House Republicans on Monday evening released their impeachment report, dismissing allegations against President Donald Trump as unsubstantiated and politically motivated.

“The Democrats’ impeachment inquiry is not the organic outgrowth of serious misconduct; it is an orchestrated campaign to upend our political system,” the report says. “The Democrats are trying to impeach a duly elected President based on the accusations and assumptions of unelected bureaucrats who disagreed with President Trump’s policy initiatives and processes.”

The minority party asserts that Trump pushed Ukrainian President Volodymyr Zelenskiy to announce investigations connected to his political rivals not for partisan gain but because Trump was suspicious of the country’s “history of pervasive corruption,” although the country had already met its anti-corruption benchmarks to receive foreign aid.

“Understood in this proper context, the President’s initial hesitation to meet with President Zelensky or to provide U.S. taxpayer-funded security assistance to Ukraine without thoughtful review is entirely prudent,” the House Republicans write.

An impeachment inquiry is underway amid allegations that Trump withheld a White House meeting and $391 million in security assistance to Ukraine in exchange for Zelenskiy publicly pursuing probes into Burisma Holdings, where former Vice President Joe Biden’s son sat on the board, and into a highly criticized theory that Ukraine executed an election interference scheme that benefited 2016 Democratic candidate Hillary Clinton. The Republicans’ findings contradict the testimonies of several witnesses who appeared before the House Intelligence Committee, many of whom stated that the president’s request contradicted diplomatic goals and equated to a political favor.

“I know that members of this committee have frequently framed these complicated issues in the form of a simple question: Was there a ‘quid pro quo?'” Gordon Sondland, the U.S. ambassador to the European Union, testified on November 20. “With regard to the requested White House call and White House meeting, the answer is yes.”

The Republican impeachment report casts such witnesses as unreliable, without the proper knowledge, and motivated by an animus for Trump’s style of governance. “They are trying to impeach President Trump because some unelected bureaucrats chafed at an elected President’s ‘outside the beltway’ approach to diplomacy,” the report says. But those depictions are somewhat puzzling, particularly in regards to Sondland, who was given his position after donating $1 million to Trump’s inaugural fund, and who described a friendly and direct working relationship with the president. Testimonies from Kurt Volker, the former special envoy to Ukraine, and Bill Taylor, the country’s chargé d’affaires, squared with Sondland’s account, with the latter telling congressional investigators that it is “crazy to withhold security assistance for help with a political campaign.”

The Republican report is also in contention with sworn comments made by Lt. Col. Alexander Vindman, who said that Trump disregarded National Security Council-approved talking points on corruption in his April and July phone conversations with Zelenskiy. White House readouts show that the president never addressed corruption, but instead asked Zelenskiy to “do us a favor” on the July 25 call. Vindman also testified that the White House readout of that conversation specifically replaced “Burisma” with “the company.”

Complaints about the impeachment process are also present in the GOP report, as House Republicans continue to accuse Democrats of stripping Trump of due process. “For the first phase of the Democrats’ impeachment inquiry, Chairman Schiff led the inquiry from his Capitol basement bunker, preventing transparency on the process and accountability for his actions,” it says. As I’ve previously noted, such claims are not based in reality: It was House Republicans who set these very rules in 2015 under then-Speaker John Boehner (R–Ohio).

All told, the report cements the likely Republican defense of Trump, should the current inquiry move to an impeachment trial.

from Latest – Reason.com https://ift.tt/33MD0JR

via IFTTT

House Republicans on Monday evening released their impeachment report, dismissing allegations against President Donald Trump as unsubstantiated and politically motivated.

“The Democrats’ impeachment inquiry is not the organic outgrowth of serious misconduct; it is an orchestrated campaign to upend our political system,” the report says. “The Democrats are trying to impeach a duly elected President based on the accusations and assumptions of unelected bureaucrats who disagreed with President Trump’s policy initiatives and processes.”

The minority party asserts that Trump pushed Ukrainian President Volodymyr Zelenskiy to announce investigations connected to his political rivals not for partisan gain but because Trump was suspicious of the country’s “history of pervasive corruption,” although the country had already met its anti-corruption benchmarks to receive foreign aid.

“Understood in this proper context, the President’s initial hesitation to meet with President Zelensky or to provide U.S. taxpayer-funded security assistance to Ukraine without thoughtful review is entirely prudent,” the House Republicans write.

An impeachment inquiry is underway amid allegations that Trump withheld a White House meeting and $391 million in security assistance to Ukraine in exchange for Zelenskiy publicly pursuing probes into Burisma Holdings, where former Vice President Joe Biden’s son sat on the board, and into a highly criticized theory that Ukraine executed an election interference scheme that benefited 2016 Democratic candidate Hillary Clinton. The Republicans’ findings contradict the testimonies of several witnesses who appeared before the House Intelligence Committee, many of whom stated that the president’s request contradicted diplomatic goals and equated to a political favor.

“I know that members of this committee have frequently framed these complicated issues in the form of a simple question: Was there a ‘quid pro quo?'” Gordon Sondland, the U.S. ambassador to the European Union, testified on November 20. “With regard to the requested White House call and White House meeting, the answer is yes.”

The Republican impeachment report casts such witnesses as unreliable, without the proper knowledge, and motivated by an animus for Trump’s style of governance. “They are trying to impeach President Trump because some unelected bureaucrats chafed at an elected President’s ‘outside the beltway’ approach to diplomacy,” the report says. But those depictions are somewhat puzzling, particularly in regards to Sondland, who was given his position after donating $1 million to Trump’s inaugural fund, and who described a friendly and direct working relationship with the president. Testimonies from Kurt Volker, the former special envoy to Ukraine, and Bill Taylor, the country’s chargé d’affaires, squared with Sondland’s account, with the latter telling congressional investigators that it is “crazy to withhold security assistance for help with a political campaign.”

The Republican report is also in contention with sworn comments made by Lt. Col. Alexander Vindman, who said that Trump disregarded National Security Council-approved talking points on corruption in his April and July phone conversations with Zelenskiy. White House readouts show that the president never addressed corruption, but instead asked Zelenskiy to “do us a favor” on the July 25 call. Vindman also testified that the White House readout of that conversation specifically replaced “Burisma” with “the company.”

Complaints about the impeachment process are also present in the GOP report, as House Republicans continue to accuse Democrats of stripping Trump of due process. “For the first phase of the Democrats’ impeachment inquiry, Chairman Schiff led the inquiry from his Capitol basement bunker, preventing transparency on the process and accountability for his actions,” it says. As I’ve previously noted, such claims are not based in reality: It was House Republicans who set these very rules in 2015 under then-Speaker John Boehner (R–Ohio).

All told, the report cements the likely Republican defense of Trump, should the current inquiry move to an impeachment trial.

from Latest – Reason.com https://ift.tt/33MD0JR

via IFTTT

“Lower For Ever”: One Bank Makes A Stunning Discovery – The Fed’s Rate Cuts Are Now Deflationary

For the past three decades, one of the most frequently asked questions in finance is ‘what has been behind the relentless bull market in treasuries’ (and collapsing interest rates), which have in turn helped push global stocks to never before seen highs amid a bull market that started in the early 1980s and has grown at what appears to be an exponential pace. The main reason for this confusion has been the majority’s strict adherence to the textbook view that the world is cyclical and mean reverting and, thus, declining yields now must surely mean rising yields later on.

Others, such as Rabobank’s Jan Lambregts in contrast, have believed that the forces which have been bearing down on yields are, in actual fact, structural in nature which has not only challenged the mean-reversion investment strategy but also thrown a spanner in the works in terms of cycle-based economic theory. And crucially, as Lambregts writes in his 2020 preview, policymakers’ attempts to provide a cyclical solution to what is a structural problem helps explain developments in the sociopolitical sphere in recent years.

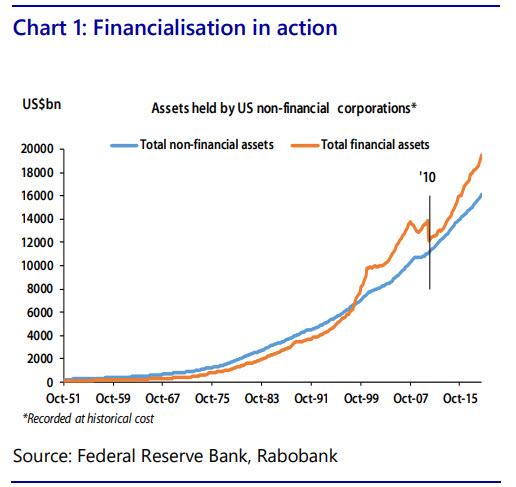

To regular readers of Zero Hedge, and generally contrarians, it will come as no surprise that the structural forces Lambregts is referring to relate principally to our financialization thesis: this refers to a trend that has been evident for decades in Western economies (but arguably increasingly elsewhere in recent years) whereby corporations have increasingly favored investment in financial rather than fixed assets.

The first chart below stylizes this thesis by showing the holdings of financial and non-financial assets on the part of US non-financial corporations since the beginning of the 1950s. As can be seen, since the mid-1990s, US companies have clearly favoured financial investment vs. the “real” thing. 2010 is highlighted on this graphic as it is at this point that the crisis-induced correction in corporate financial asset holdings rapidly reverses. This is attributable to the onset of QE which only served to further encourage corporate investment in financial assets owing to the de facto government put implied by the central bank purchase program.

As corporations focused largely on growing their financial assets, the flip side was made apparent in the corporate behavior encapsulated in the next chart, which as ING notes, shows the collapse in net fixed investment demand as a share of GDP during the financial crisis and the fact that the subsequent recovery has only taken investment’s share of the economy back to the cyclical lows repeatedly forged through the post-WWII period. This, then, helps explain a conundrum economists have been struggling with in recent years which is why fixed investment demand is still so slow this many years after the crisis despite the historical and, in certain instances, record low cost of capital. Rabobank’s thesis argues that corporates have taken advantage of low borrowing costs but not to invest in organic growth but as a means of undertaking financial value engineering.

This view also provides a plausible means of addressing another post-crisis puzzle which is why productivity growth has remained so low (since 2010, US productivity has been growing at its slowest speed on average in the post-war era). This, as Rabobank further notes, should be no surprise given the clear bias of corporates to accumulate non-productive financial assets rather than undertake productive fixed investment. This, in turn, helps explain why estimates of US potential output have collapsed in the post-crisis period. The chart below highlights this development in showing the sharp decline in recent years of New York Fed’s estimate of the natural, or neutral, policy rate. This is the real policy rate level deemed suitable for meeting the Bank’s dual mandate of full employment and 2% inflation. Crucially, trend growth is a key assumption underpinning this assessment.

This “financialisation” thesis can also help explain the scarcity of developed world wage inflation despite historically low levels of unemployment. In large part, this is owing to the fact that higher wages in the absence of productivity growth implies lower margins. This is a development that has arguably been resisted by Anglo-Saxon companies as higher wages within this context would result in workers enjoying seniority in terms of access to profits vs. shareholders – the very opposite of the share-value maximisation corporate governance model that ING argues has been increasingly prevalent since the mid-90s.

The next chart shows the long-running crowding out of the US workforce in the form of labor’s share of (declining) national income from the 1960s onwards. The chronic nature of this trend reflects the fact that there are other structural forces at play which have been disadvantageous to developed world workers – specifically, globalization and robotization. Yet while these factors have long been widely acknowledged, Rabo’s focus is upon the less appreciated “-ation” – that of financialization.

The accelerated crowding out of labor at the turn of this millennium is also reflected in the explosion of US corporate profitability shown in the next chart. Taken together with charts 2 and 4, Rabobank argues that these three visualizations make it clear that these profits failed to make their way either to labor or to fixed investment while Chart 1 implies that financial value engineering was the ultimate destination. Taken together, Charts 4 & 5 reflect a post-crisis development that has been crucial from a social perspective.

To summarize, Rabobank’s core thesis is that recent decades have seen corporates (initially in the Developed world) increasingly avoid fixed investment in favor of that of a financial variety. Central banks have, ironically, accelerated this process by directly intervening in financial markets. The upshot of this has been a rapid appreciation of financial asset values but at the direct expense of real world activity (a cannibalization of fixed investment demand), a concomitant stymieing of productivity growth and, by extension, a crowding out of labor.

In other words, it is central banks themselves that are behind the global economy’s dismal – and ever slowing – growth rate.

Viewed in this way, financialization can be judged to be a zero-sum game whereby what is good news for those long financial assets is bad news for those long income. The divergence of the lines in Charts 4 and 5 thus reflects a yawinng inequality gap that has grown markedly in the post-crisis period. This, in turn, has resulted in a growing segment of developed world populations becoming disaffected as they fall further behind and are, as a result, increasingly looking for nonestablishment political solutions. This is not simply of sociological interest but also of keen strategic importance as it argues that populism itself is structural in nature – it is a struggle for a fairer slice of the pie.

Translation: those central bankers still stumped by what trigger event unleashed Brexit, Trump and a wave of populist anger across the entire world, should look in the mirror.

This push for redistribution underpinning the populist groundswell – and the 2020 Democratic primary – is taking the historically consistent from of pushing for redistribution from foreigners to domestics which, in resulting in the erection of real and metaphorical walls (tariffs, Brexit, the US-Mexico wall), is both creating cross-border frictions and weighing on confidence more broadly. As a result, the pie itself will grow more slowly and may ultimately begin to shrink only intensifying the struggle for a fairer slice.

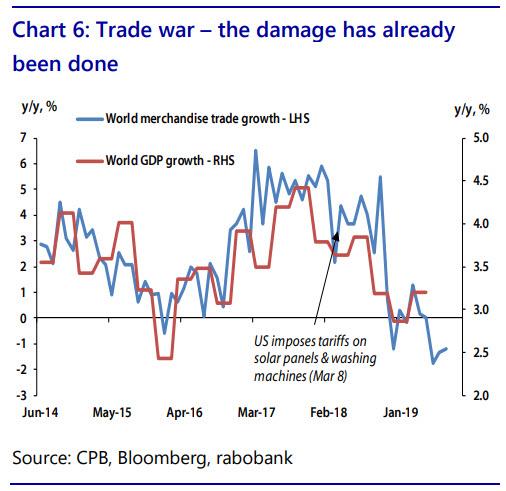

The next chart shows that notable damage has already been done, with the contraction of global merchandise trade growth portending a notable deceleration in world output even if trade-related tensions do not further intensify.

According to Lambregts, “this structural view of the world is crucial given the fact that politics is currently driving the market and politics, by its very nature, is noisy.” The above framework also allows the investor to look through this noise as it highlights the fact that Brexit/trade wars/the broadening out of social unrest in apparently unconnected parts of the world are but symptoms of a broader problem of growing inequality. As a consequence, politically-motivated improvements in market sentiment are purely tactical retracements in an otherwise longer-run strategically bullish trend.

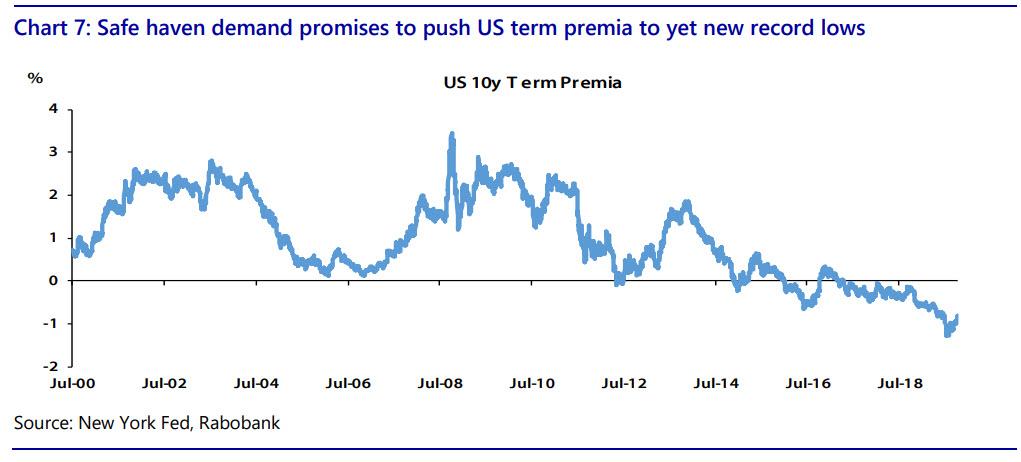

As such, Rabo concludes that populism is here to stay and represents a chronic downside risk to global demand. It also

promises to intermittently trigger flights to quality which Rabobank believes opens the way for US term premia dropping to new record lows in the coming year – Rabo believes that 10Y TSY yields will drop to just 1.00% by the end of 2020.

So what do all of the above structural issues have to do with the current central bank response?

As Rabobank explained next, the Fed is effectively responding to the above structural problems with a cyclical tool – lower policy rates. At best, this cyclical/structural mismatch could be construed as seeing this response as ineffectual; at worst Lambregts warns that “it could actually prove to be self-defeating.” The latter refers to the fact that, in so far as an easier policy stance insulates risky assets (such as equities) from the fallout from elevated geopolitical concern, the Fed is actually be providing President Trump with a freer hand in terms of ratcheting tension with China yet higher, something we discussed in August.

In other words, the Fed is inadvertently enabling Trump in his crusade to protect the US from perceived unfair trading practices and, in so doing, is paradoxically – as we explained in our take of Bill Dudley’s shocking Bloomberg op-ed – increasing the geopolitical threats to growth and inflation. In this way, as Rabobank writes, one could argue that this time really is different in that Fed rate cuts could conceivably have a paradoxically disinflationary effect. One can also make this argument by observing the exponential propagation of zombie companies, kept alive only thanks to low interest rates, and whose very existence is a scramble to capture market share irrelevant of the cost, which of course is profoundly deflationary.

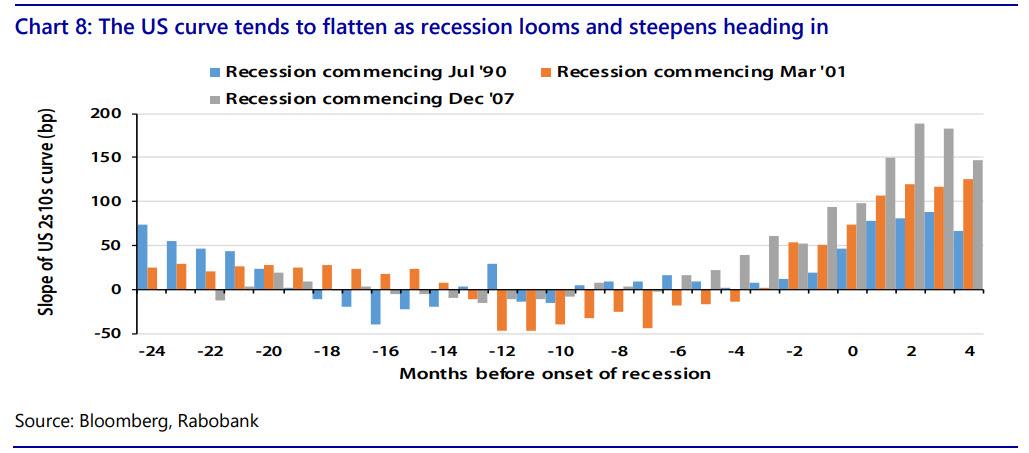

If true, the flattening of the US curve that has been seen heading into previous recessions (as shown in Chart 8 below) could be more intense this time round and the re-steepening heading into the next recession to be less pronounced.

This “this time is different” view has significant resonance with developments in the currency market, the Dutch bank adds. As the Fed embarked upon what it itself has branded a “mid-cycle adjustment”, the consensus very strongly favored a concomitant weakening of the dollar on the back of diminishing rate differentials. This view, as both we and now Rabo, noted missed three key points.

First, the Fed has been cutting rates owing to mounting downside risks to growth but growth has been slowing much faster outside of the US (which is dollar positive).

Second, geopolitical tension (potentially underpinned by Fed stimulus itself) has underpinned demand for safe assets (dollar positive).

Third, an escalation of the trade war lends itself to speculation over a narrowing US trade deficit which, in reducing the global supply of dollars, is a further positive for the greenback.

This is shown in Chart 9 above which shows the trade-weighted dollar from November 2016 (when Mr Trump became President Trump) to now. As shown, Trump’s accession to the White House triggered a long run decline in the dollar which was subsequently reversed with the onset of the trade war (appreciating by a little over 9% from March 2018). Meanwhile, as also shown above, short-dated US yields have collapsed in recent months as the escalating trade war triggered a policy turnaround by the Fed. The reason for plotting these two series side by side is to throw into relief the fact that, for those who have borrowed dollars outside of the US, any hoped for decline in the cost of servicing these obligations from lower rates when it comes to rolling them over is more than offset by the sizeable increase in repaying these debts from a local currency perspective.

Nowhere is this a more acute concern than for emerging markets, where dollar borrowing exploded in the wake of QE (and the accompanying lowering of dollar borrowing costs effected by the purchase program). Chart 10 above is based on BIS data which shows that dollar borrowing on the part of EM non-bank borrowers has jumped by 147% since the Fed first started buying USTs in March 2009. The added cost of rolling these debts over owing to the dollar’s resurgence represents a key threat to global growth and one the BIS has regularly highlighted.

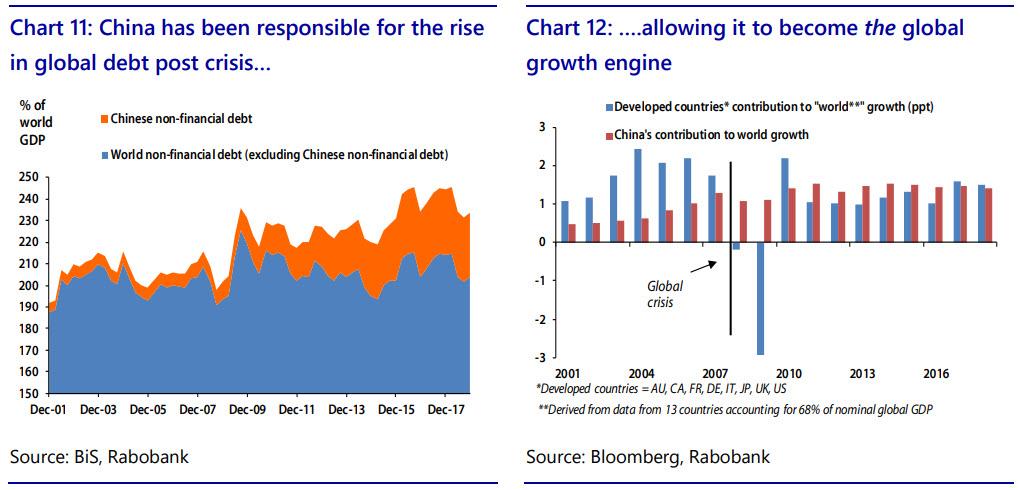

Taking a closer look at EM debt, Chart 11 below shows world non-financial debt as a share of world GDP (the blue area) together with Chinese private non-financial debt also expressed as a share of world GDP. As can be seen, the rise in global indebtedness in the post-crisis period is accounted for entirely by increasing Chinese leverage. This is key as this explains our long-running thesis why China successfully became the global growth engine over the past decade. This is further demonstrated in Chart 12 which shows Rabobank’s estimates of the percentage point contribution to world growth on the part of developed countries and that on the part of China alone. Since the Global Financial Crisis, China has, on average, accounted for one half of the increase in global output. Finally, this also explains our long-running argument (refreshed most recently just two weeks ago in “Here’s The Simple Reason Why A Global Economic Recovery Is Not Coming” ) that absent a recovery – and fresh growth – in China, the world is doomed to recession if not worse.

So in addition to the higher cost of EM dollar borrowing, the rapid build-up of debt within the region also raises a clear question mark over the outlook for global demand. EM non-financial debt currently stands at 183% of EM GDP vs. 107% at the end of 2008. While it is hard to predict how far these liabilities could yet rise before a crisis is triggered, it is safe to suggest we are closer to the end than the beginning of this process. As a consequence, and in sharp contrast to 2008, it is hard to see who will step in to support demand as the current global slowdown unfolds. In the absence of Deus ex Machina (Deus ex Ma-China?), the current low level of long-dated yields in the developed world appears perfectly logical if not poised for an additional leg lower.

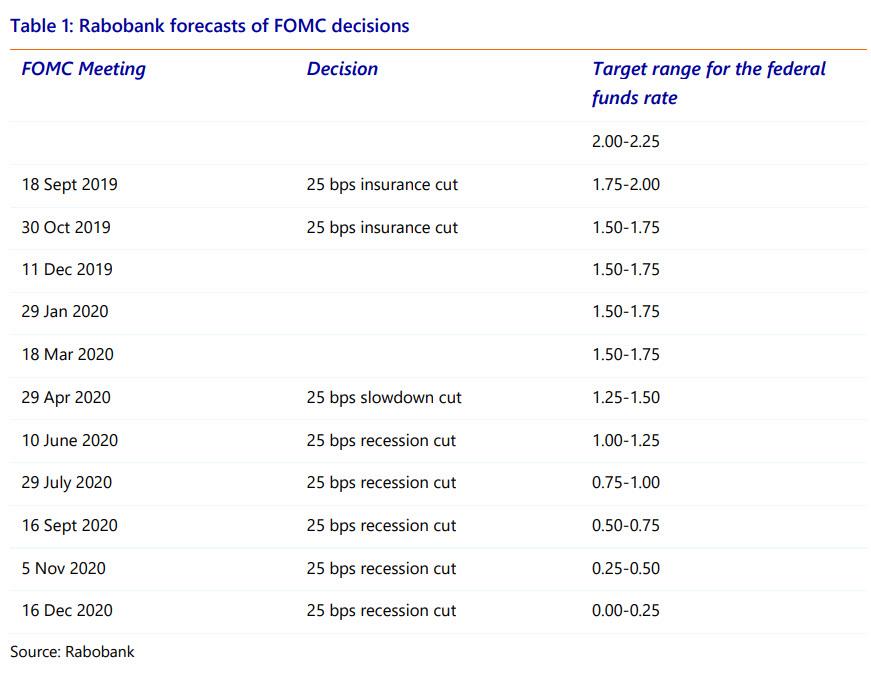

In light of the gloomy structural framework detailed above, it will come as little surprise that Rabobank’s outlook for rates is not so much “lower for longer as lower forever.” Charts 13 and 14 below show the bank’s forecasts for US policy rates and yields through to the end of next year. The bank’s Fed watcher, Philip Marey, who has been spot on in his Fed calls in the past two years, expects the Fed to be forced into cutting policy rates once again in April 2020 as a slowdown becomes more pronounced. With this deceleration of activity seen triggering a recession in the second half of next year, Rabo’s base case is for the Fed to cut rates at each subsequent meeting taking the lower end of the fed Funds target range to zero by the end of the year (a development that will naturally prompt discussion of another wave of, self-defeating, QE in addition to the NOT QE we have right now).

Finally, in terms of specific asset price targets, Rabo expects 10y yields to hit a new record low in H2 2020 with 1.0% currently viewed as the resting point at the end of the year, and strikingly, the bank states that it views the risks to this forecast “to be titled to the downside”!

Perhaps 2020 is the year when NIRP finally comes to the US? And while purely anecdotal, this view was endorsed by the 15 accounts that Rabo’s rates strategists visited on the US East Coast in October. The question they received most regularly from these investors was not whether USTs offered value (the clear consensus was that they most certainly do) but rather “what the likelihood was of US yields ultimately ending in negative territory. “

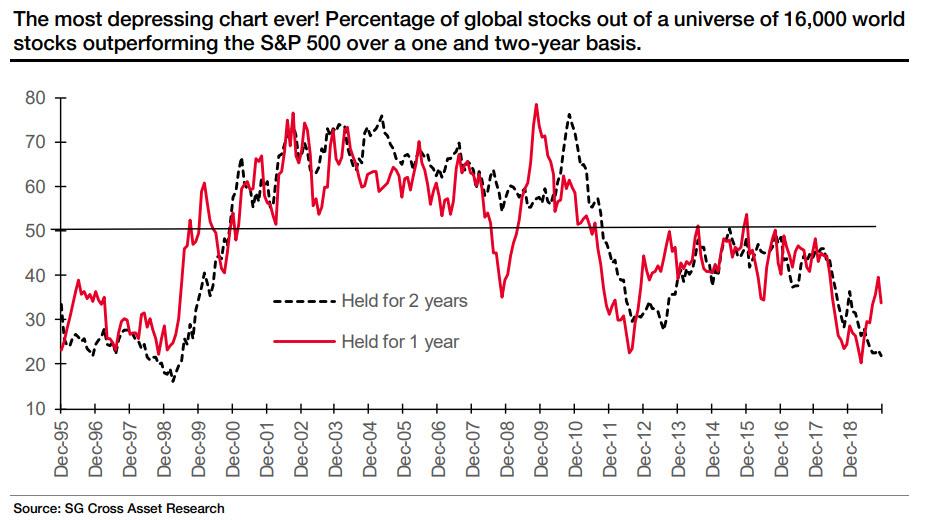

Whereas SocGen’s Albert Edwards is mostly concerned with global macro phase transitions, and specifically when the current global economy will transform into a terminal deflationary singularity, one which Edwards calls the “Ice Age”, his just as bearish SocGen colleague Andrew Lapthorne has been more preoccupied with the micro in recent years, and this morning the strategist believes he has uncovered the “most depressing chart ever” (especially for active managers).

The chart, shown below, measures how many of the world’s 16,000 stocks have beaten the S&P 500 over one and two years. What it finds is that over the last couple of years, nearly 80% of stocks have failed to beat the broader index, making a mockery of the concept of “alpha” creation, and paying someone 2 and 20 to find value beyond the broader market. On the other hand, with activist central banks actively targeting broad market indexes for the past decade, and especially any time there is even a modest swoon, or whenever they fill like boosting investor (and consumer) confidence with a little NOT QE here and not so little NOT QE there, it should not come as a surprise that it is now virtually impossible to outperform the overall market.

Below we present the highlights from Lapthorne’s note, which start of by noting that “if the world is heading into a slowdown, global equity markets don’t seem to be that bothered.”

MSCI World rose 2.7% in November, which leaves it up 21.7% in 2019. Of course, 2019 performance figures are helped by the starting point, which coincided with the turn of the year and a handbrake turn from the Fed. Picking a less generous starting point, say end-January 2018, and global equities have returned 8.6% versus 10% for 10-year global government bonds. On a total return or a risk-adjusted return basis you were better off owning bonds. Though really, and as ever, the best asset to own was simply the S&P 500.

Lapthorne then reminds us of Warren Buffett’s famous recommendation, which urged retail investors to buy the S&P 500, as stockpickers regularly failed to beat it.

“He’s not wrong. The strong performance of the S&P 500 leaves everything in its wake. This is lauded as a success and an abject failure of active fund management. But, the S&P 500 is less a measurement of corporate success and increasingly an ingredient of ever more complex financial products.”

Which brings us to the punchline: “Once in a while we create a chart that is truly depressing.”

The chart below measures the percentage of global developed and emerging market stocks that have beaten the S&P 500 on a total return USD basis over one and two years. This is a very big universe of 16,000 stocks and over the last couple of years 78% of stocks (so over 12,400 stocks) have failed to beat the S&P 500. Over the last year things have got a little better with only 66% of stocks underperforming. This high-profile index provides such a tough performance benchmark that increasing it convinces investors that just buying the S&P 500 will do.

As the Socgen strategist concludes, “this is a big shame” and explains why:

Not because I want to bang the drum for active management (admittedly a big part of our client basis), but if the measurement of company success is outperforming the 500 largest-cap US businesses supported by the US Federal Reserve, debt-funded share buybacks, and increasingly sophisticated financial products, then you can understand why less business are going public and private equity is booming. I find this depressing.”

So to all those who financial professionals who still foolishly support and cheer for the Fed, even though it is the Fed itself that is making all financial professionals obsolete in a world in which any dumb robot can just buy and hold the S&P for 0 and 0 as opposed to 2 and 20, we wonder just what else you need to see or experience before you too realize that central planning ends in tears for everyone involved. The only question is when.

House Democrats Mull Pivot Back To Russiagate To Pad Weak Case For Impeachment

As House Democrats cobble together a ‘less than compelling’ case for impeachment based on President Trump’s request that Ukraine investigate Joe Biden and his son for Obama-era dealings with the appearance of obvious corruption, some members of the House Judiciary Committee and ‘other more liberal-minded lawmakers and congressional aides’ are looking back to Russiagate and other accusations for new material to include in articles of impeachment, according to the Washington Post.

Members of the House Judiciary Committee and other more liberal-minded lawmakers and congressional aides have been privately discussing the possibility of drafting articles that include obstruction of justice or other “high crimes” they believe are clearly outlined in special counsel Robert S. Mueller III’s report — or allegations that Trump has used his office to benefit his bottom line. –Washington Post

That said, moderate Democrats wary of impeachment blowback in their GOP-heavy districts have pushed back against the idea, according to the report. In addition, Democratic leaders seeking to keep the impeachment case focused on Ukraine have resisted expanding the case against Trump as well.

The debate is expected to play out in leadership and caucus meetings this week, as the House Intelligence Committee prepares to hand the impeachment inquiry to the House Judiciary Committee. The Intelligence Committee is scheduled to vote Tuesday night on its final report on Ukraine, allowing Judiciary to then work on writing articles of impeachment based on that document.

But the Judiciary Committee also has asked other investigative panels to send any findings of Trump-related misdeeds that they believe are impeachable. And many of the committee members are hoping articles will refer to and cite their own months-long investigation into the Mueller report, which described 10 possible instances of obstruction by the president.

“One crime of these sorts is enough, but when you have a pattern, it is even stronger,” said Rep. Pramila Jaypal (D-WA), a member of the House Judiciary Committee and co-chairman of the Congressional Progressive Caucus – who added that there’s a strong case for citing the Mueller report in impeachment articles.

“If you show that this is not only real in what’s happening with Ukraine, but it’s the exact same pattern that Mueller documented . . . to me, that just strengthens the case,” she insisted.

Trump is accused of holding up nearly $400 million in military aid to Ukraine while simultaneously requesting that newly elected president, Volodomyr Zelensky, investigate the Bidens as well as other matters related to the 2016 US election. Zelensky, who didn’t know the aid was paused at the time, has insisted there was no quid pro quo, while several anti-Trump ambassadors who testified in front of Schiff’s committee could not establish that the aid hinged on Trump’s request. Instead, they assumed it did.

Perhaps this is about more than just having a weak hand on the Ukraine claims. Assuming the House votes to impeach, the GOP-controlled Senate will then hold a trial. If Democrats expand the scope of the impeachment, Senate Republicans would be forced to consider all claims levied at Trump – effectively reducing the spotlight on Ukraine by overwhelming the proceedings.

Whatever the case, even if the Trump-Ukraine claims are forced to share space with Russiagate and emoulments arguments for impeachment, Senate Republicans can still subpoena Joe and Hunter Biden to testify about Burisma, as well as House Intelligence Committee Chair Adam Schiff (D-CA), whose staff communicated with the CIA officer whose whistleblower complaint is at the heart of the impeachment.

Earlier this week, House Republicans issued a “prebuttal” of the upcoming House Intelligence Committee report expected to outline claims that Trump abused his power.

In a 123-page document, GOP investigators assert that Democrats failed to make the case that Trump committed impeachable high crimes and misdemeanors by withholding military aid and a highly sought-after White House meeting to compel Ukraine to launch investigations into his political rivals. Nor, the Republicans say, do Democrats have a basis for impeachment in Trump’s decision to spurn House document requests and witness subpoenas pertaining to Trump’s Ukraine dealings.

Instead, the GOP document contends, the impeachment effort is “an orchestrated campaign to upend our political system” — one “based on the accusations and assumptions of unelected bureaucrats who disagreed with President Trump’s policy initiatives and processes.”

According to the GOP report, “The evidence presented does not prove any of these Democrat allegations, and none of the Democrats’ witnesses testified to having evidence of bribery, extortion, or any high crime or misdemeanor.”

According to a press release on Dec. 3, the currency is part of a broader initiative to grow the local fintech sector and will be presented during the BVI Digital Economy symposium.

The coin will be a stablecoin pegged 1:1 to the U.S. dollar — which the BVI have used since 1959 — and its use is expected to reduce transactional fees, increase transaction speed and be accessible to outsiders such as tourists.

LifeLabs is also developing Rapid Cash Response, a fund meant to provide aid in case of a national emergency. The local government already announced this initiative in April. BVI Premier Andrew Fahie said:

“The importance of blockchain technology and the significant benefits it offers the BVI, are paramount to the Territory. We welcome this innovation with open arms. Our partner, LIFElabs, has demonstrated with their proven track record that their ideology is not just mere words, and we look forward to continuing our partnership with them on the rollout of BVI~LIFE, our digital currency.”

The Life token will serve as gas

LifeLabs community manager Anwar Ali claimed that the transaction fees of the BVI~LIFE stablecoin will be paid in the firm’s Life tokens. According to cryptocurrency data website Coin360, the Life token’s price increased by nearly 31% over the last 24 hours, reaching $0.000083.

While the BVI may be considering a dollar-pegged stablecoin, the Marshall Islands are developing a token in an effort to move away from the United States’ fiat currency. Earlier this year, officials announced that the Pacific island nation would develop a digital Sovereign that would be easily transmittable over the many islands that make up the country.

Fresh from their successful effort to kill Amazon’s plan for a second headquarters in New York City, Queens-area politicians, including “squad” member Rep. Alexandria Ocasio-Cortez (D–N.Y.), are trying to stop another mega-development at Sunnyside Yards.

There are good reasons to be skeptical of the Sunnyside Yards project, which involves building a massive deck over a 180-acre rail yard, creating space for the construction of new housing, offices, and community facilities. However, few of those reasons get a mention by Ocasio-Cortez and her anti-development allies.

“The proposal as it stands reflects a misalignment of priorities: development over reinvestment, commodification of public land over consideration of public good,” wrote Ocasio-Cortez and New York City Council Member Jimmy Van Bramer in a letter to the city’s Economic Development Corporation (EDC), which is coordinating an ongoing master planning process for the site.

“The proposed high-rise and mid-rise residential buildings would further exacerbate a housing crisis that displaces communities of color and parcels off public land to private real estate developers,” the two elected officials wrote.

Similar objections were raised in a letter by state Sen. Michael Gianaris (D–Queens), who wrote that the EDC “has not embraced a democratic process in implementing public input that prioritizes environmental and social justice.”

The argument that building housing where none currently exists would lead to displacement, and that dense urban development near transit would contribute to climate change, sparked a lot of eye-rolling from free market urbanists.

AOC & co. are trying to block the Sunnyside Yards project in the name of stopping displacement.

It would add 10s of thousands of units in a housing-starved city, atop a rail yard where nobody even lives. https://t.co/ZN7aswmIMk

AOC and the local council member (who once killed a 100% affordable housing project because, among other things, it didn't have enough parking) cite global warming and NYC's persistent housing crisis as reasons to be concerned about proposals to build densely near transit https://t.co/DR9KziGXUj

Michael Hendrix, the Manhattan Institute’s director of local and state policy, dismisses Ocasio-Cortez’s reasons for opposing the project as “garden-variety NIMBYism.”

The development of Sunnyside Yards offers the possibility of adding lots of new housing units, which should have the effect of reducing, not raising, housing costs and displacement.

A 2017 feasibility study prepared by the EDC at the instruction of Mayor Bill de Blasio—who’s been an enthusiastic backer of the project for years—examined three possible development test cases. A “residential” test case estimated that as many as 24,000 new units, including 7,200 that would be affordable, could be built on a decked-over version of Sunnyside Yards, alongside commercial and community space.

The other two test cases studied by the EDC envisioned less housing and more office or commercial space. Even these scenarios estimated that a Sunnyside Yards project could create a minimum of 14,000 new housing units.

That same 2017 feasibility study also identified a huge problem for project boosters: The cost of building a deck over Sunnyside Yards would massively outweigh the value of the development-friendly land that the deck is supposed to create.

The EDC study found that a deck over the rail yard would create between $3.33 billion and $3.98 billion in gross land proceeds. It also found that the costs of building the deck and supporting infrastructure would cost between $5.3 billion and $6.8 billion.

In other words, under the best-case-scenario, building a deck over Sunnyside Yard would lose $1.73 billion, with the potential for losses as high as $3.48 billion. This would, in effect, require government subsidies to make any development of Sunnyside Yards viable.

“A negative residual land value suggests that public investment is necessary to facilitate development,” reads the EDC report.

A negative residual land value also suggests that the development is not currently worth the expense, says Eric Kober, a former city planner and adjunct scholar the Manhattan Institute.

“For [Sunnyside Yards] to be viable in the long-term, the land that is being created on top of the rail yard would have to be extremely valuable. Right now, it’s not very valuable,” Kober says. “It’s not very valuable because there’re alternative places to do real estate development.”

According to Kober, there are still a lot of areas with development potential in New York City that don’t require building super-expensive decks over rail yards, including land adjacent to Sunnyside Yards in the Long Island City neighborhood, which is zoned for low-density manufacturing. Rezoning that land to allow for housing development would be a far would cost-effective way of adding new units, says Kober.

“One could imagine some decades from now, that all those opportunities will have been seized” and Sunnyside Yards becomes valuable enough to justify its development, he says. “That is not the case today.”

Of course, rezoning nearby areas to allow for redevelopment would also likely provoke the exact same concerns from anti-development politicians opposing Sunnyside Yards. Indeed, Justice For All—a community group opposed to the Sunnyside Yards project—has called for an immediate moratorium on all building permits in Long Island City.

That’s a counter-productive attitude. New York City is a rapidly growing urban area that’s been adding jobs much faster than it has been adding housing over the past decade.

The result is that more people are competing for the same number of housing units, raising rents for those who can afford to stay in the city, and forcing those who can’t into longer and longer commutes from comparatively cheaper suburbs.

Making New York City a more affordable place to live requires accommodating the city’s growth with more housing development, not fighting against such development.

Ocasio-Cortez’s opposition to Sunnyside Yards is rooted in an anti-growth mentality that will worsen problems of affordability and displacement—the very problems the congresswoman is clearly concerned about.

The master planning process for Sunnyside Yards is expected to be completed sometime next year. After that, any project at the site will spend years going through environmental review and the city’s planning process.

from Latest – Reason.com https://ift.tt/33OMMuJ

via IFTTT

Fresh from their successful effort to kill Amazon’s plan for a second headquarters in New York City, Queens-area politicians, including “squad” member Rep. Alexandria Ocasio-Cortez (D–N.Y.), are trying to stop another mega-development at Sunnyside Yards.

There are good reasons to be skeptical of the Sunnyside Yards project, which involves building a massive deck over a 180-acre rail yard, creating space for the construction of new housing, offices, and community facilities. However, few of those reasons get a mention by Ocasio-Cortez and her anti-development allies.

“The proposal as it stands reflects a misalignment of priorities: development over reinvestment, commodification of public land over consideration of public good,” wrote Ocasio-Cortez and New York City Council Member Jimmy Van Bramer in a letter to the city’s Economic Development Corporation (EDC), which is coordinating an ongoing master planning process for the site.

“The proposed high-rise and mid-rise residential buildings would further exacerbate a housing crisis that displaces communities of color and parcels off public land to private real estate developers,” the two elected officials wrote.

Similar objections were raised in a letter by state Sen. Michael Gianaris (D–Queens), who wrote that the EDC “has not embraced a democratic process in implementing public input that prioritizes environmental and social justice.”

The argument that building housing where none currently exists would lead to displacement, and that dense urban development near transit would contribute to climate change, sparked a lot of eye-rolling from free market urbanists.

AOC & co. are trying to block the Sunnyside Yards project in the name of stopping displacement.

It would add 10s of thousands of units in a housing-starved city, atop a rail yard where nobody even lives. https://t.co/ZN7aswmIMk

AOC and the local council member (who once killed a 100% affordable housing project because, among other things, it didn't have enough parking) cite global warming and NYC's persistent housing crisis as reasons to be concerned about proposals to build densely near transit https://t.co/DR9KziGXUj

Michael Hendrix, the Manhattan Institute’s director of local and state policy, dismisses Ocasio-Cortez’s reasons for opposing the project as “garden-variety NIMBYism.”

The development of Sunnyside Yards offers the possibility of adding lots of new housing units, which should have the effect of reducing, not raising, housing costs and displacement.

A 2017 feasibility study prepared by the EDC at the instruction of Mayor Bill de Blasio—who’s been an enthusiastic backer of the project for years—examined three possible development test cases. A “residential” test case estimated that as many as 24,000 new units, including 7,200 that would be affordable, could be built on a decked-over version of Sunnyside Yards, alongside commercial and community space.

The other two test cases studied by the EDC envisioned less housing and more office or commercial space. Even these scenarios estimated that a Sunnyside Yards project could create a minimum of 14,000 new housing units.

That same 2017 feasibility study also identified a huge problem for project boosters: The cost of building a deck over Sunnyside Yards would massively outweigh the value of the development-friendly land that the deck is supposed to create.

The EDC study found that a deck over the rail yard would create between $3.33 billion and $3.98 billion in gross land proceeds. It also found that the costs of building the deck and supporting infrastructure would cost between $5.3 billion and $6.8 billion.

In other words, under the best-case-scenario, building a deck over Sunnyside Yard would lose $1.73 billion, with the potential for losses as high as $3.48 billion. This would, in effect, require government subsidies to make any development of Sunnyside Yards viable.

“A negative residual land value suggests that public investment is necessary to facilitate development,” reads the EDC report.

A negative residual land value also suggests that the development is not currently worth the expense, says Eric Kober, a former city planner and adjunct scholar the Manhattan Institute.

“For [Sunnyside Yards] to be viable in the long-term, the land that is being created on top of the rail yard would have to be extremely valuable. Right now, it’s not very valuable,” Kober says. “It’s not very valuable because there’re alternative places to do real estate development.”

According to Kober, there are still a lot of areas with development potential in New York City that don’t require building super-expensive decks over rail yards, including land adjacent to Sunnyside Yards in the Long Island City neighborhood, which is zoned for low-density manufacturing. Rezoning that land to allow for housing development would be a far would cost-effective way of adding new units, says Kober.

“One could imagine some decades from now, that all those opportunities will have been seized” and Sunnyside Yards becomes valuable enough to justify its development, he says. “That is not the case today.”

Of course, rezoning nearby areas to allow for redevelopment would also likely provoke the exact same concerns from anti-development politicians opposing Sunnyside Yards. Indeed, Justice For All—a community group opposed to the Sunnyside Yards project—has called for an immediate moratorium on all building permits in Long Island City.

That’s a counter-productive attitude. New York City is a rapidly growing urban area that’s been adding jobs much faster than it has been adding housing over the past decade.

The result is that more people are competing for the same number of housing units, raising rents for those who can afford to stay in the city, and forcing those who can’t into longer and longer commutes from comparatively cheaper suburbs.

Making New York City a more affordable place to live requires accommodating the city’s growth with more housing development, not fighting against such development.

Ocasio-Cortez’s opposition to Sunnyside Yards is rooted in an anti-growth mentality that will worsen problems of affordability and displacement—the very problems the congresswoman is clearly concerned about.

The master planning process for Sunnyside Yards is expected to be completed sometime next year. After that, any project at the site will spend years going through environmental review and the city’s planning process.

from Latest – Reason.com https://ift.tt/33OMMuJ

via IFTTT

Sen. Kamala Harris is calling it quits on running for president, the California Democrat confirmed publicly on Tuesday.

The news comes after a series of bad signs for the Harris 2020 campaign, including money troubles, low morale among staff, and a rapid drop in support in recent polls of Democratic voters.

Gabbard delivered several deadly blows to the Harris campaign, offering real talk during the Democratic debates about Harris’ criminal justice record and support for the status quo in Washington. While Harris should have been prepared for such attacks on her past record as a prosecutor, she responded to this and other Gabbard criticisms by making petty comments about Gabbard’s polling numbers and questioning Gabbard’s loyalty to the United States.

If Harris had merely been mush-mouthed about her time as a cop, that might have been one thing. But Harris also stumbled on a number of other critical issues, giving vague, convoluted, or ever-changing answers when asked about everything from Medicare for All to sex work decriminalization to school busing programs.

Harris’ tendency to mug for the camera and exhibit wild tone shifts during the debates didn’t do her any favors either. Even the Saturday Night Live portrayal of Harris (by actress Maya Rudoloph) centered on Harris’ striving for meme-wothy moments over substance when she’s on stage.

Still, the sudden announcement today that Harris would be suspending her 2020 campaign came to many as a surprise.

My campaign for president simply doesn’t have the financial resources we need to continue. I’m not a billionaire. I can’t fund my own campaign. And as the campaign has gone on, it’s become harder and harder to raise the money we need to compete.

In good faith, I can’t tell you, my supporters and volunteers, that I have a path forward if I don’t believe I do. So, to you my supporters, it is with deep regret ― but also with deep gratitude ― that I am suspending my campaign today.

This afternoon, Harris tweeted: “To my supporters, it is with deep regret—but also with deep gratitude—that I am suspending my campaign today. But I want to be clear with you: I will keep fighting every day for what this campaign has been about. Justice for the People. All the people.”

This may not be the last we hear of Harris this election, however. Harris “is a rather plausible VP selection for pretty much all of the leading contenders,” suggests FiveThirtyEight Editor Nate Silver, “and withdrawing now rather than after, say, a 6th place finish in Iowa or a 4th place finish in California probably helps preserve her reputation a bit.”

from Latest – Reason.com https://ift.tt/34RTC4k

via IFTTT

Macron Hits Back, Questions Trump: How Can Turkey Buy Russian S-400s & Remain In NATO?

Macron hits back after earlier in the day Trump took his NATO “brain death” comments to task saying they were “very nasty” remarks, and the French president also took a swipe at Turkey, saying “technically it is not possible” to purchase the S-400 anti-air defense system from the Russians and be a NATO member.

Sitting next to Trump and fielding questions from reporters outlining their respective views of the state of the NATO alliance, it was clear the recent ‘bromance’ is no longer going strong.

Trump actually laughed when Macron raised the heart of the Turkey issue, saying Erdogan can’t integrate Russian S-400 defense into NATO systems without deeply compromising the alliance. Macron questioned:

How is it possible to be a member of the alliance – to work with our office, to buy our materials, to be integrated – and to buy the S-400 from Russia? Technically it is not possible…

An incredulous Macron on Turkey: “How is it possible to be a member of the alliance..and to buy the S-400 from the Russians?”

The two sparred over the question of what to do with western and European foreign fighters leaving the battlefield in Syria.

Macron said to Trump, who in the past has claimed 100% defeat of ISIS: “The number one priority, because it’s not yet finished, is to get rid of ISIS…It’s not yet done. I’m sorry to say that.”

Wow. Macron calls for end of ambiguity with #Turkey regarding #ISIS fighters and “some of these groups.”

Macron also questions Trump on how Turkey can buy #Russia S-400 and be in NATO. Trump laughs. Body gestures here tell a lot: pic.twitter.com/5LTufZKLkR

“Would you like some nice ISIS fighters?” Trump asked. “I could give them to you, you could take every one you want.”

“Let’s be serious,” Macron responded.

Macron then took Turkey to task for now being on the wrong side of counterterror efforts in Syria:

“They now are fighting against those who fight with us, who fought with us, shoulder to shoulder, against ISIS,” Macron said of Turkey.

French President Emmanuel Macron says #NATO needs to talk about more than how much its members are paying, specifically Turkey’s military incursion in northern Syria. “When I look at Turkey, they are now fighting against those who fought with us against #ISIS.” pic.twitter.com/Qok3nFtDNU

Trump, who effectively green-lit Turkey’s Syria incursion by withdrawing U.S. forces from a region on Turkey’s border, again blamed his predecessor Barack Obama for pushing Erdogan toward Moscow by allegedly refusing to sell Ankara the U.S. Patriot missile system.

* * *

earlier

With his allies up in arms over his latest tariff threats directed at France, President Trump landed in London early Tuesday, accompanied by First Lady Melania Trump, for a two-day summit marking the 70th anniversary of the military alliance’s birth. Trump is notorious for blaming America’s NATO partners for not paying their fair share when it comes to financing the military alliance.

Sitting alongside NATO General Secretary Jens Stoltenberg at Winfield House in London, Trump delivered a rambling address that marked the beginning of the summit, bragging about his progress with China, and claiming that the US is doing ‘very well’ when it comes to the still-unsigned ‘Phase One’ trade agreement.

There was talk of arms control progress, with Trump insisting that “Russia wants to do something badly and so do we.”

During previous administrations, summits like this one would have been a snoozefest. But President Trump has spiced up several NATO summits by starting drama with one or more of his fellow Nato leaders.

Justin Trudeau and Angela Merkel have been favorite targets of his in the past; but Trump is focusing his ire on French President Emmanuel Macron.

The problem is that Macron apparently told The Economist Magazine that Nato was experiencing “brain death,” and warned that members of the alliance could no longer rely on the US.

Unsurprisingly, Trump took umbrage at this, and dedicated a few minutes of his opening press conference to trashing Macron, accusing him of being “very, very nasty” and that it was “very insulting” for the French president to label Nato “brain dead.”

Trump added that relations between the US and European Nato members were not causing any divide, except with France. He could even envision France ‘breaking’ away from the military alliance.

“I do see France breaking off. I’m looking at him and I’m saying he [Macron] needs protection more than anybody and I see him breaking off, so I’m a little surprised at that,” Trump said.

Returning to the tariffs once more, Trump slammed France for trying to raise money via a “digital tax” levy on US tech giants like Facebook and Google.

“They are starting to tax other people’s products, so we are going to tax them,” Trump said

He also took a swipe a France’s economy, with its high unemployment rate, claiming that the country was “not doing well economically at all.” There’s some truth to that: The Q3 unemployment rate climbed o 8.6%.

Of course, some of the most scathing criticism of Nato has come from President Trump, with the president repeatedly declaring the alliance obsolete.

The president also made some comments about the possibility of delaying notifications.