If Google had never received a dime of local, county, state, or federal payola, and if Google had never assisted any state actor in the collection, maintenance, and sharing of data obtained pursuant to use of Google, and if there was no immunity from civil liability conferred upon Google for intentionally or negligently publishing defamatory material, or republishing the same, or for de-platforming the speech of others, then, I might be inclined to side with the Googlemeister.

[1.] As a legal matter, it’s clear: The First Amendment, by its own terms, applies only to the federal government; the Fourteenth Amendment applies the same rules to state and local governments; but private institutions—search engines, newspapers, employers, universities, landlords, and such—aren’t covered. That’s the so-called “state action doctrine” (with the “state” referring to the government, whether state or federal), and it explains why a newspaper or Google or others can pick and choose what to publish, what ads to run, and the like.

[2.] The Supreme Court held, in Rendell-Baker v. Kohn (1982), that government funding doesn’t make private entities “state actors.” If the government attaches speech-restrictive strings to the funding (e.g., “We’ll give you these funds only if you promise to restrict speech”), then the government may be held responsible for the speech restrictions. But if the government just gives the funds, and the private entity imposes speech restrictions entirely on its own, then there’s no First Amendment problem. And the Court held this in a case where the recipient was a private school that got 90% of its funding from the government.

[3.] Likewise, getting government benefits—even being given legal monopoly status (which Google doesn’t have)—doesn’t make you a state actor bound by the Bill of Rights. See Jackson v. Metropolitan Edison Co. (1974) (on which Rendell-Baker relied).

[4.] Now this all has to do with whether the Bill of Rights constrains the private entity; statutes aren’t subject to the state action doctrine, unless they are specifically limited to restricting the government. Congress imposes many statutory restrictions on private entities, whether attached to funding (as in Title VI or Title IX, which generally require recipients of federal funds not to discriminate based on race or sex) or not (as in Title VII, which generally bars most employers from discriminating, whether or not they get government funds). States might impose similar restrictions, though perhaps not on inherently interstate communications media.

Sometimes the First Amendment might itself constrain such restrictions on private entities (see, e.g., the Boy Scouts v. Dale case). But in any event, it takes a statute to restrain private entities this way, and Congress has never passed a statute purporting to limit Google’s ability to restrict speech on its platforms.

[5.] Of course, I’m talking here about the law as it is; some might argue for rejecting the state action doctrine, or for enacting statutory constraints on Google and the like. But that’s not the law today; and, if you think it ought to be the law, you might want to consider just what its scope should be: If you live in government-subsidized housing, should you be barred from ejecting guests based on their speech or their religious beliefs, on the theory that what you do on government-subsidized property becomes “state action”? If you get social security or the Earned Income Tax Credit or a government salary or similar benefits, should you be barred from engaging in viewpoint discrimination or religious discrimination in any projects you set up using that money? If you have a hard-to-get professional license—you’re a doctor or a lawyer or some such—should you likewise be subject to the First Amendment or the Due Process Clause or the Equal Protection Clause in all your professional decisions?

from Latest – Reason.com https://ift.tt/2VMhPHt

via IFTTT

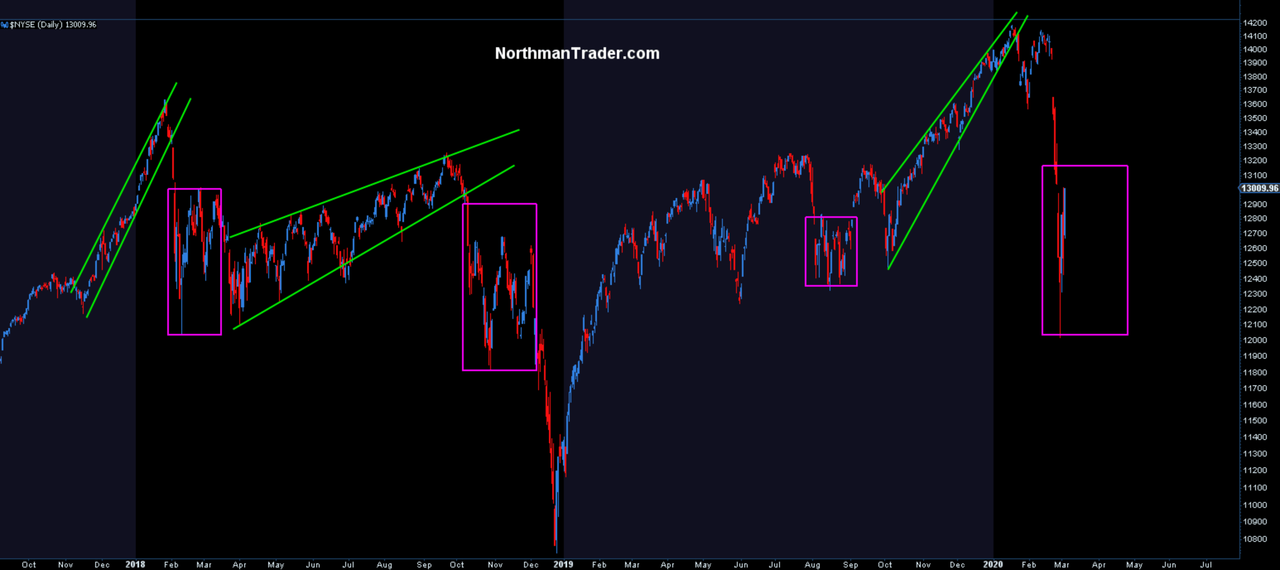

Some thoughts on the current market situation: Awe-inspiring volatility in markets these days and headlines keep coming non stop.

It’s heaven for fans of volatility and action, but it’s also a very dangerous time for traders. The temptation is to chase every headline and every move.

$DJIA flies up over 1,000 points and drops another 1,000 the next day and then repeats. Just 2 weeks ago we were staring at 2-3 handle ranges on $SPX intra-day for hours on end.Things have changed for now, get used to it.

Bears are having a blast right now, just accept it:

Everybody can choose to approach these things as they wish, but my general view here is this:

People associate the headlines with the market action.

Yes, they clearly have an influence, but don’t lose sight of the technicals.

They are a great guide especially during highly volatile times.

My view fwiw: Don’t chase every move, but rather choose wisely when/where to engage.

The message: Keep calm and look at the larger technical picture and choose wisely when and where to get engaged.

For anyone that had positioned short into February last week was fantastic. Bulls that had their fun riding the Fed liquidity and either listened to the warning signs and got out or are trapped at much higher prices. That’s the nature of the beast and now we’re in a period of wide range chop:

I submit that nothing what we are seeing here currently is unusual, except it is more violent now with tons of uncertainty thrown in including the concern that central banks finally lose control.

I’ve described the situation as binary and it remains to this day. Central banks either will maintain control or they won’t. The virus situation impact will either be short and painful, or it will have longer term ramifications. Unknowable at this very moment.

But as you can see in the chart above we’ve had periods like this before, a bunch of back and forth while markets negotiate the price action that ultimately it either resolves higher or lower. Genius I know. But that’s just reality.

The key, from my perspective, is not to get chopped up in the wild back and forth, but rather be elective, identify potential patterns and levels and then act on them, but also not be stubborn about anything. Everything is a trade at the moment and being opportunistic helps.

My attitude here is to look for spots that look interesting, test out the levels and if they work (short or long) then ride the counter move and scale out along the way.

I showed an example from our subscriber feed on twitter yesterday (see thread), this one from the long side identifying the pivot price zone to come:

then highlighting the engagement zone:

And then we saw the violent reaction to the upside yesterday:

This pattern remains unconfirmed and looks to be in trouble as of this morning, but that was a massive rip to the upside yesterday as markets moved 4% higher in a day. And that’s the point: These markets are massively volatile at the moment and one has to pick one’s spots to get engaged in and then be flexible enough to also reduce risk and lock in gains on moves such as this.

When else will you get 3%-4% moves every day? The answer is very rarely.

At market extremes people tend to get very caught up of what could happen. Just a few weeks ago everybody was rising price targets everywhere and people were screaming buy buy buy. Now we see people getting ever more bearish and calling for ever lower price targets. Stop. It’s pointless making grandiose predictions right now and get caught up in them. Yes, anything can happen, and I also remain very much open to a structural bear case, having made it repeatedly on the way up and calling out the risks.

We are engaged in a massive battle for control here between central banks, the structural problems in the global economy and now a crisis that has popped on the scene out of the blue.

Markets may appear to be in panic mode right now, but that doesn’t mean we need to be. Rather our job is exactly the opposite. To keep calm and not lose sight of the bigger picture, and most importantly: Not lose sight of the technicals as they help guide us through this mess.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Cali Governor Bars ‘Grand Princess’ Cruise Ship From Docking As Passengers Show Virus Symptoms

As we noted earlier, Cali Gov. Gavin Newsom has ordered the ‘Grand Princess’ cruise ship to remain offshore until all its passengers can be tested for the virus. We were one of the first media organizations to link the death of a 71-year-old man in California to the investigation into a previous voyage of the cruise ship and its connection to one of the patients.

Now, Fox 2 KTVU is reporting that several passengers aboard the ship are displaying flu-like symptoms.

In fact, two women have posted a YouTube video from their cabin, saying they are experiencing typical cold symptoms, but that they do not have a fever. They said in the video that they were tested for the virus, but told they didn’t have it.

In other news, Hawaii has become the fourth state to declare a state of emergency over the virus, even though no cases have been confirmed in Hawaii yet, despite several scares. But Hawaii Gov. David Ige said the declaration would allow the state to better prepare.

Regarding the latest case confirmed in California, that of an LAX airport screener, officials reportedly can’t tell if he contracted the virus at work, or “in the community” – which is extremely discouraging, if you ask us.

Cali has reported 53 cases so far.

The Grand Princess currently has 2,500 passengers. The number of crew is unclear.

In a statement, Princess Cruises said there are no confirmed cases and that only 100 individuals have been “identified for testing.”

“There are fewer than 100 guests and crew identified for testing, including all in-transit guests… those guests and crew who have experienced influenza-like illness symptoms on this voyage, and guests currently under care for respiratory illness,” the statement said.

So Newsom is going to let thousands de-board after testing a smattering of 100 people out of more than 3,000. Sounds like a great ‘containment’ plan.

We’re also starting to wonder how Carnival Cruise, which owns Princess cruises, is going to deal with this latest crisis?

Sen. Elizabeth Warren (D–Mass.) announced today that is dropping out of the presidential race. Warren ran on a platform of arch-technocratic progressivism coupled with identity politics, and her steady release of proposals drove much of the race’s policy discussion.

But after briefly rising to the top of the polls last fall, Warren’s campaign fell into a steady decline; she failed to expand her appeal beyond a core group of highly educated upper-middle-class voters. If elected, Warren promised to be a president who had mastered both the minutiae of governance and the social habits and language of the liberal elite. Her failure is a reminder that even Democratic voters don’t want a woke policy wonk in the White House.

Although she distinguished herself from the explicit socialism of Sen. Bernie Sanders (I–Vt.), her closest rival, by insisting that she was a capitalist “to her bones,” Warren never really demonstrated much fondness for markets. More often than not, she appeared to view them as an inherently corrupt system that required aggressive management from an enlightened expert class. Warren was a capitalist who hated capitalism.

No policy represented this worldview more than her wealth tax, a two-percent tax on households worth above $50 million, with an additional surcharge of 3 percent (later raised to 6 percent) on households worth more than $1 billion. Warren advertised the proposal as a fair, straightforward way to raise approximately $2.75 trillion tax revenue to pay for her education plans. All she wanted, she said, was for the very wealthy to pay a simple two-cent tax.

But behind the scenes, the tax was hardly simple: It would require the government to accurately value unique assets, an inherently complex task that would require a giant new tax collection infrastructure. The revenue estimates drew intense criticism from economists across the ideological spectrum, including former Obama administration adviser Lawrence Summers, who argued that it would not raise nearly as much money as Warren expected, leading to shortfalls and deficits. Other analysts warned that, over time, the bulk of the tax burden would fall on workers in the form of lost jobs and wages. And Warren’s supporters made little effort to hide the idea that the tax was primarily punitive, designed as much to degrade fortunes as to raise revenue.

It was health care, however, that sent Warren’s campaign into its eventual death spiral. After endorsing Sanders’ Medicare for All plan, a government-run system that would eliminate virtually all private insurance in four years, Warren was repeatedly pressed on the question of how to pay for the more than $30 trillion in estimated new government spending the idea would require.

Initially, Warren hedged in ways that made it obvious she was avoiding the question and had merely hoped to bandwagon with Sanders, peeling off some of his voters without taking full ownership of the issue herself.

Eventually, she released a plan that was simultaneously convoluted to the point of being unworkable and bad on the merits. After significant criticism, Warren released a second plan that called for implementing Medicare for All, a difficult political task in the most promising of circumstances, several years into her presidency. It was a tacit admission that she wouldn’t pursue single-payer health care at all.

Warren’s have-it-both-ways approach had become a trap. Voters who didn’t want Medicare for All believed she was for it; voters who did believed she wasn’t genuinely invested in the issue. In a race that often revolved around health care policy, Warren had put herself in a no-win position.

As her polling dipped, Warren ended up in a separate fight with Sanders over a years-old conversation in which Warren claimed that Sanders said a woman couldn’t win the presidency. Sanders denied ever having said such a thing, and in a debate-stage conversation, Warren accused Sanders of having called her a liar. The squabble appeared to backfire on Warren. As Reason‘s Matt Welch wrote, “By leaking a private conversation with Sanders in a not-particularly-convincing attempt to make him look possibly sexist, Warren’s campaign is engaging in the same kind of bad-faith word-policing that so many voters find off-putting.”

By the time voting started, Warren had slipped noticeably in the polls. She finished third in Iowa, fourth in New Hampshire and Nevada, and fifth in South Carolina. On Super Tuesday, Warren not only failed to win a single state; she finished behind both Sanders and former Vice President Joe Biden in her home state of Massachusetts.

Tonight, in her home state of Massachusetts, exit polling shows Elizabeth Warren:

– lost women to Biden by 10 points – lost "very liberal" voters to Sanders by 7 points – lost college + voters to Biden by 5 points – lost M4A supports to Sanders by 14 points

Warren won a high-profile dual endorsement from The New York Times, along with Sen. Amy Klobuchar (D–Mass.). But the Times endorsement was itself representative of the problems that plagued her campaign. Her strongest appeal was to the sort of people who write for The New York Times—highly educated, left-leaning, career-driven meritocrats who place a high-value on technocratic mastery. But even the Times editorial board couldn’t bring itself to exclusively endorse her. The dual endorsement seemed to suggest that she was a fine candidate—but not obviously the best one.

Warren’s weak performance made clear that her theory of the race was flawed: Both her strategy (to peel off persuadable Sanders voters while maintaining a nominal appeal to moderates) and her tactics (selective leaks against Sanders, Medicare for All two-stepping) weren’t working. It’s probably no surprise that voters concluded they didn’t want Warren, the plan-for-everything candidate, when her actual campaign didn’t go according to plan.

from Latest – Reason.com https://ift.tt/39vUzkY

via IFTTT

Sen. Elizabeth Warren (D–Mass.) announced today that is dropping out of the presidential race. Warren ran on a platform of arch-technocratic progressivism coupled with identity politics, and her steady release of proposals drove much of the race’s policy discussion.

But after briefly rising to the top of the polls last fall, Warren’s campaign fell into a steady decline; she failed to expand her appeal beyond a core group of highly educated upper-middle-class voters. If elected, Warren promised to be a president who had mastered both the minutiae of governance and the social habits and language of the liberal elite. Her failure is a reminder that even Democratic voters don’t want a woke policy wonk in the White House.

Although she distinguished herself from the explicit socialism of Sen. Bernie Sanders (I–Vt.), her closest rival, by insisting that she was a capitalist “to her bones,” Warren never really demonstrated much fondness for markets. More often than not, she appeared to view them as an inherently corrupt system that required aggressive management from an enlightened expert class. Warren was a capitalist who hated capitalism.

No policy represented this worldview more than her wealth tax, a two-percent tax on households worth above $50 million, with an additional surcharge of 3 percent (later raised to 6 percent) on households worth more than $1 billion. Warren advertised the proposal as a fair, straightforward way to raise approximately $2.75 trillion tax revenue to pay for her education plans. All she wanted, she said, was for the very wealthy to pay a simple two-cent tax.

But behind the scenes, the tax was hardly simple: It would require the government to accurately value unique assets, an inherently complex task that would require a giant new tax collection infrastructure. The revenue estimates drew intense criticism from economists across the ideological spectrum, including former Obama administration adviser Lawrence Summers, who argued that it would not raise nearly as much money as Warren expected, leading to shortfalls and deficits. Other analysts warned that, over time, the bulk of the tax burden would fall on workers in the form of lost jobs and wages. And Warren’s supporters made little effort to hide the idea that the tax was primarily punitive, designed as much to degrade fortunes as to raise revenue.

It was health care, however, that sent Warren’s campaign into its eventual death spiral. After endorsing Sanders’ Medicare for All plan, a government-run system that would eliminate virtually all private insurance in four years, Warren was repeatedly pressed on the question of how to pay for the more than $30 trillion in estimated new government spending the idea would require.

Initially, Warren hedged in ways that made it obvious she was avoiding the question and had merely hoped to bandwagon with Sanders, peeling off some of his voters without taking full ownership of the issue herself.

Eventually, she released a plan that was simultaneously convoluted to the point of being unworkable and bad on the merits. After significant criticism, Warren released a second plan that called for implementing Medicare for All, a difficult political task in the most promising of circumstances, several years into her presidency. It was a tacit admission that she wouldn’t pursue single-payer health care at all.

Warren’s have-it-both-ways approach had become a trap. Voters who didn’t want Medicare for All believed she was for it; voters who did believed she wasn’t genuinely invested in the issue. In a race that often revolved around health care policy, Warren had put herself in a no-win position.

As her polling dipped, Warren ended up in a separate fight with Sanders over a years-old conversation in which Warren claimed that Sanders said a woman couldn’t win the presidency. Sanders denied ever having said such a thing, and in a debate-stage conversation, Warren accused Sanders of having called her a liar. The squabble appeared to backfire on Warren. As Reason‘s Matt Welch wrote, “By leaking a private conversation with Sanders in a not-particularly-convincing attempt to make him look possibly sexist, Warren’s campaign is engaging in the same kind of bad-faith word-policing that so many voters find off-putting.”

By the time voting started, Warren had slipped noticeably in the polls. She finished third in Iowa, fourth in New Hampshire and Nevada, and fifth in South Carolina. On Super Tuesday, Warren not only failed to win a single state; she finished behind both Sanders and former Vice President Joe Biden in her home state of Massachusetts.

Tonight, in her home state of Massachusetts, exit polling shows Elizabeth Warren:

– lost women to Biden by 10 points – lost "very liberal" voters to Sanders by 7 points – lost college + voters to Biden by 5 points – lost M4A supports to Sanders by 14 points

Warren won a high-profile dual endorsement from The New York Times, along with Sen. Amy Klobuchar (D–Mass.). But the Times endorsement was itself representative of the problems that plagued her campaign. Her strongest appeal was to the sort of people who write for The New York Times—highly educated, left-leaning, career-driven meritocrats who place a high-value on technocratic mastery. But even the Times editorial board couldn’t bring itself to exclusively endorse her. The dual endorsement seemed to suggest that she was a fine candidate—but not obviously the best one.

Warren’s weak performance made clear that her theory of the race was flawed: Both her strategy (to peel off persuadable Sanders voters while maintaining a nominal appeal to moderates) and her tactics (selective leaks against Sanders, Medicare for All two-stepping) weren’t working. It’s probably no surprise that voters concluded they didn’t want Warren, the plan-for-everything candidate, when her actual campaign didn’t go according to plan.

from Latest – Reason.com https://ift.tt/39vUzkY

via IFTTT

Plaintiff’s essential allegation is that Google violated Plaintiff’s First Amendment rights by temporarily suspending its verified political advertising account for several hours shortly after a Democratic primary debate. Plaintiff’s claim, however, “runs headfirst into two insurmountable barriers—the First Amendment and Supreme Court precedent.” Prager Univ. v. Google LLC, No. 18- 15712, 2020 WL 913661, at *1 (9th Cir. Feb. 26, 2020).

The First Amendment provides: “Congress shall make no law … abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble ….” “The First Amendment, applied to states through the Fourteenth Amendment, prohibits laws abridging the freedom of speech.” In effect, “the First Amendment means that government has no power to restrict expression because of its message, its ideas, its subject matter, or its content.”

Google is not now, nor (to the Court’s knowledge) has it ever been, an arm of the United States government. “The text and original meaning of those Amendments, as well as this Court’s longstanding precedents, establish that the Free Speech Clause prohibits only governmental abridgment of speech. The Free Speech Clause does not prohibit private abridgment of speech.” Manhattan Cmty. Access Corp. v. Halleck, 139 S. Ct. 1921, 1926 (2019) (emphasis in original).

Plaintiff alleges Google has become a state actor by virtue of providing advertising services surrounding the 2020 presidential election.

“Under [the Supreme] Court’s cases, a private entity can qualify as a state actor in a few limited circumstances—including, for example, (i) when the private entity performs a traditional, exclusive public function; (ii) when the government compels the private entity to take a particular action; or (iii) when the government acts jointly with the private entity.” Plaintiff’s argument is that, by regulating political advertising on its own platform, Google exercised the traditional government function of regulating elections. “To draw the line between governmental and private, this Court applies what is known as the state-action doctrine. Under that doctrine, as relevant here, a private entity may be considered a state actor when it exercises a function ‘traditionally exclusively reserved to the State.'”

Traditional government functions are defined narrowly. “It is not enough that the federal, state, or local government exercised the function in the past, or still does. And it is not enough that the function serves the public good or the public interest in some way. Rather, to qualify as a traditional, exclusive public function within the meaning of our state-action precedents, the government must have traditionally and exclusively performed the function.” “Under the Court’s cases, those functions include, for example, running elections and operating a company town.” There is no argument that webservices or online political advertising are traditionally exclusive government functions. Plaintiff argues that, by providing some restriction on political advertising on its platform, Google is in effect regulating elections.

Disclosure: I have represented Google as a lawyer, including in writing a white paper arguing that the First Amendment protects search engine results, though that is a different question than the one I’m discussing here; I have not been asked to blog about this, and I am speaking entirely for myself here.

from Latest – Reason.com https://ift.tt/2TFH77n

via IFTTT

Threats, propaganda and the Orwellian dissolution of social trust cannot stop a withdrawal from the status quo.

Longtime readers know I’ve had an active interest in what differentiates empires/nations that survive crises and those that collapse. There is a lively academic literature on this topic, and it boils down to three general views:

1. Collapse is typically triggered by an external crisis that overwhelms the empire’s ability to handle it. Absent the external shock, the empire could have continued on for decades or even centuries.

2. Crises that could have been handled in the “Spring” of rapid expansion are fatal in “Winter” when the costs of maintaining complex systems exceeds the empire’s resources.

3. Civilization is cyclical and as population and consumption outstrip resources, the empire becomes increasingly vulnerable to external shocks.

External shocks include prolonged severe drought, pandemics and invasion. In many cases, the empire is beset by all three: some change in weather that reduces grain harvests, a pandemic introduced by trade or military adventure and/or invasion by forces from far-off lands with novel diseases and/or military technologies and tactics.

More controversial are claims that political structures become sclerotic and top-heavy after long periods of success, and these bloated, brittle hierarchies lose the flexibility and boldness needed to deal with multiple novel challenges hitting at the same time.

We lack internal-political records for most empires that have collapsed, but those records that have survived for the Western and Eastern Roman Empires suggest that eras of stability breed political sclerosis which manifests as a bloated, parasitic bureaucracy or as ruthless competition between elites that were once united in the expansive “Spring” phase.

By the “Winter” phase, the elite hierarchy is willing to sacrifice the unity needed to survive for its own short-term advantage.

All of this applies directly to China, which is experiencing not just a public health crisis (Covid-19 pandemic) but a host of overlapping crises triggered by the epidemic.

The external shock of the coronavirus has revealed the fragilities and weaknesses of China’s social, political and financial orders. These include:

1. Healthcare system crisis. The system is a patchwork that leaves non-government workers largely on their own. One doctor in Wuhan reported that a pregnant woman in his care died when the family ran out of cash for her care. (The central government announced it would cover all costs shortly after the patient died.)

The for-profit nature of much of the healthcare system is not widely understood outside China. If you want high-quality care without long waits, you must have cash.

Additionally many of the “doctors” are trained only in traditional Chinese medicine, so there is a shortage of trained personnel and facilities.

2. Food system crisis. It’s not just Swine Fever that’s straining the system; shortages are widespread and rising costs have been crimping working-class household budgets for the past few years.

3. Economic crisis: consumption and exports. As employers slash wages or close down, incomes fall and the trauma of the pandemic doesn’t engender a mindset of rampant consumption. The authorities are desperate to ramp up new car sales, for example, but everyone who can afford a car in China already has one. Demand was stagnant even before the virus.

As for the export economy: companies were already relocating abroad as a result of the trade war with the U.S. There is no reason for production that leaves to ever return to China, and there is no other source of employment and revenue to replace the export production that leaves.

On top of that structural erosion, China has adopted the just-in-time supply chain, and so it’s unprepared to deal with the chaos as the supply chain is disrupted four layers deep.

4. Financial / debt crisis: local government debt, shadow banking defaults. China fueled its expansion since 2016 with unprecedented amounts of debt and speculation. Any activity dependent on debt and speculation is exceedingly vulnerable to disruption, as debt payments that can’t be made trigger defaults which then collapse the pyramid of speculation built on the shaky foundation of debt.

This is especially problematic in China, where the shadow banking system of informal, non-institutional credit is so vast and pervasive. Private debts that default trigger defaults in the formal banking sector as counterparties fail to make good: if I fail to make my private-loan payment to you, you can’t make your bank loan payment.

China’s central bank can print money but it can’t force bankrupt companies to borrow more or bankrupt lenders to issue loans to unqualified borrowers. The entire pyramid of debt in China could collapse even as the government prints money with abandon.

5. Social contract crisis: loss of trust in authorities and institutions. That the central government/Communist Party failed the citizenry is obvious. The Party betrayed the people to protect its own image, destroying the citizens’ trust.

As I’ve noted before, betrayal has consequences. There is no quick or easy way to restore what has been lost in terms of trust and faith that the social contract between parasitic rulers and the ruled is worth restoring.

6. Housing bubble popping, threatening household wealth. Household wealth in China is concentrated in housing, and so the bursting of the housing bubble will have an extraordinarily adverse impact on household wealth and the “wealth effect” of people spending freely because they feel wealthier as their home rises in value.

The hope that the housing sector, already stagnating before the epidemic, will quickly roar back to life is completely unrealistic. Bubbles always burst, and this external shock has the potential to pop China’s vast housing bubble.

7. High expectations dashed; confidence in the future dented. I’ve often written about the extremely high expectations of the Chinese people, which have only increased after three decades of uninterrupted growth. Low expectations prepare people for disappointment and are thus reservoirs of resilience; high expectations set people up for shattering losses of faith in institutions and the future.

8. Loss of international reputation/stature. The perceptions of China as a rising superpower on the move have been dismantled and replaced by a perception of autocratic incompetence, massive centralized bureaucratic failure, an elite willing to sacrifice its citizenry and a government that cannot be trusted, a government that will lie and fabricate whatever statistics it deems most salutary for its image.

The Party’s transparent efforts to improve the optics with ham-handed propaganda only strengthens the world’s perception of incompetence and bumbling, untrustworthy elites.

In sum, the loss to China’s so-called “soft power” is consequential. Whatever doubts other nations held about China’s reliability and oppressive demands have now been confirmed.

Ironically, China’s leaders are loathe to “come clean” as that would entail a loss of face. But maintaining a desperately thin charade of bogus propaganda and fabricated statistics only serves to destroy the last shreds of domestic and international legitimacy.

China’s leadership has proven adept at handling one crisis at a time during China’s “Spring” and “Summer” growth phases, but that is no guarantee that the leadership has the wherewithal to manage multiple overlapping crises in “Winter.”

The Communist Party leadership centered around President Xi has constructed a technological wonder of Orwellian social control, but this may well prove to be the leadership’s Maginot Line, a vast defense against a previous era’s violent social disorder that is incapable of controlling the erosion of legitimacy and confidence.

This technological wonder of Orwellian social control is defenseless against a population that simply opts out of returning to work and borrowing immense sums to gamble on future “growth.” Stalinist dependence on fear to compel political obedience does not create legitimacy, trust or confidence.

Threats, propaganda and the Orwellian dissolution of social trust cannot stop a withdrawal from the status quo. If workers opt out of returning to work, and households opt out of borrowing more money, that will undermine the economy and thus the social order. There is no police force large enough to force everyone to return to work and no mechanism to force people to borrow money to gamble in speculative ventures. A quiet withdrawal is a social movement that cannot be suppressed with traditional force or dissipated with propaganda no one believes.

This applies not just to China but to every nation struggling with the pandemic, a roster that will soon include virtually every major nation on Earth.

Plaintiff’s essential allegation is that Google violated Plaintiff’s First Amendment rights by temporarily suspending its verified political advertising account for several hours shortly after a Democratic primary debate. Plaintiff’s claim, however, “runs headfirst into two insurmountable barriers—the First Amendment and Supreme Court precedent.” Prager Univ. v. Google LLC, No. 18- 15712, 2020 WL 913661, at *1 (9th Cir. Feb. 26, 2020).

The First Amendment provides: “Congress shall make no law … abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble ….” “The First Amendment, applied to states through the Fourteenth Amendment, prohibits laws abridging the freedom of speech.” In effect, “the First Amendment means that government has no power to restrict expression because of its message, its ideas, its subject matter, or its content.”

Google is not now, nor (to the Court’s knowledge) has it ever been, an arm of the United States government. “The text and original meaning of those Amendments, as well as this Court’s longstanding precedents, establish that the Free Speech Clause prohibits only governmental abridgment of speech. The Free Speech Clause does not prohibit private abridgment of speech.” Manhattan Cmty. Access Corp. v. Halleck, 139 S. Ct. 1921, 1926 (2019) (emphasis in original).

Plaintiff alleges Google has become a state actor by virtue of providing advertising services surrounding the 2020 presidential election.

“Under [the Supreme] Court’s cases, a private entity can qualify as a state actor in a few limited circumstances—including, for example, (i) when the private entity performs a traditional, exclusive public function; (ii) when the government compels the private entity to take a particular action; or (iii) when the government acts jointly with the private entity.” Plaintiff’s argument is that, by regulating political advertising on its own platform, Google exercised the traditional government function of regulating elections. “To draw the line between governmental and private, this Court applies what is known as the state-action doctrine. Under that doctrine, as relevant here, a private entity may be considered a state actor when it exercises a function ‘traditionally exclusively reserved to the State.'”

Traditional government functions are defined narrowly. “It is not enough that the federal, state, or local government exercised the function in the past, or still does. And it is not enough that the function serves the public good or the public interest in some way. Rather, to qualify as a traditional, exclusive public function within the meaning of our state-action precedents, the government must have traditionally and exclusively performed the function.” “Under the Court’s cases, those functions include, for example, running elections and operating a company town.” There is no argument that webservices or online political advertising are traditionally exclusive government functions. Plaintiff argues that, by providing some restriction on political advertising on its platform, Google is in effect regulating elections.

Disclosure: I have represented Google as a lawyer, including in writing a white paper arguing that the First Amendment protects search engine results, though that is a different question than the one I’m discussing here; I have not been asked to blog about this, and I am speaking entirely for myself here.

from Latest – Reason.com https://ift.tt/2TFH77n

via IFTTT

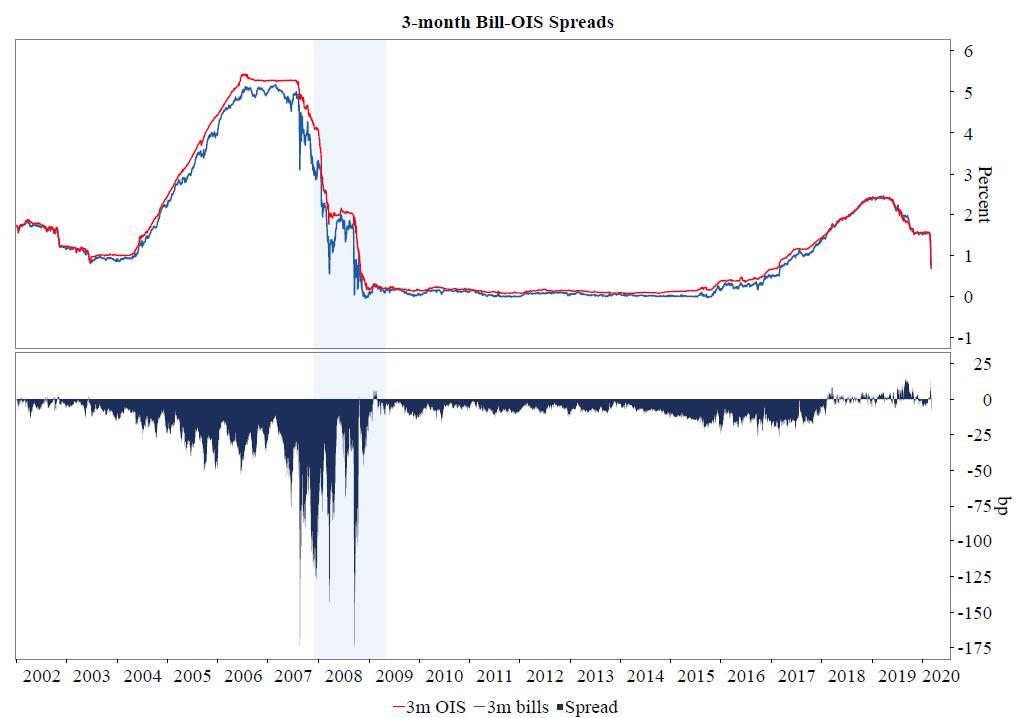

Fed Is Now Trapped: If Powell Fails To Taper “Not-QE”, He Will Admit It Was “QE 4” All Along

The unexpected scramble by dealers to obtain repo funding in recent days has taken the market, and especially STIR traders by surprise: after all, the primary catalyst behind the Fed’s decision to (emergency) cut by 50bps was to ease financial conditions. And yet the record oversubscribtion in both term and overnight repos in the past few days confirms that contrary to the Fed’s expectations, market liquidity has in fact deteriorated sharply.

And yet, as liquidity gets worse in response to the coronavirus market shock and, paradoxically, the Fed’s rate cut, the Fed faces a conundrum: will it continue tapering its repo operations and the permanent purchases of T-Bills, as it promised previously it would… or will the Fed capitulate and no only no longer taper, but in fact boost the availability of these products.

Herein lies the rub: if the Fed does in fact capitulate as most expect it to do, it will be effectively admitting that “Not QE” was in fact QE4 all the time, as this website and a handful of other Fed critics have claimed all along, and will make yet another mockery of all those finance hacks who, living in their mom’s basement, claimed that the Fed’s QE4 was not in fact QE4.

Addressing precisely this issue, on Thursday morning BMO’s rates strategist Jon Hill discusses the recent divergence in the 3M Bill-OIS spread…

… and touches on the various factors that he thinks would have an impact on a possible compression of the front-end Treasury/OIS spread, where he highlights “the possibility the Fed calls off tapering the bill purchase program”, although as noted above, he admits doing so would signal the Fed’s critics were right all along, and would be a prelude to the Fed losing even more credibility. To wit:

We still believe that the Fed will follow through on its forward guidance and taper its non-QE program. In their minds (and ours) this is not a facility designed to ease financial conditions, but rather one to address a reserve scarcity that emerged in September last year. To deviate from their tapering schedule would be to either tacitly acknowledge that it’s been shadow QE this whole time or further capitulate to some in the market’s interpretation of what the demand represents. That said, the probability that the tapering never occurs is clearly non-zero, if only because of the Committee’s extreme reticence to startle the market at this extremely precarious moment.

While in BMO’s mind, this facility may have been designed to address reserve scarcity, in “our mind” we have made it abundantly clear that the Fed’s non-QE POMO, i.e., T-Bill monetization, was meant to goose stocks all along, even if the Fed would never dare admit it. In other words, it was QE-4 all along. And we are certain that when the time comes in a few weeks, the Fed will prove us right by refusing to taper, as doing so would result in another market crash catalyst, an outcome the Fed is doing everything in its power to avoid.