Politicians and bureaucrats spend a lot of their time making new laws and regulations to “protect the public,” but now that the public is really in danger, the government is realizing that setting many of them aside is essential for our safety.

Here are 10 measures enacted in the name of public safety that have been set aside in the name of public safety.

The Centers for Disease Control and Prevention’s (CDC) testing monopoly is perhaps the biggest and most obvious clusterfuck on the list: The agency mandated that only it could create and distribute tests. When they finally did roll them out, they turned out to be painfully slow and wildly inaccurate. Only after this colossal failure did they allow private companies into the game, which has led to more testing kits that deliver faster results. If only that had happened months ago.

On March 18, the White House announced that the Department of Health and Human Services (HHS) would finally allow health care providers to work across state lines. This is fantastic news—except HHS doesn’t have that kind of authority. States have jurisdiction over who can practice within their boundaries. Not surprisingly, HHS has been pretty quiet about the issue, but at least some states have waived restrictions, making it easier for doctors to be doctors.

You know things are serious when the Transportation Security Administration (TSA) is easing stupid restrictions. Since 2006 the agency said that having more than 3.4 ounces of liquid in a container was super dangerous on airplanes, but now that actual danger is around and no one is flying, hand sanitizer in 12-ounce bottles is A-OK.

Speaking of hand sanitizer, here’s some good news from the Alcohol and Tobacco Tax and Trade Bureau: Distilleries around the country can now make hand sanitizer without jumping through a metric fuckton of red tape, including permits, bonds, authorization, formula approval, and taxes. These waivers are only approved through June 30, however—after which that same hand sanitizer might once again be very dangerous.

Anyone who makes or sells alcohol is well-versed in ridiculous and counterproductive regulation, but with the crushing blow that social distancing brings to restaurants, at least one strip of red tape is being snipped: State and local governments are lifting bans on alcohol home delivery, which is welcome news to bars, restaurants, and anyone stuck at home paying attention to the news.

The Food and Drug Administration (FDA) has been easing a bunch of restrictions, including relaxing rules on ventilator manufacturing, allowing pharmacists to make hand sanitizer, declaring previously unapproved respirators totally safe now, allowing outside groups to make diagnostic tests, easing access to antiviral drugs, allowing the use of medical devices that remotely measure vital signs, and allowing veterinarians to utilize telemedicine—which was prohibited why?

Medicare is now paying for telemedicine visits, which makes a lot of sense for people who can’t leave their house easily or are at greater risk of infection which, come to think of it, is basically everyone who was on Medicare to begin with.

Numerous states are freeing nonviolent offenders who were put behind bars for technical violations or because they simply couldn’t afford bail. Cite-and-release policies are also being enacted across the country, keeping low-level offenders out of jail if there is no risk to the community—and it’s a pretty damning admission by authorities that for a long time they’ve been just fine with locking people up who pose no risk to the community.

And plastic bags are back, baby! After a hot and heavy fling with reusable grocery bags, politicians are waking up to realize that canvas totes have a secondary function as microbial party buses. So what was once banned is now required, and vice versa…in the name of public safety…subject to change.

Produced by Austin Bragg, research by John Osterhoudt Music: Vintage Rock by Anton Iliashenko—Pond5

from Latest – Reason.com https://ift.tt/2UTOAAp

via IFTTT

Luckin Coffee Crashes 85% After Admitting “Fabricating $300 Million In Sales”

Luckin Coffee says its special committee today brought to the attention of the board information indicating that COO Jian Liu and several employees engaged in certain misconduct, including fabricating certain transactions, starting 2Q last year.

CNBC’s David Faber estimates the total ‘fake’ revenue was around $310 million.

Shares crashed 85% in early trading….

In a 6k released today they admitted:

Luckin Coffee Inc. (“Luckin Coffee” or the “Company”) (NASDAQ: LK) today announced that the Company’s Board of Directors (the “Board”) has formed a special committee (the “Special Committee”) to oversee an internal investigation into certain issues raised to the Board’s attention during the audit of the consolidated financial statements for the fiscal year ended December 31, 2019 (the “Internal Investigation”).

The Special Committee is comprised of three independent directors of the Board, Mr. Sean Shao, Mr. Tianruo Pu and Mr. Wai Yuen Chong, with Mr. Shao serving as its chairman. The Special Committee has retained independent advisors, including independent legal advisors and forensic accountants, in connection with the Internal Investigation. The Special Committee has retained Kirkland & Ellis as its independent outside counsel. Kirkland & Ellis is assisted by FTI Consulting as an independent forensic accounting expert. The Internal Investigation is at a preliminary stage.

The Special Committee today brought to the attention of the Board information indicating that, beginning in the second quarter of 2019, Mr. Jian Liu, the chief operating officer and a director of the Company, and several employees reporting to him, had engaged in certain misconduct, including fabricating certain transactions. The Special Committee recommended certain interim remedial measures, including the suspension of Mr. Jian Liu and such employees implicated in the misconduct and the suspension and termination of contracts and dealings with the parties involved in the identified fabricated transactions. The Board accepted the Special Committee’s recommendations and implemented them with respect to the currently identified individuals and parties involved in the fabricated transactions. The Company will take all appropriate actions, including legal actions, against the individuals responsible for the misconduct.

The information identified at this preliminary stage of the Internal Investigation indicates that the aggregate sales amount associated with the fabricated transactions from the second quarter of 2019 to the fourth quarter of 2019 amount to around RMB2.2 billion. Certain costs and expenses were also substantially inflated by fabricated transactions during this period. The above figure has not been independently verified by the Special Committee, its advisors or the Company’s independent auditor, and is subject to change as the Internal Investigation proceeds. The Company is assessing the overall financial impact of the misconduct on its financial statements. As a result, investors should no longer rely upon the Company’s previous financial statements and earning releases for the nine months ended September 30, 2019 and the two quarters starting April 1, 2019 and ended September 30, 2019, including the prior guidance on net revenues from products for the fourth quarter of 2019, and other communications relating to these consolidated financial statements. The investigation is ongoing and the Company will continue to assess its previously published financials and other potential adjustments.

As @GreekFire noted, “We’ve lost 46 jobs for every confirmed case of COVID-19 in the US…“

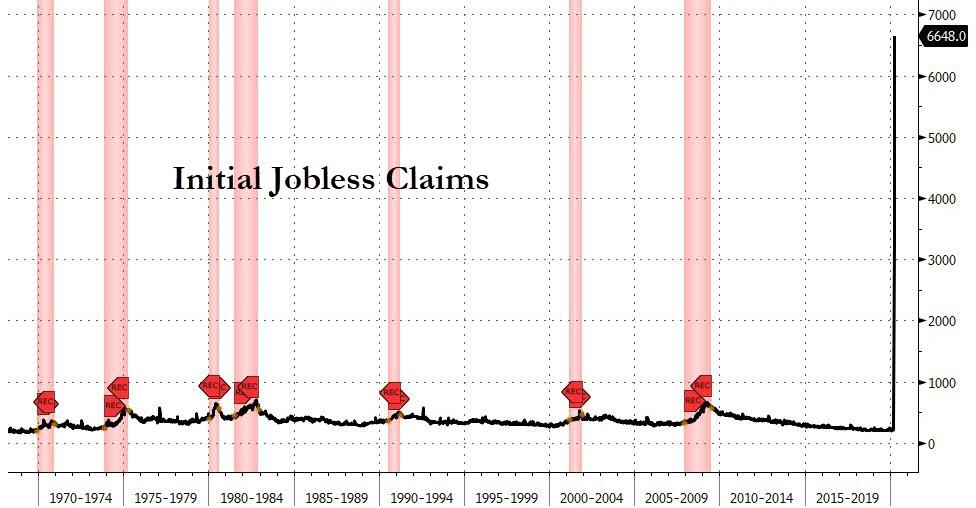

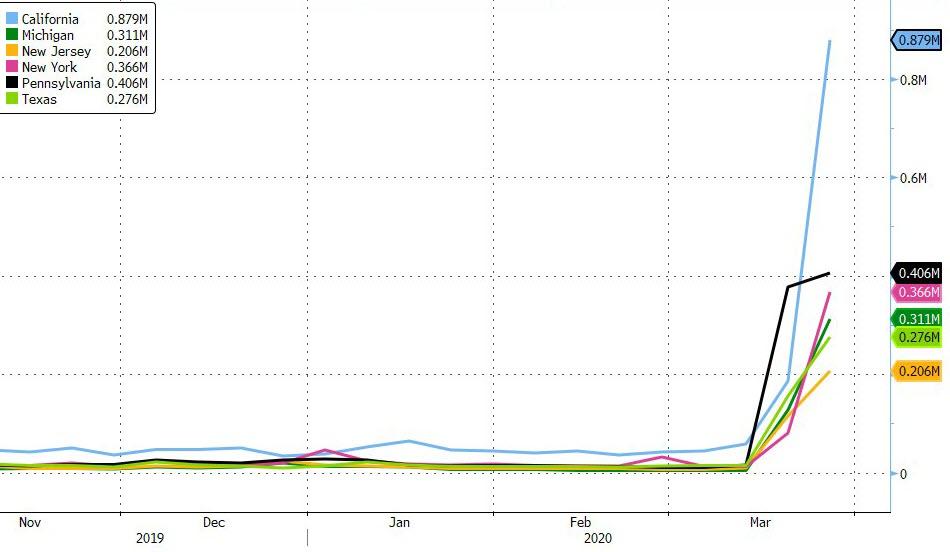

The 6.648mm print is worse than the worst of 50 estimating analysts’ expectations. Breaking down by state (which is one week lagged and so represents the prior week’s 3.3mm print detail), California, Pennsylvania, and New York dominate…

Source: Bloomberg

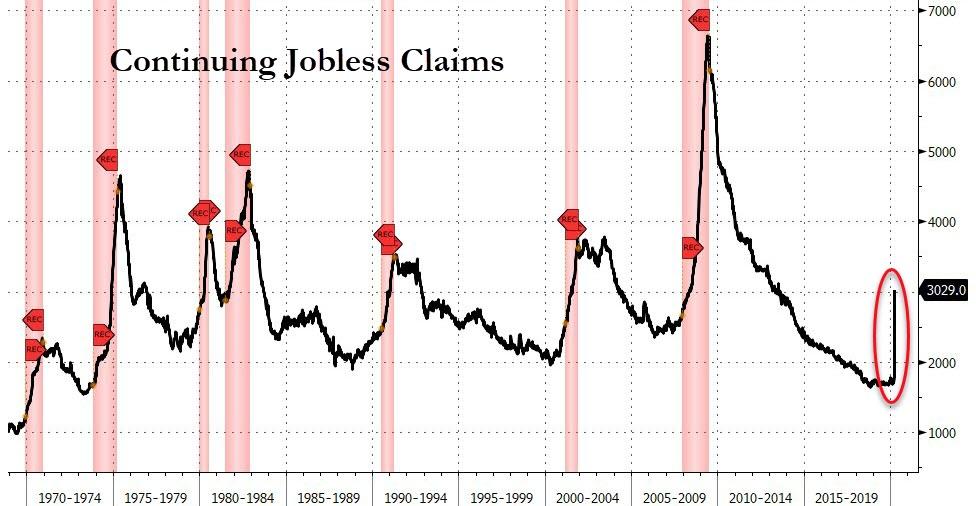

And of course, last week’s “initial” claims and this week’s “continuing” claims…

Source: Bloomberg

This is simply stunning.

“The U.S. labor market is in free-fall,” said Gregory Daco, chief U.S. economist at Oxford Economics in New York.

“The prospect of more stringent lockdown measures and the fact that many states have not yet been able to process the full amount of jobless claim applications suggest the worst is still to come.”

And another important note is that weekly jobless claims data are based on “hard facts”, UBS points out, unlike survey data

which is subject to quirks around:

a) some of the treatment of supply chains, which has flattered data,

b) the fact that many respondents will not be replying to surveys during the virus disruption period, and

c) survey data will give more accurate assessments during ‘normal’ times, perhaps not as much in unusual times.

Of course, the government is coming to the rescue. As a result of the freshly-passed ‘relief’ bill, self-employed and gig-workers who previously were unable to claim unemployment benefits are now eligible. In addition, the unemployed will get up to $600 per week for up to four months, which is equivalent to $15 per hour for a 40-hour workweek. By comparison, the government-mandated minimum wage is about $7.25 per hour and the average jobless benefits payment was roughly $385 per person per month at the start of this year.

“Why work when one is better off not working financially and health wise?” said a Sung Won Sohn, a business economics professor at Loyola Marymount University in Los Angeles.

With more than 80% of Americans under some form of lockdown, up from less than 50% a couple of weeks ago, this is far from over.

As RealInvestmentAdvice.com’s Lance Roberts warns, the importance is that unemployment rates in the U.S. are about to spike to levels not seen since the “Great Depression.” Based on the number of claims being filed, we can estimate that unemployment will jump to 15-20% over the next quarter as economic growth slides 8%, or more. (I am probably overly optimistic.)

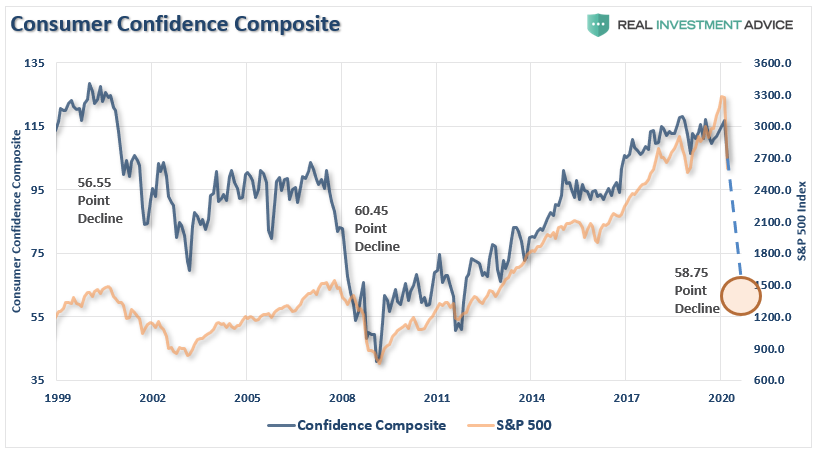

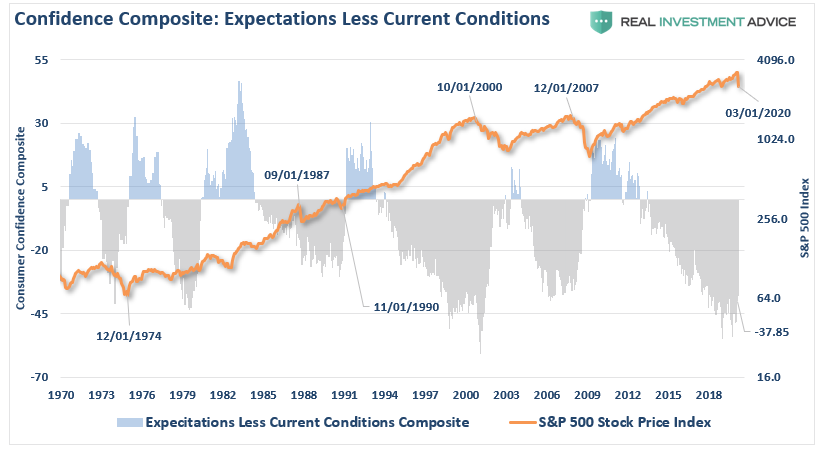

The erosion in employment will lead to a sharp deceleration in economic and consumer confidence, as was seen Tuesday in the release of the Conference Board’s consumer confidence index, which plunged from 132.6 to 120 in March.

This is a critical point. Consumer confidence is the primary factor of consumptive behaviors, which is why the Federal Reserve acted so quickly to inject liquidity into the financial markets. While the Fed’s actions may prop up financial markets in the short-term, it does little to affect the most significant factor weighing on consumers – their jobs.

The chart below is our “composite” confidence index, which combines several confidence surveys into one measure. Notice that during each of the previous two bear market cycles, confidence dropped by an average of 58 points.

With consumer confidence just starting its reversion from high levels, it suggests that as job losses rise, confidence will slide further, putting further pressure on asset prices. Another way to analyze confidence data is to look at the composite consumer expectations index minus the current situation index in the reports.

Similarly, given we have only started the reversion process, bear markets end when deviations reverse. The differential between expectations and the current situation, as you can see below, is worse than the last cycle, and only slightly higher than before the “dot.com” crash.

If you are betting on a fast economic recovery, I wouldn’t.

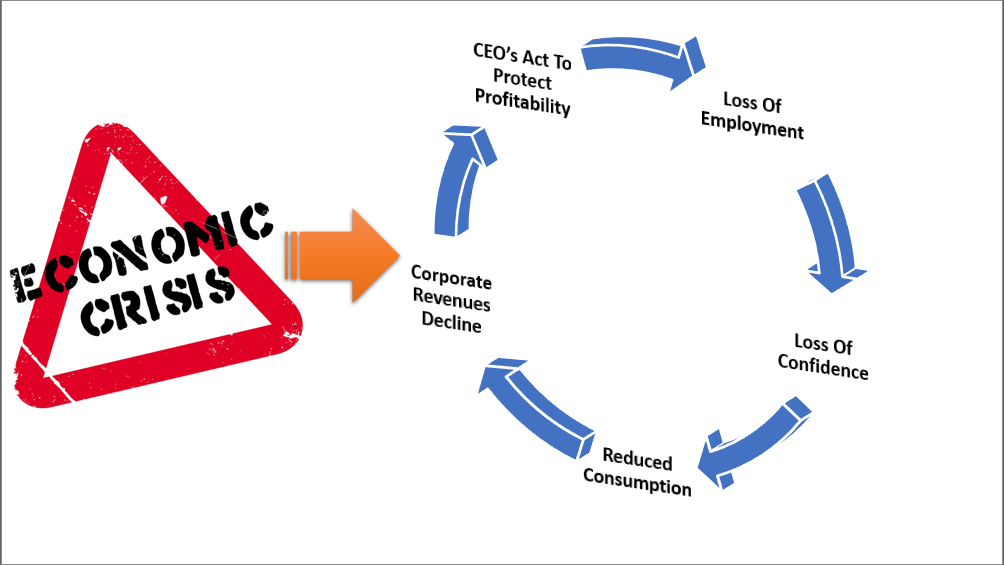

There is a fairly predictable cycle, starting with CEO’s moving to protect profitability, which gets worked through until exhaustion is reached.

As unemployment rises, we are going to begin to see the faults in the previous employment numbers that I have repeatedly warned about over the last 18-months. To wit:

“There is little argument the streak of employment growth is quite phenomenal and comes amid hopes the economy is beginning to shift into high gear. But while most economists focus at employment data from one month to the next for clues as to the strength of the economy, it is the ‘trend’ of the data, which is far more important to understand.”

That “trend” of employment data has been turning negative since President Trump was elected, which warned the economy was actually substantially weaker than headlines suggested. More than once, we warned that an “unexpected exogenous event” would exposure the soft-underbelly of the economy.

The virus was just such an event.

While many economists and media personalities are expecting a “V”-shaped recovery as soon as the virus passes, the employment data suggests an entirely different outcome.

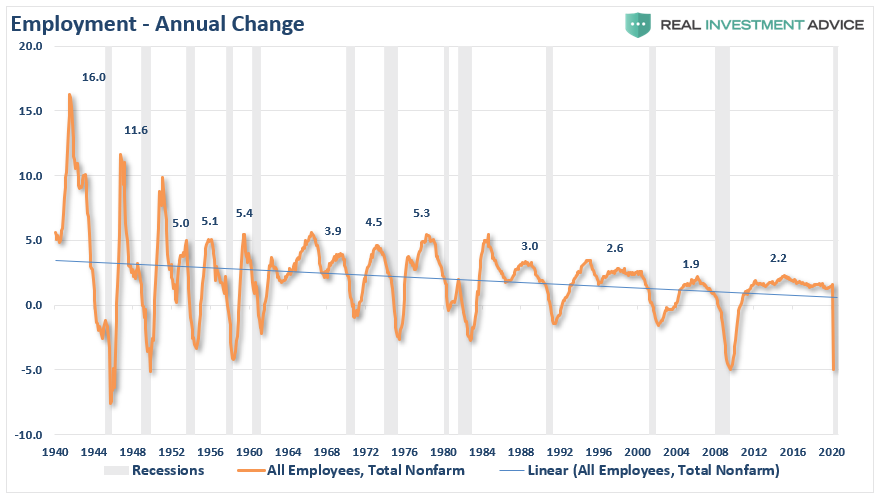

The chart below shows the peak annual rate of change for employment prior to the onset of a recession. The current cycle peaked at 2.2% in 2015, and has been on a steady decline ever since. At 1.3%, which predated the virus, it was the lowest level ever preceding a recessionary event. All that was needed was an “event” to start the dominoes falling. When we see the first round of unemployment data, we are likely to test the lows seen during the financial crisis confirming a recession has started.

No Recession In 2020?

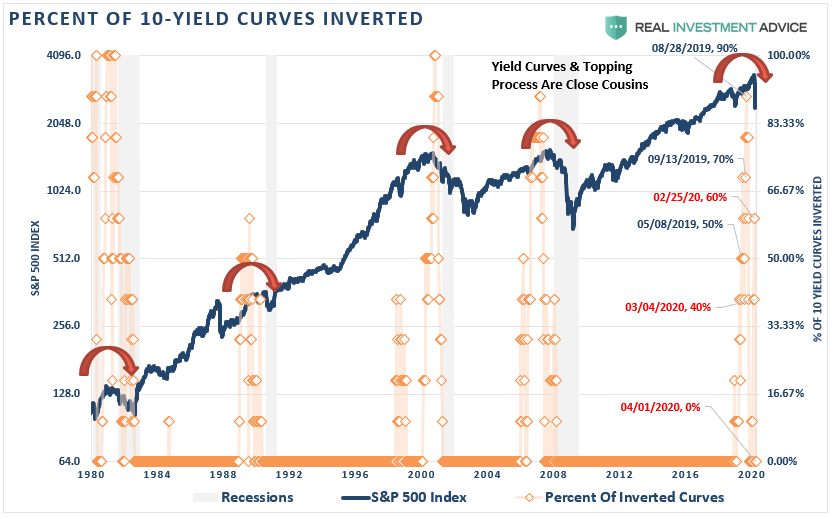

It is worth noting that NO mainstream economists, or mainstream media, were predicting a recession in 2020. However, as we noted in 2019, the inversion of the “yield curve,” predicted exactly that outcome.

“To CNBC’s point, based on this lagging, and currently unrevised, economic data, there is ‘NO recession in sight,’ so you should be long equities, right?

Which indicator should you follow? The yield curve is an easy answer.

While everybody is ‘freaking out’ over the ‘inversion,’it is when the yield-curve ‘un-inverts’ that is the most important.

The chart below shows that when the Fed is aggressively cutting rates, the yield curve un-inverts as the short-end of the curve falls faster than the long-end. (This is because money is leaving ‘risk’ to seek the absolute ‘safety’ of money markets, i.e. ‘market crash.’)”

I have dated a few of the key points of the “inversion of the curve.” As of today, the yield-curve is now fully un-inverted, denoting a recession has started.

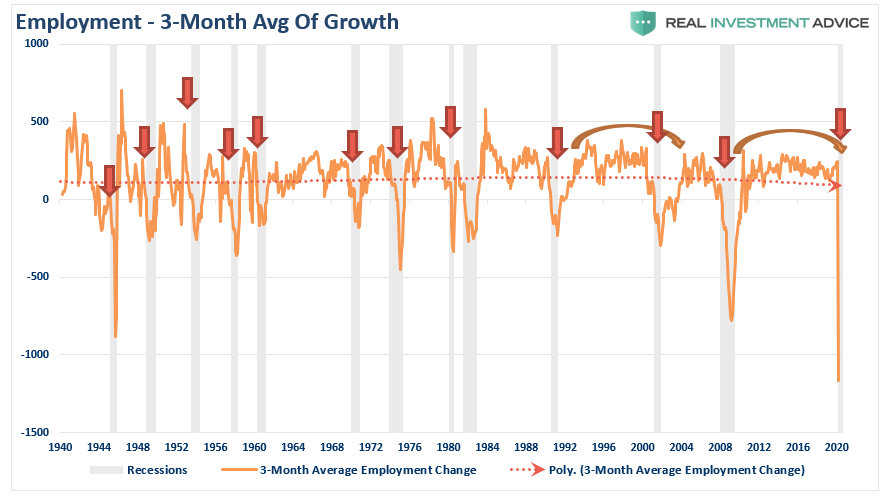

While recent employment reports were slightly above expectations, the annual rate of growth has been slowing. The 3-month average of the seasonally-adjusted employment report, also confirms that employment was already in a precarious position and too weak to absorb a significant shock. (The 3-month average smooths out some of the volatility.)

What we will see in the next several employment reports are vastly negative numbers as the economy unwinds.

Lastly, while the BLS continually adjusts and fiddles with the data to mathematically adjust for seasonal variations,the purpose of the entire process is to smooth volatile monthly data into a more normalized trend. The problem, of course, with manipulating data through mathematical adjustments, revisions, and tweaks, is the risk of contamination of bias.

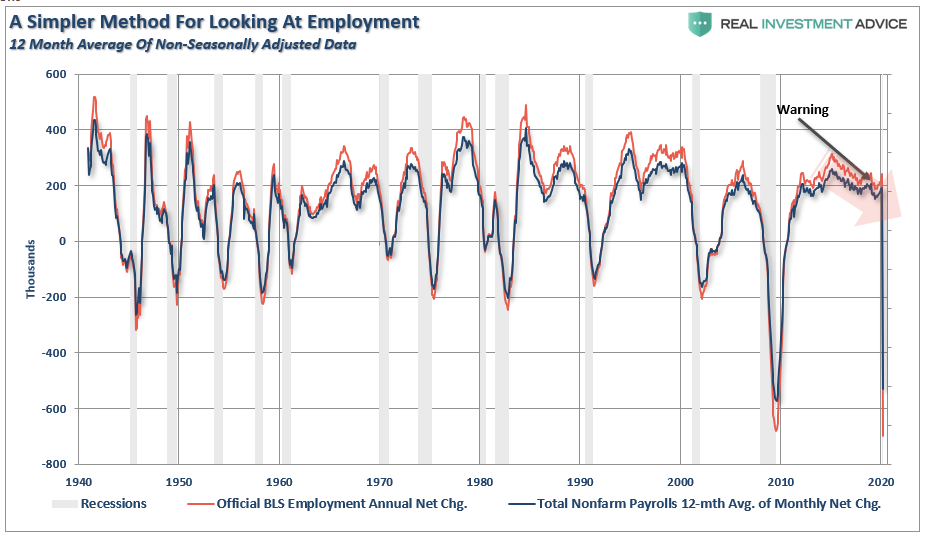

We previously proposed a much simpler method to use for smoothing volatile monthly data using a 12-month moving average of the raw data as shown below.

Notice that near peaks of employment cycles the BLS employment data deviates from the 12-month average, or rather “overstates” the reality. However, as we will now see to be the case, the BLS data will rapidly reconnect with 12-month average as reality emerges.

Sometimes, “simpler” gives us a better understanding of the data.

Importantly, there is one aspect to all the charts above which remains constant. No matter how you choose to look at the data, peaks in employment growth occur prior to economic contractions, rather than an acceleration of growth.

“Okay Boomer”

Just as “baby boomers” were finally getting back to the position of being able to retire following the 2008 crash, the “bear market” has once again put those dreams on hold. Of course, there were already more individuals over the age of 55, as a percentage of that age group, in the workforce than at anytime in the last 50-years. However, we are likely going to see a very sharp drop in those numbers as “forced retirement” will surge.

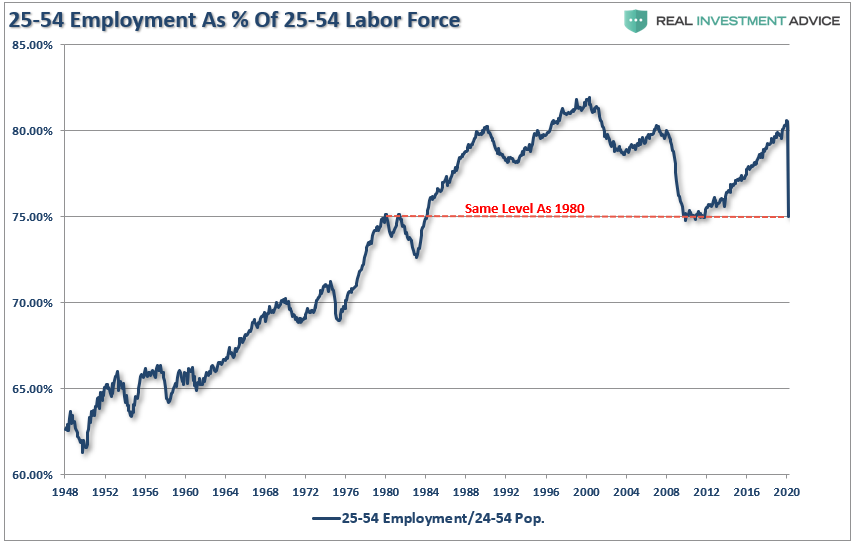

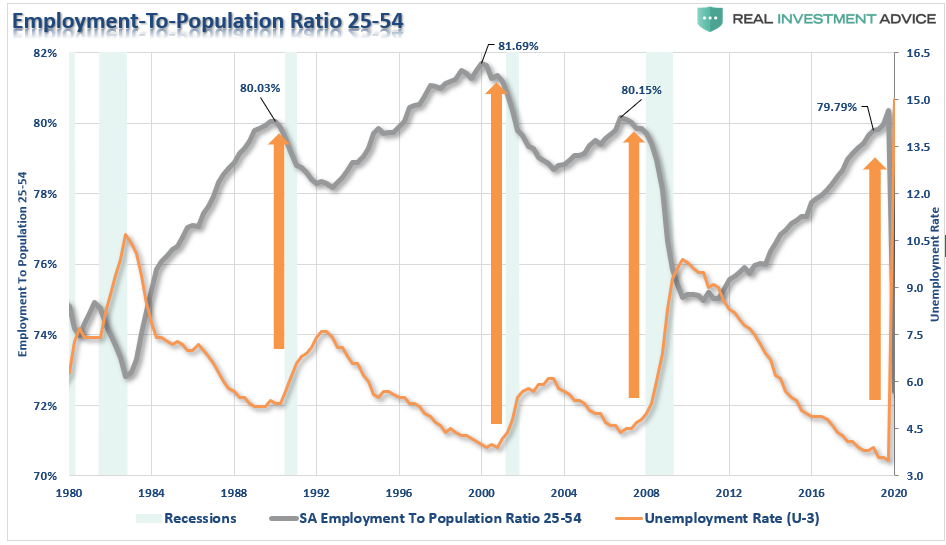

The group that will to be hit the hardest are those between 25-54 years of age. With more than 15-million restaurant workers being terminated, along with retail, clerical, leisure, and hospitality workers, the damage to this demographic will be the heaviest.

There is a decent correlation between surges in the unemployment rate and the decline in the labor-force participation rate of the 25-54 age group. Given the expectation of a 15%, or greater, unemployment rate, the damage to this particular age group is going to be significant.

Unfortunately, the prime working-age group of labor force participants had only just returned to pre-2008 levels, and the same levels seen previously in 1988. Unfortunately, it may be another decade before we see those employment levels again.

Why This Matters

The employment impact is going to felt for far longer, and will be far deeper, than the majority of the mainstream media and economists expect. This is because they are still viewing this as a “singular” problem of a transitory virus.

It isn’t.

The virus was simply the catalyst which started the unwind of a decade-long period of debt accumulation and speculative excesses. Businesses, both small and large, will now go through a period of “culling the herd,” to lower operating costs and maintain profitability.

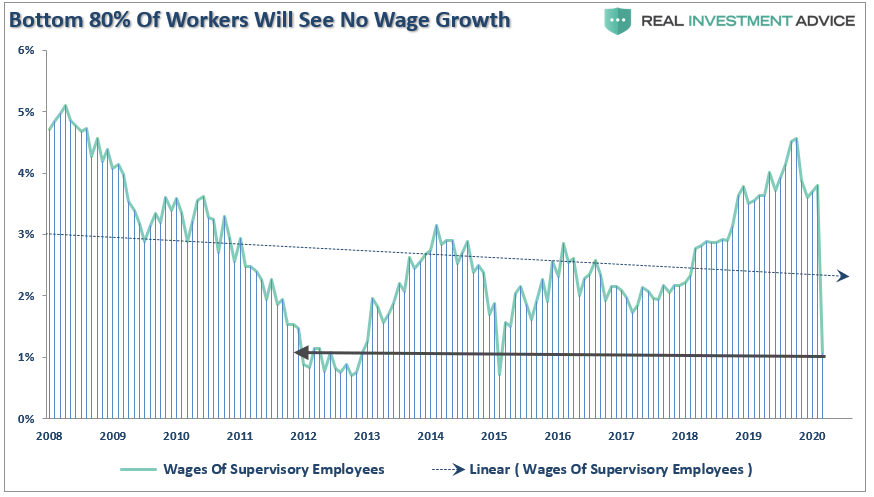

There are many businesses that will close, and never reopen. Most others will cut employment down to the bone and will be very slow to rehire as the economy begins to recover. Most importantly, wage growth was already on the decline, and will be cut deeply in the months to come.

Lower wage growth, unemployment, and a collapse in consumer confidence is going to increase the depth and duration of the recession over the months to come. The contraction in consumption will further reduce revenues and earnings for businesses which will require a deeper revaluation of asset prices.

“Every financial crisis, market upheaval, major correction, recession, etc. all came from one thing – an exogenous event that was not forecast or expected.

This is why bear markets are always vicious, brutal, devastating, and fast. It is the exogenous event, usually credit-related, which sucks the liquidity out of the market, causing prices to plunge. As prices fall, investors begin to panic-sell driving prices lower which forces more selling in the market until, ultimately, sellers are exhausted.

It is the same every time.”

Over the last several years, investors have insisted the markets were NOT in a bubble. We reminded them that everyone thought the same in 1999 and 2007.

Throughout history, financial bubbles have only been recognized in hindsight when their existence becomes “apparently obvious” to everyone. Of course, by that point is was far too late to be of any use to investors and the subsequent destruction of invested capital.

It turned out, “this time indeed was not different.” Only the catalyst, magnitude, and duration was.

Pay attention to employment and wages. The data suggests the current “bear market” cycle has only just begun.

* * *

Finally, as Southbay Research warns, by the time this mess settles, at least 20M American workers will have been furloughed. The math is relentless.

Self-isolation is crushing the Leisure & Hospitality sector (17M workers). Most of them are set to be out of work. Indeed, confirming the sector’s pain, SouthBay’s review of local job postings found a massive collapse: Leisure & Hospitality postings fell 80% compared to the same period last year. That figure will only worsen as more States and cities impose a lock down.

And that’s just one sector. Every sector is taking a hit, some more than others, but the average drop in labor demand is >50% (as reflected in job postings).

Things will get a bit uglier before they level off.

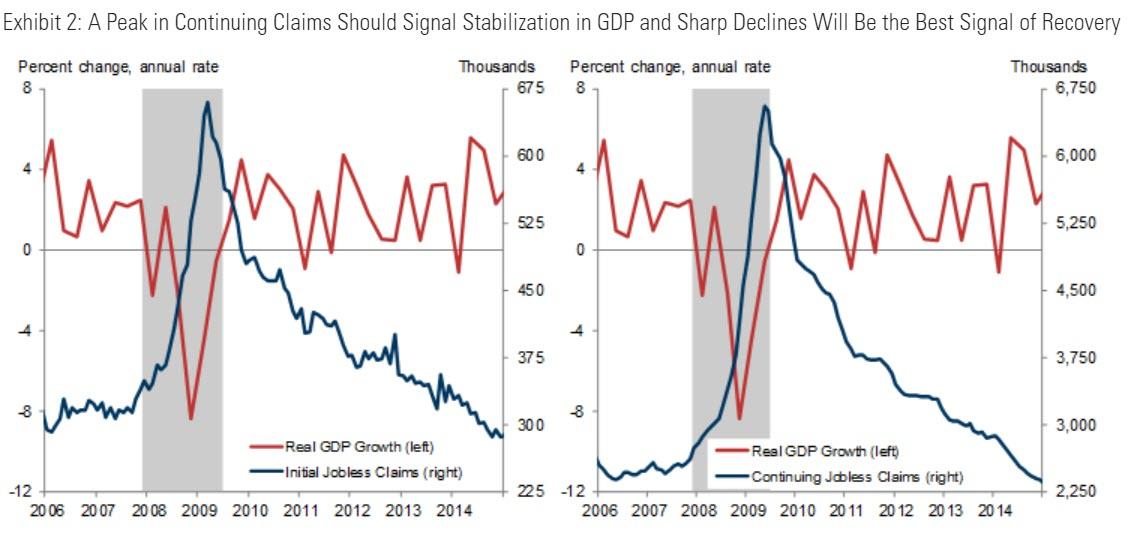

But Goldman has something positive to look for – even as this all begins to worsen dramatically – during the recovery from the last recession, GDP stabilized when initial claims first started to come down and continuing claims hit their peak. GDP started growing again when initial claims had fallen 1/3 of the way back to the pre-crisis level and continuing claims were falling quickly, as shown in Exhibit 2.

In the months ahead, we think that a levelling off of continuing claims will be a good signal that GDP has stabilized. Continuing claims will also likely be the clearer indicator that GDP has started growing again. Initial claims might normalize somewhat gradually as second-round effects of the virus shock generate ongoing layoffs. Continuing claims will better pick up an increase in hiring, which should accelerate more quickly than in a typical recession as some economic activities shut down by virus fears rebound more immediately (though this depends on the unemployment insurance benefits available at that point and on whether the economy recovers via slow adaptation or a more abrupt medical breakthrough).

US Futures Rebound From Plunge As Oil Jumps; All Eyes On Initial Claims

The market rollercoaster is back, if somewhat less stomach-churning, with US equity rebounding from yesterday’s plunge which – now that the pension fund frontrunning trade is over – was the worst start to a new quarter since the Great Depression.

S&P futures rose 1.9%, trading just below 2,500, and keeping track with the bounce in European stocks on Thursday morning…

… as investors braced for the latest unemployment data which some skeptics expect could surge as much as a record 6.5 million.

Futures on all U.S. equity indexes climbed following sharp losses a day earlier, though traders will be wary of further evidence of how the spreading coronavirus is hitting the American job market, as global cases are set to surpass 1 million today. The Stoxx Europe 600 Index fluctuated before turning higher, with energy shares outperforming as oil and gas stocks gained more than 5%, with Royal Dutch Shell, Total SA and BP jumping between 3.3% and 5.0%, thanks to the rise in oil prices. Shares in British Airways owner IAG added 1.5% after a person familiar with the matter said British Airways was in talks with its union about a plan to suspend around 32,000 staff so it can survive the coronavirus pandemic.

Earlier in the session, stocks in Asia were mixed, with Thailand’s SET and South Korea’s Kospi Index rising, and Australia’s S&P/ASX 200 and Japan’s Topix Index falling. In Japan, the Nikkei index ended down 1.37%, taking its losses to 25% so far this year as the BOJ bought less than the maximum ETFs for a second session.

The Topix declined 1.6%, with Hito Communications Holdings and Sankyo Tateyama falling the most. The Shanghai Composite Index rose 1.7%, with Sinopec Shanghai and JinJian Cereals Industry posting the biggest advances.

The market’s early bullish mood may deflate after today’s initial jobless claims report. “U.S. jobless claims are expected to surge again and in this environment we cannot talk about a recovery in equities in the short term. The best you can hope for is stablization in the current environment,” said Francois Savary, chief investment officer at Swiss wealth manager Prime Partners.

Initial claims for jobless benefits last week probably broke the week-ago record of 3.3 million, with 3.5 million expected, according to a Reuters survey of economists.

“We think last week’s print of just under 3.5 million is ripe for a dramatic upward revision,” said RBC Capital Markets’ chief U.S. economist, Tom Porcelli. “This week we look for another sizeable 4 million increase.”

Treasuries were broadly unchanged while investors again sought the safety of the U.S. dollar which hung on to recent gains despite the Fed’s announcement it would release Treasurys from its Supplemental Leverage Ratio calculation for one year, a move that in theory should release liquidity in the market and ease the dollar funding stress. The yield on safe-haven 10-year U.S. Treasuries fell as far as 0.5680% before rebounding.

“There had been fears about the bond market blowing up, but for the time being there’s a return to normal correleation in the market, so we don’t see a vicious cycle where bonds bring down equities and equities brings down bonds,” said Savary.

Euro zone government bond yields rose as investors cautiously moved back into riskier assets. The 10-year German government bond yield rose 3 basis points to -0.44%, rising away from the lows of -0.55% touched on Monday.

Oil surged as much as 13% after China unveiled plans to take advantage of a 60% plunge this year to add to stockpiles, coupled with optimism the price war between Saudi Arabia and Russia could moderate. Trump said he had talked recently with the leaders of both Russia and Saudi Arabia and believed the two countries would make a deal within a “few days” to lower production and thereby bring prices back up.

Looking at the latest virus data, China and South Korea have shown signs of controlling the virus, reporting falling numbers of new cases, but progress remains fragile and infections are soaring globally. The World Health Organization said the global case count would reach 1 million and the death toll 50,000 in the next few days. It currently stands at 46,906. U.S President Donald Trump, who had initially played down the outbreak, told reporters at the White House on Wednesday that he is considering a plan to halt flights to coronavirus hot zones in the United States. “Difficult days are ahead for our nation,” Trump said.

The Bloomberg Dollar Spot index rose while commodity currencies rallied with crude prices after a report that China plans to boost its oil reserves. Norwegian krone led Group-of-10 currency gains; USD/NOK slumped as much as 2.2% as Brent oil surged more than 12% on report of China buying plans; the Canadian, Australian and New Zealand dollars also climbed. The pound rose against both the dollar and the euro, rising an eighth straight day versus the shared currency — its best run since 2016. The yen weakened against the dollar for the first time in seven days on positioning flows. The Australian dollar gained 0.6% to $0.6110 and the Canadian dollar firmed 0.65% to C$1.4146. The euro traded down 0.3% at $1.0934 as the dollar advanced. The South African rand hit a fresh low while the Turkish lira touched a two-year low.

Expected data include jobless claims and factory orders. Walgreens Boots and Chewy are reporting earnings.

Market Snapshot

S&P 500 futures up 1.9% to 2,493.25

STOXX Europe 600 up 0.4% to 311.87

Nikkei down 1.4% to 17,818.72

Topix down 1.6% to 1,329.87

Hang Seng Index up 0.8% to 23,280.06

Shanghai Composite up 1.7% to 2,780.64

Sensex down 4.1% to 28,265.31

Australia S&P/ASX 200 down 2% to 5,154.30

Kospi up 2.3% to 1,724.86

German 10Y yield rose 2.6 bps to -0.432%

Euro down 0.4% to $1.0921

Italian 10Y yield fell 1.3 bps to 1.338%

Spanish 10Y yield rose 3.1 bps to 0.734%

MXAP down 0.3% to 133.66

MXAPJ up 0.4% to 431.64

Brent futures up 10% to $27.31/bbl

Gold spot down 0.1% to $1,590.11

U.S. Dollar Index down 0.1% to 99.55

Top Overnight News

Spain reported 950 new coronavirus fatalities on Thursday, the largest toll in a single day and taking the total number of deaths past 10,000

China said the U.S. is trying to shift the blame for the outbreak after American intelligence officials concluded the Asian nation concealed infections

China is moving ahead with plans to buy up oil for emergency reserves after prices crashed, according to people with knowledge of the matter

A county in central China has been put under lockdown again after a flare-up in coronavirus cases, pointing to the difficulty of sustaining outbreak containment in the face of carriers who show no signs of sickness

German Chancellor Angela Merkel and auto-industry officials discussed in a phone conference Wednesday measures to minimize contagion risks and protect workers’ health once assembly lines resume churning out vehicles, according to people familiar with the talks

German companies have applied for state aid worth 10.6 billion euros ($11.6 billion) under a government program run by state bank KfW

U.K. house prices were climbing at the fastest pace in more than two years before the coronavirus pandemic almost brought the market to a standstill, according to Nationwide Building Society

The number of Spaniards filing for jobless claims surged in March, the latest example of how the coronavirus pandemic is upending people’s livelihoods around the world

Asian equity markets traded mixed after a weak handover from Wall St where stocks extended on the prior quarter’s historical rout to finish the day with losses of more than 4% and the DJIA suffered a near 1000-point drop amid ongoing coronavirus fears. ASX 200 (-1.98%) was dragged lower by its top-weighted financials sector after the RBNZ ordered all banks in New Zealand to suspend dividends which pressured Australia’s big 4 that have operations across the Tasman and amid concerns there could be similar restrictions domestically, with airline shares also in a tailspin after the government denied Virgin Australia’s request for a loan and indicated it would not provide the Co. with a bailout. ASX 200 (-1.98%) was was also downbeat but off lows as the JPY-risk dynamic remained the main driver for Tokyo sentiment and with automakers lacklustre following abysmal monthly sales updates. Hang Seng (+0.8%) and Shanghai Comp. (+1.69%) initially struggled for direction amid the broad cautiousness and after PBoC liquidity inaction, while tensions with the US also risk flaring up as the latter is to tighten rules to prevent China from obtaining US tech for commercial purposes that could also be applied for military use and following US intelligence reports that alleged China concealed the coronavirus outbreak and underreported the number of cases and deaths. Finally, 10yr JGBs initially continued its pullback to below 152.50 with demand sapped heading into the 10yr JGB auction, although prices the rebounded on return from the lunch break and following mixed results in the 10yr auction which was mixed but still showed a jump in the b/c and minimal tail in price.

Top Asian News

Thailand Imposes Curfew to Step Up Fight Against Coronavirus

Qatar Is Said to Hire Banks to Raise Over $5 Billion in Bonds

Iron Ore Now at ‘More Realistic’ Price After Fall on Virus Shock

Japan Not Yet Ready to Declare Virus Emergency, Abe Says

European stocks attempt to clamber from yesterday’s steep losses (Euro Stoxx 50 +0.4%) after sentiment somewhat improved in APAC trade following a downbeat session on Wall Street. Bourses see modest broad-based gains, with Netherland’s AEX (+1.2%) leading the pack – propped up by Shell’s (+9%) Dutch listing and with ABN AMRO (+8.3%) and ING Groep (+1.8%) rebounding from the broad downside seen in banks yesterday. Meanwhile, US equity futures see more pronounced gains with the contracts higher to the tune of 2%. Sector-wise, Energy significantly outperforms – led by the price action in the oil complex as President Trump voiced optimism regarding a Saudi/Russia resolution, whilst demand from China keeps the sector underpinned. Other sectors are broadly mixed with underperformance seen in IT and Utility names – sectors do not reflect a specific risk tone. Travel & Leisure reside at the bottom of the pack as it feels no reprieve from the demand destruction caused by the virus outbreak. In terms of movers, the top of the Stoxx 600 was initially largely dominated by oil and gas names with Aker BP, Subsea losing steam as trade went underway whilst Tullow Oil (+8.0%), BP (+5.5%) and Shell remain among the top gainers. IAG (+2.5%) sees upside amid reports that the Co’s British Airways is nearing a deal to suspend 36k workers given the impact of operations from COVID-19. On the flip side; Carnival (-8.6%) sees pressure after S&P cut its rating to “BBB-“ from “BBB; the lowest investment grade level. Centrica (-7.4%) is weighed on by dividend and guidance suspensions coupled with the interruption of its Spirit Energy divestment. Elsewhere, Handelsblatt reported that the heads of Daimler (+1.0%), BMW (+3%) and Volkswagen (+1.0%) had a conversation with German Chancellor Merkel in which they wanted to explore how the corporations can rekindle production. The auto makers also raised worries regarding supply chains and expressed great concern regarding Southern Europe. On that note, Fiat Chrysler (-1.0%) slid at the open after Italy reported car registrations slumping 85.4% YY in March amid the lockdown measures in the country.

Top European News

Citigroup Hires Ex-Danish Prime Minister Rasmussen as Adviser

One of the World’s Best Welfare States is Starting to Crack

EasyJet Founder Escalates Feud With Board Over Massive Jet Order

Hungary Central Bank Pays Dividend to Boost State Virus Warchest

In FX, The Norwegian Krona and its Scandinavian partner are forging more gains on a combination of constructive technical factors, Euro underperformance and a recovery in oil prices prompted by China replenishing crude reserves at cheaper levels and US President Trump expressing confidence about resolving the spat between Russia and Saudi Arabia. Eur/Nok has been down below 11.2000 and Eur/Sek sub-10.9350, with the former also gleaning encouragement from ramped up Norges Bank selling of foreign currencies in April. Meanwhile, the Loonie is also benefiting from the firmer bounce in oil alongside the Rouble and Mexican Peso, as Usd/Cad tests support around 1.4100, Usd/RUB straddles 78.0000 and Usd/MXN pivots 24.0000. Elsewhere, the Kiwi and Aussie are consolidating off recent lows amidst less volatile trading conditions than seen of late, with Nzd/Usd holding firmly above 0.5900 and Aud/Usd not far from 0.6100 against the backdrop of relatively stable risk sentiment and Moody’s reaffirming NZ’s top notch triple A rating.

EUR/CHF/JPY – As noted above, the single currency remains under pressure across board as COVID-19 cases and deaths continue to rise in the Euro area, while chart impulses turn more bearish after shallower rebounds in Eur/Usd and even Eur/GBP despite the UK also suffering mounting nCoV infections and fatalities. Indeed, the headline pair has not been able to revisit 1.1000 and looks more prone to relinquishing 1.0900, while the cross is capped beneath 0.8800 after waning well short of 0.8900. Moreover, further or ongoing erosion in Eur/Chf towards 1.0550 is helping to keep the Franc on a fairly even keel vs the Dollar within confined 0.9687-51 parameters, and the Yen is almost as restrained between 107.56-06 eyeing big option expiries in close proximity, but also extending from 106.50 to 108.00-05 – full details on our Headline Feed as 7.29BST.

USD – Cautious trade ahead of the 2nd instalment of post-coronavirus global outbreak US initial claims that are widely expected to top last week’s circa 3.3 mn biggest ever total, with GS among those lifting already sky-high projections to 6 mn. The DXY is straddling 99.500 in the run up.

In commodities, US President Trump said he thinks Saudi and Russia will make a deal regarding oil production and suggested that he may know how to solve it. There were also comments from the US Energy Department which urged Saudi Arabia, Russia and others to work together to calm oil markets, while it noted it is frustrating that Saudi and Russia are boosting production and do not advance shared interests in stable markets. Senior Gulf source said Saudi Arabia supports cooperation among oil producers to stabilize oil markets and that oil market turmoil was caused by Russia opposition to OPEC+ cuts at the meeting in early March.

US Event Calendar

7:30am: Challenger Job Cuts YoY, prior -26.3%

8:30am: Initial Jobless Claims, est. 3.7m, prior 3.28m; Continuing Claims, est. 4.94m, prior 1.8m

8:30am: Trade Balance, est. $40.0b deficit, prior $45.3b deficit

10am: Cap Goods Ship Nondef Ex Air, est. -0.8%, prior -0.7%; Cap Goods Orders Nondef Ex Air, est. -0.8%, prior -0.8%

10am: Factory Orders Ex Trans, prior -0.1%;

10am: Durable Goods Orders, est. 1.2%, prior 1.2%; Durables Ex Transportation, est. -0.6%, prior -0.6%

10am: Factory Orders, est. 0.2%, prior -0.5%

DB’s Jim Reid concludes the overnight wrap

With governments indicating that we’re going to be in a prolonged period of lockdowns that are pushing towards the dates we outlined in our “The exit strategy” note, it wasn’t exactly the strongest start to Q2 yesterday for global equity markets. They continued to decline as investors grappled with the implications of the coronavirus moving forward. Last week was the peak week of the great stimulus reveal but this week is seeing the reality of the situation re-emerge.

The S&P 500, which had already fallen by 20% in Q1 in its worst quarterly performance since 2008 (see our March/Q1 performance review here), fell a further -4.11%. The pullback was the biggest one day drop in 2 weeks, with the index falling 3 of the past 4 days now. Every sector and industry group was lower, though defensives like consumer staples continue to outperform their more cyclical counterparts. In Europe the STOXX 600 fell -2.93%. Banks underperformed with the STOXX Banks index down -4.34% as it fell for a 4th successive session. UK banks saw some of the biggest falls, including Lloyds (-11.66%) and Barclays (-10.34%) after they announced that they would not be paying outstanding 2019 dividends, nor would there be dividend payments or share buybacks this year after guidance from their regulators. While this is an understandable move, there is a slight financial stability risk as banks need investors and if investors believe they are going to be penalised then they are less likely to commit capital. A difficult balance to strike. On this topic, overnight, the Reserve Bank of New Zealand has also asked lenders that come under its jurisdiction to stop dividend payments for an indefinite period and focus on building capital. They will also not be allowed to redeem any non-Tier 1 capital notes.

Talking of the U.K., this is one country where covid-19 fatalities are still rising. They are up +31.5% over the last 24 hours, the second largest one-day increase over the last week. Cases also increased by +17%, as Prime Minister Johnson continues to call for additional testing. Elsewhere Italy and Spain continue to see slowing trends, with day-over-day changes in fatalities dropping again. Meanwhile cases in the US continue to grow. See our Corona Crisis Daily note for the full tables, graphs, and commentary. Note that as of today we have broken New York State out in our daily tables, with the 4th largest state in the US now having more cases than those reported in China as a whole. Overall US reported cases are now in excess of 200,000 and even VP Pence yesterday suggested that the country was on a similar trajectory as Italy. President Trump also said he was considering restricting flights between heavily affected ‘hot spots’, but that it may affect industry more. Dr. Fauci says that 18 month remains the timetable for a vaccine, and that we remain on target for it.

Staying with virus-related news, overnight, an article in China’s SMCP has suggested that a county in Henan have been asked to stay at home following news that there were three infection cases due to a doctor returning from Wuhan having the virus and already spreading to his colleagues. It’s unclear if this is a one-off, but if this is a re-surge of cases particularly as mobility picks up, then clearly there is the risk of lockdowns again.

A quick check on markets this morning and most bourses in Asia have pared heavier declines from the open. The Shanghai Comp (+0.33%) and Kospi (+0.52%) are now up while the Hang Seng (-0.09%) and Nikkei (-0.33%) are posting modest losses. The Australia’s ASX is down -2.03% with banks that have subsidiaries in New Zealand under pressure following the RBNZ news mentioned earlier. Meanwhile, futures on the S&P 500 are up +1.47% with the US dollar index and yields on 10y USTs being largely unchanged. Elsewhere, Brent crude oil is up +5.78% this morning with President Trump set to meet executives from the US oil companies tomorrow as the White House seeks ways to help the industry reeling from price drop.

Over in fixed income yesterday US Treasuries rallied further, with 10yr yields down by -8.6bps to 0.583%, their second lowest level ever and closing in on their all-time closing low earlier this month of 0.541%. They rallied 5bps of that after the US equity market had closed on news that the Fed is easing strains in the Treasury market by excluding Treasuries and deposits at the Fed from its supplementary leverage ratio rule. They hope this will also make it easier for banks to extend credit. This will last a year.

The yield curve also flattened, with the 2s10s curve down by -5.0bps to 37.0bps, its flattest level in nearly 3 weeks after peaking at 68.3bps back then. In Europe peripheral spreads were set for their 4th successive widening but a story hit the tape just as the market was closing that left them more mixed, with Italy slightly tighter and Spain still a touch wider. The story suggested that the Dutch were floating the idea of a €20bn fund as an EU virus response. As a sum it hardly touches the sides of what DB thinks will be a 20pp increase in Debt/GDP in Italy and Spain in 2020, but if it shows the direction of travel after the lack of progress at last week’s EU leader’s summit then this is a small step that the market will like.

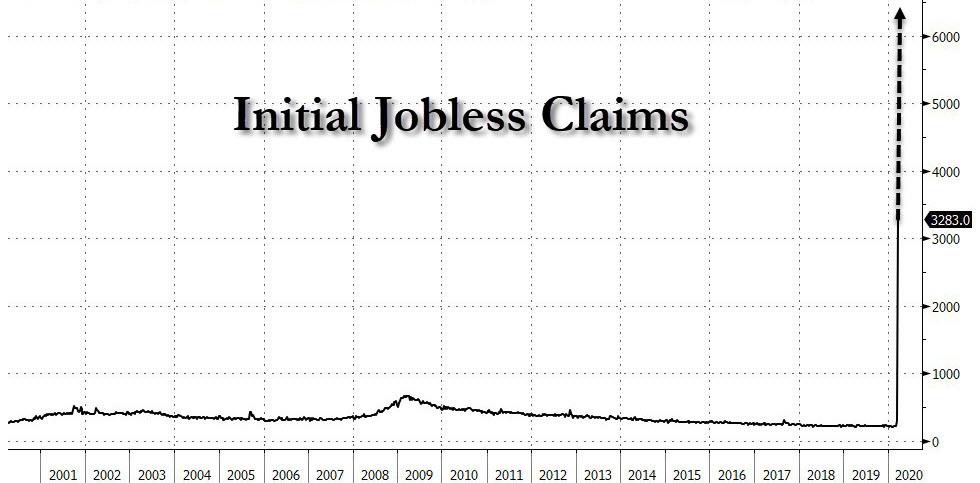

One of the main events to look out for today will be the latest weekly initial jobless claims in the US, which is one of the most important real-time indicators for markets right now as to what’s going on in the economy. Following last week’s record 3.283m claims, our US economists are forecasting 3.3m for the week ending 28 March, which as was pointed out last week far exceeds anything seen during the financial crisis, when the peak week in March 2009 was at 665k. Today’s release is actually more important than tomorrow’s jobs report for March, as the end of the survey period for that came before the spike in jobless claims we saw last week, so it won’t be as up-to-date on the current economic situation as jobless claims are.

In terms of data out yesterday, the manufacturing PMIs confirmed much of what we already knew from the flash releases last week, in that just about every country in the world has moved into contractionary territory. Looking at the major countries, the Euro Area PMI came in at 44.5 (vs. flash 44.8), while the German reading was also revised down slightly from the flash to 45.4 (vs. flash 45.7), as was the US which fell to 48.5 (vs. flash 49.2).

Over in the US, the ISM manufacturing was actually not as bad as expected, at 49.1, (vs. 44.5 expected). However, this was thanks to a jump in supplier delivery times, with the index rising to 65.0. Normally, slower deliveries mean that the economy is strengthening thanks to rising demand, but in this instance it is supply issues that are causing the problem, so it’s not much consolation. Furthermore, the new orders index fell to 42.2, the lowest since March 2009, while the employment index fell to 43.8, the lowest since May 2009.

To wrap up yesterday’s data, the ADP report of private payrolls saw a -27k decline in March (vs. -150k expected), and its second worst month going back to February 2010. However, as the ADP themselves acknowledged, the report doesn’t cover the full impact of the coronavirus as the report uses data through March 12th. We also got German retail sales for February, which rose by +1.2% mom (vs. +0.1% expected).

To the day ahead now, and there are a number of data highlights from the US, including the previously mentioned weekly initial jobless claims, factory orders and the trade balance for February, as well as the final reading for durable goods orders for February. Elsewhere, we’ll get the Euro Area PPI reading for February, the UK Nationwide house price index for March, along with Canada’s international merchandise trade for February.

The Trump administration’s Iran policy has been business as usual since the spread of the novel coronavirus began, and that’s a grave mistake. The president’s tweet today warning Iran “or its proxies” against any “sneak attack on U.S. troops and/or assets in Iraq” is merely the latest example of misplaced priorities while a pandemic worsens in the U.S.

President Trump’s “maximum pressure” approach to U.S.-Iran relations was counterproductive to our security and deleterious to diplomatic progress under ordinary conditions. Now, the United States and Iran are suffering two of the most severe COVID-19 outbreaks on the planet. Keeping up maximum pressure is a dangerous distraction for the United States and catastrophic for the Iranian people, whom Trump administration officials profess to support against their oppressive regime. Trump should abandon maximum pressure once and for all. It doesn’t work; it will damage prospects of a free and democratic Iran for decades to come; and it’s an unjustifiable distraction from vital U.S. interests in a time of pandemic.

The failure of maximum pressure was evident before the COVID-19 crisis started. After withdrawing from the Joint Comprehensive Plan of Action (JCPOA), commonly known as the Iran deal, the Trump administration re-imposed harsh sanctions the deal had lifted and deployed U.S. forces and ships (currently including two of our 11 aircraft carriers) as an unmistakable threat to Tehran.

The goal is to force Iran, as Secretary of State Mike Pompeo likes to put it, to behave like “a normal country.” The entirely foreseeable effect has been exactly the opposite. Again and again it has incentivized escalation by a regime desperate to prove it will not be cowed. It has brought us closer to war, not peace. “Through a series of relatively limited but still dangerous military actions and incremental retreat from the terms of the JCPOA, Iran has signaled that it will not concede to the U.S. demands without a fight,” explains MIT’s Barry Posen at Boston Review. Maximum pressure is exacerbating Iran’s regional troublemaking. It is making us less secure.

Posen suggests a thought experiment: What would we do were the United States under similar pressure from another nation—a nation which had, in the last two decades, invaded our near neighbors and conducted regime change operations and long-term occupations. “Given the intensity and religious elements of Iranian nationalism, the regime is unlikely to comply,” he concludes, “and the Iranian people will likely support them, despite the regime’s present domestic difficulties.”

If ever there was a chance that U.S. sanctions could push the Iranian people to rebel against their government, as Pompeo hopes, COVID-19 has killed it. U.S. sanctions have compounded the effects of cruel and stupid pandemic response decisions by Tehran, severely impeding the Iranian medical response. Although Washington insists humanitarian goods are exempted from the sanctions, restrictions on financial institutions sharply curtail movement of desperately needed supplies. However angry ordinary Iranians may be at their government, this moment will create a lasting—and still avoidable!—antipathy for the United States and the values we tout if Trump does not change course.

The novel coronavirus pandemic adds a fresh urgency to the need for a new model of U.S.-Iran relations. Whatever trivial threat Iran could pose the U.S., we have more pressing concerns here at home (and so does Tehran, for that matter). Redoubling maximum pressure, as Trump and Pompeo have done in recent weeks, is a damaging and irrational distraction. The very last thing we need is continuing escalation toward another unnecessary Mideast war. It would be reckless, wasteful, and unstrategic in the best of times. It is inexcusable when we have a pandemic to handle.

from Latest – Reason.com https://ift.tt/2R3KSTK

via IFTTT

The Trump administration’s Iran policy has been business as usual since the spread of the novel coronavirus began, and that’s a grave mistake. The president’s tweet today warning Iran “or its proxies” against any “sneak attack on U.S. troops and/or assets in Iraq” is merely the latest example of misplaced priorities while a pandemic worsens in the U.S.

President Trump’s “maximum pressure” approach to U.S.-Iran relations was counterproductive to our security and deleterious to diplomatic progress under ordinary conditions. Now, the United States and Iran are suffering two of the most severe COVID-19 outbreaks on the planet. Keeping up maximum pressure is a dangerous distraction for the United States and catastrophic for the Iranian people, whom Trump administration officials profess to support against their oppressive regime. Trump should abandon maximum pressure once and for all. It doesn’t work; it will damage prospects of a free and democratic Iran for decades to come; and it’s an unjustifiable distraction from vital U.S. interests in a time of pandemic.

The failure of maximum pressure was evident before the COVID-19 crisis started. After withdrawing from the Joint Comprehensive Plan of Action (JCPOA), commonly known as the Iran deal, the Trump administration re-imposed harsh sanctions the deal had lifted and deployed U.S. forces and ships (currently including two of our 11 aircraft carriers) as an unmistakable threat to Tehran.

The goal is to force Iran, as Secretary of State Mike Pompeo likes to put it, to behave like “a normal country.” The entirely foreseeable effect has been exactly the opposite. Again and again it has incentivized escalation by a regime desperate to prove it will not be cowed. It has brought us closer to war, not peace. “Through a series of relatively limited but still dangerous military actions and incremental retreat from the terms of the JCPOA, Iran has signaled that it will not concede to the U.S. demands without a fight,” explains MIT’s Barry Posen at Boston Review. Maximum pressure is exacerbating Iran’s regional troublemaking. It is making us less secure.

Posen suggests a thought experiment: What would we do were the United States under similar pressure from another nation—a nation which had, in the last two decades, invaded our near neighbors and conducted regime change operations and long-term occupations. “Given the intensity and religious elements of Iranian nationalism, the regime is unlikely to comply,” he concludes, “and the Iranian people will likely support them, despite the regime’s present domestic difficulties.”

If ever there was a chance that U.S. sanctions could push the Iranian people to rebel against their government, as Pompeo hopes, COVID-19 has killed it. U.S. sanctions have compounded the effects of cruel and stupid pandemic response decisions by Tehran, severely impeding the Iranian medical response. Although Washington insists humanitarian goods are exempted from the sanctions, restrictions on financial institutions sharply curtail movement of desperately needed supplies. However angry ordinary Iranians may be at their government, this moment will create a lasting—and still avoidable!—antipathy for the United States and the values we tout if Trump does not change course.

The novel coronavirus pandemic adds a fresh urgency to the need for a new model of U.S.-Iran relations. Whatever trivial threat Iran could pose the U.S., we have more pressing concerns here at home (and so does Tehran, for that matter). Redoubling maximum pressure, as Trump and Pompeo have done in recent weeks, is a damaging and irrational distraction. The very last thing we need is continuing escalation toward another unnecessary Mideast war. It would be reckless, wasteful, and unstrategic in the best of times. It is inexcusable when we have a pandemic to handle.

from Latest – Reason.com https://ift.tt/2R3KSTK

via IFTTT

Oil Surges On Report China Buying For Strategic Reserve, Hopes For Saudi-Russia Truce

Oil surged as much as 13% this morning following a report that China is planning to start buying cheap crude for its strategic reserves, as well as speculation that President Trump said he thought Saudi Arabia and Russia would resolve their differences in the oil price war that has sent supply soaring even as global oil demand tumbles.

Following massive builds in crude in the US as reported by the DOE and API, and amid sporadic reports that various storage facilities are starting to fill up:

SALDANHA BAY OIL-STORAGE FACILITY SAID TO BE NEAR CAPACITY

OIL TANKS AT VITAL AFRICA HUB ALMOST FULL AS CRUDE FLOODS MKT

… overnight, Bloomberg reported that Beijing instructed government agencies to start filling state stockpiles after oil plunged 66% over the first three months of the year, while the global benchmark’s nearest timespread also rallied strongly.

Beijing has asked government agencies to quickly coordinate filling tanks, Bloomberg source said. In addition to state-owned reserves, it may use commercial space for storage as well, while also encouraging companies to fill their own tanks. The initial target is to hold government stockpiles equivalent to 90 days of net imports, which could eventually be expanded to as much as 180 days when including commercial reserves.

According to Bloomberg calculations, 90 days of net crude imports translated to about 900 million barrels. By comparison, the U.S. currently holds about 635 million barrels in its Strategic Petroleum Reserve, according to government data.

And while the current size of China’s state reserves is unknown, and Beijing could use a different method for calculating net imports, oil traders and analysts at SIA Energy and Wood Mackenzie estimated it could amount to China buying an additional 80 million to 100 million barrels over the course of the year before it ran into logistical and operational constraints.

In September, the head of development and planning at the National Energy Administration said the country had total oil reserves, including strategic stockpiles, for about 80 days. In December, state-owned China National Petroleum Corp. said on its website that the government intends to boost the capacity of its strategic petroleum reserves to 503 million barrels by the end of this year, an indicator of the maximum amount the government can store.

The volume targeted is about the same as the Trump administration proposed buying last month for U.S. reserves to help that country’s drillers. The plan was thwarted after Democrats blocked a request for funds.

China is also planning to announce the fourth batch of strategic reserve sites, the people said. The expansion project has the dual advantage of creating larger emergency reserves and as an economic stimulus project to spur construction opportunities as the country recovers from the coronavirus.

While the purchases could help soak up some excess supply, traders said it will fall well short of offsetting the overall glut created by the virus lockdowns and the price war between Saudi Arabia and Russia.

As Bloomberg adds, China’s move comes as the physical crude market shows deepening signs of strain as supply explodes and demand collapses due to the coronavirus. Dated Brent, the benchmark for two-thirds of the world’s physical supply, was assessed at $15.135 on Wednesday, the lowest since at least 1999. Crude has slipped below $10 in some areas including Canada and shale regions in the U.S., Belarus wants to buy Russian oil for $4, while some grades have posted negative prices.

“News that China will take advantage of lower prices to add to reserves has clearly provided a boost to the market,” said Warren Patterson, head of commodities strategy at ING Bank NV. “But given the extremely bearish outlook for the market it is difficult to believe that this strength is sustainable.”

And speaking of the Saudi oil price war, overnight President Trump painted a more optimistic tone in the price war between Saudi Arabia and Russia, saying he thought the two would work out the differences even as Saudi Arabia began ramping up output to record levels in recent days. The rhetoric and the possibility of action from the White House sparked hopes for a truce in the price war between Saudi Arabia and Russia.

Speaking late on Wednesday, Trump said he expects the situation with Saudi and Russia will be resolved. He also said he’s planning to meet with independent oil producers in addition to the majors. “They’re negotiating, they’re talking, and I think they’ll come up with something,” Trump said. “I do believe there’s a way that that can be solved or pretty well solved.”

According to the WSJ, Trump is set to meet Friday with the heads of some of the largest U.S. oil companies to discuss measures to help the industry as it fights for survival. The chief executives of Exxon Mobil and Chevron are expected to attend.

Also attending the White House meeting will be Continental Resources Inc. CEO Harold Hamm, who has called for the Trump administration to intervene in the Saudi-Russian price war. Other shale companies have called on state regulators to enforce production cuts in Texas.

Trump also said he was confident Saudi Arabia and Russia would resolve their dispute over oil output and prices in the coming days. In response, Russian President Vladimir Putin said Wednesday that oil producers should cooperate to mitigate the market decline, adding that Moscow is discussing the condition of the oil market with Washington and the Organization of the Petroleum Exporting Countries.

The main driver of oil’s rally was “the announcement by Trump telling the world ‘we’ve been talking with the Russians and the Saudis and he’s quite proud of these oil diplomacy efforts,” said Bjørnar Tonhaugen, head of oil markets at consultancy Rystad Energy. “He’s trying to save the U.S. industry from collapse.”

Still, the oil rally faded and sellers emerged later in the morning as many oil-market watchers remained skeptical about the impact of any end to the price war given the impact of the lockdowns on demand.

“I don’t think this meeting significantly changes things, the oil market is still way out of balance and oil stocks are still rising at an unprecedented rate,” said Spencer Welch, director of oil markets at IHS Markit. “Producers are going to have to involuntarily cut production because there’s going to be nowhere for the oil to go.”

And as the world awaits for a change in status quo, oil storage around the world is beginning to fill up, prompting some companies to enact production cuts. Brazilian state-owned giant Petrobras last week became one of the first major companies to announce such reductions. Even with Thursday’s rally, oil prices remain below the cost of production for the U.S., Canada and Russia. Meanwhile, in the U.S. stockpiles grew by the most since 2017 on Wednesday, while consultants from IHS to FGE have said that world inventories may be full within weeks, an event Goldman previously said would be a game changer for the industry and prompted the bank to expect prices to dip in the teens if only for a short while.

Submitted by Eleanor Creagh, Australian Market Strategist at Saxo Bank

US equity markets recorded a seven-sigma move last week. Under a normal distribution, the expected occurrence of this event is equal to one day in 3,105,395,365 years

By the time this goes to print, a lot could have changed already — that is how quickly information is moving while financial markets, policymakers and communities grapple with the global pandemic.

At this stage, sentiment is stretched and we are probably nearing peak panic, but that does not necessarily coincide with the market bottoming. With limited quantitative data related to the virus outbreak, precise forecasts are scarce.

We are in uncharted waters with respect to both the global public health crisis and financial market conditions: hence the heightened cross-asset volatility. To have real confidence in a relief rally, volatility must reset meaningfully lower.

For now, the AUD remains under pressure as recession looms, but being a risk proxy there will be moments of optimism. The Reserve Bank of Australia (RBA) has lowered the cash rate to the effective lower bound of 0.25% and adopted QE policy in Australia, aiming to maintain the 3-year bond yield at 0.25% and support liquidity in fixed income markets.

Heightened volatility and risk aversion; a domestic economy that’s already in the midst of a pre-existing slowdown; stretched consumers saddled with high household debt levels and a shift to unconventional monetary policy are all weighing on the local unit. The palpable rush to the USD certainly isn’t helping. The US dollar remains a safe haven in the midst of the global equity market and liquidity rout, cementing the path for recession as the strong dollar compounds the virus damage.

The virus outbreak has sent tremors through highly leveraged financial markets, revealing multiple fault lines that we previously caught glimpses of in Q4 2018 and September 2019. These fault lines were patched over, fuelling the ever-extending complacency and yield reaching which have lulled markets and volatility alike throughout the past decade of central bank intervention. In the wake of the global pandemic, the fault lines are now fissures.

Moreover, the record lows in volatility that drove a generation to chase excess yield, momentum and passive mania have been replaced with soaring volatility, stressed liquidity and deleveraging across all corners of financial markets. Even the havens are not safe while many dash for cash.

US equity markets recorded a seven-sigma move last week. Under a normal distribution, the expected occurrence of this event is equal to one day in 3,105,395,365 years, a period almost five times longer than complex lifeforms have existed on planet. Clearly, we are not assessing these probabilities correctly. Not only has risk been misgauged due to the prior decade of financial repression surpassing volatility and spurring complacency, but the assumptions upon which we build our asset allocations are wrong and vastly understate true risk.

As Steen highlights in the introduction to this outlook, the popular idea that the spectrum of asset allocation only stretches from some mix of bonds and equities has always been flawed. This most recent rout could truly shake the long-term allocation model away from a 60/40 bond/equity allocation.

Markets are dealing with a health crisis that cannot be appeased by central banks. As the baton is passed to governments, who will be stepping up to provide cash directly to businesses and households, we enter a new regime. Whether the shockwaves of this event are truly enough to shift traditional industry thinking remains to be seen, but we should at least see a more broad-based approach to diversification over the long term — thus increasing exposure to the potential higher volatility regime shift.

Although the virus is a shorter-term issue, some of its ramifications will be long lasting. It has not only laid bare the fault lines in financial markets, but also the systemic risks embedded in our heavily interconnected and globalised supply chains. The US/China trade war was a warning shot for the global flow of goods and a reminder that tectonic shifts are underway for global geopolitical architectures and international cooperation.

Vulnerabilities throughout global supply chains, ‘just in time’ manufacturing models and the pursuit of cost minimisation above all else have been exposed by the virus outbreak. The crisis of confidence among communities has been perpetuated by political fragmentation, populism and pro-nationalist sentiment. This means the tailwind for the ongoing de-globalisation shift has only grown — and with it, nationalism, protectionism and localisation.

If low inflation has been perpetuated by globalisation and a 30-year spate of deregulation, the opposite should be true down the line. But only once the global economy emerges from the deflationary demand shock the virus crisis and oil price war brings. The assumptions that have underpinned asset prices for many decades are shifting, which favours increased portfolio diversification to counter trend assets to achieve superior risk-adjusted returns. For example, by building long-term allocations to real assets that benefit from eventual higher growth and inflation — such as commodities and precious metals.

What is currently a liquidity crisis could fast become a solvency crisis as the simultaneous shocks to demand and supply weigh on the balance sheets of otherwise solvent SMEs. This crisis is about too many to fail, as opposed to too big to fail. Distressed entities (businesses and households) desperately need a lifeline to maintain wages, rents and other such payments that do not stop as economic activity grinds to a halt. That cash flow support will be vital in providing goodwill payments to casual workers who lose shifts, extended sick pay for those unable to work and preventing layoffs for those businesses facing a material impact from the COVID-19 outbreak.

Given the level of household debt, another key area of concern for Australia is the labor market. With household leverage ratios at almost 2x incomes, a spike in unemployment could prompt a far more serious economic fallout. That is why it is paramount for the government and the RBA to consider maintaining job security as a focal point in their response measures.

The fiscal package to date is just the first line of defence that’s needed for the Australian economy. More will be necessary. The measures so far pale in comparison to the New Zealand government’s package, which is approximately 4% of GDP relative to the Morrison government’s 1.2%.

The Australian economy comes from a position of weakness and desperately needed a fiscal contribution even before the virus hit. The economy has lost momentum since the second half of 2018: unemployment has risen, the private sector is in recession and both business and consumer confidence has been in the mire. In addition, more recently the combination of bushfires and drought have served a one-two punch to Australia’s economy and battered the agriculture, tourism and recreation industries even before any travel bans came into place.

Things are moving quickly — far quicker than they did in the GFC — markets and shutdowns included. For each stimulus package announced, a corresponding travel ban is enacted or city is locked down. Shutdowns, border closures and disruptions are moving at such a pace that economists and markets alike cannot mark down growth expectations quickly enough. As the number of infections continues to rise globally, the likelihood of these measures becoming more aggressive will further impact economic activity.

With so many unknowns at large, forecasts seem little more than vague verbiage that are consistently marked to market. However, what is certain is that an exceptional policy response is necessary. TINA (there is no alternative) can be applied in a different sense as monetary policy pushes on a string and unemployment rises. Policymakers must underwrite the demand shock and helicopter drop payments directly to households along with support for cash-strapped businesses.

We have little doubt of this, given multiple conjectures toward wartime action to buy time in the virus fight while we await a vaccine or immunity. Although even this is no perfect solution, as the hit to sentiment and therefore demand cannot easily be reversed by monetary or fiscal policy. While consumers are fearful of the threat of a global pandemic, confidence will be hard to restore. Hence why containment efforts and public health policy are equally important in supporting confidence.

Although stimulus packages may ease downside risks to the economy, for markets to really recover the onus will be on reduced COVID-19 transmission rates, increased immunity and a clear containment of the outbreak. As yet, relative to previous crises, valuations have not become outright cheap. Nevertheless, hope springs eternal both in financial markets and humanity, so there will come a time for bargain hunting. However, as the rulebooks go out the window in terms of crisis rescue packages, we may eventually enter a different investment paradigm. The extraordinary fiscal stimulus, a de-globalisation tailwind and eventual recovery in economic activity will bring at the very least higher inflation expectations, and long-term bond yields may eventually rise. Perhaps we’ll see an opportunity to rethink diversification beyond the traditional 60/40 and a comeback for value, cyclicals and commodities.