After debate rules were changed in favor of allowing billionaire Mike Bloomberg to join the candidates onstage vying for the 2020 Democratic presidential nomination on Friday, Sen. Bernie Sanders’ campaign hit back, calling the decision emblematic of the corrupt political system the Vermont senator has centered his run for the White House on defeating.

“To now change the rules in the middle of the game to accommodate Mike Bloomberg, who is trying to buy his way into the Democratic nomination, is wrong,” Sanders senior adviser Jeff Weaver toldPolitico.

“That’s the definition of a rigged system,” Weaver said.

Democratic presidential candidate, former New York City Mayor Michael Bloomberg. Photo: Mark Wilson/Getty Images

The Democratic National Committee (DNC) announced Friday afternoon that the criteria for making the debate stage will no longer include a requirement about individual donors— allowing Bloomberg, whose campaign is largely self-funded, to join the candidates if his polling numbers reach the new threshold.

“DNC changing the rules to benefit a billionaire,”tweeted Sanders campaign manager Faiz Shakir. “I much prefer Democrats being a grassroots party. And under Bernie Sanders, that’s the way it will be.”

New statement from Bernie Sanders senior adviser Jeff Weaver on DNC debate rules: “To now change the rules in the middle of the game to accommodate Mike Bloomberg, who is trying to buy his way into the Democratic nomination, is wrong. That’s the definition of a rigged system.”

Candidates will need to earn at least 10% in four polls released from Jan. 15 to Feb. 18, or 12% in two polls conducted in Nevada or South Carolina, in order to participate in the Feb. 19 debate in Las Vegas. Any candidate who earns at least one delegate to the national convention in either the Iowa caucuses or New Hampshire primary will also qualify for the Nevada debate.

The rules change caught Democrats by surprise.

Some observers noted the timing of the change and wondered if it was part of a coordinated attack on Sanders from both the DNC and Bloomberg.

The Intercept‘s Ryan Grim, citing Federal Elections Commission data, noted Bloomberg donated $325,000 to the DNC in November 2019.

“Totally normal system,” said Grim.

Just before jumping into the race, @MikeBloomberg gave $325,000 to the DNC, on top of the gobs he spent on ads this month. Totally normal system. pic.twitter.com/u4JDelWb7H

The debate rules have been a source of contention throughout the primary process, with some former hopefuls like Sen. Cory Booker (D-N.J.) and former Housing and Urban Development Secretary Julián Castro questioning the restrictions on polling and donors as prohibitive to their campaigns.

If you look at the new DNC debate thresholds as anything other than “Get Andrew Yang off stage and put Mike Bloomberg on,” Then you are high.

Progressive strategist Tim Tagaris wondered what could have been different if not for the qualifications.

“How much money did candidates like Julián Castro and Cory Booker have to spend chasing donor thresholds that could have been spent building organizations in early states?” said Tagaris.

And in a now-deleted tweet, Tagaris added:

“Weaver pointed to other current & past candidates like Booker, Yang & Castro, who dropped off the stage because they couldnt meet the minimum polling threshold.

Now, suddenly because Bloomberg couldnt satisfy one of the prongs, we see it get changed?'”

Comedian and writer Jack Allison took a wry look at the changes and what they mean about the party. “Remember when they wouldn’t even think of changing them for like Cory Booker,” Allison tweeted. “This is what we mean when we talk about the DNC cheating, obviously and out in the open.”

“Thankfully seeing Bloomberg speak can only hurt his standing,” Allison added, “but still.”

But it was outspoken filmmaker Michael Moore that really went off on the DNC’s decision. Speaking Friday night at a Sanders rally in Clive, Iowa, Moore went on an expletive-filled rant against the party.

“I watched the debate in Iowa here two weeks ago – the all white debate – and the fact that the Democratic, the DNC will not allow Cory Booker on that stage, will not allow Julian Castro on that stage, but they are going to allow Mike Bloomberg on the stage?” Moore roared.

“Because he has a billion f*cking dollars!”

The crowd went wild, and Moore continued using profanity throughout his remarks.

“I am sorry, those days are over,” Moore said of the DNC moving to help Bloomberg. “Those days are over.”

A report by Chicago’s Office of Inspector General found that city police officers regularly use department-issued placards to park personal vehicles in department lots when they attend Cubs and Bears games. The lots are supposed to be used only by on-duty officers.

An Oklahoma County, Oklahoma, judge sentenced Cody Gregg to 15 years in prison after Gregg pleaded guilty to possession of cocaine with intent to distribute. Days later, a drug test found that the “cocaine” was actually powdered milk. Gregg withdrew his plea, and the judge dismissed the charge. Gregg had initially pleaded not guilty, but he changed his mind after spending two months in the Oklahoma County jail.

Australia’s Department of Home Affairs says it wants to use facial recognition technology to limit children’s access to online pornography. Those who want to watch porn would have their faces scanned and matched to the photos on their official IDs to prove they are adults. Critics say this would allow the government to know every porn site that any person goes to.

San Antonio, Texas, officials have agreed to pay $205,000 to settle a lawsuit brought by Natalie Simms after a police officer conducted a cavity search of her on a public street. Simms says she was sitting on a curb when officers approached, told her they thought she might have drugs, and asked to search her car. She agreed. While Simms was being detained, she says a female officer arrived and began to frisk her. That officer pulled down Simms’ pants and underwear and searched her vagina, pulling out Simms’ tampon and holding it up for other officers to see. The cops found no drugs.

Drexel University in Philadelphia has agreed to pay the federal government $189,062 after a former professor at the school used federal grant money to make iTunes purchases and to visit strip clubs and sports bars. That professor, Chikaodinaka D. Nwankpa, the head of Drexel’s Department of Electrical and Computer Engineering, agreed to repay $53,328 to the university and to resign.

Officials at St. Andrew’s Primary School in Hull, England, have barred parents from packing any drinks other than water with their children’s meals. They say the move is aimed at protecting students with allergies and reducing consumption of sugary drinks.

Eliana Bauta, a former employee of New York City’s Human Resources Administration, has been sentenced to two years in prison for her role in the theft of more than $300,000 in emergency benefits money from her department. Bauta used part of the money she stole to pay someone to put a voodoo spell on a former boyfriend.

Jason Kirkbride’s hair is neat, tidy, and short—too short for Hodgson Academy in England, according to his mother. She says she decided to get the 14-year-old’s hair cut a little shorter than usual so he could go longer between visits to the barber. But school rules say hair should be no shorter than a No. 2 clipper, so the boy received three days’ detention.

from Latest – Reason.com https://ift.tt/2RLxtjP

via IFTTT

A report by Chicago’s Office of Inspector General found that city police officers regularly use department-issued placards to park personal vehicles in department lots when they attend Cubs and Bears games. The lots are supposed to be used only by on-duty officers.

An Oklahoma County, Oklahoma, judge sentenced Cody Gregg to 15 years in prison after Gregg pleaded guilty to possession of cocaine with intent to distribute. Days later, a drug test found that the “cocaine” was actually powdered milk. Gregg withdrew his plea, and the judge dismissed the charge. Gregg had initially pleaded not guilty, but he changed his mind after spending two months in the Oklahoma County jail.

Australia’s Department of Home Affairs says it wants to use facial recognition technology to limit children’s access to online pornography. Those who want to watch porn would have their faces scanned and matched to the photos on their official IDs to prove they are adults. Critics say this would allow the government to know every porn site that any person goes to.

San Antonio, Texas, officials have agreed to pay $205,000 to settle a lawsuit brought by Natalie Simms after a police officer conducted a cavity search of her on a public street. Simms says she was sitting on a curb when officers approached, told her they thought she might have drugs, and asked to search her car. She agreed. While Simms was being detained, she says a female officer arrived and began to frisk her. That officer pulled down Simms’ pants and underwear and searched her vagina, pulling out Simms’ tampon and holding it up for other officers to see. The cops found no drugs.

Drexel University in Philadelphia has agreed to pay the federal government $189,062 after a former professor at the school used federal grant money to make iTunes purchases and to visit strip clubs and sports bars. That professor, Chikaodinaka D. Nwankpa, the head of Drexel’s Department of Electrical and Computer Engineering, agreed to repay $53,328 to the university and to resign.

Officials at St. Andrew’s Primary School in Hull, England, have barred parents from packing any drinks other than water with their children’s meals. They say the move is aimed at protecting students with allergies and reducing consumption of sugary drinks.

Eliana Bauta, a former employee of New York City’s Human Resources Administration, has been sentenced to two years in prison for her role in the theft of more than $300,000 in emergency benefits money from her department. Bauta used part of the money she stole to pay someone to put a voodoo spell on a former boyfriend.

Jason Kirkbride’s hair is neat, tidy, and short—too short for Hodgson Academy in England, according to his mother. She says she decided to get the 14-year-old’s hair cut a little shorter than usual so he could go longer between visits to the barber. But school rules say hair should be no shorter than a No. 2 clipper, so the boy received three days’ detention.

from Latest – Reason.com https://ift.tt/2RLxtjP

via IFTTT

China To Exempt Taxes For Certain U.S. Products To Win Fight Against “Devil Virus”

The Ministry of Finance of the People’s Republic of China published a statement Saturday, reviewed by Reuters, noting that tax exemptions for imported products from the U.S. will be enacted to help the country combat the deadly outbreak of coronavirus.

According to the statement, all products that will be tax-exempt must be directly for the use of “epidemic control” and will be exempt from import tariffs through the end of March.

Some of these products include 3M face masks, Ford or Chevy ambulances and disinfectant products.

There was no mention by the finance ministry whether Beijing would continue to honor the phase one trade deal signed with the U.S. last month.

In three weeks’ time from the signing of the trade agreement, two-thirds of China’s economy has virtually ground to a halt, major manufacturing hubs have been shuttered, more than 50 million people are quarantined, and transportation networks across the country have come to a standstill.

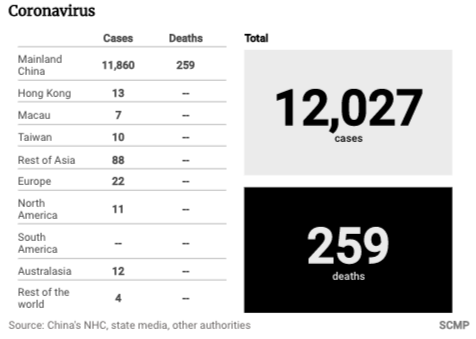

About 12,000 cases of coronavirus have so far been reported in China (as of Friday night), with 259 deaths, along with a new report from Hong Kong scientists that estimate at least 75,000 people in Wuhan might be infected.

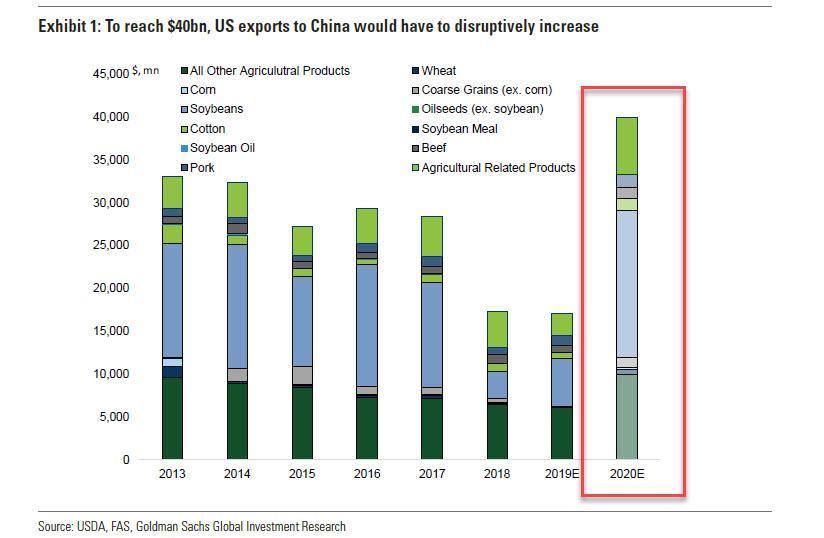

China accounts for 17% of global GDP, up from 4% in 2003, with much of the world’s supply chains are deeply rooted in the country and are currently shutdown. Growth perspectives for China and the world are plunging, the bond market and commodities say so, which means demand for products from the U.S. will decline, this makes it hard for China to meet hard targets of the phase one trade agreement.

So about that $200 billion in goods, China has to buy from the U.S…

Russian oil firm Tatneft could strike a deal with Zimbabwe to supply fuel to the crisis-stricken African country in exchange for diamonds, the Zimbabwe Independent reported on Friday, describing the potential deal as ‘murky’ because Zimbabwe’s Minister of Mining, Winston Chitando, told the news outlet that he was not aware of any such development.

“It is the first time I am hearing of that. The bottom line is that it is not true. I maintain that it is not true,” Chitando told the Zimbabwe Independent.

The potential deal, reportedly worth US$1.4 billion, would see Russia’s Tatneft ship in fuel to Zimbabwe via the Port of Beira in Mozambique, according to the Zimbabwe Independent.

Last week, Tatneft’s general director Nail Maganov told Russia’s news agency Interfax that Tatneft was indeed working on an agreement to supply fuel to Zimbabwe as part of a fuel-for-diamonds deal.

“We are working on this issue. I want to say that this is a real thing… I know that the fuel supply is real,” Maganov told Interfax on the sidelines of the World Economic Forum in Davos last week.

Previous reports had it that Russia’s diamond mining giant Alrosa would also be involved in the deal.

Alrosa is not part of this fuel for diamonds scheme, Alrosa’s press service told Interfax last week.

Zimbabwe is looking at alternatives to buying fuel amid a raging economic crisis and hyperinflation, where fuel, food, basic commodities, and necessities are scarce, while a currency shortage doesn’t allow the authorities to buy fuel on the free market.

Zimbabwe also faces a hunger crisis due to drought, the World Food Programme (WFP) said in December. The economy is in tatters, and Zimbabweans are going hungry and cannot afford basic necessities amid the hyperinflation.

“BOOOO!”: Squadmate Rashida Tlaib Boos Hillary Clinton At Bernie Sanders Event

It appears that the progressive wing of the Democratic party is still bitter over the way Bernie Sanders was treated in the 2016 primaries, after WikiLeaks email releases exposed a coordinated effort to hurt the Vermont Senator while helping then-candidate Hillary Clinton.

Clinton, meanwhile, has been taking trash against Sanders of late – lashing out at Bernie and his supporters for ‘not doing enough to unify the party in 2016’ after he was shafted, and saying “nobody likes [Sanders].”

At an Iowa campaign event on Friday, progressive ‘squadmates’ Reps. Rashida Tlaib (D-MI), Ilhan Omar (D-MN) and Pramila Jayapal (D-WA) were ending a panel discussion with moderator and activist Dionna Langford, who mentioned Clinon’s recent attacks, to which the audience began booing, according to The Hill.

Langford tried to diffuse, saying “We’re not gonna boo, we’re not gonna boo. We’re classy here.”

Tlaib, however, jumped in and said “I’ll boo. Boo,” adding “You all know I can’t be quiet. The haters will shut up on Monday when we win.”

The moment comes as underlying tensions from 2016 appear to be bubbling up in the 2020 election. Sanders supporters have fiercely defended their candidate after a new interview from Clinton criticizing her former opponent.

In an interview with The Hollywood Reporter published last week, Clinton said she stood by past comments of Sanders, saying: “Nobody likes him, nobody wants to work with him, he got nothing done.”

She also in the interview refused to confirm whether she would endorse or campaign for Sanders should he win the Democratic nomination this year. –The Hill

Sanders, meanwhile, has been shooting up in the polls – and has surpassed frontrunner Joe Biden in several state polls. This, despite Elizabeth Warren slinging sexism arrows at the 78-year-old candidate.

On Wednesday, the Federal Reserve concluded their January “FOMC” meeting and released their statement. Overall, there was not much to get excited about, as it was virtually the same statement they released at the last meeting.

However, Jerome Powell made a comment which caught our attention:

““We do see asset valuations as being somewhat elevated”

It is an interesting comment because he compares it to equity yields.

“One way to think about equity prices is what’s the premium you’re getting paid to own equities rather than risk-free debt.”

As we have discussed previously, looking at equity yield, which is the inverse of the price-earnings ratio, versus owning bonds is a flawed and ultimately dangerous premise. To wit:

“Earnings yield has been the cornerstone of the ‘Fed Model’ since the early ’80s. The Fed Model states that when the earnings yield on stocks (earnings divided by price) is higher than the Treasury yield, you should invest in stocks and vice-versa.”

The problem here is two-fold.

1. You receive the income from owning a Treasury bond, whereas there is no tangible return from an earnings yield. For example, if we purchase a Treasury bond with a 5% yield and stock with an 8% earnings yield, if the price of both assets remains stable for one year, the net return on the bond is 5% while the return on the stock is 0%. Which one had the better return? Furthermore, this has been especially true over the last two decades where owning bonds has outperformed owning stocks. (Data is total real return via Aswath Damodaran, NYU)

2. Unlike stocks, bonds have a finite value. At maturity, the principal is returned to the holder along with the final interest payment. However, while stocks may have an “earnings yield,” which is never received, stocks have price risk, no maturity, and no repayment of principal feature. The risk of owning a stock is exponentially more significant than owning a “risk-free” bond.

This flawed concept of risk, as promoted by the Federal Reserve, also undermines their view of current valuations.

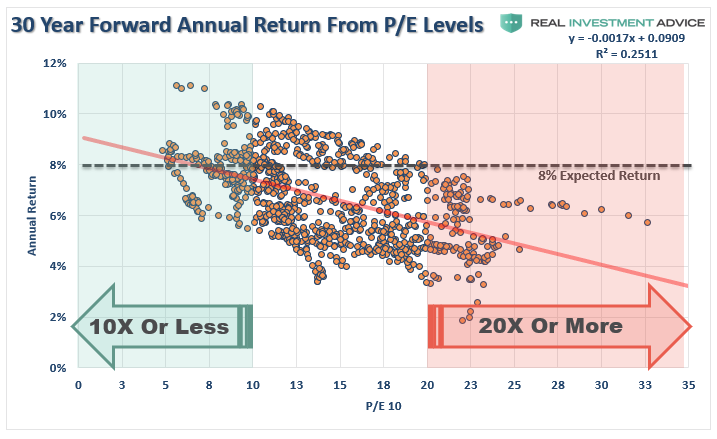

I have spilled an enormous amount of “digital ink” discussing the importance of valuations on future returns for investors, and most recently, why high starting valuations are critically important to individuals at, or near, retirement.

“Over any 30-year period, beginning valuation levels have a tremendous impact on future returns. As valuations rise, future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay for an asset today, the future returns must, and will, be lower.”

Not surprisingly, valuations are often dismissed in the short-term because there is not an immediate impact on price returns. Valuations, by their very nature, are not strong predictors of 12-month returns. This was a point made by Janet Yellen in 2017:

“The fact that [stock market] valuations are high doesn’t mean that they’re necessarily overvalued. For starters, high valuations don’t portend lackluster returns in the near term. History shows that valuations provide no reliable signal as to what will happen in the next 12 months.”

That is correct. However, over long periods, valuations are strong predictors of expected returns, which is what matters for investors.

“The problem is that P/E, even Shiller’s cyclically adjusted P/E ratio (CAPE), is a potential value-trap measure in the current economy because of three issues:

Profit margins are unsustainably high today, not only within this business cycle but compared to other business cycles making P/E ratios understated;

The P/E ratio completely ignores debt in its valuation, not a good idea at a time when corporations have record leverage; and

The most common measures of total market P/E use the mean rather than median company valuation which understates the average company’s multiple today by putting more weight on bigger, more profitable companies – the median better captures the valuation of the breadth of the market.

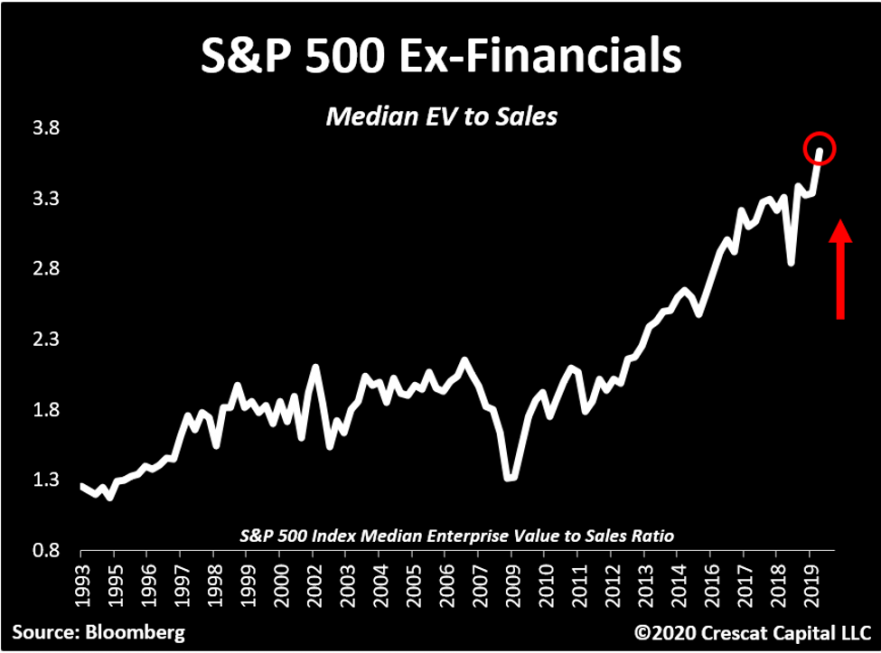

We believe median enterprise value to sales is one of the best measures to understand the extent of the bubble in the stock market today compared to history. By looking at sales and not earnings, we control for today’s likely fleeting, record-high profit margins. And because EV includes debt as well as equity in the total valuation of the company, it properly reflects the valuation of the business. Finally, our focus on the median company’s valuation illustrates the breadth of the valuation extreme in the market today.”

Let’s break down Crescat’s important points visually.

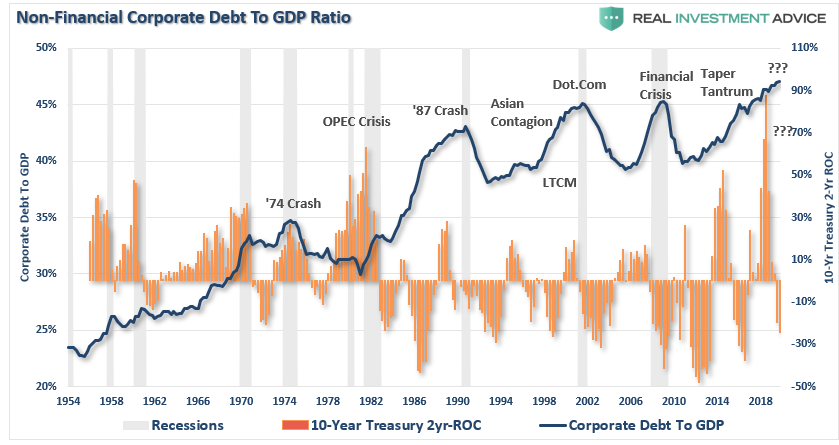

Since the economy is driven by consumption, and theoretically, companies should be taking on debt for productive purposes to meet rising demand, analyzing corporate debt relative to underlying economic growth gives us a view on leverage levels.

As Scott Minerd, CIO of Guggenheim Investments tweeted on Friday:

There is no doubt that we are in the “everything bubble.” Pick your asset class and prices are up. But the heavily indebted corporate sector is vulnerable if the #economy begins to slow.

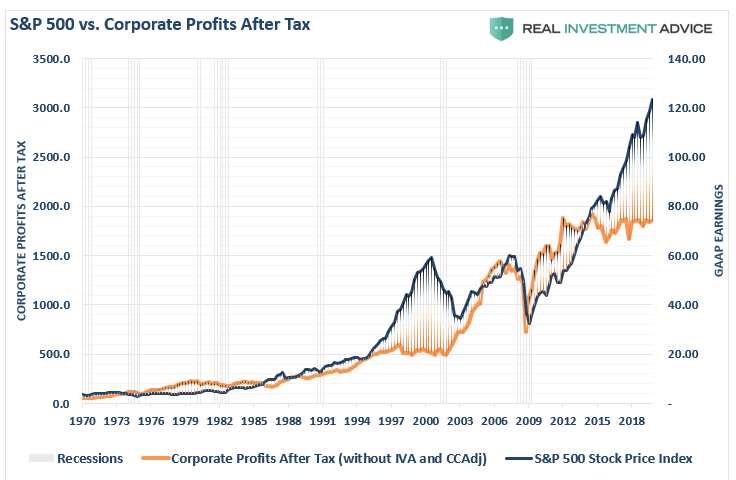

The problem with debt, of course, is it is leverage that has to be serviced by underlying cash flows of the business. While asset prices have surged to historic highs, corporate profits for the entirety of U.S. business have remained flat since 2014. Such doesn’t suggest the addition of leverage is being done to “grow” profits, but rather to “sustain” them.

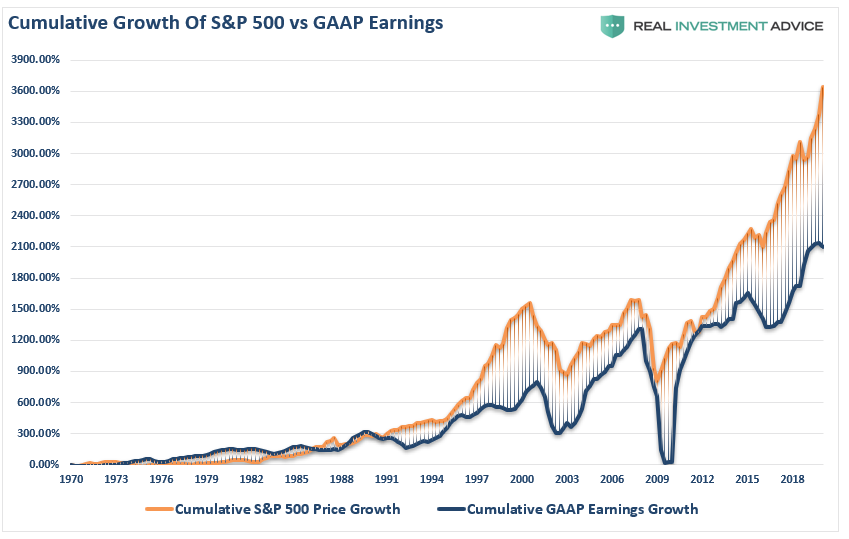

However, when it comes to GAAP earnings per share, which have been heavily manipulated by massive levels of “share buybacks,”the deviation between what investors are paying for earnings is the largest on record, far surpassing the “Dot.com” bubble era.

“The average investor does not need an advanced finance degree to understand these valuation points. It is a worthy endeavor to avoid getting caught up in the popular delusions associated with late-cycle market euphoria. We believe investors will need a good grounding in valuation and business cycle analysis to reject the common buy-the-dip advice that is soon to become prevalent in the still early stages of what is likely to become a brutal bear market.” – Crescat Capital

As I stated above, what price-to-earnings (P/E) ratios tell us is that high valuations lead to lower future returns over time. However, what Jerome Powell misses in comments that valuations are elevated, but not concerning, is that it isn’t just P/E’s which are elevated.

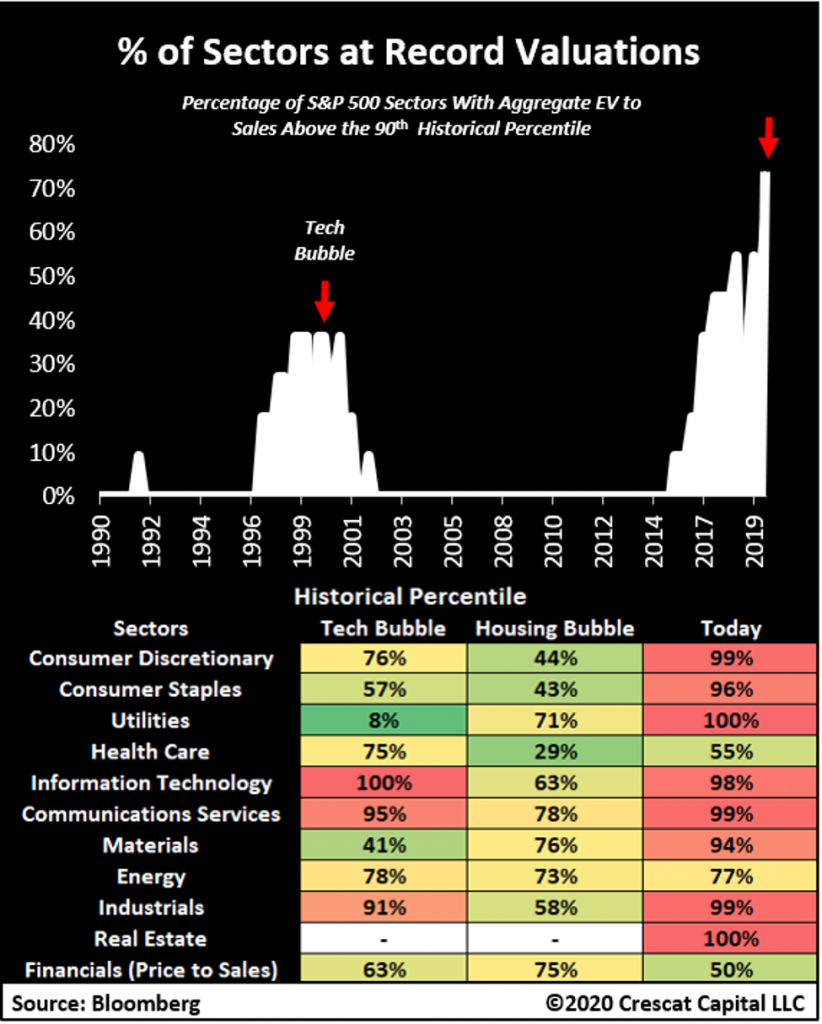

“Below is another way to visualize the current market valuation extremes to understand the risks of a severe market downturn ahead. Here we look at each sector of the S&P 500 and compare its valuation today to compared to prior market peaks in the tech and housing bubbles in 2000 and 2007. We can see that an unprecedented 8 out of 11 sectors are at top-decile, historical valuations illustrating the breadth of the current market excess.” – Crescat Capital

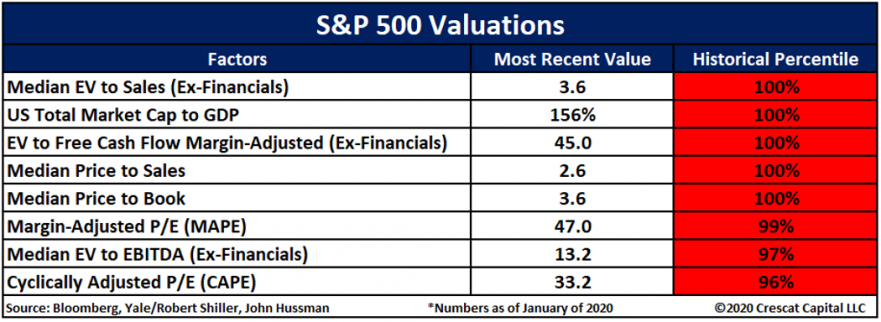

“Below we show the gamut of measures currently at record high fundamental valuation for the market at large based on their historical percentile ranking. Data for MAPE and CAPE ratios go back prior to 1929! The other measures are based on the entire history of available data which goes back at least two and half business cycles:” – Crescat Capital

Low Interest Rates Support Higher Valuations

This is where we generally hear a common refrain from the mainstream media:

“Low levels of interest rates justify higher valuations.”

To analyze the relative value argument, let’s look at the interaction of interest rates and stock valuations over the broad sweep of time. As shown, extremely high stock market valuations occurred in 1929, 2000, and recently. However, interest rates were extremely low only once (recently) during those three occurrences. If low interest rates coincide with extremely high stock valuations only one time out of three, then it is obvious that low interest rates do not cause, or justify, high stock valuations. Yet “low interest rates justify high stock valuations” is one of the certainties of the current mainstream narrative.

Source: Robert Shiller, multipl.com. Data through June 2017.

If we isolate the times when interest rates were extremely low, the 1940s and currently, we find in the 1940s stock valuations were low. So, the statement that low interest rates justify high stock valuations is only supported by one event….now.

A better understanding is achieved by the relative value argument that extremely high interest rates coincide with extremely low stock market valuations, which occurred in 1921 and 1981. Although a sample size of two observations is not enough to draw a statistically-significant conclusion, at least it is two events with the same outcome.

The historical relationship between extremes in stock market valuations with extremes in interest rates is as follows:

Extremely high interest rates, which have occurred twice, coincided with low stock market valuations.

Extremely low interest rates, which have occurred twice, have coincided with high stock market valuations only once; today.

Extremely high stock valuations have occurred three times. Only once (1/3 probability) did high stock valuations coincide with low interest rates; today.

If extremely low interest rates do not justify extremely high stock market valuations, then a rise in rates should not necessarily cause a decline in stocks, but rising rates do lead to market corrections and bear markets.

Crescat Capital also weighed in on this point as well:

“A common argument today is that low interest rates justify today’s high equity valuations. That is not true at all. When low interest rates are due to low growth and excessive debt, as is the case today, no valuation premium is justified.”

Make No Mistake

Jerome Powell clearly understands that a decade of monetary infusions and low interest rates has created an asset bubble larger than any other in history. However, they are trapped by their own policies as any reversal leads to the one outcome they can’t afford – a broad market correction.

“In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became ‘active,’ monetarily policy-wise, in the late 70’s.”

This is the problem facing the Fed.

Currently, investors have been led to believe that no matter what happens, the Fed can bail out the markets and keep the bull market going for a while longer. Or rather, as Dr. Irving Fisher once uttered:

“Stocks have reached a permanently high plateau.”

Interestingly, the Fed is dependent on both market participants, and consumers, believing in this idea. With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the “instability of stability” is now the most significant risk.

The “stability/instability paradox” assumes that all players are rational, and such rationality implies avoidance of complete destruction. In other words, all players will act rationally, and no one will push “the big red button.”

The Fed is highly dependent on this assumption as it provides the “room” needed, after more than 10-years of the most unprecedented monetary policy program in U.S. history, to try and navigate the risks that have built up in the system.

Simply, the Fed is dependent on “everyone acting rationally.”

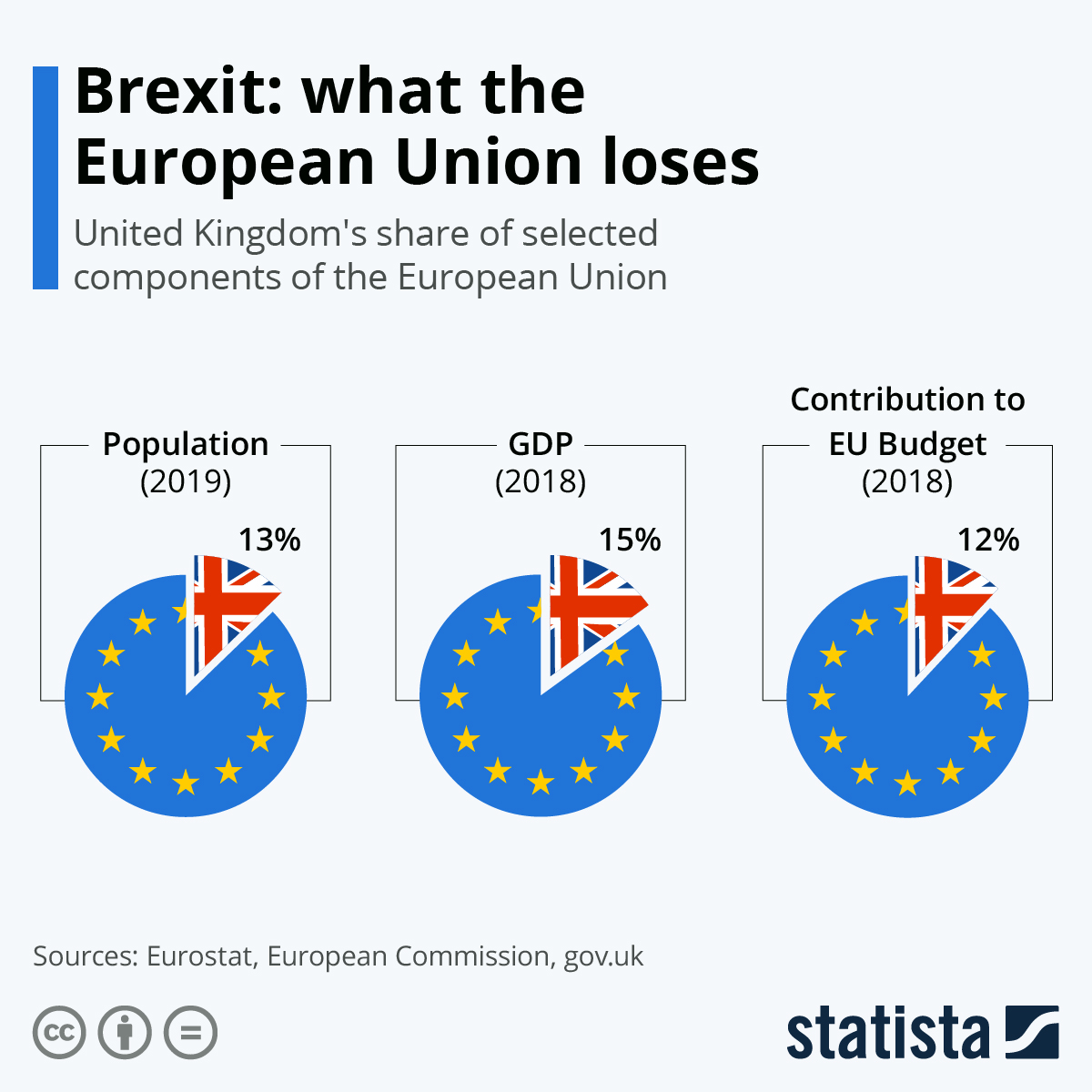

1,317 days since the nation went to the polling booths and voted to leave the European Union, ‘Brexit Day’ is finally here.

A lot has been written, forecast and argued about what the effect on the UK will be once it is finally out of the EU, but in this infographic, Statista’s Martin Armstronglooks at it from the other side.

‘Calm Before The Storm’ – How Will The Coronavirus Really Impact The Markets?

PeakProsperity’s Adam Taggart that, officials, the media, and globalist-driven organisations are downplaying Wuhan coronavirus risk, even as models suggest infections will soon soar.

The sudden slowdown in new information coming out of China has Chris Martenson spooked.

He walks us through the math here, showing how if the coronavirus follows its current geometric growth, over 100 million people could be infected by the end of February:

Don’t take the recent lack of ‘news’ as meaning the threat from this virus is dying down. This could very likely just be the calm before the storm.

In fact, as Martenson explains, it’s a true Black Swan event that stocks haven’t yet priced in.

The 2019-nCoV “coronavirus” outbreak remains serious and fluid.

Over the past several days, we’ve been publishing a steady stream of videos, reports and podcasts to keep you as up-to-date and informed as possible on the science behind this fast-developing situation. You can follow our full coverage of the coronavirus here.

But the TL;DR version is this:

The first order of business is stopping the spread of the disease, which means prevention. Your immediate and top concern should be readying yourself and your household and loved ones for the arrival of 2019-nCoV. We cover the most useful practices in this report.

Second, help your co-workers and students, passengers, or other such dependents become aware and prepared by practicing good hygiene and educating them about how the virus spreads.

IMPORTANT: Anyone who is sick, whether with nCoV or a standard flu/cold, needs to be isolated for the duration of the disease, which means 24 hours after their last fever. They should always, always, always wear a surgical mask to block virus particles before they are expelled into the air. Masks can be worn by everyone, but do the most good when worn by those who are ill.

But in addition to presenting a major public health risk, the coronavirus is already doing serious economic damage. China, the world’s second-largest economy, is essentially “closed for business” right now.

The disruption to global trade the coronavirus is likely to cause is going to be material, perhaps severe. And that will have serious negative consequences for the financial markets, which have been (and is still!) trading at the highest valuations in history.

The coronavirus has all the hallmarks of a true Black Swan event.

Markets & Global Economy Already Impacted

Note:This is an extremely fast-moving situation and the data is coming in so quickly that it has to be presented as a mosaic. I’ll do my best to make sense of it for you, but I really want you to allow yourself to trust your own assessment of what pattern the dots make. Much of this data has just been gathered this morning (1/28/20).

Remember: it’s not the fall that harms you, it’s how fast you stop.

For years now, the global economy has been debt-strangled and limping along, kept alive by constant central bank interventions and money printing. Like any weakened victim, the last thing it needs is any kind of serious shock.

The coronavirus has all the features of the proverbial Black Swan event we’ve long been worried about. Nobody saw it coming, it hit hard and fast, and is spreading far faster than government bureaucracies and the markets can adjust.

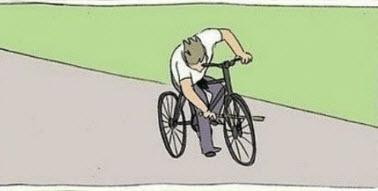

It’s the equivalent of slipping an iron bar into the front spokes of a moving bicycle.

We can’t possibly predict how all the implications of this will manifest. Our globalized economy is just too complex. We have a world-wide, just-in-time manufacturing and delivery system. Which just got a huge stick shoved between its spokes.

What does it mean to completely shut down the normal business activities of cities with 5, 10 and even 25 million inhabitants? Particularly in a country with massive property bubbles, where the median price-to-income ratio can be as sky-high as 40(!!)?

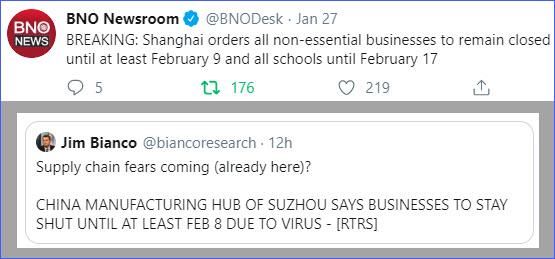

Shanghai has a population of 24 million and Suzhou another 10.7 million. Both are now all but completely shut down.

Shanghai is China’s equivalent of New York City. It hosts the main stock exchange and is where the Shanghai Gold Exchange (SGE) is located. Suzhou is a vital manufacturing hub.

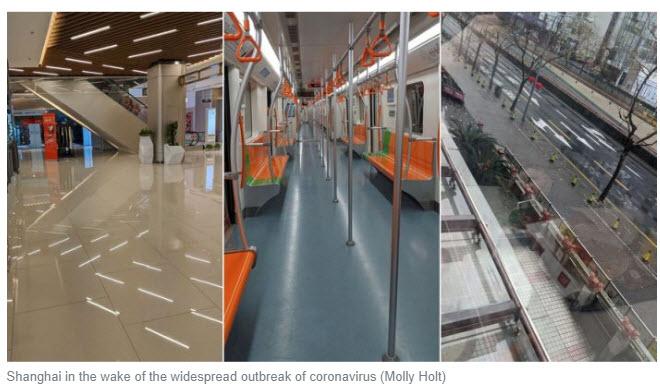

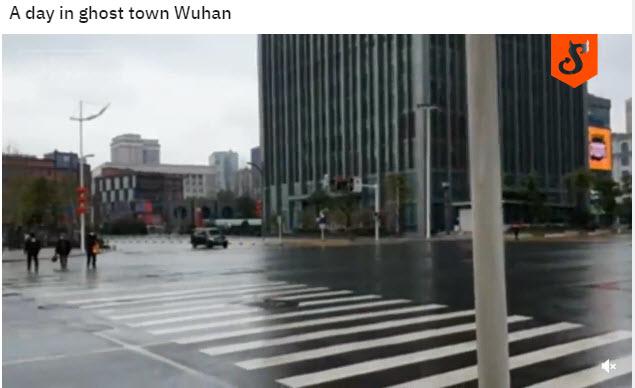

I can’t express just how crazy it is to see the videos and pictures from these towns showing empty 8-lane roads, which are normally crammed 24/7 with cars and trucks. Empty subway cars. Nearly abandoned railway stations. Empty sidewalks.

Like literal ghost towns. ‘Ghost cities’ in this case.

If that isn’t a stick in the spokes, I don’t know what is. There’s just no way to plan for such an event. You just have to brace for the impact.

Once people self-isolate (which is exactly what they should be doing, and what I will do myself should the virus makes it to my town), economic activity just… stops.

And this is being woefully underappreciated by the global equity markets right now.

Of course, I’ve long ranted that we now have bastardized ““markets””, deformed by the terribly misguided and ultimately destructive actions of the world’s central banks and their misguided money printing.

Well, good luck trying to print your way past a virus. Or of a nation’s bus drivers and factory workers staying home.

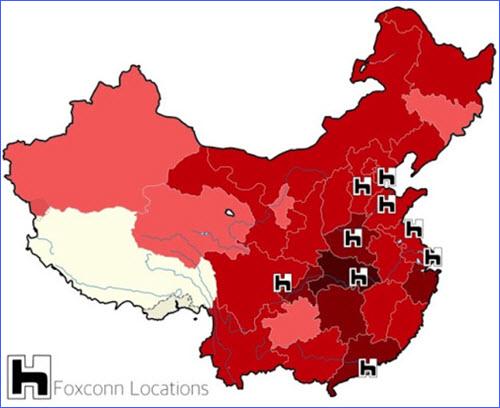

Below is a graphic showing the location of Apple’s Foxconn plants relative to the coronavirus outbreak:

And yet Apple stock is still trading within a whisker of its all-time high, up nearly 3% as I’m typing this.

I can’t really wrap my head around this cavernous train station being all but completely deserted. Anyone who’s been to Beijing knows that this place is usually furiously humming with commuters like a beehive. The contrast is really stunning.

Wuhan

The above is a usually completely crammed intersection. All we see now is a single parked car.

A few people just strolling across the equivalent of 5th Ave NY in the middle of the day without even bothering to look either way. There’s no one about.

Global Travel

Whether for business or pleasure, global travel is being impacted. Tourism is taking a huge hit. Again, there are almost too many data points to process. But here are a few:

Too Much To Process

I have too many other such data points to present. I don’t want to overload you or make this article encyclopedic. But hopefully I’ve provided enough examples above to give you a sense of the near-instantaneous halt the coronavirus has placed on China’s domestic economy and travel.

The data on its impact on manufacturing and trade won’t be known for a little longer, but it’s safe to guess it will be ‘significant.’

This is the nature of fast-moving situations. You have to rapidly grasp a lot of fragmentary data and turn it into something actionable.

And I’ll give you my sense: This is already a massive shock to the Chinese economy. Which in this hyper-connected world, will quickly translate into a shock to the entire global economy.

That hasn’t fully registered yet for most people, and therefore, the markets. But that’s coming. Soon.

The US Is Especially Vulnerable

In the US, healthcare costs are the #1 economic threat to households. More families go bankrupt due to our predatory and inhumane medical care system that any other cause.

Because people can’t afford to call an ambulance or dare to go to the emergency room for fear of being financially destroyed, they will resist seeking treatment until the very last minute. This means detecting people infected with the coronavirus will be slower than in many other countries. Which means the illness will be able to spread farther and faster as the unhospitalized sick and untreated infect more people.

“If The Dow Is Up, Everything’s OK. Right?”

Financial price bubbles require two things to sustain themselves: ample credit and a compelling story.

Ample credit has been supplied by increasingly desperate central banks willing to do “whatever it takes” to keep stock and bond prices elevated.

A normal market confronted with all the above evidence and uncertainty would be experiencing a sell-off here. Markets are supposed to based on future earnings. Less economic activity = less future earnings. Some sort of downwards repricing would be prudent, healthy and mathematically sound at this point.

But what are they doing?

Being bought furiously in the overnight ““markets””. Here’s a chart of the last week:

This is how silly and stupid things have become. The Fed and the Plunge Protection team (PPT) are now on a daily mission to keep stocks from selling off.

This is wrong, perhaps even evil. As it keeps people from appreciating the gravity of the situation. Falling markets would signal that maybe, possibly, something is wrong. That investors should start adopting more caution.

Which they should at this time. Current stock prices simply can’t be justified given what the coronavirus is doing to the world economy. No way, no how.

What Happens If….?

As I said, bubbles need two things: ample credit and a good story. The main “story” of the markets over the past few years has become almost entirely this; “The Fed won’t let them fall.”

There’s been a lot of truth to that sentiment. It’s not wrong. Or at least it hasn’t been.

But can Fed printing and market-propping make China’s empty mega-highways and grounded flights start burning more oil? No, it can’t. So, oil prices will fall. And US oil companies will suffer.

Can Fed printing and market-propping compel the Chinese workers to return to their factories? No.

Can Fed printing and market-propping make tourists return when no one wants to be around crowds? Again, no.

These and a dozen other such questions all end in “no.”

Which is why the story that has been driving the stock market bubble suddenly is breaking.

So, what will happen when the Fed is revealed to be impotent?

Well, then that’s the end. No narrative = no bubble.

And at today’s record highs?

A painful market correction, perhaps even a full-blown crash (stocks down 30-50%), will be the inevitable result.

Conclusion

Today markets are still clinging to the idea that the Fed “has got this.” The sell-off on Monday (just -1.5% on the S%P 500) was entirely too minor to count as anything at all. The vigorous futures buying the next morning says the same thing.

The market doesn’t yet believe that the coronavirus risk is real.

Which means that this may be one of those very rare moments in market history where the immediate future is briefly visible to us, just a little bit before everyone else.

Once you’ve taken the necessary steps to protect your family’s health against the coronavirus threat, then do the same for your money.

Minimize risk. Reduce your exposure to a market crash. And, for those with the risk tolerance, possibly position yourself to profit from one. (Full disclosure I am net short the US equity markets at present)

There are many ways to reduce risk in your portfolio. In this report for our premium readers, Positioning For A Downturn we detail out the wide range of options that investors have for both protecting against a downturn and, for the more courageous, profiting from one.

Again, we are in a rare and likely very brief moment where we see the risks from the coronavirus that the market does not. Use this time wisely.

Click here to read the report (free executive summary, enrollment required for full access).

Last week a California-based animal rights group released gruesome photos and other evidence it says it gathered during an undercover investigation it carried out last April at an Iowa pig farm.

The disgusting photos, which you can view here, variously show overcrowding, pigs suffering from abscesses and other open sores, severed limbs scattered on the facility floor, and dead and dying pigs. Additionally, the group says the air inside the facility was “noxious.”

“Footage shot by DxE shows the brutal toll of animal agriculture—conditions which spell an agonizing death for many Rosewood Pork pigs, and a life of continual suffering for them all,” the report declares.

While the name of the farm isn’t particularly noteworthy, its owner is Iowa State Sen. Ken Rozenboom (R). He’s both a leader in the state’s agricultural community and a “leading supporter” of Iowa’s reprehensible and unconstitutional agricultural gag (ag-gag) law—which is intended to stifle critical reporting on agricultural facilities and practices.

“Ag-gag laws, which are on the books in eight states, including Idaho, are laws that effectively ban journalists, whistleblowers, and activists from conducting or sharing the results of undercover investigations at agricultural and livestock processing facilities,” I wrote in a 2016 blog post that discussed why I had organized fellow law-school faculty in submitting an amicus brief opposing Idaho’s ag-gag law.

In that brief, we explained the First Amendment and consumer-protection harms ag-gag laws cause, arguing that they “ultimately den[y] consumers a marketplace of ideas in which they are free to weigh competing voices and decide for themselves the truth about food production.”

While Idaho’s ag-gag law was eventually overturned, similar laws are still on the books in a handful of states, including Iowa, where a court challenge has halted enforcement of the law.

This week, State Sen. Rozenboom acknowledged at least some truth behind the shocking allegations. He conceded the investigation revealed “careless animal husbandry practices that violate acceptable animal care protocols.”

“I acknowledge that there were caretaker deficiencies,” Rozenboom told the Des Moines Register. “There were things that not ought to have happened, that we’re not OK with. I’m ashamed of it.”

But he also remained defiant.

“This type of dangerous, illegal activity cannot be condoned,” Rozenboom said of the animal-rights group’s investigation. He also says he’ll ask the state to prosecute DxE investigators on trespassing charges.

“While acknowledging some problems at the facility, state Sen. Ken Rozenboom said Thursday the investigation was a ‘professional hit job’ designed to undermine consumer support for the pork industry,” the Register reports.

That’s an incredibly shortsighted and tone-deaf comment. Rozenboom must know that the conditions alleged to have existed at his farm are what really undermines consumer support for the pork industry. If the DxE investigation had captured a well-run operation that showed a modicum of regard for the animals before their slaughter, no one would be talking about Rozenboom’s farm.

Various reports indicate Rozenboom was leasing the facility in question to another farmer during the period when the DxE investigation took place. Rozenboom says he ended the business relationship with the lessee last year at least in part over concerns about the farmer’s treatment of pigs.

“He said they made the switch because they were concerned about how the former operator cared for his animals and maintained the building,” the Registerreports. “He pointed to delays in removing dead pigs from the facility as an example.”

While there is absolutely no indication Rozenboom participated in any animal abuse that may have occurred on his farm, I’ve also seen no indications that Rozenboom reported the “concern[ing]” actions of his unnamed lessee to law enforcement or state regulators.

If there was a whistle to blow, Rozenboom appears to have kept it in his pocket. That fact alone makes the DxE investigation a vitally important contribution to the marketplace of ideas.

The undercover investigation was led by Matt Johnson, a DxE official who hails from Iowa. I asked Johnson last week about DxE’s goals, including whether he and his colleagues want to end all animal agriculture and meat-eating. He didn’t mince words.

“The short answer is yes, we want to end animal agriculture,” Johnson told me by email. He also says that he and DxE believe all livestock farming is inherently inhumane. “We don’t believe in humane animal ag,” Johnson writes.

I applaud DxE for exposing what appear by every indication to be brutal, disgusting, inhumane, neglectful, and monstrous conditions at the pig farm. DxE’s investigation benefits animals and American consumers alike. But my boisterous applause ends right about there.

For DxE, investigations such as this one are a means to an end. And that end is the adoption of new laws that outlaw all animal agriculture and completely banish meat from the American diet. I could not disagree more with DxE’s goal to end all animal agriculture. I believe every person has a right to make their own food choices—whatever those may be.

I strongly support the right of farmers everywhere to raise livestock for food, a position I’ve held for years. I also believe that the overwhelming majority of food producers in this country take proper care of the animals they raise for food. In 2016, I toured a pig farm in Iowa and found it predictably smelly but otherwise clean and humane.

After a recent ruling that enjoined Iowa from enforcing its ag-gag law, Rozenboom told the Gazette he was “personally very disgusted that we can’t protect honest, hardworking Iowans but we’ll protect criminals and people that lie for a living.”

This is nonsense. It is entirely possible to support investigations like the one DxE conducted and to oppose the group’s ultimate goal; just as it is possible to support animal agriculture and the people who make it possible while opposing ag-gag laws and the people who treat animals as Rozenboom’s farm lessee reportedly did.

from Latest – Reason.com https://ift.tt/2OmfbDQ

via IFTTT

{kind=link}