Submitted by Joseph Carson, Former Director of Global Economic Research, Alliance Bernstein

Stock market booms are often based on a “good” story or a narrative of better things to come. Excess liquidity usually provides the fuel for bull market runs, as fundamentals of growth and profits usually don’t play a major role, at least not initially.

In the past 5 years, the S&P 500 stock index has risen over 50% and during that period operating profits for non-financial companies have declined over 15%, a drop that has always been associated with economic recessions.

Source: Bloomberg

The big test for policymakers is how to assess when “irrational exuberance” over easy money has gone too far, creating a vision of little risks and a persistent bull market in stocks that unduly separates finance from the economy increasing the risk of a bad outcome?

The Great Divergence

The Bureau of Economic Analysis reported that Q3 operating profits for all US companies, large and small, public and private, totaled $2.087 trillion, off 0.8% from year ago levels. The decline in profits in the past year continues a long stretch of weak corporate earnings. In fact, operating profits peaked in Q3 2014 and over the past 5 years are off nearly 5%.

The weakness in operating profits is centered in non-financial companies—with the biggest declines in the manufacturing sector. In the past year, profits for non-financial corporate businesses declined nearly 5%, bringing the cumulative 5-year fall to 15.5%–three times larger than the decline for all companies.

Profit declines of this scale, and even less, have always been associated with an economic recession. In fact, since 1975, there have been 6 recessions and of those only two— the dot.com bust and the Great Financial Recession – recorded larger declines in operating profits than the current slump.

Yet, despite the decline in operating profits the broad equity markets has posted very strong gains, with the S&P 500 index up over 50% in the past 5 years, and the NASDAQ up over 80% – with both indexes posting gains of 25% to 30% in 2019 alone.

Divergence between profits and equity markets are not uncommon, but the scale and length of the current divergence is.

The primary fuel for the stock market run has been easy money and the promise of more easy money. Even though the economy’s performance in 2019 in terms of growth, jobless rate and core inflation was fairly close to the Fed’s forecast policymakers voted to reduce official rates three times instead of the initial plan to raise rates twice. That’s the equivalent of 125 basis points of an easier money stance relative what the financial markets had been expecting. Policymakers have also made a promise not to raise official rates until reported inflation is well above its preferred rate of 2%.

In 1996, Federal Reserve Chairman Alan Greenspan raised the question “how do we know when irrational exuberance has unduly escalated asset values? Nowadays a similar question can be directed to the Fed – “How do we know when irrational exuberance over the Fed’s policy of easy money has unduly escalated asset values?”

History clearly shows excess liquidity fuels bull markets, but money has to at some point work its way into the real economy, lifting growth and profits. Bubbles form when excess liquidity remains bottled in one segment of finance or single sector of the economy – like during the dot.com and housing bubbles.

Monetary policy can create liquidity, but it can’t direct its flow – and the current flow remains unbalanced between finance and the real economy.

Today is the first day of our annual webathon. All week, we’ll be asking you to help supportReason‘s journalism. Our goal is $200,000 this year, and we hope you’ll contribute. Besides the satisfaction of donating the worthy cause of free minds and free markets (plus the tax break!) there’s some pretty good swag. And you might as well donate early, since kicking in cash now will make the popups go away for the duration of the webathon.

You’re going to hear a bunch of reasons to give to Reason over the course of the webathon, but I’m going to kick things off by asking you to support our investigative reporting. We have many folks on staff who aren’t afraid to go spelunking and share what they find—but I want to highlight the work of two reporters: Elizabeth Nolan Brown and C.J. Ciaramella.

When we look back at more than 50 years of Reason archives, we’re especially proud of the causes we adopted back when everyone else thought they were hopeless or even downright crazy. Stuff like supporting gay marriage decades before even the Democratic Party came around. Or backing drug legalization at a time when “Just Say No” was a nearly unquestioned mantra. These are stories that required Reason journalists to see what others couldn’t, but also to seek out the facts necessary to set the record straight and win skeptics over to the cause of individual freedom.

The war on sex trafficking, as Brown has been explaining in our pages for years now, is the new war on drugs. In the last year, Brown obtained secret Department of Justice memos, got the principal players in the huge story of the shutdown of the adult classified site Backpage.com to go on the record exclusively with Reason, and generally scooped the heck out of everybody else covering this important beat thanks to a combination of hard-earned access and perseverance. All of this has been in the service of demonstrating how a well-intentioned effort has gone horribly awry, threatening not only the civil liberties and personal freedoms of consenting buyers and sellers of sex, but also everyone from internet users to airline travelers to hotel guests along the way.

C.J. Ciaramella is on another one of those beats that seem crazy until you win: criminal justice reform. Reason has been beating this particular drum for so long we’re getting carpal tunnel.

But Ciaramella wakes up every day and FOIAs a new police department or writes more scripts to get information from messy state data dumps or just scans local news for opportunities to get the rest of the story—the real story—after other outlets have replayed cellphone footage for the rubberneckers and moved on.

This year Ciaramella did a deep dive on rampant police abuse in Vallejo, California, and unearthed story after story of officer misbehavior going unpunished. He reported on an Alabama couple who lost their house after police raided their house, seized their cash, and ruined their lives for $50 of marijuana. He shared the tale of a woman who was desperate to get answers about her son’s death at the hands of New York police.

But when you do stuff like release secret government memos or publish deep dive on a controversial asset forfeiture case, you’d better be sure the whole shebang is airtight. And that’s where things get expensive. We are very lucky to have a barrel full of some of the smartest lawyers around sharing quarters here at Reason.com (hi Volokhers!) but sometimes you also need the kind of lawyers who want to be paid in actual money.

Court documents and Freedom of Information requests cost money (though they shouldn’t!). So do plane tickets to Arizona where your subjects are on house arrest. So does a big wall to tack up newspaper clippings and connect them with colored string. (Just kidding, Liz and C.J. don’t do that. Probably.) And coffee. Lots of coffee.

If you want to see more of the kind of investigative journalism Brown and Ciaramella produce, please consider donating to Reason. If you have donated in the past, thank you for your support. We hope you’ll donate again this year. If you haven’t donated before, but you like what you read, watch, and listen to at Reason, consider supporting the work of principled libertarian journalists who work hard to dig up truths no one else even thought to look for.

from Latest – Reason.com https://ift.tt/37Y84tk

via IFTTT

…we are reminded that it was his use of Twitter when talking about British cave diving hero Vern Unsworth that will be leading Musk into the courtroom this morning, as he heads to trial for allegedly defaming Unsworth when he referred to him as “pedo guy”.

Unsworth helped play a key role in saving 12 boys and their soccer coach who were trapped in the Tham Luang Nang Non cave in Thailand in July 2018.

Musk had proposed his own solution for the rescue, embarking on a boastful public quest to construct a device that could help rescue the trapped children. But, ultimately, the rescue was done by actual professionals and without the help of Musk.

In a post-rescue interview with CNN, Unsworth laughed off Musk’s proposed solution and told the billionaire he could “stick it where it hurts”, disregarding Musk’s effort as a “PR stunt”.

Musk, like a child who had just been bested on an elementary school playground, fired back by calling Unsworth names and insisting that he was a pedophile both on Twitter, and in communications with a reporter at BuzzFeed.

Unsworth obviously contends that Musk’s statements are false and that he should pay punitive and other damages for harming his reputation.

The trial will last about 5 days and Musk is scheduled to be one of the first, if not the first, witness to testify.

Several weeks ago, the judge presiding over the cast tossed the idea of Musk having a free speech defense, ruling that the statements did not have any basis in any public controversy involving Unsworth. Unsworth’s lawyer, L. Lin Wood said after the hearing that “the burden of proof for negligence is lower than that for actual malice”.

This means that Unsworth will only have to convince the jury by a preponderance of the evidence, rather than clear and convincing evidence, making it easier for the panel to find Musk liable for defamation, Wood said.

Punitive damages could come as a result of the jury finding that Musk acted with malice, according to Wood.

Recall, back in October, we noted that Musk called himself a “fucking idiot” of his choice of words about Unsworth when he emailed a reporter unverified information about the cave diver.

We also documented when Unsworth first filed suit in late 2018.

Today is the first day of our annual webathon. All week, we’ll be asking you to help supportReason‘s journalism. Our goal is $200,000 this year, and we hope you’ll contribute. Besides the satisfaction of donating the worthy cause of free minds and free markets (plus the tax break!) there’s some pretty good swag. And you might as well donate early, since kicking in cash now will make the popups go away for the duration of the webathon.

You’re going to hear a bunch of reasons to give to Reason over the course of the webathon, but I’m going to kick things off by asking you to support our investigative reporting. We have many folks on staff who aren’t afraid to go spelunking and share what they find—but I want to highlight the work of two reporters: Elizabeth Nolan Brown and C.J. Ciaramella.

When we look back at more than 50 years of Reason archives, we’re especially proud of the causes we adopted back when everyone else thought they were hopeless or even downright crazy. Stuff like supporting gay marriage decades before even the Democratic Party came around. Or backing drug legalization at a time when “Just Say No” was a nearly unquestioned mantra. These are stories that required Reason journalists to see what others couldn’t, but also to seek out the facts necessary to set the record straight and win skeptics over to the cause of individual freedom.

The war on sex trafficking, as Brown has been explaining in our pages for years now, is the new war on drugs. In the last year, Brown obtained secret Department of Justice memos, got the principal players in the huge story of the shutdown of the adult classified site Backpage.com to go on the record exclusively with Reason, and generally scooped the heck out of everybody else covering this important beat thanks to a combination of hard-earned access and perseverance. All of this has been in the service of demonstrating how a well-intentioned effort has gone horribly awry, threatening not only the civil liberties and personal freedoms of consenting buyers and sellers of sex, but also everyone from internet users to airline travelers to hotel guests along the way.

C.J. Ciaramella is on another one of those beats that seem crazy until you win: criminal justice reform. Reason has been beating this particular drum for so long we’re getting carpal tunnel.

But Ciaramella wakes up every day and FOIAs a new police department or writes more scripts to get information from messy state data dumps or just scans local news for opportunities to get the rest of the story—the real story—after other outlets have replayed cellphone footage for the rubberneckers and moved on.

This year Ciaramella did a deep dive on rampant police abuse in Vallejo, California, and unearthed story after story of officer misbehavior going unpunished. He reported on an Alabama couple who lost their house after police raided their house, seized their cash, and ruined their lives for $50 of marijuana. He shared the tale of a woman who was desperate to get answers about her son’s death at the hands of New York police.

But when you do stuff like release secret government memos or publish deep dive on a controversial asset forfeiture case, you’d better be sure the whole shebang is airtight. And that’s where things get expensive. We are very lucky to have a barrel full of some of the smartest lawyers around sharing quarters here at Reason.com (hi Volokhers!) but sometimes you also need the kind of lawyers who want to be paid in actual money.

Court documents and Freedom of Information requests cost money (though they shouldn’t!). So do plane tickets to Arizona where your subjects are on house arrest. So does a big wall to tack up newspaper clippings and connect them with colored string. (Just kidding, Liz and C.J. don’t do that. Probably.) And coffee. Lots of coffee.

If you want to see more of the kind of investigative journalism Brown and Ciaramella produce, please consider donating to Reason. If you have donated in the past, thank you for your support. We hope you’ll donate again this year. If you haven’t donated before, but you like what you read, watch, and listen to at Reason, consider supporting the work of principled libertarian journalists who work hard to dig up truths no one else even thought to look for.

from Latest – Reason.com https://ift.tt/37Y84tk

via IFTTT

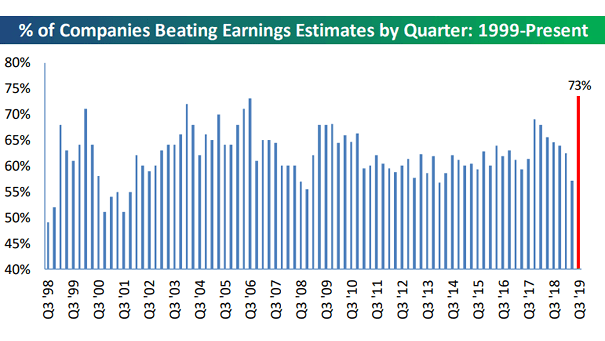

With the third quarter of 2019 reporting season mostly behind us, we can take a look at what happened with earnings to see what’s real, what’s not, and what it will mean for the markets going forward.

The Good

As always is the case, the majority of companies beat their quarterly estimates, as noted by Bespoke Investment Group.

With 73% of companies beating estimates, it certainly suggests that companies in the S&P 500 are firing on all cylinders, which should support higher asset prices.

However, as they say, the “Devil is in the details.”

One of the reasons given for the push to new highs was the ‘better than expected’ earnings reports coming in. As noted by FactSet:

“73% have reported actual EPS above the mean EPS estimate…The percentage of companies reporting EPS above the mean EPS estimate is above the 1-year (76%) average and above the 5-year (72%) average.”

The problem is the ‘beat rate’ was simply due to the consistent ‘lowering of the bar’ as shown in the chart below:

Beginning in mid-October last year, estimates for both 2019 and 2020 crashed.

This is why I call it ‘Millennial Soccer.’

Earnings season is now a ‘game’ where scores aren’t kept, the media cheers, and everyone gets a ‘participation trophy’ just for showing up.

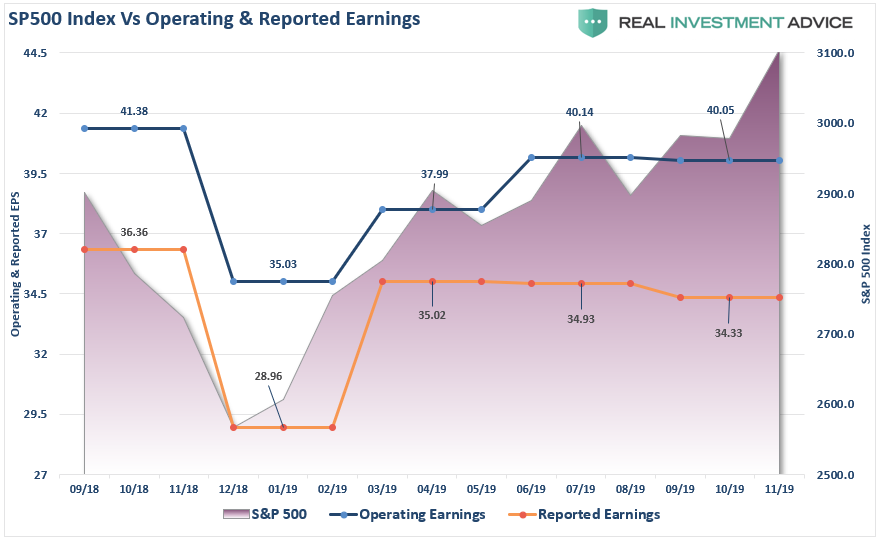

Let’s take a look at what really happened with earnings.

During Q3-2019, quarterly operating earnings declined from $40.14 to $40.05 or -0.25%. While operating earnings are completely useless for analysis, as they exclude all the “bad stuff” and mostly fudge the rest, reported earnings declined by from $34.93 to $34.33 or -1.75%.

While those seem like very small declines in actual numbers, context becomes very important. In Q3-2018, quarterly operating earnings were $41.38 and reported earnings were $36.36. In other words, over the last year operating earnings have declined by -3.21% and reported earnings fell by -5.58%. At the same time the S&P 500 index has advanced by 7.08%.

It’s actually worse.

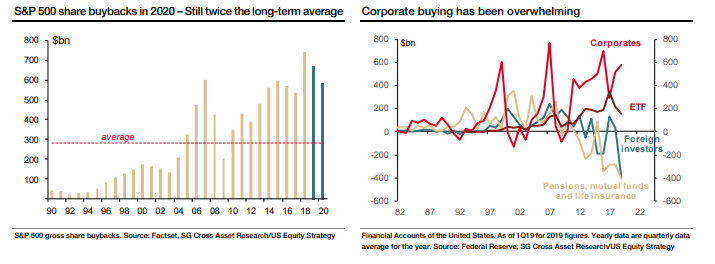

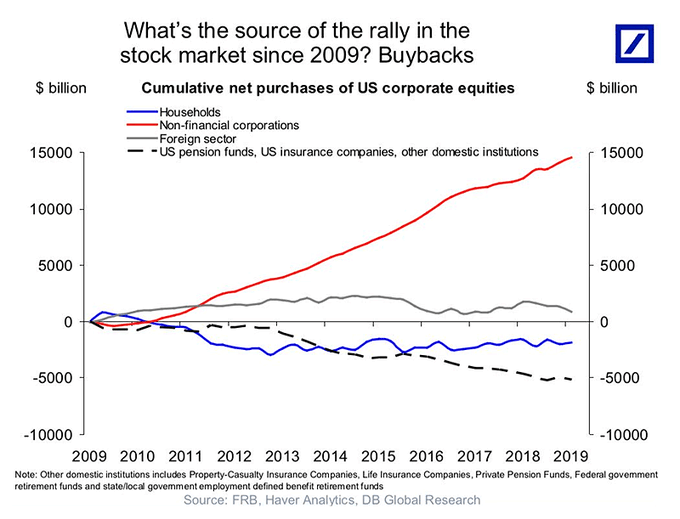

Despite the rise in the S&P 500 index, both Operating and Reported earnings have fallen despite the effect of substantially lower tax rates and massive corporate share repurchases, which reduce the denominator of the EPS calculation.

“Research published by the French bank Societe Generale shows that S&P 500 companies have bought back the equivalent of 22% of the index’s market capitalization since 2010, with more than 80% of the companies having a program in place.

The low cost of debt is one reason for the surge, with interest rates not that far above zero, and President Trump’s package of tax cuts in 2017 further triggered a big repatriation of cash held abroad. Since the passage of the Tax Cuts and Jobs Act, non-financial U.S. companies have reduced their foreign earnings held abroad by $601 billion.

This repatriation may have run its course, and stock buybacks should decline from here, but they will still be substantial.”

This is no small thing.

As noted in “4-Risks To The Bullish View,” previously, share repurchases have made up roughly 100% of the net purchases of stocks over the last year.

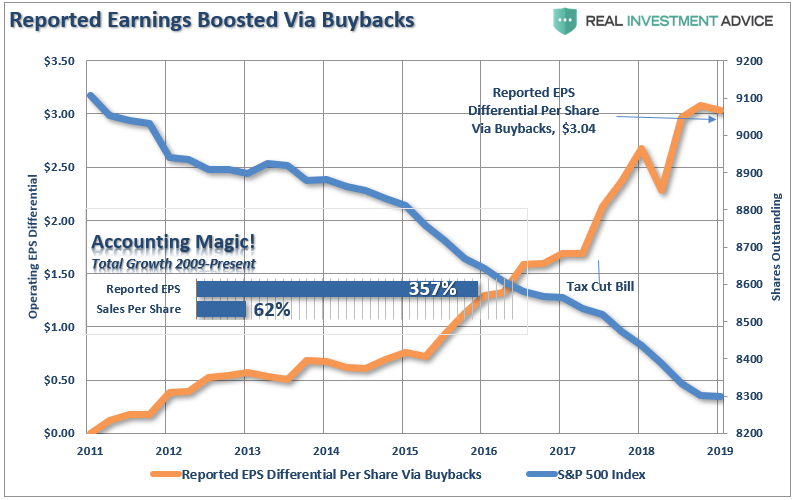

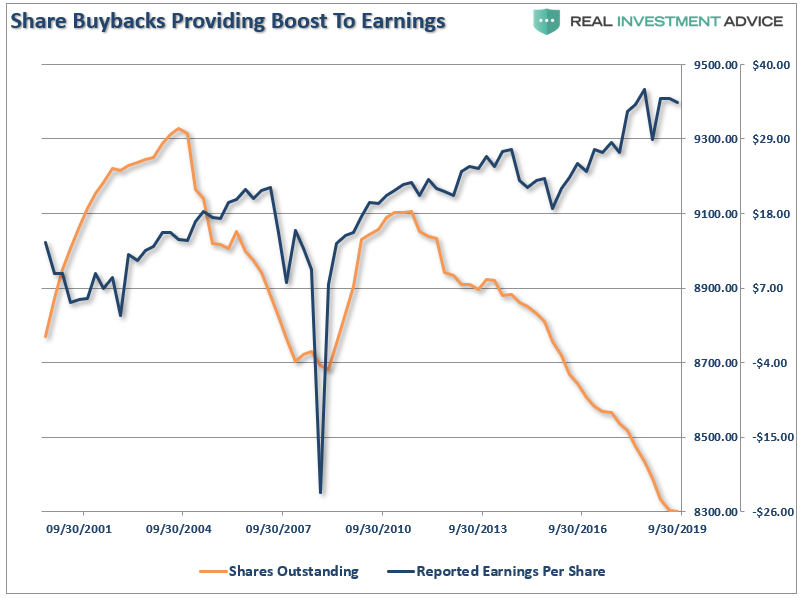

We have discussed the issue of “share buybacks” numerous times and the distortion caused by the use of corporate cash to lower shares outstanding to increase earnings per share.

“The reason companies spend billions on buybacks is to increase bottom-line earnings per share, which provides the ‘illusion’ of increasing profitability to support higher share prices. Since revenue growth has remained extremely weak since the financial crisis, companies have become dependent on inflating earnings on a ‘per share’ basis by reducing the denominator.As the chart below shows, while earnings per share have risen by over 360% since the beginning of 2009; revenue growth has barely eclipsed 50%.”

Chart updated through Q3-2019

The problem with this, of course, is that stock buybacks create an illusion of profitability. However, for investors, the real issue is that almost 100% of the net purchases of equities has come from corporations.

The issue is two-fold:

That corporate spending binge is slowing down, as noted by Mr. Goldstein; and,

If a recession sets in, share repurchases could easily cease altogether.

If you don’t think that’s important, the charts above and below should at least make you reconsider.

Of course, such should not be a surprise.

Since the recessionary lows, much of the rise in “profitability” have come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, which is directly connected to a consumption-based economy, has remained muted.

Since 2009, the operating earnings per share of corporations has risen 296%. However, the increase in earnings did not come from a commensurate increase in actual revenue which has only grown by a marginal 62% during the same period. At the same time, investors have bid up the market more than 300% from the financial crisis lows of 666.

Needless to say, investors are once again extremely optimistic they haven’t overpaid for assets once again.

Always Optimistic

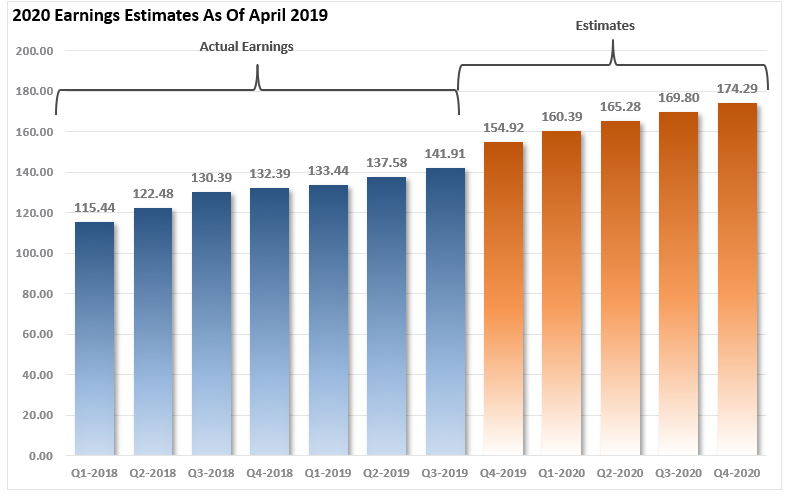

But optimism is certainly one commodity that Wall Street always has in abundance. When it comes to earnings expectations, estimates are always higher regardless of the trends of economic data. As shown, Wall Street is optimistic the current earnings decline is just a blip on the way to higher-highs.

As of April 2019, when Wall Street first published their estimates for 2020, the expectations were that earnings would grow to $174.29 by the end of next year.

The difference between Wall Street’s expectations and reality tends to be quite dramatic.

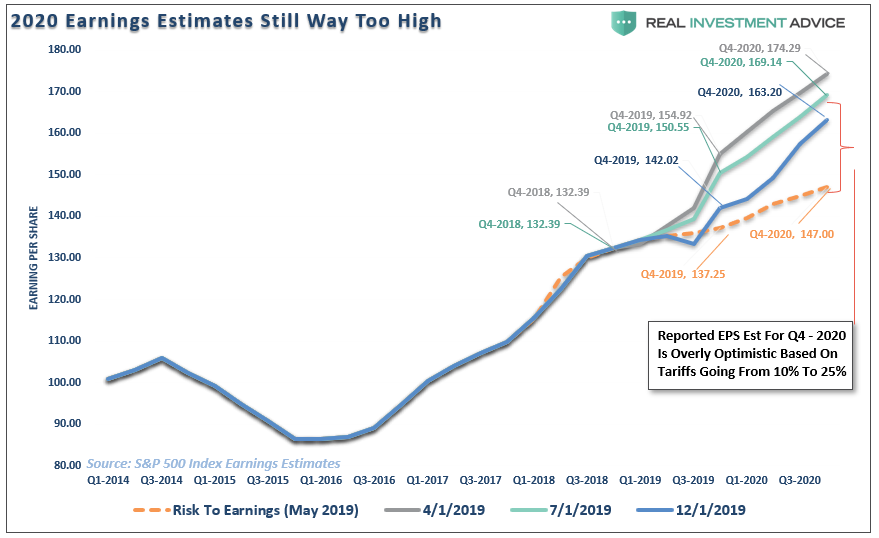

You can see the over-optimism collided with reality in just a few short months. Since April, forward expectations have fallen by more than $11/share as economic realities continue to impale overly optimistic projections.

Unfortunately, estimates are still too high and have further to fall. It is very likely, particularly if “tariffs” remain in place into 2020, that the majority of expected earnings growth will be reversed.

(This shouldn’t surprise you. We previously warned that by the end of 2018, the entirely of the “Trump Tax Cut” benefit would be erased.)

The Ugly

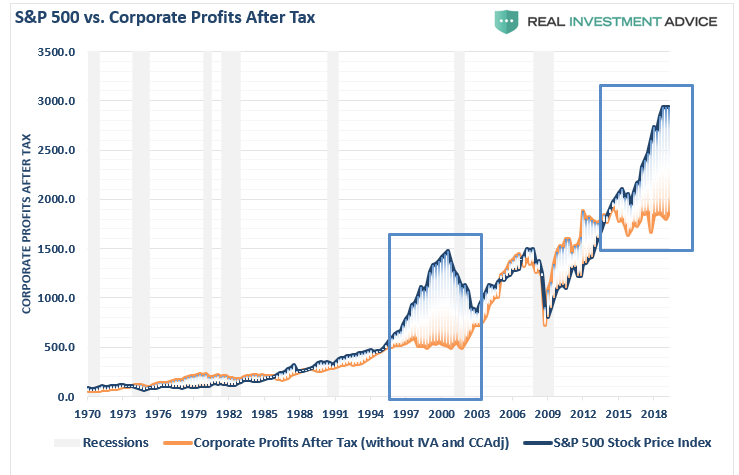

This divergence in stock prices not only shows up in operating earnings but also in reported corporate profits. As noted previously,the deviation between prices and profits is at historically high levels which cannot be sustained indefinitely.

“If the economy is slowing down, revenue and corporate profit growth will decline also. However, it is this point which the ‘bulls’ should be paying attention to. Many are dismissing currently high valuations under the guise of ‘low interest rates,’ however, the one thing you should not dismiss, and cannot make an excuse for, is the massive deviation between the market and corporate profits after tax. The only other time in history the difference was this great was in 1999.”

While the market has rallied sharply in 2019 on continued “hopes” for a “trade deal,” and more accommodative actions from the Federal Reserve, the deviations from fundamentals have reached extremes only seen at peaks of previous market cycles.

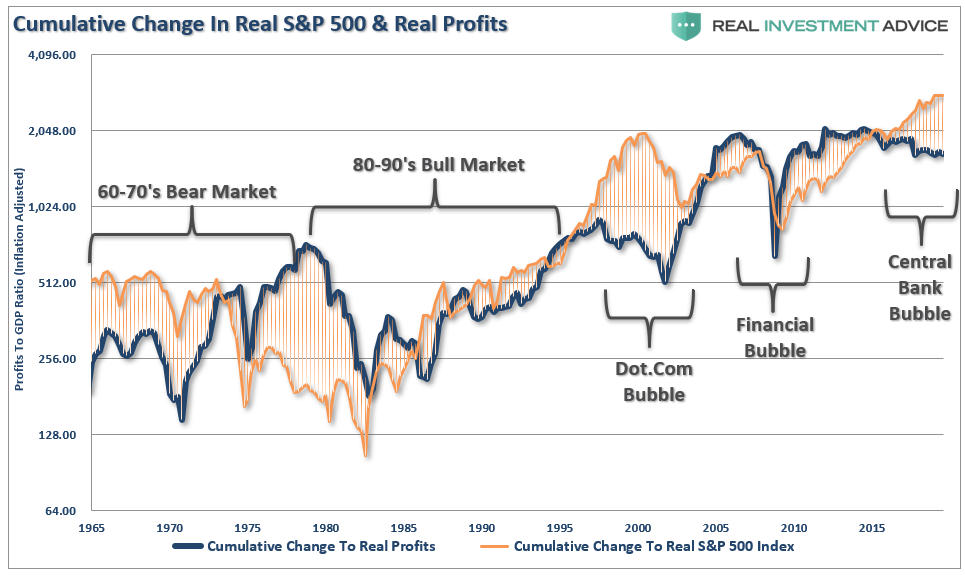

The chart below shows the real, inflation-adjusted, profits after-tax versus the cumulative change to the S&P 500. Here is the important point – when markets grow faster than profitability, which it can do for a while; eventually a reversion occurs. This is simply the case that all excesses must eventually be cleared before the next growth cycle can occur. Currently, we are once again trading a fairly substantial premium to corporate profit growth.

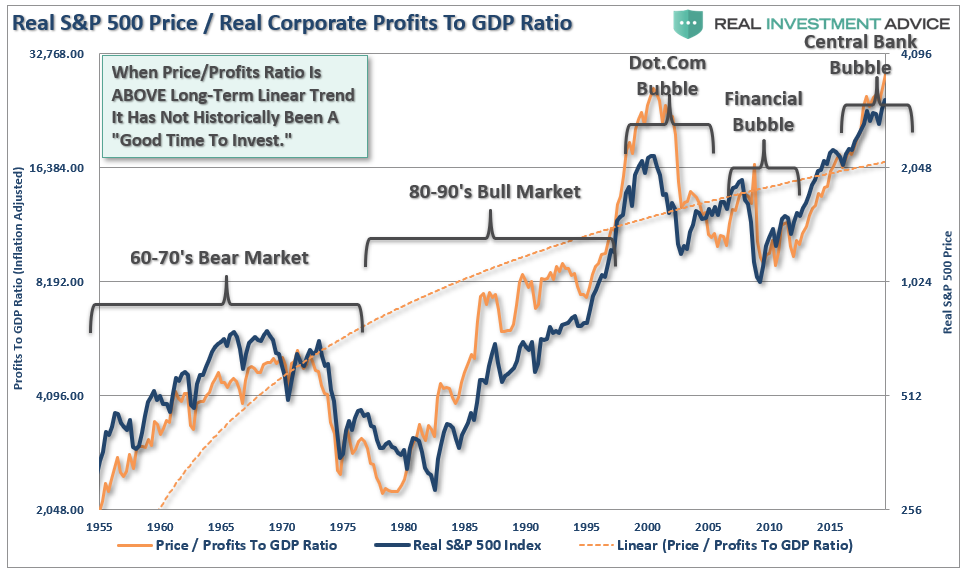

Since corporate profit growth is a function of economic growth longer term, we can also see how “expensive” the market is relative to corporate profit growth as a percentage of economic growth. Once again, we find that when the price to profits ratio is trading ABOVE the long-term linear trend, markets have struggled, and ultimately experienced a more severe mean-reverting event. With the price to profits ratio once again elevated above the long-term trend, there is little to suggest that markets haven’t already priced in a good bit of future economic and profits growth.

While none of this suggests the market will “crash” tomorrow, it is supportive of the idea that future returns will be substantially weaker in the future.

Currently, there are few, if any, Wall Street analysts expecting a recession currently, and many are certain of a forthcoming economic growth cycle. Yet, at this time, there are few catalysts supportive of such a resurgence.

Economic growth outside of China remains weak

Employment growth is going to slow.

There is no massive disaster currently to spur a surge in government spending and reconstruction.

There isn’t another stimulus package like tax cuts to fuel a boost in corporate earnings

With the deficit already pushing $1 Trillion, there will only be an incremental boost from additional deficit spending this year.

Unfortunately, it is also just a function of time until a recession occurs.

Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

While no one on Wall Street told you to be wary of the markets in 2018, we did, but it largely fell on deaf ears as “F.O.M.O.” clouded basic investment logic.

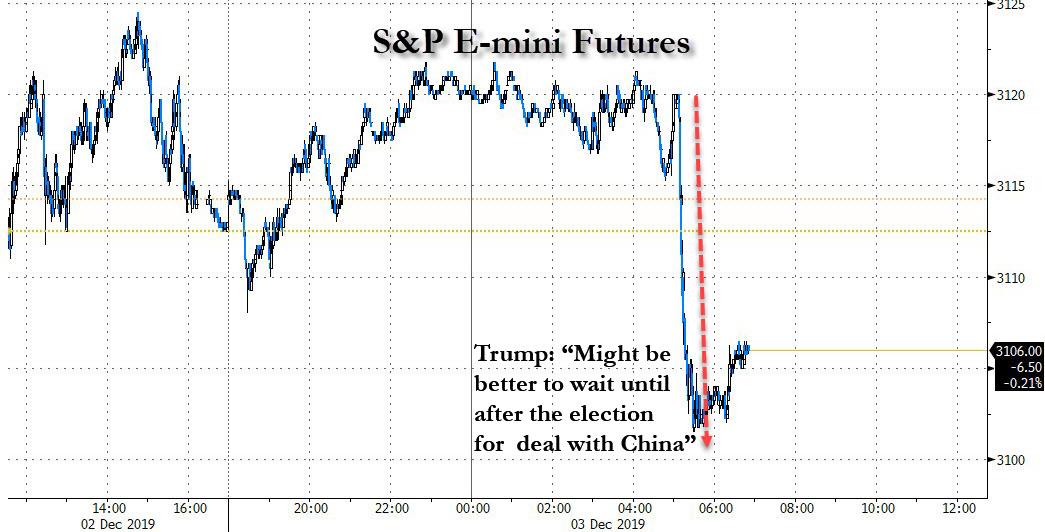

Futures Take Another Leg Lower After China’s Global Times Accuses US Of Backpedaling In Trade Talks

Late last Wednesday, with hours left until the Thanksgiving holiday, Trump signed the controversial Hong Kong bill, knowing well it would upset Beijing and risk an escalation in the trade war, however as we said, “it appears the president was confident enough that a collapse in trade talks won’t drag stocks too far lower” with the S&P just hitting an all time high above 3,150. Since then, the assessment that Trump was confident enough that a resumption in trade hostilities wouldn’t have too negative of an impact on the market has only been borne out, resulting in Trump launching new trade war fronts in both Latin America and Europe, and this morning, appearing to hammer the final nail in any trade deal with China in 2019, and perhaps ever, when he said it may be better to wait for a trade deal until after the 2020 election.

The news promptly sent US equity futures tumbling below the critical 3,100 level where there is a mountain of dealer gamma, and where negative convexity means selling will beget more selling.

Meanwhile, China also decided to remind Trump that it would have a say in the matter, and moments ago the Global Times directly accused the US of “backpedaling”, but noting that it was prepared for such as “worst case scenario”, to wit:

The US appears to be backpedaling in #tradetalks as officials threaten tariff hikes, but that will have zero effect on China’s stance because Chinese officials have long prepared for even the worst scenario: Mei Xinyu, an expert close the Chinese Commerce Ministry.

The US appears to be backpedaling in #tradetalks as officials threaten tariff hikes, but that will have zero effect on China’s stance because Chinese officials have long prepared for even the worst scenario: Mei Xinyu, an expert close the Chinese Commerce Ministry pic.twitter.com/P7Ai3NYXdO

And just in case the complete collapse in diplomatic relations was lost on someone, moments ago the director of the Chinese foreign ministry Hua Chunying compared Mike Pompeo to a mentally ill woman.

CN Spokeswoman Hua Chunying called Pompeo “Xianglin Auntie” (祥林嫂) today, quoting a character from Lu Xun novel to paint Pompeo, who criticized IP theft, as a mentally illed woman who keeps repeating stories. It’s tone deaf af even by China standards. Literature breakdown: 1/n pic.twitter.com/Hght7FM9yJ

— Toni (but what’s your *real* name?) (@tony_zy) December 3, 2019

In any case, the rapidly deteriorating back and forth sent futures to another sharp leg lower, now well below 3,100…

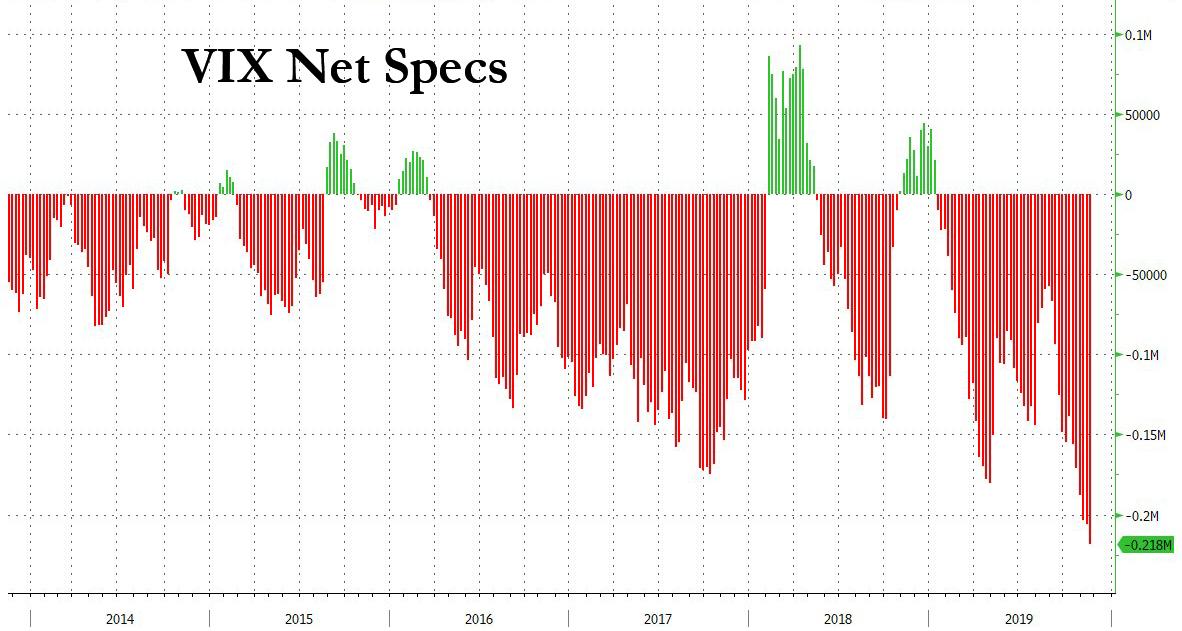

… and the risk is that the record VIX short position we have been warning about, is about to see a historic squeeze.

Trump Torpedoes Global Markets As Trade War Returns

Last week, when Trump signed the Hong Kong bill, we asked if Trump was willing to reignite the trade war now that the S&P hit an all time high of 3,150.

That question was especially apt this morning, when European shares slumped back into the red on Tuesday, reversing an earlier attempt to claw their way back from three days of falls, US equity futures tumbled for the second day in a row and the Chinese yuan sank on renewed trade tensions after President Trump said at the start of his British NATO summit visit that a that a trade deal with China might be delayed until after November 2020 elections, denting hopes of a quick resolution to a dispute that has weighed on the world economy.

“I have no deadline, no. In some ways, I think I think it’s better to wait until after the election with China,” Trump told reporters in London, where he was due to attend a meeting of NATO leaders. “In some ways, I like the idea of waiting until after the election for the China deal. But they want to make a deal now, and we’ll see whether or not the deal’s going to be right; it’s got to be right.”

Those comments, made as Trump landed in Britain for a NATO summit, also sent the offshore-traded Chinese yuan to near five-week lows.

France, the latest U.S. trade war target, saw shares tumble more than 0.6% to a one-month low, and dragged Europe’s Stoxx 600 index down 0.2%, giving up earlier modest gains and extending Monday’s 1.6% tumble which was its biggest one-day loss in two months.

U.S. stock futures also turned negative, with S&P 500 futures down 0.4%.

“The markets were spooked because they didn’t expect Trump to be that severe on China,” said WisdomTree researcher Aneeka Gupta. “It’s worrying for Europe too, because it was waiting for a decision on the auto tariffs from the U.S. Investors weren’t expecting Trump to be launching trade wars on all fronts.”

Trump’s willingness to open new fronts in the trade war – with Argentina, Brazil and France – despite signs of economic damage and less than two weeks away from the China tariff deadline, spooked markets. Indeed, his latest comments dashed hopes that an agreement with China could be reached before another round of tariff hikes kicks in on Dec. 15, and suggests talks could in fact could drag on for another year.

As Reuters notes, markets had fallen sharply on Monday after Trump tweeted he would slap tariffs on Brazil and Argentina for what he saw as both countries’ “massive devaluation of their currencies.” The United States then threatened duties of up to 100% on French goods from champagne to handbags because of a digital services tax that Washington says harms U.S. tech companies.

“Each step back and each step forward is just part of a slow trend toward increased barriers to international trade,” said Jonathan Bell, CIO of Stanhope Capital. “The market’s taken an optimistic view so far this year on the likelihood of a successful outcome to trade negotiations and we worry … the market may turn back to being more concerned.”

Shares in some French luxury goods firms had been hit hard, with LVMH shedding almost 2% to one-month lows and champagne maker Vranken Pommery down 0.5%. “If history is any guide the Europeans are likely to find U.S. crosshairs start to move increasingly their way, the closer to next year’s U.S. election we get,” CMC Markets told clients.

As a result, the MSCI world equity index was down for the fourth day in a row to one-week lows. There were also hefty losses across Asian bourses earlier in the day, led by consumer staples firms, tracking U.S. declines. Most markets in the region were down, with Australia leading losses and China advancing. Japan’s Topix slid, dragged down railway companies and automakers. The Shanghai Composite Index reversed morning losses to close higher, as Ping An Insurance Group and Will Semiconductor offered support. Two Chinese companies failed to repay bonds worth a combined half a billion dollars Monday, as debt risks rose in a slowing economy. India’s Sensex declined, with ICICI Bank and HDFC Bank among the biggest drags.

Meanwhile, investors were waiting for even more shoes to drop and China’s next response: Beijing has already barred U.S. military ships and aircraft from Hong Kong in response to U.S. support for pro-democracy protesters in the Chinese-ruled territory. Fears that the prolonged tariff spat will snuff out any upturn in global growth were fanned on Monday when the U.S. ISM report said manufacturing had contracted for a fourth straight month as new orders slid. That crippled the cheer from upbeat Chinese factory surveys as well as higher-than-expected manufacturing and inflation readings from the euro zone.

So with trade suddenly in limbo, hopes are now being pinned on the U.S. consumer to keep the economy afloat. Cyber Monday sales were expected to hit a record following $11.6 billion in online sales during the Thanksgiving and Black Friday shopping bonanza.

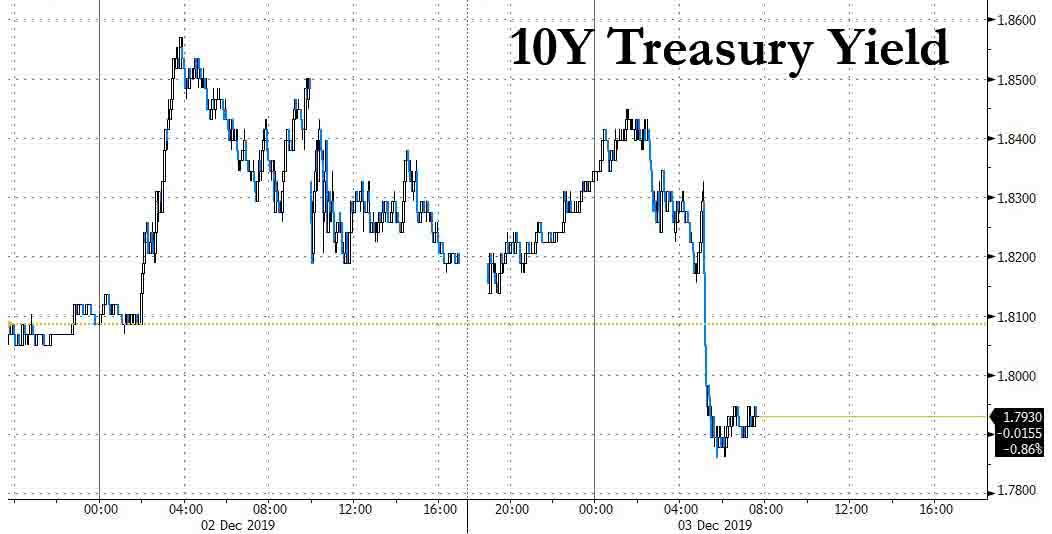

In rates, Trump’s hints of trade deal delays sent bond yields tumbling as investors dumped stocks, however, with 10-year U.S. Treasury yields falling 5 basis points to 1.79% from the previous day’s two-week high, despite a sharp selloff in Japanese bonds following a report that Tokyo is preparing a 25 trillion yen fiscal package, which in turn resulted in the worst bid to cover in the Japanese 10Y auction in three years.

German bond yields slipped off three-week highs but bond prices are likely to stay under pressure amid renewed risks of early elections or a minority government in the biggest euro zone economy.

The safe-haven bid was seen across FX too, with the yen at a one-week high to the dollar. The euro edged away from a near two-week peak versus the greenback, while the dollar reversed losses after Trump’s statement. “This may have run its course, but there’s no reason to chase the dollar’s upside from here,” Daiwa Securities’ foreign exchange strategist Yukio Ishizuki said, noting that the weak manufacturing data had forced many to cut long dollar positions. “Trade friction remains a lingering threat, which is not good for market sentiment.”

Elsewhere, oil fluctuated as traders gauge the probability of OPEC and allied producers tightening supplies when they meet later this week. Australia’s dollar rose after upbeat comments on the global economy by its central bank, while its government bonds dropped.

Looking at the day ahead in the US, the only data due out are the November vehicle sales numbers. Away from the data, we’re due to hear from the ECB’s Coeure and Hernandez de Cos. Elsewhere the NATO conference kicks off in London. Salesforce and Workday are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.3% to 3,103.50

STOXX Europe 600 up 0.4% to 402.40

MXAP down 0.4% to 164.17

MXAPJ down 0.4% to 522.79

Nikkei down 0.6% to 23,379.81

Topix down 0.5% to 1,706.73

Hang Seng Index down 0.2% to 26,391.30

Shanghai Composite up 0.3% to 2,884.70

Sensex down 0.3% to 40,676.21

Australia S&P/ASX 200 down 2.2% to 6,712.29

Kospi down 0.4% to 2,084.07

German 10Y yield fell 0.4 bps to -0.285%

Euro down 0.01% to $1.1078

Italian 10Y yield rose 11.7 bps to 1.002%

Spanish 10Y yield fell 0.9 bps to 0.481%

Brent futures little changed at $60.96/bbl

Gold spot up 0.6% to $1,470.47

U.S. Dollar Index little changed at 97.78

Top Overnight News from Bloomberg

ECB officials face increasing pushback against their negative interest-rate policy in private engagements with the region’s finance ministers, according to people with knowledge of the matter

Pacific Investment Management Co. has become the latest high-profile critic of negative interest rates, warning that one of the key central-bank tools in economically beleaguered Europe and Japan may do more harm than good

The ECB’s shift in net asset purchases to corporate bonds may become a more lasting and self- fulfilling feature of this QE leg, as it expands the shopping list while encouraging new issuance

France’s government said the EU would retaliate if the U.S. follows through on a threat to hit about $2.4 billion of French products with tariffs over a dispute concerning how large tech companies are taxed

At a summit in Brussels next week, EU leaders will commit to cutting net greenhouse-gas emissions to zero by 2050, according to a draft of their joint statement for the Dec. 12-13 meeting. To meet this target, the EU will promise more green investment and adjust all of its policy making accordingly

After five years of negative rates imposed by the ECB, German lenders are breaking the last taboo: Charging retail clients for their savings starting with very first euro in the their accounts

The Bank of Thailand said measures taken so far to curb capital inflows are “baby steps” and policy makers have plenty of tools available to deploy to curb the currency’s strength

Asian equity markets retreated amid headwinds from the US where the major indices all but wiped out last week’s gains due to fresh trade concerns with lacklustre ISM Manufacturing data also adding to downbeat tone. ASX 200 (-2.2%) and Nikkei 225 (-0.6%) were lower with underperformance in Australia due to hefty losses across its sectors including financials amid continued Westpac-related woes and with life insurers facing increased capital penalties, while sentiment in Tokyo was dragged by the adverse currency flows. Hang Seng (-0.2%) and Shanghai Comp. (+0.3%) also weakened on the trade uncertainty (although the latter pared losses heading into the close) with some analysts reading in between the lines of the metal tariff resumption on Brazil and Argentina, suggesting that it could be another front in the trade war following the nations’ recent agricultural deals with China. In addition, China’s retaliation to the Hong Kong bill by sanctioning US non-profit groups and barring US military visits to Hong Kong, as well as expectations for the US House to pass a Xinjiang-related bill further exacerbated the already-opaque trade environment. Finally, 10yr JGBs failed to take advantage of the widespread risk averse tone, as prices remained dejected following the recent bond rout and with selling also triggered after the 10yr JGB auction showed weaker results across all metric including the lowest b/c since August 2016.

Top Asian News

Japan’s GPIF Stops Lending Shares in Blow to Short Sellers

Dalio Out of Favor at Asia Wealth Manager as Flagship Fund Falls

Hong Kong Economist Says His Views on China Cost Him His Job

Nomura Sets Ambitious China Hiring Plans as Rebound Persists

Major European bourses (Euro Stoxx 50 Unch) are mixed, having reversed earlier gains US President Trump said that there was no deadline on a China deal, and that it may be better to wait until after the November 2020 Presidential Election to strike a deal. Elsewhere, some underperformance is being seen in the FTSE 100 on unfavourable currency effects, while the CAC 40 is being weighed by under performance in some of its heavy weight luxury names, Kering (-1.4%), LVMH (-1.4%) and Hermes (-1.9%), on US/EU trade concerns after the US responded to France’s digital sales tax.Meanwhile, sectors are mostly in the red, apart from Utilities (+0.4%), Tech (+0.5%) and Healthcare (+0.1%). In terms of individual movers of note; easyJet (-0.5%) shares were initially higher on the news that the Co. is set to return to the FTSE 100 and will replace Hiscox (-1.3%), although gains have since reversed. Elsewhere, Telenor (+1.2%) was buoyed by an upgrade at Citigroup. Laggards include Aston Martin (-5.5%), who sunk after being downgraded to neutral from buy at Goldman Sachs.

Top European News

German Banks Open Floodgates to Negative Rates for all Savers

ECB Sub-Zero Rate Policy Faces Pushback From Finance Ministers

Italy’s Agnellis Add La Repubblica Publisher to Media Assets

In FX, both outperforming in the G10 FX sphere, more-so the Aussie in the aftermath of the RBA’s latest monetary policy meeting in which the Cash Rate was left unchanged. Key themes in the statement were largely a copy-and-paste job from recent meetings which repeated the gentle turning point in the economy but reaffirmed data dependency and the readiness to inject further stimulus if needed. However, desks note of a slightly more positive tone in the statement which linked rising house prices to a potential lift in spending and residential construction. AUD/USD extends its gains above the 0.6800 level and surpassed its 100 and 21 DMA (at 0.6818 and 0.6820 respectively) to a current high of 0.6860 (vs. low of 0.6815) with clean air until the psychological 0.6900 mark. The Kiwi piggybacks on its antipodean partner’s gains and covers more ground above the recently claimed 0.6500 level vs. the USD to a high of 0.6530 ahead of its 200 DMA at 0.6544.

GBP, EUR – Sterling rose in the G10 ranks in early European hours after the retrieval of 1.2950+ status vs the Dollar spurred upside momentum (amid potential stops/orders), and with tailwinds from the latest election Kantar poll (showing a widening gap between Tories and Labour) underpinning the currency in recent trade. Cable rose to a current high of 1.2994 after eclipsing its Nov 18th high (1.2985) with eyes remaining on election developments as election day looms. Meanwhile, the Single Currency held onto most of its gains vs. the Buck despite France’s growing trade tension with the US which prompted the latter to propose duties of up to 100% on certain French imports. EUR/USD meanders around the middle of a tight 1.1072-1.1086 intraday band, ahead of potential resistance at 1.1097 (Nov 21st high), with little impetus derived from ECB Board nominees and sources reports of pushback on the ECB’s NIRP by EZ finance ministers.

DXY, JPY, CNH – The broad Dollar and Index resumes their downward trajectories following yesterday’s dismal manufacturing prints and with little by way of fresh fundamental catalysts. DXY hovers around the bottom of today’s current 97.74-94 range with little on the today’s docket in terms of tier 1 data. Meanwhile, USD/JPY convincingly fell below the 109.00 mark (to a low of 108.84 vs. high 109.20) after US President Trump signalled no rush for a US-Sino trade deal. USD/JPY also sees hefty options of around USD 1bln expiring between strikes 109.00-10 and a further USD 1bln at 109.50. Subsequently, USD/CNH was bolstered to fresh session highs of 7.0690 (vs. low of 7.0360) in light of Trump’s comments on trade.

EM – The EM space trades mostly on the backfoot with the Rand underperforming as South Africa’s economy contracted on a QQ basis, missing expectations for modest growth. USD/ZAR took out its 200 DMA to the upside (14.5772) to a high of 14.6900 with little seen by way of resistance ahead of 14.7000. Meanwhile, the Lira recovered from initial loses which emanated from US senators urging Secretary of State Pompeo to sanction Turkey over its purchase and testing of the Russian-made S-400 system. The TRY has since pared back a bulk of its losses as President Trump continues to support Turkey.

In commodities, crude markets are flat/higher and off best levels, as risk assets take a hit following the latest US President Trump’s trade comments. However, price action remains well within yesterday’s ranges; technicians will be eyeing resistance at the USD 56.65/bbl and USD 62.10/bbl levels and support at the USD 55.65/bbl and USD 60.78/bbl levels for WTI Jan’ 20 and Brent Feb’ 19 futures (yesterday evening’s trading range). Crude specific news flow has been light; Russian Energy Minister Novak said that Russia is yet to finalise their position for OPEC+ meeting in Vienna, which takes place at the end of the week. Amid rumours that OPEC+ are considering up to an additional 400k bpd in production cuts, the Russians are known to have been resistant to further cuts, instead preferring an extension of existing cuts until mid-2020. In terms of the metals, gold gained as risk soured, with the yellow metal briefly advancing above USD 1,470/oz from overnight lows of USD 1,460/oz. Meanwhile, trade concerns are hitting copper; the red metal has slumped from overnight highs of USD 2.6550/lbs to near USD 2.6300/lbs lows. , Iron Ore prices gained overnight after its largest miner, Vale, lowered its production outlook. On Monday, the miner said that it would cut output from it Brucutu mine in Brazil for up to two months while the stability of the nearby Laranjeiras dam in assessed.

US Event Calendar

Wards Total Vehicle Sales, est. 16.9m, prior 16.6m

DB’s Jim Reid concludes the overnight wrap

In the last 24 hours we’ve gone from a potential Santa Claus rally to a more Scrooge-like environment as the ghost of trade wars past came back to haunt the market. Indeed sentiment took a hit following President Trump’s tweet that tariffs would be reinstated on steel and aluminium from Argentina and Brazil and then on Commerce Secretary Ross telling Fox that President Trump will increase tariffs on China if nothing happens between now and December 15th. That undid some of the good work from the majority of global PMIs released earlier in the day. However, a weaker US ISM manufacturing print did bring in an element of doubt and confusion to the picture.

More on the data shortly but first off President Trump’s tweet that “Brazil and Argentina have been presiding over a massive devaluation of their currencies which is not good for our farmers” and that “effective immediately, I will restore the tariffs on all steel and aluminium that is shipped into the US from those countries”. The President followed with the Fed “should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar by further devaluing their currencies”.

The implications of President Trump’s tweet is important less for the direct economic impact and more because it shows the current state of President Trump’s thinking on tariffs, and thus the read-through to China. The latter came into play after Ross’ comments with the markets taking another leg down after the headlines hit. These were partially alleviated by subsequent comments from White House advisor Kellyanne Conway, who said that a deal is possible before year-end. So a fair bit resting on the next couple of weeks ahead of the December 15 tariff increase deadline. However, some reports have suggested they could still be suspended even without a deal, as long as productive talks are continuing. Nevertheless, this date is creeping up on us and something has to happen before it one way or another. Later in the day, and separately, the USTR said that it will consider higher tariffs on the EU to compensate for subsidies given to Airbus, citing a WTO ruling, though the dollar amounts under consideration are small.

After all this, the NASDAQ and trade-sensitive semi-conductor indices closed down -1.12% and -1.46%, respectively. The S&P 500 and DOW fared slightly better but still closed down -0.85% and -0.96%, while the VIX climbed to 14.64 and to the highest level since mid-October. European equities fared even worse, with the STOXX 600 ending -1.58%, its worst session since 2nd October. The DAX and CAC were down -2.05% and -2.01%, and the V2X mirrored the VIX by rising +2.72pts to 15.89.

Overnight the Global Times said that the Chinese government will soon publish a list of “unreliable entities” that could lead to sanctions against US companies. China had originally threatened to publish the list in May in response to the restrictions the US placed on Huawei. The timing seems to be linked to an accelerated US House of Representatives vote – expected today – on the Xinjiang bill, which was passed by the Senate in September. This could put sanctions on officials linked to alleged abuses of Uighur Muslims. It remains to be seen whether this will impede the path towards the Phase 1 deal, which according to President Trump yesterday has already been complicated by the signing of Hong Kong bill into law.

Elsewhere, after the US markets closed last night, Bloomberg reported that the US is proposing tariffs on roughly $2.4 bn in French products, in response to a tax on digital revenues that hits large American tech companies including Google, Apple, Facebook and Amazon. The office of the United States Trade Representative said in a statement that “France’s digital services tax discriminates against U.S. companies.” USTR Robert Lighthizer added that the agency is also exploring whether to open investigations into similar digital taxes by Austria, Italy and Turkey before saying that, “the USTR is focused on countering the growing protectionism of EU member states, which unfairly targets US companies.” The tariffs would be imposed after a public comment period concludes in early 2020. As we write this on a cold December morning it doesn’t feel like the global trade problems are going to thaw anytime soon.

A quick refresh of our screens this morning shows that most Asian markets are trading lower with the Nikkei (-0.72%), Hang Seng (-0.18%), Shanghai Comp (-0.04%) and Kospi (-0.43%) all down. However, most indices are off their intraday lows. As for FX, the Australian dollar is up +0.41% this morning after the RBA held its key interest rate unchanged and highlighted that past easing is having an impact. Yield on 10y USTs are up +2.1bps while those on 10y JGBs are up +3.3bps to -0.028% as demand for the benchmark debt fell at an auction. Elsewhere, futures on the S&P are up +0.18%.

In other news, Hong Kong’s Chief Executive Carrie Lam said overnight that the government would soon announce new moves to prop up the city’s flagging economy without giving any details of what those measure would be. She just mentioned that the measures would be “targeted.” Yesterday, Financial Secretary Paul Chan said that he expected the first fiscal year budget deficit since the early 2000s, and said that the turmoil has dragged down economic growth by some 2pp this year. Elsewhere, North Korea reiterated overnight that the US has until the end of the year to make a better offer in nuclear negotiations, saying the “Christmas gift” the US receives will depend on what it brings to the table.

The bond sell-off overnight follows a similar move yesterday where 10y Treasury yields rose +4.5bps. Front-end rates rallied though, possibly pricing in slightly higher odds that the Fed will end up having to cut again next year. Two-year yields fell -1.0bps, taking the yield curve +5.7bps steeper to 21.7bps. Bunds sold off +8.0bps to -0.284% after the shock weekend SPD news (updates below). Other European bond markets followed the German move, with OATs and Gilts +7.8bps and +4.1bps, respectively. BTPs underperformed, with 10-year yields up +11.9bps, as investors de-risked.

Alongside the SPD news, the earlier decent PMIs seemed to kick start the bond sell-off. In terms of the PMIs, after China’s beat, the PMIs in Europe saw the Euro Area manufacturing print revised up 0.3pts to 46.9. That is the second consecutive monthly increase – something that hasn’t happened since 2017, which is a stunning stat – and also to the highest reading since August. Half of the increase came from Germany and France – the former revised up to 44.1 and the latter to 51.7. Also encouraging was the fact that all of the key components – including new orders, new export orders and employment – saw slight upward revisions. The outright level of the PMI is still clearly a concern but it still lends an argument to seeing a stabilisation in the data.

In the afternoon the US manufacturing PMI was revised up 0.4pts to 52.6, which matches the April levels once again. However, to complicate the picture, 15 minutes later the November ISM manufacturing missed at 48.1 (vs. 49.2 expected). You could argue that the data has stabilised somewhat – the reading was only down 0.2pts from 48.1 and remains above the 47.8 low print from September. That being said, the gap to the PMI (and regional fed surveys) is muddying the waters. In addition, the details didn’t add much encouragement with new orders down to 47.2, employment down to 46.6 and new export orders down to 47.9.

Coming back to yesterday where the fallout from the SPD leadership election in Germany played out with German Finance Minister Scholz, despite losing the leadership bid, announcing that he will still attend a meeting of Eurozone finance ministers tomorrow. Our German economists published their thoughts post the election in a note yesterday, which you can find here . In their view, the vote for Walter-Borjans and Esken increased the probability of the Groko falling apart but does not translate into an automatic or immediate collapse of the government coalition. Their baseline view remains that the new party leaders and delegates at the SPD’s December 6-8 party conference will support a (possibly conditional) continuation of the Groko until the 2021 elections and that the SPD will not pull out of Groko immediately. Still, as the CDU/CSU are reluctant to renegotiate the Groko treaty, non-negligible risks of a premature end to the government coalition remain. It must be said that the internal debate within DB continues to be around how much more likely it is that fiscal spending eventually increases as a result of this political shockwave. There is little doubt that the chances have increased but the timing and scale of any policy changes are still up for much debate.

Elsewhere, new ECB President Lagarde testified to the European Parliament for the first time in her new position, but did not reveal any major policy details. She promised that policy will “continue to support the economy and respond to future risks in line with our price stability mandate.” She refused to prejudge the planned policy review, saying that the “direction and timeline” of the process is still to be determined. This tempers any expectations for near-term policy moves by the ECB, including at this month’s meeting. Notably, Lagarde did talk more about “the side effects of our policies,” which has thus far been the biggest departure from Draghi’s rhetoric and likely signals reduced appetite to cut the deposit facility rate deeper into negative territory.

To the day ahead now, which this morning includes Q2 labour costs and the November construction PMI in the UK and October PPI for the Euro Area. In the US the only data due out are the November vehicle sales numbers. Away from the data, we’re due to hear from the ECB’s Coeure and Hernandez de Cos. Elsewhere the NATO conference kicks off in London.

Yesterday, the Supreme Court heard oral argument in NYS Rifle and Pistol Association v. City of New York. Certiorari was granted in February 2019. After the grant, New York City repealed the challenged provisions of the premise license law. Subsequently, New York State enacted a law that made it impossible for New York City to reenact the challenged provisions. I discuss the background of this case in a Federalist Society SCOTUSBrief video.

Prior to oral argument, I predicted that the Supreme Court would dismiss the case as moot. My prediction has not changed after reading the transcript.

No “Collateral Consequences”

Chief Justice Roberts will likely cast the deciding vote. He did not ask any questions of Paul Clement, who represented the plaintiffs, or of Deputy Solicitor General Jeff Wall. He asked a few questions of Richard Dearing, who represented New York City.

First, Roberts asked if “there [is] any way in which any violation” of the repealed ordinance in the past “could prejudice a gun owner” in the future? Dearing replied, “Not that I can think of. The city is committed to to closing the book on that old rule and we’re not going to take it into effect.” Second, Roberts followed up, and asked, “Is there any way in which a finding of mootness would prejudice further options available to the Petitioners in this case, for example, seeking damages?” Dearing didn’t think so. He stated that the Plaintiffs “never made any allegations related to damages” prior to the grant of certiorari. Dearing also stated that the Plaintiffs had never asserted that “past violations” could prejudice them in the future.

At that point, Justice Gorsuch interjected. He asked if there would be any “collateral consequences to anyone for violating the city’s prior ban, any kind of collateral consequences.” Dearing replied that there wouldn’t be.

Chief Justice Roberts asked one final question. Would anyone be “prejudiced in any way, for example, with respect to qualifying for a premises license under the new law” based on violating the old law.” That is, would violating the old law justify the denial of a new license? Dearing replied that no would be prejudiced. Roberts asked no further questions.

This representation reminded me of a similar colloquy from NFIB v. Sebelius. Solicitor General Verrilli represented that there were no “collateral consequences” for going uninsured. From pp. 179-180 of Unprecedented:

But if there was no mandate, what would happen if a person failed to purchase insurance? Justice Sotomayor asked the solicitor general whether there was any “collateral consequence for the failure to buy” health insurance—that is, would there be any criminal penalties for not buying insurance? The solicitor general responded, emphatically, “No.” The only consequence would be that the person would have to pay a tax. . . .

Verrilli then offered an important “representation” to the Court on how the Obama administration viewed the law. This representation proved pivotal. The “only consequence” of not having health insurance was the “tax penalty.” Verrilli noted that the government “made a representation, and it was a carefully made representation, in our brief that it is the interpretation of the agencies charged with interpreting this statute, the Treasury Department and the Department of Health and Human Services, that there is no other consequence apart from the tax penalty.” In other words, there was no mandate or legal requirement to buy insurance, despite the statute stating that there was such a requirement.

Roberts’s saving construction in NFIB relied on this representation:

While the individual mandate clearly aims to induce the purchase of health insurance, it need not be read to declare that failing to do so is unlawful. Neither the Act nor any other law attaches negative legal consequences to not buying health insurance, beyond requiring a payment to the IRS. The Government agrees with that reading, confirming that if someone chooses to pay rather than obtain health insurance, they have fully complied with the law. Brief for United States 60–61; Tr. of Oral Arg. 49–50 (Mar. 26,2012).

I think New York persuaded the Chief that there are no possible “collateral consequences” for past violations, and this controversy is no longer live. Justices Ginsburg, Breyer, Sotomayor, and Kagan seemed to agree with New York. There are at least five votes for this position. What about the newest member of the Court? Justice Kavanaugh was silent. He did not say a word.

DIG or Decide?

If a majority of the Court agrees that the case is moot, there are two options going forward. First, the Court could simply dismiss the petition as improvidently granted at the December 6, 2019 conference. (This move is known as a DIG.) We would learn of the dismissal with the next release of orders, probably on December 9, 2019. These sorts of dismissals are unsigned. Justices can register their dissents from the DIG.

The upshot of this approach is that the Court could add another Second Amendment case to its docket, with an argument scheduled for March or April. Indeed, there are many gun cases that are fully briefed, that have been hanging in SCOTUS purgatory for months. There was obviously some appetite to weigh in on the Second Amendment, after nearly a decade of silence following McDonald v. Chicago. A quick DIG would allow the Justices to address another live case now.

Second, the Court could issue a signed opinion to explain why the controversy is moot. That decision would take some time to prepare, and would likely occasion a written dissent. The Court’s mootness doctrine is quite muddled. Perhaps the Court could clean up the doctrine. However, this case is a terrible vehicle. The facts of this case are so unique. I’m not sure these specific conditions–the City repealed the ordinance, and the State prevented its re-enactment–would ever recur.

Mooting the Case

I can see one or more possible dissents. Justice Gorsuch seemed to accept Dearing’s representation about the lack of collateral consequences. But on three occasions, he asked if there was some “delta” (that is, difference) between the relief the plaintiffs currently have, and the relief that could be awarded with a permanent injunction. Gorsuch may go along with the Chief here. Though, he was far more cynical about New York’s post-certiorari strategy. He chastised the City’s “herculean, late-breaking efforts to moot the case.” Clement twice used the phrase “post-certiorari maneuvers.” Wall used the term “post-grant maneuvering.”

Justice Alito was, by far, the most critical of New York’s strategy. He suggested that it is unfair to hold the Plaintiffs to a precise pleading standard, and demand “specific allegations in the complaint to defeat a claim of mootness that the plaintiffs had no reason whatsoever to anticipate until after we granted certiorari and the city decided to try to moot this case.” He added “how could any plaintiff possibly have anticipated” they would need to seek damages “until you took the quite extraordinary step of trying to moot the case after we granted review?

Dearing replied, that the New York “state legislature has passed a new State law here,” not New York City. Alito interjected, “Yeah. And did the city have nothing to do with the enactment of that law?” Dearing said that the City “supported the law,” but there was nothing nefarious about this support. The new law was “a good thing, not a bad one. The government should respond to litigation, should assess its laws or other -or political subdivisions’ laws when they are challenged.” Dearing made a similar point earlier: “it’s a good thing and not a cause for concern when the government responds to litigation by resolving matters through the democratic process.” Justice Breyer likewise found New York’s strategy was praiseworthy: “I don’t think it’s bad when people who have an argument settle their argument.”

Text and History

There were a few colloquies about the merits. Paul Clement made a broader point of how the lower courts have approached the Second Amendment. He explained that the lower-courts have only used history to uphold laws; not to declare them unconstitutional:

The way the lower courts have interpreted Heller is like text, history, and tradition is a one-way ratchet.

If text, history, and tradition sort of allow this practice, then they’ll uphold the law. But if text, history, and tradition are to the contrary, then the courts proceed to a watered-down form of scrutiny that’s heightened in name only.

And I think this Court should reaffirm that text, history, and tradition essentially is the test and can be administered in a way that provides real protection for Second Amendment rights.

Jeff Wall presented a similar argument:

If I could turn to the merits for just a minute, I think all that the Petitioners are asking for, and it’s a fairly modest ask, is for the Court to reiterate what it said in Heller, that the lower courts have been correct in starting with text and history and tradition, but they have created, as Mr. Clement said, this sort of asymmetry where they find that history and tradition can give a thumbs up to a law but not a thumbs down.

Justice Sotomayor was extremely skeptical about the Plaintiff’s historical-based approach. She stated that the Court does not use such a framework in the First Amendment context:

In what other area, constitutional area, the First Amendment in particular, have we decided any case based solely on text, history, and tradition?

This seems sort of a made-up new standard. And I thought Heller was very careful to say we don’t do that. We treat it like any other constitutional provision. And if I analogize this to the First Amendment, which is what Heller suggested we should do, this seems to me to be a time, place, and manner restriction. It may not pass any of the standards of scrutiny, but, if you’re looking at a First Amendment right to speak, it’s never absolute. There are some words that are not protected. We’re going to have a different fight about that at some point. Or there are some weapons that are not protected, just like there might be some words that are not protected.

The emphasized sentences look like an aside about future battles to come. We can speculate about what “words” she is talking about. Justice Sotomayor’s Iancu v. Brunetti dissent suggested that “one particularly egregious racial epithet” should not be protected by the First Amendment.

She continued:

We know under the First Amendment that there are time, place, and manner restrictions that a government can impose on the basis of safety and other things. On the basis of safety, you can’t have a demonstration at will. You need a permit, and you have to have certain equipment and certain protections and certain things.

So, if I treat it in that way, we might have a fight about whether text, history, and tradition permits a time, manner, and place restriction of this type, but I don’t know why that’s a free-standing test.

Jeff Wall replied:

I understand the requirement that you carry the gun unloaded or that you do it in a locked container. But a ban is not a time, place, or manner restriction. And in determining which category it falls into and what’s permissible, Heller said you start with text, history, and tradition.

And the Court commonly does that, even under the First Amendment with respect to categories, the Fourth Amendment for a search, the Seventh Amendment for the jury trial right. Heller just says you start here. And starting here, I think this is a straightforward case. There is no historical analogue and a contrary tradition.

Scrutiny

Justice Alito asked Dearing how the Court should review gun control laws.

JUSTICE ALITO: Well, how should -what methodology should the courts use in approaching Second Amendment questions?

If they conclude that text and history protect a –the text and history of the Second Amendment protect a particular activity, is that the end of the question or do they then go on and apply some level of scrutiny?

Dearing replied that history plays some role in the inquiry:

MR. DEARING: I think –I think, first, we look –we look to history and determine whether history answers the question one way or the other, whether it’s constitutional or unconstitutional. . . .And in a significant number of cases, history will not speak with one voice or conclusively on that subject and then the right step is to move on to an assessment of justification and fit under a means and scrutiny approach.

Justice Alito also seemed to suggest that the now-repealed law was completely irrational, because it never actually promoted public safety:

JUSTICE ALITO: Mr. Dearing, are the –are people in New York less safe now as a result of the enactment of the new city and state laws than they were before?

MR. DEARING: We –we –no, I don’t think so. We made a judgment expressed by our police commissioner that –that it was consistent with public safety to repeal the prior rule and to move forward without it.

JUSTICE ALITO: Well, if they’re not less safe, then what possible justification could there have been for the old rule, which you have abandoned? …

JUSTICE ALITO: So you think the Second Amendment permits the imposition of a restriction that has no public safety benefit?

I don’t expect the Court to address the merits. Justice Breyer, if he is so inclined, may perpetually dissent from Heller. At one point, Dearing described Heller. Breyer said that he still did not agree:

MR. DEARING: If history conclusively shows that the restriction is impermissible, then I –I think –as in Heller, Heller is an example of that phenomenon. Heller determined without consulting means and scrutiny, that the –that the law in question sort of went to the core of and destroyed, in essence, the -the –the –the Second Amendment right and, therefore, was –and more severe than any -any historical, any analogous or prior law and its degree of burden on the Second Amendment –

JUSTICE BREYER: No –

MR. DEARING: –right.

JUSTICE BREYER: –you’re supposed to do there, because you’re correctly stating the views of some judges.

MR. DEARING: Right.

JUSTICE BREYER: And some judges had an opposite view.

MR. DEARING: I’m aware –I’m aware of that, that’s correct.

(Laughter.)

Staten Island

My hometown of Staten Island was also referenced several times:

JUSTICE ALITO: Why will they have to work harder? Somebody who lives in midtown is stopped and –with a gun and the officer says, where are you going? I’m going to a firing range in Jersey City, which is right across the river.

That’s tougher than, I’m going to a firing range in Staten Island. And I think three of your seven ranges are in Staten Island; am I right?

MR. DEARING: Two –two are in Staten Island. JUSTICE ALITO: Two are in Staten Island?

MR. DEARING: I think it is a little bit tougher but of course the –the person may not say Jersey City either.

JUSTICE ALITO: All right. How about somebody who lives in the north Bronx says, I’m going across the border to Westchester County. That’s tougher for you to –to look into than,

yes, I’m going all the way to Staten Island?

MR. DEARING: Well, still the –still what happens in Staten Island is within the Police Department’s jurisdiction.

Growing up, I was not even aware Staten Island had any shooting ranges.

from Latest – Reason.com https://ift.tt/34NeTvY

via IFTTT

Are Americans eager to be forced to surrender labor and years of their lives to work on government projects? Not so much, a recent survey reveals. When asked about a reinstated draft, roughly a third of of those in the age range most likely to be affected say they would resist—and their opposition extends beyond military conscription to all sorts of mandatory service.

Young Americans are particularly unthrilled at the prospect of a reinstated draft. Thirty-one percent of “male Millennials say that they would ‘try to avoid being conscripted into the armed forces,'” the polling firm YouGov reported last week. Just as interesting, only 23 percent of male millennials said they would not try to avoid conscription (other respondents answered “don’t know” or “not applicable”).

Thirty-two percent of female millennials also said they would try to avoid conscription, while only 15 percent said they would not.

An even higher percentage of male respondents in the post-millennial Gen Z said they would try to avoid conscription, but their representation in the survey was too small to be considered representative.

Opposition to conscription unsurprisingly dropped among older generations, who are almost certainly beyond draft age.

“Wait a minute!” national service advocates complain. “We never said it had to be the military! It could be all sorts of peaceful government busywork.”

South Bend, Indiana, Mayor Pete Buttigieg—whose presidential campaign recently reached double-digit support nationally for the first time, after first showing signs of life in Iowa polls—specifically calls for the creation of new agencies, including a Community Health Corps, Intergenerational Corps, and Climate Corps, to facilitate non-military forms of national service. On his website, the Navy veteran emphasizes “a universal, national expectation of service for all 4 million high school graduates every year, such that the first question asked of every college freshman or new hire is: ‘where did you serve?'”

Back in April, Buttegieg told MSNBC’s Rachel Maddow that he wanted “to make it, if not legally obligatory but certainly a social norm, that anybody after they’re 18 spends a year in national service.”

Coy phrases like “if not legally obligatory” make it unclear as to whether that “universal, national expectation of service” will be enforced by government or by magic. (Fellow Democratic hopeful John Delaney, who is allegedly still in the race, makes no bones about the “mandatory” nature of the national service he favors.) In a large, diverse, and factionalized country, it’s difficult to imagine how you arrive at “universal” anything without (perhaps conscripted) enforcers.

Unfortunately for Buttigieg and other advocates of national service, the people who would be drafted into those non-military “service opportunities” don’t seem to like them better.

“Almost half (49%) of Americans favor requiring young men and women to give a year of service to the nation,” Gallup reported in 2017. “But a majority (57%) of the group most likely to be affected—those under the age of 30—oppose the idea.”

An earlier survey found similar results.

“While solid support exists for voluntary service, 71 percent say they would oppose a system of national service if it were mandatory,” Hart Research reported in 2013. “More than half (52 percent) are strongly opposed to the idea. Younger voters, age 18 to 39, most strongly oppose a mandatory system (59 percent), compared with 42 percent of voters over 65.”

Basically, if you want enthusiastic support for compelled labor, ask those who won’t have to do it. The folks who will be subject to involuntary servitude are largely resentful of the idea of compulsory national service. Any why wouldn’t people oppose compelled service, no matter how well-intentioned, and even if it somehow rises above the level of inefficient busywork that inevitably accompanies every large-scale government project? After all, the core component of these schemes of mandatory national service is to take away the participants’ freedom to choose.

“What is freedom? It is the right to choose one’s own employment. Certainly it means that, if it means anything,” Frederick Douglass, the 19th century escaped slave, writer, and reformer responded to the U.S. Army’s Civil War-era policy in Louisiana of extracting one year of forced (albeit compensated) agricultural labor from freedmen on behalf of the federal government. “And when any individual or combination of individuals, undertakes to decide for any man when he shall work, where he shall work, at what he shall work, and for what he shall work, he or they practically reduce him to slavery.”

It wasn’t just life-long chattel slavery that Douglass opposed, it was compulsion that deprived people of their right to choose where and how to work.

Plenty of the people that Pete Buttigieg and other oh-so-concerned politicians and pundits would conscript into government service obviously agree with Douglass. In large numbers, they say they would resist a military draft. But they also oppose any sort of compelled labor on behalf of the government (or anybody else, we can assume).

Maybe Pete Buttigieg really is the less-awful presidential candidate when compared to a host of unimpressive rivals. But if he wants to convince voters that he’s the guy they should put in the White House, he should drop his unpopular scheme to conscript the country into his pet projects.

from Latest – Reason.com https://ift.tt/2LfuNHK

via IFTTT