On Wednesday, Starbucks Executive Vice President Rossann Williams published an open letter detailing a number of steps the company was taking to prevent the transmission of COVID-19, the disease caused by the new coronavirus, including a temporary suspension of their use of reusable cups in stores.

“The health and well-being of our partners and customers remains top of mind and our highest priority,” said Williams, saying that “we are pausing the use of personal cups and ‘for here’ ware in our stores.

Customers who arrive with their own, potentially infected coffee cups, or who ask for a reusable “for here” mug will still receive the existing 10 cent discount Starbucks offers. They will, however, have to make do with a single-use cup until this current pandemic dies down.

Williams announced a slew of other measures to combat coronavirus, including stepped-up cleaning and sanitation, postponing large company meetings, and restricting company travel.

“We are optimistic this will be a temporary situation,” said Williams in her letter.

The company’s announcement highlights one of the often-overlooked benefits of single-use items: they’re clean. Once you are done using it, you can throw it away, in a landfill maybe. Reusable items, by contrast, leave open the possibility that contaminants from the last thing or person the item came in contact with will be passed on to the next user.

Already we rely on single-use condoms and surgical gloves to prevent the spread of all sorts of diseases and infections. In the context of a quickly spreading pandemic, single-use cups and straws also have their role to play.

from Latest – Reason.com https://ift.tt/3cxQ7UI

via IFTTT

The coronavirus is now exposing a far more deadly disease: Namely, the poisonous brew of easy money, cheap debt, sweeping financialization and unbridled speculation that has been injected into the American economy by the Fed and Washington politicians.

It has turned Wall Street into a dangerous gambling casino while leaving Main Street buried under mountainous debts, faltering investment in growth and productivity and the hand-to-mouth economics of spending more than you earn.

It has also left the American economy exceedingly vulnerable to external shocks. That’s because 80% of households have no appreciable rainy day funds and businesses have hollowed out their balance sheets and artificially extended their supply chains to the four corners of the earth in order to goose short-run profits and share prices.

However, this unprecedented fragility is becoming evident as public health authorities around the world aggressively move to contain the Covid-19 contagion. This will mean separating workers from their workplaces, consumers from the malls, diners from the restaurants, travelers from the airlines, hotels and resorts and much more like and similar disruptions to the supply-side of the economy.

In short, the world’s supply chains are buckling and freezing-up, thereby causing production and incomes to fall abruptly. In turn, shrunken incomes and cash flows will pull the legs out from under the edifice of debt and speculation that has been piled atop the American economy.

So both a renewed financial and economic crisis and an abrupt change of course lie dead ahead. The 30-year era of False Prosperity is over.

Accordingly, the Turbulent Twenties have begun. This will be a decade when the chickens come home to roost. It will be a time when the cans of delay and denial may no longer be kicked down the road to tomorrow.

To the contrary, the 2020s will mark an era when today’s economic and political fantasies are crushed by America’s accumulated due bills.

Bubbles will be burst. Speculators will get carried out on their shields. Easy money wealth will evaporate. Fiscal trauma will ensue. The national joy ride will end.

The decade of reckoning that lies ahead is rooted first and foremost in the fecklessly incurred mega-debts of the private and public sectors alike. Together they have soared to the staggering sum of $75 trillion.

That’s 5X more than the $14 trillion outstanding three decades ago.

Yet the proceeds from these massive borrowings were not used to invest and provide for tomorrow, but to live high on the hog today. After three decades of such artificial debt-fueled “prosperity”, the very warp and woof of American society has been deformed.

For example, eighty percent of U.S. households live essentially hand-to-mouth. But that’s not because they are naturally imprudent; it’s because they have been incentivized to borrow and spend, while being punished for saving and setting aside for life’s unforeseen contingencies and setbacks.

Likewise, the C-suites of corporate America have been rewarded for strip-mining their balance sheets and cash flows in order to pump money into Wall Street for stock buybacks and M&A.

But this has caused investment in productive plant, equipment, technology and human resources to be shortchanged. Consequently, the growth capacity of the main street economy has been progressively eviscerated.

And most especially, the public sector has been fiscally ruined.

During the 32-years since Alan Greenspan launched the present era of reckless and relentless monetization of the public debt in 1987, there have been only four balanced budgets sandwiched between 28 years of sheer fiscal promiscuity.

That has already taken the Federal debt from $3 trillion to $23 trillion, and it’s now heading, inexorably, toward $43 trillion by the end of the 2020s. The public debt-to-GDP ratio will then reach a Greek-style 150%.

Worse still, the nation’s political system studiously ignores this obvious fiscal malignancy. That’s because the Fed and other central banks have removed the sting of rising interest rates and the “crowding out” of private investment.

So politicians have succumbed to the latest version of free lunch economics.

This has permitted, in turn, national governance to degenerate into bitter partisan warfare that has festered so long that it now threatens the very future of constitutional government.

Rather than facing tough policy choices, the Dems have retreated into identity politics and sanctimonious racialist moralizing. They’ve abandoned virtuous pursuit of the public good for cheap virtue signaling to their base.

Likewise, the GOP has prioritized building border walls and keeping people out of America’s historic melting pot on the fear they might not vote Republican. But in feeding red meat to their political base, they’ve abandoned the GOP’s real job—functioning as watchdog of the treasury and guardian of sound money.

Beyond the water’s edge, the bipartisan duopoly has immersed itself in the projects of Empire and pretensions to being the world’s indispensable nation and global gendarme. So doing, it has actually undermined homeland security while saddling the nation with trillions of debt to fund Forever Wars that are illegal, immoral and pointless.

These perversions of governance ultimately resulted in the freakish 2016 election in which the GOP accidentally nominated a bombastic outsider—a Great Disrupter who had not been house-trained by the Washington establishment.

Yet the very prospect of a Trump presidency caused the incumbent Dems to baldly and illegally deploy the surveillance tools of the national security apparatus to detour his candidacy. And then to attempt to abort his presidency via the RussiaGate and UkraineGate/Impeachment hoaxes once the voters had spoken.

At the same time, even as the Donald has brashly and pugnaciously fought the unconstitutional coup against his presidency, he, too, has gone about the business of filling the Swamp even deeper, rather than draining it as he promised on the campaign trail.

In fact, the Federal Leviathan—including its national security branch—has never been bigger, fatter and more wasteful than under Trump.

The Donald has increased Federal spending in constant dollars (2019 $) by $180 billion per year during his term to date. That compares to $120 billion per year under George Bush the Younger, $80 billion under Obama and $40 billion per year under Clinton.

So there isn’t anything which resembles MAGA coming down the pike during the 2020s and beyond. Trump has only made the inherited trend of soaring debts and diminishing growth measurably worse with his four-pronged assault on sound economics.

Trade Wars. Border Wars. Fiscal Debauchery. Easy Money attacks on the Fed.

These are not the route to MAGA. They are the path to bigger government in Washington, dangerous bubbles on Wall Street and diminished prosperity, opportunity and liberty on Main Street.

Accordingly, it is now way too late for a stick save from either political party or any state institution bivouacked in the Imperial City. And that especially includes the madcap money printers at the Federal Reserve.

The fact is, the engines of free market capitalism have been corroded and paralyzed by three decades of bad money and bad policy.

What has passed for “recovery” since the Great Recession has been only a temporary debt-fostered reprieve. Likewise, the soaring stock market reflects the greatest monetary deformation in history, not the rational discounting of a beneficent future.

Accordingly, ten malefic trends will dominate national life during the long night of reckoning which lies ahead.

The spectacular failure of Keynesian central banking;

A prolonged, painful reversal of the three-decade long hyper-inflation of financial asset prices that has resulted in the Everything Bubble;

The violent implosion of America’s fiscal accounts;

An intensified central bank war on savers, fixed income retirees and holders of cash;

Peak Debt-induced suffocation of domestic economic growth;

Ferocious global economic headwinds arising from the demise of the Red Ponzi;

An outbreak of unprecedented partisan acrimony rendering Washington completely dysfunctional and imperiling America’s very constitutional foundation;

The lapse of Imperial Washington into belligerence, retreat and failure all around the planet;

The Baby Boom retirement tsunami, which will cause entitlement spending to soar and generational conflict to erupt like never before; and

A virulent outbreak of class warfare and redistributionist political conflict unprecedented in American history owing to a stagnating economic pie.

Moreover, there is a powerful reason to keep abreast of these Turbulent Ten trends.

To wit, these baleful developments are not just possibilities. They are well nigh certainties!

And they are ultimately rooted in a common cause.

Namely, the three decade long explosion of debt, speculation and financialization that was initiated in October 1987 when Alan Greenspan bailed out Wall Street gamblers and launched what has become a toxic worldwide regime of Keynesian central banking.

Consequently, America’s current $74 trillion mountain of public and private debt has become contagious.

On a worldwide basis, total debt outstanding now totals $255 trillion or a staggering 3X global GDP of $85 trillion. It now constitutes the greatest barrier to continued growth, prosperity and financial stability in all of economic history.

Even more crucially, these brobdingnagian figures did not materialize during the last three decades because everyday people suddenly lost their senses and became addicted to unsustainable levels of debt, leverage and financial speculation.

To the contrary, the people here and abroad were misled, induced and baited into burying themselves under crushing debts by agents of the state—especially its central banking branch.

The tools of deceit were falsified interest rates, artificially inflated asset prices and a hoary theory that debt-fueled “stimulus” injections by the state can create a permanent increase in economic growth and societal wealth.

No they can’t!

These mountains of debt can temporarily goose GDP, of course, because GDP accounting is inherently incomplete: It views the economy as simply a matter of sequential flows—quarter after quarter, year upon year– without regard to balance sheets and the accumulated carry cost of debt over time.

Moreover, this Keynesian blindness to balance sheets and their systematic impairment has gotten far more consequential since Greenspan launched a wholly new form of monetary central planning in October 1987.

Under the latter, the price of debt has been deeply and systematically falsified by the central banks, thereby providing a powerful artificial incentive to borrow and a misleading signal to debtors about its longer-run implications.

Balance sheets have been deeply impaired for households and governments especially because they do not borrow in order to acquire productive assets capable of defraying the accumulating cost of carry. Instead, all the added debt went into living high on the hog today.

Nor has the private business sector escaped the damage caused by deep repression of interest rates. That’s because the cost of benchmark debt (i.e. the 10-year U.S. treasury note) is really the master “cap rate” or valuation multiple for the entire financial system.

Artificial and sustained repression of cap rates, therefore, results in proportionately higher asset prices and increased price/earnings multiples—meaning that cheaper debt and richer share prices are one of the most toxic consequences of Keynesian central banking.

It provides powerful incentives to the corporate C-suites to borrow at sub-economic costs and use the proceeds to fund stock buybacks, thereby increasing per share earnings and goosing the value of top executives’ own ample stock options.

Likewise, cheap debt causes a huge distortion in the M&A market. Acquisitions are made to look “accretive” not because the make business sense or because there are true, sustainable synergies, but because they carry cost of purchase debt is so low.

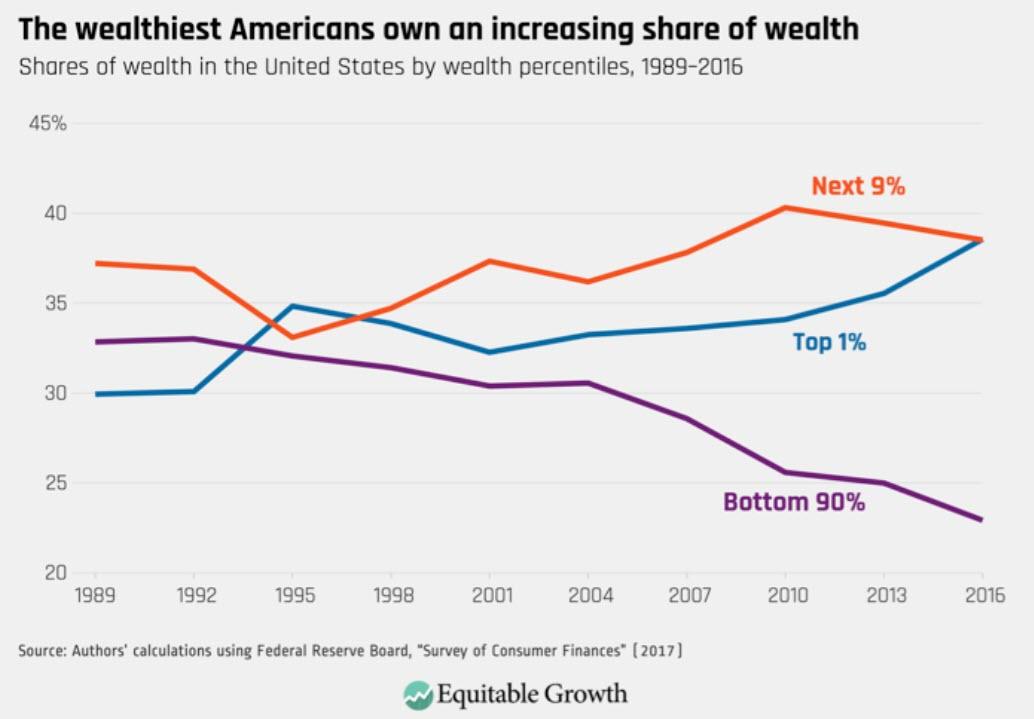

Needless to say, these forms of financial engineering redistribute financial wealth to the top 1% and 10% of households. The latter own 40% and 85% of the stock, respectively, and they have gained mightily since Greenspan initiated the present era of Keynesian central banking in the late 1980s.

At the end of the day, the relentless and ever deepening financial repression—especially during the decade since the financial crisis— has generated precious little gain in national output and jobs beyond what capitalism does on its own.

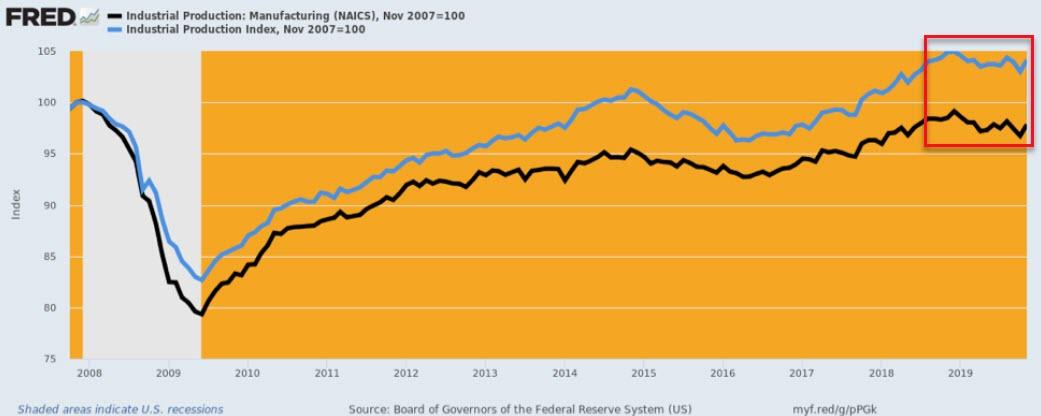

For example, manufacturing production is still 2% below pre-crisis levels of November 2007. And total industrial production has crept just 4% higher over 12 years.

Moreover, even the huge one-time inflation of financial asset prices on Wall Street didn’t embody sustainable real wealth because it was primarily based on multiple expansion, not earnings growth.

Exactly 31-years ago in early 1989, for instance, the S&P 500 index stood at 295 where it represented 12X earnings of $25 per share.

At the same PE multiple today, the index would weigh in at just 1600 or less than half of the 3240 level where it ended 2019.

Stated differently, 56% of the S&P 500 gain since 1989 is owing to PE multiple expansion, not earnings growth, and it materialized during a three decade interlude when the long-term growth capacity of the US economy was being ground to the vanishing point.

That is, PE multiples should have been falling, not soaring to the nosebleed section of history.

Indeed, this “bad money” regime of the Keynesian central bankers has now finally taken itself hostage.

The central bankers have fostered such massive and egregious bubbles that they are literally terrified by the prospect of another stock market meltdown like those of 2000-2002 and 2008-2009.

In turn, the latter would bring a renewed bout of desperate restructurings, layoffs and asset liquidations in the C-suites and a new round of recession on main street.

So the Fed has simply launched a Hail Mary which is so transparent and incendiary that it will surely catalyze the final blow-off top early in the 2020s.

After it had distorted, falsified and inflated financial asset prices beyond all recognition—the Fed dithered and delayed shrinking its balance sheet, thereby putting the lie to Bernanke’s solemn pledge that after the unusual and exigent conditions of the financial crisis had passed they would reduce the Fed’s massive trove of Treasury and GSE debt to pre-crisis levels.

It didn’t. After a tepid 15% balance sheet retrenchment through August 2019, the Fed actually turned tail and ran in the face of bitter attacks from the White House and unrelenting pressure from the bully boys and crybabies of Wall Street.

And now the last bit of sanity in the Eccles Building has vanished. From a low of $3.76 trillion on August 28, the Fed has already pumped $406 billion into the bond pits. That represents a staggering $1.1 trillion annualized rate of balance sheet expansion.

That’s money printing on steroids. It is also the great monetary match. Stated differently, the repo ruckus last September was the warning bell that the 30-year era of Bubble Finance was fixing to blow.

But the fools in the Eccles Building, blindly fixated on enforcing their interest rate pegs, effectively got out a gasoline hose and fueled what is now the blow-off top.

And that will pave the way for the Turbulent Twenties, and for the unfolding of all the baleful factors listed above.

There has rarely been such a fraught moment in American history.

During the Turbulent Twenties ahead we are heading for the double whammy of a political/constitutional crisis and a thundering financial breakdown at the same time.

Indeed, this perfect storm will gravely impact the personal liberty and economic welfare of every American citizen—so you need to understand what’s coming down the pike and how it will impact Washington and Wall Street alike.

You also need to understand that there has been no Trump b0om, whatsoever—even if the Donald was right during the campaign. That’s when he castigated Washington’s failed economic policies and labeled the faux prosperity of 2016 as a big fat ugly bubble that was fixing to implode on the American people.

Still, just because Donald Trump targeted the symptoms correctly that doesn’t mean he had a plan to fix the American economy or the skills and know-how to move the turgid, essentially paralyzed, machinery of the Federal government constructively forward.

In fact, the mainstream media has the whole story wrong. The Donald is not remotely the force of nature he’s been made to seem by the Trump-obsessed journalists and talking heads.

To the contrary, he’s actually a political flyweight, megalomaniacal incompetent and bile-ridden bully who stumbled into the Oval Office against all odds; and then lucked-out a second time by riding high on the final three-year crest of a deeply impaired and unsustainable economic recovery and monumental stock market bubble.

And here is where experience comes in. Since starting in Washington as a legislative assistant in 1970, we have seen every business cycle and President up close and personal.

So we know that the Donald committed the most egregious rookie mistake in the history of the American presidency.

That is, he insouciantly embraced a financial bubble that was destined to crash and took ownership of a struggling, geriatric business cycle expansion that had “recession ahead” written all over its forehead.

After all, the Donald was sworn in during month #90 of what was already the third longest business expansion in American history. It is now month #126 and it will be month #138 when his first term ends.

Here’s the thing. We are already at a point never, ever reached before.

Even the tech boom of the 1990s—previously the longest ever cycle—ended in recession during month #119, and back then there were plenty of tailwinds to keep it going.

Those year 2000 tailwinds, of course, have now become ferocious 2020s headwinds.

Europe is rolling over into recession. The Red Ponzi is floundering under its massive load of $40 trillion of debt and staggering malinvestments.

And the US economy is imperiled by $74 trillion of public and private debt and egregious Wall Street bubbles whose days are clearly numbered.

Moreover, recessions have not been outlawed by the economic gods and there are overwhelming odds that the next one will hit sometime soon as the 2020s unfold.

And when it does, Wall Street, the US economy and the Donald’s fantasy of MAGA will come tumbling down with it.

Accordingly, we think the Donald will mainly be remembered not as the restorer of MAGA nor as the statesman who rescued America from a day of reckoning that has been building for more than three decades.

Instead, the Donald is destined to be remembered as the Great Disrupter. His lasting contribution will be that he rambunctiously discredited the handiwork of Imperial Washington.

And that will prove to be progress itself as the Turbulent Twenties unfold.

After all, it is the self-serving consensus of the bipartisan ruling class in favor of permanent war, unchained entitlements, fiscal incontinence, unsustainable debt-fueled household spending, rampant corporate financial engineering and Keynesian monetary repression and “wealth effects” based central banking that lies at the roots of our current economic malaise.

At the same time, it should be crystal clear by now that Trump has no real program to restore domestic prosperity and that he has actually made matters inestimably worse with his four misbegotten wars on the American economy.

We are referring to the above referenced Trade War on domestic consumers; Border War on needed immigrant labor; political war on the Fed when it was belatedly trying to normalize; and what amounts to a war on the nation’s solvency embedded in the Donald’s runaway additions to the soaring national debt.

As to the “undrainable swamp”, it should never be forgotten that its deep-end lies on the Pentagon side of the Potomac. Yet the Donald has fed the military/industrial- surveillance complex like never before, thereby defeating his own stated goal.

That is, America’s desperately needed pivot to fiscal and national security sanity was stopped cold by Trump’s mindless $140 billion per year boost to an already vastly excessive and waste-ridden national defense budget.

And now that crucial pivot has been further blocked by a reckless economic and political war against Iran that will do exactly nothing to further the security and safety of the American homeland.

Needless to say, even if the Donald’s policies were better focused, his efforts to make MAGA never had a chance owing to the utterly groundless Russia-collusion investigation, the Mueller witch hunt and now the UkraineGate/Impeachment farce.

These political attacks are groundless, but nevertheless have functioned to disable Trump’s presidency.

In fact, the Donald’s fluke elevation to the Oval Office has finally caused the Deep State to come out of hiding and bare its fangs against American democracy itself.

So doing, it has finally awakened the sleepwalkers of the Foxified Right about the immense dangers of the Warfare State and the sweeping surveillance and police state apparatus that has been created in the service of the neocons’ misbegotten war on terrorism and quest for Empire.

Moreover, the terrifying capabilities, resources and (purported) credibility of the nation’s $75 billion per year intelligence community were literally hijacked by Obama officials led by then CIA director, John Brennan.

It is now more than evident that they illegally pursued a plot to first forestall Trump’s election, and then to re-litigate the outcome and eviscerate his Presidency after the voters had spoken.

At the end of the day, however, the result will be a thoroughly paralyzed government in Washington.

As the 2020s unfold, therefore, the latter will prove to be utterly incapable of stopping the twin fiscal menace of the Warfare State and Welfare State—a monster that the Donald has made immeasurably worse.

After taking the $2 trillion per year of uncontrolled entitlements off the table, Trump then added insult to injury via his unfunded $1.7 trillion tax cut and massive defense and domestic spending increases.

All told, the result will be a guaranteed $20 trillion explosion of the Federal debt (on top of the existing $23 trillion) over the coming decade.

Stated differently, crunch time is coming to the casino and that’s what is sure to bring the Donald down.

The stock market is heading not only for another 50% correction (1600 on the S&P 500), but also a long L-shaped bottom rather than a quick V-shaped rebound which occurred after 2009.

So the combination of the mess he inherited and the compounding damage from his four misguided wars on the American economy add-up to a looming catastrophe.

To be sure, we do not know exactly when the brown stuff will hit the fan. But we do know that Washington’s Empire abroad and phony prosperity at home are terminally failing and that the sell-by date draws near.

We also know that whatever comes next, it won’t be MAGA. Not by a long shot.

Indeed, once upon a time the prospect of $43 trillion of public debt—even a decade down the road— was literally unfathomable.

In fact, in one of our favorite remembrances from our White House days, we recall telling President Reagan in the photo below that America was on the verge of having a $1 trillion national debt.

That was in January 1981, and at the time crossing the $1 trillion mark was almost a nightmarish prospect.

But President Reagan was not intimidated. He properly insisted that this looming Rubicon was emblematic of the mess he had inherited, and that under his watch the nation’s soaring public debt would finally be stopped cold.

Alas, it wasn’t. By the time he left office, the national debt was pushing $3 trillion, and it was off to the races from there.

When Bill Clinton packed his bags to leave the White House the public debt was $5.7 trillion, then soared to $10.7 trillion by the end of George W. Bush’s two terms, stood at $19.9 trillion when Obama moved on and has already passed $23.0 trillion on the Donald’s watch.

But here’s the thing. President Trump is no Ronald Reagan. If the Gipper couldn’t stop the Washington deficit and debt brigades, there is not a snowball’s chance in the hot place that the Donald will.

In truth, unlike all of the Gipper’s successors, who relentlessly added to the debt during their turn at the helm but at least gave lip service to the notion of fiscal rectitude, the Donald just flat-out doesn’t care and he’s taking the GOP with him into fiscal fantasy-land.

What this means is that America is now fast drifting toward the Debtberg. It is only a matter of time before the impending collision shatters the faux prosperity and wanton complacency that prevails on both Wall Street and in Washington.

Still, it is not too late to get prepared.

* * *

For those concerned about the economic threat David has has highlighted, we highly recommend considering subscribing to his Contra Corner financial newsletter, published daily.

Alabama man Nathaniel Woods is scheduled to be executed tonight for three murders prosecutors acknowledge he did not commit. Woods was charged and convicted as an accomplice in the shooting deaths of police officers Charles Bennett, Carlos “Curly” Owen, and Harley Chisholm III at a suspected drug house in Birmingham. Under Alabama law, accomplice to murder is a capital offense punishable by death.

Prosecutors contend that on June 17, 2004, the three officers, as well as Officer Michael Collins, arrived at the house, which they knew to be a place where people bought drugs, and were insulted by Woods. They ran his name through the police database and found he had an outstanding warrant from Fairfield, Alabama. In a letter to Alabama Governor Kay Ivey (R) contesting Woods’ commutation request, Alabama Attorney General Steven T. Marshall says that Woods refused to come outside the house, and that officers followed him inside and arrested him on the Fairfield warrant. After they had Wood in handcuffs, however, Kerry Spencer, a friend of Woods who was already inside the house, opened fire on the officers, killing three and wounding Collins.

For his role in the incident, Woods’ jury convicted him and voted 10-2 that he be executed.

Spencer, who is also on death row, told The Appeal that Woods is “100 percent innocent. All he did that day was get beat up and he ran.” Spencer testified that he was napping after heavy drug use the night before when the police entered the apartment. He said he was roused from his sleep by a commotion, grabbed his rifle, and fatally shot the officers because they were attacking Woods and he feared for their lives.

Prosecutors offered a very different perspective at trial, reports The Appeal:

Woods, Jefferson County prosecutors told the jury at his 2005 trial, hated law enforcement and had lured the officers into the house so Spencer could kill them. Though he did not fire the fatal shots, Woods had masterminded the plan, making his actions as equally significant as Spencer’s, argued assistant district attorney Mara Sirles. “He wanted them to be fish in a barrel,” she said during her closing argument.

Prosecutors called witnesses who testified they’d heard Woods talking about his disgust for the police. They called a so-called handwriting expert to tell the jury that Woods had written lyrics to a song by rapper Dr. Dre on a piece of paper in his county jail cell that referred to the police as “pigs.” They called Collins, who recounted the events that unfolded at the house on the day of the shooting. And they called the victims’ widows, who said they wanted Woods to be sentenced to die.

The Appeal found other jarring and alarming discrepancies in Woods’ case:

Woods’s attorneys have collected evidence that they say shows that neither Woods nor Spencer plotted to kill the officers. The shooting, they argue, had been brought on by years of police misconduct involving a bribery scheme. They’ve alleged that key witnesses falsely testified or didn’t testify at all as part of undisclosed deals with the police. And they’ve alleged that the performance of Woods’s trial attorneys—neither of whom had tried a capital murder case before—was deficient.

Jefferson County Circuit Court Judge Tommy Nail did not allow evidence of police corruption to be presented at Woods’ trial because he was not arguing self-defense. This fact, and inadequate representation by his trial and appellate lawyers, ultimately doomed him to death.

Advocates have since slammed the decision to convict Woods for a murder he ultimately did not commit and the poor representation he received at the trial.

“Alabama is scheduled to execute a man who did not commit the murder he has been charged with and his lawyer had no previous experience with death penalty cases. How many more lives will be subject to this failure of a policy?” Hannah Cox, National Manager of Conservatives Concerned About the Death Penalty, told Reason.

Martin Luther King III, son of the iconic civil rights leader, was among the prominent voices pleading for Alabama to spare Woods’ life. “Killing this African American man, whose case appears to have been strongly mishandled by the courts, could produce an irreversible injustice,” King wrote in his letter to Ivey. “Are you willing to allow a potentially innocent man to be executed?”

These are not the only issues. There is also the use of a non-unanimous verdict, an issue that is currently being presented before the Supreme Court of the United States. The Court has agreed to hear Ramos v. Louisiana, a case that will decide whether or not the Sixth Amendment right to an impartial jury applies to the states, not just the federal government.

A second issue was raised after the state approved execution via nitrogen hypoxia, an alternative to its lethal injection protocol, in 2018. The state failed to inform Woods that his execution would be prioritized if he did not volunteer to be executed by nitrogen hypoxia. The Equal Justice Initiative has since reported that Alabama has publicly acknowledged that it sought execution dates for certain inmates solely because they did not elect to be killed by nitrogen hypoxia.

Woods is highly unlikely to receive a stay of execution. On Wednesday, Alabama Attorney General Steve Marshall released a statement calling Woods a “cop-killer” and rebuffing the reporting on his innocence claims.

from Latest – Reason.com https://ift.tt/2xbW21v

via IFTTT

Alabama man Nathaniel Woods is scheduled to be executed tonight for three murders prosecutors acknowledge he did not commit. Woods was charged and convicted as an accomplice in the shooting deaths of police officers Charles Bennett, Carlos “Curly” Owen, and Harley Chisholm III at a suspected drug house in Birmingham. Under Alabama law, accomplice to murder is a capital offense punishable by death.

Prosecutors contend that on June 17, 2004, the three officers, as well as Officer Michael Collins, arrived at the house, which they knew to be a place where people bought drugs, and were insulted by Woods. They ran his name through the police database and found he had an outstanding warrant from Fairfield, Alabama. In a letter to Alabama Governor Kay Ivey (R) contesting Woods’ commutation request, Alabama Attorney General Steven T. Marshall says that Woods refused to come outside the house, and that officers followed him inside and arrested him on the Fairfield warrant. After they had Wood in handcuffs, however, Kerry Spencer, a friend of Woods who was already inside the house, opened fire on the officers, killing three and wounding Collins.

For his role in the incident, Woods’ jury convicted him and voted 10-2 that he be executed.

Spencer, who is also on death row, told The Appeal that Woods is “100 percent innocent. All he did that day was get beat up and he ran.” Spencer testified that he was napping after heavy drug use the night before when the police entered the apartment. He said he was roused from his sleep by a commotion, grabbed his rifle, and fatally shot the officers because they were attacking Woods and he feared for their lives.

Prosecutors offered a very different perspective at trial, reports The Appeal:

Woods, Jefferson County prosecutors told the jury at his 2005 trial, hated law enforcement and had lured the officers into the house so Spencer could kill them. Though he did not fire the fatal shots, Woods had masterminded the plan, making his actions as equally significant as Spencer’s, argued assistant district attorney Mara Sirles. “He wanted them to be fish in a barrel,” she said during her closing argument.

Prosecutors called witnesses who testified they’d heard Woods talking about his disgust for the police. They called a so-called handwriting expert to tell the jury that Woods had written lyrics to a song by rapper Dr. Dre on a piece of paper in his county jail cell that referred to the police as “pigs.” They called Collins, who recounted the events that unfolded at the house on the day of the shooting. And they called the victims’ widows, who said they wanted Woods to be sentenced to die.

The Appeal found other jarring and alarming discrepancies in Woods’ case:

Woods’s attorneys have collected evidence that they say shows that neither Woods nor Spencer plotted to kill the officers. The shooting, they argue, had been brought on by years of police misconduct involving a bribery scheme. They’ve alleged that key witnesses falsely testified or didn’t testify at all as part of undisclosed deals with the police. And they’ve alleged that the performance of Woods’s trial attorneys—neither of whom had tried a capital murder case before—was deficient.

Jefferson County Circuit Court Judge Tommy Nail did not allow evidence of police corruption to be presented at Woods’ trial because he was not arguing self-defense. This fact, and inadequate representation by his trial and appellate lawyers, ultimately doomed him to death.

Advocates have since slammed the decision to convict Woods for a murder he ultimately did not commit and the poor representation he received at the trial.

“Alabama is scheduled to execute a man who did not commit the murder he has been charged with and his lawyer had no previous experience with death penalty cases. How many more lives will be subject to this failure of a policy?” Hannah Cox, National Manager of Conservatives Concerned About the Death Penalty, told Reason.

Martin Luther King III, son of the iconic civil rights leader, was among the prominent voices pleading for Alabama to spare Woods’ life. “Killing this African American man, whose case appears to have been strongly mishandled by the courts, could produce an irreversible injustice,” King wrote in his letter to Ivey. “Are you willing to allow a potentially innocent man to be executed?”

These are not the only issues. There is also the use of a non-unanimous verdict, an issue that is currently being presented before the Supreme Court of the United States. The Court has agreed to hear Ramos v. Louisiana, a case that will decide whether or not the Sixth Amendment right to an impartial jury applies to the states, not just the federal government.

A second issue was raised after the state approved execution via nitrogen hypoxia, an alternative to its lethal injection protocol, in 2018. The state failed to inform Woods that his execution would be prioritized if he did not volunteer to be executed by nitrogen hypoxia. The Equal Justice Initiative has since reported that Alabama has publicly acknowledged that it sought execution dates for certain inmates solely because they did not elect to be killed by nitrogen hypoxia.

Woods is highly unlikely to receive a stay of execution. On Wednesday, Alabama Attorney General Steve Marshall released a statement calling Woods a “cop-killer” and rebuffing the reporting on his innocence claims.

from Latest – Reason.com https://ift.tt/2xbW21v

via IFTTT

“The Worst Is Yet To Come”: Nomura Now Sees As Many As 1.5 Million Covid Cases By June

“The worst is yet to come.”

That’s the self-explanatory title of Nomura’s latest analysis assessing the consequences from the coronavirus pandemic, and which comes just two weeks after the Japanese bank issued its first preliminary assessment on the fallout from the global pandemic, which as readers will recall we found unduly optimistic. Well, a lot has happened since then, and as the report’s title suggests, the outlook has deteriorated sharply.

In the bank’s new base case, it revises down further its Q1 2020 GDP growth forecast for China to 0% y-o-y, and for the world to 0.9%. While Nomura still envisages a V-shaped global recovery in Q2 in its new base case, it now has a “U” in its new “bad scenario” and a downright depressionary “L” (non) recovery in the new severe scenario.

Below are the details on how in just two short weeks, the situation went from bad to downright catastrophic, in the bank’s own words:

The positive news is the marked decline in the number of new daily confirmed COVID-19 cases in China, but it has also demonstrated the challenging trade-off other governments now face between public health security controls – ranging from adequate resources of health services to containment and mitigation measures – and economic growth.

China imposed draconian controls, sealing off Hubei’s nearly 60m inhabitants, blocking transport and locking down dozens of cities. China’s authoritarian state may have won the battle against the virus but at a huge short-run cost to economic growth. Our new base case assumes that China’s lockdowns end late this month, which will be too late to avoid our forecast of GDP growth slowing to 0% y-o-y this quarter, which translates to -4.4% q-o-q.

This contraction in China’s economy will have major negative spillover effects on the rest of the world, particularly in the rest of Asia – and this is only just starting to show up in the economic data. However, what has really spooked financial markets is the rapid contagion of COVID-19 outside China to 76 countries (and counting), with a handful of hotspots – South Korea, Italy and Iran. These hotspots are now experiencing the same severe simultaneous demand (public fear factor) and supply (business disruption) shocks as China in addition to the negative spillover effects from China’s contracting economy.

While COVID-19 has not been as deadly as SARS (the case fatality outside China and Iran is 1.5% vs 10% for SARs), what is now clear is that it spreads much more easily. As COVID-19 spreads, governments will need to weigh the trade-off between health security and economic growth and it remains to be seen whether they have the resources and wherewithal to increase their health security controls – and the public’s willingness to follow them – to the same force and effectiveness as China has done. If not, the rest of the world could, in the not too distant future, lose control in trying to contain COVID-19.

Separately, for those urging for a central bank response, Nomura’s economists caution that in this abnormal economic slump, “macroeconomic policies are less well equipped to help (or “can only help so much”). If health security controls fail to contain the spread of COVID-19, financial markets may soon have to accept that a global recession is a forgone conclusion.”

In short, the situation is bad, and could get much worse if the pandemic spreads unchecked even faster around the globe.

How much worse? To consider the magnitudes, Nomura crudely assumes COVID-19’s attack rate (the percent of the population infected) in the rest of the world ends up being, on average, similar to that in China – then number of world confirmed cases could peak at 445,000. But if the rest of the world’s security controls are half as rigorous (the attack rate is twice as high as China’s) the number of world confirmed cases could peak at 890,000, and if world’s controls are one-quarter as rigorous, the peak could be 1.78m.

Consider the 2009 H1N1 Influenza. It started in the US in late April 2009 and spread with great intensity. By 11 June, it had reached 74 countries with a total of 30,000 cases and it was on this date that the WHO declared a global pandemic (it has not declared one since); by early November it has reached over 200 countries with 0.5m cases. We estimate that over the same period since the initial outbreak, the number of COVID-19 cases is about 3x more than 2009 H1N1, and if it tracks the 2009 H1N1 case trajectory there could be 1.5m COVID-19 cases by June 2020.

* * *

Extending on the above analysis, to get a relative sense of which countries outside China are most vulnerable to becoming high infection hotspots from COVID-19, Nomura has expanded the scorecard in our earlier Anchor report to 40 countries (Figure 2). Of the nine indicators, higher values indicate a higher risk of contagion, except in the case of geographical proximity and the global health security index, where lower values indicate higher vulnerability. The bank then normalizes the values of each of the nine indicators across countries, by calculating Z-scores, and sums up the nine Z-scores for each country and add 100. The results line up reasonably well with the COVID-19 contagion so far with South Korea, Iran and Italy ranking as highly exposed.

Glancing at country temperatures, there is support for the notion that COVID-19 is weaker in warmer climates, but the analysis shows several countries with mild temperatures that are at risk of becoming hotspots. The two most exposed – Hong Kong and Singapore – have been relatively successful in containing COVID-19 so far.

And while there is much more in the full 64-page analysis, we can summarize the analysis with the following three somber warnings:

The COVID-19 shock is quickly morphing into a global crisis. In addition to major economic spillover effects from China’s large GDP contraction in Q1, an increasing number of countries are having to contend with their own local demand and supply-side shocks from the spread of COVID-19, plus a tightening in global financial conditions.

In terms of rapid policy response, the Fed is really the only game in town (we expect the Fed to cut rates by a further 50bp in our base case and 125bp in our bad scenario). The ECB and BOJ have limited room, and fiscal stimulus will take time to deploy.

This is an abnormal global economic slump. The most effective immediate policy response is not monetary or fiscal policies; it’s health security controls. If health security controls fail to contain the spread of COVID-19, financial

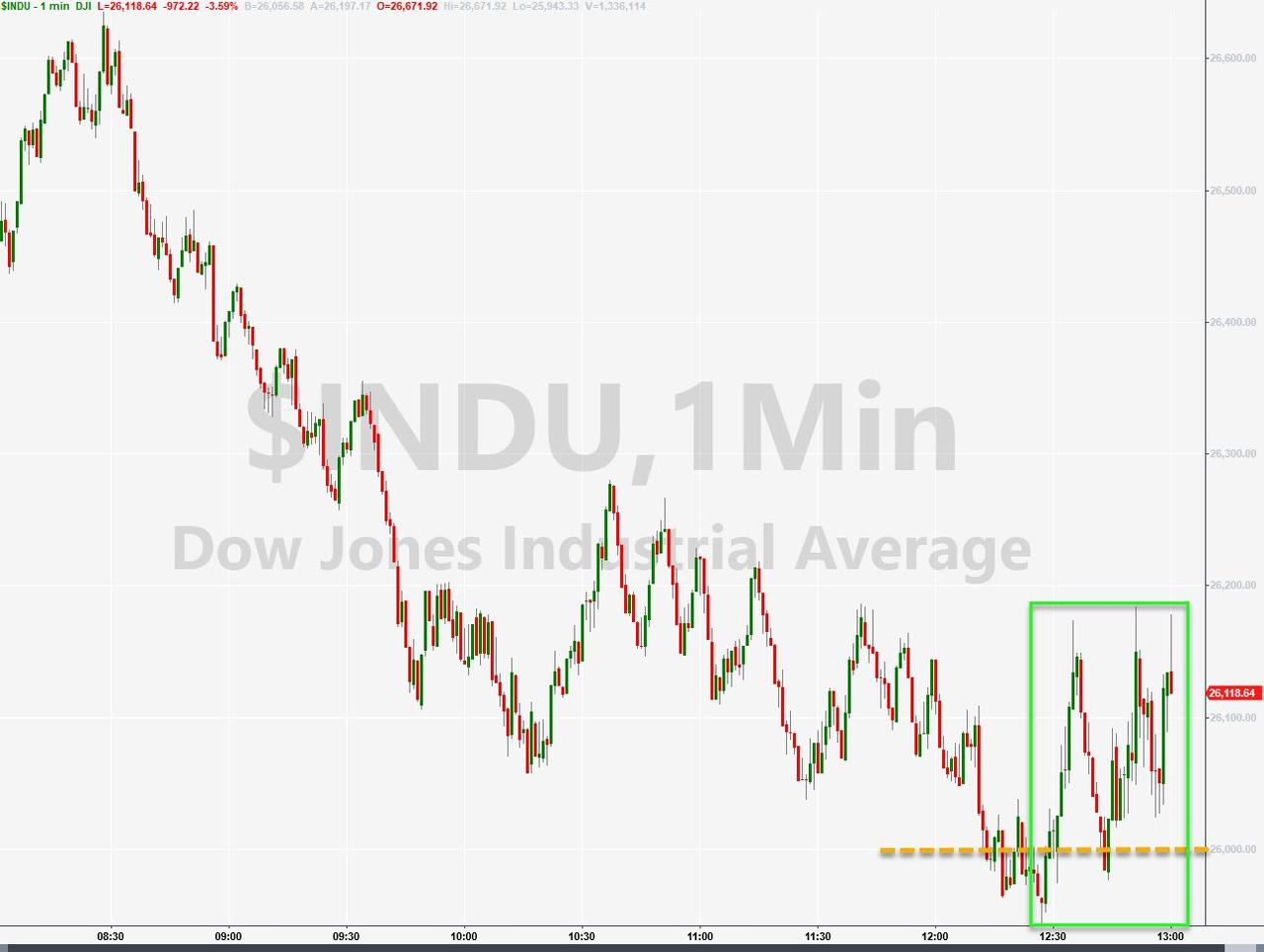

“Super Puke” – US Stocks Crash As Credit Markets & Yields Collapse

So much for the ‘Biden Bounce’. Watching the markets today – as The Dow plunged 1000 points, Treasury yields collapsed to record lows, credit markets imploded, and demands for more Fed intervention exploded – has one veteran trader remarking, “this is becoming a super-puke.”

It seems the stock market is ‘stuffed’ with Fed intervention and ‘just one waffer-thin mint’ more may spark the total destruction of markets.

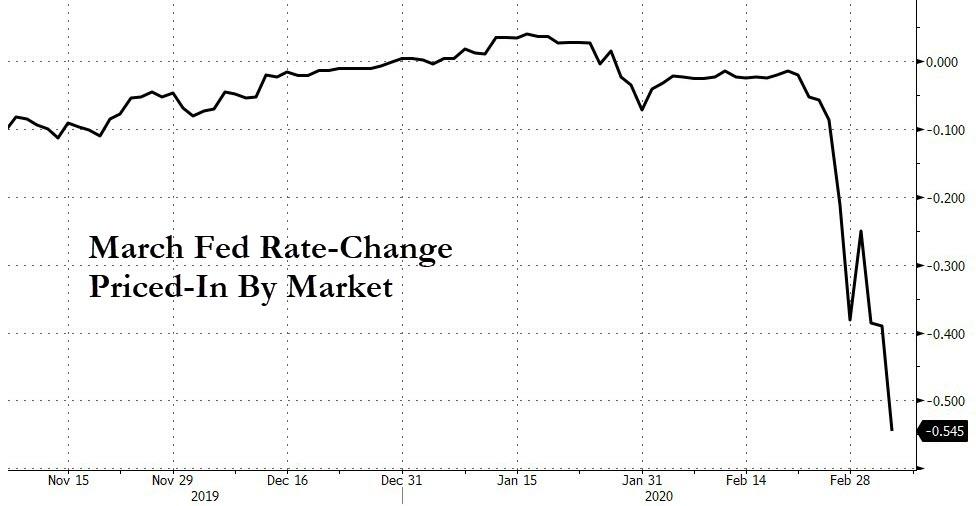

The market is in panic mode – demanding over 50bps more rate-cuts in March as stocks collapse…

Source: Bloomberg

Credit spreads are exploding wider (decompressing 9 of the last 11 days – the biggest blowout since June 2013) – now at their widest since 2016…

Source: Bloomberg

Sending an ugly message to stocks…

Source: Bloomberg

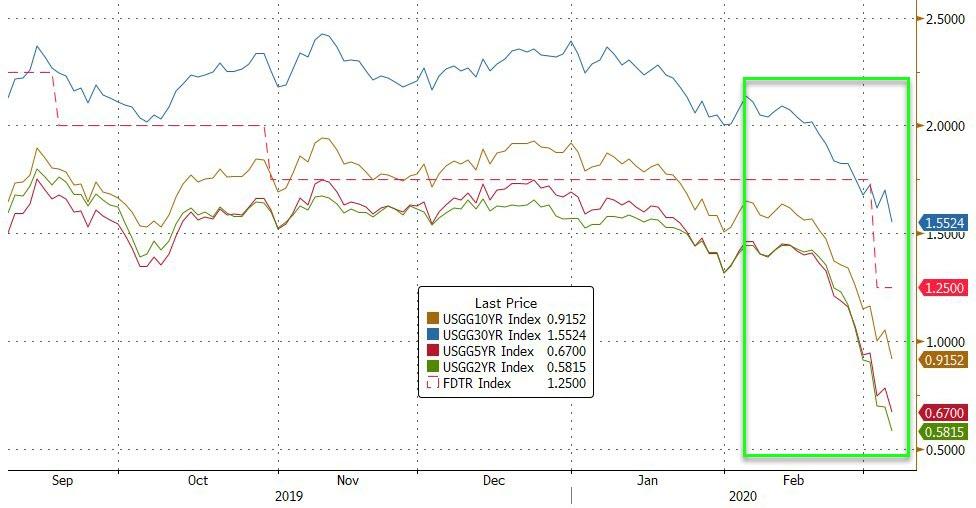

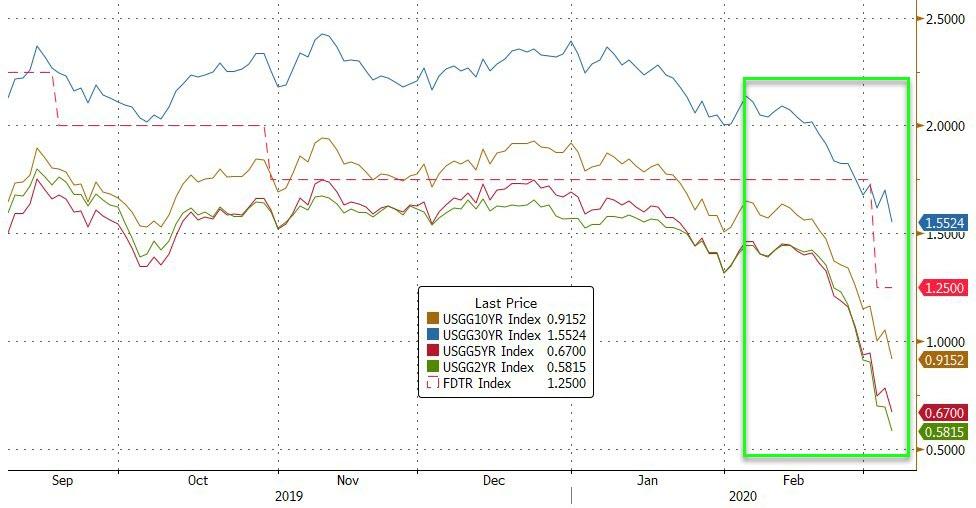

10Y Treasury yields plunged to new record lows…

Source: Bloomberg

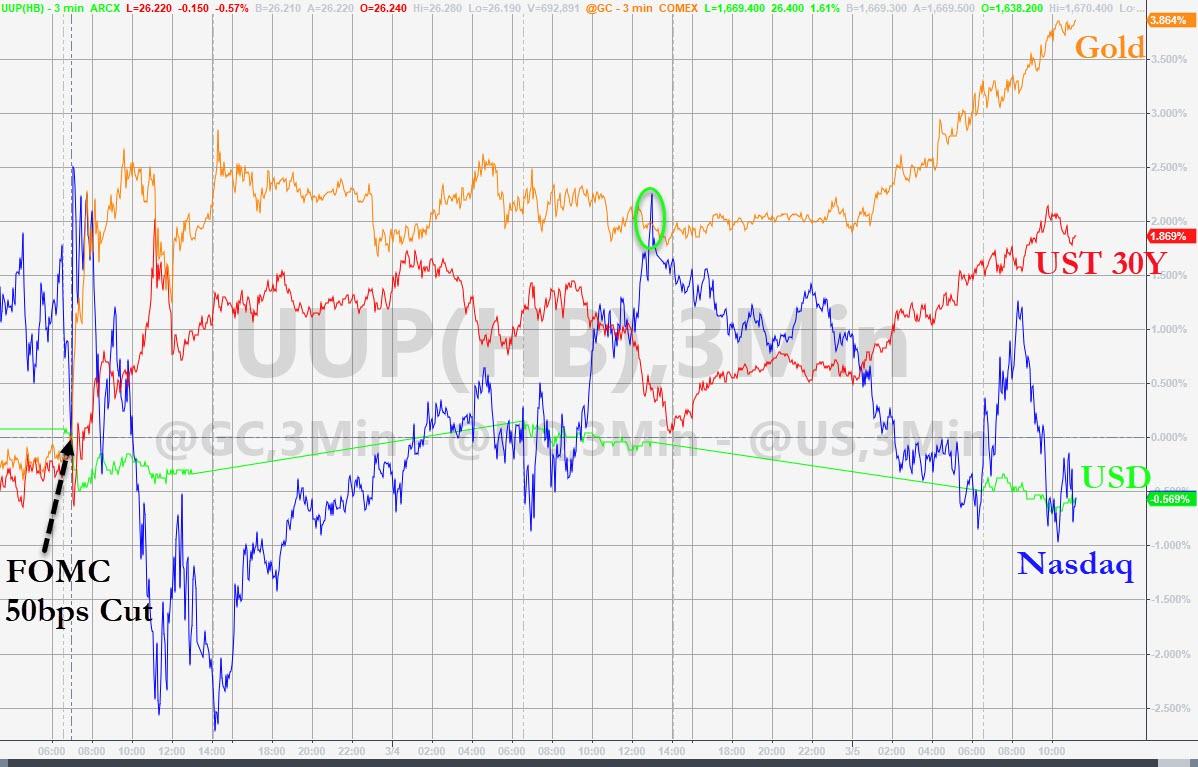

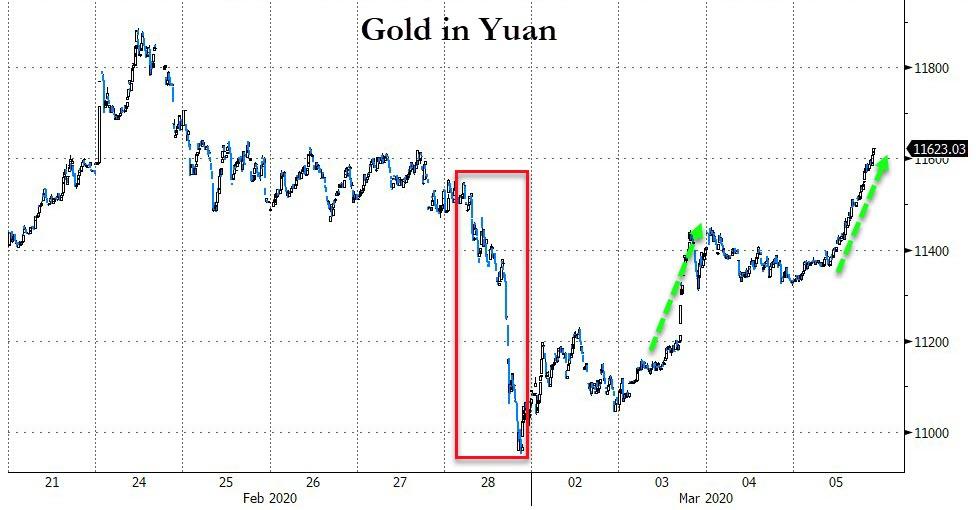

And gold (safe-haven) was aggressively bid…

In fact, since The Fed enacted an emergency 50bps rate-cut, Gold is soaring as the dollar and stocks faded…

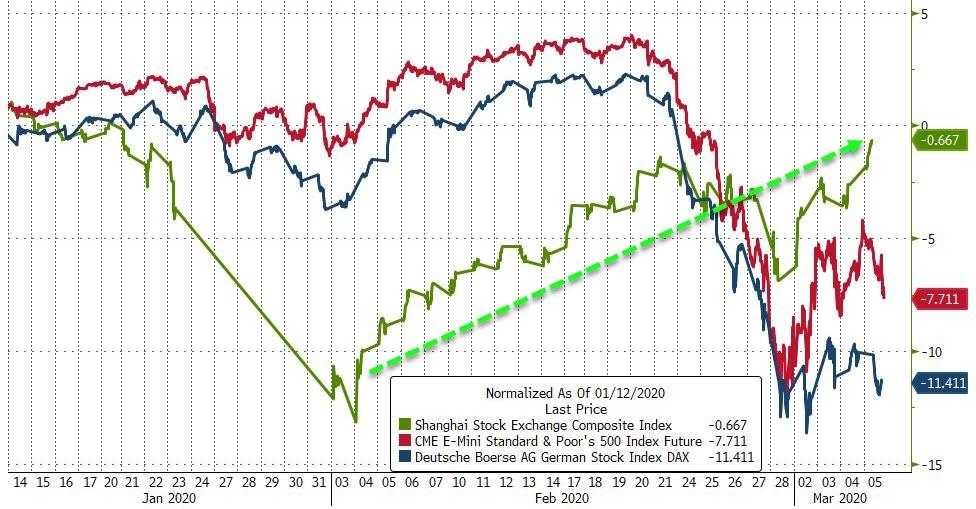

And before we dive into some of the details, this made us laugh – China – the epicenter of the collapse in global supply chains – has seen its stock market MIRACULOUSLY soar back to pre-Covid-19 levels… as Europe and US crash…

Source: Bloomberg

Amid all this chaos, Dow, Nasdaq, and S&P are still up 2-3% on the week, Small Caps and Trannies are red though…

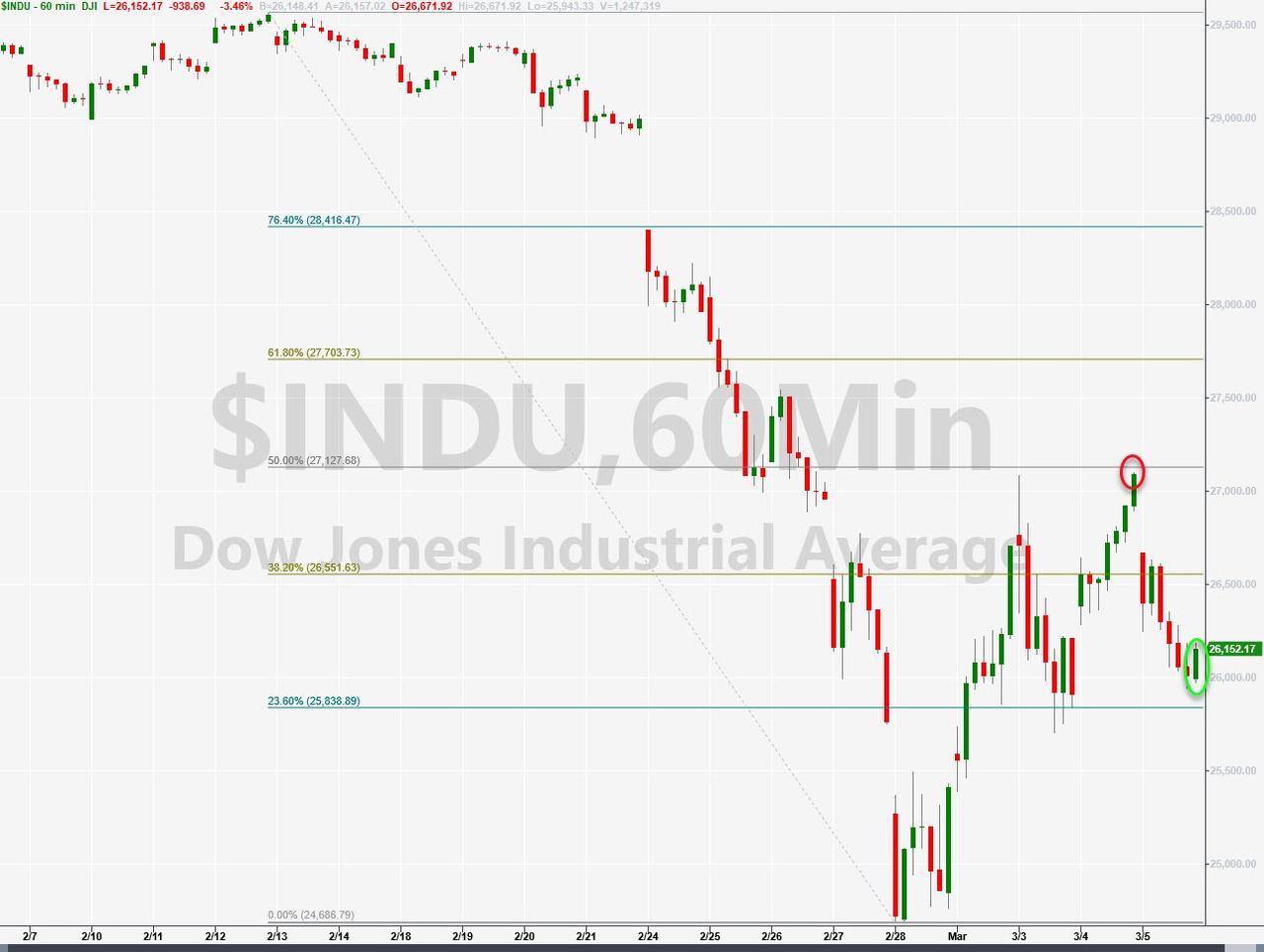

Dow tumbled back below 26k and then the battle began for the algos…

Yesterday’s top was at an almost perfect 50% retrace of the initial crash…

Another 1000-point day for the Dow – just how crazy is this vol? It’s the most extreme since the very peak of Europe’s debt crisis…

Source: Bloomberg

On the week, Defensives have dominated with Cyclicals unchanged (although today saw both hit just as hard)…

Source: Bloomberg

Bank stocks entered a bear market today, tumbling to their weakest since Jan 2019…

Source: Bloomberg

Global Systemically Important Banks are collapsing…

Source: Bloomberg

The Big US Banks were clubbed like baby seals…

Source: Bloomberg

VIX smashed higher, back above 42 intraday…

The VIX term structure is its most inverted since Lehman…

Source: Bloomberg

While stocks feel like they have plunged, they have a long way to go to catch up to bonds’ reality…

Source: Bloomberg

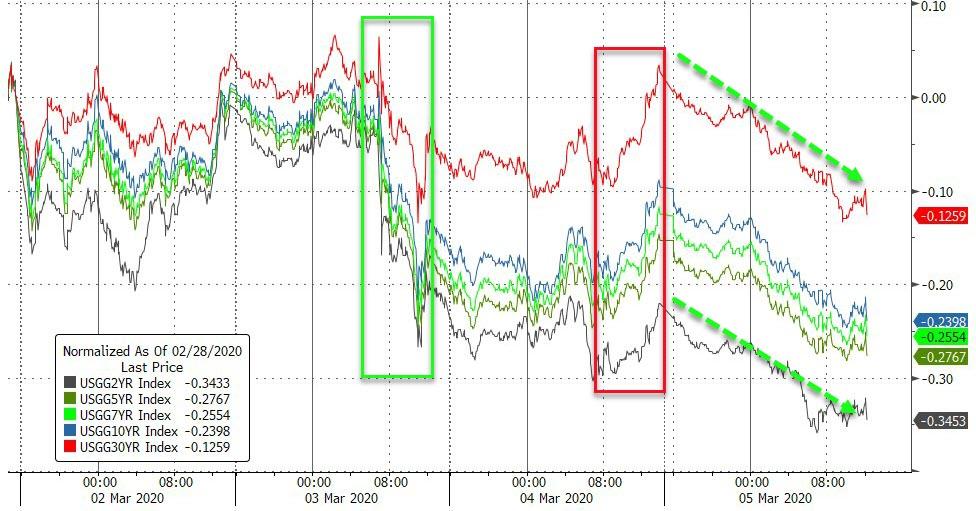

Treasury yields crashed today down 10-15bps across the curve with the long-end outperforming…

Source: Bloomberg

Yields are hitting record or cycle lows across the entire curve…

Source: Bloomberg

The Dollar slipped back to post-Powell-cut lows – this is the lowest for the dollar since January…

Source: Bloomberg

Cryptos were bid today, lifting all the major coins into the green for the week…

Source: Bloomberg

Commodities were clearly divided today with gold and silver soaring and copper and crude crushed…

Source: Bloomberg

WTI plunged back to a $45 handle after OPEC+ talks did not seem to go well (damn you Putin!)…

Gold soared higher all day – to its highest close since Jan 2013

And also surged again Yuan…

Source: Bloomberg

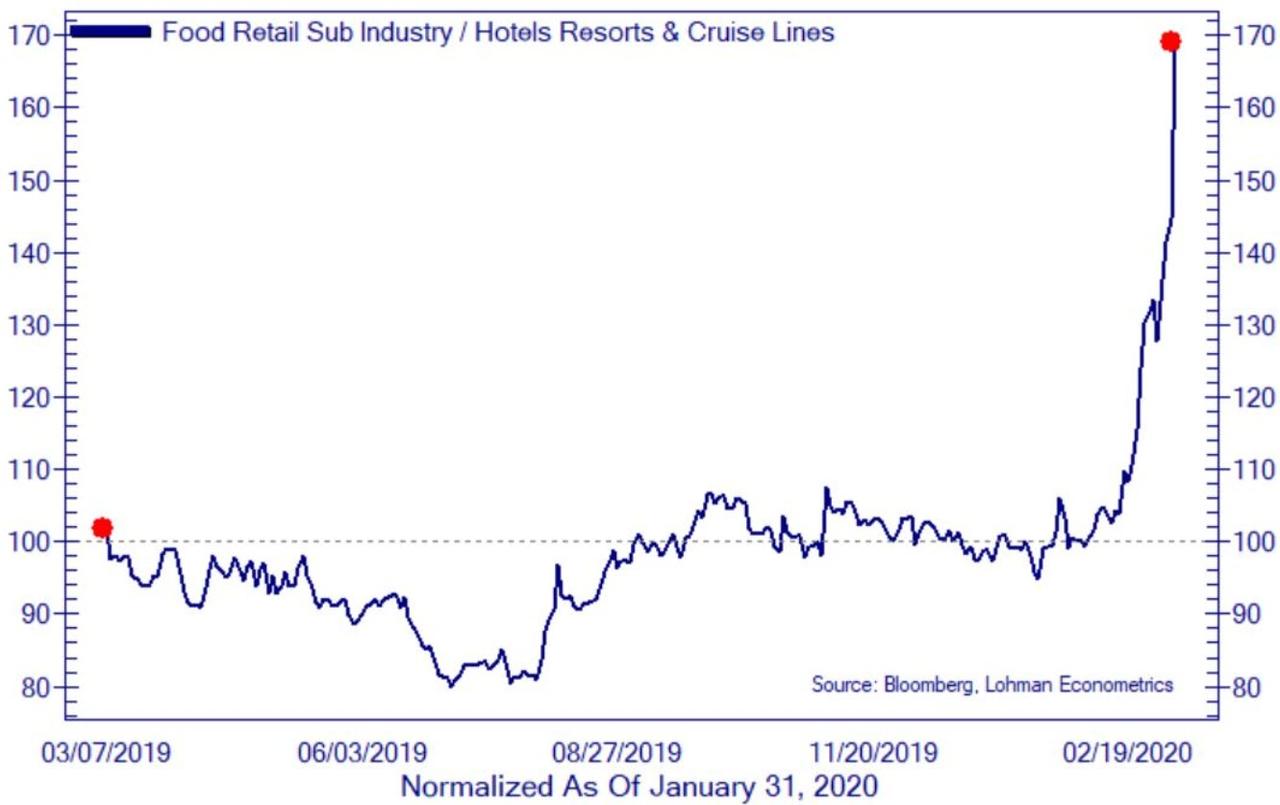

Finally, with a h/t to John Lohman, the Coronavirus Fear Index is exploding… “Long panic-buying food, short travel and entertainment”

MSCI Warns US Stocks Could Fall Another 11% As Coronavirus Outbreak Worsens

Shortly before US stocks suffered another triple-digit point drop at the open – dampening the cheers of traders and pundits who gleefully celebrated stocks going positive for the week on Wednesday – MSCI warned on Thursday that another double-digit drop could be in store for US stocks, Reuters reports.

Like most other analysts, Thomas Verbraken, the executive director for risk management at the research and indices giant, said his risk models suggest that a short-term drop in growth of 2 percentage points, and an attendant drop in corporate earnings, could hammer stocks even lower, erasing much (but not nearly all) of the gains since President Trump’s inauguration.

“We’ve conducted a what-if scenario analysis that assumes a short-term drop in growth of 2 percentage points and a risk-premium increase of 2 percentage points,” Thomas Verbraken, executive director at MSCI’s risk management solutions research told clients.

“Our model indicates that, in such a scenario, there’s room for further short-term losses:U.S. equities — already down 11% from Feb. 19 through March 3 – could drop a further 11%.”

Earlier this week, the OECD became the first major NGO to warn that the virus could seriously restrain global growth if the outbreak doesn’t fade with the warm spring weather, like President Trump hopes it will. The OECD said that global growth could shrink “by half” thanks to the outbreak, as the twin supply- and demand-side disruptions wreak havoc on consumption and manufacturing.

All told, two consecutive 11% drops would be equivalent to a more than 20% decline from the all-time highs, which would put the US market solidly into bear-market territory.

Most Wall Street banks have been slower to lower their equity year-end forecasts, but suffice it to say, a 20% drop would leave stocks well below where most of the big banks expect they will be at year’s end.

Putin & Erdogan Announce Major Idlib Ceasefire After Tense 6-Hour Negotiations

Russia and Turkey have announced a major ‘de-escalation’ and ceasefire agreement in Idlib, which — we should note, is very likely to unravel and fail similar to the recent much-hyped US-Taliban ceasefire in Afghanistan which began falling apart a mere 24-hours after it was signed.

But Thursday’s talks between Turkish President Recep Tayyip Erdogan and his Russian counterpart Vladimir Putin were intense, lasting six hours, during which they hashed out details — the key of which is an announced ceasefire set to begin just after midnight on March 6th. “At 00.01 tonight, as in, from midnight, the ceasefire will be put in place,” Erdogan said.

Putin and Erdogan in a less than warm greeting just before six hour talks on Thursday, via TASS.

Previously improving ties between Moscow and Ankara been severely damaged, recently reaching breaking point, since the Syrian-Russian joint offensive beginning in December to liberate Idlib province from al-Qaeda factions which have held it since 2015. Turkey has lost scores of troops, including in what’s widely believed to have been a Russian strike on Turkish positions a week ago, which killed at least 34 Turkish soldiers.

Here are the three key points agreed upon after the six hour talks between Putin and Erdogan, per Middle East Eye:

Agreed to establish a six-kilometer-wide security corridor along the M4 highway connecting Latakia with northern Syria.

Agreed to establish joint Turkish-Russian patrols along the highway on 15 March, stretching from the Trumba settlement just west of the strategic town of Saraqeb, to the Ain al-Havr settlement.

Ceasefire in Idlib to begin at midnight.

Obviously this leaves much out, highlighting likely continuing deep points of contention between the two, for example the fate of hundreds of thousands of displaced refugees and the status of territories in southern Idlib captured by the Syrian Army over the past months (the latter only a problem from Ankara’s point of view of course).

Spectacular displays of passive-aggression from Putin and Erdogan as they both try and leave the other guy hanging while they chat to their bros pic.twitter.com/efFi4BoYdJ

According to Russia’s RT, the document signed following negotiations Thursday crucially “underlined that both Moscow and Ankara remained committed to maintaining the territorial integrity and sovereignty of Syria.”

This despite Erdogan recently speaking and acting as if the northwest Syrian province must be ‘defended’ in the way of some kind of Turkish possession.

Meanwhile, in a sign this is surely doomed to be very short-lived — if it even gets off the ground at all (considering especially we’re dealing with non-state actors on the ground, namely, al-Qaeda faction Hayat Tahrir al-Sham), just as news of the ‘de-escalation’ agreement broke in the afternoon Turkey’s Defense Ministry announcedtwo Turkish soldiers killed and three others wounded in Idlib by Syrian national forces.

Nothing makes government grow like a crisis. People get scared, politicians respond to that fear with promises that the state will step in and make everything better, and government ends up larger and more powerful. The pandemic of COVID-19 coronavirus threatens a world-wide wave of sickness, but it’s the healthiest thing to happen to government power in a very long time. As it leaves government with a rosy glow, however, our freedom will end up more haggard than ever.

“You can look at it as socialized medicine,” Rep. Ted Yoho (R-Fla.) said on Tuesday about White House proposals to have the federal government foot the bill for uninsured COVID-19 patients. “But in the face of an outbreak, a pandemic, what’s your options?”

Yoho isn’t the only Republican to have found a new place in his heart for government control of healthcare; obviously, the Trump administration is on-board, too. During Senate testimony, the U.S. Department of Health and Human Services’ Robert Kadlec, who coordinates the department’s COVID-19 efforts, floated the idea of treating virus patients as disaster victims eligible for federal funds.

What else can you do “in the face of an outbreak, a pandemic” that has, so far, resulted in an estimated 94,000 cases and 3,200 deaths worldwide (though the numbers continue to grow)? You could, I suppose, rely on the same not-yet-entirely government-dominated health system that deals with influenza outbreaks every year. In the 2019-20 flu season, according to the Centers for Disease Control and Prevention our long-time viral enemy has, so far, infected 32 million Americans, sent 310,000 to the hospital, and killed 18,000.

That’s not to say that COVID-19 isn’t serious, or that people aren’t suffering from its effects. But we forget about our annual wrestling match with a deadly disease, the flu, while freaking out about the emergence of a virus that is frightening mostly because of its novelty, despite any evidence that we’re inadequate to the challenge.

Fear is the key here to Yoho’s sudden love for socialized medicine, as well as other panicked proposals for the government to somehow save us from the pandemic. Fear is a survival characteristic, but it makes us vulnerable to the impulse—or demand—that we surrender control to somebody else.

“All animals experience fear—human beings, perhaps, most of all. Any animal incapable of fear would have been hard pressed to survive,” wrote economic historian Robert Higgs, the author of Crisis and Leviathan (1987), a book-length examination of how bad times drive government to grow in power and scope. “The people who have the effrontery to rule us, who call themselves our government, understand this basic fact of human nature. They exploit it, and they cultivate it. Whether they compose a warfare state or a welfare state, they depend on it to secure popular submission, compliance with official dictates, and, on some occasions, affirmative cooperation with the state’s enterprises and adventures.”

Or, as Rahm Emanuel put it in 2008: “You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before.”

Politicians are human beings, too (allegedly so, anyway) and subject to fear, including fear of being voted out of office by panic-stricken constituents looking for officials to “do something.” So, their instinct to exploit a crisis complements their inclination to soothe the fearful by making efforts—even counterproductive ones—to assure the public that everything will be just fine.

That combination of calculation and fright gave us not only a proposal to stick the taxpayers with the medical bills of the uninsured, but also a seemingly pointless cut in the fed funds rate by the Federal Reserve, and proposals for massive federal spending to off-set economic disruptions by the spread of COVID-19.

“The Federal Reserve has become the default doctor for whatever ails the U.S. economy,” noted a skeptical Wall Street Journal editorial board. But economic fallout from the virus “relates mainly to the damage to global supply chains and expected limits on travel and commerce as the world tries to mitigate the rates of infection. Nobody is going to take that flight to Tokyo because the Fed is suddenly paying less on excess reserves.”

That combination of calculation and fear also gives us Massachusetts Democratic Sen. Elizabeth Warren’s proposal to “enact at least a $400 billion fiscal stimulus package to head off the potential economic impact of coronavirus” on top of “free care for coronavirus” that she also endorses. Will the spending repair disrupted supply chains and put production lines back in operation a minute sooner than demand for goods and services dictates? Not a chance—but Warren probably hoped it would look sufficiently compassionate to those looking for government to “do something” to keep her (now-concluded) presidential campaign on life support.

Public health has long been a playing field for fear and calculation, giving us intrusive laws that sit on the books, waiting to be invoked by the next microorganism to catch the public’s attention.

Those laws include a nearly unlimited power to quarantine people suspected of exposure to infectious diseases—and then bill them for the confinement, as has happened to Americans returning from Wuhan, China, where COVID-19 appears to have originated. Never mind that “quarantines of passengers arriving from mainland China appear excessive and are inconsistent with available epidemiologic data,” according to bioethicists Lawrence Gostin and James Hodge. Crises breed more government authority, not sensible restraint.

There’s usually little pushback because “people are pretty compliant as long as they believe that their best interests are being taken care of,” Wendy K. Mariner, a health law professor at Boston University, told The Washington Post.

Like all crises, the COVID-19 pandemic will pass, hopefully with a minimum of illness and death. But it will leave behind a residue of laws, spending, and precedents for future government actions that won’t depart in its wake. That’s because of what Higgs calls the “ratchet effect,” by which each crisis sees government shrink a little, but never back to its pre-crisis status. “Thus, crisis typically has produced not just a temporarily bigger government but also permanently bigger government,” he wrote.

So, even after the public panic retreats, the politicians’ calculations subside, and COVID-19 becomes more knowable and treatable, we’ll be left with the permanent swelling of government caused by the latest crisis.

from Latest – Reason.com https://ift.tt/2uVzuRS

via IFTTT

Nothing makes government grow like a crisis. People get scared, politicians respond to that fear with promises that the state will step in and make everything better, and government ends up larger and more powerful. The pandemic of COVID-19 coronavirus threatens a world-wide wave of sickness, but it’s the healthiest thing to happen to government power in a very long time. As it leaves government with a rosy glow, however, our freedom will end up more haggard than ever.

“You can look at it as socialized medicine,” Rep. Ted Yoho (R-Fla.) said on Tuesday about White House proposals to have the federal government foot the bill for uninsured COVID-19 patients. “But in the face of an outbreak, a pandemic, what’s your options?”

Yoho isn’t the only Republican to have found a new place in his heart for government control of healthcare; obviously, the Trump administration is on-board, too. During Senate testimony, the U.S. Department of Health and Human Services’ Robert Kadlec, who coordinates the department’s COVID-19 efforts, floated the idea of treating virus patients as disaster victims eligible for federal funds.

What else can you do “in the face of an outbreak, a pandemic” that has, so far, resulted in an estimated 94,000 cases and 3,200 deaths worldwide (though the numbers continue to grow)? You could, I suppose, rely on the same not-yet-entirely government-dominated health system that deals with influenza outbreaks every year. In the 2019-20 flu season, according to the Centers for Disease Control and Prevention our long-time viral enemy has, so far, infected 32 million Americans, sent 310,000 to the hospital, and killed 18,000.

That’s not to say that COVID-19 isn’t serious, or that people aren’t suffering from its effects. But we forget about our annual wrestling match with a deadly disease, the flu, while freaking out about the emergence of a virus that is frightening mostly because of its novelty, despite any evidence that we’re inadequate to the challenge.

Fear is the key here to Yoho’s sudden love for socialized medicine, as well as other panicked proposals for the government to somehow save us from the pandemic. Fear is a survival characteristic, but it makes us vulnerable to the impulse—or demand—that we surrender control to somebody else.

“All animals experience fear—human beings, perhaps, most of all. Any animal incapable of fear would have been hard pressed to survive,” wrote economic historian Robert Higgs, the author of Crisis and Leviathan (1987), a book-length examination of how bad times drive government to grow in power and scope. “The people who have the effrontery to rule us, who call themselves our government, understand this basic fact of human nature. They exploit it, and they cultivate it. Whether they compose a warfare state or a welfare state, they depend on it to secure popular submission, compliance with official dictates, and, on some occasions, affirmative cooperation with the state’s enterprises and adventures.”

Or, as Rahm Emanuel put it in 2008: “You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before.”

Politicians are human beings, too (allegedly so, anyway) and subject to fear, including fear of being voted out of office by panic-stricken constituents looking for officials to “do something.” So, their instinct to exploit a crisis complements their inclination to soothe the fearful by making efforts—even counterproductive ones—to assure the public that everything will be just fine.

That combination of calculation and fright gave us not only a proposal to stick the taxpayers with the medical bills of the uninsured, but also a seemingly pointless cut in the fed funds rate by the Federal Reserve, and proposals for massive federal spending to off-set economic disruptions by the spread of COVID-19.

“The Federal Reserve has become the default doctor for whatever ails the U.S. economy,” noted a skeptical Wall Street Journal editorial board. But economic fallout from the virus “relates mainly to the damage to global supply chains and expected limits on travel and commerce as the world tries to mitigate the rates of infection. Nobody is going to take that flight to Tokyo because the Fed is suddenly paying less on excess reserves.”

That combination of calculation and fear also gives us Massachusetts Democratic Sen. Elizabeth Warren’s proposal to “enact at least a $400 billion fiscal stimulus package to head off the potential economic impact of coronavirus” on top of “free care for coronavirus” that she also endorses. Will the spending repair disrupted supply chains and put production lines back in operation a minute sooner than demand for goods and services dictates? Not a chance—but Warren probably hoped it would look sufficiently compassionate to those looking for government to “do something” to keep her (now-concluded) presidential campaign on life support.

Public health has long been a playing field for fear and calculation, giving us intrusive laws that sit on the books, waiting to be invoked by the next microorganism to catch the public’s attention.

Those laws include a nearly unlimited power to quarantine people suspected of exposure to infectious diseases—and then bill them for the confinement, as has happened to Americans returning from Wuhan, China, where COVID-19 appears to have originated. Never mind that “quarantines of passengers arriving from mainland China appear excessive and are inconsistent with available epidemiologic data,” according to bioethicists Lawrence Gostin and James Hodge. Crises breed more government authority, not sensible restraint.

There’s usually little pushback because “people are pretty compliant as long as they believe that their best interests are being taken care of,” Wendy K. Mariner, a health law professor at Boston University, told The Washington Post.

Like all crises, the COVID-19 pandemic will pass, hopefully with a minimum of illness and death. But it will leave behind a residue of laws, spending, and precedents for future government actions that won’t depart in its wake. That’s because of what Higgs calls the “ratchet effect,” by which each crisis sees government shrink a little, but never back to its pre-crisis status. “Thus, crisis typically has produced not just a temporarily bigger government but also permanently bigger government,” he wrote.

So, even after the public panic retreats, the politicians’ calculations subside, and COVID-19 becomes more knowable and treatable, we’ll be left with the permanent swelling of government caused by the latest crisis.

from Latest – Reason.com https://ift.tt/2uVzuRS

via IFTTT

{kind=link}