Vladimir Putin shocked the West when he dismissed longtime prime minister Dmitri Medvedev after announcing plans in January to completely overhaul the Russian constitution.

Yet his pick for the new PM, former tax minister Mikhail Mishustin, shows Putin is aiming for more than his usual placeholder. His technological experience provides Putin with a vehicle to strengthen authoritarianism while giving people the impression that he wants to improve the dwindling economy.

“Mishustin was a suitable choice for Putin, because his obscurity makes it unlikely for people to see him as an official successor,” Alexander Morozov, an expert at the Boris Nemtsov Academic Center for the Study of Russia, told Reason.

Mishustin will also be adept at appropriating funds for the government’s infrastructure projects, Morozov added, as inadequate government spending is a pressing issue for the Kremlin.

He also has a reputation in the Russian business community of getting things done, economist Sergei Guriev said in an interview with Echo of Moscow Radio. Putin might use him to show Russian citizens that the country’s public development projects are continuing, giving them the impression that Putin is concerned for their welfare.

Prior to entering the public sector in 1998, Mishustin worked in information technology. In 1992, after graduating with a systems engineering degree, Mishustin worked at the International Computer Club, a nonprofit organization that collaborated with Western tech firms to help modernize the Russian system. With the help of Boris Fyodorov, Russia’s first finance minister, Mishustin gained substantial exposure to finance and government affairs before being named tax chief of Russia in 2010.

Using Mishustin’s technological prowess, former White House economist Joseph Sullivan points out in Foreign Policy, Putin likely intends to bolster a form of “techno-authoritarianism” similar to that of China:

As taxman, Mishustin developed a set of futuristic technologies that allowed Russia’s government to raise revenues. But these technologies also enhanced surveillance capabilities of Putin’s authoritarian state. For it’s not as if Russia’s tax authorities simply set an algorithm on heaps of data to do the impersonal bidding of state administration. Putin’s political appointees, like Mishustin, also maintain the ability to identify subjects and dredge up transaction-level data at their own discretion.

During his tenure as a government official, Mishustin revamped the tax collection system through rapid modernization and eased regulatory burdens on international traders.

In a 2010 interview with Russian newspaper Vedomosti, Mishustin touted electronic services as invaluable for catching “corrupt officials.” Later, in 2018, he claimed that Russia’s tax revenue had increased by almost 70 percent in the past five years.

Despite the emphasis Putin and Mishustin place on fixing government spending, they have also made plans to expand the country’s social welfare program. Shortly after Mishustin was appointed as PM, Putin’s new executive cabinet introduced a bill in the Duma, the parliament’s lower chamber, that would allocate approximately $31.2 billion in federal funds for services such as free school lunches, financial aid for low-income individuals, and healthcare system improvements.

At the very least, Mishustin has a better reputation than Medvedev, whom the public has regarded as increasingly corrupt as the years progressed. Putin’s selection also provides more clarity about his plans after the 2024 presidential election: Even if he leaves office, Putin’s recent changes to the Russian constitution will ensure that he maintains a substantial influence over the state.

from Latest – Reason.com https://ift.tt/39lWgRQ

via IFTTT

Sen. Bernie Sanders (I–Vt.) has rocketed to the top of the Democratic presidential primary field by proposing a massive expansion of government: single-payer health care, free public college tuition, student loan forgiveness, universal pre-K, and more.

His plans could cost as much as $60 trillion dollars over the next decade, more than doubling the federal budget.

More than any single policy, however, Sanders has run on an idea: Democratic socialism, with the economies of Denmark, Norway, and Sweden as models.

At times in his life, however, he’s also had kind words for socialist revolutionaries and regimes that are more authoritarian—although he has also condemned their harshest practices.

So what is Sanders’ vision of democratic socialism? And what would it mean for the country? To find out, Reason Features Editor Peter Suderman spoke with Jim Pethokoukis. He is the Dewitt Wallace Fellow at the American Enterprise Institute, where he writes and edits the AEIdeas blog.

Interview by Peter Suderman. Edited by Ian Keyser. Intro by Paul Detrick. Cameras by Austin and Meredith Bragg.

Rabobank: What Level Of Interest Rates Will Incentivize You To Risk The Death Of Yourself And Your Family

Submitted by Michael Every of Rabobank

“Tonight the super trouper lights are gonna find me

Shining like the sun (sup-p-per troup-p-per)

Smiling, having fun (sup-p-per troup-p-per)

Feeling like a number one…”

So sang markets yesterday in excitement as we enter what I am dubbing “Super Trouper Tuesday”. Indeed, the Dow Jones went up a whole baseball cap-and-a-bit to close at 26,703 even as the 10-year US remain at an unprecedented 1.12%. Not because the Fed mumbled something on Friday, but didn’t act, and not because the BOJ pumped all of USD4.6bn into markets yesterday, and not because the RBA cut rates 25bp to a new low of 0.50% earlier today, meaning that they now have one more cut left to go before it’s “Oz-QE, Oz-QE, Oz-QE” (Oi!Oi!Oi!) time. (Good timing not only due to Covid-19, as building approvals tumbled -15.3% m/m in January anyway.)

It’s also not due to more signs the virus spread is in “uncharted territory” according to the WHO (which means “pandemic” but is contractually obliged not to ever say it, it seems), with more deaths, and as UK police and army draw up lockdown plans and supermarkets plot their own contingency plans, for just one real-life example.

Rather it’s a reflection of the fact that the not-so-magnificent G-7, and G-7 central banks, have pledged that they will meet today to act jointly on the virus, and the IMF and World Bank are also prepared to help if needed; Covid-19, it seems, is a threat that requires immediate action in a way that the potential risk of the end of life on earth (if you are Green), or increasingly Victorian/Gilded Age levels of wealth inequality (if you are Piketty) are not. Then again we have to recall that stocks had just fallen by over 10% in a week, and that house prices risk following: Come on you cynical people, priorities, please!

So here we are at Super Trouper Tuesday. I am sure that a global virus-crisis meeting led by none other than world-famous virus expert US Treasury Secretary Steven Mnuchin will provide us all with the kind of comfort that deserves a whole baseball-cap in Dow movement. I am just not sure which direction.

Answer this first, key question: what level of interest rates is required to incentivize you to risk the death of yourself and your family? I am sure that there are policy wonks out there who believe they can correctly capture that precise equilibrium level on monetary policy. The point is that lower rates don’t help in this situation at all. If demand is destroyed by people bunkering down at home for weeks, and supply chains being disrupted, all lower borrowing costs can do is help tide businesses over if banks agree to extend loans and credit cards, etc. (as China is already now doing) – and all that does paint us further into the corner we are already in, because those rates won’t be able to rise again.

Nonetheless, those rates cuts are coming – because they push up equities very near-term. Indeed, our Fed watcher Philip Marey, who had already been calling Fed cuts this year, has now revised his 2020 rates call. He now expects the Fed to start cutting rates in March instead of April, with a 50bp reduction this month, again in June, and in September. In other words, it is back to the zero-bound by autumn (ahead of his original call, which was December).

Arguably even more interesting are the other rumours that are flying about over the G-7 meeting. Crucially, will this be the start of an open coordination between the government and central banks? Will central banks say that states can spend whatever they want to get us through Covid-19, and they will cover the required deficits? In other words, MMT? I would like to remind regular readers that such ‘unthinkable’ policy options are something we have openly flagged as a logical inevitability, even in developed markets: we just felt that the Green New Deal, or a war somewhere, would be the better ‘sell’ to the public. There are also enormous downside risks to any such strategy, which we have covered before in detail. Not everyone can “get away with it”, meaning a huge shift in relative power. Moreover, once you have shown that you CAN get free money like this, how is that genie put back in the bottle politically? This is actually an anti-Piketty argument: his view that we are doomed to see inequality rise is based on the concept that capital is the result of accrued savings rather than being created de novo as needed by (central) banks.

Of course, if we don’t see any major fiscal stimulus then it’s hard to imagine how one can remain too optimistic either. Notably, Mnuchin is keen on a tax cut rather than any higher state spending, and if that is any indication of what the G-7 will agree on, then we are in real trouble. All that returned cash is going to sit there on hold until the virus has been and gone, however long that is; and then the recovery will be too aggressive the other direction. The change in baseball caps that will be required up and down and up again could be extremely challenging, especially now Chinese supply chains to the US for things like baseball caps are damaged.

At the same time, it’s also Super Trouper Tuesday in US politics, where Joe “White Walker” Biden has been levelled up to become the Night King; that after Pete Buttigieg came, was from Indiana and spoke Norwegian, and went, and Amy Klobuchar, came, was from Minnesota, and went, both dropped out and backed Biden. Ahead of the slew of states voting in primaries today that means it is Game of Thrones vs. Curb Your Enthusiasm. Oh, and Mike Bloomberg is still in the race too, and very generously doing what Piketty et al., have long argued billionaires should be doing: redistributing lots of their own wealth to no particular end.

“But it’s gonna be alright; (You’ll soon be changing everything)

Everything will be so different; When I’m on the stage tonight

Tonight the super trouper lights are gonna find me

Gold Jumps, Dollar Dumps After ‘Emergency’ 50bps Fed Rate-Cut

Trump wins? … but what is The Fed so afraid of?

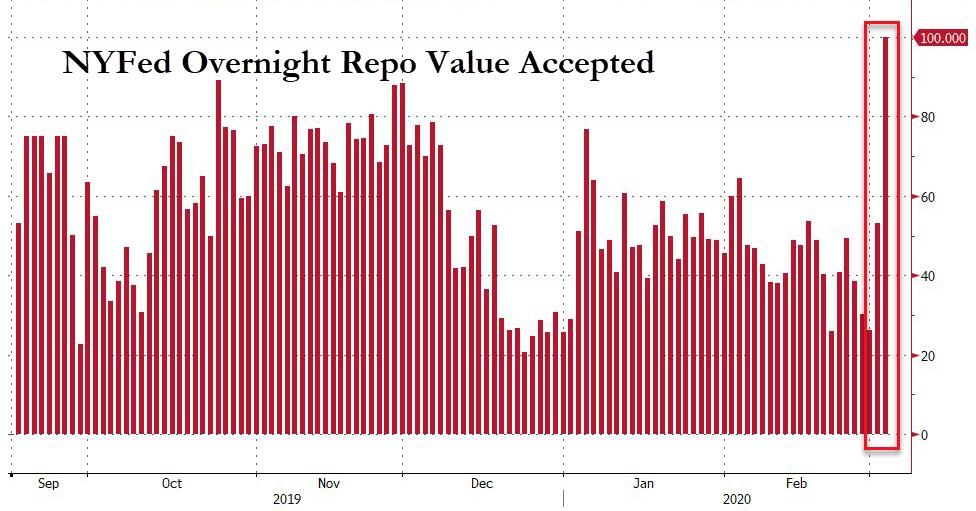

Shortly after the G-7 meeting promised to do whatever it takes, and the biggest demand for Fed repo liquidity since the program began…

A desperate Fed has once again met market expectations,The Fed has just announced an emergency 50bps rate-cut.

The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity.

In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate by 1/2 percentage point, to 1 to 1‑1/4 percent.

The Committee is closely monitoring developments and their implications for the economic outlook and will use its tools and act as appropriate to support the economy.

This is the largest rate-cut since the fall of 2008, and just the ninth emergency rate cut in history…

So you have to wonder, just how huge a deal is the virus’ impact on the global economy – despite consensus that this dip in economic activity will almost immediately v-shaped recover back to the new normal?

Stocks are spiking…

But, we note, that stocks are losing their initial gains…

Gold is jumping…

And the dollar is dumping…

But hey, The Fed managed to un-invert the yield curve…

“Does The Fed really want to have a put every time the market gets nervous? …Coming off all-time highs, does it make sense for The Fed to bail the markets out every single time… creating a trap?”

“The Fed has created this dependency and there’s an entire generation of money-managers who weren’t around in ’74, ’87, the end of the ’90s, anbd even 2007-2009.. and have only seen a one-way street… of course they’re nervous.“

“The question is – do you want to feed that hunger? Keep applying that opioid of cheap and abundant money?“

the market is dependent on Fed largesse… and we made it that way…

…but we have to consider, through a statement rather than an action, that we must wean the market off its dependency on a Fed put.”

The market is now pricing in no more rate-cuts in March but a high probability of at least one rate-cut in April.

Sen. Bernie Sanders (I–Vt.) has rocketed to the top of the Democratic presidential primary field by proposing a massive expansion of government: single-payer health care, free public college tuition, student loan forgiveness, universal pre-K, and more.

His plans could cost as much as $60 trillion dollars over the next decade, more than doubling the federal budget.

More than any single policy, however, Sanders has run on an idea: Democratic socialism, with the economies of Denmark, Norway, and Sweden as models.

At times in his life, however, he’s also had kind words for socialist revolutionaries and regimes that are more authoritarian—although he has also condemned their harshest practices.

So what is Sanders’ vision of democratic socialism? And what would it mean for the country? To find out, Reason Features Editor Peter Suderman spoke with Jim Pethokoukis. He is the Dewitt Wallace Fellow at the American Enterprise Institute, where he writes and edits the AEIdeas blog.

Interview by Peter Suderman. Edited by Ian Keyser. Intro by Paul Detrick. Cameras by Austin and Meredith Bragg.

The trains and buses might not be on time, but the movement for free public transit keeps on rolling.

On Sunday, Washington D.C. City Councilmember Charles Allen announced his intention to introduce new legislation that would provide every District resident, regardless of income, with a $100 monthly stipend they could spend on public buses and trains.

✅$100/month WMATA subsidy for every DC resident. ✅Millions to improve bus service, starting in communities that need it most. ✅Great for DC businesses & employees.

Let’s get this started! Join me tomorrow in front of the Wilson Building at 11:30am to kick off! https://t.co/KM1PLf19gK

Residents would have to sign up each year for the $100 benefit. Any money they don’t use in a given month would be recycled back into the pool of available funds. Allen’s proposal would also create a new fund to improve bus service in D.C.’s lower-income neighborhoods.

The program would cost between $50 million and $150 million a year. The final figure would be dependent on what kind of bulk discount on fares the city might be able to negotiate with the Washington Metropolitan Area Transportation Authority (WMATA), says Allen. He says that the program will be funded by excess tax revenue the city expects to collect, and therefore will not necessitate tax increases or service cuts.

Allen’s proposal is different from a lot of other free transit proposals that have been proposed or passed in other U.S. cities. Those, like the program implemented in Kansas City, Missouri, in January, simply make riding public transit fully free.

The D.C. proposal, which the Washington Post reports has the backing of seven of 13 city councilmembers, would instead function more like a universal transit voucher. That’s a major improvement over other programs.

For starters, it wouldn’t blow a hole in WMATA’s budget. Other free transit proposals that just abolish fares leave transit agencies themselves scrambling to make up the money they would have gotten from riders.

So long as these agencies are covering some of their operating costs, they should keep doing so, Baruch Feigenbaum, a transportation policy expert with the Reason Foundation (which publishes this website), said back in December.

“Whether it’s 20 percent of the recovery rate or 40 percent of the recovery rate, it’s a lot better than zero percent of the recovery rate,” he said. “From a fiscal perspective, you should do it just because you need the funding.”

By giving a subsidy to the rider, and not WMATA, Allen’s bill also maintains the agency’s incentive to retain and grow ridership.

“By providing a subsidy to residents, there’s a market-based incentive for WMATA to earn riders. If service isn’t reliable, safe, and predictable, people with options won’t change their transit habits,” reads a summary of Allen’s proposal tweeted out by NBC reporter Adam Tuss. In contrast, if a transit agency’s revenue is totally disconnected from ridership, riders become just another cost to bear.

There are still a number of problems with Allen’s transit voucher idea. For starters, it’s a universal benefit, meaning that even the wealthiest D.C. residents could take advantage of it. This is deliberately done to encourage ridership across all income groups. “We don’t want to ‘other’ our public transit. It’s for everyone and a shared public good,” reads a summary of the legislation.

I don’t quite understand how not giving a transit voucher to someone making $200,000 a year will make that person “other” public transit more than they already do, in the same way that I don’t imagine giving only low-income people food stamps encourages the othering of grocery stores.

As Allen already acknowledges, wealthier commuters’ decision to take transit has less to do with the price of a trip and more to do with the level of service being offered. Rather than give the least price-sensitive commuters a voucher, why not just take that money and spend it on more service improvements?

According to a 2019 survey from TransitCenter, riders—including low-income riders—prioritize service improvements over fare cuts.

The argument that the program is already paid for by excess tax revenue might be technically true but is still misleading. If the D.C. government is collecting more money than it needs for current levels of spending, the best thing to would be to undo recent tax hikes. We can then have a discussion about whether taxes should be raised to pay for additional benefits.

Allen’s proposal has not been officially introduced, and will surely change as it works its way through the city council. It’s better in design than many other free transit policies being proposed in other cities. It would nevertheless see a lot of tax dollars being spent on wealthy riders who don’t need a subsidy to get to work.

from Latest – Reason.com https://ift.tt/38iKx5e

via IFTTT

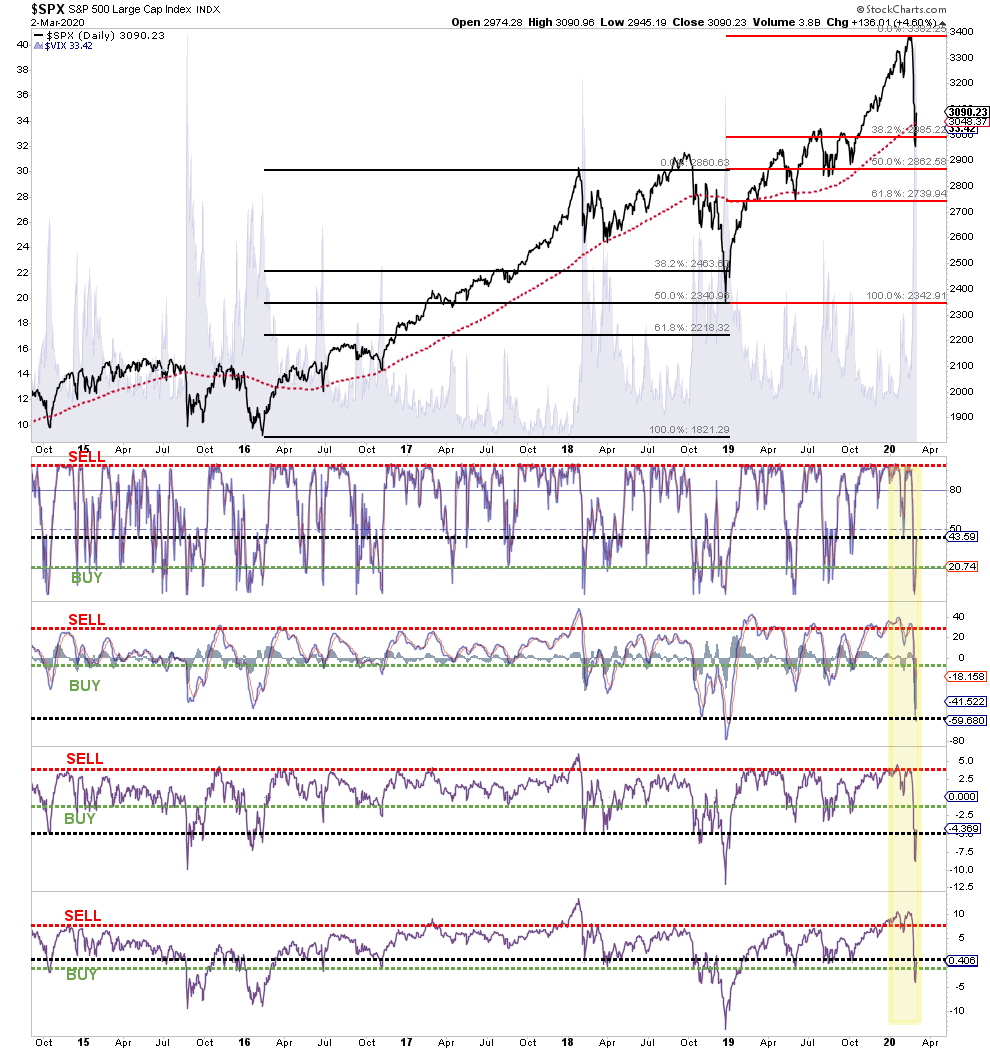

Typically, “Technically Speaking,” is an analysis of Monday’s market action, and the relevant risk/reward dynamics for investors. However, this week, we need to update the strategy we lain out in this past weekend’s newsletter, “Market Crash & Navigating What Happens Next.”

Specifically, we broke down the market into three specific time frames looking at the short, intermediate, and long-term technical backdrop of the markets. In that analysis, our premise was a “reflexive bounce” in the markets, and what to do during the process of that move. To wit:

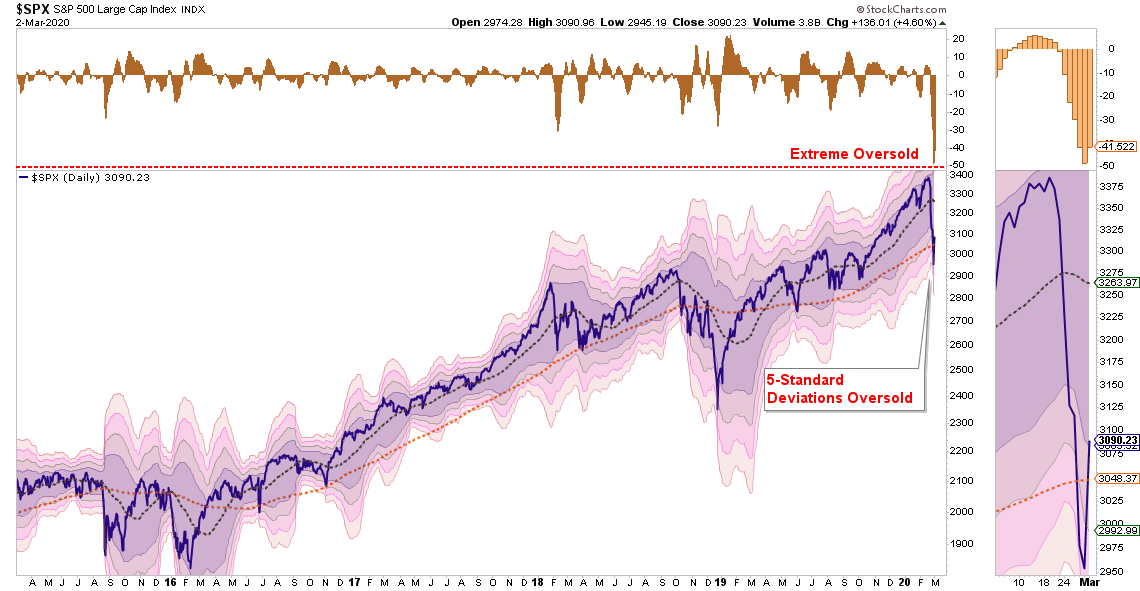

“On a daily basis, the market is back to a level of oversold (top panel) rarely seen from a historical perspective. Furthermore, the rapid decline this week took the markets 5-standard deviations below the 50-dma.”

Chart updated through Monday.

“To put this into some perspective, prices tend to exist within a 2-standard deviation range above and below the 50-dma. The top or bottom of that range constitutes 95.45% of ALL POSSIBLE price movements within a given period.

A 5-standard deviation event equates to 99.9999% of all potential price movement in a given direction.

This is the equivalent of taking a rubber band and stretching it to its absolute maximum.”

Importantly, like a rubber band, this suggests the market “snap back” could be fairly substantial, and should be used to reduce equity risk, raise cash, and add hedges.”

Importantly, read that last sentence again.

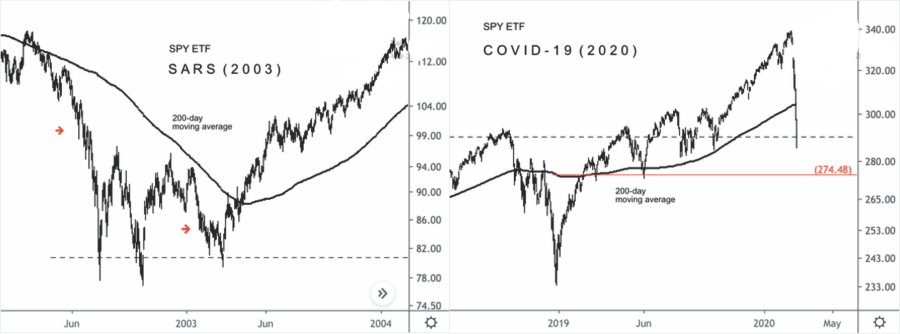

The current belief is the “virus” is limited in scope, and once the spread is contained, the markets will immediately bounce back in a “V-shaped” recovery. Much of this analysis is based on assumptions that “COVID-19” is like “SARS” in 2003, which had a very limited impact on the markets.

However, this is likely a mistake as there is s very important difference between COVID-19 and SARS, as I noted previously:

“Currently, the more prominent comparison is how the market performed following the ‘SARS’ outbreak in 2003, as it also was a member of the ‘corona virus’ family. Clearly, if you just remained invested, there was a quick recovery from the market impact, and the bull market resumed. At least it seems that way.”

“While the chart is not intentionally deceiving, it hides a very important fact about the market decline and the potential impact of the SARS virus. Let’s expand the time frame of the chart to get a better understanding.”

“Following a nearly 50% decline in asset prices, a mean-reversion in valuations, and an economic recession ending, the impact of the SARS virus was negligible given the bulk of the ‘risk’ was already removed from asset prices and economic growth. Today’s economic environment could not be more opposed.”

“Unlike today, the S&P 500 ETF (SPY) spent about a year below its 200-day moving average (dot-com crash) prior to the SARS 2003 outbreak. Price action is much different now. SPY was well above its 200-day moving average before the coronavirus outbreak, leaving plenty of room for profit-taking.”

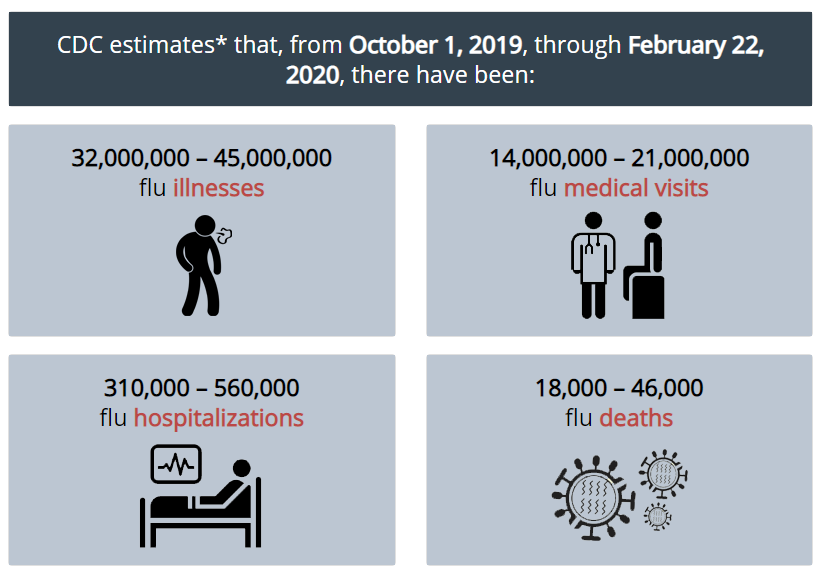

Importantly, the concern we have in the intermediate-term is not “people getting sick.” We currently have the “flu” in the U.S., which, according to the CDC, has affected 32-45 MILLION people and has already resulted in 18-46,000 deaths.

Clearly, the “flu” is a much bigger problem than COVID-19 in terms of the number of people getting sick. The difference, however, is that during “flu season,” we don’t shut down airports, shipping, manufacturing, schools, etc. The negative impact on exports and imports, business investment, and potential consumer spending are all direct inputs into the GDP calculation and will be reflected in corporate earnings and profits.

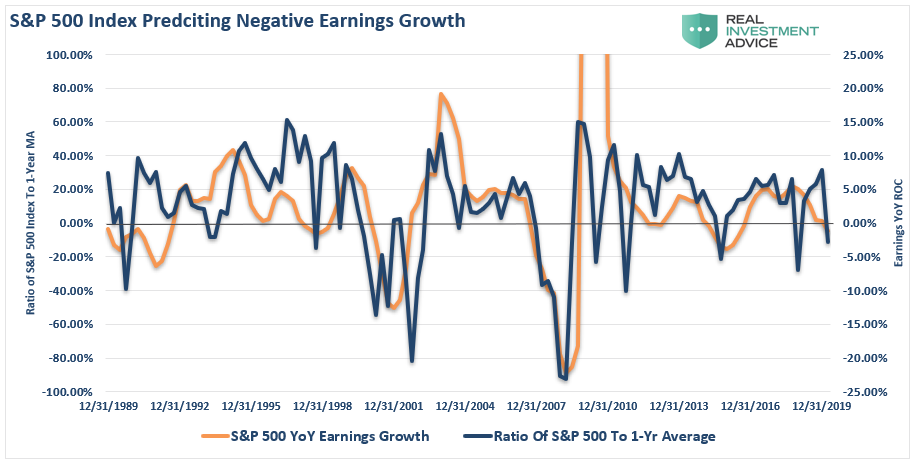

The recent slide, notwithstanding the “reflexive bounce” on Monday, was beginning the process of pricing in negative earnings growth through the end of 2020.

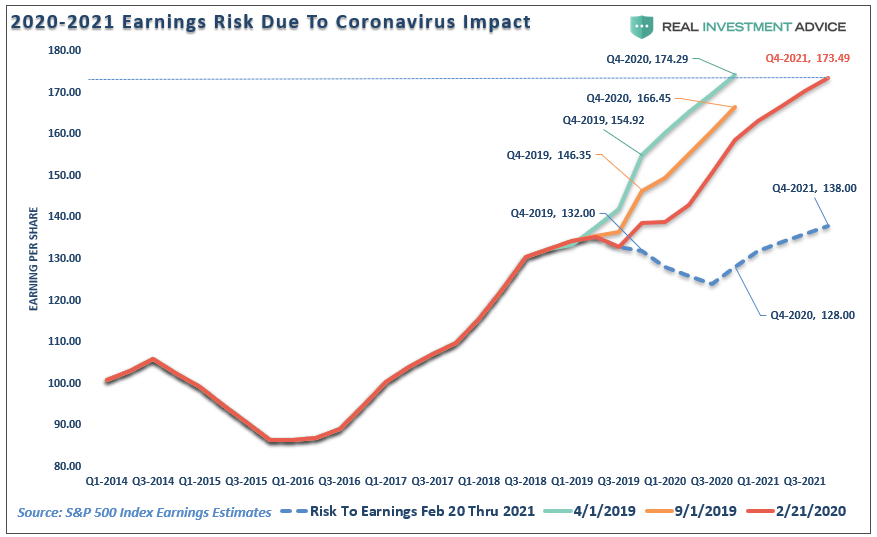

Importantly, earnings estimates have not been ratcheted down yet to account for the impact of the “shutdown” to the global supply chain. Once we adjust (dotted blue line) for the negative earnings environment in 2020, with a recovery in 2021, you can see just how far estimates will slide over the coming months. This will put downward pressure on stocks for the rest of the year.

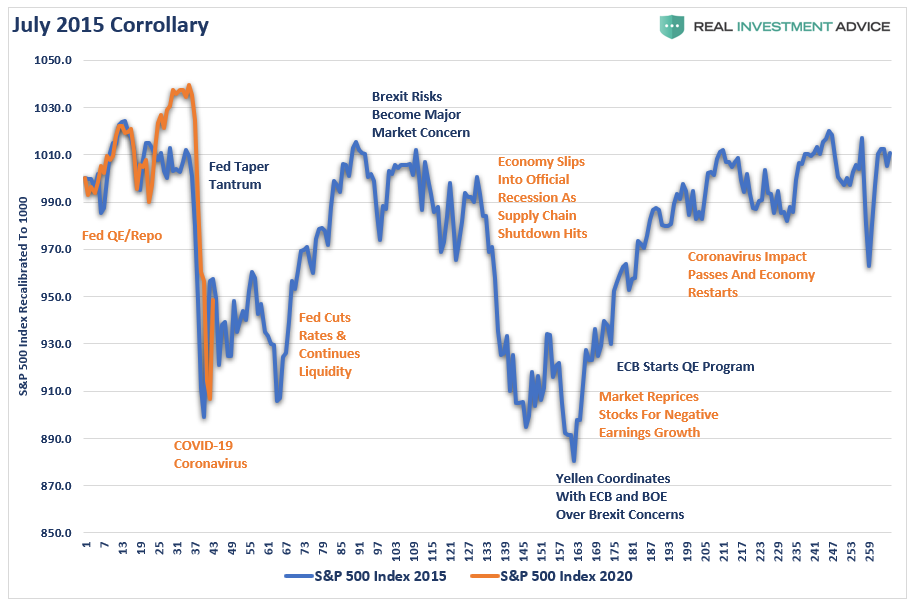

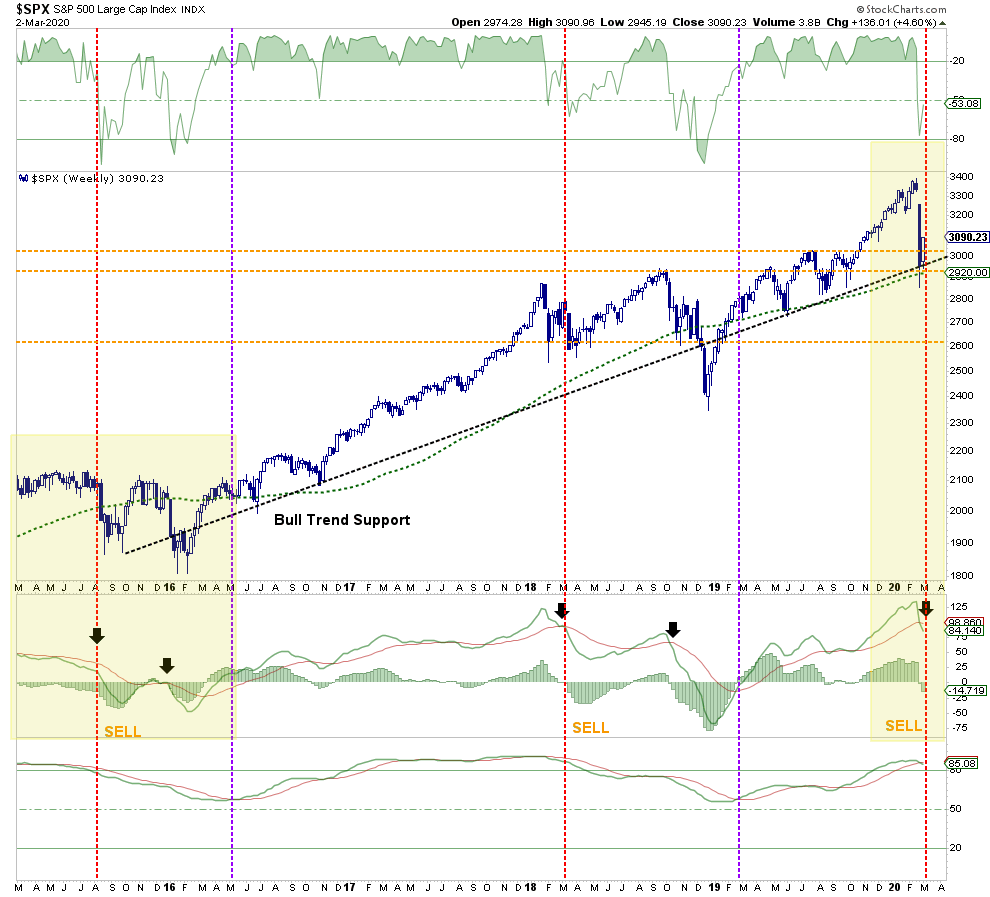

Given this backdrop of weaker earnings and economic growth in the coming months, this is why we suspect we could well see this year play out much like 2015-2016.

In 2015, the Fed was beginning to discuss tapering their balance sheet, which initially led to a decline. Given there was still plenty of exuberance, the market rallied back before “Brexit” risk entered into the picture. The market plunged on expectations for a negative economic impact but immediately bounced back after Janet Yellen coordinated with the BOE, and ECB, to launch QE in the Eurozone.

Using that model for a reflexive rally, we will likely see a failed rally and a retest of last week’s lows, or potentially even set new lows, as economic and earnings risks are factored in.

Rally To Sell

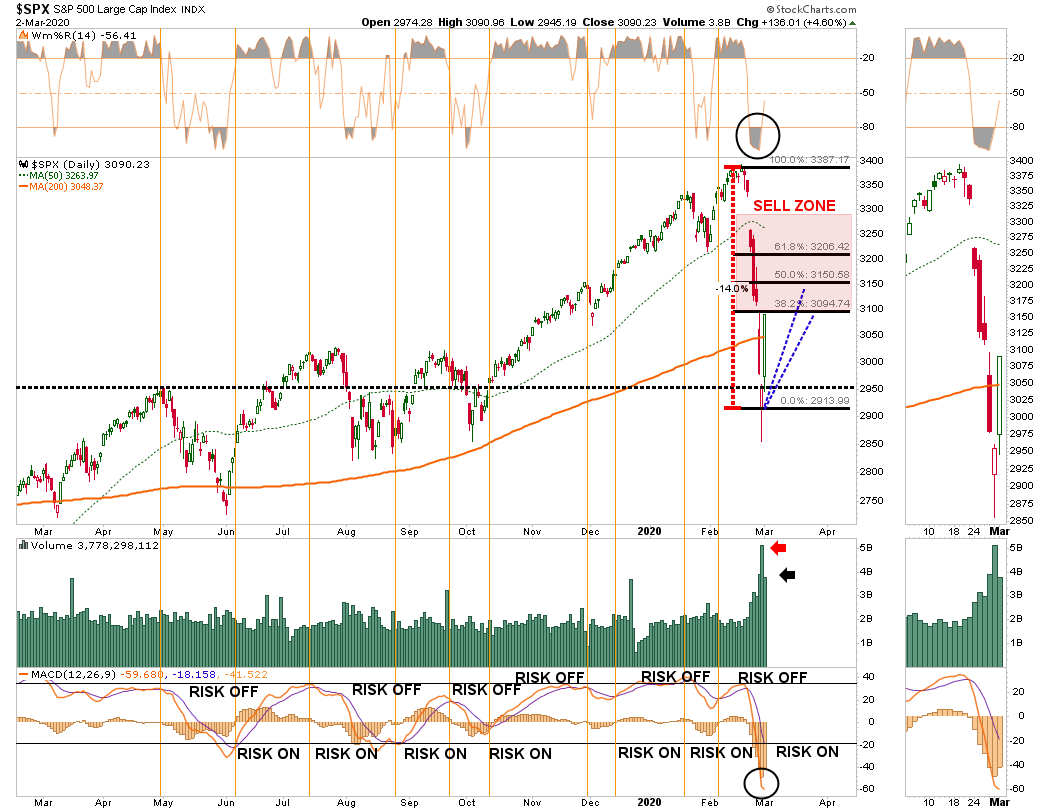

As expected, the market rallied hard on Monday on hopes that the Federal Reserve, and Central Banks globally, will intervene with a “shot of liquidity” to cure the market’s “COVID-19” infection.

The good news is the rally yesterday did clear initial resistance at the 200-dma, which keeps that important break of support from being confirmed. That push also cleared the way for the market to rally back into the initial “sell zone” we laid out this past weekend.

Importantly, while the volume of the rally on Monday was not as large as Friday’s sell-off, it was a solid day nonetheless and confirmed the conviction of buyers. With the markets clearing the 200-dma, and still oversold on multiple levels, there is a high probability the market will rally into our “sell zone” before failing.

For now, look for rallies to eventually be “sold.”

The End Of The Bull

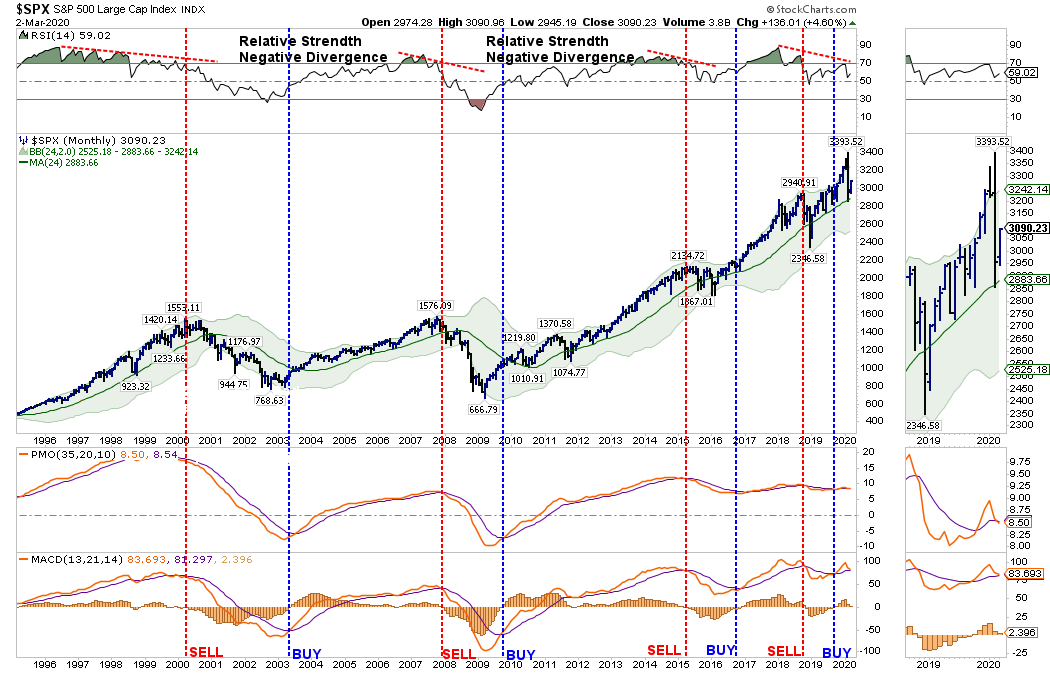

I want to reprint the last part of this weekend’s newsletter as any rally that occurs over the next couple of weeks will NOT reverse the current market dynamics.

“The most important WARNING is the negative divergence in relative strength (top panel). This negative divergence was seen at every important market correction event over the last 25-years.”

“As shown in the bottom two panels, both of the monthly ‘buy’ signals are very close to reversing. It will take a breakout to ‘all-time highs’ at this point to keep those signals from triggering.

For longer-term investors, people close to, or in, retirement, or for individuals who don’t pay close attention to the markets or their investments, this is NOT a buying opportunity.

Let me be clear.

There is currently EVERY indication given the speed and magnitude of the decline, that any short-term reflexive bounce will likely fail. Such a failure will lead to a retest of the recent lows, or worse, the beginning of a bear market brought on by a recession.

Please read that last sentence again.

Bulls Still In Charge

The purpose of this analysis is to provide you with information to make educated guesses about the “probabilities” versus the “possibilities” in the markets over the weeks, and months, ahead.

It is absolutely “possible” the markets could find a reason to rally back to all-time highs and continue the bullish trend. (For us, such would be the easiest and best outcome.) Currently, the good news for the bulls, is the bullish trend line from the 2015 lows held. However, weekly “sell signals” are close to triggering, which does increase short-term risks.

With the seasonally strong period of the market coming to its inevitable conclusion, economic and earnings data under pressure, and the virus yet to be contained, it is likely a good idea to use the current rally to rebalance portfolio risk and adjust allocations accordingly.

As I stated in mid-January, and again in early February, we reduced exposure in portfolios by raising cash and rebalancing portfolios back to target weightings. We had also added interest rate sensitive hedges to portfolios, and removed all of our international and emerging market exposures.

We will be using this rally to remove basic materials and industrials, which are susceptible to supply shocks, and financials which will be impacted by an economic slowdown/recession, which will likely trigger rising defaults in the credit market.

Here are the guidelines we recommend for adjusting your portfolio risk:

Step 1) Clean Up Your Portfolio

Tighten up stop-loss levels to current support levels for each position.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.

Step 2) Compare Your Portfolio Allocation To Your Model Allocation.

Determine areas requiring new or increased exposure.

Determine how many shares need to be purchased to fill allocation requirements.

Determine cash requirements to make purchases.

Re-examine portfolio to rebalance and raise sufficient cash for requirements.

Determine entry price levels for each new position.

Determine “stop loss” levels for each position.

Determine “sell/profit taking” levels for each position.

(Note: the primary rule of investing that should NEVER be broken is: “Never invest money without knowing where you are going to sell if you are wrong, and if you are right.”)

Step 3) Have positions ready to execute accordingly, given the proper market set up. In this case, we are adjusting exposure to areas we like now, and using the rally to reduce/remove the sectors we do not want exposure too.

Stay alert; things are finally getting interesting.

How The Super Rich Are Preparing For The Coronavirus

The interesting thing about the coronavirus is that its a problem that uniquely affects everybody. And as there’s no vaccine even close to ready, that means that the super rich are left scrambling to fend for themselves against a problem they can’t just throw money at and solve.

The super rich are bracing for an outbreak in the U.S. in the same way that every else is. While some of them may be calling hospitals that they help donate wings to instead of speaking to their local family physicians, according to Bloomberg, there really isn’t really a solution that the super rich can afford that others can. As many know, for now, it boils down to washing your hands and being careful, the same way you would while trying to avoiding the normal flu.

Ken Langone, the co-founder of Home Depot Inc., called a top executive and a top scientist at NYU Langone Health with his inquiries. He was told what the rest of us have been told, regardless of whether or not it’s the truth:

“What I’ve been told by people who are smarter than me in disease is, ‘As of right now it’s a bad flu.’”

He says he’d expect “no special treatment” if he had to return home and head to NYU Langone. Sure, and the rest of us speak with top executives and top scientists there all the time…

Ken Langone and the CEO of NYU Langone Health/BBG

Like the rest of the world, many billionaires are simply just washing their hands more. Others are preparing private plane rides out of town, consultations with world-leading experts and access to over the time medical care.

Jordan Shlain, an internist and managing partner of Private Medical, a high-end concierge service said:

“It’s been a full-on war-room situation over here. The company is procuring hundreds of full-body coverings for work that includes visits in San Francisco, Silicon Valley, Los Angeles and New York. We have to beg, borrow or steal. Well, not steal — beg, borrow and pay.”

Tim Kruse, a doctor that makes house calls in Aspen, Colorado, said:

“The wealthy aren’t going to necessarily have access to things that the common person is not going to have access to. But that hasn’t stopped them from asking if they can get their hands on a coronavirus vaccine. The answer is no. They just want to know.”

Finally, a virus that’s worried about solving inequality…

A co-founder of a major hedge fund said he might fly to a house he has in Italy, quickly becoming the epicenter of the outbreak, if everyone starts to hunker down because plane tickets would likely be cheaper.

Charles Stevenson, an investor who was the longtime board president at a Park Avenue co-op that’s home to several billionaires, said:

“I don’t feel concerned at the moment — it’s not near me right now. If people in the village have coronavirus, I’d get out of here. I’d fly to Idaho and close myself off in a cabin.”

Mitchell Moss, who studies urban policy and planning at New York University, said that shacking up with your significant other as a result of a lockdown could lead to unexpected consequences:

“This is going to destroy the marriages of the rich. All these husbands and wives who travel will now have to spend time with the person they’re married to.”

But despite the super rich now being faced with many of the same problems everyone else has (both the virus AND their marriages), they still have some advantages. Jewel Mullen, associate dean for health equity at the University of Texas at Austin’s Dell Medical School concluded:

“Resources like money and transportation and information give people head starts on protective and preventive measures, and can help create more comfortable scenarios for people to cope with disaster. That’s where you really get to see disparate needs.”

The trains and buses might not be on time, but the movement for free public transit keeps on rolling.

On Sunday, Washington D.C. City Councilmember Charles Allen announced his intention to introduce new legislation that would provide every District resident, regardless of income, with a $100 monthly stipend they could spend on public buses and trains.

✅$100/month WMATA subsidy for every DC resident. ✅Millions to improve bus service, starting in communities that need it most. ✅Great for DC businesses & employees.

Let’s get this started! Join me tomorrow in front of the Wilson Building at 11:30am to kick off! https://t.co/KM1PLf19gK

Residents would have to sign up each year for the $100 benefit. Any money they don’t use in a given month would be recycled back into the pool of available funds. Allen’s proposal would also create a new fund to improve bus service in D.C.’s lower-income neighborhoods.

The program would cost between $50 million and $150 million a year. The final figure would be dependent on what kind of bulk discount on fares the city might be able to negotiate with the Washington Metropolitan Area Transportation Authority (WMATA), says Allen. He says that the program will be funded by excess tax revenue the city expects to collect, and therefore will not necessitate tax increases or service cuts.

Allen’s proposal is different from a lot of other free transit proposals that have been proposed or passed in other U.S. cities. Those, like the program implemented in Kansas City, Missouri, in January, simply make riding public transit fully free.

The D.C. proposal, which the Washington Post reports has the backing of seven of 13 city councilmembers, would instead function more like a universal transit voucher. That’s a major improvement over other programs.

For starters, it wouldn’t blow a hole in WMATA’s budget. Other free transit proposals that just abolish fares leave transit agencies themselves scrambling to make up the money they would have gotten from riders.

So long as these agencies are covering some of their operating costs, they should keep doing so, Baruch Feigenbaum, a transportation policy expert with the Reason Foundation (which publishes this website), said back in December.

“Whether it’s 20 percent of the recovery rate or 40 percent of the recovery rate, it’s a lot better than zero percent of the recovery rate,” he said. “From a fiscal perspective, you should do it just because you need the funding.”

By giving a subsidy to the rider, and not WMATA, Allen’s bill also maintains the agency’s incentive to retain and grow ridership.

“By providing a subsidy to residents, there’s a market-based incentive for WMATA to earn riders. If service isn’t reliable, safe, and predictable, people with options won’t change their transit habits,” reads a summary of Allen’s proposal tweeted out by NBC reporter Adam Tuss. In contrast, if a transit agency’s revenue is totally disconnected from ridership, riders become just another cost to bear.

There are still a number of problems with Allen’s transit voucher idea. For starters, it’s a universal benefit, meaning that even the wealthiest D.C. residents could take advantage of it. This is deliberately done to encourage ridership across all income groups. “We don’t want to ‘other’ our public transit. It’s for everyone and a shared public good,” reads a summary of the legislation.

I don’t quite understand how not giving a transit voucher to someone making $200,000 a year will make that person “other” public transit more than they already do, in the same way that I don’t imagine giving only low-income people food stamps encourages the othering of grocery stores.

As Allen already acknowledges, wealthier commuters’ decision to take transit has less to do with the price of a trip and more to do with the level of service being offered. Rather than give the least price-sensitive commuters a voucher, why not just take that money and spend it on more service improvements?

According to a 2019 survey from TransitCenter, riders—including low-income riders—prioritize service improvements over fare cuts.

The argument that the program is already paid for by excess tax revenue might be technically true but is still misleading. If the D.C. government is collecting more money than it needs for current levels of spending, the best thing to would be to undo recent tax hikes. We can then have a discussion about whether taxes should be raised to pay for additional benefits.

Allen’s proposal has not been officially introduced, and will surely change as it works its way through the city council. It’s better in design than many other free transit policies being proposed in other cities. It would nevertheless see a lot of tax dollars being spent on wealthy riders who don’t need a subsidy to get to work.

from Latest – Reason.com https://ift.tt/38iKx5e

via IFTTT

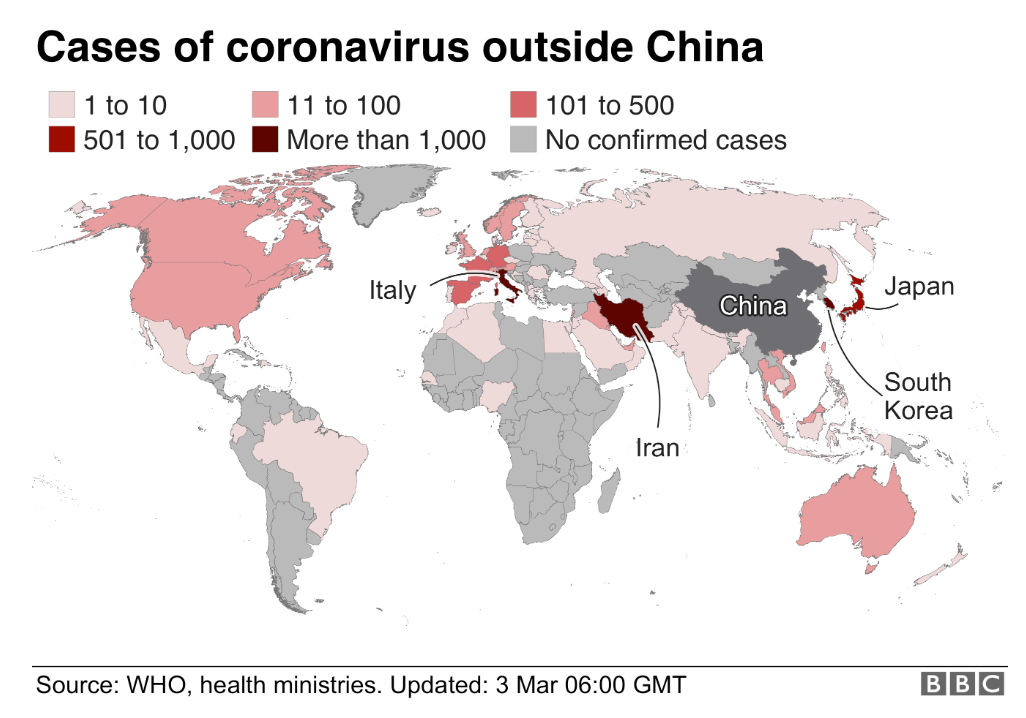

Coronavirus update: Cases of COVID-19, or coronavirus, continue to climb in the U.S., and the disease seems to pose a special risk to older adults, especially if they’re in poorer health to start. But fears about coronavirus death rates are likely inflated.

The numbers: Over 100 U.S. cases of coronavirus have been confirmed now, including six cases that were fatal. The deaths all occurred in King County, Washington, including four residents at a single nursing home. Overall, 15 states have reported coronavirus cases but only Washington has so far seen fatalities.

Where in the U.S. has coronavirus been diagnosed?: Cases are being treated in Arizona, California, Florida, Georgia, Illinois, Massachusetts, Nebraska, New Hampshire, New York, Oregon, Rhode Island, Texas, Utah, Washington, and Wisconsin.

Why it’s still not time to panic: “Misleading arithmetic,” as the Cato Institute’s Alan Reynolds puts it:

Assuming the number of people who have reportedly died from COVID-19 is reasonably accurate, then the percentage of infected people who die from the disease (the death rate) must surely have been much lower than the 2–3% estimates commonly reported. That is because the number of infected people is much larger than the number tested and reported.

The triangle graph [here], from a February 10 study from Imperial College London, shows that most people infected by COVID-19 are never counted as being infected. That is because, the Imperial College study explains, “the bottom of the pyramid represents the likely largest population of those infected with either mild, non‐specific symptoms or who are asymptomatic.”

As the Director General of the World Health Organization (WHO), Tedros Adhanom, explained in his February 28 briefing, “Most people will have mild disease and get better without needing any special care.” Several studies have found that about 80% of all the COVID-19 cases have relatively minor symptoms which end without severe illness and therefore remain unreported.

As of yesterday, there were 89,253 confirmed cases worldwide (about 96 percent of them in Asia). Reynolds also points out that there have “been 45,393 known recoveries from COVID-19 (compared to 3,048 cumulative deaths) and, importantly, recoveries have been outnumbering new cases.”

To put that in perspective:

… the SARS coronavirus killed 774 people out of 8,096 known cases in 2003, which was a death rate of 9.6% before it vanished the next year. Bird flu in 1997 was predicted to be a deadly pandemic, but it killed very few people before it disappeared.

Today is International Sex Worker Rights Day (ISWRD). And this year, there’s actually something to celebrate, suggests sex worker, author, and Reason contributor Maggie McNeill. “In the past two years, the tide of sex worker rights has completely turned,” she writes on her blog, The Honest Courtesan. More:

Read the rest here. And check out the #ISWRD hashtag on Twitter for information about sex work criminalization and sex worker rights activism around the world.

FREE MARKETS

Federal drug warriors get grabby in Ohio. “Federal prosecutors are seeking the forfeiture of more than $356,000 from an Akron man they say made money from trafficking drugs,” reports Cleveland.com. They also seized marijuana edibles, a gold Rolex watch, and $67,000 worth of jewelry. But the man, Cory Grandison, “has not been charged with a drug crime.”

Grandison did plead guilty to owning a gun and some ammunition, which is prohibited since he has a felony conviction in his past. The gun charge comes with at least two and a half years in federal prison and possibly a bit over three years.

New: Tennessee legislators have advanced a bill to shrink Tennessee's draconian drug-free school zones, citing data @laurenkrisai and I put together showing that more than 25% of area within city limits in the state is within an enhanced sentencing zone https://t.co/4GesHHVlrR

{kind=link}

{kind=link}