—in this case, preventing gun violence. But as the gun owners who challenged New York’s rules note, “The only ‘evidence’ the City has ever mustered to support the tailoring of its policy is an affidavit from a former commander of the state licensing division hypothesizing, with no evidentiary support whatsoever, that the mere presence of a handgun—even unloaded, secured in a pistol case, separated from its ammunition, and stowed in the trunk of the car—might pose a public-safety risk in ‘road rage’ or other ‘stressful’ situations.”

That implausible scenario was enough to persuade the 2nd Circuit. In the appeals court’s view, the city’s assertion that the transport ban was necessary to protect public safety—a claim it has now disavowed—outweighed the plaintiffs’ “trivial” interest in using their guns for self-defense outside the city or in honing the skills required for that constitutionally protected purpose.

Such casual disregard for the right to keep and bear arms is plainly inconsistent with what the Supreme Court has said about the Second Amendment. That’s why the city is so desperate to prevent the justices from considering an argument that was good enough until now.

Pedophile Mueller Witness Charged With Steering Illegal Campaign Contributions To Hillary Clinton

A convicted pedophile who became a key witness in Robert Mueller’s Russia investigation has been indicted on charges of illegally funneling campaign funds to Hillary Clinton’s 2016 campaign using straw donors, according to Politico.

Lobbyist George Nader, who was arrested this June at JFK airport for sex-trafficking a 14-year-old boy, has lobbied on both sides of the aisle for Middle Eastern associates – acting as an informal conduit to the Trump campaign, while embarking on a scheme to gain influence in Clinton’s inner circle when everyone thought she was a sure-winner in the last election.

While the DOJ did not reveal which 2016 candidate Nadler funneled funds to, Politico reports that “campaign finance records make clear that the candidate was Clinton.“

Nader was named along with Ahmad “Andy” Khawaja – a Lebanese-American businessman who has donated to Clinton,Adam Schiff, Joe Biden, Chris Coons, Dianne Feinstein and a host of other Democrats who received up to $3 million in campaign funds. He also gave $1 million to Priorities USA, the primary super PAC supporting Clinton, and $1 million to Trump’s inaugural fund.

Nader embarked on the scheme in a bid to gain influence in Clinton’s circle while reporting to a foreign official, according to the Justice Department.

Among his alleged co-conspirators is Ahmad “Andy” Khawaja, the CEO of a payments processing company, according to the Justice Department news release announcing the unsealing of the indictment, which was made by a grand jury in the District of Columbia.

Nader conspired with Khawaja to secretly fund $3.5 million in donations that were made in the name of Khawaja, his wife and his firm, Allied Wallet Inc., according to the indictment.

In 2016, Khawaja co-hosted an August fundraiser for Clinton which included a laundry list of high-profile guests, including Univision owner Haim Saban, movie mogul Jeffrey Katzenberg and basketball legend Magic Johnson, according to the report. According to the indictment, Khawaja conspired with six other individuals to conceal his excessive contributions. Others who were indicted were also linked to donations to Clinton and other Democrats.

According to a written statement by Assistant Attorney General Brian A. Benczkowski of the Justice Department’s criminal division and FBI Washington Field Office chief Timothy R. Slater, Nader, 60 and Khawaja, 48, were charged along with Roy Boulos, Rudy Dekermenjian, Mohammad “Moe” Diab, Rani El-Saadi, Stevan Hill and Thayne Whipple. The latter six were charged with conspiring with Khawaja and each other to make conduit campaign contributions and conceal excessive contributions and related offenses, U.S. authorities said.

Khawaja’s donations earned him access to Clinton during the 2016 campaign and a post-election Oval Office visit with Trump, the Associated Press reported in a 2018 investigation. At that time, Khawaja, the payment processing company he founded, Allied Wallet, and top executives had contributed at least $6 million to Democratic and Republican candidates and groups. –Washington Post

Nader, also a Lebanese businessman, has a shadowy record that includes a 1991 conviction on child pornography charges in the US – for which he served only six months in a halfway house thanks to his role in helping to free American hostages in Beirut. He was also charged and convicted in the Czech Republic in 2002 on 10 counts of sexually abusing minors, and eventually received a one-year prison sentence.

On 29 November 2018, defendant Davin Eldridge, a frequent publisher for a Facebook page called “Trappalachia,” entered the Macon County Courthouse. The officer working the metal detector saw defendant had a small tape recorder and “advised [defendant that] he [could] not record inside the courtroom.[“] Defendant acknowledged the officer’s instruction and entered a courtroom. As he did so, defendant bypassed signs posted on the entranceways stating: “BY ORDER OF THE SENIOR RESIDENT SUPERIOR COURT JUDGE: DO NOT use or open cell phones, cameras, or any other recording devices inside the courtrooms. Violations of this order will be contempt of court, subjecting you to jail and/or a fine. Your phone may be subject to seizure and search.”

While in the courtroom, defendant was observed sitting on the second row with a cell phone, holding it “shoulder-chest level” towards the front of the courtroom. The officer went over to defendant and instructed him to put his phone away. Defendant replied, “I’m not doing anything.” The Honorable William H. Coward, Superior Court Judge of Macon County, was presiding over a criminal matter at that time. Judge Coward was informed that a live posting of the hearing in session was streaming from a Facebook page. Based on that information, Judge Coward interrupted the hearing to issue a reminder that recordings of courtroom proceedings were prohibited by law. At the conclusion of the hearing, Judge Coward viewed the Facebook postings by defendant, which included footage of the inside of the courtroom and the prosecutor presenting his closing argument.

Judge Coward then held Eldridge in criminal contempt for violating the restrictions, and the court unanimously upheld the punishment. But, more controversially,

[T]he trial court sentenced defendant to be confined in the Macon County Detention Center for thirty days. Defendant’s sentence was suspended for twelve months, upon six specific conditions for him to meet during his probationary sentence: 1) serve an active sentence of 96 hours; 2) pay the costs of the action; 3) pay a fine of $500.00; 4) draft a 2,000-3,000 word essay on the following subject: “Respect for the Court System is Essential to the Fair Administration of Justice,” forward the essay to Judge Coward for approval, and following approval, post the essay on all social media or internet accounts that defendant owns or controls or acquires hereafter during his period of probation and attributed to defendant, without negative comment or other negative criticism by defendant or others, during said period of probation; 5) not violate any order of Court or otherwise engage in further contemptuous behavior; and, 6) not attend “any court session in Judicial District 30A unless and until his essay has been approved and posted as required herein and he has fully complied with all other provisions of this order.”

The majority, in an opinion by Judge Wanda Bryant, joined by Judge John M. Tyson, upheld this:

Given defendant’s questionable and intentional conduct, his frequent visits to the courtroom, and his direct willingness to disobey courtroom policies, we discern no abuse of discretion in the trial court’s decision to impose conditions on defendant’s probationary sentence. Such conditions are reasonably related to the necessity of preventing further disruptions of the court by defendant’s conduct, and the need to provide accountability without unduly infringing on his rights.

Judge Christopher Brook dissented as to the delete-negative-comments portion of the sentence:

While I agree with the majority that the sentencing judge’s decision to require Defendant, who violated multiple court orders by recording and livestreaming courtroom proceedings on social media, to write an essay about respect for the courtroom and publish this essay on his social media and internet accounts bears a reasonable relationship to Defendant’s criminal contempt of court, and to his rehabilitation for this crime, I do not agree that requiring Defendant to monitor comments made on this essay by third-parties and delete any comments the court might consider critical bears a reasonable relationship to Defendant’s crime or to his rehabilitation, as N.C. Gen. Stat. § 15A-1343 requires….

The [comment-monitoring] condition … holds Defendant responsible for what is essentially the behavior of others; and while there is some truth to the adage that we are only as good as the company we keep, the relevant community in this context is incredibly diffuse, extending through cyberspace….

Our Court has a “settled policy” of avoiding constitutional questions “when a case can be disposed of on appeal without reaching the constitutional issue[.]” Because I vote to vacate the condition of probation requiring Defendant to delete negative comments on the essay [on statutory grounds], I do not delve deeply into what I consider deeply troubling constitutional problems with this condition of probation. Although we generally do not review constitutional questions that have not first been raised in the trial court, suffice it to say that the sentencing judge has not only compelled Defendant to speak within the meaning of the First Amendment, he has compelled Defendant to then continue speaking by censoring the viewpoints of others expressed in response to speech compelled by the court. This compelled speech silencing third-party viewpoints expressed in response to compelled speech raises serious First Amendment concerns.

Note that, under First Amendment precedents, conditions on criminal sentences can indeed restrict or compel speech, though only so long as the conditions are “reasonably related to legitimate penological objectives,” a pretty vague standard under which the government often wins, but sometimes loses.

from Latest – Reason.com https://ift.tt/2r4bvhF

via IFTTT

It’s Day Two of Reason’s annual webathon—and before I ask you for money, I want to thank you.

Over the past 12 months, Reason TV generated a record 29.5 million views at our YouTube channel. Holy hell, that is simply amazing and humbling! That’s more views than Texas has people. And dig this: Viewers watched our documentaries, interviews, and viral videos for a combined 2.7 million hours! If you contributed even a little to those gargantuan totals, I want to thank you personally for watching.

I also want to ask you to make a (tax-deductible!) donation to Reason Foundation, the nonprofit that publishes this website. Go here to donate and see the great swag associated with different giving levels.

Your generous support is the reason we can make amazing videos such as last year’s single biggest hit, “The Insane Battle To Sabotage a New Apartment Building Explains San Francisco’s Housing Crisis,” by Justin Monticello. Justin’s film, which has pulled nearly 900,000 views at YouTube, documents the insanity gauntlet run by Bob Tilman, who spent five years and $1.4 million to earn the right to turn his coin-operated laundromat into an apartment building in one of the most over-zoned, hyper-expensive cities on the planet. It’s got a happy ending—he did eventually get the OK to move forward with his project—but the documentary will make your blood boil. Nobody should have to go through what he did, especially with his own goddamned property!

These pieces exemplify what we set out to do a dozen years ago when longtime Reason reader, sitcom legend, and The Price Is Right host Drew Carey came to us with the visionary idea of making online videos. Virtually nobody in the magazine space was thinking that way at the time, and even though we have a track record of adopting new technologies with gusto, Drew had to sell us on the idea. Video, said Drew, would allow us to reach whole new audiences and connect with them emotionally—to win hearts along with minds.

In October 2007, Reason TV went live with a video hosted by Drew, called “Gridlock.” It documented how awful traffic in Los Angeles and other cities is, explained how to fix traffic jams with free-market solutions courtesy of the transportation policy wonks at Reason Foundation, and threw in a free helicopter ride for the poor schmo with the worst commute in the City of Angels.

Since then, the folks at Reason TV, now led by Meredith Bragg, have released over 1,900 documentaries, interviews, and viral comedy hits; snagged a basketful of awards, including two prestigious nominations for National Magazine Awards (for the series Reason Saves Cleveland with Drew Carey and for “UPS vs. FEDEX“); partnered with the musical-comic genius Remy, future Fox Business host Kennedy, and journalistic giant John Stossel; and produced no fewer than 17 videos that have each yielded more than 1 million views at YouTube.

Drew was right. Video has allowed us to reach new and different audiences, especially younger people who are searching for information and analysis they’re not getting in high school and college or from ideologically rancid cable networks. Last year, fully 56 percent of our YouTube audience was under 35 years old.

As a viewer of Reason TV, I know how invaluable these videos are in the fight for a freer, fairer, and more fun world. As the former editor in chief of Reason TV, I also know how hard it is to put together a video that pulls 1,000 views, much less 1 million. Your donations—which are tax deductible!—are what makes it all happen. So please give what you can.

Here’s another big hit from last year. Enjoy Remy’s parody of Post Malone’s “Better Now?” And again, thanks.

from Latest – Reason.com https://ift.tt/2LnmIkb

via IFTTT

New York’s uniquely onerous restrictions on transporting guns were so hard to justify that the city stopped trying. Instead it rewrote the rules after the Supreme Court agreed to consider a constitutional challenge to them, and now it argues that the case is moot.

Despite the obvious vulnerability of New York’s regulations, the city successfully defended them for five years, obtaining favorable rulings from a federal judge and the U.S. Court of Appeals for the 2nd Circuit. That track record highlights a glaring problem the Supreme Court could address if it rejects the city’s mootness claim: More than a decade after the justices recognized that the Second Amendment imposes limits on gun control, lower courts routinely treat the right to keep and bear arms as a minor hindrance that can be overcome by the slightest excuse.

Under New York’s rules, licensed pistol and revolver owners were not allowed to leave home with their handguns, even if they were unloaded and stored in a locked container separate from the ammunition, unless they were traveling to or from one of seven gun ranges in the city. If a New Yorker wanted to practice at a range, participate in a competition, or defend himself at a second home outside the five boroughs, the only legal option was to buy (or rent) additional handguns.

The justification for those seemingly arbitrary restrictions was always hard to fathom, as Justice Ruth Bader Ginsburg, no one’s idea of a Second Amendment fanatic, noted during oral arguments on Monday. “What public safety or any other reasonable end is served by saying you have to have two guns instead of one,” she wondered, “and one of those guns has to be maintained in a place that is often unoccupied and that therefore [is] more vulnerable to theft?”

Richard Dearing, the attorney representing New York City, was stumped. “Petitioners have identified a difficult application of our former rule that wasn’t really contemplated when the rule was adopted,” he said.

Justice Samuel Alito asked Dearing if New Yorkers are “less safe” now that the city has loosened its restrictions. “No, I don’t think so,” Dearing replied. “We made a judgment, expressed by our police commissioner, that it was consistent with public safety to repeal the prior rule.”

In that case, Alito wondered, “what possible justification could there have been for the old rule, which you have abandoned?” Dearing again had no good answer, except to say that it was a bit easier for police to verify that a gun owner was on his way to or from a range on Staten Island, as opposed to a range in Yonkers or New Jersey.

Restrictions on fundamental rights usually pass muster only if they are narrowly tailored to further a compelling government interest—in this case, preventing gun violence. But as the gun owners who challenged New York’s rules note, “The only ‘evidence’ the City has ever mustered to support the tailoring of its policy is an affidavit from a former commander of the state licensing division hypothesizing, with no evidentiary support whatsoever, that the mere presence of a handgun—even unloaded, secured in a pistol case, separated from its ammunition, and stowed in the trunk of the car—might pose a public-safety risk in ‘road rage’ or other ‘stressful’ situations.”

That implausible scenario was enough to persuade the 2nd Circuit. In the appeals court’s view, the city’s assertion that the transport ban was necessary to protect public safety—a claim it has now disavowed—outweighed the plaintiffs’ “trivial” interest in using their guns for self-defense outside the city or in honing the skills required for that constitutionally protected purpose.

Such casual disregard for the right to keep and bear arms is plainly inconsistent with what the Supreme Court has said about the Second Amendment. That’s why the city is so desperate to prevent the justices from considering an argument that was good enough until now.

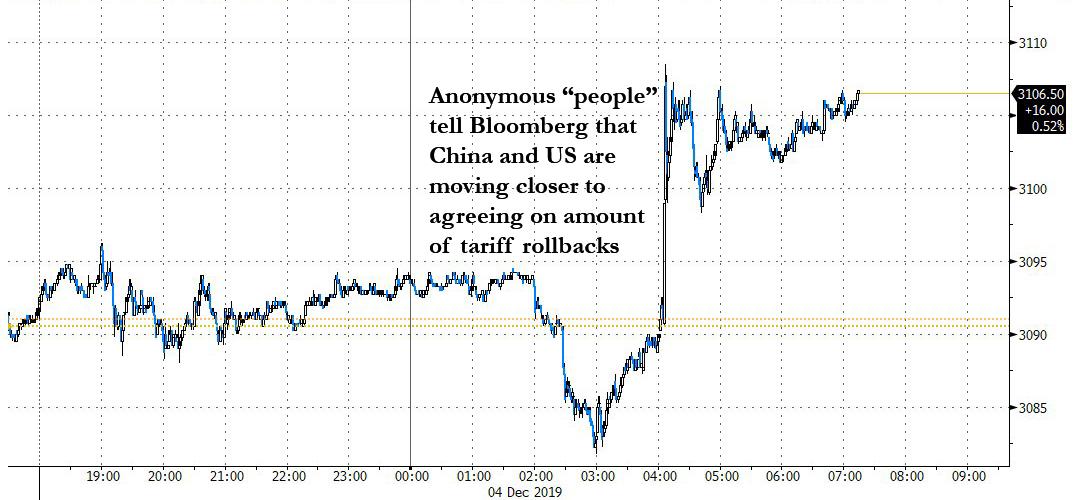

Global Markets Rocket Higher After Blue Horseshoe Loves China Trade Deal

The worst start to a December since 2008 for the S&P500 was apparently too much for certain people who asked Bloomberg not to be identified.

With hopes of a trade deal in shambles, optimism that a “Phase 1” getting signed in 2019 cracking after Trump said yesterday it may be better to delay the deal until after the Nov 2020 election, and China threatening retaliation after the latest House bill almost unanimously voted to sanction Chinese officials over Uighur abuse, even the Global Times’ notorious twitter troll, Hu Xijing, tweeted this morning that there is “a high probability that President Trump or a senior US official will openly say in a few hours that China-US trade talks have made a big progress in order to pump up the US stock markets. They’ve been doing this a lot.”

He was almost 100% accurate, because at almost the exact same time, just after 4am as US futures were sharply rolling over, and a perfectly normal time for such articles market-moving articles, Bloomberg reported that according to “people familiar who asked not to be identified”, the U.S. and China were actually “moving closer to agreeing on the amount of tariffs that would be rolled back in a phase-one trade deal despite tensions over Hong Kong and Xinjiang” and that Trump’s comment “downplaying the urgency of a deal shouldn’t be understood to mean the talks were stalling, as he was speaking off the cuff.”

In other words, Larry KudlowBlue Horseshoe loves China trade deal.

There were naturally question about the Bloomberg piece: like why does an “unknown” source who “thinks” the deal is imminent take presedence, when very known people, , i.e., the US president and Wilbur Ross, both said a deal may not happen for almost a year and that if there is no substantial progress, another round of duties on Chinese imports would take effect on Dec. 15; or why was this “respected” Larry Kudlow source so terrified to give his name on the record if everything checks out?

None of that mattered however, and the market response, as Hu predicted, was instantaneous, sending not only S&P futures sharply higher and importantly, above the critical for dealer gamma level of 3,100, instantly reversing the gloom of the past few days…

… but sent global stocks into a sea of green.

The short squeeze that was triggered after investors layered on shorts into the worst first two days of a December since the financial crisis, went global and miners and chemical producers led the rise on the Stoxx Europe 600 gauge, which rocketed over 1% higher in early trading, even though IHS Markit’s composite PMI index for the euro zone reading at 50.6 pointed to growth of only 0.1% in the fourth quarter. That would be the weakest since the 19-nation region emerged from recession in 2013.

Earlier in the session, markets closed lower across much of Asia as the Bloomberg deus ex ma-China came out too late to help them, with Australia and Hong Kong bearing the brunt of the declines. Declines were led by energy producers, as investors were still focused on the story du jour – at least until the Bloomberg unnnamed sources became “it” – in which trade tensions mounted between Beijing and Washington with a new tariff hike on Chinese goods looming large. Almost all markets in the region were down, with South Korea and Hong Kong leading declines. The Topix retreated, driven by electronic companies and drug makers, as Japan’s government called for decisive fiscal action combined with powerful central bank easing. The Shanghai Composite Index slid, with large insurers and banks among the biggest drags. China is likely to cut the reserve ratio for lenders in the first quarter of next year, the China Securities Journal said in a front-page commentary Wednesday. India’s Sensex edged lower a day before an expected rate cut aimed at reviving growth, as Reliance Industries and HDFC Bank weighed on the gauge.

Treasuries initially caught a bid to session highs on reports that passage of the latest bill could jeopardize a U.S.-China phase one deal. However, the haven bid for Treasuries during Asia session was unwound in European morning trade on the Bloomberg report, overriding negative comments earlier from China’s Ministry of Foreign Affairs. The TSY curve steepened, unwinding a portion of Tuesday’s aggressive bull-flattening move. Yields were higher by 1.2bp to 2.4bp across the curve led by long-end, steepening 2s10s, 5s30s by 1.2bp and 0.5bp; 10-year yields at 1.738%, cheaper by 2.2bp vs. Tuesday’s close. Treasuries were supported during Asia session after China’s Ministry of Foreign Affairs said U.S. will “pay price” for legislation imposing sanctions on Chinese officials over human-rights abuses.

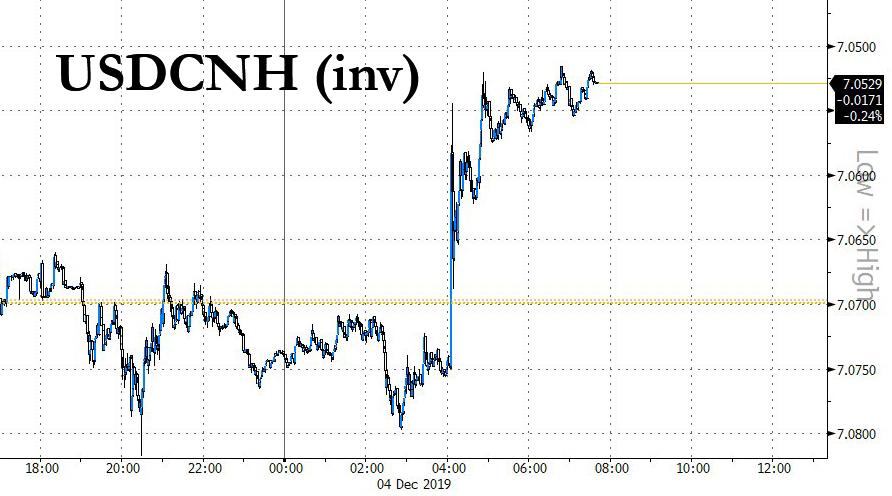

In FX, the dollar briefly recovered against major peers, then headed sharply lower. The euro edged down after a manufacturing report showed that the single-currency economy is barely expanding. The British pound climbed to an almost seven-month high against the dollar and its strongest level since May 2017 against the euro as polls showed the Conservatives have increased their lead before the election. Tracking the positive newsflow, the Chinese yuan spiked, in a virtual mirror image of the move in US futures.

As expected, crude markets were bolstered on the news that the US and China are moving closer to a deal despite recent “heated” rhetoric. Elsewhere, the latest batch of comments from the Iraqi oil minister continues to support prices; an additional 400k bpd cut for OPEC+ is apparently in circulation but not final, while the Saudi’s also reportedly prefer deeper cuts, although this contradicts sources reports seen last month. “If all members were compliant with the [current] deal this may be the case, however, with a number of members falling well short in cutting output, including Iraq, other members may be reluctant to cut further” says ING, who goes on to conclude that “reassurance of stronger compliance will likely be needed before other members agree to deeper cuts.”

Looking at the day ahead, this morning the focus will be on the final November PMI revisions (services and composite) in Europe while we’ll also get that data for the US, along with the November ISM non-manufacturing and November ADP employment report. Away from that, we’re due to hear from the ECB’s Villeroy, Visco, Makhlouf and Hernandez de Cos while the Fed’s Quarles is due to speak on supervision and regulation. Campbell Soup and Synopsys are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.4% to 3,102.00

STOXX Europe 600 up 1% to 402.43

MXAP down 0.7% to 163.21

MXAPJ down 0.8% to 518.12

Nikkei down 1.1% to 23,135.23

Topix down 0.2% to 1,703.27

Hang Seng Index down 1.3% to 26,062.56

Shanghai Composite down 0.2% to 2,878.12

Sensex up 0.4% to 40,822.98

Australia S&P/ASX 200 down 1.6% to 6,606.51

Kospi down 0.7% to 2,068.89

German 10Y yield rose 0.7 bps to -0.341%

Euro down 0.1% to $1.1070

Italian 10Y yield fell 6.4 bps to 0.938%

Spanish 10Y yield rose 0.2 bps to 0.413%

Brent futures up 1.9% to $61.96/bbl

Gold spot down 0.2% to $1,474.90

U.S. Dollar Index little changed at 97.76

Top Overnight News from Bloomberg

The U.S. House of Representatives overwhelmingly approved legislation that would impose sanctions on Chinese officials over human rights abuses against Muslim minorities, prompting Beijing to threaten possible retaliation just as the world’s two largest economies seek to close a trade deal

“I don’t have a deadline,” President Trump tells reporters in London after being asked if he sees phase one of a trade deal with China concluding this year. “I like the idea of waiting until after the election for the China deal. But they want to make a deal now and we’ll see whether not the deal is going to be right”

Australia’s economy slowed last quarter as interest-rate cuts and government tax rebates failed to spur household spending, reinforcing expectations the central bank will need to resume easing next year

Oil defied trade-deal bearishness to rise for a third day after an industry report pointed to shrinking U.S. crude stockpiles and before OPEC+ decides on its output-cut policy later this week. OPEC+ sends mixed signals about deeper output cuts before talks

House Democrats laid out their most comprehensive case yet for impeaching Donald Trump, declaring the president “a clear and present danger” over his rush to get foreign governments to investigate a political rival and making his intimidation of witnesses tantamount to a crime

U.S. President Donald Trump revived both his “Rocket Man” nickname for Kim Jong Un and the threat of military force against North Korea, in the latest sign of rising tensions ahead of Pyongyang’s year-end deadline

While IHS Markit’s composite Purchasing Managers’ Index for the euro zone stabilized at 50.6 in November, above the flash reading of 50.3, it points to growth of only 0.1% in the fourth quarter. That would be the weakest since the 19-nation region emerged from recession in 2013

Foreign direct investment into China jumped last year to $139 billion even as trade tensions escalated, bucking a trend that saw global flows sink 13% from 2017 levels

OPEC and its allies sent mixed signals about whether they were considering deeper production cuts, fanning oil-market speculation before crucial talks in Vienna this week

Germany’s Social Democrats backed away from a threat to ditch their alliance with Chancellor Angela Merkel and eased demands for the government to abandon its balanced-budget policy

Asian equity markets extended on declines as global risk appetite remained sapped by the turbulent trade climate following yesterday’s comments by US President Trump. ASX 200 (-1.6%) and Nikkei 225 (-1.0%) were lower with pressure in the trade-related sectors resulting in Australia’s continued underperformance which was also not helped by a miss in quarterly GDP growth, while the Japanese benchmark tracked the recent slide in USD/JPY and with reports noting the GPIF’s move to end stock lending could rattle markets. Hang Seng (-1.3%) and Shanghai Comp. (-0.2%) were dampened by the increased trade pessimism after President Trump’s comments and with Global Times suggesting the US appears to be back-pedalling in trade talks. The US House’s overwhelming support for the Uighur human rights bill demanding sanctions on Chinese officials, which it passed through 407-1 vote, also contributed to the bilateral tensions and spurred resolute opposition from China which will respond depending on how the situation develops. Nonetheless, losses in the mainland have been stemmed after strong Chinese Caixin Services and Composite PMI numbers added to the country’s recent flurry of strong activity data and as Chinese press op-ed suggested the PBoC are expected to cut RRR in Q1. Finally, 10yr JGBs were higher after the recent gains in T-notes due to safe-haven bids, but with prices off their best levels after failing to hold above the 153.00 level and with the lack of BoJ presence in the market contributing to the mild overnight retracement.

Top Asian News

India Is Said to Mull Easing Lending Rules for Shadow Banks

Hong Kong Announces Further Stimulus Worth $500 Million

China’s First IPO Flop Since 2012 Shows Confidence Breaking

Major European bourses (Euro Stoxx 50 +1.3%) are firmer following reports that the US and China are moving closer to a deal despite recent “heated” rhetoric gave a boost to risk appetite. The FTSE 100 (+0.3%) is a laggard due to a firmer sterling. In terms of further fundamental catalysts on the horizon; Day 2 of the NATO summit begins and traders will be on the look-out for further clues as to the state of play on the US/EU and US/China front, quite possibly in the form of off-the-cuff comments from the US President, with the former two in the midst of clashes over the WTO’s ruling on EU Airbus subsidies and most recently France’s proposed Digital Services Tax, while tensions between the latter two have most recently been worsened following the US House’s passing of the Uighur Human Rights Bill. Sectors are mostly in the green, with Telecoms (unch.) the laggard as the sector is weighed by underperformance in heavyweight Orange (-3.8%), with traders reportedly disappointed by the Co.’s most recent dividend outlook. Elsewhere, Italian banks, including Intesa Sanpaolo (+1.8%) and UniCredit (+1.6%), are on the front foot after Moody’s upgraded the outlook for Italian banking to stable from negative. Solid earnings from US Microchip last night is acting as supportive for European chipmakers, including Infineon Technologies (+2.2%). In terms of other notable individual movers; Elior (+7.8%) opened higher after the Co. posted strong earnings, in which FY net profit posted solid Y/Y gains. Further gains were seen for easyJet (+2.1%), with the Co. set to join the FTSE 100, and Hiscox (-1.0%) and Fresnillo (-3.8%) to be dropped. In terms of the losers; Aviva (+0.2%) lags the FTSE 100, having been downgraded at Barclays. Elsewhere, Securitas (unch.) underperforms following a downgrade at Deutsche Bank.

Top European News

U.K. Economy on Course for Contraction as Services Falter

Euro- Area Economy Is Just About Growing as Factory Slump Spreads

GAM Faces Regulator Penalty for Misstating Quant Fund Deal

ECB Places Goldman Unit Under Direct Supervision Amid Brexit

In FX, the sterling rose to the top of the G10 ranks in early EU hours following a relatively sideways APAC session in which GBP/USD meandered on either side of 1.3000. The pair gained momentum after tripping stops at 1.3013 and advanced to a current intraday high of 1.3063 (ahead of its 200 WMA around 1.3100) before waning off highs and back below its 100 WMA at 1.3048. News-flow has been light for Sterling, with the currency little influenced by a revision higher to its November services and composite PMI metrics. That said, IHS noted that the PMI figures point to a GBP contraction of ~0.1% in the Q4, but the December numbers are yet to be released. Meanwhile, the Eur has been moving at the whim of the Buck and largely shrugged off upward revisions to the pan-European services and composite numbers – with the GDP tracker suggesting growth of 0.1% in Q4 for the EZ. IHS did warn that the services sectors are poised for its weakest QQ expansion for fives years, “hinting strongly that the slowdown continues to spread”. EUR/USD moved into negative territory and back below its 100 DMA (1.1069) after hitting an intraday peak 1.1088, with little EU-specific data/speakers left on the docket.

DXY, JPY – The broad Dollar and Index has recouped earlier losses with upside coinciding with constructive trade headlines from sources, prompting the DXY to rebound off its 200 DMA at 97.63 back to yesterday’s closing levels around 97.75. Meanwhile, USD/JPY ekes mild losses amid the aforementioned headlines with the pair back above the 108.50 mark (coincides with its 50 DMA), to a high of 108.80 ahead of the rough figure. Traders will be eyeing any trade/geopolitical headlines with NATO summit day 2 underway and US President Trump’s presser scheduled for 15:30GMT.

AUD, NZD – Both lower on the day, but more-so the Aussie on the back of disappointing GDP figures with the QQ metric showing growth of only 0.4%, down from the prior of 0.5%. Analysts mention that the most concerning aspect of the release is the representation of a fifth consecutive quarter which private demand contracted or was flat. Westpac notes that the RBA will be disappointed with the figure and believes that the Central Bank and the Government will have to revisit their growth forecasts. AUD/USD climbed off lows in wake of optimistic US-China trade headlines, but gains remain capped due to the overnight data. The pair remains in the red around the middle of its 0.6813-0.6846 band having briefly dipped below its 100 DMA at 0.6816. The Kiwi piggybacks on the Aussie’s losses and hovers just above the 0.65 mark, off highs of 0.6530.

In commodities, Iraq Oil Minister stated that an additional 400k bpd cut for OPEC+ is in circulation but not final and that all members should share the burden, while he added that slower demand is a bigger impact next year than non-OPEC supply. Furthermore, the Oil Minister added that it is his understanding that Saudi prefers a deeper cut and that deeper cuts are preferred by members. Crude markets are bolstered (in line with other risk assets) on the news that the US and China are moving closer to a deal despite recent “heated” rhetoric. Elsewhere, the latest batch of comments from the Iraqi oil minister continues to support prices; an additional 400k bpd cut for OPEC+ is apparently in circulation but not final, while the Saudi’s also reportedly prefer deeper cuts, although this contradicts sources reports seen last month. “If all members were compliant with the [current] deal this may be the case, however, with a number of members falling well short in cutting output, including Iraq, other members may be reluctant to cut further” says ING, who goes on to conclude that “reassurance of stronger compliance will likely be needed before other members agree to deeper cuts.” Moreover, yesterday saw the OPEC+ Joint Technical Committee meet in Vienna ahead of the full ministerial meetings on Thursday and Friday and they reportedly did not discuss deeper cuts. Reports did suggest that the Joint Technical Committee is considering Russia’s request to exclude condensate from its oil production cuts, which has been rising as of late in line with the country’s rising gas output and has been cited as the reason for the country’s poor OPEC+ compliance. Elsewhere, also underpinning the crude complex is last night’s larger than expected draw in headline API Inventories; traders will now focus on EIA Inventory data this afternoon for further confirmation. WTI futures meanders around USD 57/bbl while its Brent counterpart eyes USD 62/bbl to the upside having earlier eclipsed the level. Moving onto metals, risk on has hit gold prices, which have fallen to just above USD 1470/oz from earlier highs of USD 1490/oz. Meanwhile, copper has been buoyed, popping to USD 2.6450/lbs highs from its earlier USD 2.62-2.63/lbs range. Elsewhere, iron ore prices found further impetus after data showed that shipments from Brazil had dropped since the last week; prices have been underpinned in recent days by the news that Vale, the world’s largest miner of Iron Ore, cut its production outlook and production at its Brutucu mine has been halted due to safety issues regarding a nearby dam.

DB’s Jim Reid concludes the overnight wrap

7am: MBA Mortgage Applications, prior 1.5%

8:15am: ADP Employment Change, est. 135,000, prior 125,000

9:45am: Markit US Services PMI, est. 51.6, prior 51.6; 9:45am: Markit US Composite PMI, prior 51.9

10am: ISM Non-Manufacturing Index, est. 54.5, prior 54.7

DB’s Jim Reid concludes the overnight wrap

A quiz question to start this morning. Complete the following sequence… 19.6%, 25.7%, 20.5%, 27.3%, 15.5%, 10.8%, 13%, 16%, 13.3%, 18.7%, xxx%…….??? ….. answer at the end of today’s EMR.

If you’ve had enough of 2020 outlooks as we progress through December then don’t fear as later today my team and I will publish our latest Konzept magazine where we will “Imagine 2030” and look at a number of eclectic articles suggesting what the world might look like at the end of the next decade. So if you want to know about the end of credit cards, whether we’ll still be using cash, the future of crypto currencies, how you will consume food, the rise of the drones, the outlook for India and China, what Europe needs to do to compete and catch-up, and what we think will be the main populism battleground in 2030 then watch out for this later. There are 24 articles in total and some are more serious than others. One of my favourites is one from Luke on the future of pro sports stats. Every potential move will be AI analysed by 2030 and players trained accordingly. Hopefully, I’ll also have a robot swinging a golf club for me by then.

If 2030 is too far out for you, a reminder that you can find our 2020 macro credit view here , and our IG and HY specific views here and here .

Back from the future now and what a difference a couple of days can make. Mr Trump has completely taken the momentum out of financial markets this week and the December 15th date will increasingly become a focal point over the next couple of weeks. Last week the mood music suggested that even if a “phase one” deal hadn’t been reached by then, then there was a good chance tariffs planned to be implemented on that date would be postponed. After the stepping up of negative global tariff rhetoric over the last 48 hours, yesterday’s headlines suggesting that the US is going forward with the December 15 tariffs grabbed the limelight, although markets had already been trading weaker prior to that. Fox’s Edward Lawrence said that “trade sources tell me that the Dec 15th tariffs on basically the rest of what China imports into the US are still going forward as of today.” He went on to clarify that the next tranche could still be called off, if a phase one deal gets finalised or “something else positive happens.” For his part, President Trump said that a trade deal is “dependent on whether I want to make it” and “in some ways it is better to wait until after the election…and we’ll see whether the deal is going to be right”.

This might be a late negotiating ploy ahead of a deal but its impossible to tell at the moment and from something that looked like a case of “when not if” a couple of weeks ago now is a case of “if not when.” If that wasn’t enough, Trump also said later on in the day that “those countries that don’t deal with NATO obligations will be dealt with, maybe through trade”. Meanwhile, Wilbur Ross hardly painted a rosier picture, saying that the US has “more ammunition left against China” and also that the US “has a legitimate complaint with Europe over trade.”

The end result for markets were drops of -0.66%, -0.55% and -1.01% for the S&P 500, NASDAQ and DOW but with markets nearly three-quarters of a percent off their early session lows. The trade sensitive semiconductor index was also hit -1.54%, taking it now down -4.04% over the last three sessions, the worst such stretch since August. In Europe, the STOXX 600 closed down -0.93%, taking the two-day loss to -2.20%. Credit also suffered with US HY spreads +11bps while in bond markets we saw yields rally, including a fairly brutal -10.7bps move for 10y Treasuries, which was the most since August 14. The curve also flattened -3.9bps and there are now 20bps of cuts implied between now and next July. In Europe, yields were broadly lower with Bunds -6.8bps and back within a basis point of where they were before the weekend SPD news (more later). In commodities gold (+1.03%) and silver (+1.54%) benefited from the risk off while in currencies it was the Swiss franc (+0.41%) and yen (+0.33%), which also caught a bid at the expense of EM currencies like the South African rand (-0.67%) and the offshore renminbi (-0.35%).

Overnight, the US House of Representatives passed a bill that would impose sanctions on Chinese officials over alleged human rights abuses. However, the House passed an amended version of the Senate bill by adding provisions that require the president to sanction Chinese government officials responsible for the repression of Uighurs and places restrictions on the export of devices that could be used to spy on or restrict the communications or movement of members of the group and other Chinese citizens. Also, among other provisions, the bill requires the president to submit to Congress within 120 days a list of senior Chinese government officials guilty of human rights abuses against Uighurs in Xianjiang or elsewhere in China. Bloomberg further reported that lawmakers are working to resolve differences between the House and Senate bills to agree on one version that can pass swiftly through Congress before the end of the year. In response, China’s foreign ministry urged the US to stop the bill and vowed to further respond if it progresses, without providing any details. The Global Times editor has just tweeted that “US politicians with stakes in China should be careful”.

Overnight, Asian markets are trading lower following Wall Street’s lead with the Nikkei (-1.06%), Hang Seng (-1.08%), Shanghai Comp (-0.31%) and Kospi (-0.69%) all down. The USDCNY fix earlier was the biggest miss to the daily model since August 2nd just after Trump had tweeted about additional tariffs on China. So one to watch as the stakes are raised.

Staying with FX, the Australian dollar is down -0.351% this morning as the Q3 GDP miss raised the probability of a rate cut by the RBA. Elsewhere, futures on the S&P 500 are up +0.07%. As for overnight data releases, China’s November Caixin services PMI came in at 53.5 (vs. 51.2 expected) thereby bringing the composite PMI to 53.2 (vs. 52.0 last month). So an impressive read but one that will be difficult to get too positive about given the trade news this week. Meanwhile, Japan’s final November services and composite PMI both came in one tenth lower than the initial read at 50.3 and 49.8, respectively.

In other better news on trade, Bloomberg reported that Mexico is considering a US proposal to remove protections for biologic drugs from a renegotiated Nafta trade deal. The proposed change would drop language in the U.S.-Mexico-Canada Agreement offering 10 years of market protection for drug makers from cheaper generic spinoffs. It has proved one of the sticking points in getting the deal passed in the US as House Democrats have raised concern that locking in a time frame for pharmaceutical rules could hinder their ability to reduce protections for biologics sooner, as part of an effort to bring down soaring drug prices. Meanwhile, Ways and Means Chairman Richard Neal, the Democrat who’s in charge of the negotiations in the House, said it’s “possible” that Democrats would agree to a deal this week and added that he would like the House to vote on the implementing legislation by the end of the year.

Later today, we’ll get the final services and composite PMIs in Europe and the US as well. Expectations are for the euro area services PMI to remain at 51.5 from the flash reading, though there is likely some upside to the composite number (50.3 flash) after the upward revision to the manufacturing index on Monday. On a country level, the readings in France and Germany are expected to stay steady from the flash estimates, while the prints for Spain and Italy are both expected to fall, by -0.8pts and -1.0pts, respectively, from the October results. Later in the day, the US services PMI is expected to stay at 51.6 from the flash reading, while the non-manufacturing ISM is expected to decline -0.2pts from October to 54.5. Our economists will be watching the employment subindex, which is a strong leading indicator for private payrolls growth.

As an update to the SPD developments, ahead of their 3-day conference on Friday a draft text suggested that the party will call for additional public investment and that it should not be prevented by ‘dogmatic positions’ such as ‘black zero’. So the stage is set for them to demand more as a cost of staying in the GroKo. We will see after that who is going to call the other’s bluff within the coalition, though it does bode well that the draft does not explicitly call for an end to the coalition. New SPD chief Walter-Borjans even said “one thing is clear, we do not want to get out of the grand coalition head over heels.” Whatever that means.

Staying with politics, in terms of the latest UK polls 8 days before the election, the two yesterday showed a 12pt and a 9pt lead for the Conservatives – up 1pt and flat relative to the last time these pollsters last published a few days before. The Labour Party has definitely had a little more momentum over the last couple of weeks but poll of polls are only back to where they were at the start of the campaign (around 10pt lead) and have perhaps only narrowed a couple of points from the peak lead. So there will have to be a very late swing or a bad widespread polling sampling error across the industry for the Tory’s not to win a majority. Labour’s last hope is probably a last minute collapse of the LibDem vote. Throughout the campaign the support for the Tories has been impressively stable at between 40-45% so it doesn’t feel like this is going to fall away now. Labour will need to get closer to this from elsewhere and likely hope for a hung parliament. At this point even if they are well behind the Tories they are likely to be the only party able to form a coalition.

Finally, there wasn’t much to report from the data yesterday. In the US, November vehicle sales came in quite strong at 17.09mn (vs. 16.90mn expected). Meanwhile in Europe PPI printed at +0.1% mom for October (vs. 0.0% expected) while the November construction PMI for the UK was a little better than expected (45.3 vs. 44.5 expected) – albeit still at very low levels.

Looking at the day ahead, this morning the focus will be on the final November PMI revisions (services and composite) in Europe while this afternoon we’ll also get that data for the US, along with the November ISM non-manufacturing and November ADP employment report. Away from that, we’re due to hear from the ECB’s Villeroy, Visco, Makhlouf and Hernandez de Cos while the Fed’s Quarles is due to speak on supervision and regulation.

*** The answer to the final number in the sequence is 3.5%. Yes, after a decade of expecting large double digit returns in the S&P 500 in his year ahead outlooks, our US equity strategist Binky Chadha is ‘only’ expecting 3.5% return from the S&P 500 out to the end of 2020 from current levels. It’s actually 0% for 2020 as a whole as his YE 2019 and 2020 forecasts are the same. So this is a major relative change in view, considering we’ve all marvelled at the bullishness (proved correct) of his previous numbers. For an explanation of why please see the link here ***