From Commonwealth v. Mueller, decided Wednesday by a Pennsylvania Superior Court appellate panel:

On June 8, 2018, police conducted a traffic stop in Brookhaven Borough. During the course of the stop, Appellant, who was a bystander and not involved with the traffic stop, approached the scene. Appellant stood over the vehicle’s occupants, and Officer Hughes asked her to step back. Appellant refused to comply. Officer Hughes asked Appellant to step away from the immediate area, and he told her that she could observe from across the street. Officer Barth arrived, spoke with Appellant, and asked her to move.

Appellant began to videotape the scene with her cell phone and refused to move. Officer Barth threatened to arrest Appellant if she did not move, and Appellant moved into the intersection and obstructed traffic. Officer Barth asked Appellant to move again.

Appellant said: “This is fucking ridiculous.” Appellant subsequently walked away and went to work. The police issued a citation, charging Appellant with disorderly conduct at Section 5503(a)(3) (uses obscene language or makes obscene gesture) [for which Appellant was convicted and (a)(4) (creates hazardous or physically offensive condition by any act which serves no legitimate purpose) [for which she was acquitted]

A person is guilty of disorderly conduct under Section 5503(a)(3) if, “with intent to cause public inconvenience, annoyance or alarm, or recklessly creating a risk thereof, [she]…uses obscene language, or makes an obscene gesture.” Where a person uses profane language or other “angry words” that are not used to describe an act of sex or to appeal to anyone’s prurient interest, this Court has found insufficient evidence to sustain a conviction under Section 5503(a)(3). See, e.g., Pennix, supra (reversing conviction under subsection (a)(3) where appellant became agitated during search of her book bag in courthouse and screamed: “Fuck you I ain’t got time for this,” “Fuck you police” and “I don’t got time for you fucking police”; while appellant’s words were disrespectful, insulting and offensive, they were not “obscene” within meaning of Section 5503(a)(3)); Commonwealth v. McCoy, 69 A.3d 658 (Pa.Super. 2013), appeal denied, 623 Pa. 761, 83 A.3d 414 (2014) (reversing conviction under subsection (a)(3) where appellant shouted “fuck the police” multiple times during funeral procession for police officer; record showed no evidence that appellant’s chant was intended to appeal to anyone’s prurient interest or to describe sexual conduct in patently offensive way).

Instantly, the record shows Appellant uttered “this is fucking ridiculous,” after police had repeatedly asked her to back away from the scene of a traffic stop. Nothing in the record indicates that Appellant intended to describe an act of sex or appeal to anyone’s prurient interest.

The Commonwealth agrees the evidence was insufficient to sustain the conviction under Section 5503(a)(3). Accordingly, we reverse Appellant’s conviction and vacate the judgment of sentence. {Due to our disposition, we do not have to consider Appellant’s challenge under the First Amendment.}

from Latest – Reason.com https://ift.tt/39oOYMl

via IFTTT

On Tuesday, March 3, at 10:00 a.m., the Supreme Court heard oral arguments in Seila Law v. LLC. That case considered the constitutionality of the CFPB’s structure. (I analyzed the arguments here.) At some time that same day (I am not sure the exact time), the Fifth Circuit decided CFPB v. American Check Cashing. This case also considered the constitutionality of the CFPB’s structure. I criticized that decision as an untimely amicus brief. The panel should have held the case in abeyance until the Supreme Court decided Seila.

Last week, sua sponte, the Fifth Circuit agreed to hear American Check Cashingen banc. The panel decision was vacated. I suspect the en banc court will simply wait to see what happens in Seila, and remand to the district court–effectively a circuit GVR.

The Fifth Circuit does not have a consistent approach to resolving issues that the Supreme Court has granted review on. Consider the following four examples:

1. Whole Woman’s Health v. Paxton, No. 17-51060 (5th Cir.)

This case considered Texas’s prohibition of “dismemberment abortions.” The panel (Stewart, Dennis, and Willett) heard oral arguments on November 5, 2018. Six months later, on March 13, 2019, the panel issued an order placing the case in abeyance:

This appeal will be held in abeyance pending the disposition in the Supreme Court of a forthcoming (presumably) petition for a writ of certiorari in June Medical Services, L.L.C. v. Gee. [FN1] Once the Supreme Court disposes of June Medical, either by denying the petition or by deciding the merits, this appeal will be returned to this panel for further proceedings.

[FN1] 1 905 F.3d 787 (5th Cir. [Sept. 26,] 2018); see also June Med. Servs., L.L.C. v. Gee, 139 S. Ct. 663, 663 (2019) (mem.) (granting a stay “pending the timely filing and disposition of a petition for a writ of certiorari”).

Let’s consider the chronology.

The Fifth Circuit decided June Medical v. Gee on September 26, 2018, before the dismemberment case was argued.

And on March 13, 2019, the panel held the dismemberment case in abeyance for June Medical.

A petition for certiorari was filed in June Medical in April 2019.

Cert was granted on October 4, 2019.

Did the panel act properly here? I can see two sides. Following the stay, it was very likely that the Supreme Court would grant certiorari. Indeed, the Supreme Court’s stay order specifically referred to the “timely filing” of a cert petition. The panel may have reasonably concluded that any ruling should wait till Justices resolve the dispute from Louisiana dispute. Otherwise, their decision would simply be GVR’d by the Supreme Court.

On the other hand, there will probably be an eighteen-month gap between oral arguments in the Fifth Circuit (November 2018) and a final SCOTUS decision (June 2020). At that point, the Fifth Circuit will probably require new briefing, and perhaps another round of oral argument. And Texas’s law will have been enjoined for nearly four years. There is a cost to waiting around till the Supreme Court decides a related case.

The court could have asked the parties to opine on whether abeyance was appropriate. Specifically, the question presented in June Medical is not perfectly aligned with the question in the dismemberment case. It is entirely possible June Medical could be resolved on some ground that doesn’t affect the question before the panel. In that case, the two-year wait will have been for naught. But the court here acted sua sponte.

In any event, the panel’s sua sponte decision here places American Cash Checking in a very poor light. An eighteen-month delay is debatable. The CFPB panel couldn’t even wait four months before issuing its decision.

2. Whole Woman’s Health v. Smith, No. 18-50730 (5th Cir.)

This case concerns Texas’s law that requires burial of fetal remains. On September 5, 2018, a district court judge declared the law unconstitutional. One year later to the date, the Fifth Circuit heard oral arguments on September 5, 2019. During the oral arguments, the court asked the parties whether abeyance would be proper, but there were no written filings on the subject. On October 7, 2009, three days after cert was granted in June Medical, the panel (Barksdale, Stewart, and Costa) issued an order:

On October 4, 2019, the Supreme Court granted two petitions for writ of certiorari in June Medical Services, L.L.C. v. Gee, 905 F.3d 787 (5th Cir. 2018). See Supreme Court Nos. 18-1323, 18-1460. This appeal will be held in abeyance pending the Supreme Court’s disposition of June Medical. See Whole Woman’s Health v. Paxton, Fifth Circuit No. 17-51060 (Order of March 13, 2019) (holding case in abeyance pending Supreme Court’s disposition in June Medical). After the Supreme Court decides June Medical, this appeal will be returned to this panel for further proceedings.

This post-certiorari order makes more sense than the pre-certiorari order in the dismemberment case. And the panel asked the parties about holding the case in abeyance. It would be ideal to allow for formal briefing on this issue. Again, it is possible that June Medical would not resolve the precise issue with fetal remains.

In any event, both Texas abortion cases were handled far better than the CFPB case. That panel failed to hold the case in abeyance after the precise question presented had already been argued.

Does the Fifth Circuit have a general rule that all abortion cases will be held in abeyance for June Medical? Nope. Two abortion cases from Mississippi were not held in abeyance at all.

3. Jackson Women’s Health Organization v. Dobbs, No. 18-60868 (5th Cir.)

This case considered Mississippi’s prohibition on abortion after fifteen weeks. The Fifth Circuit panel heard oral arguments on October 7, 2019 (Higginbotham, Dennis, and Ho). Three days earlier, certiorari had been granted in June Medical. One of the questions presented in the Louisiana case was whether third-party standing was permissible. In the Mississippi Case, the Plaintiffs included “Jackson Women’s Health Organization, the only licensed abortion facility in Mississippi, and one of its doctors.” This case raised the same third-party standing issues that are presented in June Medical. There were no individual plaintiffs in the Mississippi case.

The Fifth Circuit panel did not hold the case in abeyance. Instead, it resolved the case barely two months later on December 13, 2019.

Subsequently, a petition for rehearing en banc was denied. I suspect a cert petition to be filed soon enough, and ultimately, a GVR following June Medical.

Consider one more abortion case with the same name.

4. Jackson Women’s Health Organization v. Dobbs, No. 19-60455 (5th Cir.)

This case considers Mississippi’s prohibition on abortions after a “fetal heartbeat has been detected.” The panel (King, Costa, and Ho) heard arguments on February 6, 2020 at the University of Houston Law Center. (I was unable to attend in person). This case was not held in abeyance. To the contrary, the panel issued a per curiam decision two weeks later on February 20, 2020.

***

Why were the Texas cases placed on hold while June Medical was pending, but the Mississippi case were decided so quickly? Perhaps June Medical may affect the former cases, but not the latter cases. I’m not persuaded. The Fifth Circuit’s approach is ad hoc, and not standardized. The judges should consider this issue, and come up with some coherent policy. The current regime is unfair to litigants, and fails to accord due deference for the Supreme Court. At a minimum, the parties should be offered the opportunity to brief the issue before a sua sponte abeyance order is issue.

Perhaps the Texas abortion cases got it right. Or maybe the Mississippi abortion cases got it right. But the CFPB case, without question, got it wrong. I am glad that opinion has been vacated. It should no longer serve as a precedent.

from Latest – Reason.com https://ift.tt/346Rs1b

via IFTTT

From Commonwealth v. Mueller, decided Wednesday by a Pennsylvania Superior Court appellate panel:

On June 8, 2018, police conducted a traffic stop in Brookhaven Borough. During the course of the stop, Appellant, who was a bystander and not involved with the traffic stop, approached the scene. Appellant stood over the vehicle’s occupants, and Officer Hughes asked her to step back. Appellant refused to comply. Officer Hughes asked Appellant to step away from the immediate area, and he told her that she could observe from across the street. Officer Barth arrived, spoke with Appellant, and asked her to move.

Appellant began to videotape the scene with her cell phone and refused to move. Officer Barth threatened to arrest Appellant if she did not move, and Appellant moved into the intersection and obstructed traffic. Officer Barth asked Appellant to move again.

Appellant said: “This is fucking ridiculous.” Appellant subsequently walked away and went to work. The police issued a citation, charging Appellant with disorderly conduct at Section 5503(a)(3) (uses obscene language or makes obscene gesture) [for which Appellant was convicted and (a)(4) (creates hazardous or physically offensive condition by any act which serves no legitimate purpose) [for which she was acquitted]

A person is guilty of disorderly conduct under Section 5503(a)(3) if, “with intent to cause public inconvenience, annoyance or alarm, or recklessly creating a risk thereof, [she]…uses obscene language, or makes an obscene gesture.” Where a person uses profane language or other “angry words” that are not used to describe an act of sex or to appeal to anyone’s prurient interest, this Court has found insufficient evidence to sustain a conviction under Section 5503(a)(3). See, e.g., Pennix, supra (reversing conviction under subsection (a)(3) where appellant became agitated during search of her book bag in courthouse and screamed: “Fuck you I ain’t got time for this,” “Fuck you police” and “I don’t got time for you fucking police”; while appellant’s words were disrespectful, insulting and offensive, they were not “obscene” within meaning of Section 5503(a)(3)); Commonwealth v. McCoy, 69 A.3d 658 (Pa.Super. 2013), appeal denied, 623 Pa. 761, 83 A.3d 414 (2014) (reversing conviction under subsection (a)(3) where appellant shouted “fuck the police” multiple times during funeral procession for police officer; record showed no evidence that appellant’s chant was intended to appeal to anyone’s prurient interest or to describe sexual conduct in patently offensive way).

Instantly, the record shows Appellant uttered “this is fucking ridiculous,” after police had repeatedly asked her to back away from the scene of a traffic stop. Nothing in the record indicates that Appellant intended to describe an act of sex or appeal to anyone’s prurient interest.

The Commonwealth agrees the evidence was insufficient to sustain the conviction under Section 5503(a)(3). Accordingly, we reverse Appellant’s conviction and vacate the judgment of sentence. {Due to our disposition, we do not have to consider Appellant’s challenge under the First Amendment.}

from Latest – Reason.com https://ift.tt/39oOYMl

via IFTTT

Futures Rollercoaster As Global Coronacases Approach 1 Million

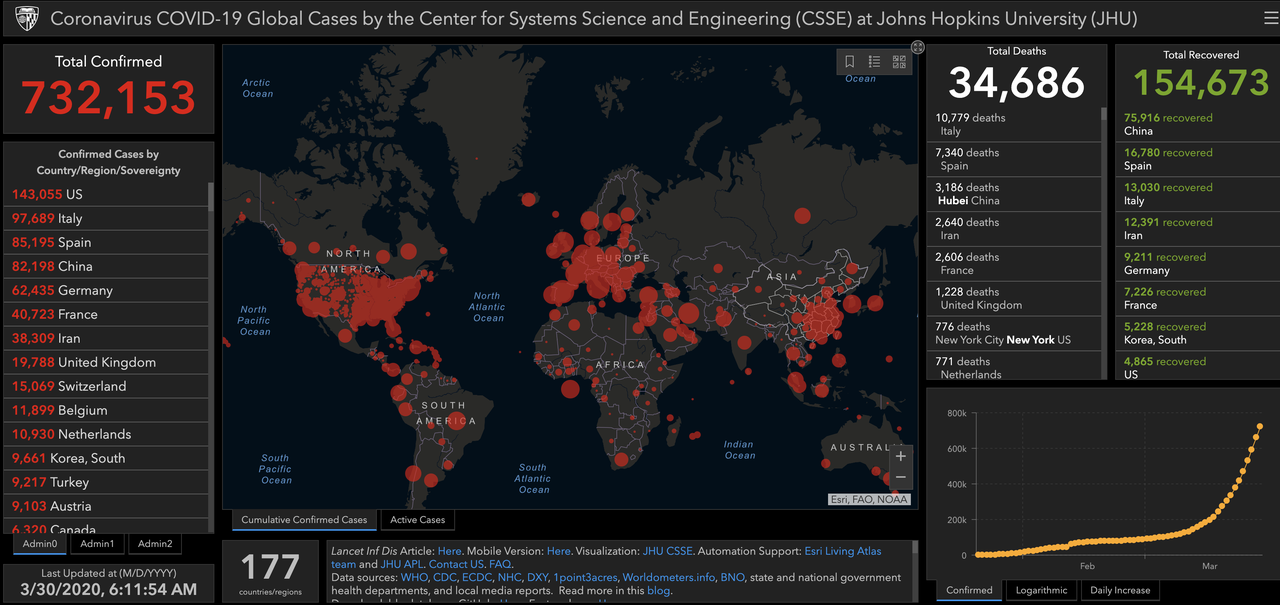

Global markets started off the new week wobbly, with stocks around the world trying desperately to find firm footing even as the global coronavirus cases rose above 732,000 on Monday morning and are set to hit 1 million by the end of the week.

U.S. stock index futures see-sawed on Monday after a strong recovery last week, swinging between losses and gains after President Trump abruptly abandoned his ambition to return American life to normal by Easter raising fears of a larger economic hit from the slump in business activity. After opening more than 4% lower on Sunday, futures have stince staged a rebound, and were trading slightly above Friday’s close when stocks sold off after the Fed announced it would taper its Unlimited QE from $75BN to $60BN. Abbott Labs was a standout, jumping in early trading after unveiling a five-minute coronavirus test.

Shares in Europe followed earlier declines across much of Asia, though they too staged a comeback and traded mostly unchanged as traders were transfixed by the surge in new cases, which rose by 60,000 overnight to 732,153 (and 34,686 deaths). Total cases are now expected to hit 1 million in 3-4 days.

Earlier in the session, Asian stocks fell, led by industrials and IT, after rising in the last session. Most markets in the region were down, with Singapore’s Straits Times Index dropping 4.7% and India’s S&P BSE Sensex Index falling 3.7%. The Topix declined 1.6%, with AP Co and PIA falling the most. The Shanghai Composite Index retreated 0.9%, with Beijing Aritime Intelligent Control and Henan Oriental Silver Star Investment posting the biggest slides.

There were some bright spots, with Australian equities posting a standout surge as the government launched a super-sized support program. Australia’s benchmark ASX200 registered a late surge, closing 7% up after Prime Minister Scott Morrison unveiled a $130 billion ($79.86 billion) package to help to save jobs.

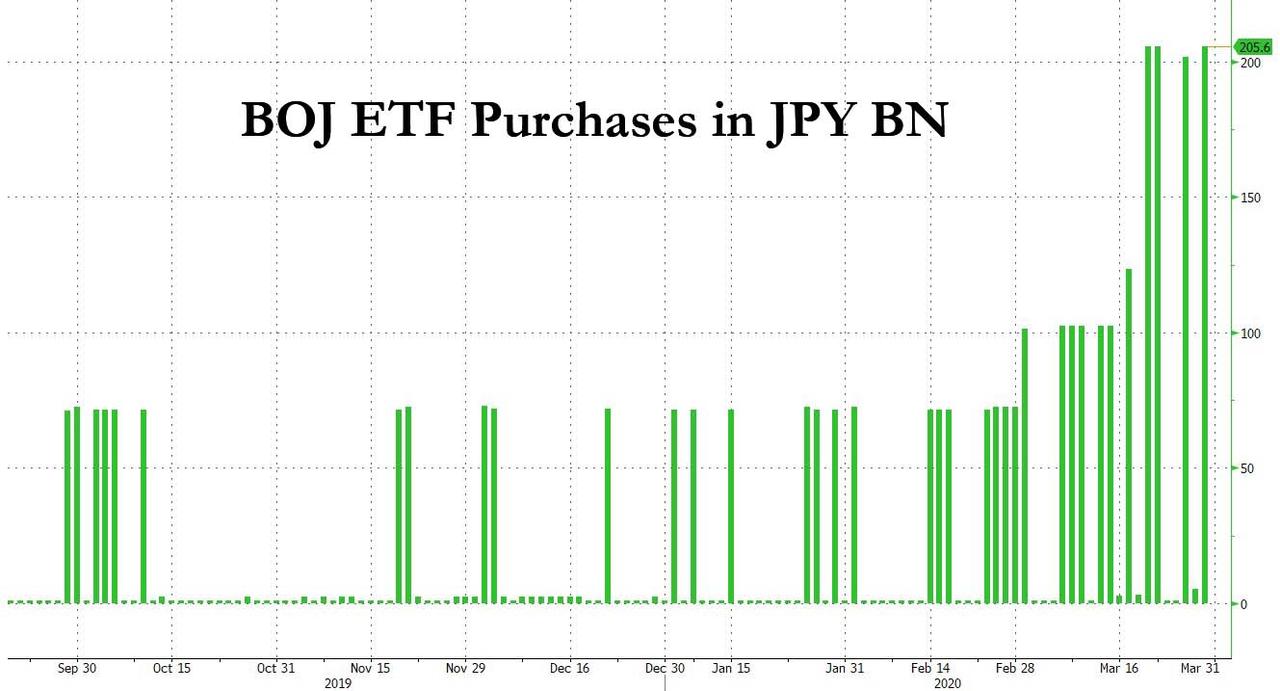

Japan’s Nikkei had led the rest of Asia lower and Europe’s main markets slumped by 1.5-2.5% in early trade, adding to what has already been the region’s worst quarter since 1987. Stocks dropped even as the Bank of Japan purchased another record 201.6b yen of ETFs Monday as it steps up efforts to calm markets.

“I have been in this business almost 30 years and this is the fastest correction I have seen,” Lombard Odier’s Chief Investment Officer Stephane Monier said of this year’s plunge in global markets.

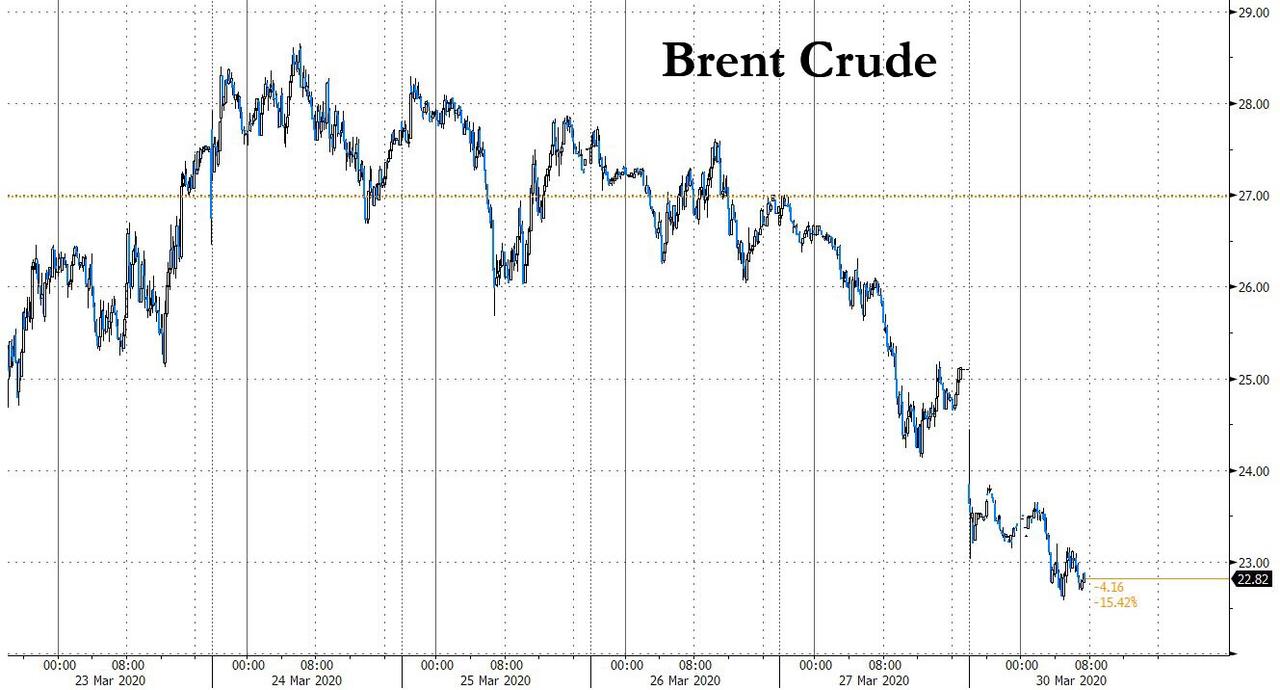

The big standout in overnight trading was oil, which took another eyewatering 8% tumble on Monday, with some now expecting price to drop to zero (or negative) as storage facilities fill up. The rout in oil took crude to its lowest since 2002. Brent was at only $22 a barrel by 0815 GMT, hammering petro currencies such as Russia’s rouble, Mexico’s peso and the Indonesian rupiah by as much as 2%. Brent futures were down 8%, or $2, at $22.50 a barrel – their lowest for 18 years. U.S. West Texas Intermediate (WTI) crude futures fell as far as $19.92, near a 2002 low hit this month.

It didn’t help that the U.S. dollar was back on the climb. The euro and pound were both batted back by about 0.6%, leaving the former near $1.1070 and sterling at $1.2350. On Friday Britain had become the first major economy to have its credit rating cut because of the coronavirus.

JPMorgan now predicts that global GDP could contract at a 10.5% annualized rate in the first half of the year: “We continue to mark down 1H20 global GDP forecasts as our assessment of both the global pandemic’s reach and the damage related to necessary containment policies,” said JPMorgan chief economist Bruce Kasman. As a result, central banks have mounted an all-out effort to bolster activity with rate cuts and massive asset-buying campaigns, which have at least eased liquidity strains in markets.

On Monday, China became the latest to add stimulus, with a cut of 20 basis points to a key repo rate, the largest in nearly five years. Singapore also eased as the city state’s bellwether economy braced for a deep recession while New Zealand’s central bank said it would take corporate debt as collateral for loans.

Rodrigo Catril, a senior FX strategist at NAB, said the main question for markets was whether all the stimulus would be enough to help the global economy withstand the shock: “To answer this question, one needs to know the magnitude of the containment measures and for how long they will be implemented,” he added. “This is the big unknown and it suggests markets are likely to remain volatile until this uncertainty is resolved.”

In rates, bond investors are bracing for a long haul, with European government bond yields dipping and those at the very short end of the U.S. Treasury curve turning negative. 10-year TSYs dropped a steep 26 basis points last week and were last standing at 0.65%. That drop has combined with efforts by the Federal Reserve to pump more U.S. dollars into markets, dragging the currency off recent highs.

Against the yen, the dollar was pinned at 107.74, well off the recent high of 111.71, but its gains against the euro, pound and heavyweight emerging market currencies suggested it was regaining strength.

“Ultimately, we expect the USD will soon reassert itself as one of the strongest currencies,” argued analysts at CBA, noting the dollar’s role as the world’s reserve currency made it a countercyclical hedge for investors. “This means the dollar can rise because of the deteriorating global economic outlook, irrespective of the high likelihood the U.S. is also in recession.”

The dollar’s retreat had provided a fillip for gold, but buying stalled as investors were forced to liquidate profitable positions to cover losses elsewhere. The metal was last at $1,613.6 an ounce, although physical gold was selling for at least 10% higher, and in many places, for much more. The premium of physical silver over spot is as much as 100%.

“Central banks have been easing (monetary policy) and governments have been offering stimulus packages, but they are only supportive measures, not radical treatments.”

Expected data include pending home sales and Dallas Fed Manufacturing Outlook. RH is reporting earnings

Market Snapshot

S&P 500 futures up 0.4% to 2,533.25

STOXX Europe 600 down 1.4% to 306.62

MXAP down 0.8% to 136.73

MXAPJ down 0.4% to 429.75

Nikkei down 1.6% to 19,084.97

Topix down 1.6% to 1,435.54

Hang Seng Index down 1.3% to 23,175.11

Shanghai Composite down 0.9% to 2,747.21

Sensex down 3.4% to 28,813.44

Australia S&P/ASX 200 up 7% to 5,181.38

Kospi down 0.04% to 1,717.12

German 10Y yield fell 6.0 bps to -0.534%

Euro down 0.6% to $1.1079

Italian 10Y yield rose 10.0 bps to 1.157%

Brent futures down 8.5% to $22.82/bbl

Gold spot down 0.4% to $1,621.29

U.S. Dollar Index up 0.5% to 98.80

Top Overnight News

Global coronavirus cases climbed above 720,000 and a top scientist suggested U.S. deaths may reach 200,000, while President Donald Trump abandoned his ambition to return American life to normal by Easter

European officials warned against loosening lockdowns after the coronavirus outbreak claimed more than 3,000 lives in Spain and Italy over the weekend. Strains in health-care systems increased as Spain said its intensive-care wards are stretched beyond capacity and a German public-health leader said the country may face a ventilator shortage

China’s central bank cut the interest rate it charges on loans to banks by the biggest amount since 2015, as the authorities ramp up their response to the worsening economic impact from the coronavirus pandemic.

Oil slumped to a 17-year low as coronavirus lockdowns cascaded through the world’s largest economies, leaving the market overwhelmed by cratering demand and a ballooning surplus of crude

Australia’s central bank netted about 2.5% of the bond market in its first six days of purchases. Yet, the scale of government fiscal stimulus in the pipeline sees little danger of it following Japan’s path and holding too many securities

European lenders including UniCredit SpA, ABN Amro Bank NV and ING Groep NV suspended dividend payments on 2019 earnings, bowing to European Central Bank pressure to retain capital

Japan will issue an extra 16t yen in government bonds from July to cover a stimulus package for coronavirus impact, Reuters reports; The Bank of Japan purchased 201.6b yen of ETFs Monday as it steps up efforts to calm markets

Just two weeks after South Korea adopted one extra budget, President Moon Jae-in said another is already being planned to help insulate households against the impact of the coronavirus pandemic

Asian equity markets resumed their selling, and US equity futures also began the week on the backfoot (before gradually recouping losses) as coronavirus woes continued to weigh on risk appetite and following last Friday’s declines on Wall St after the US overtook China with the greatest number of coronavirus cases. In addition, President Trump recently announced to extend federal guidelines on coronavirus until April 30th and NIH’s Fauci projected a possible 100k-200k deaths. The risk appetite was dampened across most the regional bourses with losses in Nikkei 225 (-1.6%) exacerbated by the flows into the JPY and with notable weakness seen in Softbank shares after a Co.-backed satellite start-up filed for bankruptcy, while ASX 200 (+7%) bucked the trend on stimulus measures with the government to announce support for employers and employees today. Furthermore, the Australian Banking Association said banks are to permit businesses with up to AUD 10mln in loan facilities to defer repayments up to 6 months which will apply to AUD 100bln of business loans, and regulator APRA announced the deferral of capital reform implementation by 1 year. Hang Seng (-1.3%) and Shanghai Comp. (-0.9%) were downbeat despite PBoC efforts in which it injected liquidity through repos for the first time since mid-Feb and lowered the 7-Day Reverse Repo rate by 20bps. Improved earnings including China’s largest banks did little to spur risk appetite amid the broad cautiousness and with press reports suggesting 100mln jobs could be at risk from the coronavirus fallout, while participants also await this week’s upcoming key data including the latest Chinese PMI numbers. Finally, 10yr JGBs were higher and briefly approached the 153.00 level amid the subdued risk appetite and after recent comments by PM Abe who vowed an unprecedented economic package which will include fiscal and monetary stimulus, while prices also tracked T-notes which gapped higher at the open to briefly test resistance at 139.00.

Top Asian News

Tokyo Economy Could Face Lockdown From Few Dozen Virus Cases

How a $100 Billion South Korean Insurer Became a Penny Stock

Fed May Follow Japan and Australia Into Yield-Curve Regime: HSBC

Pessimistic Indian Doctors Brace for Tsunami of Virus Cases

A choppy session in the equity space with European futures fully paring its pre-market gains and then some, whilst cash markets move in tandem (Eurostoxx 50 -0.5%). APAC bouses closed the trading day mostly lower, whilst US equity futures reversed earlier upside of almost 1.5% having opened lower by some 1.8%. Stocks in general lack conviction as coronavirus uncertainty feels counterforce (in the short-term at least) from month and quarter-end rebalancing – which models thus far see outflows from Treasuries and inflows into stocks. Back to Europe, major bourses see broad-based losses, whilst in the periphery – Spain’s IBEX (-1.5%) modestly underperforms the region after the county suffered its worst day yet in terms of coronavirus deaths. Subsequently, sectors remain in the red across Europe with defensives faring slightly better than cyclicals at the time of writing. Looking at the breakdown, Travel and Leisure see another session of steep losses, Oil and Gas is also weighed on by price action in respective complexes. However, Banks underperform having been dealt with the prospect of prolonged share buyback and dividend suspensions alongside a lower yield environment. As such, ING (-6.7%) sees itself towards the bottom of the Stoxx 600 after it announced a dividend suspension until at least 1st October, whilst rebuffing FY20 interim payments. Meanwhile, ABN AMRO (-7.4%) is pressured by anticipated Q1 losses, FY and interim dividend postponements. In terms of other movers – Airbus (-7.5%) tackles subdued aircraft demand as airlines ground their fleets, with easyJet (-6.9%) announcing its entire fleet will be non-operational with no timeframe for the resumption of commercial flights. Elsewhere, Hammerson (-18%) rests at the foot of the pan-European index after noting material impacts on 2020 results and withdrawing dividend and guidance. On the flip side, ASML (+2.8%) sees some reprieve after announcing that its supply chain issues have been resolved, albeit the Co. decided to refrain from Q2 share buybacks.

Top European News

Giant Oil-Field Boost Is Bad for Market, Good for Norway

Euro- Area Confidence Posts Record Drop With Economy in Lockdown

German Bonds Extend Gains After State Inflation Data Disappoint

Stelios Tells EasyJet Need to Cancel GBP4.5-Billion Airbus Order

In FX, it’s debatable whether the Dollar is benefiting from supportive rebalancing flows for the final trading day of March, the current quarter and the 2019/2020 financial year, or improving chart impulses alongside weakness in rival currencies on specific bearish factors, but suffice to say that the Greenback has pared more of its recent losses. Indeed, the DXY has bounced further from Friday’s low (98.284) towards 99.000 and is currently close to a potentially pivotal technical marker around 98.810 that roughly coincides with a Fib retracement and the 21 DMA. However, jittery risk sentiment and arguably greater demand for the Yen over month/Q1/Japanese half fy end appears to be capping the index.

JPY – Bucking the overall G10 trend as noted above, with Usd/Jpy meeting heavy offers above 108.00 from Japanese exporters and various domestic names repatriating funds for tomorrow. The headline pair is now hovering around 107.50 after a knee-jerk spike above the big figure on reports that JGB issuance will be ramped up to fund the fiscal fight against COVID-19, while taking a 4th record equalling amount of BoJ ETF buying in stride.

CAD/GBP/CHF/EUR/NZD/AUD – All overwhelmed if not completely consumed by the Buck’s partial recovery, as the Loonie also digests the latest BoC rate cut and venture into the realms of QE, including commercial paper, on top of another downturn in crude prices. Usd/Cad is towards the top of a 1.4097-1.3993 range, while Cable is sub-1.2400 within 1.2467-1.2319 parameters and Eur/Gbp meandering between 0.8988-21 following Fitch’s 1 run UK ratings downgrade and seemingly 2-way flows into March 31. Nevertheless, the Euro is nearer the base of 1.1143-1.1062 extremes against the Dollar as the coronavirus case and fatality totals continue to pile up in Spain and Italy, and the single currency is also lagging vs the Franc (Eur/Chf sub-1.0600) even though Usd/Chf is hugging 0.9550 from just over 0.9500 at one stage in wake of latest Swiss sight deposits implying increased intervention. Elsewhere, the Kiwi is underperforming down under, or in fact the Aussie is outperforming on the back of bigger financial support efforts from the Government overnight that boosted the ASX. Nzd/Usd is only just keeping afloat of 0.6000 in contrast to Aud/Usd pivoting 0.6150 and the Aud/Nzd cross looking more comfortable on the 1.0200 handle after a brief dip below.

EM – Broad losses vs the Usd against the backdrop fluctuating/fickle risk asset moves, but with the Rouble undermined by Brent’s retracement as well, while the Rand hit fresh record lows circa 18.0750 following Moody’s SA cut to junk, albeit widely anticipated. Conversely, the Singapore Dollar was not unduly ruffled by limited MAS tweaks to the currency peg as it kept the midpoint and corridor unchanged after trimming the band to zero, and the offshore Yuan is off lows post-PBoC 20 bp repo rate cut.

In commodities, another detrimental session for the crude markets thus far amid further crystallisation of the demand impact from the virus outbreak as global economies come to a standstill, whilst supply-side woes refuse to subside. Over the weekend, Saudi Arabia opposed an emergency meeting that the OPEC President was urging as oil markets continue to tumble. This rejection would mean that the market will have to wait until the scheduled meeting in June for any revision of output policy. Analysts at ING believe that this will be too late to counter the surplus expected over Q2, and as such the Dutch bank has cut its ICE Brent forecasts to USD 20/bbl vs. Pre. USD 33/bbl for Q2 2020. Meanwhile, Goldman Sachs stated that oil demand this week is seen lower by 26mln BPD and suggested it is impossible to shut down that level of demand with the absence of large and persistent ramifications to supply. In terms of today’s trade, WTI front-month prices briefly dipped below USD 20/bbl to fresh 17yr lows but meander around the level at the time of writing, meanwhile, its Brent counterpart modestly underperforms with added pressure from OPEC – prices breached USD 23/bbl to the downside. Elsewhere, spot gold remains relatively uneventful on either side of USD 1615/oz ahead of this week’s key risk data releases, and with the macro themes also in the fray. Copper prices meanwhile mimic the choppy action in stock markets – with the red metal having given up its APAC gains during early European trade.

US Event Calendar

10am: Pending Home Sales MoM, est. -2.0%, prior 5.2%

10am: Pending Home Sales NSA YoY, est. 6.0%, prior 6.7%

10:30am: Dallas Fed Manf. Activity, est. -10, prior 1.2

DB’s Jim Reid concludes the overnight wrap

I hope you had as good a weekend as is possible in these strange and troubled times. As forewarned last week we erected a 16 foot trampoline over the weekend in what were pretty icy temperatures. If you have nothing better to do in the lockdown and you want to see how we got on via a time lapse video then look at the link on my Bloomberg header. Failing that search for “Trampoline Travails with Twins” in YouTube. As you’ll see at the end the kids and Trudi got rid of a week of self-isolation frustrations.

Talking of which, it does feel like the last week has been one big rush of adrenaline for markets as unparalleled stimulus has swept through the main economies. However while we all talk about “epi curves” it feels like the stimulus curve is now going to start flattening out after the shock and awe of the last couple of weeks. We are instead going to be left with having to deal with a decline in activity that will be as sharp as anything seen since the Great Depression and likely greater in some countries.

Indeed going forward now, the bad news will come from the real time data and earnings reports that could in some cases create existential risks. The good news will come from a run of slower new virus case growth numbers and mortality rates around the world. If investors can get some visibility on when western economies can re-open and what the pace of such re-openings will look like then they are more likely to look through the worst of the upcoming news. The economic/earnings news will be very bad though in many places and not all companies (or their bond and equity holders) will make it through or will see a significant scar. One area we’ve discussed a lot over the last couple of years is the huge fallen angel risk when we do see the next downturn. This risk is now upon us and this morning Nick and Craig in my team have updated the analysis of what has already been downgraded to HY from IG and names that are potentials. Lots of stats and graphs for your perusal. Link to the complete report here.

Back to the virus and the full round up of the very latest on growth of new cases and mortality rates are in the new “Corona Crisis Daily” which has lots of tables and graphs showing the latest evolution of covid-19. This will be out around the same time as this. However in brief, the highlights are that the percentage growth in new cases and mortality are slowing in the Western economies furthest along the “epi curve”. So for this and more on the latest news see our new sister daily.

To Asia now where markets have kicked off the week on the back foot with the Nikkei (-2.96%), Hang Seng (-1.29%), Shanghai Comp (-1.59%) and Kospi (-1.21%) all down. The Nikkei is leading declines as most Japanese stocks are trading ex-dividend. In FX, the US dollar index is up +0.34% while sterling is down -0.72% following Fitch downgrading the UK’s credit rating to AA- from AA with negative outlook on Friday evening. Elsewhere, futures on the S&P 500 are down -0.40% while Brent crude oil prices are down -6.14%.

The moves in China this morning follow the PBoC cutting the 7-day reverse repo rate to 2.2% from 2.4%. That is the biggest cut since 2015 and should set the stage for the MLF rate cut in April. Meanwhile, the Monetary Authority of Singapore also lowered the midpoint of the currency band and reduced the slope to zero, implying that the central bank will allow for a weaker exchange rate to help support export-driven growth and to ward off deflationary threats.

In other overnight news, President Trump said in a press conference that social distancing protocols would remain in place through all of April, stepping back from hopes of opening the economy back up by Easter. He also added that the hoped the country would reach the “the bottom of the hill” by June 1st.

Moving on. As we move into Q2 later this week the highlights will be the final global PMIs on Wednesday (manufacturing) and Friday (services) and the weekly US initial claims on Thursday which will probably be more real time than the payrolls report on Friday. Note that China’s first set of PMIs will come very early tomorrow London time.

For the final PMIs they rarely change too much from the flash numbers but given the fast moving shutdowns in the second half of this month there’s a chance that they will fall even more from what were already record lows across many of the indices. Italy and Spain’s numbers will be interesting given that we didn’t get a flash number and with them being the worst hit European countries by the virus at the moment. Maybe some comfort could come in China’s numbers (from tomorrow) as activity progressively rebooted during the month. A decent bounce is expected which may give some optimism for all those further behind the “epi curve”. For the rest of the week ahead see the day by day diary at the end.

Recapping last week now and markets across the globe rallied as stimulus in Europe and the US caused optimism to return even as Covid-19 cases in Italy and the US climbed above those reported in China by the end of the week. The S&P 500 recorded its best week since 2009, following on from the worst week since around the same time. Last week the index rose +10.26% (-3.37% Friday), but in total the index is still down -24.95% from the all-time highs. European equity markets slightly underperformed their US counterparts, though that follows on from their outperformance the week before. The STOXX 600 rallied +6.09% over the week (-3.26% Friday), for the largest one week gain since December 2011 and breaking a 5 week losing streak. The DAX gained +7.88% (-3.68% Friday), the IBEX +5.19% (-3.63% Friday) and the FTSE MIB +6.16% over the 5 days (-5.25% Friday) as the three most highly infected countries in Europe saw a stimulus fueled rebound even if Friday saw weakness.

Asian equities also joined in the rally, led by the Nikkei. Japanese equities rallied +17.14% (+3.88% Friday), while the Kospi rallied +9.68% (+1.87%) on the week. With S&P 500 daily move remaining elevated, the VIX was mostly unchanged on the week, finishing just -2.9 points lower at 59.1. Even as equites rallied on the week, other risk assets like crude continued to sell off. Brent and WTI crude oil fell -7.60% (-5.35% Friday) and -4.10% (-4.82% Friday) as both types of crude fell for the 5th straight week with the economic slowdown and price war showing limited to no signs of abating. Elsewhere in commodities, Gold had its best week since December 2008 as the typical haven asset rose on delivery issues and due to the huge stimulus being pumped into the system. The Dollar index sold off over the last 4 days of the week after a 10-day rally, as stress in the funding market dissipated somewhat.

Even with risk rallying, sovereign bonds rose on the week possibly because of all the new QE in the system and that likely coming. However most of the rally occurred on Friday when risk-off came back to town. The 10yr U.S. Treasury yields ended the week -17.1 bps lower at 0.675% (-17.0bps Friday). 10yr Bund yields fell -15.3 bps on the week (-11.3bps Friday) to finish at -0.47%. Peripheral debt tightened over the week, even as spreads widened on Friday. French, Italian, and Spanish 10yr bonds all tightened to 10yr Bunds by -2bps, -15bps, and -4bps over the week respectively but note that the Italian spread widened +21 bps on Friday as EU leaders were unable to agree on further fiscal aid the previous evening. Credit spreads had a much better week, especially US IG after the Fed’s corporate bond buying program was unveiled. US HY cash spreads were -110bps tighter on the week (-30bps Friday), while IG was -63bps tighter on the week (-9bps Friday). In Europe, HY cash spreads were -77bps tighter over the 5 days (-5bps tighter Friday), while IG was 9bps wider on the week (-1bp tighter Friday).

Spain’s COVID-19 Case Total Passes China’s, South Korea Reports Disturbing Rebound In New Cases: Live Updates

Summary:

Dr. Fauci says 100k-200k Americans may die from COVID-19

Trump extends guidelines to April 30

Spain case total passes China

South Korea reports worrying rebound in cases around Seoul

Russia expands Moscow lockdown throughout country

NYC remains undisputed center of US outbreak

Seattle area reports optimistic slowdown in new cases, deaths

New York surpasses 1k deaths

Indian migrant workers ‘washed’ with disinfectant

JNJ announces encouraging progress on vaccine

Chinese press publishes photo of Xi standing in public without mask

Australia launches worker subsidy program

* * *

Hours after Dr. Anthony Fauci appeared on CNN’s “State of the Union” yesterday and declared that the current modeling projects between 100k and 200k deaths in the US alone, President Trump stood up at last night’s Rose Garden press conference and declared that the White House would extend its current guidelines – which call for Americans to avoid gatherings of 10 or more, along with a host of other commandments intended to help “flatten the curve” – through the end of April.

Trump added that the “peak” in new cases & deaths should arrive in two weeks, but by June 1, everything should be fine. This, as New York City hospitals have been transformed into “war zones”, while the number of confirmed cases globally closes in on 1 million. Mayors are cracking down, giving police the authority to hand out fines to anybody who isn’t obeying the terms of the crackdown.

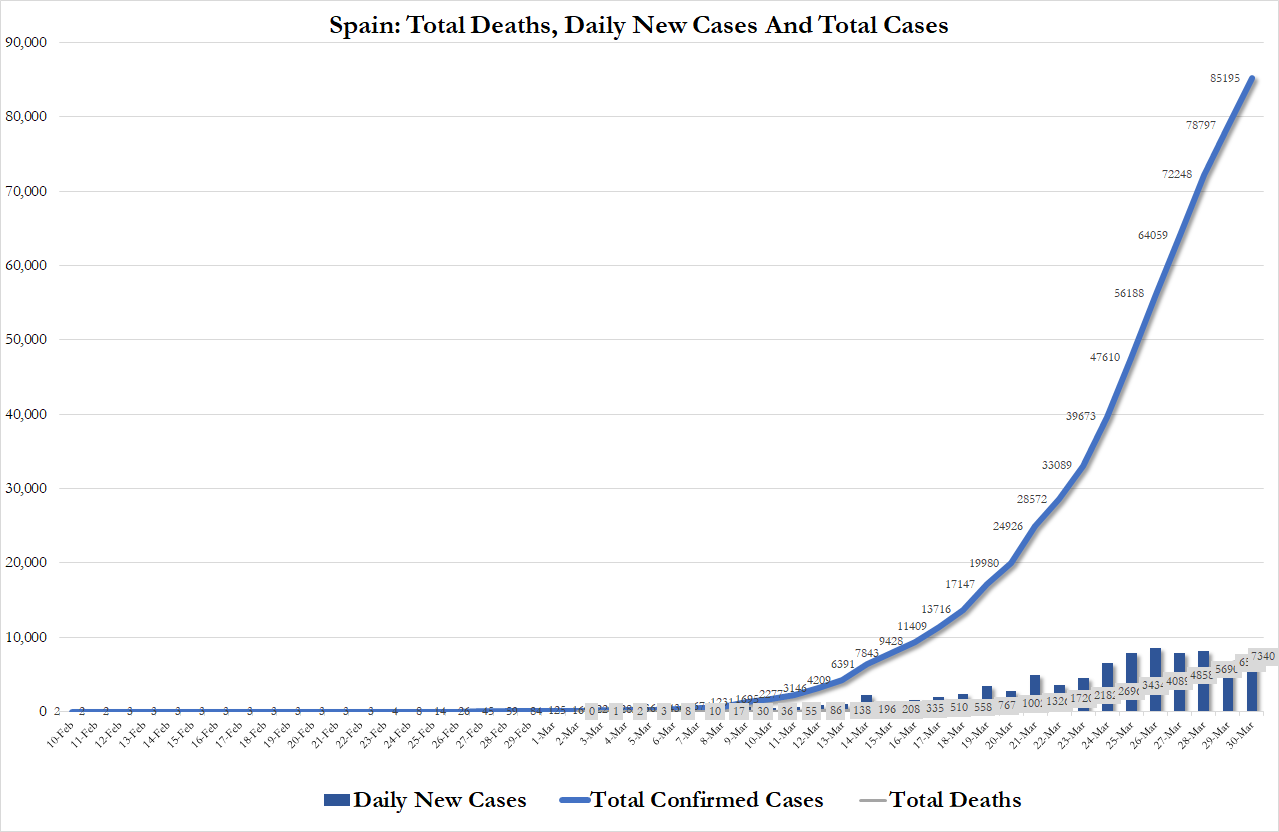

The biggest headline overnight: Spain has surpassed China in the total number of confirmed coronavirus infections (joining Italy and the US) as the number of cases rose from 78,797 on Sunday to 85,195 on Monday, with Spain’s death toll rose by 812 to 7,340, according to the Spanish Health Ministry.

Spanish authorities reported more than 6,000 new cases within 24 hours again on Monday. Among those testing positive: Fernando Simon, the leader of the country’s coronavirus task force.

In the US, New York City remains the undisputed epicenter of the national outbreak as the number of new cases out of the Seattle area has noticeably declined. An area that produced 37 of the first 50 fatalities in the US has seen deaths drop off markedly, while hospitals have been mercifully underwhelmed. While each infected person was spreading the virus to an average of 2.7 other people earlier in March, that number appears to have dropped, with one projection suggesting that it was now down to 1.4, according to the New York Times.

That’s largely thanks to strict measures implemented early on by Washington Gov. Jay Inslee. While NYC Mayor Bill de Blasio was still encouraging New Yorkers to go out and have a good time in late February, Inslee was barring gatherings of more than 250 people and cautioning Washingtonians to stay home and be careful.

New York, meanwhile, surpassed 1k deaths from COVID-19 over the weekend.

As of Monday morning, the US had reported 143,055 cases, according to Johns Hopkins, roughly 1 in 5 global cases (the global case total was 732,000). Projections claim that the global case total should surpass 1 million by the end of the week.

As Tokyo health officials recorded another surprising jump in mostly travel-related cases as of Monday, officials in South Korea warned that they were recording a “sustained increase” in new cases, suggesting new clusters forming around Seoul. Meanwhile, EasyJet, one of Europe’s largest airlines, said it would ground its entire fleet as demand for personal travel collapses.

Across India, migrant workers have struggled with Prime Minister Narendra Modi’s sudden lockdown, which left millions of Indians with only hours to prepare. The PM apologized yesterday, and now, news organizations are reporting on some of the draconian steps that local governments are taking to “disinfect” poor migrant workers returning home.

Back in Europe, the border closures across the Schengen Area have shuttered borders that haven’t been closed since the fall of the Soviet Union. Here’s a guide produced by a non-profit in the region, which recently noted how many Europeans are now meeting loved ones at borders to share a kiss or a quick hello.

Our analysts have come up with a very useful map to track the temporary restrictions put in place throughout the EU, Schengen Area and the UK to deal with #COVID19#stayathomepic.twitter.com/3D5kCPYAt4

As the Russian capital commenced a mandatory self-isolation regime Monday, Prime Minister Mikhail Mishustin called on regional governors to extend the system across the country to control the coronavirus.

Now that world leaders expect the virus to last for most of the year, Australia’s government planned to subsidize the wages of private-sector employees for up to six months to help businesses and workers struggling with the impact of the coronavirus shutdown: “We will pay employers to pay their employees,” said Prime Minister Scott Morrison as he announced what he dubbed a “job keeper” program. “Our government has made a decision today…that no government has made before in Australia,” according to the Washington Post.

The program is part of an $80 billion package.

In Spain, the number of new cases has surpassed China’s “official” total in the number of confirmed coronavirus infections, as the number of cases rose from 78,797 on Sunday to 85,195 on Monday. The death toll rose by 812 to 7,340.

The Chinese press on Sunday published a photo of President Xi standing out in public without a facemask, a notable development as China continues to report no or almost zero new home-grown cases of COVID-19.

In a photo released by Xinhua on Sun, President #XiJinping was seen, for the first time, inspecting a public place without a face mask since the onset of the outbreak. He was seen adhering to health protocols by maintaining a distance from others on a dock. pic.twitter.com/Q7DrRIkUFS

JNJ meanwhile reported Monday that it has produced a “lead candidate” in its trials for a new COVID-19 vaccine. However, it likely won’t be available until 2021, though it’s certainly a reassuring headline for those who fear the pandemic could continue for 18 months.

Finally, Treasury Secretary Mnuchin said Monday that a new bank lending program passed as part of the $2 trillion stimulus bill late last week will be ready by Friday, and he encouraged every business to apply because the loans will be “forgivable” for companies that hire back workers and retain them.

To the great consternation of many a left-leaning Americans, the latest polls from Gallup, Reuters/Ipsos, and Economist/YouGov all show the president’s job approval at 49%, crushing the dreams of those who hoped Coronavirus would finish what the Russia and Ukraine investigations never could.

Claims of misinformation aside, could this be the real reason biased news outlets have decided to stop covering Trump’s briefings?

No Love From The Left

Love him or hate him, there’s no denying the man is a ratings goldmine. According to Nielsen, 12.2 million people watched the president’s Monday briefing on Fox News, CNN, and MSNBC – that’s up there with Monday Night Football. And that doesn’t cover the millions more who watched via ABC, CBS, NBC, or online streaming sites. But is that a good enough reason for media outlets to cover him? That’s the question The New York Times asked recently – a question answered by a Seattle area NPR affiliate, KUOW, with a resounding “no.”

The Washington radio station cited “a pattern of false or misleading information provided that cannot be fact checked in real time” as the reason to dump Trump. And they’re not alone. The Washington Post’s Erik Wemple calls the decision wise, hinting at Fox News, CNN, and MSNBC that they could learn a thing or two if only they would pay attention. MSNBC and CNN, it seems, took the hint, as staffers of both networks have argued the case against airing Trump’s pressers, saying it likely amplifies the spread of misinformation. The president’s son, Eric, took to Twitter to bemoan the trend:

NBC, CNN and others say they will likely stop broadcasting @realDonaldTrump virus briefings. This is truly sick in the time of national emergency and once again tells you everything you need to know about the #MSM. #JournalismIsDead

While the media outlets claim this is all in the name of furthering the truth, the timing is suspicious. The president – who, you may recall, is in the middle of a re-election campaign – is enjoying impressive approval numbers, including amongst many Democrats. He has garnered bipartisan support from both houses of Congress in his handling of the Coronavirus crisis. Even Joe Biden – the man who launched his presidential campaign from the platform that Trump is terrible for the country and must be removed at all costs – has said the president is doing a good job during the emergency and expressed hope for his continued success.

The track record of these outlets was already disappointing, thanks to their backfired attempts to bury Trump in negative coverage from the moment he first announced his candidacy. They couldn’t stop him from being elected, they couldn’t get him impeached, and now it seems they can’t get him blamed for COVID-19. How else can they prevent his re-election? Well, if nonstop negative coverage helped Trump win the White House in 2016, perhaps refusing to publish his pressers will cost him the win in 2020. These regular updates have been called by many in the media little more than Trump campaign events, so this move should come as no surprise.

What about the claim that the briefings are chock full of lies? The Associated Press took it upon themselves to fact check the president, to once and for all prove either that Trump is a liar or that the anti-Trump media is simply biased. You can likely guess how they ruled on this issue.

Thankfully, Liberty Nation’s newest contributor, Dave Patterson, decided to fact check the fact-checkers – and found them woefully wanting.

“AP introduced inaccuracy when the writers conflated two quotations, losing precision and making the single quotation wrong,” he wrote.

“Additionally, they did not put President Trump’s statements in context and created an inaccurate perception for the reader of what the president said.”

When Dave lined up what the AP attributed to the president beside what Trump actually said and the historical data that backs up his claim, the discrepancies – and the AP’s bias – became glaringly clear.

Why are these media outlets really pushing back against covering the president? Either to try to oust him from the White House in November or perhaps out of pure spite, it would seem.

Setting aside the increasingly common conflict of profits vs political bias, isn’t there a far more compelling reason for the press to report the actions and words of Donald Trump than whether or not they think he’s honest or what kind of ratings he can draw?

He is the president of the United States, and almost everything he says and does – certainly anything said during a media briefing – is a matter of national history.

What does it say about our press that they would refuse to report on the president during a time of national emergency?

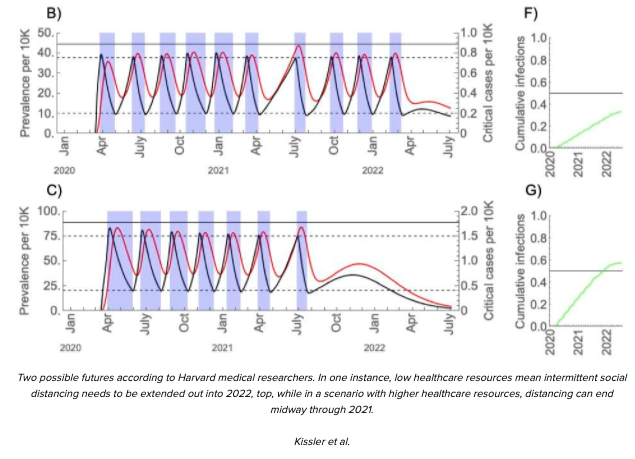

Harvard Researchers Propose “Intermittent” Lockdowns And “Widespread Surveillance” Of Americans To Avoid Critical-Care Capacity

Researchers from Harvard’s T.H. Chan School of Public Health published a study titled “Social distancing strategies for curbing the COVID-19 epidemic,” Tuesday (March 24) on the medRxive pre-print server for health sciences, detailing how a single prolonged widespread lockdown of the country is not the best strategy to combat the COVID-19 pandemic. Instead, the study calls for “intermittent” lockdowns and “widespread surveillance” to mitigate the spread and prevent hospital systems from being overwhelmed.

The study’s authors Stephen Iissler, Christine Tedijanto, Marc Lipsitch, and Yonatan Grad of the Chan School said that “a single period of social distancing will not be sufficient.” They said without repeated intervals of distancing, “there was a resurgence of infection when the simulated social distancing measures were lifted” in the computer model scenarios.

Keep in mind, as per ZDNet’s Tiernan Ray, the study is not yet peer-reviewed, suggesting other scientists have not vetted the computer models of “intermittent” social distancing to solve the virus crisis.

However, the computer models are based on other pandemics and already show that one prolonged lockdown of the country is not the best solution because the virus will return in waves.

The study says some parts of the country where virus cases are low can remain open for business. While other parts that are hard-hit can enforce trict “stay-at-home” public health orders to mitigate the risks of overwhelming hospital systems.

“The SARS-CoV-2 [the virus that causes COVID-19] pandemic is straining healthcare resources worldwide, prompting social distancing measures to reduce transmission intensity,” read the study. “The amount of social distancing needed to curb the SARS-CoV-2 epidemic in the context of seasonally varying transmission remains unclear.”

The study said the pandemic would likely hit in waves, with the virus subsiding this summer, but could return this fall.

“Using a mathematical model, we assessed that one-time interventions will be insufficient to maintain COVID-19 prevalence within the critical care capacity of the United States. Seasonal variation in transmission will facilitate epidemic control during the summer months but could lead to an intense resurgence in the autumn.”

The study concludes by saying, “intermittent distancing measures” on 20-week intervals for specific geographical regions could be turned on and off like a water spigot through 2022.

“Intermittent distancing measures can maintain control of the epidemic, but without other interventions, these measures may be necessary into 2022. Increasing critical care capacity could reduce the duration of the SARS-CoV-2 epidemic while ensuring that critically ill patients receive appropriate care.”

As for what determines if an area should be locked down for a 20-week interval is if cases exceed 37.5 cases of the disease per 10,000 adult people in the population. This threshold, the researchers note, would allow health care systems in those regions to maintain an adequate number of hospital beds and ICU-level treatments.

We noted on Friday that governments and corporations are partnering as a collaborative force to employ big data and “widespread surveillance” to monitor if civilians are abiding by social distancing rules. The authors of the study also agreed that surveillance tools are required to monitor the spread and make sure critical care capacity is not being overwhelmed in certain regions.

To sum up, “intermittent” social distancing could become a reality, embraced by the Trump administration to avoid a prolonged depression in the US as much of the economy is shut down at the moment.

Most judges balk at the prospect of jury nullification—the right and power of juries to bring “not guilty” verdicts when defendants violate laws that jurors consider unjust or wrongly applied. Some of them get extremely mad when a fellow judge endorsesthe practice in his own courtroom.

That’s exactly what happened in December 2019, when a divided three-judge panel of the U.S. 2nd Circuit Court of Appeals rebuked U.S. District Judge Stefan Underhill for telling prosecutors and defense attorneys that before them was a “shocking case” that “calls for jury nullification.”

The prosecution that shocked Underhill was a dubious federal “child pornography” charge growing out of a state statutory rape case. A U.S. Attorney’s Office press release alleged that defendant Yehudi Manzano, 31, “sexually assaulted a 15-year-old female victim in Connecticut, video recorded the assault with his cell phone, and uploaded the video to his Google account.” Yet “the only people who ever saw it were the guy who made it, the girl who was in it, and the federal agents,” Norman Pattis, Manzano’s attorney, says.

How did the feds get jurisdiction in what would normally be a state criminal case? “Apparently, the mere fact that the recording equipment was manufactured outside Connecticut is sufficient to meet the interstate commerce requirement of the [federal child pornography] statute,” Judge Underhill marveled.

Charging Manzano in federal court is no small thing. According to the same press release, “the charge of production of child pornography carries a mandatory minimum term of imprisonment of 15 years…and the charge of transportation of child pornography carries a mandatory minimum term of imprisonment of five years.” Such a sentence would be in addition to the one to 20 years in state prison faced by Manzano for having sex with a 15-year-old who was incapable, under Connecticut law, of consenting to the relationship.

Manzano’s attorneys argued that their client should be allowed to inform the jury of the potential sentence and argue for jury nullification. Judge Underhill agreed.

“I am absolutely stunned that this case, with a 15-year mandatory minimum, has been brought by the government,” Underhill said in court in response to the defense’s motion to be allowed to argue for nullification. “I am going to be allowed no discretion at sentencing to consider the seriousness of this conduct or the lack or seriousness of this conduct, and it is extremely unfortunate that the power of the government has been used in this way.”

Prosecutors promptly filed an emergency motion seeking a “writ of mandamus” that would bar Judge Underhill from permitting the defense to inform the jury of the potential sentence and to argue in favor of nullification. Two of the three appeals court judges hearing the case sided with the prosecution.

“Our case law is clear: ‘it is not the proper role of courts to encourage nullification,'” Judge Richard J. Sullivan wrote in a ruling joined by Judge Denny Chin. “As a practical matter, there is no meaningful difference between a court’s knowing failure to remove a juror intent on nullification, a court’s instruction to the jury that encourages nullification, and a court’s ruling that affirmatively permits counsel to argue nullification.”

The appeals court did not bar Underhill from allowing sentencing information to be presented to the jury, since there are potentially grounds other than nullification that could justify its introduction.

Judge Barrington D. Parker opposed the writ of mandamus regarding both sentencing and jury nullification. “An especially unsettling aspect of this case is that the record the prosecution presented to the District Court and to this Court is barren of anything that would explain, much less justify, the prosecutors’ decision to file the most serious child pornography charges available to them against a man who made a single video which no one else ever saw and which he then attempted to erase,” Parker argued in his dissent.

“Faced with the Government’s charging decision, Judge Underhill could, I suppose, have acquiesced in whatever the prosecutors wanted,” Parker continued. “But he is not a piece of Steuben glass. Instead, witnessing what he perceived to be abuse, he pushed back. I believe that most conscientious jurists would have done the same. I have no difficulty concluding that Judge Underhill was right to do so.”

from Latest – Reason.com https://ift.tt/2vXsEvF

via IFTTT