After Purell Sells Out, Titos Says Stop Using Vodka As Hand Sanitizer

Americans have been panic buying masks, Purell, and food in the last several weeks as pandemic fears soar. We showed over the weekend how thousands of people rushed to Costco stores across the country to load up on supplies.

The latest run on products started with Purell last week. Brick and mortar and e-commerce stores ran out of the hand sanitizer made of an ethyl alcohol solution. As a result of surging demand and now shortages, it forced many people to experiment at-home in concocting their own hand sanitizer blend with vodka.

Austin-based Tito’s Vodka noticed Twitter users in the last 24 hours were using their spirits to make at-home sanitizers. Tito’s social media team was quick to inform anyone who was experimenting with Tito’s products that the concentration of alcohol in the products wasn’t high enough to be rated as an effective sanitizer. “Per the CDC, hand sanitizer needs to contain at least 60% alcohol. Tito’s Handmade Vodka is 40% alcohol, and therefore does not meet the current recommendation of the CDC,” Tito’s Vodka tweeted.

Per the CDC, hand sanitizer needs to contain at least 60% alcohol. Tito’s Handmade Vodka is 40% alcohol, and therefore does not meet the current recommendation of the CDC. Please see attached for more information. pic.twitter.com/DtpfsAHZKJ

“As soon as we saw the incorrect articles and social posts, we wanted to set the record straight,” a spokesperson for Tito’s said in a statement provided to The Dallas Morning News. “While it would be good for business for our fans to use massive quantities of Tito’s for hand sanitizer, it would be a shame to waste the good stuff, especially if it doesn’t sanitize (which it doesn’t, per the CDC).”

Per the CDC, hand sanitizer needs to contain at least 60% alcohol. Tito’s Handmade Vodka is 40% alcohol, and therefore does not meet the current recommendation of the CDC. Please see attached for more information. pic.twitter.com/QNEFOXxYPQ

Per the CDC, hand sanitizer needs to contain at least 60% alcohol. Tito’s Handmade Vodka is 40% alcohol, and therefore does not meet the current recommendation of the CDC. Please see attached for more information. pic.twitter.com/J5ifkV3Jah

Per the CDC, hand sanitizer needs to contain at least 60% alcohol. Tito’s Handmade Vodka is 40% alcohol, and therefore does not meet the current recommendation of the CDC. Please see attached for more information. pic.twitter.com/96uldE8uMe

As the fast-spreading virus infects America, what products will people hoard this coming weekend? We’re sure more videos will surface on social media of runs on stores.

It is not uncommon to encounter political theorists and pundits who insist that political centralization is a boon to economic growth. In both cases, it is claimed the presence of a unifying central regime – whether in Brussels or in Washington, DC, for example – is essential in ensuring the efficient and free flow of goods throughout a large jurisdiction. This, we are told, will greatly accelerate economic growth.

In many ways, the model is the United States, inside of which there are virtually no barriers to trade or migration at all between member states. In the EU, barriers have been falling rapidly in recent decades.

The historical evidence, however, suggests that political unity is not actually a catalyst to economic growth or innovation over the long term. In fact, the European experience suggests that the opposite is true.

Why Did Europe Surpass China in Wealth and Growth?

A thousand years ago, a visitor from another planet might have easily overlooked European civilization as a poor backwater. Instead, China and the Islamic world may have looked far more likely to be the world leaders in wealth and innovation indefinitely.

Why is it, then, that Europe became the wealthiest and most technologically advanced civilization in the world?

Indeed, the fact that Europe had grown to surpass other civilizations that were once more scientifically and technologically advanced had become apparent by the nineteenth century. Historians have debated the question of the origins of this “European miracle” ever since.

consists in a simple but momentous fact: It was in Europe—and the extensions of Europe, above all, America—that human beings first achieved per capita economic growth over a long period of time. In this way, European society eluded the “Malthusian trap,” enabling new tens of millions to survive and the population as a whole to escape the hopeless misery that had been the lot of the great mass of the human race in earlier times. The question is: why Europe?

Across the spectrum of historians, theories about Europe’s economic development have been varied, to say the least. But one of the most important characteristics of European civilization—ever since the collapse of the Western Roman Empire—has been Europe’s political decentralization.

Raico continues:

Although geographical factors played a role, the key to western development is to be found in the fact that, while Europe constituted a single civilization—Latin Christendom—it was at the same time radically decentralized. In contrast to other cultures—especially China, India, and the Islamic world—Europe comprised a system of divided and, hence, competing powers and jurisdictions.

Although modern EU centralizers are attempting it, at no point has European civilization ever fallen under the dominion of a single state as has been the case in China. Even during the early modern period, as some polities managed to form absolutist states, much of Europe — such as the highly dynamic areas in the Low Countries, Northern Italy, and the German cities — remained in flux and highly decentralized. The rise of the merchant classes, banking, and an urban middle class — which began as early as the Middle Ages and were so essential in building the a future industrial Europe — thrived without large states.

After all, while a large polity with few internal borders can indeed lead to large markets with fewer transaction costs, concentrating power in one place brings big risks; a state that can facilitate trade across a large empire is also a state that can stifle trade through regulation, taxation, and even expropriation.

The former vast kingdoms and empires of Asia may have once been well positioned to foster the creation of a wealthy merchant class and middle class. But the fact is this didn’t happen. Those states instead focused on stifling threats to state power, centralizing political control of markets, and extorting the public through the imposition of fines and penalties on those who were disfavored by the ruling classes.

The Benefits of “Anarchy”

In contrast, Europe was relatively anarchic compared to other world civilizations and became the home of the great economic leap forward that we now take for granted. This isn’t “anarchy” in the sense of “chaos,” of course. This is anarchy as understood by political scientists: the lack of any single controlling state or authority. In key periods of the continent’s development—as now—there was no ruler of “Europe” and no European empire. Thus, in his book The Origins of Capitalism, historian Jean Bachler concludes:

The first condition for the maximization of economic efficiency is the liberation of civil society with respect to the state….The expansion of capitalism owes its origins and raison d’être to political anarchy. (emphasis in original)

For many years, economic historians have attempted to find correlations between this political anarchy and Europe’s economic success. Many have found the connection to be undeniable. Economist Douglass North, for instance, concludes:

The failures of the most likely candidates, China and Islam, point the direction of our inquiry. Centralized political control limits the options—limits the alternatives that will be pursued in a context of uncertainty about the long-run consequences of political and economic decisions. It was precisely the lack of large scale political and economic order that created the environment essential to economic growth and ultimately human freedoms. In the competitive decentralized environment lots of alternatives were pursued; some worked, as in the Netherlands and England; some failed as in the case of Spain and Portugal; and some, such as France, fell in between these two extremes.

Competition among Governments Means More Freedom

But why exactly does this sort of radical decentralization “limit the options” for ruling princes and kings? Freedom increases, because under a decentralized system, there are more “alternatives”—to use North’s term—available to those seeking to avoid what E.L. Jones calls “predatory government tax behavior.” Thus, historian David Landes emphasized the importance of “multiple, competing polities” in Europe in setting the stage for

private enterprise in the West possess[ing] a social and political vitality without precedent or counterpart. This varied, needless to say, from one part of Europe to another…And sometimes adventitious events like war or a change of sovereign produced a major alteration in the circumstances of the business classes. On balance, however, the place of private enterprise was secure and improving with time; and this is apparent in the institutional arrangements that governed the getting and spending of wealth.

It was this “latent competition between states,” Jones contends that drove individual polities to pursue policies designed to attract capital. More competent princes and kings adopted policies that led to economic prosperity in neighboring polities, and thus “freedom of movement among the nation-states offered opportunities for ‘best practices’ to diffuse in many spheres, not least the economic.” Since European states were relatively small and weak—yet culturally similar to many neighboring jurisdictions—abuses of power by the ruling classes led to declines in both revenue and in the most valuable residents. Rulers sought to counter this by guaranteeing protections for private property.

This doesn’t mean there were never abuses of power, of course, but as Landes observed:

To be sure, kings could, and did, make or break men of business; but the power of the sovereign was constrained by the requirements of states…and international competition. Capitalists could take their wealth and enterprise elsewhere and even if they could not leave, the capitalists of other realms would not be slow to profit from their discomfiture.

Nor was decentralization limited to the international system of separate sovereign states.

Thanks to the longtime tug-of-war between the state and the church, and between kings and nobles, decentralization was common even within polities. Raico continues:

Decentralization of power also came to mark the domestic arrangements of the various European polities. Here feudalism—which produced a nobility rooted in feudal right rather than in state-service—is thought by a number of scholars to have played an essential role….Through the struggle for power within the realms, representative bodies came into being, and princes often found their hands tied by the charters of rights (Magna Carta, for instance) which they were forced to grant their subjects. In the end, even within the relatively small states of Europe, power was dispersed among estates, orders, chartered towns, religious communities, corps, universities, etc., each with its own guaranteed liberties.

Over the long term, however, it was the system of international anarchy that appears to have ensured that states were constrained in their ability to tax and extort the merchant classes and middle classes, who were such a key component of Europe’s rising economic fortunes.

We Need a Return to Smaller Polities

Even today, we continue to see these factors at work. Small states—especially in Europe and the Americas—tend to have higher incomes and have greater openness. We can see this in the microstates of Europe and in the Caribbean. Small states, seeking to attract capital, often undercut larger neighbors in terms of taxes.

It is true that one of the most economically successful polities in the world today is a large one: the United States. The US’s success, however, can be attributed to the enduring presence of political decentralization internally—especially during the nineteenth century—and to the latent, albeit receding, economic liberalism esteemed by much of its population. Europe, of course, was already rich—and relatively politically free compared to the despotic regimes of the East—long before it began to centralize political power under the banner of the European Union.

Today, however, we are seeing the impoverishing downside of decades of political centralization in both the US and Europe. Government regulations decreed from Brussels and Washington continue to stifle innovation and entrepreneurship. The EU has sought to crack down on low taxes in smaller member states. Both the EU and the US are erecting trade barriers to producers outside their trading blocs.

The antidote to all of this is to decentralize. Decentralization, after all, has never been a true barrier to economic growth. If anything, the rise of mobile capital and global trade has made economic success more attainable for small states than ever before. Moreover, the implosion of the Soviet Union provides yet another example of how the disintegration of a large state can lead to far more economic progress than had been thought possible.

Unfortunately, those in power, who benefit from the status quo and from holding the reins of large states, are unlikely to relinquish their power without a fight.

Bloomberg Launching New Group To Support Democratic Nominee, Attack Trump

‘Mini’ Mike Bloomberg is forming a new organization which will support the Democratic nominee and attack President Trump, according to the Washington Post.

This type of stuttering, mental impairment and overall cognitive decline is frequently seen in patients who suffer from a neurological disease like dementia. pic.twitter.com/WpjErGaS96

To take on President Trump in November – in the midst of a potentially (some would say unavoidably) serious coronavirus outbreak blanketing the country.

Bloomber’s new group – which has yet to disclose its name while it’s in teh trademark application process – will absorb hundreds of the billionaire’s presidential campaign staffers in six swing states.

One major hurdle is the fact that Bloomberg’s ‘meme team’ is the best money can buy, and they’re still not funny.

Bloomberg’s meme team is sure to do wonders for Joe Biden.

“I’ve always believed that defeating Donald Trump starts with uniting behind the candidate with the best shot to do it,” Bloomberg said Wednesday after suffering a staggering defeat during Super Tuesday. “After yesterday’s vote, it is clear that candidate is my friend and a great American, Joe Biden.”

Bernie Sanders’s advisers, meanwhile, say they want no help from Bloomberg’s crack team of electioneers.

Bloomberg’s advisers have identified Wisconsin, Michigan, Pennsylvania, Arizona, Florida and North Carolina as the six states that will decide the electoral college winner this year. Staffers in each of those states have signed contracts through November to work on the effort.

The new group also could serve as a vehicle for Bloomberg to support Democratic candidates for the House and Senate. In 2018, Bloomberg gave $20 million to Senate Majority PAC to support Democratic senatorial candidates. A separate group he founded, Independence USA, spent $38 million to help Democrats retake the U.S. House. –Washington Post

In addition to Bloomberg’s new organization, he will continue to fund Hawkfish – a political data company which is supporting Democratic campaigns, according to a person familiar with the discussions. The company has signed a long-term lease in the same building in Times Square which has been home to Bloomberg’s presidential campaign.

Suppose that a government has a trillion dollars that it wishes to use to subsidize private spending toward some objective. For example, it might want to launch a massive campaign against the spread of COVID-19. There might be many ways to spend the money, on items large and small–say, research, education, salary for sick people who skip work, quarantine centers, ventilators, hand soap, and so on. The government could create a large administrative agency, writing rules about who is entitled to government checks and performing claim adjudication. But it would be challenging to scale such an agency even under the best of circumstances to handle processing of tens of millions of claims. The challenge is especially acute if we assume that the core goal is difficult to translate into rules, for example because a large number of factors are relevant to assessing the social utility of particular spending projects. If the process is to be governed by standards, there will be inconsistency based on who makes the decision.

In a new article, I describe and defend a novel approach that the government can use to distribute money at scale, without creation of a large bureaucracy and without enacting extensive rules. The paper provides applications focused on climate change rather than on COVID-19, but the approach can be applied to any massive governmental spending program. Here’s how it would work: Anyone who claims to have contributed to the specified goal could file a claim. To discourage frivolous claims, a small fee might be applied. Rights to payment on claims could be sold. The government would commit to randomly select a small number of claims, say 1,000. An agency would then estimate social benefits produced for each of these claims, using panels of multiple decisionmakers and considering expert evidence where appropriate. It would then distribute the entire trillion dollars to the claims’ owners, in proportion to the measurement of social value for the corresponding claims.

Because claims are transferable and only a tiny percentage of claims will be eligible for reimbursement, intermediaries would aggregate diverse portfolios of claims. This will allow intermediaries to bear the risk associated both with the random selection of only a small percentage of claims and with the unpredictability of the government’s assessment of claims randomly selected. An intermediary will pay more for a claim that it expects will be worth more on average, if randomly selected for consideration. A claim is thus worth what it will fetch in the market. An individual or entity might perform actions to meet the government’s objective and then create a claim, or it might sell a claim via a contract in which it promises the intermediary that it will invest the money provided by the intermediary in a particular way.

The principal virtue of the system is that it requires very little bureaucratic infrastructure, even if the government is distributing an enormous sum of money to a very large pool of claimants. All the government needs to do is randomly select a very small number of claims and perform adjudications where it estimates the associated social benefits. Moreover, the government need not create detailed rules. The adjudications can be based on a vague standard, such as “estimated social benefits in reducing the spread of COVID-19.” Use of a standard means that there will be uncertainty, and this is the primary drawback of the system. But diversified intermediaries can bear the risk of that uncertainty relatively cheaply. Standards should be much more tolerable than in a typical administrative regime, because uncertainty will not impose risk on regulated individuals (who may offload the risk onto intermediaries), and because uncertainty will not increase adjudication costs (because the same number of claims will be adjudicated regardless of the total number filed). As usual, a standard avoids the overinclusiveness and underinclusiveness of rules, thus reducing the danger that funds will be spent inefficiently.

My claim is not that this system is necessarily better than traditional approaches to distributing government funds. My claim is simply that this is a new approach and that it might have advantages in certain contexts. Whether this makes sense for COVID-19 prevention or for any other application depends on how good a job one thinks the government can do with a more traditional, centralized system for spending money directly or choosing private projects to receive government money. This evaluation depends in part on whether one believes that the government can make its assessments relatively free of political considerations, and in part on how expensive it will be for the government to make these determinations. A more traditional system will be preferable when there are relatively few claims so achieving scale is not an issue, and when the purposes of the program can be efficiently translated into rules.

Emergency spending (whether of a trillion dollars or a mere eight billion) is potentially a good application of the market-based approach, because the government may not be equipped to make large numbers of high quality decisions extremely quickly. Eventually, government decisionmakers will need to evaluate spending in a few cases, and bad decisions ex post are possible. The system’s performance, however, must be evaluated not based on the actual ex post valuations that the agency will produce, but on the market’s ex ante expectations of these ex post valuations. Even if the agency is likely to make many errors ex post, the ex ante expectations might track social value reasonably well. The market process itself will impose costs, as intermediaries will seek to make a profit, but competition will tend to reduce these by driving up the amount that intermediaries offer. Because intermediaries do not need to provide due process, their costs of assessing claims may be less than the costs of relatively formal governmental adjudicative processes. Even if the government is slow, claimants will be able to receive payment quickly from intermediaries, instead of queuing while awaiting administrative determinations.

The law review article describes the functioning of the market and of the government agency in much more detail and responds to objections. I’ll look at the comments for the strongest and most recurrent objections and will address these in a subsequent post.

from Latest – Reason.com https://ift.tt/3axPOaM

via IFTTT

A new study from the American Petroleum Institute (API), with modeling data provided by the consulting firm OnLocation, details how a nationwide ban on hydraulic fracturing (colloquially known as “fracking”) could trigger a recession, would seriously damage U.S. economic and industrial output, considerably increase household energy costs, and make life much harder and costlier for American farmers.

In America’s Progress at Risk: An Economic Analysis of a Ban on Fracking and Federal Leasing for Natural Gas and Oil Development, API argues that a fracking ban would lead to a cumulative loss in gross domestic product (GDP) of $7.1 trillion by 2030, including $1.2 trillion in 2022 alone. Per capita GDP would also decline by $3,500 in 2022, with an annual average decline of $1,950 through 2030. Annual household income would also decline by $5,040.

In 2022 alone, 7.5 million jobs would be lost (almost 5 percent of the U.S. total workforce), while annual job losses would average roughly 3.8 million through 2030. More than 3.6 million jobs would be lost in five states alone in 2022: 1.103 million in Texas, 765,000 in California, 711,000 in Florida, 551,000 in Pennsylvania, and 500,000 in Ohio. States with the highest job losses as a share of overall employment would be North Dakota (76,000), Oklahoma (319,000), New Mexico (149,000), Wyoming (48,000), Louisiana (321,000), West Virginia (109,000), Kansas (208,000), and Colorado (353,000).

Household energy costs would also increase significantly, 14 percent by 2030, even though household energy use is projected to decline by 12 percent. American families would see, on average, a $618 annual increase in their energy costs, as electricity prices would rise by, on average, 20 percent annually. Gasoline prices would also increase by 15 percent.

Farm incomes would decline by 43 percent, with a cumulative loss in farm income of $275 billion, or more than $25 billion on average annually. The costs of wheat farming would increase by 64 percent, while corn farming costs would increase by 54 percent and the costs of soybean farming would increase by 48 percent.

This is not the only recent study to highlight the immense economic costs of a ban on hydraulic fracturing. A report released in November 2019 by the U.S. Chamber of Commerce’s Global Energy Institute concludes a ban would eliminate 19 million jobs through 2025 and reduce GDP by $7.1 trillion. The report also estimates household incomes would be reduced by $3.7 trillion by 2025. Consumers would be paying $5,661 more per capita for energy and goods and services thanks to a doubling of gasoline prices and a 324 percent increase in the price of natural gas over that same time period.

The fracking revolution of the past dozen years has considerably spurred economic development throughout the United States. According to the Federal Reserve Bank of Dallas, the shale industry alone drove 10 percent of U.S. GDP from 2010 to 2015. In 2018, according to the National Bureau of Economic Research, oil and gas extraction accounted for $218 billion of U.S. economic output.

A September 2019 report conducted by Kleinhenz & Associates for the Ohio Oil and Gas Energy Education Program shows increased oil and natural gas production from fracking has saved American consumers $1.1 trillion in the decade from 2008 to 2018. This breaks down to more than $900 in annual savings to each American family, or $9,000 in cumulative savings.

Meanwhile, the White House Council of Economic Advisors estimated in October 2019 that fracking saves American families $203 billion annually on gasoline and electricity bills, roughly $2,500 per family. For low-income families, who spend the largest share of their income on energy costs, these savings are very significant. For those families in the lowest income quintile, it represents a savings of 6.8 percent of their total income.

Hydraulic fracturing activity delivers $1,300 to $1,900 in annual benefits to local households, including “a 7 percent increase in average income, driven by rises in wages and royalty payments, a 10 percent increase in employment, and a 6 percent increase in housing prices,” according to a December 2016 study conducted by researchers at the University of Chicago, Princeton University, and the Massachusetts Institute of Technology.

Another study published in the American Economic Review in April 2017 found “each million dollars of new [oil and gas] production produces $80,000 in wage income and $132,000 in royalty and business income within a county. Within 100 miles, one million dollars of new production generates $257,000 in wages and $286,000 in royalty and business income.”

Hydraulic fracturing enables the cost-effective extraction of once-inaccessible oil and natural gas deposits. These energy sources are abundant, inexpensive, environmentally safe, and can ensure the United States remains a leading energy producer for years to come. Therefore, policymakers across the country should refrain from considering any sort of fracking ban or moratorium, while also making sure not to place unnecessary burdens on the natural gas and oil industries, which are safe and positively impact their states’ economies.

Suppose that a government has a trillion dollars that it wishes to use to subsidize private spending toward some objective. For example, it might want to launch a massive campaign against the spread of COVID-19. There might be many ways to spend the money, on items large and small–say, research, education, salary for sick people who skip work, quarantine centers, ventilators, hand soap, and so on. The government could create a large administrative agency, writing rules about who is entitled to government checks and performing claim adjudication. But it would be challenging to scale such an agency even under the best of circumstances to handle processing of tens of millions of claims. The challenge is especially acute if we assume that the core goal is difficult to translate into rules, for example because a large number of factors are relevant to assessing the social utility of particular spending projects. If the process is to be governed by standards, there will be inconsistency based on who makes the decision.

In a new article, I describe and defend a novel approach that the government can use to distribute money at scale, without creation of a large bureaucracy and without enacting extensive rules. The paper provides applications focused on climate change rather than on COVID-19, but the approach can be applied to any massive governmental spending program. Here’s how it would work: Anyone who claims to have contributed to the specified goal could file a claim. To discourage frivolous claims, a small fee might be applied. Rights to payment on claims could be sold. The government would commit to randomly select a small number of claims, say 1,000. An agency would then estimate social benefits produced for each of these claims, using panels of multiple decisionmakers and considering expert evidence where appropriate. It would then distribute the entire trillion dollars to the claims’ owners, in proportion to the measurement of social value for the corresponding claims.

Because claims are transferable and only a tiny percentage of claims will be eligible for reimbursement, intermediaries would aggregate diverse portfolios of claims. This will allow intermediaries to bear the risk associated both with the random selection of only a small percentage of claims and with the unpredictability of the government’s assessment of claims randomly selected. An intermediary will pay more for a claim that it expects will be worth more on average, if randomly selected for consideration. A claim is thus worth what it will fetch in the market. An individual or entity might perform actions to meet the government’s objective and then create a claim, or it might sell a claim via a contract in which it promises the intermediary that it will invest the money provided by the intermediary in a particular way.

The principal virtue of the system is that it requires very little bureaucratic infrastructure, even if the government is distributing an enormous sum of money to a very large pool of claimants. All the government needs to do is randomly select a very small number of claims and perform adjudications where it estimates the associated social benefits. Moreover, the government need not create detailed rules. The adjudications can be based on a vague standard, such as “estimated social benefits in reducing the spread of COVID-19.” Use of a standard means that there will be uncertainty, and this is the primary drawback of the system. But diversified intermediaries can bear the risk of that uncertainty relatively cheaply. Standards should be much more tolerable than in a typical administrative regime, because uncertainty will not impose risk on regulated individuals (who may offload the risk onto intermediaries), and because uncertainty will not increase adjudication costs (because the same number of claims will be adjudicated regardless of the total number filed). As usual, a standard avoids the overinclusiveness and underinclusiveness of rules, thus reducing the danger that funds will be spent inefficiently.

My claim is not that this system is necessarily better than traditional approaches to distributing government funds. My claim is simply that this is a new approach and that it might have advantages in certain contexts. Whether this makes sense for COVID-19 prevention or for any other application depends on how good a job one thinks the government can do with a more traditional, centralized system for spending money directly or choosing private projects to receive government money. This evaluation depends in part on whether one believes that the government can make its assessments relatively free of political considerations, and in part on how expensive it will be for the government to make these determinations. A more traditional system will be preferable when there are relatively few claims so achieving scale is not an issue, and when the purposes of the program can be efficiently translated into rules.

Emergency spending (whether of a trillion dollars or a mere eight billion) is potentially a good application of the market-based approach, because the government may not be equipped to make large numbers of high quality decisions extremely quickly. Eventually, government decisionmakers will need to evaluate spending in a few cases, and bad decisions ex post are possible. The system’s performance, however, must be evaluated not based on the actual ex post valuations that the agency will produce, but on the market’s ex ante expectations of these ex post valuations. Even if the agency is likely to make many errors ex post, the ex ante expectations might track social value reasonably well. The market process itself will impose costs, as intermediaries will seek to make a profit, but competition will tend to reduce these by driving up the amount that intermediaries offer. Because intermediaries do not need to provide due process, their costs of assessing claims may be less than the costs of relatively formal governmental adjudicative processes. Even if the government is slow, claimants will be able to receive payment quickly from intermediaries, instead of queuing while awaiting administrative determinations.

The law review article describes the functioning of the market and of the government agency in much more detail and responds to objections. I’ll look at the comments for the strongest and most recurrent objections and will address these in a subsequent post.

from Latest – Reason.com https://ift.tt/3axPOaM

via IFTTT

Lebanon Prosecutor Freezes Assets Of 20 Banks After $2.3BN In ‘Illegal’ Transfers

Lebanon’s state news agency NNA said on Thursday the country’s top financial prosecutor has moved to freeze the assets of 20 Lebanese banks, including the property of the bank chiefs and boards.

Heightened security outside the entrance of the Association of Banks in downtown Beirut. File image via Reuters.

“Judge Ali Ibrahim decided to freeze the assets of twenty Lebanese banks. He also imposed a freeze on the assets of the heads and members of boards of directors of these banks,” state-run NNA said.

It comes amid a broader ongoing probe into the alleged illegal transfer of some $2.4 billion overseas and the recent sale of Eurobonds to foreign funds. Fourteen bankers are reportedly under scrutiny as the Lebanese economy teeters on the brink of collapse, and crucially with a March 9 deadline looming for repayment of $1.2 billion in Eurobonds.

Bloomberg lists some among Lebanon’s biggest lenders including “Bank Audi, Fransabank, Blom Bank and the Lebanese unit of Societe General” under investigation.

And further “The prosecutor also questioned the head of the Association of Banks in Lebanon, Salim Sfeir, who is also chairman of Bank of Beirut,” according to the report.

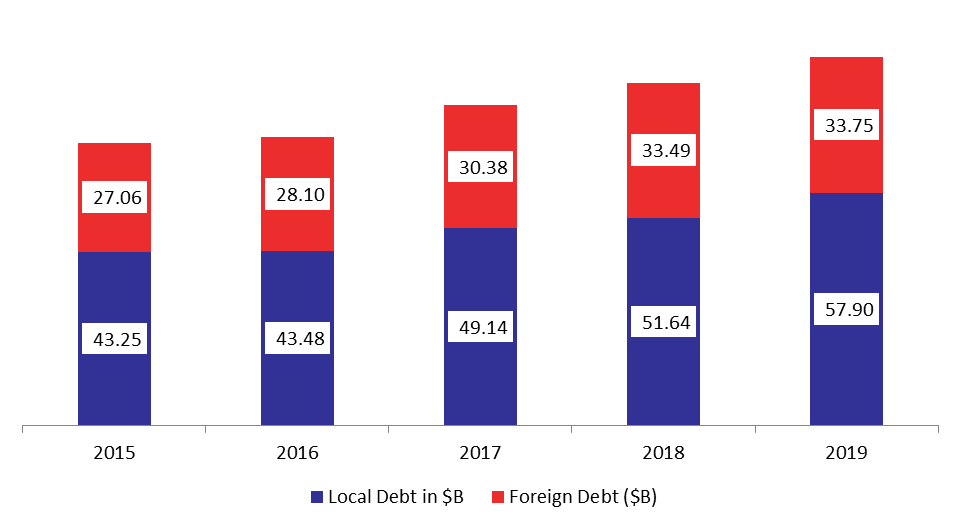

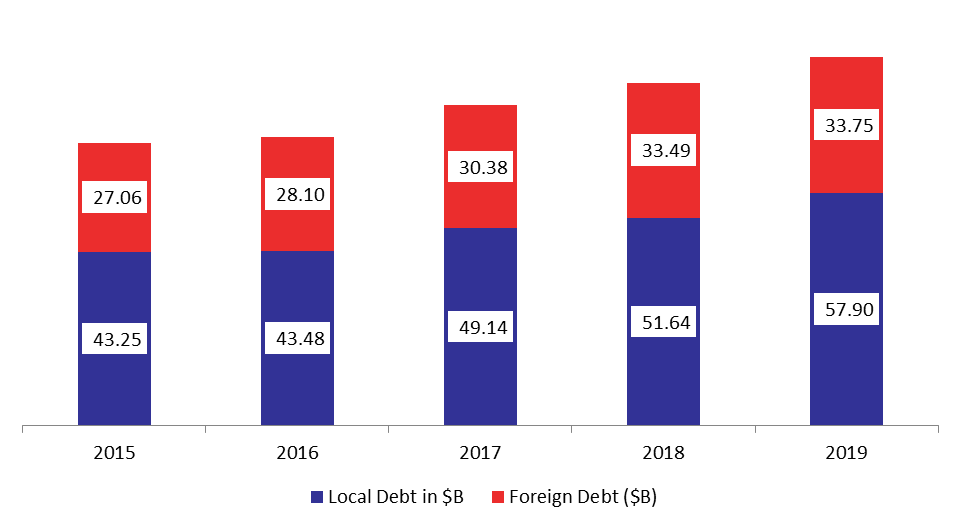

Chart: In Billions$. Source: Lebanon’s Ministry of Finance (MoF)/Blominvest, Blom Bank Group Research

The government charges that bankers are actively thwarting attempts to restructure the country’s debt, while the banks say they needed cash to meet demand of patrons for basic staples including wheat, fuel and medicines amid the ongoing liquidity crisis.

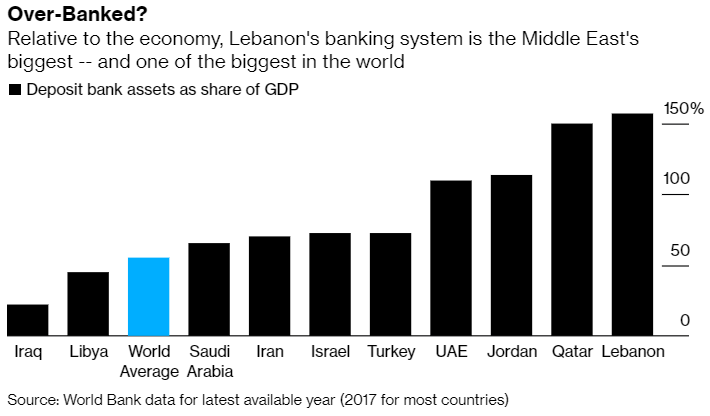

The Institute of International Finance (IIF) now lists Lebanon as having among the highest debt-to-gross domestic product ratios in the world at 166%.

Chart via Bloomberg: “Relative to the economy, Lebanon’s banking system is the Middle East’s biggest — and one of the biggest in the world.”

This after its public debt increased by an annual 7.6% to $91.64 billion at the close of 2019.

Over the past number of months the country has seen repeat intermittent bank closures, also as banks have blocked most transfers abroad for their clients, and maintained tight controls over hard-currency withdrawals, policies which have in many instances led to riots and reports of threats against bank staff.

The Texas Attorney General is often criticized for forum shopping–that is, filing cases in specific courts where there is a high probability of drawing a specific judge. This criticism is unwarranted. All lawyers forum shop–even government lawyers. Attorneys who fail to secure the best venue for their client engage in legal malpractice. If you represent a Plaintiff, you generally want to be in state court. And if you represent a Defendant, you generally want to be in a federal court. If you represent a criminal defendant, and can file a valid motion for change of venue, you should do so.

Generally, in large cities, where several judges sit on a given bench, it is impossible for Plaintiffs to pick and choose which judge they get. But in smaller cities, specific divisions may have one or two judges. By choosing from among many single-member divisions, lawyers can, in some cases, choose what judge or judges take their case.

Advocacy groups understand have long understood this point. I recently visited the federal district courthouse in Montgomery, Alabama. The building is named after Judge Frank M. Johnson. The legendary Eisenhower appointee issued many important civil rights rulings. The New York Times listed several of the cases in his obituary:

In a career that spanned almost four decades—24 years in Federal District Court in Alabama and 13 years on an appeals court with wide jurisdiction in the South—Judge Johnson ordered the desegregation of public schools and colleges, parks, libraries, museums, depots, airports, restaurants, restrooms and other public places, as well as the Alabama State Police.

In 1965 he issued another historic order that allowed Dr. King to lead a 52-mile march from Selma to Montgomery to protest the denial of black voting rights. He did so after Alabama troopers clubbed marchers and used tear gas in a spectacle witnessed on television by a horrified nation, and after President Lyndon B. Johnson federalized the Alabama National Guard to protect the marchers.

For some time, Judge Johnson was the only federal judge in Montgomery. Plaintiffs who filed suit in Montgomery had a 100% chance of drawing Judge Johnson. Why did the Plaintiffs file suit in Montgomery (the terminus of the march) rather than in Selma (the origin of the march)? A lawyer in Montgomery told me that civil rights groups forum shopped, and directed the case to Judge Johnson’s docket. As they should have.

In Unprecedented, I discussed how the Florida Attorney General filed suit against the ACA in Pensacola, rather than Tallahassee (the state capital), to avoid a specific judge on that bench.

The Attorney General’s office is located in Tallahassee, which is situated in the Northern District of Florida. This court had divisions in Pensacola, Gainesville, and Tallahassee. Attorney General McCollum decided against filing in Tallahassee because he and his staff had grown “very frustrated” with that court’s chief judge, Robert Lewis Hinkle, who was appointed by President Clinton in 1996.

If the action was filed in Tallahassee, McCollum thought that Hinkle could assign the case to whomever he wanted. Under the local practice, a case filed in Gainesville could be pulled to Tallahassee. A senior attorney in the office told me that McCollum, concerned with how this big and political case “might be handled before Hinkle,” decided that filing in Pensacola would be ideal.

One attorney said that McCollum “knows his benches,” but said it was “horseshit” that the attorney general picked Pensacola based on the political affiliation of the judges. But in response to a question about the affiliations of the judges, another lawyer from Florida told me, coyly, “We knew where judges come from.” Be that as it may, the three judges in Pensacola had been appointed by Republican presidents. Judge Margaret Rodgers was appointed by President George W. Bush in 2003. Judge Lacey Collier was appointed by President George H. W. Bush in 1991. And most importantly, Judge Roger Vinson was appointed by President Ronald Reagan in 1983. The case was assigned to Judge Vinson.

Forum shopping, on the left and the right, is possible in just about any state. Even Texas! Today, Perkins Coie filed a suit on behalf of Sylvania Bruni, the Texas Democratic Party, the Democratic Senatorial Campaign Committee, and the Democratic Congressional Campaign Committee. The complaint challenges Texas’s decision to repeal “straight-ticket” voting. The defendant was the Texas Secretary of State. Was the complaint filed in the Western District of Texas in Austin, where the Secretary of State resides, and where the Texas Democratic Party is also located? Seems like a convenient venue. Indeed, the firm filed at least two other election cases against the Secretary of State in that division (Gilby v. Hughs and Miller v. Hughs).

No, they did not choose Austin. Instead the suit was filed in the Southern District of Texas, Laredo Division. Why did they choose that border-town, which is a four-hour drive from Austin?

Sylvia Bruni, the named plaintiff, is “Chair of the Webb County Democratic Party, the countywide organization representing Democratic candidates and voters throughout Webb County.” Laredo is in Webb County. Texas has 254 counties. At quick glance, the Texas Democratic Party has a chair for most, if not all counties. Of all the counties in Texas, why did the Plaintiffs choose Webb County?

I can offer a guess. By my count, the Laredo Division is the only division in the Southern District of Texas where there is a 0% chance of drawing a Republican-appointed judge. In contrast, the bench in Western District in Austin has appointees from several Presidents. This practice is not new in Texas. Several years ago, a string of prominent voting-rights case were filed in the Corpus Christi division and not in the state capital. At the time, there was a 0% chance of drawing a Republican-appointed judge.

As a general rule, when a party files a suit in a specific division, and there is no necessary connection to that division, I presume the Plaintiffs shopped for an ideal forum. And there is nothing wrong with that decision.

Law students, weaned on Erie, are lead to believe forum shopping is bad. No way. Forum shopping is entirely rational. To the extent a problem exists, Congress can eliminate single-judge districts. Or in case of single-judge districts, a certain percentage of cases can be assigned, at random, to judges elsewhere in the division, and not just the Chief Judge, as is now the practice in the Northern District of Texas, Wichita Falls Division. But don’t blame the lawyers.

from Latest – Reason.com https://ift.tt/2xeFO7X

via IFTTT

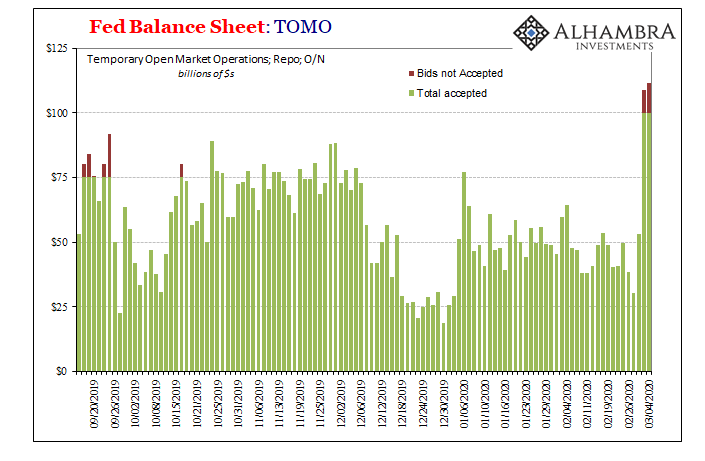

Taking another look at what I wrote about repo and the latest developments yesterday, it may be worthwhile to spend some additional time on the “why” as it pertains to so much determined official blindness, an unshakeable devotion to otherwise easily explained lunar events.

The short version: monetary authorities as well as the “experts” describe almost perfectly risk averse behavior among the central money dealing system in outbreaks like September’s repo – but then bend over backward trying to come up with any other kind of explanation for it. The problem must be some complicated stew of otherwise benign technical issues because there’s no possible way, they tell themselves, it can be anything else. Not with bank reserves abundantly over a trillion (now rising again) and Jay Powell pleasantly whispering in their ears about the unemployment rate every other day.

It takes on religious, cult-like properties to try so hard to prove (to themselves) what has already been so thoroughly disproven.

Start with the bond market and interest rates. Over the last half decade or so, ever since Janet Yellen’s ill-advised first rate hike in December 2015 amidst a near recession, a move she immediately regretted, central bankers and Bond Kings have been on a mission to convince the world monetary policy was a tremendous success. It had to have been because it was the biggest thing ever devised and those devising it had promised it was so big the flood of “easing” couldn’t possibly fail.

Something about a printing press.

Anyway, that’s not logic so much as self-delusion and rationalizing; the fallacy of sunk costs. Rather than recognize all the warning signs that it all had indeed failed, policymakers and Economists instead convinced themselves it just needed more time.

Except, by 2015 and 2016 time was running out (see: Trump, Donald, and Britain, exit). People were growing anxious as even politicians like President Obama had exhausted what had been a deep reservoir of patience (thus, his June 2016 comment about a manufacturing “magic wand”).

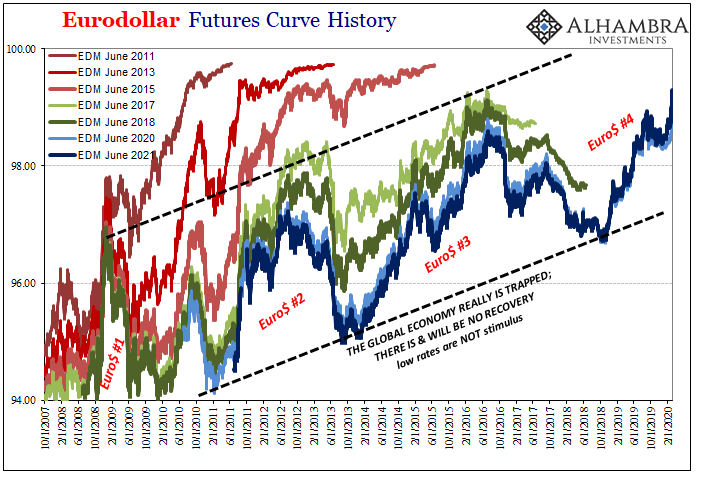

Along came 2017 and Reflation #3 – just in time to be hyped into that very mode of success all officialdom had been waiting on. President Trump was only too happy to take credit. It was given a catchy name, globally synchronized growth, and described in the most emphatic of terms. The game changer had arrived, the final end to what had by then been far too many years of lethargy and uncertainty.

What that would’ve meant for the bond market was clear: an explosion in yields. The combination of risky opportunities (recovery), the end of macro slack (inflation), and a resolute central bank aggressively trying to keep it all within bounds (hawkishness) would lead to the BOND ROUT!!!!

It never happened. Nope. Not even when yields were rising, as I wrote in March 2018 amidst what had been true hysteria:

No, when they call for an end to the 30-year bond bull market (though there is no such thing as a bond bull market) they are claiming the reverse to March 2008; a paradigm shift of near or equal potency. An end to the crisis at long last.

The problem with such an idea is that it just doesn’t appear anywhere. Markets have been trading on mild “reflation” sentiment, that’s it. And there really isn’t much conviction behind it, either.

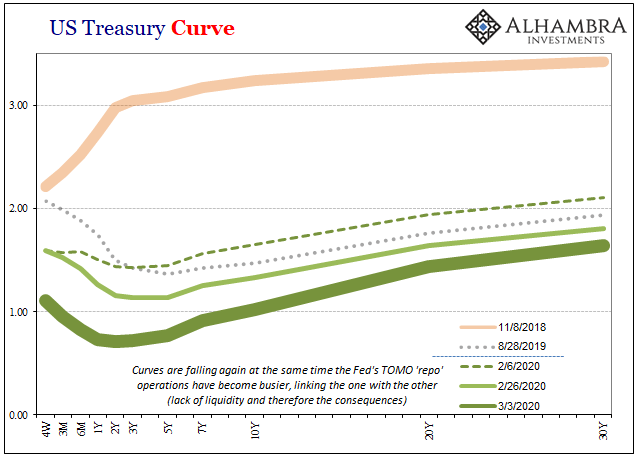

The curves uniformly said that the game changer scenario just wasn’t playing out. By flattening where they did, around 3% nominal, it was a very clear signal that something was still wrong. The same thing that had been wrong the entire time since August 2007.

But, since central bankers had so much riding on a positive outcome, they reversed engineered persistently low bond yields into something they could spin as consistent with globally synchronized growth and the tremendously optimistic factors behind the BOND ROUT!!!!

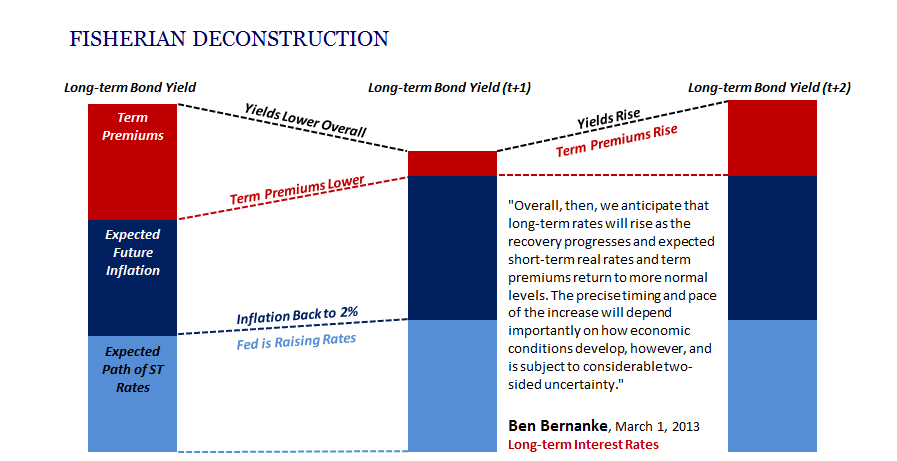

According to the conventional theory, since yields weren’t actually rising in the manner they “should” have been the only way to decompose them without disproving the whole game was to claim, without outside corroboration, by subjective statistical modeling only, inflation expectations really were rising, that the bond market really was figuring on much higher short-term money rates due to rate hikes, but that it was also experiencing some revelation of past forward guidance (mostly Delphic, but maybe some Odyessean, too) which only in an Economist’s mind can be priced out as a negative term premium.

Common sense dictated that low and, since November 2018, falling yields would have been the product of persistently low and falling inflation expectations plus persistently low and falling future short-term rates. Term premiums simply wouldn’t factor – unless you are desperately trying to accomplish some other goal than honest analysis.

The thing is, as I pointed out last August as the shockingly “unexpected” drop in yields was happening, we have markets for both of those yield components. They tell us within all reasonable standards what yields are made of. And it wasn’t falling term premiums.

The reason it has to be term premiums is because Bernanke, Janet Yellen, or Jay Powell all say inflation is going to rise and so will short-term interest rates. Guaranteed. Take it to the bank. The Fed will therefore be hiking short-term rates and since they don’t believe the bond market would ever, ever disagree with them, process of elimination, it therefore must be term premiums that are causing yields to fall (when these same people say they should be rising).

Even last August, when the yield curve was at its most public (other than now), these people continued to talk about negative term premiums (related, of course, to R*) seriously. No matter how much and many events go against them, they never, ever change their view. Again going back to what I wrote in March 2018:

March 2008 was a very long time ago, and the technocrats have been repeatedly predicting its mirror positive image almost every year since. Having surpassed a decade now, there is religious fervor about it. It doesn’t matter how much the yield curve collapses on the narrative (the long end, even as it rises somewhat in nominal terms, continues its stubborn and obvious resistance against the idea), the BOND ROUT!!! like actual inflation is certain for tomorrow.

Interest rates have nowhere to go but up no matter how low they keep going. The bond market, like repo problems, are all dissected from this other, deeply unscientific perspective. Central bankers start, not end, with the premise that the world is fixed and awesome – and then seek to validate this predetermined conclusion.

But, because it is a faulty and ultimately incorrect conclusion, it takes some real mental gymnastics and tortured logic to get back to it. Repo is nothing more than technical factors. Falling bond yields are really a good sign, even more negative term premiums. The BOND ROUT!!!! is still penciled in for tomorrow.

A growing chorus of strategists and money managers is voicing concern as investors charge into government debt at seemingly any price.

The fear is they’re exposing themselves to interest rate risk like never before, risking a precipitous slump on even a modest bump in yields. One breakthrough in the fight against the illness, or a sign the global economy is recovering faster-than-expected, might be all it takes.

That wasn’t written in March 2018 nor March 2019. It was published yesterday, of all days. And here’s the kicker, “The moves highlight belief in some corners that policy action will stoke growth, creating upward pressure for stocks and bond yields.”

Even now, after the clunker that was Powell’s unscheduled fifty, after last year’s three rate cuts that no one bothers to remember, the myth of monetary potency remains imagined as the godhead of the maestro’s legacy. No matter how many times all its central tenets disproven, the cult remains stocked with true believers.

These people – central bankers, Bond Kings, Economists, repo experts – they all claim that because the moon is an ages-old symbol of the nighttime that when it suddenly appears in the sky during the day, as happens, that when it does daytime is actually night. The fact that no one has any lights on is explained by technical factors like some imagined, regression-deduced shortage of light bulbs rather than the obviousness of the real time of day. The Fed moves to renew its abundant light bulb policy rather than recognize and adjust its clock.

Moon = night. QE = success.

So steadfastly convinced that the moon must only be a nighttime phenomenon, repo has to be technical factors rather than the more obvious risk aversion behavior. Low interest rates have to be negative term premiums (how negative will term premiums have to be if, really when, nominal yields are themselves?) instead of the deepest, most sophisticated combination of markets in human history describing, point blank, rapidly rising liquidity risks and the long run consequences of them.

Thus, nothing changes. Nothing did in 2017, that’s for sure. It’s all just the same broken system. That alone is why there was never a BOND ROUT!!! as well as why there won’t be. All these things go hand in hand; broken repo and low yields, risk aversion and the lack of inflationary acceleration.

If it wasn’t for this Greenspan Moon Cult these problems might’ve been solved, at least properly recognized, a long time ago.

{kind=link}

{kind=link}