Mike Pence Wiped His Nose With His Hand Before Shaking Doctors Hands At Coronavirus Press Conference

The gist of how everyone wants you to respond to the coronavirus mostly boils down to normal hygiene: wash your hands, don’t touch your face and keep your distance from people that appear to be sick.

Vice President and coronavirus czar Mike Pence violated all of these rules in one fell swoop during last week’s coronavirus press conference when he wiped his nose with his hands, moments before shaking the hands of doctors on the stage tasked with combating the ongoing virus outbreak, according to The Independent.

Talk about setting the cause back…

Today at the corona virus press conference, @VP wiped his nose with his hands then proceeded to shake everyone’s hands 😳😅

Pence’s appointment has already been controversial, with many claiming he is “anti-science” and has a lack of medical experience.

Others have said he is dangerously slow to respond to health crises, as indicated by his response to an HIV/AIDS outbreak in his home state of Indiana while he was Governor.

Following this press conference last week, in which President Trump said the virus was under control, dozens of more cases and several deaths have been reported in the U.S.

In an interview yesterday with Bloomberg, Dr Anthony Fauci, the director of the National Institute of Allergy and Infectious Diseases, said coronavirus was at “pandemic” levels.

Perhaps self-confessed germophobe President Trump might consider “picking” someone different to lead the charge…

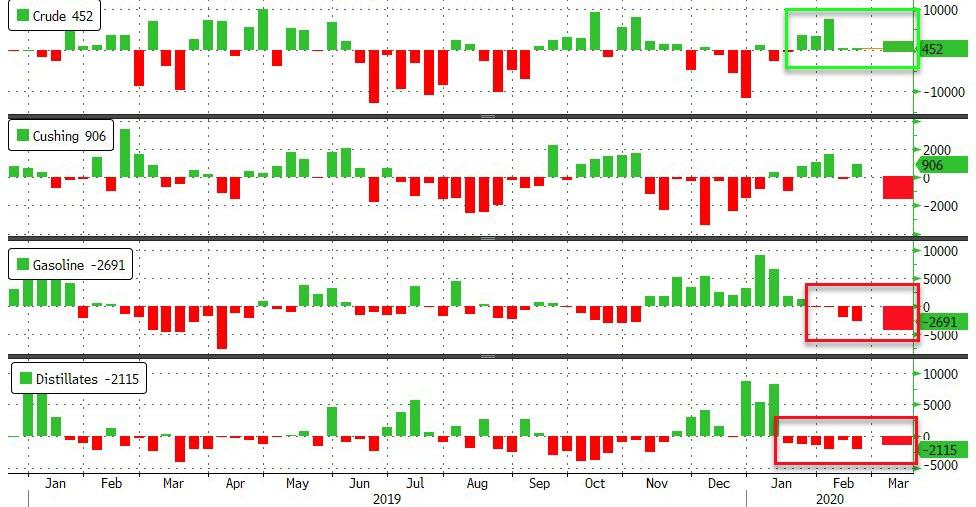

WTI Holds OPEC+ ‘Hope’ Gains After Smaller Than Expected Crude Build

Oil prices have been volatile in the last few days, rallying on an OPEC+ committee recommendation that the group agree to production cuts of up to one-million barrels per day (but Russia still on the fence about deeper cuts) when the group meets later this week.

“Concerns of weak demand are still present. We’ll be looking to see if exports slowed due to the coronavirus,” says Phil Flynn, senior market analyst at Price Futures Group.

For tonight, all eyes are once again on inventories for any signs of the start of the demand collapse hitting supplies.

API

Crude +1.69mm (+3mm exp)

Cushing -1.352mm

Gasoline -3.9mm (-1.87mm exp)

Distillates -1.7mm (-2mm exp)

Expectations were for crude inventories to rise for the 6th straight week and API confirmed that but the build was smaller than expected. However, major draws in products were notable…

Source: Bloomberg

WTI was hovering around $47.30 ahead of the API data and barely budged on the inventory data…

“While lower rates would marginally reduce costs of carrying oil inventory, this factor is modest in relation to the dramatic cut in petroleum demand that is currently being seen around the world,” analysts at Ritterbusch & Associates wrote in a Tuesday note.

Further on the downside, Goldman forecast a 150k b/d decline in oil demand in 2020 – the lowest annual growth rate since the 2008/2009 financial crisis, cutting its Brent forecast for Q2 to $47 (from %57).

The Fed’s move is “a sign that the economic fall out may be worse than expected,” said Phil Flynn, senior market analyst at The Price Futures Group.

“There seems to be a lot of uncertainty, but we know that ultimately the rate cut will stabilize the market,” he told MarketWatch. “Don’t be surprised if we get a snap back later.”

At current demand forecast, Goldman says current spot prices are already pricing in a 2m b/d production cut by OPEC in 2Q… which may be a little over-optimistic.

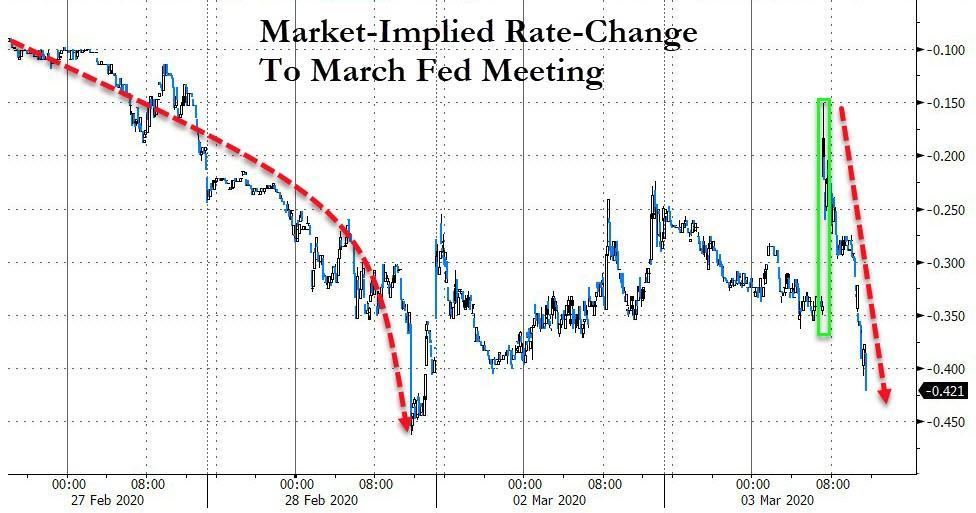

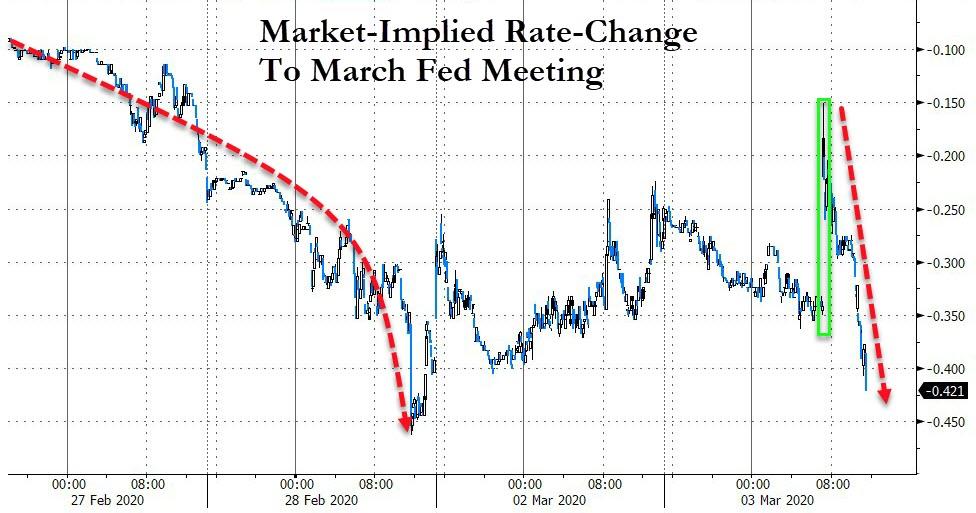

Fed Capitulates To Stock Vigilantes: Goldman Sees Two More Rate Cuts In Next Month

It’s damage control time for Jerome Powell: having cut 50bps on Tuesday, it’s first 50bps emergency, intermeeting rate cut since Oct 8, 2008, the peak of the financial crisis (which in turn followed another panicked, 75bps rate cut when Jerome Kerviel put on a couple of terrible trades and blew up SocGen), stocks jumped… for about 10 minutes and then crashed, leading to an outcome which BMO politely said was “not what Powell had in mind.”

A less polite observation is that Powell’s Fed – which for a few months appeared ready to undo the idiotic boom-bubble-bust policies of previous Fed chairs only to fold like a Made in Wuhan lawn chair after a little pressure from markets – finally shat the bed, and not only deployed a “bazooka” which turned out to be a sad water pistol, but the central bank now has about half the dry ammo it had this morning and stocks are tumbling.

And now, in just two short weeks the Committee will be faced with an even more difficult decision of either underwhelming investors’ expectations or quickly utilizing the limited rate-cutting potential afforded by the low outright yield environment.

Sure enough, having once again capitulated to the stock vigilantes, the market has already spoken and it will keep tantruming until it gets another 40bps, or almost two full rate cuts, in the March meeting, resulting in a fed funds rate of just above 0 entering April.

Goldman agrees: commenting on today’s shocking Fed announcement and market reversal, the bank’s chief economist Jan Hatzius writes that Fed Chairman Jerome Powell stated that risks from the coronavirus outbreak had “changed materially” after he cut by 50bps. He also termed the current policy stance “appropriate,” he also said “we are prepared to use our tools and act appropriately.” And while the near-term policy implications were somewhat ambiguous, in Goldman’s view, “the press conference was consistent with further Fed easing in coming months. We retain our forecast of another 50bp but are now penciling in 25bp moves on March 18 and April 29 (versus April and June previously).”

The full Goldman note confirming that the Fed has now capitulated to the stock vigilantes:

1. At the press conference following the Fed’s intermeeting decision to cut the funds rate by 50bp, Chairman Powell stated that the risks from the coronavirus outbreak to the US outlook had “changed materially,” and that the virus would “weigh on economic activity here and abroad for some time.” With regard to future policy moves, his message was somewhat ambiguous. On the one hand, he said that “we do like our current policy stance…we think it’s appropriate to support our dual mandate goals.” On the other hand, he noted that the Fed was “prepared to use our tools and act appropriately,” echoing the official statement. In response to a question on whether rate cuts would be effective in response to a supply shock, Chair Powell argued that Fed action would “provide a meaningful boost to the economy” and would help avoid a tightening in financial conditions. Chair Powell stated that the Fed would do its part to “keep the US economy strong as we meet this challenge” and that it was “possible” that there would be more formal coordination from policymakers going forward.

2. The mixed signals in the statement and press conference left the timing of future rate cuts somewhat ambiguous. Historically, a promise by the Fed to “act as appropriate” in response to a growth shock is a very strong signal of imminent cuts, especially when inflation is low. But Powell also described the current policy stance as “appropriate,” and he said that future changes depend on “the flow of events” and “a range of things.” Uncertainty is high across several dimensions—the Fed’s reaction function, the number of US cases to be reported in coming weeks, the extent of the weakness in upcoming US and global data, and financial conditions. But all things considered, our baseline expectations are an additional 25bp cut at the March 17-18 meeting followed by a 25bp cut in April (previously, we had expected both of these cuts in Q2).

Needless to say, if Powell does miraculously grow a spine by March 18 and for once surprises the market by refusing to be pushed around by stock bulls demanding ever more from the Fed, then watch out below.

And so castles made of sand fall in the sea, eventually.

– Jimi Hendrix

There’s a widespread belief out there that the U.S. and the global economy in general is on much sounder footing ever since the financial crisis of a decade ago. Unfortunately, this false assumption has resulted in widespread complacency and elevated levels of systemic risk as we enter the early part of the 2020s.

All it takes is a cursory amount of research to discover nothing was “reset” or fixed by the government and central bank response to that crisis. Rather, the entire response was just a gigantic coverup of the crimes and irresponsible behavior that occurred, coupled with a bailout designed to enrich and empower those who needed and deserved it least.

Everything was papered over in order to resuscitate a failed paradigm without reforming anything. Since it was all about pretending nothing was structurally wrong with the system, the response was to build more castles of sand on top of old ones that had unceremoniously crumbled. The whole event was a huge warning sign and opportunity to change course, but it was completely ignored. Enter novel coronavirus.

I’ve been concerned about the coronavirus outbreak from the start, and have been tweeting about it consistently for well over a month.

We have no idea what’s actually happening with this thing, yet planes are landing from China all over the world. We may very well avoid a global disaster here, but if we do it’ll be because of luck.

This observation proved prescient within just a few weeks, as the U.S. Centers for Disease Control (CDC) screwed up its early response to the pandemic in the most sloppy and unimaginable way possible. For whatever reason, the CDC instituted ridiculously stringent guidelines for testing potential infections by limiting testing to only those who recently traveled from China or had contact with someone known to be infected. The CDC continued to stick to these insane guidelines as the disease began to spread rapidly all over the world, particularly in South Korea and Italy.

The event that finally prompted the CDC to change its guidelines was the emergence of the first confirmed incidence of community spread coronavirus in the U.S., which occurred in northern California. The health professionals caring for that patient had requested testing days earlier, but the CDC rejected the initial request, putting medical staff and others at risk for no good reason. On top of all that, the limited testing kits the CDC had sent out didn’t work properly. The level of incompetence and failure we’ve seen from the CDC is almost hard to fathom, but given how hollowed out and corrupt our society has become, shouldn’t be surprising.

At this point, nobody knows what the eventual impact of the coronavirus on the planet will be. Anyone who says they know for sure is lying, but I think we should be taking it very seriously given the potential tail risks. A global pandemic is an uncertain and dangerous thing in the most robust and healthy of systems, but the consequences within a fragile house of cards system such as ours can be devastating.

A month ago, stock market valuations were near the highest ever and interest rates were near the lowest they’ve been in recorded human history. A gigantic “everything bubble” of historic proportions had been blown and investors were flying too close to the sun. It was a balloon looking for a pin, and it found one in the coronavirus. Nobody knew what the pin would be, which is exactly why the stock market collapsed so rapidly the moment investors began to appreciate the gravity of the situation. The fragility of the financial markets should be taken as a warning sign with regard to the rest of the system.

Financial assets have been intentionally blown to nonsensical levels in order to coverup the massive rot underneath. They’ve been masking the fact that much of the underlying economy consists of little more than financial engineering scams and war-making enterprises. The imperial oligarchy we live under is an utterly rotten, corrupt, and fragile superstructure that’s been carefully hidden for ten years under a facade of euphoric markets and a mass of debt-based consumption slaves.

The coronavirus itself should be seen in this context. The global system as it exists is simply not prepared for anything like this, but the reality is things like this do occur from time to time. Maybe we’ll get lucky and avoid the worst case scenario with this virus, but that’s not the point. There will always be other pins, and when your entire superstructure is fundamentally fragile and led by mediocre, corrupt sociopaths, it doesn’t take much to bring it down faster than you can imagine.

We stand at a moment where the fragility of our Potemkin Village paradigm will increasingly confront the harsh realities of meatspace. Coronavirus is a warning. It’s exposing a lot already, and will likely expose far more as it continues to spread. It’s exposing our ridiculous financial bubbles, it’s exposing the fact the U.S. can’t even manufacture its own surgical masks or medicines, and it’s exposing the clownish ineptitude of our leaders and institutions.

It’s insane that a country with the size and power of the U.S. can’t manufacture its own hospital masks, equipment and medicine.

If coronavirus doesn’t wake us up to the dangers of a completely hollowed out financialized economy, something else will.

It’s important we take this warning to heart and do something useful with it. It’s crucial we understand that the current paradigm is long past its useful life and likely won’t be hanging around much longer. Don’t cry or experience nostalgia for what was, rather, get your stuff together so you can help build and usher in the new world to come.

Those too attached to the way things have been will have a particularly hard time adjusting to the turbulent times ahead, so you want to do whatever you can in order to avoid being in that group. Change doesn’t have to be bad, but resistance to change can be deadly. Don’t allow yourself to be a casualty.

* * *

Liberty Blitzkrieg is an ad-free website. If you enjoyed this post and my work in general, visit the Support Page where you can donate and contribute to my efforts.

World Bank Pledges $12 Billion To Combat Virus Outbreak

The World Bank announced Tuesday afternoon that it would fund an initial $12 billion in financing to combat the Covid-19 outbreak that is threatening to plunge the global economy into recession. The virus has now spread to 60 countries, infecting more than 92,000 people, resulting in 3,100 deaths.

BREAKING: The @WorldBank Group is providing up to $12 billion in immediate support for countries coping with the health and economic impacts of the #COVID19 outbreak. https://t.co/Ng3yKS44fj

World Bank President David Malpass said there are still “many unknowns” about the fast-spreading virus. Malpass said more aid could be required in the future.

“We are working to provide a fast, flexible response based on developing country needs in dealing with the spread of COVID-19,” he said.“This includes emergency financing, policy advice, and technical assistance, building on the World Bank Group’s existing instruments and expertise to help countries respond to the crisis.”

He called on the global community to coordinate efforts to limit the transmission of the virus, indicating that the faster everyone acts, the more lives that can be saved.

Not sure if the World Bank is living up to “whatever it takes” or “throw the kitchen sink at it.” Surely, this isn’t the global fiscal stimulus investors were hoping for as stocks puke late in the session on Tuesday.

It’s almost certain that many more tranches of funding will be needed. This could be round one…

People were already panicking… (empty water shelves at Costco)

And now the market and The Fed are too…

After Friday’s greatest Dow point loss ever was followed by yesterday’s greatest Dow point gain ever, the question is – after The Fed unleashed $100 billion of repo liquidity and 50bps of rate cuts today, but leaving stocks lower – will it work (whatever work means)?

Scott Minerd doesn’t think so.

“While I believe this rate cut is a necessary act, I doubt it is sufficient to bail out the market. Now is the moment of truth…

…We will now see how impotent monetary policy is at addressing this crisis.”

Last week, amid the collapse in markets, Minerd, who is Guggenheim’s CIO, said the outbreak is “possibly the worst thing” he’s seen in his career because of its potential global spread and the Fed’s limited tools to staunch potential economic fallouts.

“This has the potential to reel into something extremely serious,” Minerd told Bloomberg TV last week.

“It’s very hard to imagine a scenario where you can actually contain this thing.”

And no matter what The Fed delivers, it will never be enough as Minerd sees the 10Y Treasury yield hitting 25bps by the time this is over… and another 15% or so lower in stocks.

This is the largest rate-cut since the fall of 2008, and just the ninth emergency rate cut in history…

So, The Fed cut 50bps… but the market quickly priced in demands almost two more rate-cuts in March!!

Source: Bloomberg

But lost in much of the hype around the rate-cut was the fact that term and overnight repo liquidity exploded to its highest since the crisis began last September…

Source: Bloomberg

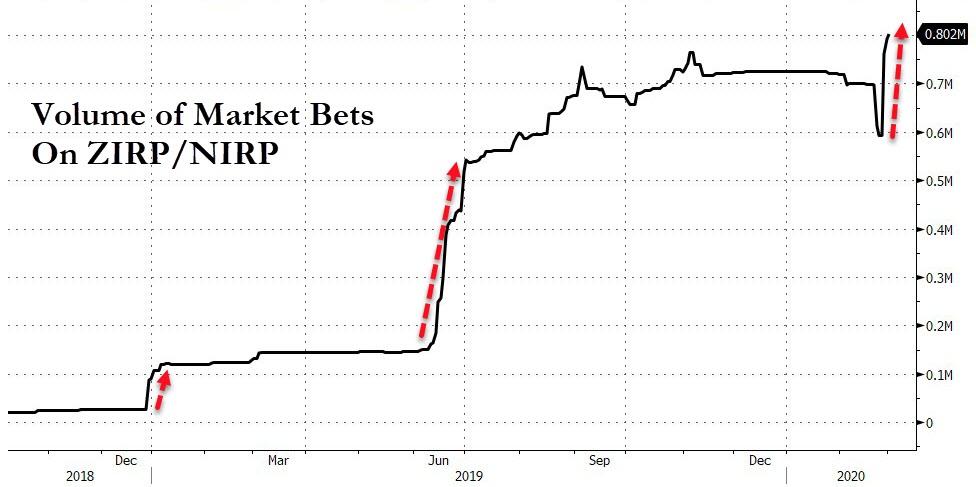

Bets on interest-rates going to zero, or negative, have exploded…

Source: Bloomberg

Believe it: MESTER: FED’S FRAMEWORK REVIEW INCLUDES STUDYING NEGATIVE RATES

And as rates plunged and that headline hit, bank stocks cratered…

Source: Bloomberg

Airline stocks also tumbled back to their lowest close since Oct 2016…

Source: Bloomberg

US markets were briefly exuberant after The Fed cut rates, then the questions began…

US markets also fell back into correction (sub-10%) territory today…

Futures show the real action on the day as buyers panicked into stock on the rate-cut but were devastatingly rejected…

Nasdaq closed below its 100DMA and S&P closed below its 200DMA…

No one should be surprised by this drop… earnings had plunged before it…

Source: Bloomberg

VIX trading was insane today, flash-crashing below 25 when The Fed cut rates, only to explode back higher, topping 40 intraday, before fading back in the last hour…

Source: Bloomberg

Stocks continue to catch down to bonds’ reality…

Source: Bloomberg

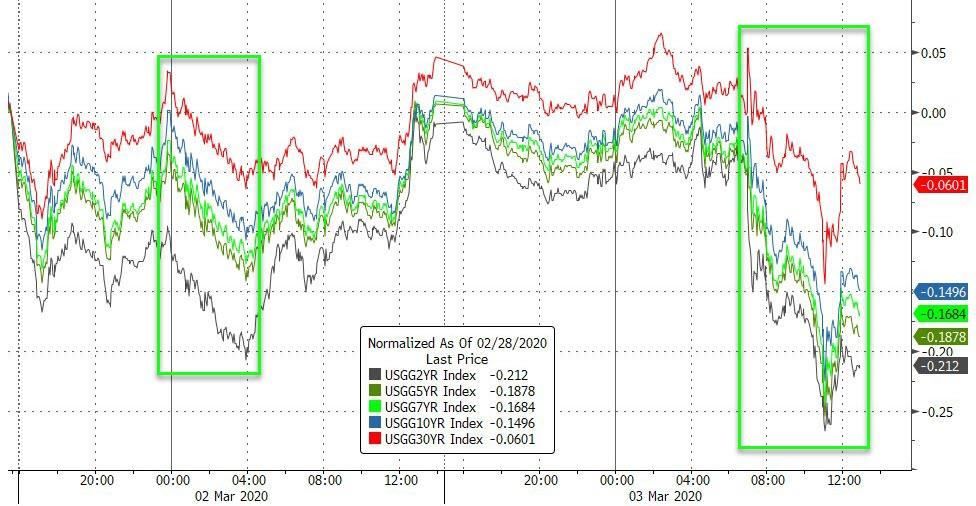

Treasury yields plunged today after The Fed rate-cut…

Source: Bloomberg

With yields at or near new record lows across the curve…

Source: Bloomberg

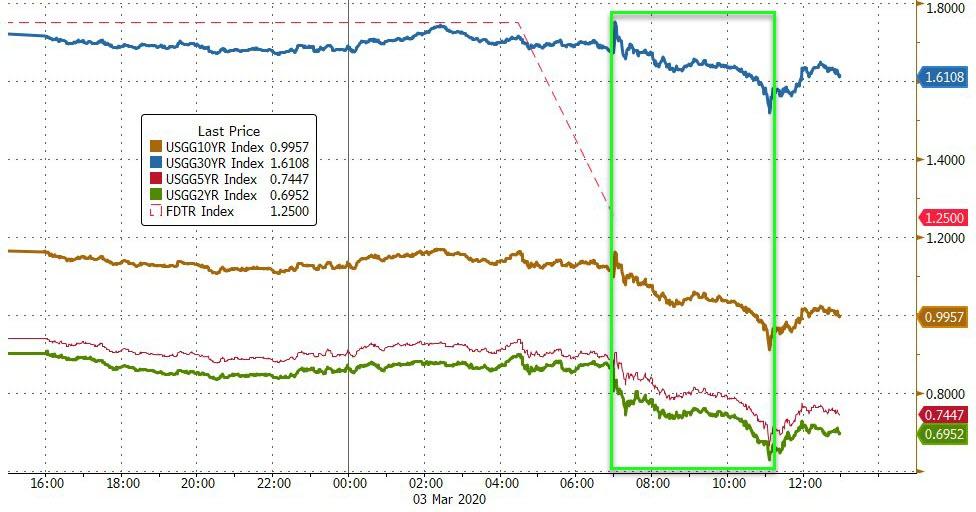

10Y plunged below the Maginot Line of 1.00% yield…

Source: Bloomberg

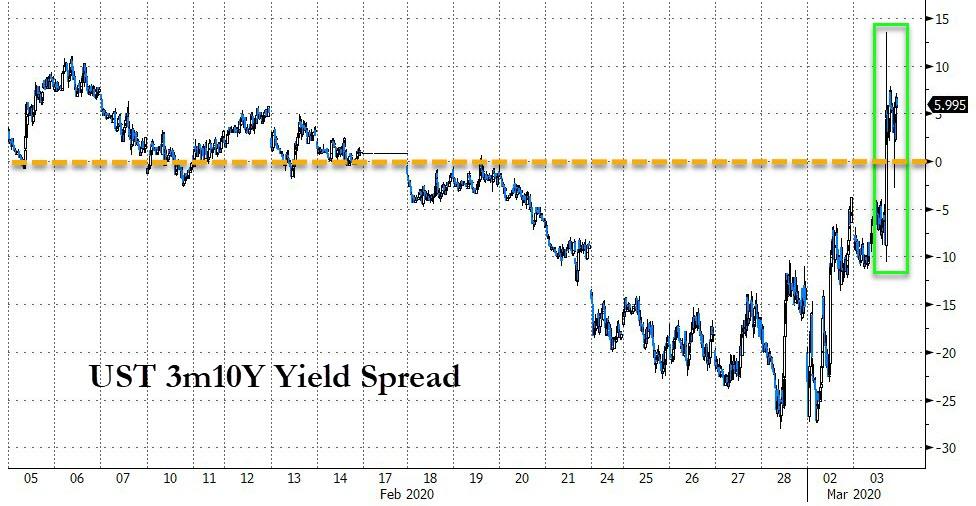

The yield curve steepened (as the short-end was utterly destroyed)

Source: Bloomberg

30Y TIPS yields crashed into negative territory for the first time ever…

Source: Bloomberg

The Dollar puked lower on the rate-cut, holding at 4-week lows…

Source: Bloomberg

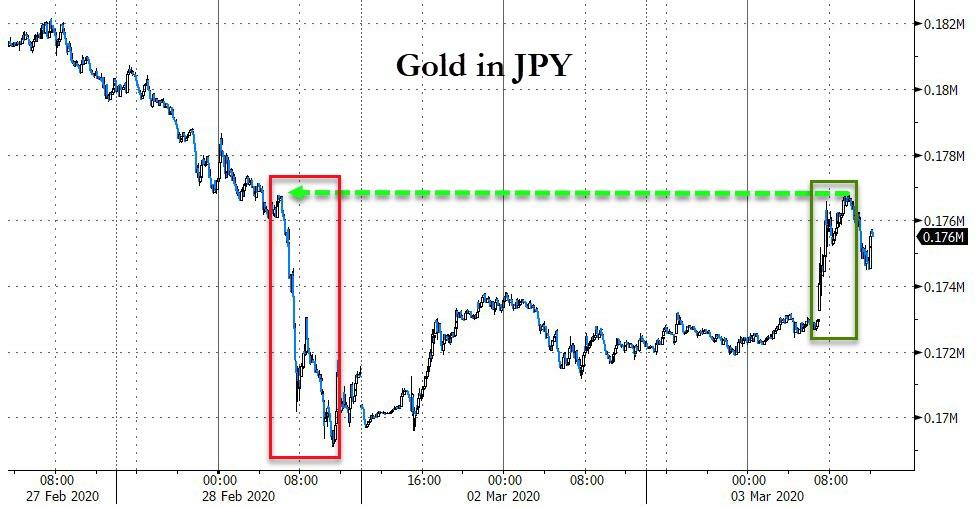

JPY weakened notably against gold today, erasing the forced selling from last week…

Source: Bloomberg

Cryptos rolled over today amid the market slump, with Bitcoin back below $9000…

Source: Bloomberg

Commodities initially all spiked on the rate-cut, then oil and copper plunged as PMs held gains…

Source: Bloomberg

Gold soared higher today after The Fed cut rates, erasing last week’s puke with futures tagging $1650 intraday…

WTI traded up to $48.50 intraday, but ended back below $47.50…

So, finally, we ask, did The Fed just swing from omnipotence to impotence?

It seems an emergency rate-cut of 50bps has done more to damage confidence that rebuild it… “what do they know?”

Did The Fed get an early glimpse of this week’s payrolls data?

We wonder what Powell and Trump are thinking?

As Rabo noted earlier, in order to decide what to do after The Fed cut, answer this first, key question:

what level of interest rates is required to incentivize you to risk the death of yourself and your family?

I am sure that there are policy wonks out there who believe they can correctly capture that precise equilibrium level on monetary policy. The point is that lower rates don’t help in this situation at all. If demand is destroyed by people bunkering down at home for weeks, and supply chains being disrupted, all lower borrowing costs can do is help tide businesses over if banks agree to extend loans and credit cards, etc. (as China is already now doing) – and all that does paint us further into the corner we are already in, because those rates won’t be able to rise again.

Of course, if we don’t see any major fiscal stimulus then it’s hard to imagine how one can remain too optimistic either.

“Does The Fed really want to have a put every time the market gets nervous? …Coming off all-time highs, does it make sense for The Fed to bail the markets out every single time… creating a trap?”

“The Fed has created this dependency and there’s an entire generation of money-managers who weren’t around in ’74, ’87, the end of the ’90s, anbd even 2007-2009.. and have only seen a one-way street… of course they’re nervous.“

“The question is – do you want to feed that hunger? Keep applying that opioid of cheap and abundant money?“

And they will never learn, as we noted above, the market is now demanding more rate-cuts…

Because, as Fisher concluded ominously: “the market is dependent on Fed largesse… and we made it that way… but we have to consider, through a statement rather than an action, that we must wean the market off its dependency on a Fed put.”

And then there’s this… Biden and Bernie all tied up in the prediction markets ahead of tonight’s Primary…

“It Smells Like Panic”: This Is Not What Powell Had In Mind…

Commenting on the Fed’s emergency rate cut, which while expected was extremely unusual and only the first one since the financial crisis, Obama’s chief economic advisor Larry Summers laid out the problem Powell is facing, especially now that the Fed appears to have lost much of its remaining credibility:

Fed Risks ‘Scaring People’ With Rate Cut. My interview today on the Fed’s emergency rate-cut on @BloombergTV.

When you have limited ammunition you have to conserve it. The Fed has limited ammunition with interest rates so low. Interest rates don’t cure the #coronovarius and interest rates don’t repair supply chains.

While Larry Summer’s opinion has been repeatedly discredited over the years, he does bring up a valid point: why is the Fed wasting half of all of its ammo just to delay what is now an inevitable crash, and why scramble with an “intermeeting” cut when it could have jawboned for the next two weeks and waited until the regular March 18 FOMC meeting. If anything, it would at least eliminate the sense of Fed panic from the equation.

Worse, as BMO’s Ian Lyngen puts it, what happened after the Fed’s emergency 50bps rate cut, the biggest since Jerome Kerviel blew up SocGen, “the situation didn’t play out exactly as Powell might have envisioned.“

So just how bad is it? Well, as plunging stocks demonstrate, the Fed is this close from losing all credibility…. and since the market has been held up for the past 11 years on nothing but Fed faith – and trillions in Fed liquidity – this could be a very, very big problem.

Lyngen explains:

The Fed’s emergency 50 bp rate cut brought 10-year yields to fresh record lows and a 0-handle was realized. To a

great extent, we’ll argue the situation didn’t play out exactly as Powell might have envisioned. It’s doubtful that

when JP left home this morning he thought ‘50 bp will really crush the stock market.’ So it goes.

The precipitous slide in equities was the driver behind the ease to begin with – as the spike in equity vol translated to tighter financial conditions via this now well-traveled path. This is where it becomes problematic; while stocks initially rallied on the ‘good news’ of rate cuts, the optimism quickly faded as the intermeeting nature of the move raised more questions than it answered. On one hand, the Fed is willing to be proactive but on the other, how much more will rates ultimately need to be cut?

If the FOMC wanted this exercise to be a ‘one-and-done’ event, that message wasn’t correctly communicated to the futures market which presently has roughly 60% odds of another move in two short weeks priced in. Admittedly, the 100% probability for the next cut being a quarter-point is worth a nod. Given the way in which risk markets are responding to today’s half-point, it’s challenging to imagine a 25 bp move would be met by the warm risk-on embrace to which monetary policymakers have become accustomed. We’ll stop shy of labeling it a ‘face-in-hand’ day for the Fed; if nothing else the question of whether or not just 50 bp would suffice has been answered… hint: it was ‘no’.

The biggest risk was always that by acting too proactively and aggressively Powell would signal that the situation is worse than initially feared. Check.

With 10-year yields on a slippery slope to 75 bp (there, we said it) and 2s conceivably poised to touch 50 bp, it’s somewhat concerning that the 2s/10s curve hasn’t steepened out any more – 34.5 bp remains the line in the sand. The rationale for the reluctance to steepen is sound; lower rates cannot cure the coronavirus and are unlikely to fully offset the hit to consumption, confidence, and inflation. As a result, the accommodation only creates a muted inflationary impulse.

It gets worse:

In two short weeks the Committee will be faced with a very difficult decision of either underwhelming investors’ expectations or quickly utilizing the limited rate-cutting potential afforded by the low outright yield environment.

Once the effective lower-bound is established, expanding the balance sheet will become topical and if risk sentiment isn’t restored by dropping rates, the next tool in the policy box will be expanding the balance sheet. As the Fed determines the next installment of accommodation, the signaling power for responding to Tuesday’s stock selloff will undoubtedly be a consideration; after all, the takeaway from the first 50 bp was that another will quickly follow and there is information held at the Fed which investors can only utilize by following the lead of central bankers.

Said differently, if Powell’s nervous, perhaps we all should be. At least that was the sentiment behind the flight-to-quality that brought 10-year yields to just 89 bp intraday.

“The DoD is concerned not only the impact COVID-19 has on mission readiness, but the risk to inadvertently spread the virus to the U.S. by returning members who may have been exposed,” a senior Pentagon official told Newsweek…

…When asked for comment, Jessica R. Maxwell, a DOD spokesperson, said the DoD has “contingency plans in place and are taking steps to educate and safeguard our military and civilian personnel, family members and base communities in preventing widespread outbreak.” But ultimately, “Commanders of individually affected geographic commands will be and are issuing specific guidance to their forces as their situations may require.”

…The use of the term “pandemic” in the briefing documents described a global outbreak, whereas an “epidemic” would be confined to a country,” a senior Pentagon official told Newsweek. During a pandemic, a large number of people in several countries or continents are affected, according to the CDC. (source)

The National Center for Medical Intelligence (the NCMI) raised the Risk of Pandemic warning from WATCHCON 2 to WATCHCON 1, according to the document obtained by Newsweek. WATCHCON 2 is used in the event of a “probable crisis” and WATCHCON 1 means the crisis is imminent.

The CDC also feels that the risk of a pandemic is high.

The Centers for Disease Control also notes that the likelihood of a global pandemic is high.

At this time, however, most people in the United States will have little immediate risk of exposure to this virus. This virus is NOT currently spreading widely in the United States. However, it is important to note that current global circumstances suggest it is likely that this virus will cause a pandemic. This is a rapidly evolving situation and the risk assessment will be updated as needed.

Current risk assessment:

For the general American public, who are unlikely to be exposed to this virus at this time, the immediate health risk from COVID-19 is considered low.

People in communities where ongoing community spread with the virus that causes COVID-19 has been reported are at elevated though still relatively low risk of exposure.

Healthcare workers caring for patients with COVID-19 are at elevated risk of exposure.

Close contacts of persons with COVID-19 also are at elevated risk of exposure.

Travelers returning from affected international locations where community spread is occurring also are at elevated risk of exposure. (source)

The CDC has been harshly criticized regarding its response to the virus. Tests that they sent out to health departments were faulty, losing weeks of possible containment in the United States. (More on the lack of containment in this article.)

The WHO refuses to call it a pandemic.

Perhaps in an effort to ratchet down the level of fear and panic across the globe, the World Health Organization has not deemed Covid-19 a pandemic.

“Does this virus have pandemic potential? Absolutely, it has. Are we there yet? From our assessment, not yet,” Director-General Tedros Adhanom Ghebreyesus told journalists in Geneva.

He explained that the decision to use the word ‘pandemic’ is based on an ongoing assessment of the geographical spread of the virus, the severity of disease it causes, and the impact on society.

“For the moment, we are not witnessing the uncontained global spread of this virus, and we are not witnessing large-scale severe disease or death,” he said, adding that what is occurring is coronavirus epidemics in different parts of the world, which are affecting countries differently. (source)

One must wonder, why is there so much ado about a word? Why is the World Health Organization so reluctant to call this what it is, a pandemic outbreak when it is one, even by their own definition? (That definition, found here, is “A pandemic is the worldwide spread of a new disease.”)

The preparedness and alternative media worlds are not alone in asking this question.

Lauren Sauer, director of operations for the Johns Hopkins Office of Critical Event Preparedness, told a reporter for the Washington Post, “Personally, I think we’re doing everyone a disservice by continuing this debate…It is creating more panic than just declaring it and moving on.”

The World Bank has an insurance policy against pandemics.

In a possibly unrelated aside, the World Bank has an insurance policy against pandemics but unless certain conditions occur, it won’t pay out, which greatly benefits investors. I use the word “unrelated” because apparently the bonds aren’t dependent on the WHO’s classification of an outbreak.

According to the World Bank, which created the fund three years ago, it was designed to “swiftly funnel funds from the deep-pocketed financial sector to health authorities in poorer countries before international assistance could be mobilized.”

They sold $320 million of these securities, which will mature in July of this year. If it matures, investors could receive double-digit yields. If a pandemic does occur, however, they could lose every penny they put into the fund.

The Class B bond covers conditions that are non-influenza related, like Ebola. But interestingly, the bond never paid out despite the ongoing crisis in the Congo based on the conditions laid out by the bond.

What are those conditions?

The primary one is that there must be more than 250 deaths attributed to the pandemic illness. But for the bond to be payable, there must be more than 20 deaths in a second country, which hasn’t yet occurred with either the coronavirus or Ebola. You can read more about the pandemic bond in these documents.

Whatever you want to call it, Covid-19 is widespread.

People in the United States are definitely concerned if the weekend’s shopping frenzy means anything. To learn more about preparing specifically for this outbreak, go here. To learn more about getting prepped for a quarantine, go here.

Yesterday’s WHO Sitrep report divulged the following information.

Armenia, Czechia, Dominican Republic, Luxembourg, Iceland, and Indonesia all now have confirmed cases of Covid-19.

A WHO team has arrived in Tehran to help with the Iranian response to their outbreak.

Covid-19 has been confirmed in 65 countries across the globe.

It never hurts to get prepared with some extra food, toilet paper, and other supplies. If the Department of Defense is warning that we’re facing a pandemic within 30 days, we can safely say the pandemic has already arrived.

Today’s Super Tuesday contests present Democratic primary voters with a stark choice between the Democratic Party of old, represented by former Vice President Joe Biden, and a radical vision of what the party could be, offered by Sen. Bernie Sanders (I–Vt.). Neither is good news for liberty.

Sanders heads into Super Tuesday as the presumptive frontrunner, having come in first or second place in every primary and caucus held so far, and leading the delegate count by a slim margin.

Biden’s 30-point blowout in South Carolina on Saturday, meanwhile, has breathed fresh life into his once-flagging campaign, pushing him to first place in the popular vote count, and convincing his moderate rivals Pete Buttigieg and Sen. Amy Klobuchar (D–Minn.) to drop out and endorse him.

Of the 14 states that vote today, Sanders leads in California (which awards 415 of the 1,357 delegates up for grabs) and his home state of Vermont. FiveThirtyEight has Biden the heavy favorite in North Carolina, Virginia, and Alabama.

Still holding out hopes of winning a few delegates are Sen. Elizabeth Warren (D–Mass.) and former New York City Mayor Michael Bloomberg. Rep. Tulsi Gabbard (D–Hawaii) is also still in the running.

Effectively, we’re down to a two-person race. Or as New York Times columnist David Leonhardt put it, it’s “Bernie or Biden. Period.”

The candidates offer Democratic-leaning voters a clear choice: Restore the Democratic Party or revolutionize it.

Biden is the self-styled candidate of restoration. His oft-repeated line is that he is running to “restore the soul of this country” after the damaging aberration that has been the presidency of Donald Trump. His campaign literature is peppered with references to the successes of the “Obama-Biden” administration, an implicit promise that a Biden presidency would be a return to the Democratic-led normalcy of the pre-2016 word.

On policy, the former vice president isn’t above proposing expensive new initiatives. Yet, when making the case for his candidacy, he talks almost exclusively about what he’s already done.

Take his answer in the last CBS debate, when asked why voters should trust him to take on the issue of mass shootings. “Because I am the only one that’s ever got it done nationally. I’ve beat the NRA twice. I’ve got assault weapons banned. I got magazines that could hold more than 10 rounds, I got them eliminated,” said Biden.

He’s taken the same tack on healthcare. After his opposition to Medicare for All surfaced prominently in the first Democratic debate, Biden released a video in which he told voters, “I understand the appeal of Medicare for All. But folks supporting it should be clear. It means getting rid of Obamacare, and I’m not for that.”

There’s nary an issue on which Biden doesn’t pitch his presidency as a return to the best parts of a past he helped create.

That is in complete contrast with Sanders. His campaign is predicated on the idea of overthrowing a long-outdated status quo. The Vermont independent proudly wears the label of “democratic socialist.” He talks openly of taking on the Democratic establishment, right alongside Republicans.

The pre-Trump past that Biden likes to cast in positive terms is, to Sanders, just decade after decade of wage stagnation for the working class. Low unemployment and GDP growth are, to Sanders, just more indicators that the rich are getting richer.

“The economy is doing really great for people like Mr. Bloomberg and other billionaires,” said Sanders at last Tuesday’s debate, when asked if his message of radical change could succeed during good economic times. “In the last three years,” Sanders said, “billionaires in this country saw an $850 billion increase in their wealth. But you know what? For the ordinary American, things are not so good.”

Sanders’ policy proposals are radical. He wants a Green New Deal. He wants national rent control. He wants a federal jobs guarantee and protectionist tariffs. He wants to raise middle-class taxes to pay for a $32 trillion health care plan that also bans private insurance.

When asked how he’ll get any of this ambitious agenda passed, Sanders answer is that he’ll mobilize a flood of new voters who’re chomping at the bit for real, socialist change. A New York Times article from last week quotes Sanders on the campaign trail promising he can “bring millions of people into the political process who normally do not vote.”

The differences between Biden and Sanders couldn’t be more apparent. For libertarians, however, it’s a hard call determining which is the lesser of two evils.

For each of Sanders’ budget-busting, property rights-destroying proposals, there’s another one that reveals a genuine appreciation for civil liberties. He’s in favor of radical criminal justice reform and of bringing the troops home. His immigration plan is pretty good, past statements about wage suppression and billionaire conspiracies notwithstanding. While Biden is still flip-flopping on marijuana, Sanders is promising to legalize pot on day one by executive order.

Biden’s aversion to anything even remotely radical means the country would likely be safe from socialism with him in the White House. But his absence of a radical vision for the future is undercut by a past record that’s been none too good for liberty.

The long-serving Delaware senator helped pass major federal tough on crime legislation that contributed to mass incarceration. He supported the Iraq war and the PATRIOT Act. He’s a drug warrior and a gun grabber. Sanders’ Medicare for All plan is currently just a promise. Biden helped give us Obamacare, which remains the law of the land.

As Reason‘s Eric Boehm has documented, Biden’s career “is one long lesson about the dangers of bipartisan consensus politics.”

Today, Democratic voters will choose between these two visions. Unfortunately, neither one leaves much room for limited government.

from Latest – Reason.com https://ift.tt/2TlV2Ao

via IFTTT

Today’s Super Tuesday contests present Democratic primary voters with a stark choice between the Democratic Party of old, represented by former Vice President Joe Biden, and a radical vision of what the party could be, offered by Sen. Bernie Sanders (I–Vt.). Neither is good news for liberty.

Sanders heads into Super Tuesday as the presumptive frontrunner, having come in first or second place in every primary and caucus held so far, and leading the delegate count by a slim margin.

Biden’s 30-point blowout in South Carolina on Saturday, meanwhile, has breathed fresh life into his once-flagging campaign, pushing him to first place in the popular vote count, and convincing his moderate rivals Pete Buttigieg and Sen. Amy Klobuchar (D–Minn.) to drop out and endorse him.

Of the 14 states that vote today, Sanders leads in California (which awards 415 of the 1,357 delegates up for grabs) and his home state of Vermont. FiveThirtyEight has Biden the heavy favorite in North Carolina, Virginia, and Alabama.

Still holding out hopes of winning a few delegates are Sen. Elizabeth Warren (D–Mass.) and former New York City Mayor Michael Bloomberg. Rep. Tulsi Gabbard (D–Hawaii) is also still in the running.

Effectively, we’re down to a two-person race. Or as New York Times columnist David Leonhardt put it, it’s “Bernie or Biden. Period.”

The candidates offer Democratic-leaning voters a clear choice: Restore the Democratic Party or revolutionize it.

Biden is the self-styled candidate of restoration. His oft-repeated line is that he is running to “restore the soul of this country” after the damaging aberration that has been the presidency of Donald Trump. His campaign literature is peppered with references to the successes of the “Obama-Biden” administration, an implicit promise that a Biden presidency would be a return to the Democratic-led normalcy of the pre-2016 word.

On policy, the former vice president isn’t above proposing expensive new initiatives. Yet, when making the case for his candidacy, he talks almost exclusively about what he’s already done.

Take his answer in the last CBS debate, when asked why voters should trust him to take on the issue of mass shootings. “Because I am the only one that’s ever got it done nationally. I’ve beat the NRA twice. I’ve got assault weapons banned. I got magazines that could hold more than 10 rounds, I got them eliminated,” said Biden.

He’s taken the same tack on healthcare. After his opposition to Medicare for All surfaced prominently in the first Democratic debate, Biden released a video in which he told voters, “I understand the appeal of Medicare for All. But folks supporting it should be clear. It means getting rid of Obamacare, and I’m not for that.”

There’s nary an issue on which Biden doesn’t pitch his presidency as a return to the best parts of a past he helped create.

That is in complete contrast with Sanders. His campaign is predicated on the idea of overthrowing a long-outdated status quo. The Vermont independent proudly wears the label of “democratic socialist.” He talks openly of taking on the Democratic establishment, right alongside Republicans.

The pre-Trump past that Biden likes to cast in positive terms is, to Sanders, just decade after decade of wage stagnation for the working class. Low unemployment and GDP growth are, to Sanders, just more indicators that the rich are getting richer.

“The economy is doing really great for people like Mr. Bloomberg and other billionaires,” said Sanders at last Tuesday’s debate, when asked if his message of radical change could succeed during good economic times. “In the last three years,” Sanders said, “billionaires in this country saw an $850 billion increase in their wealth. But you know what? For the ordinary American, things are not so good.”

Sanders’ policy proposals are radical. He wants a Green New Deal. He wants national rent control. He wants a federal jobs guarantee and protectionist tariffs. He wants to raise middle-class taxes to pay for a $32 trillion health care plan that also bans private insurance.

When asked how he’ll get any of this ambitious agenda passed, Sanders answer is that he’ll mobilize a flood of new voters who’re chomping at the bit for real, socialist change. A New York Times article from last week quotes Sanders on the campaign trail promising he can “bring millions of people into the political process who normally do not vote.”

The differences between Biden and Sanders couldn’t be more apparent. For libertarians, however, it’s a hard call determining which is the lesser of two evils.

For each of Sanders’ budget-busting, property rights-destroying proposals, there’s another one that reveals a genuine appreciation for civil liberties. He’s in favor of radical criminal justice reform and of bringing the troops home. His immigration plan is pretty good, past statements about wage suppression and billionaire conspiracies notwithstanding. While Biden is still flip-flopping on marijuana, Sanders is promising to legalize pot on day one by executive order.

Biden’s aversion to anything even remotely radical means the country would likely be safe from socialism with him in the White House. But his absence of a radical vision for the future is undercut by a past record that’s been none too good for liberty.

The long-serving Delaware senator helped pass major federal tough on crime legislation that contributed to mass incarceration. He supported the Iraq war and the PATRIOT Act. He’s a drug warrior and a gun grabber. Sanders’ Medicare for All plan is currently just a promise. Biden helped give us Obamacare, which remains the law of the land.

As Reason‘s Eric Boehm has documented, Biden’s career “is one long lesson about the dangers of bipartisan consensus politics.”

Today, Democratic voters will choose between these two visions. Unfortunately, neither one leaves much room for limited government.

from Latest – Reason.com https://ift.tt/2TlV2Ao

via IFTTT