“The bond market is rallying because The Fed has reacted the seizure in the corporate bond market – which is not getting enough attention.”

The Fed cut rates, he added, “in reaction to even the investment being shutdown for 7 business days.“

Gundlach noted that Powell’s background in the private equity world – rather than academic economist land – has meant that his reaction function is driven by problems in the corporate bond market as “this will be problematic for the buyback aspect of the stock market.”

And today, even investment grade spreads are blowing out – by the most since at least 2011…

As HY is already at its widest since 2016…

And that’s why Gundlach is long gold:

“I turned bullish on gold in the summer of 2018 on my Total Return webcast when it was at 1190. And it just seems to me, as I talked about my Just Markets webcast, which is up on DoubleLine.com on a replay, that the dollar is going to get weaker.

And the dollar getting weaker seems to be a policy. And the Fed cutting rates, slashing rates is clearly going to be dollar negative. And that means that gold is going to go higher.“

Twin Suicide Bombings Target US Embassy In Tunisia

The US Embassy in the Tunisian capital of Tunis was targeted in a twin suicide attack on Friday, described as the most serious attack on any US diplomatic building in months.

Tunisia’s interior ministry confirmed that two suicide bombers blew themselves up just outside the embassy, killing themselves and wounding five police officers and a civilian.

Suicide bomber targets US Embassy in Tunisia on 6 March 2020, via Middle East Monitor/Twitter.

“Witnesses said a man on a motorbike blew himself up near the diplomatic mission in the Berges du Lac district, causing panic among pedestrians at the site,” Al Jazeera reports of the details.

The street outside the embassy appeared littered with debris and destroyed vehicles in the attack aftermath. However, the attackers didn’t appear to get past the embassy’s external security perimeter.

“We heard a very powerful explosion … we saw the remains of the terrorist lying on the ground after he went on the motorbike towards the police,” a local shopkeeper was cited in Al Jazeera as saying.

BREAKING: Huge explosion reported in Tunis, the capital Tunisia, reports say #US embassy was targeted. No casualties reported so far. pic.twitter.com/WAbn1VjUVz

At least one militant on a motorbike blew himself up outside the US embassy in Tunisia today, wounding police officers, witnesses said, in the country’s most serious attack in months, Reuters reported.

The explosion took place near the embassy’s main gate, where a Reuters journalist saw a scorched, damaged motorbike and a damaged police vehicle lying amid debris as police gathered around and a helicopter whirled overhead. — Middle East Monitor

Since the 2011 Arab Spring swept away Tunisia’s hard line secular regime, Salafists and other Muslim fundamentalists have reportedly been more visible in public life.

Security forces inspect the blast site near the US embassy, via AFP.

The North African Mediterranean country has also witnessed sporadic terror attacks over the past years, including a major one last summer involving ISIS coordinating three blasts in the capital including near the French embassy.

A policeman had been killed in that prior attack last year, which also wounded five others.

While ISIS and al-Qaeda linked factions have been active over the past years in Tunisia and the region, and have typically been quick to own up to their attacks, there was no immediate claim of responsibility in the early aftermath of Friday’s embassy attack.

The term “black swan event” is increasingly being used to describe this coronavirus outbreak, and many are concerned that what we are headed for will be much worse than what we experienced in 2008 and 2009. Already, we have witnessed a staggering drop in global demand, Wall Street has had to deal with the wildest week in eight years, and people all over the globe are hoarding toilet paper, face masks and hand sanitizer. That may sound like a plot from one of my books, but it is not. This is actually happening, and it appears that we are still only in the very early chapters of this crisis.

It seems like just yesterday that everyone was freaking out because there were a few dozen confirmed cases here in the United States. Now there are 70in the state of Washington alone…

A cruise ship remains at arms length from San Francisco and the number of confirmed cases of coronavirus in Washington state ballooned to 70 on Thursday – pushing the U.S. total above 220 – as the global struggle against the outbreak intensified.

The nation’s death toll rose to 12, 11of them in Washington. Fifty-one of the confirmed cases are in King County, home to Seattle, where ten of the deaths have occurred, state health officials said.

As I write this article, the total number of confirmed cases in the U.S. has now risen to 233, but of course that number is going to go much higher now that the U.S. has finally decided to ramp up testing for the virus.

If you live in the Seattle area, you are going to want to avoid public places for the foreseeable future. In fact, officials in King County are already recommending that all businesses “allow their employees to telecommute throughout March”…

A Washington state county, where 31 coronavirus cases and 9 deaths have been reported, has recommended to its 2.2 million residents that they should work from home to help slow the spread of the infectious disease, and further urged everyone over 60 to stay indoors.

Public Health officials in King County on Wednesday recommended that businesses allow their employees to telecommute throughout March in an effort to reduce the amount of face-to-face contact between large numbers of people during this “critical period” in the COVID-19 outbreak.

Unfortunately, other hotspots are starting to emerge as well. The total number of cases in California is up to 53, and the number of cases in New York just doubled…

California declared a state of emergency after a coronavirus-related death and 53 confirmed cases in the state. The number of infections in New York also doubled overnight to 22 as the state ramps up its testing.

Predictably, U.S. stocks plunged on Thursday as the bad news came rolling in. By the end of the trading session, the Dow Jones Industrial Average was down 969 points…

Stocks plunged on Thursday, erasing most of the steep gains in the previous session, as markets remained highly volatile in the face of the fast-spreading coronavirus.

The Dow Jones Industrial Average ended the day 969.58 points, or 3.5%, lower at 26,121.28 after tanking nearly 1,150 at its session low. The S&P 500 dropped 3.3%, or 106.18, to 3,023.94 and the Nasdaq Composite fell 3.1%, or 279.49, to 8,738.60. All 11 S&P sectors finished the day in the red. Stocks turned sharply lower as the 10-year Treasury yield fell to an all-time low below 0.9%.

This is precisely the sort of wild market behavior that we witnessed during the financial crisis of 2008. One day stocks would be way down, and the next day they would be way up. When we see extreme volatility such as this, it is a clear indication that investors are very nervous.

After watching what transpired on Thursday, one trader described the market’s current behavior as “a super-puke”…

Watching the markets today – as The Dow plunged 1000 points, Treasury yields collapsed to record lows, credit markets imploded, and demands for more Fed intervention exploded – has one veteran trader remarking, “this is becoming a super-puke.”

Of course if this coronavirus outbreak starts to fade, it is entirely possible that the markets could settle back down.

But that hasn’t happened so far, and experts are warning that we should expect to see more market volatility ahead. Here is one example…

“We expect markets to remain volatile,” Mark Haefele, chief investment officer at UBS Global Wealth Management, said in a note. “The unfolding nature of the coronavirus threat—both real and perceived—is not yet quantifiable, and, as such, the current global policy response can’t immediately be judged as sufficient or insufficient for restoring investor confidence in the short term.”

Meanwhile, the fear that this coronavirus outbreak has created is hitting the real economy exceedingly hard.

Southwest Airlines CEO Gary Kelly told CNBC on Thursday that the company has lost several hundred million dollars in a week’s time thanks to a decline in bookings amid increasing fears over COVID-19. Kelly added that the drop-off was “noticeable” and “precipitous” and has continued declining on a daily basis.

We are seeing similar things happen in industry after industry.

So what is going to happen if this outbreak continues to intensify in the months ahead?

Needless to say, we could soon be facing a worst case scenario for the global economy. According to Egon von Greyerz, the party is indeed “over” and we are headed for the worst economic crisis that any of us have ever experienced…

This is it! The party is over. The world is now facing the gravest economic and social downturn in Modern Times (18th century). We are now entering a period of global crisis that will change the world for a very long time to come. This should come as no surprise to the people who have studied history and also read my articles for the last few years. Many others have also warned about the same thing. But since MSM never talks about the excesses in the world or the risks, 99.9% of people are totally unprepared for what is coming next.

Will he be correct?

We shall see.

It would be wonderful if this virus would just go away and life could get back to normal. Unfortunately, this crisis just seems to escalate with each passing day.

Deputies responded to the Chino Hills Costco at 10.15am on Thursday morning after receiving a report of a disturbance, a San Bernadino County Sheriff’s Department spokeswoman told DailyMaill.com.

On the scene, deputies learned that ‘a large group of customers were upset’ that items such as toilet paper, paper towels, and bottled water were out of stock, said Public Information Officer Cindy Bachman.

All over America, people have been hoarding essential supplies like crazy. If people are this delirious already, how are they going to act once things start getting really bad?

It was inevitable that stock prices would crash from the ridiculously elevated levels that we witnessed earlier this year.

And the next economic downturn has been building for a really long time.

But now events are starting to move at a pace that is absolutely breathtaking, and it looks like all of our lives are about to change in a major way.

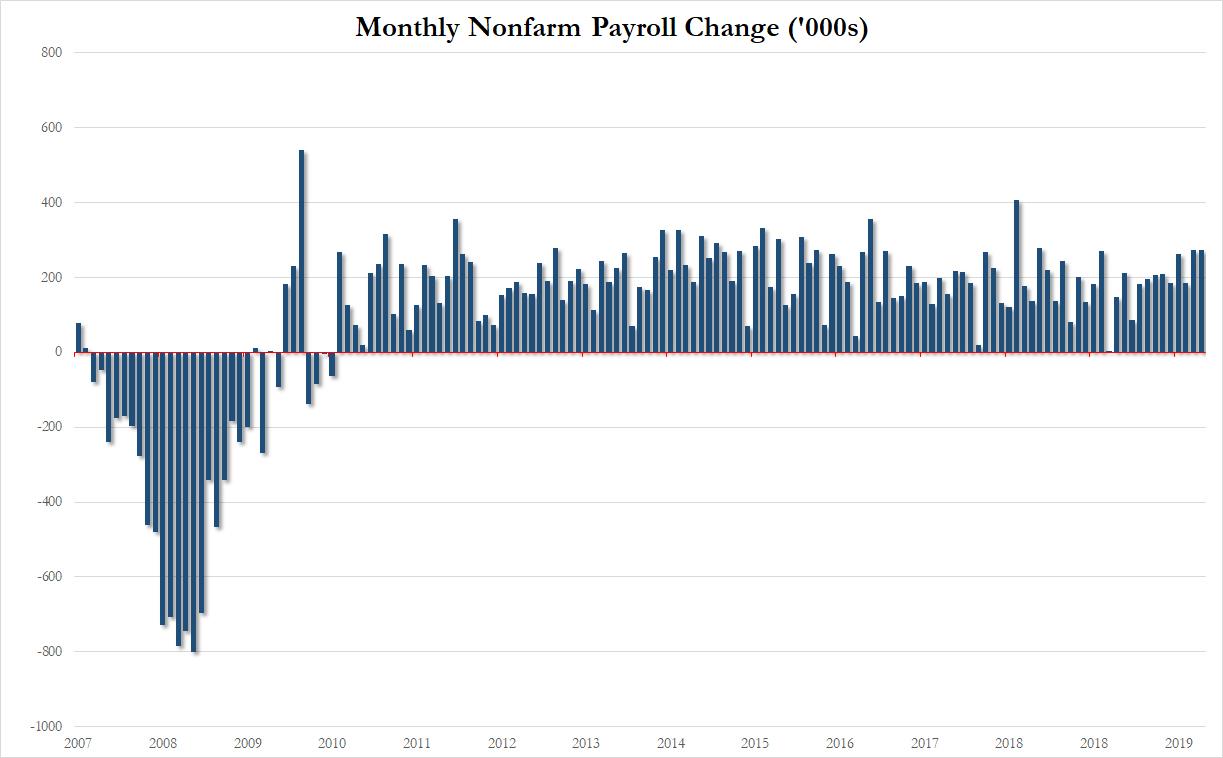

Blockbuster Jobs Report: Feb Payrolls Soar By 273,000, Smashing Expectations, As Unemployment Rate Drops… But Does Anyone Care?

After January’s payrolls revision, which saw almost a million jobs wiped out from the historical record, many analysts were expecting that the BLS would take advantage of the ongoing market shock and “kitchen sink” even more bad news, missing the consensus payrolls expectations of a 175K print for February. They were extremely wrong, because moments ago the BLS reported that in February the US economy added a whopping 273K jobs, smashing the consensus expectation of 175K by one hundred thousand, and tied for the best monthly increase since May 2018.

But wait, there’s more good news, because despite some initial disappointment, the change in total nonfarm payroll employment for December was revised up by 37,000 from +147,000 to +184,000, and the change for January was revised up by 48,000 from +225,000 to +273,000. With these revisions, employment gains in December and January combined were

85,000 higher than previously reported. This means that after revisions, job gains have averaged 243,000 per month over the last 3 months after averaging 178,000 per month in January. Try explaining that to anyone who claims the economy is late cycle.

There were less fireworks in the average hourly earnings data, which increased by 0.3% M/M in February, as expected, and rose 3.0% compared to a year ago, also in line with expectations. That said, the trend in annual wage growth is clearly lower.

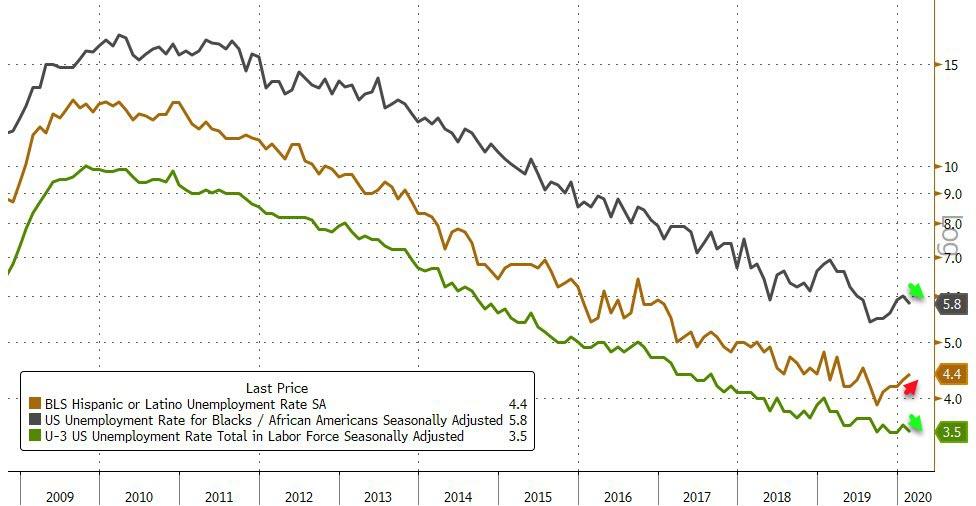

The unemployment rate also improved, sliding from 3.6% to 3.5%, the lowest since July 2018…

… while the participation rate rose to the highest since mid-2013, or 63.4%

Finally, a breakdown by industry reveals the following:

Employment in health care and social assistance increased by 57,000 in February. Health care added 32,000 jobs, with gains in offices of physicians (+10,000), home health care services (+10,000), and hospitals (+8,000). Employment in social assistance increased by 25,000, with a majority of the gain in individual and family services (+18,000). Over the past 12 months, employment increased by 368,000 in health care and by 191,000 in social assistance.

Food services and drinking places added 53,000 jobs in February. Employment in the industry has increased by 252,000 over the past 7 months, following a lull in job growth earlier in 2019.

In February, government employment increased by 45,000, led by a gain in state government education (+16,000). Federal employment increased by 8,000, reflecting the hiring of 7,000 temporary workers for the 2020 Census.

Construction added 42,000 jobs in February, following a similar gain in January (+49,000). In 2019, job gains averaged 13,000 per month. In February, employment gains occurred in specialty trade contractors (+26,000) and residential building (+10,000).

In February, employment in professional and technical services increased by 32,000. Job growth occurred in architectural and engineering services (+10,000) and in scientific research and development services (+5,000). Employment continued to trend up in computer systems design and related services (+8,000). Over the past 12 months, professional and technical services has added 285,000 jobs.

Employment in financial activities increased by 26,000 in February, with gains in real estate (+8,000) and in credit intermediation and related activities (+6,000). Over the past 12 months, financial activities has added 160,000 jobs.

Employment in other major industries, including mining, manufacturing, wholesale trade, retail trade, transportation and warehousing, and information, changed little over the month.

Overall, this was a blockbuster jobs report, the only question we have is does anyone care not only since this was the “most irrelevant jobs report ever” and failed to capture to second half of February slowdown, but also because now that a rate cut to 0%, and even negative, is very much priced in, does any good news matter?

“I am a home-schooler trying to play sports at high levels in order to get into college,” says Caleb Carter, a 17-year-old soccer player from Charleston, West Virginia. “I’m seeing all these players that I’ve competed with for years…[chasing] after their dreams, and I’m sitting here frustrated knowing that I can’t because the Tim Tebow Bill didn’t pass.”

In 1996, Florida passed the first law allowing home-schoolers to play on public school teams, and since then, over 31 states have followed suit. These laws are often named after Tim Tebow, the former NFL quarterback and Heisman Trophy winner, who was able to play football on his local school team thanks to the Florida law.

In West Virginia, advocates have been fighting since 2011 for home-schoolers to have access to school sports teams. And they’re on the verge of scoring a partial legislative victory.

“The Tim Tebow Act is something that has been on the table and in discussion in West Virginia for almost a decade,” says Jamie Buckland, the executive director of Appalachian Classical Academy, a tutorial program for home-schoolers, and a leading proponent of the bill. In 2017, the Tebow Act passed in the state legislature but was vetoed by Gov. Jim Justice.

“I have a son and he’s a really good pitcher,” says Buckland, “and he missed out on those 11th and 12th-grade years of being able to play any organized sports.”

In 2017, Gov. Justice passed a law that effectively allows home-schooled students to play school sports if they take four state-approved online courses per year.

Caleb Carter tried to meet the online course requirement during his freshman year but found the mandate too onerous. “He ended up having to go to the school three to four times per week because they wouldn’t allow him to take even quizzes without being proctored by someone at the school closest to us,” says Tiffany Carter, Caleb’s mother.

“I don’t know of any student who has pursued virtual school for more than one year,” says Buckland. “[The state] is asking parents to sacrifice a curriculum that they have designed for their child specifically.”

On March 2, 2020, the West Virginia state legislature passed a bill reducing the requirement for online classes from four to one. Gov. Jim Justice is expected to sign the bill.

Buckland says that this version of the Tebow Act is a step in the right direction, but that the fight isn’t over. “We are settling for it this year,” Buckland says, “with the intention of amending it next year.”

Produced by Qinling Li and Arthur Nazaryan; Cinematography by Arthur Nazaryan and Qinling Li; edited by Qinling Li; Graphics by Lex Villena.

Music: “Daisy” by Chad Crouch, Attribution-NonCommercial 3.0 International License; “Remnants of Effervescence” by Brylie Christopher Oxley, Attribution License; “machinery” by Kai Engel, Attribution-NonCommercial License.

from Latest – Reason.com https://ift.tt/2IrzZWU

via IFTTT

At a leftist event years ago, I heard a speaker disparage economist Adam Smith and his idea that a nation can best prosper by letting individuals make their own decisions. With the Bernie Sanders candidacy on the rise, anti-market attitudes have gained steam—even among people who express them on nifty electronic gadgets and do so, presumably, with a full belly. Attendees seemed to find the Smith approach crazy.

Granted, the “invisible hand” of the marketplace is, well, invisible. One doesn’t see the millions of individual decisions that place the exact widget you need for your repair project in your hardware store. I’m not sure why leftists don’t see the marvel of this process. If they want real insanity, they should look at the alternative: the clenched and visible fist of government.

You might have noticed California is enduring housing and homeless crises. The market solution to housing shortages is simple: Government should reduce regulations, slow-growth restrictions, rent controls and fees that limit supply and drive up prices. Let builders build. Homelessness is a more complicated problem because homeless people often have addiction and mental-health issues, but more housing would help.

I can’t say exactly how it will work, just as I can’t say exactly how a molly bolt gets from the foundry in India to Home Depot in Sacramento. But I can tell you what won’t work—namely the policies our government now is championing. Gov. Gavin Newsom spent most of his recent State of the State speech detailing a blueprint for dealing with the “disgraceful” homeless situation, which involves more public spending and programs.

But, as The Sacramento Bee reported following the talk, the governor’s ambitious plans “depend on a state department that is understaffed, lacking permanent leaders and struggling to adjust to change, according to documents and interviews.” You can take this to the bank: The new money will be consumed in a bureaucratic hiring frenzy, used to pay state-level salaries and pensions, and build a bigger “homeless industrial complex.”

That’s a facetious, but accurate, phrase used by critics of the state’s homeless policies. They’ve noticed there’s big money in the homeless business. I’m not referring to the serious and important work Rescue Missions and other charities do to alleviate the sting of homelessness, but rather to the armies of bureaucrats and subsidized businesses who have little incentive to reduce homelessness—and every reason to seek more public revenues.

An investigation from this newspaper group found that a third of the apartments being built through the $1.2 billion Prop. HHH bond measure, which voters approved in 2016 to fund supportive housing, “will each cost more than $546,000, the median sale price of a condominium in Los Angeles.” The report found it “uncertain if the program will reach its goal of 10,000 new permanent housing units.”

I’d think it’s fairly certain the bond will run out of cash before its targeted numbers are met and city leaders will be back asking voters for more money. It’s also certain such projects will at best help a fraction of LA’s homeless. Some projects in Southern California have seen per-unit costs approaching $700,000. This is nuts. So, too, is a widely discussed tweet Gov. Newsom recently made regarding the homeless situation.

Newsom’s initial tweet was fine, albeit mostly pabulum: “We need to start targeting social determinants of health. What’s more fundamental to a person’s well-being than a roof over their head?” Well, sure, no one suggests that sleeping in the cold near a freeway interchange is healthy. But then he tweeted this eye-opener: “Doctors should be able to write prescriptions for housing the same way they do for insulin or antibiotics.”

This shows a fundamental lack of seriousness on the part of our governor. I doubt he really would want doctors to prescribe such things. I can imagine what Blue Cross would say when it received a bill for a three-bedroom bungalow in Santa Monica. (I’d hope my doctor would say my health depended on beachfront living.) As others have noted, this amounts to the “magic wand” theory.

The federal Boisedecision limits the ability of localities to remove homeless people from public places—unless officials have a place to house them. Apparently, our governor hasn’t followed the ensuing problems. Cities don’t have a place for all of them. When cities build these units, they end up costing more than a mini-mansion in Texas, so cities run out of money fast.

It gets zanier. Assemblywoman Lorena Gonzalez, the San Diego Democrat who authored the anti-contracting law (Assembly Bill 5) that is decimating the freelance industry, just announced her “Housing for All” package. I fear she’ll do to the housing market what she already has done to the labor market. At some point, even Californians might realize that free markets are the best way to address problems and that trusting officials is true madness.

This column first appeared in the Orange County Register.

from Latest – Reason.com https://ift.tt/3cDjdCg

via IFTTT

Sequoia Capital Warns Of “Black Swan” As Covid-19 Outbreak Persists

Sequoia Capital, a top Silicon Valley venture capital firm, issued a “black swan” warning on Thursday about the Covid-19 outbreak.

In a memo to Sequoia founders, employees, and CEOs of its portfolio companies, it provided “guidance on how to ensure the health of their business while dealing with potential business consequences of the spreading effects of the coronavirus.”

The last time Sequoia sent out a warning like this, it was titled “RIP. Good Times,” and sent to its portfolio companies with some tips for surviving the 2008 financial crisis.

Sequoia calls Covid-19 “the black swan of 2020.” It predicts a severe economic shock will strike the global economy, advising firms in its portfolio to prepare for the worst; “We suggest you question every assumption about your business.”

“Having weathered every business downturn for nearly fifty years, we’ve learned an important lesson — nobody ever regrets making fast and decisive adjustments to changing circumstances,” the memo said. “In some ways, business mirrors biology. As Darwin surmised, those who survive ‘are not the strongest or the most intelligent, but the most adaptable to change.'”

Sequoia’s portfolio of companies extends across the world. It said, “we are gaining first-hand knowledge of coronavirus’ effects on global business.” Here are some of the challenges the venture capital firm has already seen as a result of the virus outbreak:

Drop in business activity. Some companies have seen their growth rates drop sharply between December and February. Several companies that were on track are now at risk of missing their Q1–2020 plans as the effects of the virus ripple wider.

Supply chain disruptions. The unprecedented lockdown in China is directly impacting global supply chains. Hardware, direct-to-consumer, and retailing companies may need to find alternative suppliers. Pure software companies are less exposed to supply chain disruptions, but remain at risk due to cascading economic effects.

Curtailment of travel and canceled meetings. Many companies have banned all “non-essential” travel and some have banned all international travel. While travel companies are directly impacted, all companies that depend on in-person meetings to conduct sales, business development, or partnership discussions are being affected.

Sequoia suggests that every company in its portfolio must prepare for economic disruptions. It offered several ways to do that:

Cash runway. Do you really have as much runway as you think? Could you withstand a few poor quarters if the economy sputters? Have you made contingency plans? Where could you trim expenses without fundamentally hurting the business? Ask these questions now to avoid potentially painful future consequences.

Fundraising. Private financings could soften significantly, as happened in 2001 and 2009. What would you do if fundraising on attractive terms proves difficult in 2020 and 2021? Could you turn a challenging situation into an opportunity to set yourself up for enduring success? Many of the most iconic companies were forged and shaped during difficult times. We partnered with Cisco shortly after Black Monday in 1987. Google and PayPal soldiered through the aftermath of the dot-com bust. More recently, Airbnb, Square, and Stripe were founded in the midst of the Global Financial Crisis. Constraints focus the mind and provide fertile ground for creativity.

Sales forecasts. Even if you don’t see any direct or immediate exposure for your company, anticipate that your customers may revise their spending habits. Deals that seemed certain may not close. The key is to not be caught flat-footed.

Marketing. With softening sales, you might find that your customer lifetime values have declined, in turn suggesting the need to rein in customer acquisition spending to maintain consistent returns on marketing spending. With greater economic and fundraising uncertainty, you might even want to consider raising the bar on ROI for marketing spend.

Headcount. Given all of the above stress points on your finances, this might be a time to evaluate critically whether you can do more with less and raise productivity.

Capital spending. Until you have charted a course to financial independence, examine whether your capital spending plans are sensible in a more uncertain environment. Perhaps there is no reason to change plans and, for all you know, changing circumstances may even present opportunities to accelerate. But these are decisions that should be deliberate.

Sequoia is the latest financial behemoth to urge doomsday preparations.

None of this should be surprising to ZeroHedge readers considering the WeWork implosion in the fall of 2019 was the likely top. Then shortly after, Silicon Valley VC firms held an emergency meeting of unicorn companies in October, specifying how the IPO market was shutting. By early 2020, the VC bubble cracked, and a readjustment in company valuations has been seen. Since the virus outbreak, credit and IPO markets have gone cold, outlining that no matter how much central banks print, they’re powerless in the face of a global health crisis (unable print vaccines and helpless to do anything that will help restart global supply chains or consumption). Sequoia is right, and the “black swan” is here. Prepare Now.

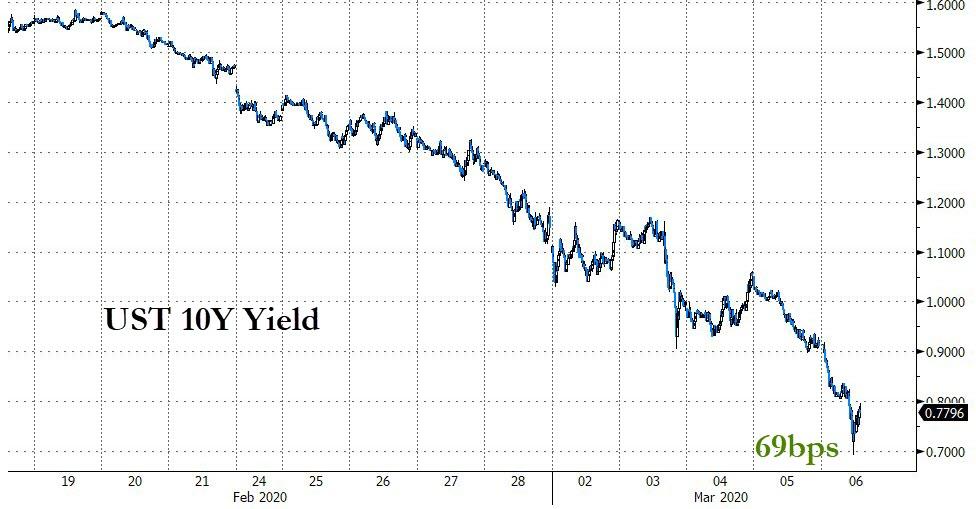

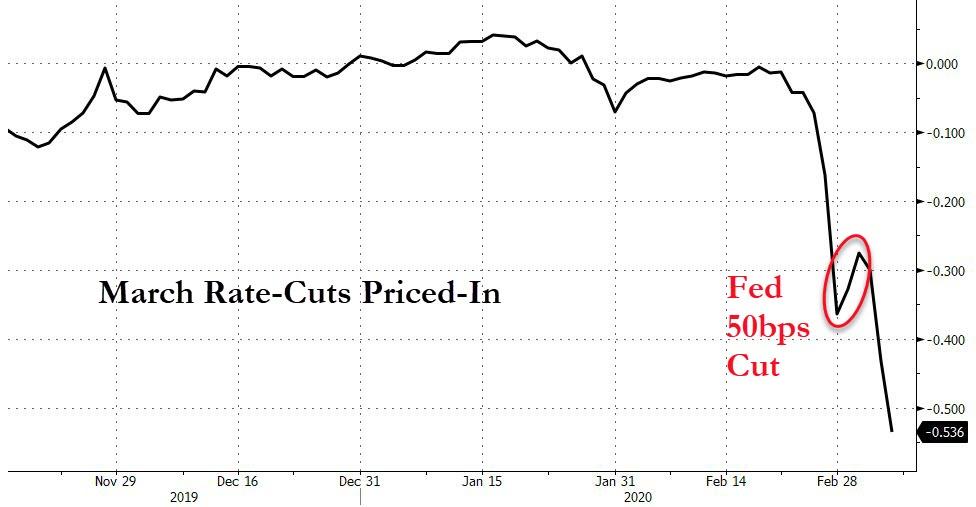

I had previously said I think 10yr US Treasury yields could bottom in April at 75-85bps. Well six days later we are below that range… risk happens fast I guess.

I think the Fed needs to steepen the curve to stop Japanese and European banks selling to primary dealers and crushing liquidity.

This chart below shows the repatriation of capital back to Yen when the curve inverts.

EU and Japanese banks have lent about $4Tn in this cycle via QE leakage to the US government, hence USD weakness and EUR and JPY strength on risk off/ curve inversion.

So if they actually understand what they are doing, The Fed should do an emergency 75bps. Until then we have liquidation, same as what was happening in October.

But if they do cut, it could turn the tables quite quickly. March is already priced for an additional 55bps of cuts (so 75bps would be a major surprise)…

But of course would scream “panic” to the market – and effectively empty The Fed’s rate-cut gun.

If the Fed cuts to 30bps or so EFFR it will mean the curve is steep and we start to see the capital come back out of Japan and EU.

But will they do 75bps in an emergency meeting next week? Or wait for the FOMC on the 18th or just do 50bps? Who knows.

The S&P on the other hand looks to me like it could punch below 2800 without hitting too much technical resistance if there is no emergency meeting.

However, later this month I think the ‘Coronavirus is going exponential’ fears should subside. And I do think there is a second half economic rebound. So perhaps this slowdown and market clear out will be the pause that refreshes?

February Payrolls Preview: The Most Irrelevant Jobs Report Ever

While the market’s attention will be far from today’s payrolls report which i) is a lagging indicator, ii) failed to capture the late February inflection point in the global economy due to the coronavirus and iii) will get far worse in coming months as more Americans self-quarantine and either work from home and take an extended sabbatical, algos will stick react, even if briefly, to the headlines from today’s report, which incidentally will be handily convenient on your favorite trading terminal as the BLS’ decision to end the media lockup has been delayed indefinitely meaning those familiar flashing red Bloomberg headlines will be there to guide the algos what to. That said, as Goldman cautions, the February survey period was too early to show a meaningful impact of the coronavirus outbreak on hiring. With that in mind here is what to expects at 830am ET today courtesy of RanSquawk,

Non-farm Payrolls: Exp.175k, Prev. 225k.

Unemployment Rate: Exp. 3.6%, Prev. 3.6%. (FOMC currently projects 3.5% at end-2019, and 4.1% in the long run).

TREND RATES: After a couple of strongly above-trend readings within the last three reports, the trend of payroll growth has seen shorter term averages rise above longer-term averages, indicating momentum in the pace of hiring: the 3-month average is now 211k (from 198k), 6-month now at 206k (from 200k), and 12- month now at 171k (from 175k). However, the street looks for a print of 178k in February.

Goldman sestimate nonfarm payrolls increased 195k in February, above consensus of +175k. In addition to a 20-30k boost from weather, the bank’s forecast reflects solid labor market fundamentals in early 2020 indicated by very low jobless claims and rebounding business surveys. What is most notable, is that the February survey period was too early to show a meaningful impact of the coronavirus outbreak on hiring.

INITIAL JOBLESS CLAIMS: In the payroll survey week, the initial jobless claims headline came in at 210k, in line with the expected, with the four-week moving average falling to 209k, a welcome development since it was around 216,250 heading into the January NFP survey period. Continuing claims, meanwhile, were a touch above expectations at 1.726mln, rising from a revised 1.701mln.

ADP PAYROLLS: ADP reported 183k payrolls were added to the US economy in February, topping the consensus of 170k; the prior month’s print was downwardly revised, to 209k from 291k (some analysts explained that the large downward revision was due to back-fitting past ADP data to the official BLS series, and not to over-read into it regarding the strength of the labour market). ADP said that the labor market remains firm, and that job creation remained heavily concentrated in large companies, which continue to be the strongest performer. However, Moody’s economist Zandi noted in the report that it did not show any impact from the coronavirus: “COVID-19 will need to break through the job market firewall if it is to do significant damage to the economy. The firewall has some cracks but judging by the February employment gain it should be strong enough to weather most scenarios.” Zandi also noted that decent weather conditions helped the data.

BUSINESS SURVEYS: The manufacturing ISM’s employment sub-index rose slightly in February, to 46.9 from 46.6 (a reading over 50.8 is generally consistent with an increase in the BLS manufacturing employment growth). ISM noted that this was the seventh month of employment contraction, but at a slower rate compared to January. Among the six big industry sectors, two expanded and four contracted, and panellist comments were generally cautious regarding future employment potential, ISM said. The non-manufacturing ISM, meanwhile, was more constructive, seeing the employment sub-index rise to 55.6 from 53.1, meaning employment has been growing for 72 straight months. ISM said comments from respondents included “hiring labor needed to complete work order backlog” and “human resources is working off their backlog.” Looking at other surveys, Markit reported that employment continued to increase midway through Q1, though it was growing at the slowest pace in the current four-month sequence of growth; both manufacturers and service providers alike registered a rise in workforce numbers, Markit said, although the pace of job creation eased in both monitored sectors.

CONSUMER CONFIDENCE: The unemployment rate is seen unchanged at 3.6%, slightly above the FOMC’s 3.5% projection for 2020 as a whole. Analysts note that the latest Conference Board report on consumer confidence saw the differential between jobs ‘plentiful’ and jobs ‘hard to get’ declined to 29.8, which is a marginal negative heading into this week’s payrolls report (the higher this rate goes, the more downward pressure it puts onto the jobless rate, the theory goes). Consumers’ outlook for the labour market was mixed, CB noted, and the proportion expecting more jobs declined slightly from 16.5 to 16.2, but those anticipating fewer jobs in the months ahead also decreased, from 12.9 to 11.1.

WAGE GROWTH: Meanwhile, the pace of wage growth is seen picking-up slightly in the official data, with the Street looking for a 0.1ppts rise to 3.2% Y/Y, and the M/M pace coming in at 0.3%, accelerating slightly from the 0.2% seen in the January report. The CB report noted that there has been a slight moderation in consumers’ view of their short-term income prospects, with the percentage of consumers expecting an increase rising from 21.6 to 22.0, while the proportion expecting a decrease declined from 8.0 to 6.7.

JOB CUTS: Challenger job cuts improved in February (-16% M/M, -4% Y/Y) where 56,660 employees were laid off, down from the 67,735 in January, boding well for the NFP report. The breakdown was led by tech jobs, retail and transportation, although none of which cited the coronavirus as a reason. Challenger states “Despite widespread concerns about COVID-19, it has yet to impact job cut announcements. This may change if the supply side remains dormant, as companies grapple with whether to keep operations open without product. It could also impact Retail, Hospitality, and Travel companies, if concerns keep people at home”, adding measures are being taken by companies such as limited travel, and to work from home if technology allows them to do so. On the coronavirus, Challeger stated “While the majority of cases worldwide have been mild and many people who contract it may not even require a hospital stay, that is not the case for high-risk populations”.

Arguing for a stronger report:

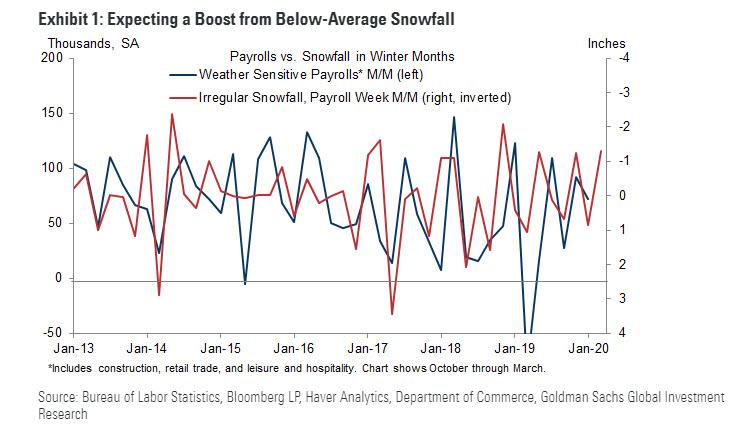

Winter weather. Despite winter storms in the Midwest on the Thursday of the survey week, our population-weighted snowfall dataset was below average for the nation as a whole, and it declined relative to the January survey period (see Exhibit 1, right axis inverted). Accordingly, we are assuming a weather boost of 20k-30k in the February report.

Jobless claims. Initial jobless claims decreased in the four weeks between the payroll reference periods, averaging 209k (vs. 218k in the January payroll month). Continuing claims rebounded 19k from survey week to survey week. Overall, jobless claims data remain consistent with a subdued pace of layoff activity.

Employer surveys. Business activity surveys were firm on net in February despite late-month weakness in the manufacturing sector. For the month as a whole (the payroll data tracks employment in the middle of the month), our nonmanufacturing survey tracker rose 1.5pt to 55.8 and our manufacturing survey tracker rose 0.4pt to 53.2. The employment components exhibited similar patterns, with improvement in services (+0.7pt to 53.4, a 6-month high) but a decline in the manufacturing analog (-1.3pt to 51.6). Our employment survey composite has also increased recently (see Exhibit 2)—supported by de-escalation of the trade war and a decline in uncertainty as of mid-February. Service-sector job growth was +174k in January and averaged 177k over the last six months, while manufacturing payroll employment declined by 12k in January and averaged +1k job growth over the last six months.

Labor market slack. With the labor market somewhat beyond full employment, the dwindling availability of workers may incentivize firms to pull forward spring hiring into the late-winter. As shown in Exhibit 3, first-print February job growth indeed tends to be strong when the labor market is tight.

Census hiring. Temporary employment related to the 2020 Census rose 5k in January. There were only 13k Census employees in the January payroll counts, but we expect this number to rise modestly in February (by about 10k) with still a few months before the major Q2 surge for the enumeration process.

Arguing for a weaker report:

ADP. The payroll-processing firm ADP reported a 183k increase in February private employment, 13k above consensus and close to the average pace of the previous three months (+179k). While the inputs to the ADP model probably contributed to the modest beat, ADP also noted a boost from weather that could support job growth in the official measure as well. On net, we view the ADP report as a neutral to slightly positive factor this month.

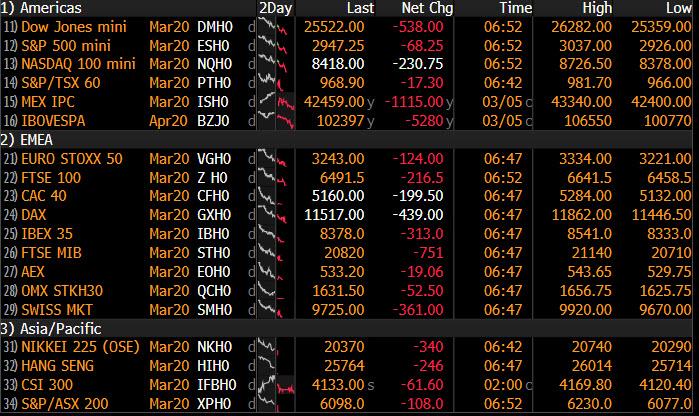

Meltdown: Stocks Tumble, Yields Crater As Coronapanic Infects Traders

Stock markets tumbled, and bond yields cratered on Friday amid a rising trader panic as the number of coronavirus infections neared 100,000 and the economic damage wrought by the outbreak intensified resulting, appropriately enough, in business districts around the world that have begun to empty amid coronavirus evacuations. As a result, global markets were a sea of red amid mounting concern over the economic fallout of the spreading coronavirus.

European shares opened sharply lower, with travel stocks bearing the brunt. The pan-European STOXX 600 index, set for a second day of sharp losses, was down as much as 3.6%, with Germany’s DAX, Britain’s FTSE 100 and France’s CAC 40 all in freefall.

The MSCI All-Country World Index was down 0.72%; all 19 industry groups in the red, as the cost of insuring the region’s high-yield corporate debt climbed to the highest since 2016. After their worst weekly performance since the 2008 financial crisis, global stocks as measured by the index are up 1.7% this week, as sentiment recovered on the back of stimulus from policymakers to combat the economic fallout of the virus. However, at this rate panic is moving markets this morning, we may soon see all of this week’s gains – which include two 1,000+ Dow point gains – reverse.

In the US, contracts on all main index futures pointed to heavy losses at the open after Thursday’s rout, as officials and companies in Britain, France, Italy and the United States are struggling to deal with a steady rise in virus infections that have in some cases triggered corporate defaults, office evacuations, and panic buying of daily necessities. Overnight S&P Index futures slumped as much as 2.5%…

…while the VIX soared as high as 47 on Friday during Asian hours. The number of coronavirus cases worldwide approached 100,000 as the outbreak in the U.S. gathered pace, while China and South Korea continued to report new infections and deaths.

The latest leg of the sell-off kicked off in Asia, where stocks from Tokyo and Sydney to Hong Kong and Seoul slumped more than 2%, falling only for the first time this week, led by energy and finance companies, on mounting concerns over the economic impact of the spreading coronavirus. All Asian markets dropped, with Japan’s Topix index completing a fourth week of declines and Australia’s S&P/ASX 200 closing at its lowest level in almost a year. The Topix declined 2.9%, with Raccoon Holdings and Curves HD falling the most. The Shanghai Composite Index retreated 1.2%, with Ningbo Fuda and Shanghai Lonyer Fuels posting the biggest slides. Shares in China CSI300 finally fell 1.22%, while stocks in Hong Kong, another city hard hit by the virus, fell 2.12%.

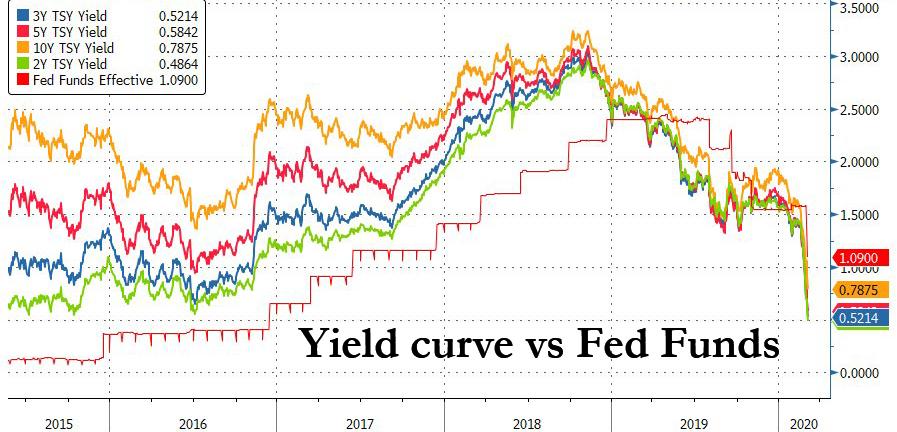

However, while stocks were in freefall, the biggest move was in rates, where the 10Y crashes as low as 0.70% overnight…

… with the entire yield curve now trading below the effective fed funds rate suggesting the Fed may have to cut as much as 75bps in two weeks.

The yields on both 10-year and 30-year treasuries fell to fresh record lows as investors fretted over an expanding health crisis that risks disrupting global supply chains. Germany’s benchmark 10-year Bund yield fell to a six-month low within striking distance of last year’s record lows.

Minneapolis Federal Reserve President Neel Kashkari said late on Thursday the Fed could cut rates further if needed. ANd indeed, money markets are pricing in more than 50 basis-point-cut from the current 1% to 1.25% range at the next Fed meeting on March 18-19.

The corona outbreak has now spread across the United States on Thursday, surfacing in at least four new states. “The interplay of virus containment fears and stimulus measures means that in the near term we expect market volatility to persist,” said Mark Haefele, chief investment officer at UBS Global Wealth Management.

An increasing number of people faced a new reality as many were asked to stay home from work, schools were closed, large gatherings and events canceled, stores emptied of staples like toiletries and water, and face masks a common sight. In London, Europe’s financial capital, the Canary Wharf district was unusually quiet. S&P Global’s large office stood empty after the company sent its 1,200 staff home, while HSBC has asked around 100 people to work from home after a worker tested positive for the illness. In New York, meanwhile, JPMorgan divided its team between central locations and a secondary site in New Jersey while Goldman Sachs sent some traders to nearby secondary offices in Greenwich, Connecticut and Jersey City.

While concerted efforts from central banks and governments to soften the blow from the virus spurred gains across equity markets earlier in the week, investors were clearly back to taking risk off the table and piling into the world’s safest and most liquid assets. The number of coronavirus cases globally approached 100,000, as more infections were reported in the U.S., Germany and South Korea.

“The focus is very much on the spread of coronavirus outside China and really markets aren’t going to settle until we see some sort of peak,” QIC managing director Susan Buckley told Bloomberg TV. “This is going to go on longer than most of us expected.”

In FX, plunging yields hammered the dollar, which fell to a six-month low versus the yen and close to a two-year trough against the Swiss franc. The yen rallied to its strongest since August versus the dollar, advancing against all G-10 peers. The euro climbed to $1.1324, its highest level since mid-2019, and was set for its best week against the greenback since 2016, even thought markets in the euro zone are pricing in a 93% chance that the European Central Bank will cut its deposit rate, now minus 0.50%, by 10 basis points next week. The single currency has now reversed all its earlier losses for the year, rising from below $1.08 a few weeks ago to above $1.13. ING analysts said they were targeting $1.15 in the coming weeks as aggressive U.S. rate cuts contrasted with the limited room for action at the European Central Bank. “For now, expect USD weakness vs G10 FX to continue, and the G10 FX segment outperforming EM FX, with carry trades under pressure,” they said in a research note.

In commodities, oil plunged below $44 per barrel in New York and was set for even greater losses if OPEC failed to reach a production cut with Russia. Focus for the crude complex remains on today’s OPEC+ meeting, where we are still awaiting remarks from Russian Energy Minister Novak himself after OPEC yesterday agreed to a 1.5mln BPD cut and an extension of existing measures. However, comments this morning from a Russian high-level source that Moscow will only agree to extend the existing OPEC+ oil cuts, will not agree to extra cuts and its position will not change caused a significant drop in crude prices.

The price action in metals has been just as fervent and spot gold has printed a new multi-year high at USD 1689.99/oz, surpassing the USD 1689.29/oz which was set last month; a high which takes us all the way back to January 2013.

To the day ahead now where the focus is on the February employment report in the US while the January trade balance and January wholesale inventories are also due to be released. Expect the Fedspeak to also be a big focus today with Evans, Mester, Bullard, Williams, Rosengren and George all due to speak.

Market Snapshot

S&P 500 futures down 2.1% to 2,951.00

STOXX Europe 600 down 2.7% to 370.50

MXAP down 2% to 156.87

MXAPJ down 2% to 516.33

Nikkei down 2.7% to 20,749.75

Topix down 2.9% to 1,471.46

Hang Seng Index down 2.3% to 26,146.67

Shanghai Composite down 1.2% to 3,034.51

Sensex down 2.3% to 37,589.36

Australia S&P/ASX 200 down 2.8% to 6,216.21

Kospi down 2.2% to 2,040.22

German 10Y yield fell 3.7 bps to -0.723%

Euro up 0.4% to $1.1282

Italian 10Y yield rose 5.4 bps to 0.901%

Spanish 10Y yield rose 4.1 bps to 0.254%

Brent Futures down 2.6% to $48.67/bbl

Gold spot up 1% to $1,688.42

U.S. Dollar Index down 0.8% to 96.07

Top Overnight News from Bloomberg

Markets aren’t prepared for how severe the fallout of the global spread of coronavirus could get, according to the manager of a fund which outperformed 98% of its peers over the last month

The number of coronavirus cases globally approached 100,000 as the outbreak in the U.S. gathered pace, and China and South Korea continued to report new infections and deaths

Dollar-funding markets are showing signs of stress as U.S. stocks tank and rates markets price for aggressive easing by the Federal Reserve resulting in a regime change of rates

German factories saw a rebound in demand just before China became engulfed by the coronavirus outbreak that has since spread across the globe.

A key indicator of Japan’s economic outlook fell to its lowest level since the global financial crisis, offering an early official sign that the coronavirus is pushing Japan’s economy into recession.

Federal Reserve Bank of Dallas President Robert Kaplan said the pace of acceleration in the coronavirus across the U.S. will be an important factor as he weighs the need for another interest rate cut when policy makers meet later this month

The Fed’s surprise emergency interest-rate cut has put the central bank in a good position to shelter the record U.S. economic expansion, New York Fed President John Williams said

China’s 10-year sovereign bond yield fell to the lowest since 2002, joining a global rally of government debt as concern mounts that the coronavirus outbreak will derail economic growth this year

Oil extended its slide from the lowest close in more than two years as investors wait for a Russian response to OPEC’s plan for deeper and longer cuts to offset the demand destruction caused by the coronavirus

Asian equity markets slumped across the board as the sell-off rolled over from Wall St. where all major indices declined over 3%, led by a near 1000-point drop in the DJIA amid coronavirus fears which spurred a mass flight to safety and pressured US 10yr yields to fresh record lows. ASX 200 (-2.8%) fell deeper into correction territory as tech and financials resumed their recent underperformance although defensives and gold miners showed some resilience on the safe-haven play, while Nikkei 225 (-2.7%) was the worst performer and retreated below the 21000 level to a 6-month low with losses exacerbated by detrimental currency flows and contractions in Household Spending. Elsewhere, Hang Seng (-2.3%) and Shanghai Comp. (-1.2%) were also heavily pressured alongside the global stock rout and continued PBoC liquidity inaction. On the coronavirus front, the pace of additional confirmed cases and deaths in mainland China continued to show a mild improvement, although this failed to spur markets as attention was also on the increasing number of cases in other countries leading to fears of a global pandemic. Finally, 10yr JGBs were higher amid the bloodbath in stocks and as bond prices tracked their US counterparts higher against the backdrop of record low US 10yr Treasury yields, while the JSCC noted an emergency margin call was triggered for long-term JGB futures and China’s 10yr yield also slipped to its lowest since 2002.

Top Asian News

China Bond Rally Pushes 10-Year Yield to Lowest Since 2002

Virus Adds to Woes of Indonesian Carrier Facing Big Debt Payment

Indian Bank Meltdown Takes Out Walmart’s Leading Payments App

Erdogan’s Ottoman Dreams Lie Broken on the Syrian Battlefield

Further pain for European equities this morning (Eurostoxx 50 -3.1%) as losses in global stock markets show no sign of letting up. Once again, there hasn’t been too much in the way of notable macro newsflow, instead, attention remains on the ongoing climbing case count with particular focus Stateside amid a pickup in COVID-19 diagnosis’ and reports of 2733 people being quarantined in New York City. Commentary around the 2020 Presidential election race continues to impose itself on the market narrative, however, it appears to still be playing second fiddle to the fallout from COVID-19. Furthermore, the market is also trying to wrestle with the narrative over who will be the most favourable candidate for Trump to face in November with Biden viewed as more market-friendly than Sanders, with Sanders an easier candidate for Trump to defeat. In terms of price action in Europe, the sell-off for the DAX gathered momentum early doors (as did other global asset classes) with the Mar’20 contract taking out support at 11617 (March 2nd low) before finding some composure after stalling at 11600. However, as the session progressed, the velocity of the price action in markets accelerated dramatically with the index eventually troughing at 11446. Stateside, futures unsurprisingly indicate a negative open with the e-mini S&P lower by circa 80 points. All ten sectors in Europe are lower with slight underperformance in industrials, consumer discretionary and IT names, whilst consumer staples and telecoms are faring marginally better than their peers, however, are ultimately lower on the session. In terms of individual movers, there is a distinct lack of green on the board with focus instead, once again, to the downside with Capita (-12.6%) the notable laggard in the Stoxx 600 after adding to yesterday’s dire performance. Elsewhere, Prysmian (-9.5%) are markedly lower following disappointing FY results, Atlantia (-8%) are being weighed on after its Autostrade unit delayed results, Airbus (-6.0%) are being sold after posting no new orders in February, whilst executives at Boeing remain bullish on a return of the 737 MAX by mid-year.

Top European News

German Factories Saw Signs of Recovery Before Coronavirus Hit

Deadly Bridges Expose Italy’s Toxic Red Tape and Self Interest

Ray-Ban Maker’s Management Dispute Smolders Amid CEO Search

Hammerson Falls to Lowest Since 1993 After Goldman Downgrade

In FX, the Dollar continues to slide vs major peers while outperforming against the majority of its EM counterparts as US Treasury and other core global bond yields tank amidst more pronounced bull-flattening across the debt curves. As a result, the DXY has extended post-Fed emergency ease lows to 95.993 and there’s little in the way of technical support ahead of 95.950 if the purely psychological or sentimental round number really gives way. NFP looms and usually matters, but in the current environment China’s COVID-19 and contagion appears all consuming

NZD/JPY/CHF/EUR/AUD/GBP – The strongest G10 currencies and roughly in descending order, partly due to relative rate differentials and grades of safe-haven appeal, as Nzd/Usd gathers pace through 0.6350 and Usd/Jpy recoils from 106.30+ overnight peaks below 105.00 (touted as the BoJ’s tolerance line), with supposed bids around 105.50 filled effortlessly along the way. Meanwhile, Usd/Chf is now under 0.9400 and Eur/Chf is threatening another downside breach of 1.0600 that will no doubt ring alarm bells at the SNB, especially as Eur/Usd is bid and now testing 1.1300. Back down under, Aud/Usd has been hampered to a degree by weak Aussie retail sales, though still comfortably above 0.6600, and Cable is approaching 1.3000 even though Eur/Gbp is hovering just shy of 0.8700. In terms of upside bullish objectives, contacts are flagging the 200 WMA around 1.3021, but chart levels are hardly being observed let alone respected at present.

CAD/NOK/SEK – The Loonie is lagging given more dovish BoC guidance in wake of Wednesday’s ½ point rate cut, as Usd/Cad hugs 1.3400 and the same goes for the Scandinavian Kronas irrespective of ordinarily supportive Norwegian GDP and manufacturing production in advance of Riksbank remarks from Ohlsson pledging prompt action (stimulus) if required and then a relatively bland official statement effectively delivering the same message.

EM – In short, risk aversion akin to a rout has taken a toll on all regional currencies, but with the Rouble also undermined by sinking Brent prices awaiting OPEC+, and actually Russia to give its approval to a deeper output cut pact that looks highly unlikely given comments attributed to a top ranking source. However, some solace for the Lira via truce in Syria, albeit fragile.

In commodities, focus for the crude complex remains on today’s OPEC+ meeting, where we are still awaiting remarks from Russian Energy Minister Novak himself after OPEC yesterday agreed to a 1.5mln BPD cut and an extension of existing measures. However, comments this morning from a Russian high-level source that Moscow will only agree to extend the existing OPEC+ oil cuts, will not agree to extra cuts and its position will not change caused a significant drop in crude prices. Prior to this, price action was very much subdued anyway in-line with overall sentiment as the rot in global yields and broad-based safe haven flows has exacerbated this morning to such an extent that WTI and Brent crude futures are posting losses in excess of USD 2/bbl at present, and have breached the USD 44/bbl and USD 47/bbl to the downside; with price action generally showing little signs of abating at present. Note, next week does see the monthly oil market reports released and ahead of this OPEC’s 2020 global oil demand forecast is expected to be at 480kBPD, which is a reduction from the 990kBPD mark in February. Moving to metals, where price action has been just as fervent and spot gold has printed a new multi-year high at USD 1689.99/oz, surpassing the USD 1689.29/oz which was set last month; a high which takes us all the way back to January 2013.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 175,000, prior 225,000

8:30am: Change in Private Payrolls, est. 160,000, prior 206,000

8:30am: Change in Manufact. Payrolls, est. -3,000, prior -12,000

8:30am: Unemployment Rate, est. 3.6%, prior 3.6%

8:30am: Underemployment Rate, prior 6.9%

8:30am: Labor Force Participation Rate, est. 63.4%, prior 63.4%

8:30am: Average Hourly Earnings MoM, est. 0.3%, prior 0.2%; Average Hourly Earnings YoY, est. 3.0%, prior 3.1%

8:30am: Average Weekly Hours All Employees, est. 34.3, prior 34.3

8:30am: Trade Balance, est. $46.1b deficit, prior $48.9b deficit

Market participants are scrambling to look at big data techniques to analyse real time global economic data at the moment. Indeed we’ve had great success in looking at our shipping data in China. My slightly less sophisticated model is looking at the people traffic at Heathrow yesterday and judging by my experience it was around 10-20% lower than when I last travelled a couple of weeks ago. Supermarkets must be seeing an increase in spending though. Early last week I discussed how at home we thought ourselves clever by getting an extra big shop last week. However the online delivery services in our area now have no slots for 5 days (you can normally get one next day) and we’re running out of normal supplies. So while we have toilet roll and nappies in abundance we don’t have much fresh food or milk (it’s gets drunk by the gallon in our household). Hopefully we can find some through the inconvenience of going to an actual shop this weekend.

Yesterday we updated our credit spread view from our 2020 outlook “Wider spreads…but how wide?” to bring forward the peak of the widening and increase the magnitude. In broad terms we think EU/US IG and HY have around 40bps and 250bps of widening still to come. I would like to think we are the only team on the street that have tightened their YE 2020 spread targets in this sell-off over the last two weeks though. The basic argument being that if the peak comes quicker so does the recovery relative to our previous expectations. See the full report here for more details. In addition the payments expert in my team Marion published a fascinating note yesterday about the spread of the virus via cash notes, the fact that China have destroyed cash because of it, and how it might speed up digitalisation, especially in China. See her report here.

Another day, another wild swing for markets as 2-4% moves in either direction for equities are becoming more commonplace. As for bonds it’s not either direction it’s just a straight line down in yields at the moment. The S&P 500 closed down -3.40% and this week alone we’ve seen 4 moves of at least 2% every day either up or down – the last time that happened was August 2011, when the US credit rating was cut. The market came close in August 2015, when there were 5 of 6 days in a row that saw those outsized moves. If we extend that analysis to last week then of the 9 trading days, 7 have featured moves of at least 2% which is the most since December of the global financial crisis, which was also the last time we saw a full 5 day week of such moves. Along a similar vein, the VIX closed over 30 for a full calendar week for the first time since October 2011.

Last week was all about the negatives of the virus, whereas this week there has been much more tension between worsening virus news but increasing chatter of and actual stimulus. Yesterday the bad news won out though. Indeed the developments over the last 24 hours include NYC reporting news cases, a first case in San Francisco, over 2 million being urged to work from home in Washington County, HSBC partially clearing its London trading floor following a reported case, Switzerland and the U.K. reporting their first deaths, France, Germany and Italy reporting a big jump in cases and the Trump administration admitting that the US will be unable to meet its target of having a million coronavirus tests available by the end of this week. Here in the UK we also saw Flybe go into administration – albeit a budget airline which was already under considerable pressure prior to the coronavirus. This hurt the global travel industry more yesterday. Travel and Leisure was the 3rd worst sector in the STOXX 600 yesterday down -2.90 %, with airlines making 4 of the worst 8 performers – similarly Airlines in the US were down -8.19% and the worst performing industry in the SPX. Driving the point home on airlines and travel, TUI and Air France-KLM widened +122bps and +128bps respectively yesterday to 690bps and 453bps respectively. Lufthansa was the worst performing European IG CDS yesterday widening +44bps to 160bps. It was below 60bps just two weeks ago.

Risk off has continued in Asia this morning with the Nikkei (-2.95%), Hang Seng (-2.16%), Shanghai Comp (-0.94%) and Kospi (-2.16%) all down. As for FX, the Japanese yen is up +0.32% while most EM fx is trading weak this morning and the US dollar index is down -0.29%. Elsewhere, futures on the S&P 500 are down a further -1.36% while yields on 10y USTs are down another -10.3bps to an all-time low of 0.811% and those on the 30y are down -12.5bps to 1.417% – also a record low and first time below 1.5%. Brent crude oil prices are down -1.24% to $49.37 this morning and gold prices are up +0.42%. As we go to print, Bloomberg is reporting that Thailand’s government is planning to give cash handouts to its citizens to combat the virus induced slowdown. With this it becomes 2nd country after Hong Kong to suggest such a measure. Helicopter money is coming.

Back to yesterday where there were also big moves lower for the NASDAQ (-3.10%), DOW (-3.58%) and STOXX 600 (-1.43%). Oil also fell -2.25% despite OPEC trying to lay the ground to cut daily crude output by 1m barrels in the second quarter with further cuts also expected from non-OPEC allies. But the oil producing nations are facing opposition from Russia, and could make the cuts contingent on them joining, which sent Brent lower in the NY afternoon session. In bonds, US 10y yields went under 1% again, rallying 14.0bps to 0.912%, breaching the low mark of 0.924% from earlier this week. Front end yields fell a similar amount keeping the 2s10s curve around 31bps while it’s worth noting also that Freddie Mac 30y mortgage rates fell to a record low 3.29%. In Europe we saw 10y Bund yields down 4.8bps to -0.69% while the periphery sold-off 5-7bps. European Banks were actually down -3.89% with the index testing the August lows again and down -23.78% since the local peaks just 2 weeks ago. Credit markets were also weaker with cash HY spreads in the US 26.4bps wider. Finally the USD was weaker, with the DXY down -0.53%.

30y US Treasuries closed at fresh lows of 1.54%, which is the first time it has closed lower than the SPX div yield for multiple days since the financial crisis. Staying with long bonds, the 100 year Austrian bond (2117 maturity) now trades at a price of over 218 having started the year at around 158 – nearly a 40% return in just over two months. At the start of March last year it was just under 120. I can’t help wishing I had a long dated fixed income pension portfolio in Austria. I also can’t help wishing I was still alive when it matures.

After the close last night we heard from a few Fed officials. Fed president Williams said that his baseline outlooks for the US was still “pretty darn good”, yet he saw risks for the outlook around growth in China and the global economy. He saw inflation moving up to the 2% goal, with growth around 2.25%, even with issues around the virus on China’s growth outlook. Finally he cited his concerns surrounding the transition from Libor, and called it the “biggest challenge to our financial system.” Fed president Kaplan was equally concerned about the virus and said that the spread would be important to view when deciding on whether another interest rate cut was needed, but did not view the equity moves as tightening financial conditions excessively. Fed president Kashkari cited the cut this week as insurance against negative economic effects from the spread of the virus, but acknowledged that more cuts may be needed.

Moving on. While today’s payrolls report would usually be the focal point for markets, for now the data is very much playing second/third/insert as necessary* fiddle to what is going on with the coronavirus given that it’s all too backward looking. So it’s likely markets will somewhat look beyond what the data shows however for completeness the consensus for today is 175k following a 225k print last month. This should be enough to keep the unemployment rate at 3.6% while average hourly earnings are expected to rise +0.3% mom with the annual rate at +3.0% yoy.

The same can be said for the data that was released yesterday. In fairness the claims data was about as real time as we can get and that showed no deterioration (216k versus 219k the week prior). Expect the market to be focused on this data from next week onwards however. Elsewhere Q4 nonfarm productivity was revised down to 1.2% qoq and core capex orders were unrevised in January at +1.1% mom. In Europe the only data of note was the February construction PMI in Germany which rose 0.9pts to 55.8 and the highest since January 2018.

To the day ahead now where this morning the data includes January factory orders in Germany. This afternoon the focus is on the February employment report in the US while the January trade balance and January wholesale inventories are also due to be released. Expect the Fedspeak to also be a big focus today with Evans, Mester, Bullard, Williams, Rosengren and George all due to speak.

{kind=link}

{kind=link}