John McGinnis wrote an essay for Law & Liberty, titled “The Empire Strikes Back Against Originalism.” I encourage you to read it. John provides a thorough summary of how originalism stands today in our legal order, and how its critics are coming to grips with it. Much of the essay focuses on a recent New York Times Magazine article by Emily Bazelon. (James Phillips and I were quoted by Bazelon.) Here is an excerpt:

Bazelon is often caught in a time warp in her criticisms of originalism, as if we were still in the infancy of its revival without the benefit of mature scholarship responding to opponents’ claims. She says that Brown v. Board is inconsistent with originalism without even addressing the scholarship, like Michael McConnell’s, that argues that it is not. She suggests that originalism will necessarily require a wholesale repudiation of precedents that undergird the modern state without taking account of work like my own and Mike Rappaport’s that identifies a role for precedent within originalist theory.

But the strongest evidence of the strength of originalism is that much of her criticism of the current Court comes from originalists or originalist methods. She quotes my colleague, the originalist Steven Calabresi criticizing an opinion of Justice Scalia’s as getting history wrong. Similarly, she objects to Gorsuch’s Gundy v. United States dissent, which cast doubt on the breadth of Congress’ authority to delegate legislative power to the executive, by quoting work from two scholars at Michigan Law School who argue that the original Constitution did indeed permit such delegations. She also argues that a study of the linguistic record of “keep and bear arms” at the time of the Second Amendment shows that the phrase was used in a military context. Unfortunately, she does not assess the correctness of these contending positions (she would have more space if she left out Gorsuch’s car, home, and work as a private litigator). But all these criticisms are actually disputes about original meaning, not rejections of it.

Disagreement about meaning does not mean that the Constitution is indeterminate. Indeed, because original meaning depends on facts, it is, in principle, ascertainable, unlike the personal values that other judicial decision-making approaches require judges to use when deciding which of many inconsistent precedents to apply.

I whole-heartedly agree with John. The debates we have today are originalist debates. The Constitution may mean one thing or the other, but it has a meaning, which we can ascertain. Read the entire piece.

from Latest – Reason.com https://ift.tt/39rSgzo

via IFTTT

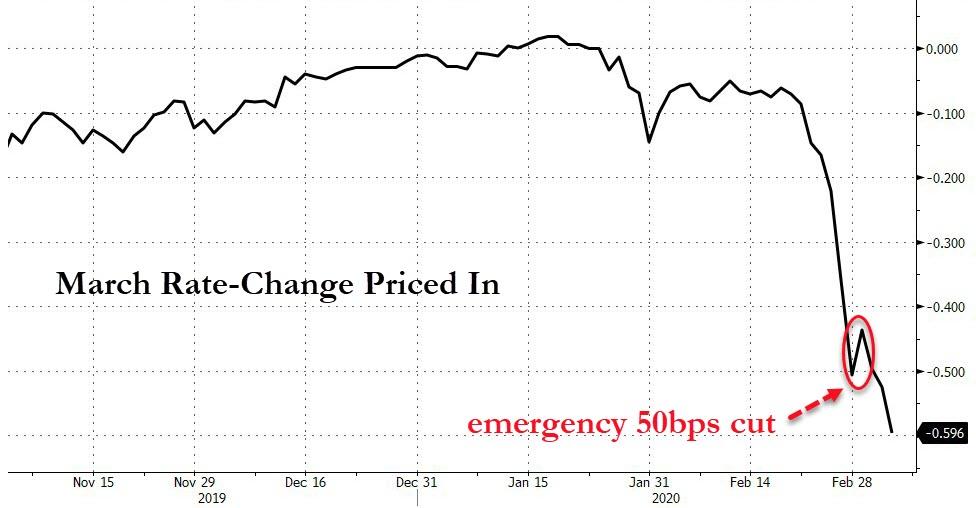

Stop and pause for a moment and think about what just happened. The Federal Reserve says the US economy is strong, but it just initiated emergency monetary policy last seen during the worst financial crisis since the Great Depression.

Something doesn’t add up.

The Fed cut rates 50 basis points on Tuesday. It was the first interest rate move between regularly schedule FMOC meetings since the 2008 financial crisis. The Fed funds rate now stands between 1.0 and 1.25%.

The decision to cut rates was unanimous.

As the Wall Street Journal pointed out, this kind of Federal Reserve move has been reserved for “when the economic outlook has quickly darkened, as in early 2001 and early 2008, when the US economy was heading into recession.” The 50-basis point cut was the first cut of such magnitude since December 2008. Pacific Management investment economist Tiffany Wilding called it a “shock-and-awe approach.”

It may have been shocking, but the results weren’t awesome.

Stocks tanked anyway.

The Dow Jones closed down 785.91 points, a 2.94% plunge. The S&P 500 fell 2.81%. The Nasdaq experienced a similar drop, closing down 2.99%.

Meanwhile, gold rallied, quickly pushing back above $1,600 and gaining over $50. Wednesday morning, the yellow metal was knocking on the door of $1,650.

Bond yields sank again as investors continued their retreat into safe-havens. The yield on the 10-year Treasury dipped below 1%.

In a press conference after the announcement, Federal Reserve Chairman Jerome Powell said the central bank “saw a risk to the economy and chose to act.”

“The magnitude and persistence of the overall effect on the US economy remain highly uncertain and the situation remains a fluid one. Against this background, the committee judged that the risks to the US outlook have changed materially. In response, we have eased the stance of monetary policy to provide some more support to the economy.”

Just the day before, Powell hinted at the possibility of a rate cut while insisting “The fundamentals of the US economy remain strong. However, the coronavirus poses evolving risks to economic activity.”

Mises Institute senior editor Ryan McMaken pointed out that Powell’s statement sounds an awful lot like John McCain in September 2008 when he said, “The fundamentals of our economy are strong, but these are very, very difficult times.”

McMaken raises the crucial question: If fundamentals are so strong, why the need to enact the biggest rate cut in more than a decade?

And further, “If the Fed is slashing interest rates while ‘fundamentals are strong,’ what must it do when things aren’t so ‘strong?’ Negative rates and QE seem to be the logical next step.”

In his podcast Tuesday, Peter Schiff put it another way.

You shoot your bullets at Super Man and they bounce off his chest; then what do you do?”

Schiff said his first reaction was, “They’re going to need a bigger rate cut.”

Just like the guy from Jaws, ‘We’re gonna need a bigger boat to catch this shark,’ the Fed is going to need a much bigger rate cut if they want to stop this bear market.”

But Schiff said he doesn’t think there’s a big enough rate cut to do it.

I think the air is coming out of this bubble. As I said, the coronavirus was the pin. At this point, it doesn’t matter what happens to the pin. They could find a cure for the virus. It doesn’t matter. Once the pin pricks the bubble, doesn’t matter what happens to the pin. What matters is the air is now coming out of that bubble and that’s exactly what’s happening.”

From a practical standpoint, it remains unclear how an interest rate cut will solve the potential economic problems associated with coronavirus. It appears that the move was primarily intended to rescue the financial markets. This is not unlike the way the Fed moved when stocks started to tank in the fall of 2008. In a rather convoluted statement, Powell even conceded that rate cuts won’t address the specific economic issues raised by the virus.

A rate cut will not reduce the rate of infection. It won’t fix a broken supply chain. We get that. But we do believe that our action will provide a meaningful boost to the economy.”

The real worry for the Fed is that the stock market will pull the economy down with it. After all, the central bank built the economic “recovery” after the 2008 financial crisis on a “wealth effect.” Easy money pumped up asset prices and made people feel richer. If that wealth effect unwinds, the underlying economy will likely unwind with it.

[ZH: the market is already pricing in 50bps more rate-cuts in March…]

Schiff said another concern is the amount of debt built up in the economy going into the next recession. Normally, during an expanding economy, people pay down debt. But over the last decade, Americans have piled on debt. The federal government is running trillion-dollar deficits. Consumer debt is at record levels. Rising levels of corporate debt have even set off warning bells at the Fed.

So, if we have another economic downturn, that debt is a much bigger problem than its ever been in other recessions. It’s likely going to cause a worse financial crisis than the one we had in 2008. And so to try to keep that from happening, the Fed is cutting rates, because it wants to make it easier for people who have debt to service that debt. And it also wants to delay the recession it knows we can’t survive.”

The Fed simply doesn’t have the bullets in its arsenal to fight a deep recession. That’s why it is firing them know, hoping to hold it off. But Schiff said the best-case scenario is that they buy some time. To do that, they’re going to need bigger rate cuts.

Senators Admit US Virus Test Rollout Goals Won’t Be Met: “It’s Way Smaller Than A Million”

Just as we warned two days ago, the Trump administration won’t be able to meet its promised timeline of having a million coronavirus tests available by the end of the week, according to senators speaking after a briefing Thursday from health officials.

“There won’t be a million people to get a test by the end of the week,” Republican Senator Rick Scott of Florida said.

“It’s way smaller than that. And still, at this point, it’s still through public health departments.”

Bloomberg reports that Scott and other lawmakers said the government is “in the process” of sending test kits out and people still need to be trained on how to use them.

“By the end of the week they’re getting them out to the mail,” Republican Senator James Lankford of Oklahoma said.

“It’s going to take time to be able to get them, receive them, re-verify them and then be able to put them into use.”

As we noted previously, without the tests, it will take longer for public health officials to figure out how widespread the virus truly is, giving the market a false impression that containment efforts have been a success. The only problem is that containing a virus isn’t like negotiating a trade deal. While a certain amount of bluster is acceptable, at a certain point, you actually need to fix the problem.

And just yesterday, we reported, Dr. Fauci appeared on cable news and warned that the outbreak has likely reached “pandemic proportions” regardless of the WHO’s reluctance to label it accordingly.

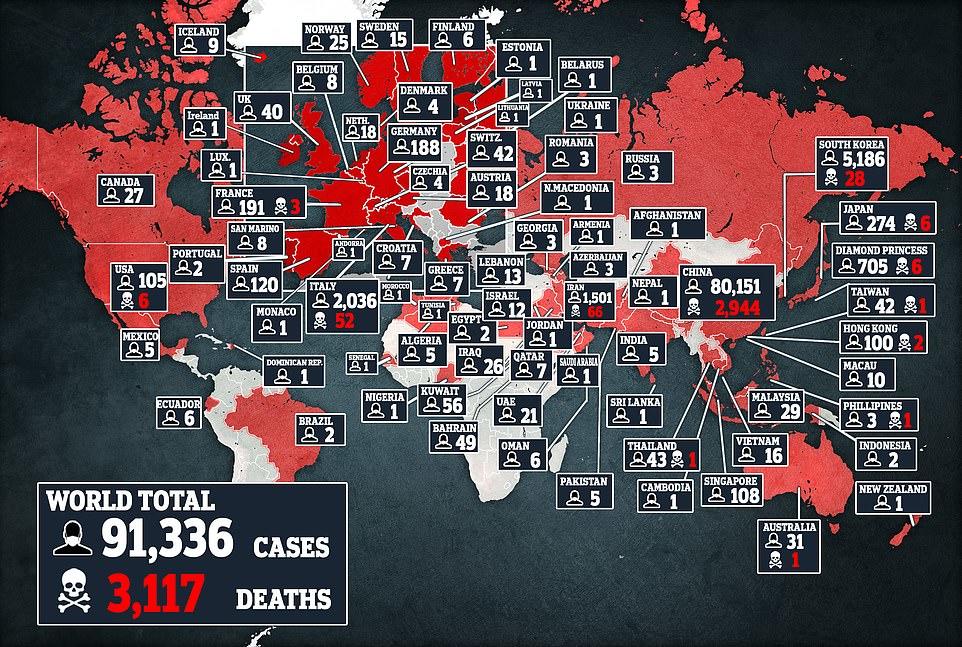

We haven’t seen anything cause this much worldwide fear in a really long time. But even though there is so much fear, we still don’t know if this is going to evolve into the next great global pandemic that kills millions of people or not. I wish that I had a definitive answer for you. At this point we do know that the number of confirmed cases outside of China continues to rise at a very alarming rate, and we also know that this virus is about 34 times more deadly than the flu according to the latest numbers. But in order for it to kill millions of people, a substantial percentage of the global population would have to be infected, and we don’t know if that is actually going to happen.

But in major cities around the globe where there has been an eruption of COVID-19 cases, we are seeing severe disruptions in normal activity.

For example, now that several coronavirus deaths have been reported in the area, the lack of tourists has turned downtown Seattle into “a ghost town”…

In Seattle, bracing for the coronavirus also means preparing for what could be a devastating economic impact. Business owners and residents have already seen a drop-off in tourists in areas of the city that heavily depend on foot traffic.

“It’s like a ghost town,” Francisco said about the famous Pike Place Market where she has her shop.

If you have ever been to Pike Place Market, then you know that it is normally bustling with activity.

But now virtually everyone wants to stay away, and you can’t exactly blame them. With this virus on the loose, I wouldn’t want to venture down there either.

Seattle Mayor Jenny Durkan has already declared a state of emergency, and this will give her the power to cancel a wide range of public events…

As the death toll climbed Tuesday, Seattle Mayor Jenny Durkan, a Democrat, proclaimed a civil emergency. The declaration allows her to bypass regulations to increase city spending, contracting and borrowing to address the growing public health threat. It will also allow her office to close facilities and cancel events to prevent the virus from spreading further.

The streets of Seoul, the South Korean capital, stood nearly empty this week. Those who do venture out wear masks. The normally busy subways have few passengers and riders make sure to sit far away from one another. Many residents are relying on grocery and restaurant delivery apps.

Most Americans don’t realize this, but the population of Seoul actually exceeds the population of New York City.

Normally it is one of the busiest cities on the entire planet, but due to the fear that more than 5,700 confirmed cases in South Korea has caused, it has also become something of “a ghost town”.

Speaking of busy cities, Beijing’s 21 million residents continue to wait for life to return to normal.

Most people are staying home as much as possible, and those that do venture out risk having their temperatures scanned “at regular checkpoints”…

Many shops are still closed in Beijing, and residents’ temperatures are scanned at regular checkpoints, as well as inside each store. On streets that are normally so crowded that people are forced to brush shoulders, those who are out keep a good distance from one another.

Could you imagine the uproar that would ensue if similar “checkpoints” were set up here in the United States?

In Milan, Italy’s business capital and the center of the country’s outbreak, restaurants, bars and train stations are much less crowded than normal. The usually teeming Piazza del Duomo, home to the city’s cathedral and lined with shops and bars, was almost empty at points Monday.

Italian authorities are absolutely desperate to get this outbreak under control, and so they are implementing pretty extreme measures.

Incredibly, that even includes banning fans from all sporting events until April 3rd…

The Italian government have taken drastic measures to help prevent the outbreak of coronavirus by closing all sport events to fans throughout the entire country until April 3. Italy has been the worst-hit European country from the coronavirus, with 107 deaths so far.

It is nice that they have set a deadline, but what are they going to do if we get to April 3rd and this outbreak has gotten even worse?

Could it be possible that Italian fans will not be able to attend sporting events for the foreseeable future?

And will other western countries soon follow suit?

Our lives could be about to change in ways that we couldn’t even imagine just a few weeks ago.

Britons could be forced to put their lives on hold for three months under a ‘battle plan’ to combat Coronavirus amid warnings today that the deadly disease could incapacitate a fifth of the UK’s workforce.

Boris Johnson today set out the Government’s blueprint to deal with a mass outbreak of the bug that includes a raft of socially and economically costly contingency moves as a last resort.

Could you put your life on hold for three months?

Of course most major pandemics last longer than just three months. In fact, the Spanish Flu pandemic lasted for three years and it killed tens of millions of people.

Hopefully this outbreak will not be anything like that.

But without a doubt, this is a truly horrible virus. The following is an excerpt from the account of a 25-year-old British man that actually caught COVID-19…

Day 12: I’ve had a relapse. Just as I thought the flu was getting better, it has come back with a vengeance. My breathing is laboured. Just getting up and going to the bathroom leaves me panting and exhausted. I’m sweating, burning up, dizzy and shivering. The television is on but I can’t make sense of it. This is a nightmare.

By the afternoon, I feel like I am suffocating. I have never been this ill in my life. I can’t take more than sips of air and, when I breathe out, my lungs sound like a paper bag being crumpled up. This isn’t right. I need to see a doctor. But if I call the emergency services, I’ll have to pay for the ambulance call-out myself. That’s going to cost a fortune. I’m ill, but I don’t think I’m dying — am I?

I certainly do not want to experience that, and I am sure that you do not want to either.

Coming into this year, I warned about what was ahead, but I definitely did not anticipate that we could potentially be facing a full-blown global pandemic by early March.

Donald Trump’s reelection campaign says The Washington Post defamed the president. It’s truly the golden era of frivolous defamation suits filed by political figures and groups who wish to quash free speech that doesn’t suit them. (Sigh. Scream.) The latest of these legally dubious—but nonetheless threatening—endeavors comes from the Trump 2020 presidential campaign. After suing The New York Times for alleged libel last month, Donald J. Trump For President Inc. has now filed a complaint against The Washington Post.

In both cases, the president’s people object to opinion pieces that were clearly labeled as such. Op-eds aren’t immune from libel claims. But for something to rise to the level of defamation against a public figure (especially one so thoroughly public and newsworthy as the president of the United States), the item published must not only be false and reputation-damaging; it must issue from an entity that knew it was false and maliciously published it anyway.

As C.J. Ciaramella noted in February, “Trump has repeatedly opined that libel laws need to be ‘opened up’ to remove the strong protections that news outlets have enjoyed from defamation lawsuits since the landmark 1964 Supreme Court case New York Times v. Sullivan.”

Since that case, “the American system of libel law has made it harder for public officials and public figures to recover,” explains attorney Mike Godwin:

The theory is that the First Amendment provides stronger protections when people utter—or publish—critical opinions about politicians. This long-standing precedent does not please President Trump, who’d like to make it easier to sue his critics for libel (and win), and it recently has been criticized by Justice Clarence Thomas.

The new case, filed in the U.S. District Court for the District of Columbia, alleges that The Washington Post “published false and defamatory statements of and concerning the Campaign in two articles published in June 2019.”

One piece, published June 13, 2019, concerned Special Counsel Robert Mueller’s report on Russia and the Trump 2020 campaign (released last April). The lawsuit objects to a sentence in which the op-ed author characterized the report as saying the campaign “tried to conspire” with Russia.

The second piece concerned the 2020 election. The suit objects to this line: “Who knows what sort of aid Russia and North Korea will give to the Trump campaign, now that he has invited them to offer their assistance?”

It concludes that the newspaper published these pieces “as part of a systematic campaign of bias” against the Trump campaign.

Even if there’s little chance Trump’s campaign will prevail here, suits like these send a chilling message to journalists and publishers, especially when they’re effectively coming from the leader of the country.

Bye bye, Bloomberg! (And good riddance!) Former New York Mayor Michael Bloomberg quit his presidential campaign on Wednesday after failing to gain the Super Tuesday boost he was seeking.

Former Vice President Joe Biden ultimately got the most delegates on Super Tuesday, securing approximately 670. His chief rival, Sen. Bernie Sanders (I–Vt.), got 589.

QUICK HITS

The Consumer Financial Protection Bureau is on trial.

Donald Trump’s reelection campaign says The Washington Post defamed the president. It’s truly the golden era of frivolous defamation suits filed by political figures and groups who wish to quash free speech that doesn’t suit them. (Sigh. Scream.) The latest of these legally dubious—but nonetheless threatening—endeavors comes from the Trump 2020 presidential campaign. After suing The New York Times for alleged libel last month, Donald J. Trump For President Inc. has now filed a complaint against The Washington Post.

In both cases, the president’s people object to opinion pieces that were clearly labeled as such. Op-eds aren’t immune from libel claims. But for something to rise to the level of defamation against a public figure (especially one so thoroughly public and newsworthy as the president of the United States), the item published must not only be false and reputation-damaging; it must issue from an entity that knew it was false and maliciously published it anyway.

As C.J. Ciaramella noted in February, “Trump has repeatedly opined that libel laws need to be ‘opened up’ to remove the strong protections that news outlets have enjoyed from defamation lawsuits since the landmark 1964 Supreme Court case New York Times v. Sullivan.”

Since that case, “the American system of libel law has made it harder for public officials and public figures to recover,” explains attorney Mike Godwin:

The theory is that the First Amendment provides stronger protections when people utter—or publish—critical opinions about politicians. This long-standing precedent does not please President Trump, who’d like to make it easier to sue his critics for libel (and win), and it recently has been criticized by Justice Clarence Thomas.

The new case, filed in the U.S. District Court for the District of Columbia, alleges that The Washington Post “published false and defamatory statements of and concerning the Campaign in two articles published in June 2019.”

One piece, published June 13, 2019, concerned Special Counsel Robert Mueller’s report on Russia and the Trump 2020 campaign (released last April). The lawsuit objects to a sentence in which the op-ed author characterized the report as saying the campaign “tried to conspire” with Russia.

The second piece concerned the 2020 election. The suit objects to this line: “Who knows what sort of aid Russia and North Korea will give to the Trump campaign, now that he has invited them to offer their assistance?”

It concludes that the newspaper published these pieces “as part of a systematic campaign of bias” against the Trump campaign.

Even if there’s little chance Trump’s campaign will prevail here, suits like these send a chilling message to journalists and publishers, especially when they’re effectively coming from the leader of the country.

Bye bye, Bloomberg! (And good riddance!) Former New York Mayor Michael Bloomberg quit his presidential campaign on Wednesday after failing to gain the Super Tuesday boost he was seeking.

Former Vice President Joe Biden ultimately got the most delegates on Super Tuesday, securing approximately 670. His chief rival, Sen. Bernie Sanders (I–Vt.), got 589.

QUICK HITS

The Consumer Financial Protection Bureau is on trial.

Illegal Immigrants Can Face Criminal Charges For Using Stolen Info On Tax Docs: Supreme Court

The Supreme Court ruled on Tuesday that illegal immigrants who use stolen personal information when filling out tax forms for employment can face criminal charges, despite federals laws which liberal justices say should protect those committing fraud, according to Fox News.

Federal law states that information “contained in” an I-9 work authorization form cannot be used for law enforcement, while the Immigration Control and Reform Act (IRCA) states that it’s a federal crime to lie on the document. On Tuesday, the Supreme Court ruled in a mixed decision that if workers use the same information in tax documents, they can face charges.

“Although IRCA expressly regulates the use of I–9’s and documents appended to that form, no provision of IRCA directly addresses the use of other documents, such as federal and state tax-withholding forms, that an employee may complete upon beginning a new job,” wrote Justice Samuel Alito in the court’s opinion. He was joined by fellow conservative justices John Roberts, Neil Gorsuch, Brett Kavanaugh and Clarence Thomas.

The IRCA also prohibits state or local charges or civil cases against “those who employ, or recruit or refer for a fee for employment, unauthorized aliens,” but Alito noted that this “makes no mention of state or local laws that impose criminal or civil sanctions on employees or applicants for employment.” –Fox News

The court was considering the case of Kansas v. Garcia, in which three illegal immigrants used a stolen Social Security number on their I-9 forms. The state dropped charges that used the forms as evidence and agreed not to use them during their trials – claiming that the law doesn’t prevent people from using someone else’s social security numbers on tax documents.

All three defendants in the case were convicted, which was upheld by the Kansas Court of Appeals – only to be reversed by the Kansas Supreme Court, which ruled that the charges were improper because “[t]he fact that this information was included in the W–4 and K–4 did not alter the fact that it was also part of the I–9.”

USSC Justice Alito found this logic to be faulty and overly restrictive.

“Taken at face value, this theory would mean that no information placed on an I–9— including an employee’s name, residence address, date of birth, telephone number, and e-mail address—could ever be used by any entity or person for any reason,” he wrote.

That seems to be the message from the equity markets, which have followed a strong US lead (S&P +4.2%) into the green. Does the rest of the world really benefit from the possibility of Joe Biden running against Donald Trump for the presidency in November though? I ask, as that is being touted as the proximate cause of the rally. (On which note, as I quipped to a friend and then immediately heard echoed on ABC’s “The View” in earnest, will Mike Bloomberg potentially be replacing Steven Mnuchin in 2021?) The rally certainly can’t have been based on anything actually going on around us apart from that.

If you want the perfect encapsulation of how our comfortable, services-based Western economy–whose elite haven’t suffered a real crisis (I mean one where people die on a large scale) in three generations–is being hit by Covid-19, consider that the latest Bond movie is seeing its release date pushed back by months because nobody is going to see it in April – and not just because of its title (…or because of traditional Hollywood reasons like it being as bad as ‘Spectre’, which would be a ‘Quantum of Solace’.)

If even Bond, James Bond is being pushed back by months, why not every other movie? Is anyone going to go to cinemas, theatres, pubs, restaurants, parties, festivals, hotels, conventions, sports events, etc., if this virus continues to spread? Of course, many events are still going ahead for now: SXSW in Texas, for example, or the Olympics,…apparently. Little green bits of paper take priority over little green viruses, despite the risk that this provides perfect conditions for Covid-19 to spread, and public-health havoc this will wreak. Yet some are being more proactive. Nobody in Italy will be seeing any movies for a while as all theatres are shut down, along with schools, and universities likely to follow. The elderly also being advised to stay inside.

Regardless, most of the West and the world continue to lag far behind the aggressive virus-containment tactics that China has employed, and the results are obvious.: case numbers and fatalities are growing exponentially, even with limited testing. Germany’s finance minister says this is “a global pandemic”, saving the WHO the work. In the US we now have 11 deaths, up from 1, and a state of emergency declared in New York, Washington, and Florida. No internal travel restrictions are being imposed though even as – so hope the person you sit next to at SXSW doesn’t come from one of those states.

As we published yesterday, at this stage the economic damage is done. Either governments close things down at great cost, as in China and Korea, or they don’t – and the virus and public panic close things down anyway. In the UK the Flybe airline has just collapsed – and like virus victims, this will only spread across the whole services sector.

As we also stressed, we are about to see a whole flurry of new virus-fighting policies, from the conventional to the unconventional to the ‘unconversational’ in response. Indeed, besides the 50bp cut from the Fed, we also got a 50bp cut from the BoC – but that is conventional and of almost no practical use right now. More to come regardless though.

We have seen fiscal stimulus packages in Malaysia and Korea, and the Chinese press talk about the potential for the mother of all stimulus packages (“despite the side-effects”) that would be larger than the USD574bn seen in 2008-09, although whether this means in USD terms of as a percentage of GDP is unclear. In the US we have seen USD7.8bn virus spending package passed, and in the UK statutory sick-pay changes have been introduced for those self-quarantining, although the self-employed are still out of luck.

The IMF is also announcing a USD50bn virus-fighting loan fund, which will be interest free and countries do not need to have an existing facility to tap it. This does not come with the usual IMF caveats about privatising SOEs, slashing subsidies, and cutting state spending on healthcare and pensions. Imagine how strong global growth might be if this kind of largesse was available when the IMF wasn’t afraid of dying.

On the unconventional side the Fed is obviously still doing ludicrous level of reverse repo, which shows that even despite slashing rates, there is massive market demand for USD liquidity, which central banks are obviously going to have to plug.

The ‘unconversational’ has already arrived too as the incoming BoE governor, who starts work 16 March, states that UK SMEs are at risk and that the Bank will need to step forward to support their supply chains: “We are going to have to move very quickly to do that,” he added. So the BoE has moved on from its original task of providing cheap funds to the British government during wars against France; from its expanded task of stoking the economy; from its follow-up role of keeping inflation at desired levels; and from its expanded mandate of financial stability, meaning bailing out the system during crises. Now is to directly support millions of British SMEs’ supply chains too?

It isn’t that this isn’t the right thing to do, because the alternative is a swathe of businesses closing, and a depression: to which surely any central bank not wishing to replay 1929 is going to say “No Time To Die”. The larger issue is how this can be done – and quickly. Loans to corner shops and family restaurants and small workshops and self-employed window cleaners will be channelled how exactly? On whose authority? By which bureaucracy? On what scale? On what terms? And how does one prevent fraud? Then how is one paid back? The implications are either that central planning banking is going to a whole new level; or that this cannot be done in developed markets, and hence we need to brace for the imminent economic fallout.

If so even Biden, Joe Biden won’t be able to save us with a gadget. It will be time for Ms. Funnymoney.

Put that together and it still says lower bond yields than we see now; lower stocks, presuming these are not also added to the list of central bank bailouts, which they might be; and wild FX swings ahead, which are most likely to end up with USD bobbing up again after first being pushed down.

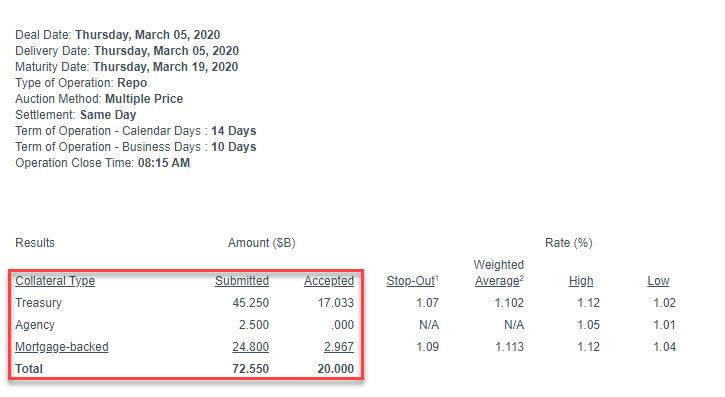

Term Repo Record Oversubscribed As Market Liquidity Craters

Yesterday, when discussing the most oversubscribed overnight term repo operation yet, in which dealers scrambled to obtain $111.5BN in liquidity from the Fed’s $100BN overnight repo operation, we said that it was “the second day in a row the overnight funding repo operation was oversubscribed (and it is virtually certain that tomorrow’s downsized term-repo will be oversubscribed as well).“

We were right, because moments ago not only did the Fed announce that the latest 14-day term repo was indeed oversubscribed, but it was in fact the most oversubscribed term-repo on record, surpassing even the funding needs indicated at the start of the repo crisis last September.

While the Fed tapered the size of the term-repo operation from $25BN to $20BN as we entered March, the demand for the liquidity it unlocks has not only refused to go down, but has in fact soared, and rose to an all time high of $72.6BN consisting of $45.25BN in Treasurys, $2.5BN in Agency and $24.8BN in MBS tendered to the Fed.

As a result, with the full amount of eligible liquidity, or $20BN, released, this meant that today’s term repo operation was 3.6x oversubscribed – the most on record.

This continuing liquidity crunch is bizarre, as it means that not only did the rate cut not unlock additional funding, it actually made the problem worse, and now banks and dealers are telegraphing that they need not only more repo buffer but likely an expansion of QE… which will come soon enough, once the Fed hits 0% rates in 2 months and restart bond buying.

Will that be enough to stabilize the market? We don’t know, but in light of the imminent corona-recession, on Tuesday Credit Suisse’s Zoltan Pozsar repo guru published a lengthy piece whose conclusion – at least on the liquidity front – is that the Fed should “combine rate cuts with open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary.“

In short, a liquidity avalanche is coming to prevent a market crash. It’s only a matter of time.