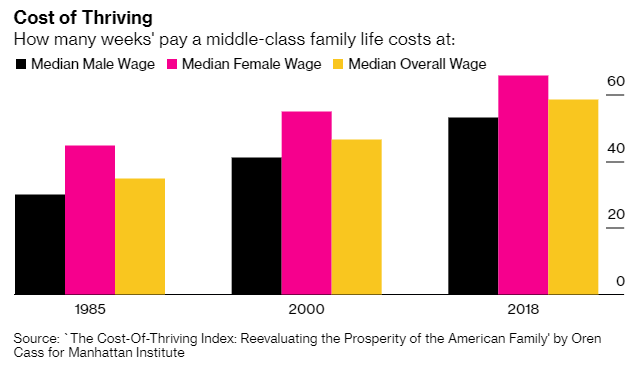

New Study Shows Average U.S. Worker Needs 53 Weeks In A Year Just To Earn “Middle Class” Lifestyle

A new study by Oren Cass at the Manhattan Institute confirms that a 52 week year just doesn’t cut it for the average American worker looking to simply make a “middle-class” life for themselves. For women, the news is even worse: it requires 66 weeks to earn a middle class lifestyle.

These figures compare wildly to 1985, when males at the median weekly wage needed to work only 30 weeks and women only needed to work 45 weeks, according to Bloomberg.

The paper tried to compile a “cost of thriving” index for the purposes of gauging quality of life. The “middle class” is defined as a 3 bedroom house just below the mid range of market prices, family health insurance, costs associated with a vehicle and a semester at public college.

The study’s author, Oren Cass, is a former adviser to Mitt Romney’s 2012 presidential campaign. He says that while his index is imperfect and it doesn’t account for wide cost and income difference, it’s a “starting point”. It also doesn’t account for larger houses, advances in medicine and safer cars.

Cass introduces the problem by saying: “A dramatic divergence between data and experience is confounding America’s policy debates. The data seem to show that households have attained unprecedented prosperity, and wages have (at worst) held their own against inflation, or (at best) risen much faster than prices. By conventional measures, material living standards everywhere in the income distribution are at all-time highs, and technological progress continues to improve them.”

He continues: “Yet many jobs able to support a family in the past no longer do. Millennials are in worse financial shape than were those of Generation X at the same age, who themselves had fallen behind the baby boomers. The stories appear irreconcilable.”

Cass thrashes the case that quality of life has improved enough to outpace inflation and the widening inequality gap. He says workers don’t always have the option to substitute worse, but cheaper, goods if their incomes aren’t rising fast enough to afford newer and better products.

He also found that only incomes among men holding Bachelor’s degrees have risen more than consumer prices since 1980.

Cass concludes: “The explanation is this: inflation does not measure affordability. Key assumptions built in to inflation indexes for the purpose of measuring the underlying, economy-wide upward pressure on prices are different from, and often counter to, the key assumptions necessary for assessing the economic choices and constraints faced by households. When analysts use inflation adjustments to compare household resources over time, they have chosen the wrong vantage point, and their view is obscured.”

His study also concludes that economists and families see three things differently:

Quality Adjustment. Products and services that rise substantially in price but in proportion to measured quality improvements can become unaffordable, while having no effect on inflation.

Risk-Sharing. New products and services can increase costs for the entire population yet deliver benefits to only a very small share, while having no effect on inflation.

Social Norms. Society-wide changes in behaviors and expectations can alter the value or necessity of a good or service, while having no effect on inflation.

A lot of folks have distrusted the numbers coming out of China since the very beginning of the coronavirus outbreak. That uneasy feeling was justified when it was discovered that many patients weren’t being counted because they were never tested. Once an alternative testing method was temporarily approved, the number of infected people skyrocketed. This was only temporary though because Chinese officials reverted quickly to their previous method of only relying on the nucleic acid test, which is infamous for false negatives. (There are reports that suggest certain infected people tested negative as many as six times before a positive test occurred, according to MedicineNet.)

Looking at China’s official response and looking at the American official response, I see some troubling similarities that make me wonder if our own numbers are accurate at all.

Hardly anyone is actually being tested in the United States.

First of all, very few tests have actually been performed in the United States. As of Feb. 26, 2020, the CDC reported that only 466 tests had been performed in the US and the criteria for being tested is so narrow as to render the statistics useless.

This was proven to be the case with the patient in California who was finally tested after four days and found to have Covid19, even though she has not been to China or knowingly been in contact with anyone from China. Why wasn’t she tested sooner?

Because she didn’t fit “the criteria” laid out by the CDC for testing.

Hospital administrators said they immediately requested diagnostic testing from the Centers for Disease Control and Prevention, but the procedure was not carried out because the case did not qualify under strict federal criteria: She had not traveled to China and had not been in contact with anyone known to be infected. (source)

So this delay in testing was not the fault of physicians caring for her, but because the CDC decided from afar that only certain patients could be tested. If this sounds familiar, it’s because, in China, only certain patients were given tests while thousands of others were turned away from healthcare facilities without assessment.

Here’s the narrow criteria to get tested. Basically, if you haven’t been to an affected country or been exposed to someone from an affected country, you’re unlikely to be tested.

And it gets even worse.

The first batch of tests sent out to health departments around the country was faulty.

…expanded testing has been delayed because of an unspecified problem with one of the compounds used in the CDC test. About half of state labs got inconclusive results when using the compound, so the CDC said it would make a new version and redistribute it. (source)

So 466 people have been tested with potentially flawed tests. Countless people have been untested simply because they haven’t traveled to certain countries or knowingly been in contact with someone who has traveled to certain countries.

In comparison, New York Magazine reports that more than 7,100 coronavirus tests have been conducted in the UK, South Korea has tested more than 30,000 people in “drive-thru” testing facilities, and the province of Ontario, Canada has tested 629 people. All of these places have far lower populations than the United States but they’ve tested a lot more people.

We were all upset when we learned China was testing so few people and fudging the cause of death of others. But here we are, also testing very few people.

What about all those people being “monitored?”

You’ve probably seen that thousands of people across the country are being “monitored” by health departments. Unfortunately, that monitoring doesn’t mean that they’re being tested before they’re released from self-quarantine. It simply means the local health department is getting their temperatures and asking if they have symptoms.

So monitoring is mainly self-instituted and no testing is being done. Don’t be lulled into any sense of false security over “monitoring.” Actual monitoring would mean that the quarantined people would have to test negative to the virus before they were released from quarantine.

To be absolutely clear, those being “monitored” are basically staying home for a couple of weeks then going on their merry way, with no testing involved. And considering there have been instances of asymptomatic people spreading the virus, this is hardly comforting.

And now Vice President Pence has issued a gag order.

If the obfuscation above isn’t bad enough, now all statements from health officials must be cleared by Vice President Mike Pence, the unofficial Covid19 Czar, before they can be made public.

The vice president’s first move appeared to be aimed at preventing the kind of contradictory statements from White House officials and top government health officials that have plagued the administration’s response. Even during his news conference Wednesday, Trump rejected the assessment from a top health official that it was inevitable that the coronavirus would spread more broadly inside the United States.

Dr. Anthony Fauci, one of the country’s leading experts on viruses and the director of the National Institute of Allergy and Infections Diseases, told associates that the White House had instructed him not to say anything else without clearance. (source)

So not only is the US government restricted who can be tested, sending out faulty tests, and poorly managing the diagnostic process, they’re also filtering any further information the American people are allowed to get. All those warnings last week about how we could expect “severe disruptions” to our daily lives? The talk about potential quarantines and getting prepared to work and educate from home?

It looks like those may be the only warnings we get.

Remember how just weeks ago we were talking about the horrible dishonesty and subterfuge in China’s handling of the Covid19 outbreak? It kind of seems like deja vu but right here in America.

This goes right along with the Ebola crisis management playbook.

I’ve mentioned before about how the Ebola outbreak completely vanished from the news, and it looks like we’re watching exactly the same thing play out now with VP Pence in charge. Just a few days ago, I wrote:

The government prefers to “manage” the flow of information, as they did during the Ebola outbreak in 2014, when they instituted an outright blackout on information.

That information blackout was a little bit different, as it was aimed toward the media. In Cat Ellis’s book, The Wuhan Coronavirus Survival Manual, she wrote that the editors of mainstream media outlets were told by the President to stop reporting on it.

To counter the rising public tension, President Obama appointed Ron Klaine, a Fannie Mae lobbyist with no health care background at all as his Ebola Response Coordinator. Klaine was known in and around Washington DC as being a man who could circumnavigate government bureaucracy and regulations. The media referred to Klaine as Obama’s “Ebola Czar”.

Within weeks of Klaine’s appointment, the Associated Press released a statement that was sent to editors. There were to be no more stories on Ebola unless it is linked to a massive upset or delay. All stories about suspected cases disappeared from the mainstream television news coverage, although you could still find articles on their websites occasionally.

So, if it is a standard for governments to downplay the severity of an infectious disease in order to control public panic, it is reasonable to examine what we know and understand that the situation is likely worse than it appears to be. (source)

Heaven knows, President Trump isn’t exactly popular with the media, which explains why the tactic this time is different and aimed at people who answer directly to the government. The tactic may be different but the strategy itself is the same.

In his recent press conference about the coronavirus, the President repeatedly compared Covid19 to the flu, when the two viruses are hardly comparable. He downplayed concerns and recommended more handwashing (which, while good advice, is hardly sufficient for an illness that is so highly contagious.)

Why would the government hide the severity of Covid19?

Of course, any government would want to avoid a panic. When people panic, things can devolve very quickly as Selco has warned. But is that the only reason they’re downplaying the spread of the virus?

As with most things when powerful people are involved, we can probably follow the money.

The market has been in a freefall and as Michael Snyder writes, it’s doing things we’ve never seen before, including yesterday’s plummet that was “the largest single-day point decline in all of U.S. history.”

Without a doubt, stocks could potentially fall a long, long way. Thanks to a tremendous rally earlier this year, stock prices were pushed to the most overvalued levels that we have ever seen. It was inevitable that prices would fall, and this coronavirus outbreak looks like it could greatly accelerate that process.

Meanwhile, analysts are increasingly coming to the realization that this virus is going to have very serious implications for the entire global economy.

…Up until recently, Wall Street had been acting as if this was a temporary problem that would soon fade.

But now it has become clear that we will be battling this virus for many months to come.

And what happens if this crisis is like the Spanish Flu pandemic which lasted for three years? (source)

So perhaps the biggest reason for all the secrecy and lack of testing is economic.

Chief of Staff Mick Mulvaney had some outrageous suggestions when he spoke with reporters in an attempt to assuage fears about the administration’s handling of the Covid19 outbreak. Here are the key points he made.

White House chief of staff Mick Mulvaney on Friday suggested that Americans should ignore media reports about the coronavirus amid fears of the deadly disease spreading into the U.S.

Mulvaney claimed that the media has only started paying close attention to the coronavirus because “they think this is going to be what brings down the president.”

Mulvaney said he was asked by a reporter, “What are you going to do today to calm the markets?” “I’m like, ‘Really what I might do today [to] calm the markets is tell people turn their televisions off for 24 hours.’” (source)

And of course, the inevitable flu comparison.

“This is not Ebola … it’s not SARS, it’s not MERS,” Mulvaney said. “We sit there and watch the markets and there’s this huge panic and it’s like, why isn’t there this huge panic every single year over flu?” Mulvaney asked rhetorically. (source)

So, don’t worry. Just ignore the news. Keep going to work, spending money, and thinking happy thoughts.

Should we be concerned?

So, given that the President, the Vice President, and the White House Chief of Staff say this is no big deal, and that the CDC is hardly allowing the testing of anyone, should we still be concerned about the possibility of widespread illness and quarantines?

Personally, I’m even more concerned. Why would they go to such lengths to silence health officials? Why would testing and reporting be so shady?

If it gets to the point where information can no longer be hidden and a mandatory quarantine is announced, it’s going to be too late to get the food and supplies you need to hunker down for an indefinite period of time.

With the new gag order on health officials, don’t expect for a moment to get information of value before it’s too late to act on it.

I think we’re watching a desperate coverup to try and save the plummeting economy. I think there are likely to be far more infections in the United States than anybody knows about because so few people meet the criteria for testing. I think that is deliberate.

I do not trust the official numbers in the United States. Do you?

About Daisy

Daisy Luther is a coffee-swigging, globe-trotting blogger who writes about current events, preparedness, frugality, voluntaryism, and the pursuit of liberty on her website, The Organic Prepper. She is widely republished across alternative media and she curates all the most important news links on her aggregate site, PreppersDailyNews.com. Daisy is the best-selling author of 4 books and runs a small digital publishing company. You can find her on Facebook, Pinterest, and Twitter.

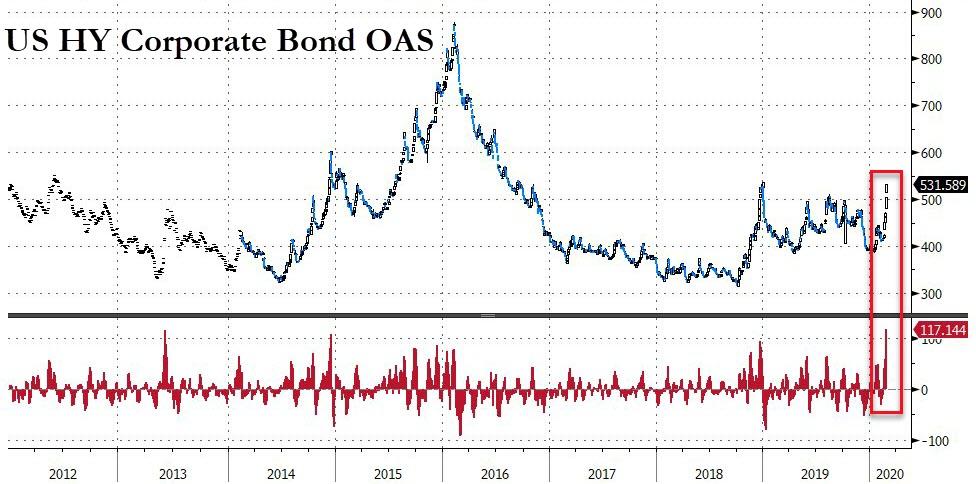

First Credit, Now The Corona-Crash Is Freezing Equity Market Issuance

On the heels of global credit markets grinding to a halt this week as the Covid-19 outbreak, it appears the freeze has spread to equity markets as Bloomberg reportsmore than $650 million in IPOs to be pulled from European capital markets.

As we detailed previously, high yield and investment-grade spreads have surged this week, illustrating the stress permeating underneath markets.

In fact, high yield spreads have widened +117bps in a matter of days, the biggest move since the financial crisis.

And now that chaotic chill is rolling over to the equity market, as Bloomberg notes DRI Healthcare was the second company in days to pull a new listing in Europe, citing deteriorating market conditions driven by virus fear.

“The company [ DRI Healthcare Plc] is seeking to raise as much as $350 million in London. Raising equity capital in Europe was already tricky because of a growing disconnect between buyers’ and sellers’ valuation expectations. Now the market’s slump is making investors even more averse to risk, thinning out an already depleted pipeline,” said Bloomberg.

DRI, a fund that invests in rights to royalty-paying pharmaceuticals, didn’t set a new date for its initial public offering, which had been planned for March 11.

Somewhat stunningly, only 10 companies have priced IPOs in Europe this year, including three in London, as raising equity capital in Europe was already tricky because of a growing disconnect between buyers’ and sellers’ valuation expectations, and now the surge in risk is keeping investors even further away.

“If the selloff continues into next week, no one will want to price with that level of weakness in the market,” said Marco Schwartz, head of KPMG’s equity capital markets advisory team.

“Our advice to companies about to launch offerings would be to hold off and wait.“

Sustainable Farmland Income Trust Plc was another company this week that pulled its $300 million planned listing on the London exchange, citing market turbulence.

The IPO of Wintershall DEA, an oil and gas firm, was also postponed and could wait until the second half of the year to list.

Nacon SA, a French maker of computer parts, managed to price a $128.2 million IPO this week, despite increasing volatility in global equity markets.

With central bankers seemingly impotent in the face of a health crisis (unable print vaccines and powerless to do anything that will help restart global supply chains or consumption), the sudden velocity of Covid-19’s effect on global markets has been nothing short of astonishing and while secondary trading markets are important, contagion spreading to the primary markets, freezing IPO and credit issuance this week is a significant problem.

Are you ready for this week’s absurdity? Here’s our Friday roll-up of the most ridiculous stories from around the world that are threats to your liberty, your finances, and your prosperity.

* * *

Man fined almost $7 million for painting his own property

In 2002, the owner of some dilapidated warehouses in New York City decided to make use of the property.

He hired an artist to decorate the warehouses with graffiti, and curate graffiti art from others. Soon it became a bustling art hub, with artists renting out space to do their work.

But after eleven years, the owner decided to demolish the warehouses to make way for luxury apartments.

That’s when the artists sued to protect ‘their’ graffiti.

But the owner of the property went ahead and whitewashed the artwork while the lawsuit was ongoing.

After years of legal battles, the court sided with the artists and demanded the owner pay $6.75 million to the artists whose work he destroyed. And now on appeal, another court affirmed that decision.

Turns out, you don’t have the same property rights when it comes to art.

New York has a Visual Artists Rights Act. It doesn’t matter who owns the art, or the building it’s affixed to. Artists still maintain certain rights to their work, even if it is sold (or they never owned the canvass).

So in New York, you better be careful who you let decorate your property. It may become their property.

Now California will refer to “at risk youth” instead as, “at promise youth.”

Legislation went into effect at the beginning of this year which changed the state’s legal term for children at risk of entering the criminal justice system.

The point is to change the negative connotation of the phrase “at risk”.

Uplifting, right? But these people always fail to understand that changing words doesn’t change reality.

Progessive parking tickets could make rich pay more

Boston Massachusetts tickets drivers as much as $40 for an expired parking meter.

Boston collected over $61 million worth of fines in 2018, the same year it began increasing parking fines. Now some parking tickets run up to $120.

But a new city councillor is concerned that some Boston residents may have to decide between paying a parking ticket, and putting food on the table.

She has introduced rules that would scale the cost of a parking ticket based on the violator’s income.

So rich people will still face huge fines for tiny infractions– maybe even higher than they are currently. But low-income folks will pay lower fines for parking illegally.

The proposal says, “for some a $40 parking ticket is simply the cost to park illegally while for others it is a major financial setback.”

So, as usual, the solution is to redistribute the wealth.

“From each according to his means,” to pay parking tickets, as Karl Marx would say.

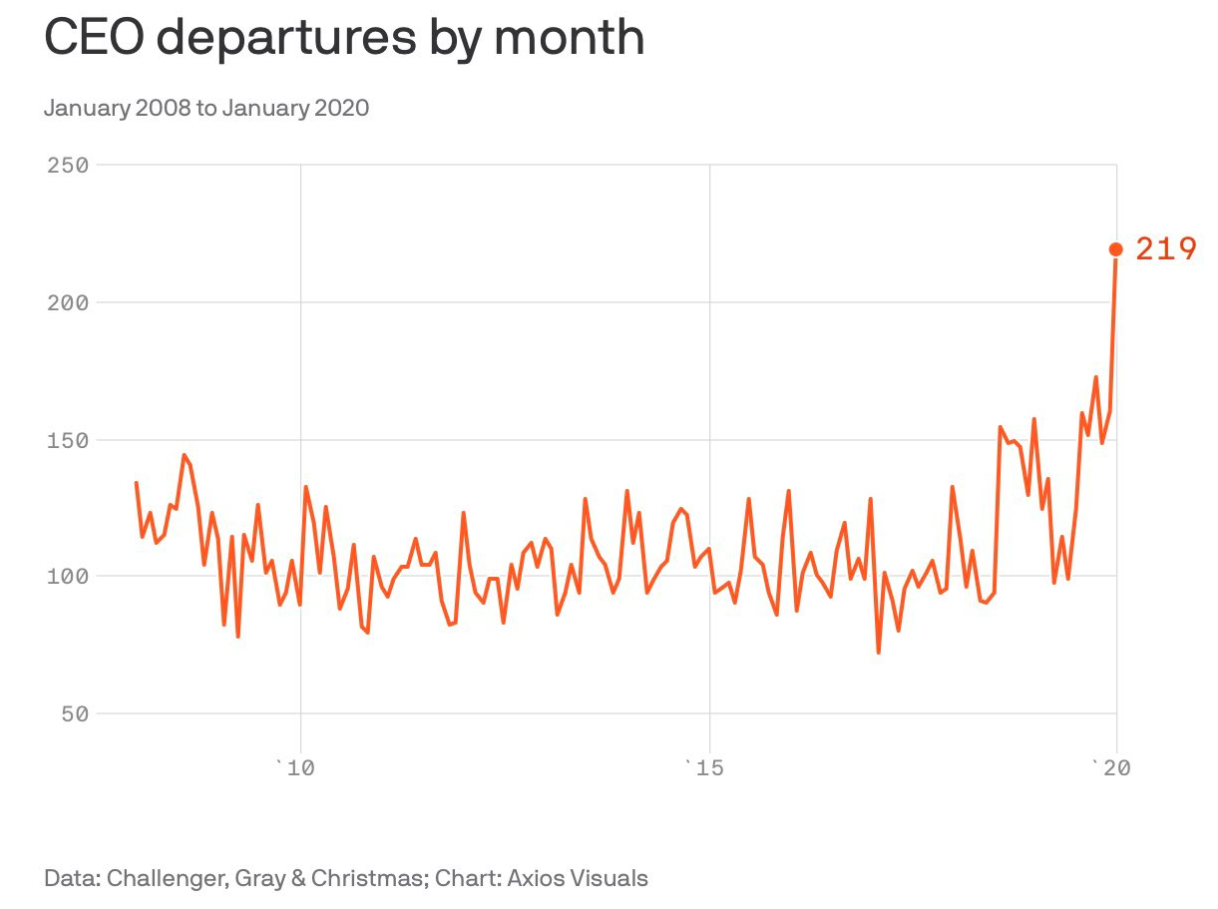

Calling The Top: Record Numbers Of CEOs Quit In January

CEO departures like that of Bob Iger from Disney have stunned the investing world recently. Iger said earlier this week that he was going to step down from his job after a decade and a half of success.

He was responsible for bringing Disney into the streaming era, creating Disney +, launching the company’s biggest theme park in Shangai and bringing ESPN to streaming, according to Axios.

Could Iger – and other CEOs like him – be sounding the alarm? While Iger claimed on Disney’s conference call that the “plans had been in the works for some time,” it is difficult not to notice the timing with which he – and other CEOs like him – have decided to call it quits.

In fact, their timing has been extraordinarily prescient. Every CEO that has announced their departure before the coronavirus pandemic that has taken a hold of the global markets may have just arguably exited at the best possible time. Since the beginning of January, $5 trillion has now been wiped off of markets worldwide.

And there’s plenty of reason to believe that the pain is going to continue.

219 CEOs have left their jobs in January, which is a 37% increase from December and 27% increase from the previous high, which was in October.

Even in December, the breakneck pace with which CEOs were leaving was highlighted by Axios, who noted that names like Patrick Byrne of Overstock, Kevin Plank of Under Armor and Adam Neumann of WeWork had all stepped down from their positions as Chief Executive Officer.

Additionally, the #MeToo movement claimed names like Steve Easterbrook of McDonald’s.

Since 1958 the S&P 500 has declined by +5% in a day some 22 times. In 82% of those events, stocks were already oversold. Outside the Financial Crisis, the average 3-month return after a crash is +8.5%, with only 1 significant (11%) drawdown. From the first 5% down day of the Financial Crisis (which had 12 5% days), 1-year returns were still essentially flat. Bottom line: markets right now are vulnerable to a crash. Be ready to at least stick a toe in the water if that happens.

* * *

“Markets don’t crash when they’re overbought… they crash when they’re already oversold.” I first heard that bit of wisdom in 2000 from a trader at SAC Capital who went by the name of “Spider”. Yes, he was a wiry sort of fellow, but his nom du guerre came from his adeptness at trading SPY.

Given current market conditions, we’ll dedicate Story Time Thursday to his quip and analyze both how true it is and whether we can make money buying crashes.

First, we need to define what a “Crash” even is and for that we’ll use 1-day return data for the S&P 500 back to its 1958 inception:

On average the S&P rises by 0.03% a day.

The standard deviation of those daily returns is 0.98%, which incidentally is why Jessica uses 1% days as our basic measure of US equity market volatility.

In the scientific community an observation of 5-standard deviations is one widely accepted benchmark of statistical robustness. It was, for example, the metric used to announce the discovery of the Higgs Boson particle.

That makes a 5% (4.89%, if you want to be precise) 1-day decline in the S&P a legitimately unusual observation, along with any 5% (4.95%) 1-day upside move.

This math explains why statistically minded investors think of equity returns as having “fat tails” rather than those defined by a normal distribution:

The odds of a 5-standard deviation move are about 1 in 3.5 million.

And yet, since 1958 (15,647 trading days) there have been a total of 39 days with +5% moves: 17 positive, and 22 negative.

The bottom line is that a 5% decline is a good definition of a “Crash”, so let’s look at all the instances where that has occurred and what was happening around/after those events:

#1: October 19 1987, a 20.5% decline:

US stocks had been on a tear from January – September 1987, up 33% YTD through the end of the month and hitting fresh all-time highs in the process.

The S&P 500 then hit a wall in October, declining by 12.2% from the 1st through 16th.

If you bought the close and held for 3 months you saw a 12.1% gain.

Conclusion: this is undoubtedly the source of the “crash from oversold” aphorism, and buying the drop netted a very good short-term return.

#2: September 2008 – January 2009:

During the depths of the Financial Crisis the S&P 500 had a +5% drop on 12 days, the largest cluster in the 1958 – present data.

The first instance was on September 29, 2008 with an 8.8% decline. Month-to-date returns prior to that day were -5.7% and -17.7% YTD.

So yes – that first “Crash” of the Financial Crisis came during already rough market conditions. But, unlike buying the close of the 1987 Crash, holding 3 months after the September 2008 crash delivered a -21.4% return. Holding for a year did get you to essentially break even (-4% price return, +3% dividend payout), however.

The reason for that disappointing “buy the crash return”: 11 other 5% crashes over the next 4 months. The last one wasn’t until January 20, 2009.

Conclusion: crashes can cluster, and it can take a year (and a lot of volatility) to recoup a “buy the crash” purchase.

#3: Finally, here is a list of the other 9 crashes back to 1958 and the details around them:

October 26, 1987: -8.3%, from obviously still oversold conditions post Black Monday. The 3-month future return from the close was +9.6%.

October 27, 1997: -6.9%, NOT in a clearly oversold market since the S&P was only down 0.6% MTD. The 3-month future return: +10.5%.

August 31, 1998: -6.8%, from an oversold S&P 500 down 8.3% MTD. The 3-month future return: +21.6%.

January 8, 1988: -6.8%, but NOT from clearly oversold conditions (MTD +4.8%, 1-month +12.3%). The 3-month future return: +9.4%.

May 28, 1962: -6.7%, from an oversold market down 7.1% MTD. The 3-month future return: +5.9%.

August 8, 2011: -6.7%, from clearly oversold conditions (-7.2% MTD, 1-month -10.4%). The 3-month future return: +14.0%.

October 13, 1989: -6.1%, NOT from an already oversold market (+1.8% MTD, 1-month +1.9%). The 3-month future return: +1.0%.

April 14, 2000: -5.8%, from a market JUST entering oversold from the start of the dot com bubble bursting (-3.8% MTD, but 1-month +6.0%). The 3-month future return: +11.3%.

October 16, 1987: -5.2%, from oversold conditions as noted in Point #1 above. Because of Black Monday, the forward 3-month return from this close was -10.8%.

Now, let’s aggregate this data and draw some conclusions:

In 18 of the 22 cases here (82%), the S&P 500 did drop by 5% in a day (our “Crash” definition) after already experiencing significant losses.

Trading myth confirmed: markets crash when already under significant duress.

Outside of the 2008 – 2009 Financial Crisis, if you bought the close of a down 5% day you made an average of 8.46% over the next 3 calendar months with 90% of those instances yielding positive returns. The only exception, but still notable, was October 16th 1987.

Looking just at the 2008 – 2009 experience, buying the first down 5% move on September 29th was not a great idea, but if you had the fortitude to stick with it you were at least whole in a year.

So, let’s move this discussion to the present day: what if we get a 5% crash day as a result of concerns about COVID-19’s effect on the global economy? Two final thoughts:

History says buy that close and the data is crystal clear on that point. Crashes are opportunities to make solid 3-month returns with little risk of further cataclysmic drawdowns.

If you think COVID-19 bears closer resemblance to the 2008 Financial Crisis than a “garden variety” crash, then history says to buy the first down 5% close in small size and wait for more to add to positions.

Bottom line: we’re going into a Friday-Monday sequence that will remind many old hands of 1987 and 2008 – 2009, so let’s be prepared for the possibility of a down 5% day and stay clear headed about what to do next.

Misinformation about COVID-19, a type of coronavirus, is spreading almost as fast as the virus itself—and that’s really saying something, considering that an estimated 80,000 people worldwide are now infected.

Here’s a quick look at some of the fake news that’s circulating like a worrisome sneeze on a crowded airliner.

No, the CDC’s Budget Hasn’t Been Cut

During Tuesday’s Democratic primary debate, several candidates—including former Vice President Joe Biden, former New York City Mayor Michael Bloomberg, and Sen. Elizabeth Warren (D–Mass.)—accused the Trump administration of cutting key funding from the Centers for Disease Control (CDC) that impaired America’s readiness for a pandemic.

There is plenty to critique about the way the Trump administration has handled the outbreak so far (Mike Pence as virus czar? Really?), but this attack is inaccurate. Trump has proposed budget cuts for the CDC in each of his budgets since taking office, but Congress never approved those proposals. Trump’s most recent budget plan calls for a 16 percent cut to the CDC, but that budget has yet to be approved by Congress. It’s fair to say Trump has tried to defund the CDC, but it’s inaccurate to say that he has succeeded—or that those fictitious cuts have affected the agency’s ability to respond to COVID-19.

When Trump was asked about those budget cuts, and about his firing of some top CDC officials, at Wednesday’s press briefing on the virus, he offered a pretty good defense. “I’m a businessperson. I don’t like having thousands of people around when you don’t need them,” said Trump. “When we need them, we can get them back very quickly.”

Indeed, that’s a good way for the government to operate.

No, Corona Beer Is Not Responsible for the Virus (and Most People Know That).

It seems insane to have to point this out but, incredibly, some people seem incapable of distinguishing a deadly respiratory illness that emerged in China from the golden-hued Mexican beer of the same name.

Citing a consumer survey from 5W Public Relations, CNN reported on Friday that 38 percent of Americans wouldn’t buy Corona “under any circumstances” because of the outbreak. Constellation Brands, the conglomerate that owns Corona, has seen its stock fall by more than 8 percent since the outbreak of the coronavirus.

But most Americans are smart enough to tell the difference. What the survey actually says is that only four percent of beer-drinkers wouldn’t buy Corona because of the outbreak. The 38 percent figure reported by CNN is the number of people who say they wouldn’t buy Corona for any reason.

The survey, it turns, out, does not say this!

What it says: -38% of beer drinkers say they wouldn't buy Corona (for any reason at all, including, presumably…they prefer other beer) -4% of people who usually drink Corona say they would stophttps://t.co/X4Wa6tLR3zhttps://t.co/r37un3LRSG

C’mon, CNN. The network that’s supposed to be “the most trusted name in news” also gets the blame for misleading readers into thinking they could fight the coronavirus with a razor. This chart, which CNN misleadingly said the CDC was publishing for “coronavirus safety” shows which types of facial hair can be fitted under respirator masks. Other outlets, including the New York Post, picked up the story as well.

Except that chart was created by the CDC as guidance for doctors participating in “No-Shave November,” a prostate cancer awareness campaign. It was not a guide for preventing the spread of the coronavirus.

Don't shave because of the coronavirus. We talked to the CDC today and they said this graphic was for No Shave November, not the virus outbreak. pic.twitter.com/PTjLUBlRXo

No, There’s Not a Shortage of Medical Equipment in the U.S.

Is there any problem the Trump administration doesn’t believe can be solved with a centrally planned industrial policy? Probably, but the coronavirus isn’t it.

Reuters reported on Friday afternoon that the Trump administration “is considering invoking special powers through a law called the Defense Production Act to rapidly expand domestic manufacturing of protective masks and clothing to combat the coronavirus.” The law was originally passed in 1950 to ensure the U.S. could requisition necessary supplies.

The White House is reportedly considering this action because of fears that Chinese supply chains for protective masks and other medical equipment could be disrupted by the coronavirus’ spread. “Very little of this stuff is apparently made in the [United] States, so if we’re down to domestic capability to produce, it could get tough,” one unnamed official told Reuters.

But the Food and Drug Administration (FDA) says there is little evidence to suggest that those fears will come true.

“We are aware of 63 manufacturers which represent 72 facilities in China that produce essential medical devices; we have contacted all of them,” the agency said in a statement on Friday. “While the FDA continues to assess whether manufacturing disruptions will affect overall market availability of these products, there are currently no reported shortages for these types of medical devices within the U.S. market.”

When it comes to protective equipment like surgical gowns, gloves, masks, and respirators, the FDA protective devices, or other medical equipment designed to protect the wearer from injury or the spread of infection or illness—the FDA says it is “currently not aware of specific widespread shortages of medical devices.”

Circumstances could change, of course, but there does not seem to be any need for aggressive government action that will centralize more control in the hands of Washington bureaucrats. Even if only intended as a temporary measure, such things rarely disappear when crises pass.

And even if circumstances do change, it’s unlikely that your Corona beer will get you sick. Well, at least not this type of sick.

from Latest – Reason.com https://ift.tt/386jH0g

via IFTTT

Coronavirus Reappearing Weeks Later In Discharged Patients

An alarming number of coronavirus patients in China and around the world are testing positive after ‘recovering’ and being discharged from the hospital – with the disease reappearing weeks later in some cases, according to Reuters.

On Wednesday, Japan’s Osaka prefectural government revealed that a female tour-bus guide had tested positive for coronavirus for a second time – which comes on the heels of Chinese reports that discharged patients throughout the country were testing positive after their release from the hospital.

That said, China’s National Health Commission said on Friday that reinfected patients were not transmitting the disease to others. The two running theories is that COVID-19 is “biphasic” and lies dormant before reappearing, or that patients are not building sufficient antibodies to fight a new infection.

Experts say there are several ways discharged patients could fall ill with the virus again. Convalescing patients might not build up enough antibodies to develop immunity to SARS-CoV-2, and are being infected again. The virus also could be “biphasic”, meaning it lies dormant before creating new symptoms.

But some of the first cases of “reinfection” in China have been attributed to testing discrepancies.

On Feb. 21, a discharged patient in the southwestern Chinese city of Chengdu was readmitted 10 days after being discharged when a follow-up test came back positive. –Reuters

Deputy director of the infectious diseases center at the West China Hospital, Lei Xuezhong, told People’s Daily that hospitals had been using nose and throat samples to test patients, while new tests were finding the virus in the lower respiratory tract.

A study by the Journal of the American Medical Association which analyzed four infected medical personnel treated in Wuhan found that it was likely that some recovered patients would remain carriers even after meeting discharge criteria.

In China, for instance, patients must test negative, show no symptoms and have no abnormalities on X-rays before they are discharged.

Allen Cheng, professor of infectious diseases epidemiology at Monash University in Melbourne, said it wasn’t clear whether the patients were re-infected or had remained “persistently positive” after their symptoms disappeared. But he said the details of the Japan case suggested the patient had been reinfected.

Song Tie, vice director of the local disease control center in southern China’s Guangdong province, told a media briefing on Wednesday that as many as 14% of discharged patients in the province have tested positive again and had returned to hospitals for observation.

He said one good sign is that none of those patients appear to have infected anyone else.

“From this understanding … after someone has been infected by this kind of virus, he will produce antibodies, and after these antibodies are produced, he won’t be contagious,” he said. –Reuters

Meanwhile, a “low level” of the virus was found in the pet dog of a patient in Hong Kong, throwing a “weak positive” when tested.

Typically patients will develop specific antibodies which will protect them from reinfection, however this does not appear to be the case with a certain percentage of coronavirus patients, similar to HIV.

“In most cases though, because their body has developed an immune response to the first infection, the second infection is usually less severe,” said Adam Kamradt-Scott, an infectious diseases specialist at the University of Sydney.

Other experts have suggested that the disease may even feature “antibody-dependent enhancement,” meaning that exposure to viruses could make patients more at risk of further infections and worse symptoms.

This confirms a report from several weeks ago from the Taiwan Times that reinfection may be deadlier than the initial infection in some patients, causing sudden death from heart failure in several instances.

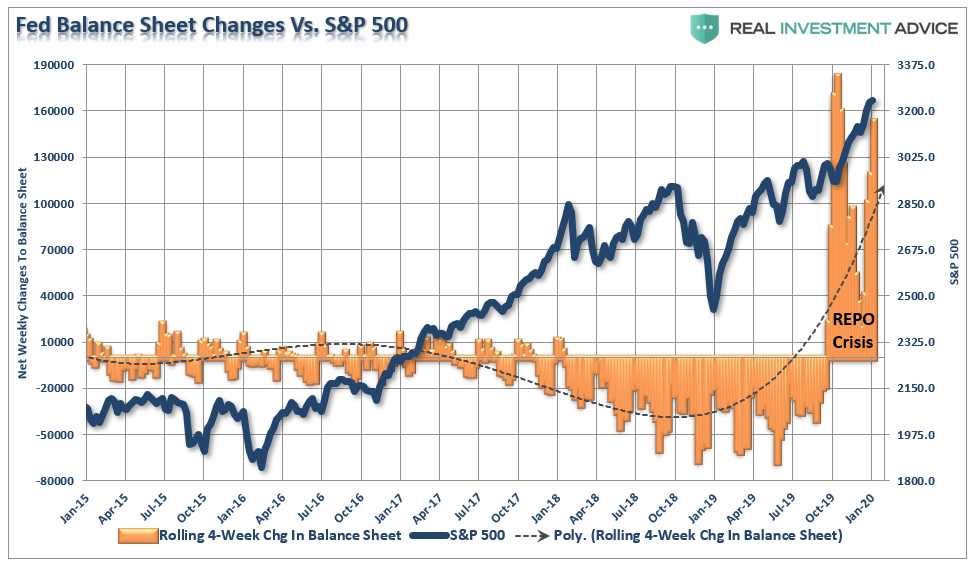

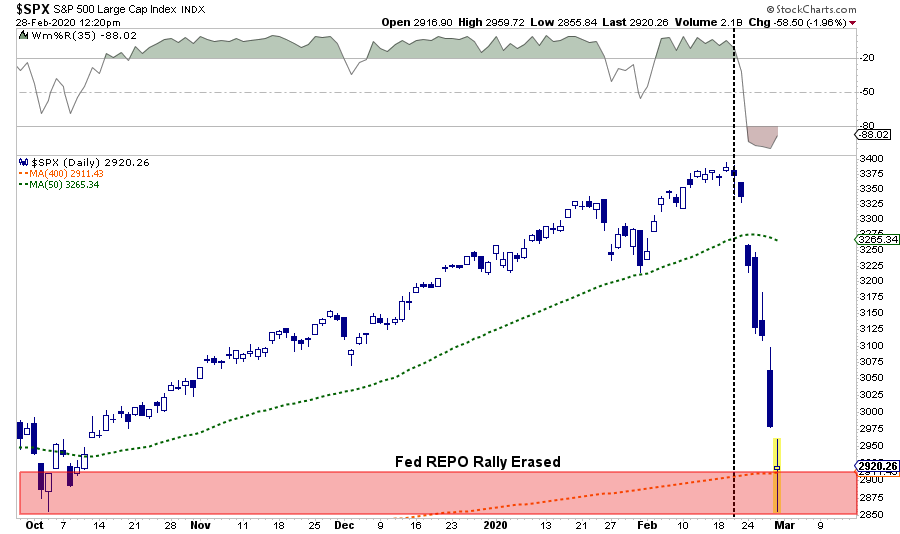

On Jan 3rd, I wrote an article entitled: “Will The Market Repeat The Start Of 2018?”At that time, the Federal Reserve was dumping a tremendous amount of money into the financial markets through their “Repo” operations. To wit:

“Don’t fight the Fed. That is the current mantra of the market as we begin 2020, and it certainly seems to be the right call. Over the last few months, the Federal Reserve has continued its “QE-Not QE” operations, which has dramatically expanded its balance sheet. Many argue, rightly, the current monetary interventions by the Fed are technically “Not QE” because they are purchasing Treasury Bills rather than longer-term Treasury Notes.

However, ‘Mr. Market’ doesn’t see it that way. As the old saying goes, ‘if it looks, walks, and quacks like a duck…it’s a duck.’”

As I noted then, despite commentary to the contrary, there were only two conclusions to draw from the data:

There is something functionally “broken” in the financial system which is requiring massive injections of liquidity to try and rectify, and;

The surge in liquidity, whether you want to call it a “duck,” or not, is finding its way into the equity markets.

Let me remind you this was all BEFORE the outbreak of the Coronavirus.

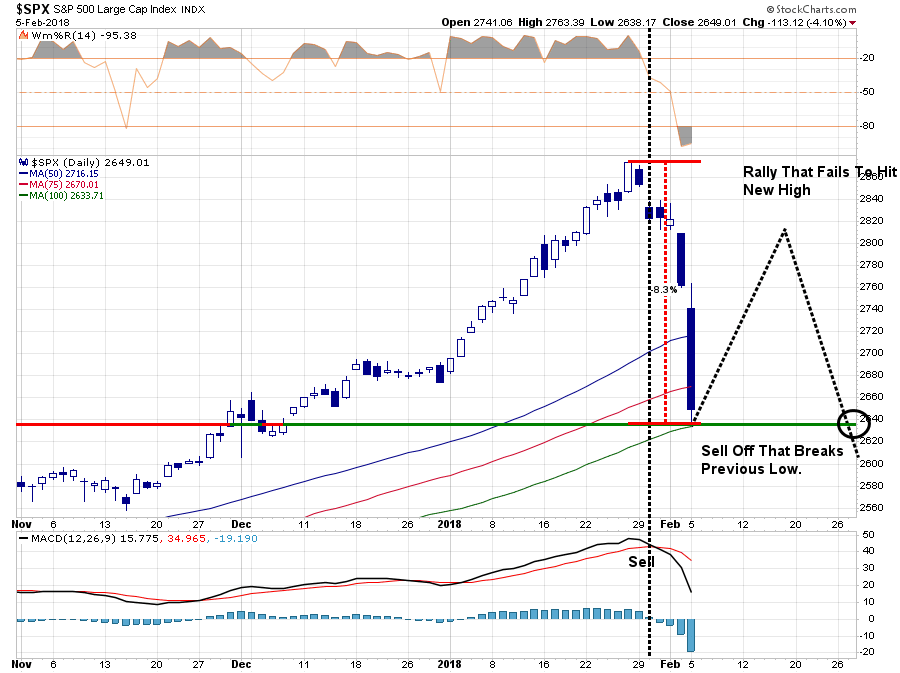

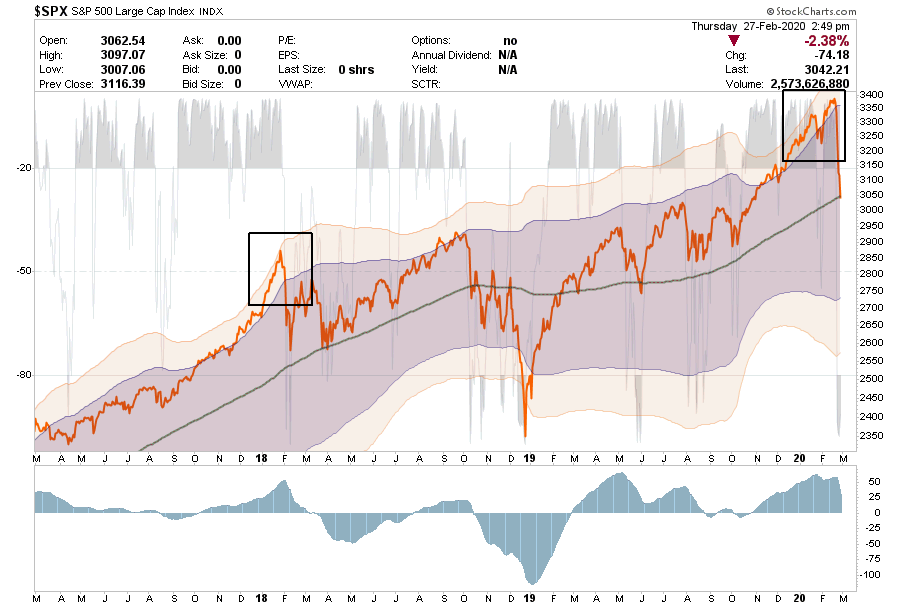

The Ghosts Of 2018

“Well, this past week, the market tripped ‘over its own feet’ after prices had created a massive extension above the 50-dma as shown below. As I have previously warned, since that extension was so large, a correction just back to the moving average at this point will require nearly a -6% decline.”

‘The problem is that it has been so long since investors have even seen a 2-3% correction, a correction of 5%, or more, will ‘feel’ much worse than it actually is,which will lead to ’emotionally driven’ mistakes.’

The question now, of course, is do you “buy the dip” or ‘run for the hills?’”

Yesterday morning, the markets began the day deeply in the red, but by mid-morning were flirting with a push into positive territory. By the end of the day, the Dow had posted its largest one-day point loss in history.”

Besides the reality that the only thing that has occurred has been a reversal of the Fed’s “Repo” rally, there is a striking similarity to 2018. That got me to thinking about the corollary between the two periods, and how this might play out over the rest of 2020.

Let’s go back.

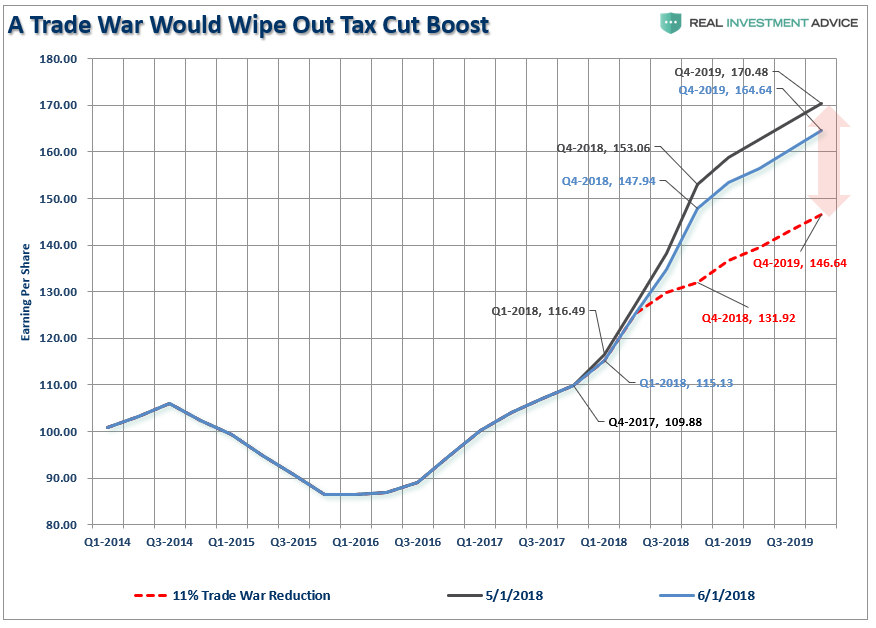

Heading in 2018, the markets were ebullient over President Trump’s recently passed tax reform and rate cut package. Expectations were that 2018 would see a massive surge in earnings growth, due to the lower tax rates, and there would be a sharp pickup in economic growth.

However, at the end of January, President Trump shocked the markets with his “Trade War” on China and the imposition of tariffs on a wide variety of products, which potentially impacted American companies. As we said at the time, there was likely to be unintended consequences and would kill the effect of tax reform.)

“While many have believed a ‘trade war’ will be resolved without consequence, there are two very important points that most of the mainstream analysis is overlooking. For investors, a trade war would likely negatively impact earnings and profitability while slowing economic growth through higher costs.”

Over the next few months, the market dealt, and came to terms with, the trade war and the Fed’s tightening of the balance sheet. As we discussed in May 2018, the trade war did wind up clipping earnings estimates to a large degree, but massive share repurchases helped buoy asset prices.

Then in September, the Fed did the unthinkable.

After having hiked rates previously, thereby tightening the monetary supply, they stated that monetary policy was not “close to the neutral rate,” suggesting more rate hikes were coming. The realization the Fed was intent on continuing to tighten policy, and further extracting liquidity by reducing their balance sheet, sent asset prices plunging 20% from the peak, to the lows on Christmas Eve.

It was then the Fed acquiesced to pressure from the White House and began to quickly reverse their stance and starting pumping liquidity back into the markets.

And the bull market was back.

Fast forward to 2020.

“The exuberance that surrounded the markets going into the end of last year, as fund managers ramped up allocations for end of the year reporting, spilled over into the start of the new with S&P hitting new record highs.

Of course, this is just a continuation of the advance that has been ongoing since the Trump election. The difference this time is the extreme push into 3-standard deviation territory above the moving average, which is concerning.” – Real Investment Report Jan, 5th 2018

As noted in the chart below, in both instances, the market reached 3-standard deviations above the 200-dma before mean-reverting.

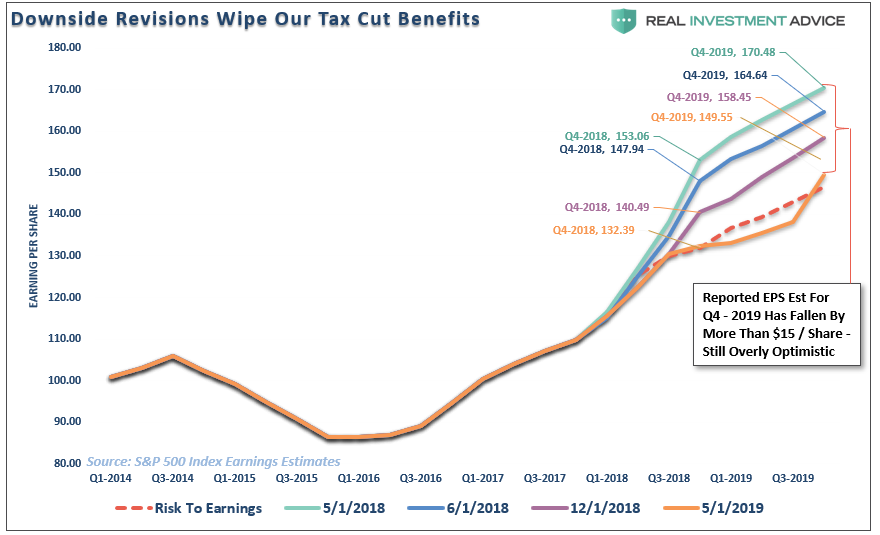

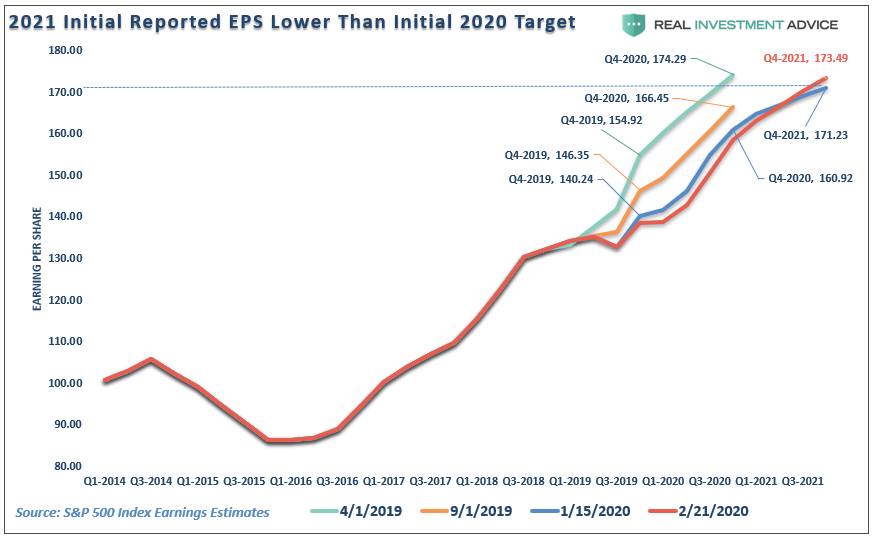

Of course, while everyone was exuberant over the Fed’s injections of monetary support, we were discussing the continuing decline in earnings growth estimates, along with the lack of corporate profit growth. To wit:

With equities now more than 30% higher than they were then, the Fed mostly on hold in terms of rate cuts, and ‘repo’ operations starting to slow, it certainly seems that expectations for substantially higher market values may be a bit optimistic.

Furthermore, as noted above, earnings expectations declined for the entirety of 2019, as shown in the chart below. However, the impact of the ‘coronavirus’ has not been adopted into these reduced estimates as of yet.These estimates WILL fall, and likely markedly so, which, as stated above, is going to make justifying record asset prices more problematic.”

Just as the “Trade War” shocked the markets and caused a repricing of assets in 2018, the “coronavirus” has finally infected the markets enough to cause investors to adjust their expectations for earnings growth. Importantly, as in 2018, earnings estimates have not been revised lower nearly enough to compensate for the global supply chain impact coming from the virus.

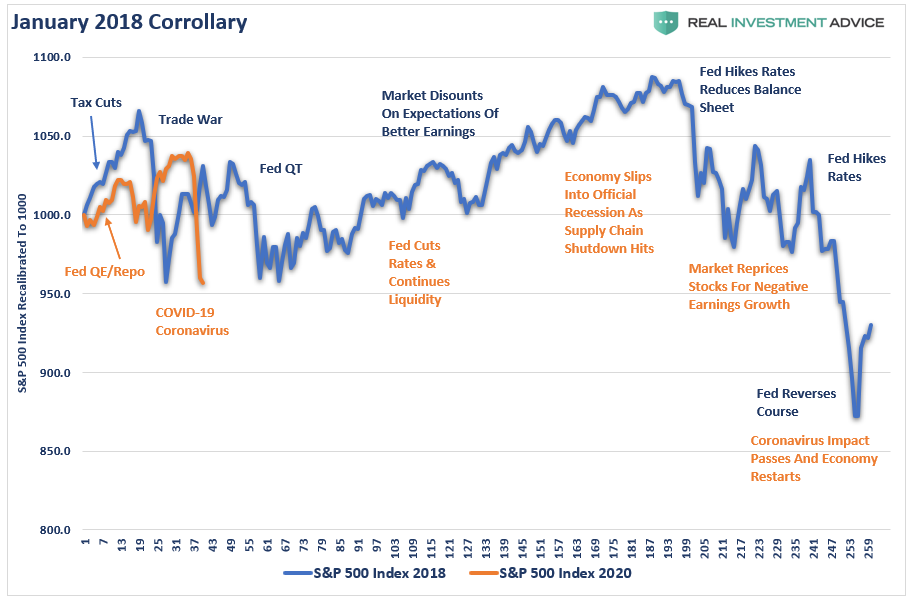

While the beginning of 2020 is playing out much like 2018, what about the rest of the year?

There are issues occurring which we believe will have a very similar “feel” to 2018, as the impact of the virus continues to ebb and flow through the economy. The chart below shows the S&P 500 re-scaled to 1000 for comparative purposes.

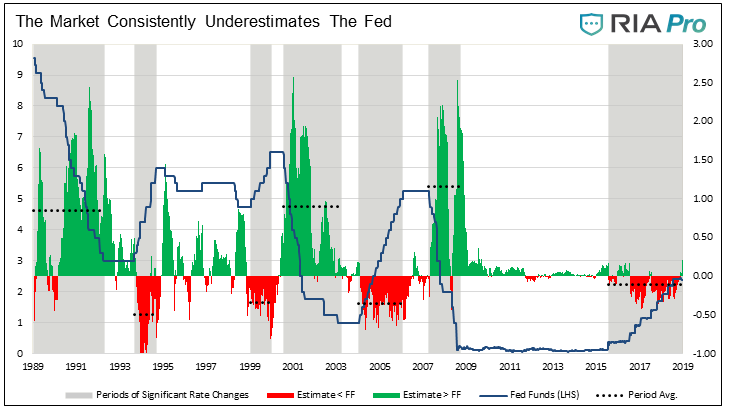

Currently, the expectation has risen to more than a 70% probability the Fed will cut rates 3x in 2020. Historically, the market tends to underestimate just how far the Fed will go as noted by Michael Lebowitz previously:

“The graph below tracks the comparative differentials (Fed Funds vs. Fed Fund futures) using the methodology outlined above. The gray rectangular areas represent periods where the Fed was systematically raising or lowering the Fed funds rate (blue line). The difference between Fed Funds and the futures contracts, colored green or red, calculates how much the market over (green) or under (red) estimated what the Fed Funds rate would ultimately be. In this analysis, the term overestimate means Fed Funds futures thought Fed Funds would be higher than it ultimately was. The term underestimate, means the market expectations were lower than what actually transpired.”

Our guess is that in the next few weeks, the Fed will start using “forward guidance” to try and stabilize the market. Rate cuts, and more “quantitative easing,” will likely follow.

Such actions should stabilize the market in the near-term as investors, who have been pre-conditioned to “buy” Fed liquidity, will once again run back into markets. This could very well lift the markets into second quarter of this year.

But it will likely be a “trap.”

While monetary policy will likely embolden the bulls short-term, it does little to offset an economic shock. As we move further into the year, the impact to the global supply chain will begin to work its way through the system resulting in slower economic growth, reduced corporate profitability, and potentially a recession. (See yesterday’s commentary)

This is a guess. There is a huge array of potential outcomes, and trying to predict the future tends to be a pointless exercise. However, it is the thought process that helps align expectations with potential outcomes to adjust for risk accordingly.

A Sellable Rally

Just as in February 2018, following the sharp decline, the market rallied back to a lower high before failing once again. For several reasons, we suspect we will see the same over the next week or two, as the push into extreme pessimism and oversold conditions will need to be reversed before the correction can continue.

While 2019 ended in an entirely dissimilar manner as compared to 2018, the current negative sentiment, as shown by CNN’s Fear & Greed Index is back to the extreme fear levels seen at the lows of the market in 2018.

On a short-term technical basis, the market is now extremely oversold, which is suggestive of a counter-trend rally over the next few days to a week or so.

It is highly advisable to use ANY reflexive rally to reduce portfolio risk, and rebalance portfolios. Most likely, another wave of selling will likely ensue before a stronger bottom is finally put into place.

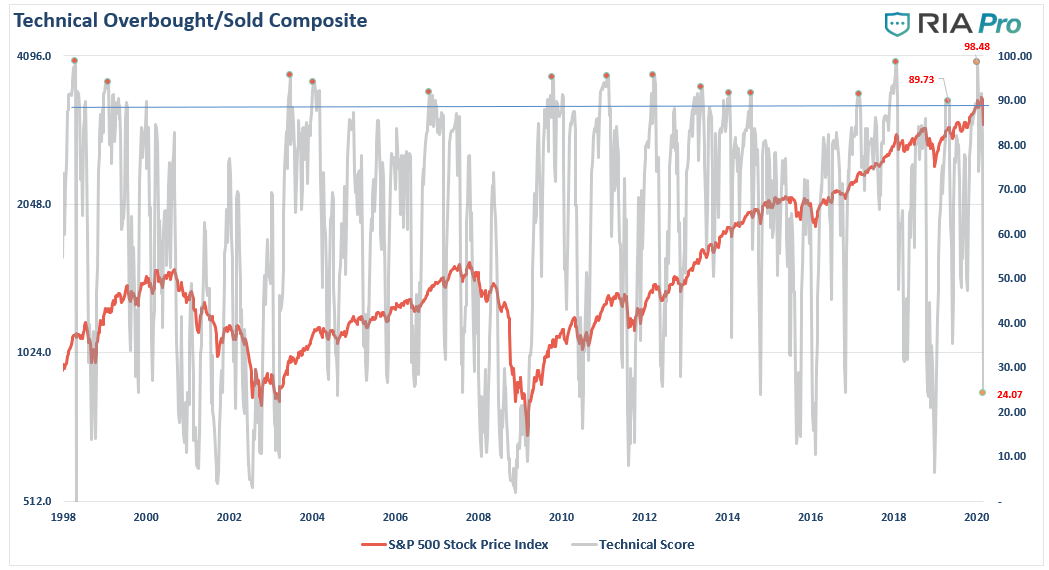

Lastly, our composite technical overbought/oversold gauge is also pushing more extreme oversold conditions, which are typical of a short-term oversold condition.

In other words, in 2019 “everyone was in the pool,” in 2020 we just found out “everyone was swimming naked.”

Rules To Follow

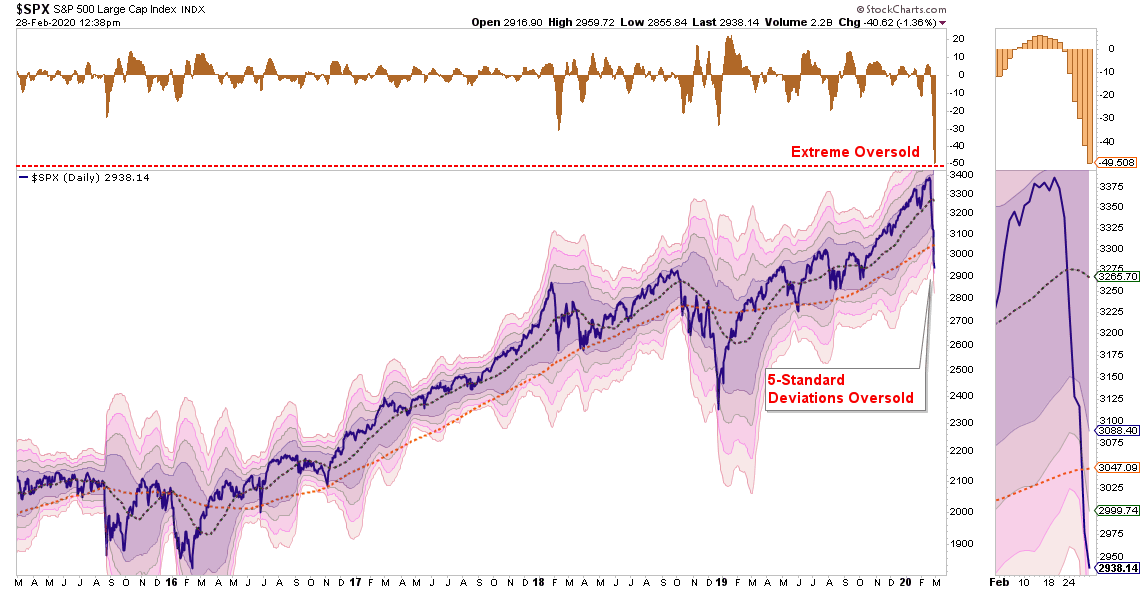

One last chart.

I just want you to pay attention to the top panel and the shaded areas. (standard deviations from the 50-dma)

We were not this oversold even during the 2015-2016 decline, much less the two declines in 2018.

Currently, not only is the market extremely oversold on a short-term basis, but is currently 5-standard deviations below the 50-dma.

Let me put that into perspective for you.

1-standard deviation = 68.26% of all possible price movement.

2-standard deviations = 95.45%

3-standard deviations = 99.73%

4-standard deviations = 99.993%

5-standard deviations = 99.9999%

Mathematically speaking, the bulk of the decline is already priced into the market.

“I get it. We are gonna get a bounce. So, what do I do?”

I am glad you asked.

Step 1) Clean Up Your Portfolio

Tighten up stop-loss levels to current support levels for each position.

Take profits in positions that have outperformed during the rally.

Sell laggards and losers (those that lagged the rally, probably led the decline)

Raise cash, and rebalance portfolios to reduced risk levels for now.

Step 2) Compare Your Portfolio Allocation To Your Model Allocation.

Determine areas where exposure needs to be increased, or decreased (bonds, cash, equities)

Determine how many shares need to be bought or sold to rebalance allocation requirements.

Determine cash requirements for hedging purposes

Re-examine the portfolio to ensure allocations are adjusted for FORWARD market risk.

Determine target price levels for each position.

Determine “stop loss” levels for each position being maintained.

Step 3) Be Ready To Execute

Whatever bounce we get will likely be short-lived. So have your game plan together before-hand as the opportunity to rebalance risk will likely not be available for very long.

This is just how we do it.

However, there are many ways to manage risk, and portfolios, which are all fine. What separates success and failure is 1) having a strategy to begin with, and; 2) the discipline to adhere to it.

The recent market spasm certainly reminds of 2018. And, if we are right, it will get better, before it gets worse.

Misinformation about COVID-19, a type of coronavirus, is spreading almost as fast as the virus itself—and that’s really saying something, considering that an estimated 80,000 people worldwide are now infected.

Here’s a quick look at some of the fake news that’s circulating like a worrisome sneeze on a crowded airliner.

No, the CDC’s Budget Hasn’t Been Cut

During Tuesday’s Democratic primary debate, several candidates—including former Vice President Joe Biden, former New York City Mayor Michael Bloomberg, and Sen. Elizabeth Warren (D–Mass.)—accused the Trump administration of cutting key funding from the Centers for Disease Control (CDC) that impaired America’s readiness for a pandemic.

There is plenty to critique about the way the Trump administration has handled the outbreak so far (Mike Pence as virus czar? Really?), but this attack is inaccurate. Trump has proposed budget cuts for the CDC in each of his budgets since taking office, but Congress never approved those proposals. Trump’s most recent budget plan calls for a 16 percent cut to the CDC, but that budget has yet to be approved by Congress. It’s fair to say Trump has tried to defund the CDC, but it’s inaccurate to say that he has succeeded—or that those fictitious cuts have affected the agency’s ability to respond to COVID-19.

When Trump was asked about those budget cuts, and about his firing of some top CDC officials, at Wednesday’s press briefing on the virus, he offered a pretty good defense. “I’m a businessperson. I don’t like having thousands of people around when you don’t need them,” said Trump. “When we need them, we can get them back very quickly.”

Indeed, that’s a good way for the government to operate.

No, Corona Beer Is Not Responsible for the Virus (and Most People Know That).

It seems insane to have to point this out but, incredibly, some people seem incapable of distinguishing a deadly respiratory illness that emerged in China from the golden-hued Mexican beer of the same name.

Citing a consumer survey from 5W Public Relations, CNN reported on Friday that 38 percent of Americans wouldn’t buy Corona “under any circumstances” because of the outbreak. Constellation Brands, the conglomerate that owns Corona, has seen its stock fall by more than 8 percent since the outbreak of the coronavirus.

But most Americans are smart enough to tell the difference. What the survey actually says is that only four percent of beer-drinkers wouldn’t buy Corona because of the outbreak. The 38 percent figure reported by CNN is the number of people who say they wouldn’t buy Corona for any reason.

The survey, it turns, out, does not say this!

What it says: -38% of beer drinkers say they wouldn't buy Corona (for any reason at all, including, presumably…they prefer other beer) -4% of people who usually drink Corona say they would stophttps://t.co/X4Wa6tLR3zhttps://t.co/r37un3LRSG

C’mon, CNN. The network that’s supposed to be “the most trusted name in news” also gets the blame for misleading readers into thinking they could fight the coronavirus with a razor. This chart, which CNN misleadingly said the CDC was publishing for “coronavirus safety” shows which types of facial hair can be fitted under respirator masks. Other outlets, including the New York Post, picked up the story as well.

Except that chart was created by the CDC as guidance for doctors participating in “No-Shave November,” a prostate cancer awareness campaign. It was not a guide for preventing the spread of the coronavirus.

Don't shave because of the coronavirus. We talked to the CDC today and they said this graphic was for No Shave November, not the virus outbreak. pic.twitter.com/PTjLUBlRXo

No, There’s Not a Shortage of Medical Equipment in the U.S.

Is there any problem the Trump administration doesn’t believe can be solved with a centrally planned industrial policy? Probably, but the coronavirus isn’t it.

Reuters reported on Friday afternoon that the Trump administration “is considering invoking special powers through a law called the Defense Production Act to rapidly expand domestic manufacturing of protective masks and clothing to combat the coronavirus.” The law was originally passed in 1950 to ensure the U.S. could requisition necessary supplies.

The White House is reportedly considering this action because of fears that Chinese supply chains for protective masks and other medical equipment could be disrupted by the coronavirus’ spread. “Very little of this stuff is apparently made in the [United] States, so if we’re down to domestic capability to produce, it could get tough,” one unnamed official told Reuters.

But the Food and Drug Administration (FDA) says there is little evidence to suggest that those fears will come true.

“We are aware of 63 manufacturers which represent 72 facilities in China that produce essential medical devices; we have contacted all of them,” the agency said in a statement on Friday. “While the FDA continues to assess whether manufacturing disruptions will affect overall market availability of these products, there are currently no reported shortages for these types of medical devices within the U.S. market.”

When it comes to protective equipment like surgical gowns, gloves, masks, and respirators, the FDA protective devices, or other medical equipment designed to protect the wearer from injury or the spread of infection or illness—the FDA says it is “currently not aware of specific widespread shortages of medical devices.”

Circumstances could change, of course, but there does not seem to be any need for aggressive government action that will centralize more control in the hands of Washington bureaucrats. Even if only intended as a temporary measure, such things rarely disappear when crises pass.

And even if circumstances do change, it’s unlikely that your Corona beer will get you sick. Well, at least not this type of sick.

from Latest – Reason.com https://ift.tt/386jH0g

via IFTTT