During a house-shopping visit to a small industrial city in Ohio where I had taken my first newspaper job, I asked a local, “What’s that smell?” His answer: “What smell?” Residents there had become so accustomed to the industrial scents from the city’s massive chemical plant and oil refinery that they didn’t notice them anymore. When out-of-town visitors would ask me the same question, I’d say: “It’s the smell of money and jobs.”

After the refinery announced plans to shut down, local and state officials desperately tried to convince the company to stay put—and finally intervened to help find a buyer. I don’t believe in such government meddling, but viewed the reaction as understandable. Officials rarely want to lose companies—even old, smelly ones—that fund their budgets and employ their residents.

California, however, is a different animal. Democratic leaders have long lived up to one of Ronald Reagan’s best quotations: “Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

Lately though, they have taken this further by singling out the innovative tech sector for torment—as if they’re purposely trying to drive these companies to Texas or Arizona. Unlike in Rust Belt states, that industry provides jobs and money without the air-polluting stench. In fact, these are among the most environmentally friendly industries imaginable.

California officials are constantly bleating about our status as the world’s fifth-largest economy. Its $2.7 trillion Gross Domestic Product has surpassed Great Britain—putting California behind the United States as whole, China, Japan, and Germany. The biggest economic driver here is the tech economy.

Officials should not provide tech firms with special favors—nor should they hobble them. The most obvious example of the latter is Assembly Bill 5, which codifies the California Supreme Court’s 2018 Dynamexdecision. The court created a strict new “ABC Test” for determining when a company can use contractors as workers. Simply put, they can never use them to fulfill core company functions (e.g., drivers for a delivery company).

Lawmakers carved out myriad exemptions for traditional businesses (lawyers, engineers, insurance brokers, etc.)—and have agreed to carve out more (musicians) after the law’s implementation led to widespread job losses. But the measure specifically targeted Transportation Network Companies (TNCs) such as Uber and Lyft, and app-based delivery services such as DoorDash and Amazon. The state refuses to relent, even though AB 5 undermines these companies’ business model.

This month, the California Public Utilities Commission, which regulates these businesses, announced that these “drivers are presumed to be employees and the commission must ensure that TNCs comply with those requirements that are applicable to the employees of an entity subject to the commission’s jurisdiction.” The agency will not wait until lawsuits and a November ballot initiative resolve matters.

Meanwhile, Attorney General Xavier Becerra and city attorneys from Los Angeles, San Diego and San Francisco last month filed a controversial lawsuit against Uber and Lyft. They alleged that, “the illicit cost savings defendants have reaped as a result of avoiding employer contributions to state and local unemployment and social insurance programs totals well into the hundreds of millions of dollars.” Gov. Gavin Newsom included $20 million to fund enforcement actions.

In a separate matter, the California Department of Tax and Fee Administration last year sent letters to small businesses across the country that sell products to Californians on online platforms such as Fulfillment by Amazon. The department told them they owe eight years of back taxes. It considers these mostly mom-and-pop firms to have a “physical presence” in California if they distributed products through a third-party warehouse. It was a troubling attack on small businesses, but also on the tech-based firms that drive California’s economy.

During the coronavirus shutdowns, Tesla CEO Elon Musk became so frustrated with California officials that he threatened to move his Palo Alto headquarters to Texas. He announced plans to defy stay-at-home orders and even sued Alameda County, where his Fremont factory is located, but later dropped the suit after working out a deal with the county. The issue was resolved, but it’s telling when a prominent business leader has to threaten to move to get regulatory relief.

In recent years, local governments haven’t been particularly friendly to their hometown companies, either. San Francisco officials have been blaming tech firms for growing income inequality and soaring home prices—even though such problems are largely the fault of the city’s tax and regulatory policies. They’ve proposed hefty taxes that target—and punish—tech companies and they sometimes direct vitriol toward them.

There’s no need to pity successful companies or grant them special deals. It’s strange, however, when state officials are so blinded by their anti-corporate ideology that they become immune to the smell of jobs and money.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/3eGicda

via IFTTT

This week I’ve been posting about principles of style that made the writing of Lincoln, Churchill, and Holmes so potent. The posts are all taken from this new book that I hope you will check out if you’ve found the discussions interesting. (Otherwise I just thank you for your patience.)

The examples this week have all involved the choice between different kinds of words: Latinate vs. Saxon, simple vs. complex, abstract vs. visual. The book also talks about many other issues: the lengths of sentences, active vs. passive voice, cadences, etc. It shows how great writers have made use of contrast in working with those variables, and how the contrasts have lent power to their words.

Those examples are part of a general argument that I mentioned on Monday and to which I’ll return here in brief. It is that our culture of advice about good writing is inadequate. Don’t get me wrong: usually being clear and concise is the best thing a writer can do, and sometimes it’s the only thing a writer should worry about. But if you want your words to do more than just convey information—if you want to move others to action, or even just hold their attention—there is more to know. The “more” is the study of rhetoric.

To put it differently: conventional books about writing often talk as though you get better by pushing as far as you can in one direction: toward more simplicity. But rhetorical force requires two things, not one. The two things might be plain and fancy words, long and short sentences, high or rich substance and low or simple style (or vice versa), the concrete and the abstract, the formal and the informal, or other pairs. If you want your writing to cook, learn how to play with those polarities.

You might wonder what relevance rhetoric can have in the age of Trump. But Trump confirms the importance of all this. He is a user of polarities. Put dignified language into his mouth and he amounts to nothing; put his undignified language into the mouth of someone with ordinary status, and he too would amount to nothing. But such a casual lack of dignity in a tycoon, television star, and presidential candidate—this was something! A more vivid collision of high and low would be hard to devise, and many people have found it compelling or refreshing or amusing enough to make all objections seem trivial.

My book isn’t quite about that sort of rhetorical polarity—not principally, anyway. It’s about other polarities that have been effective in the hands of talented writers and talkers. The methods of earlier eras may not be working as well as the methods of Trump under current conditions (but don’t jump to conclusions; Trump hasn’t been challenged by a Lincoln). Even if so, however, the comings and goings of such appeals run in cycles. The principles of rhetorical power are always worthy of study—or, failing that, fun to know about—no matter what shape they’re taking at the moment.

If you’re interested in these themes, here’s a last link to the book that goes into detail about them; it’s part of a series on rhetoric that also includes this one and this one.

I’m very grateful to Eugene and his crew for letting me visit their great blog and talk about all this. I’ve posted about other books here before—one about thinking like a lawyer, another about the law of restitution, another about Stoic philosophy—and have made good friends among those who found them here. Keep up the good work, Eugene!

from Latest – Reason.com https://ift.tt/3i0Cpwx

via IFTTT

During a house-shopping visit to a small industrial city in Ohio where I had taken my first newspaper job, I asked a local, “What’s that smell?” His answer: “What smell?” Residents there had become so accustomed to the industrial scents from the city’s massive chemical plant and oil refinery that they didn’t notice them anymore. When out-of-town visitors would ask me the same question, I’d say: “It’s the smell of money and jobs.”

After the refinery announced plans to shut down, local and state officials desperately tried to convince the company to stay put—and finally intervened to help find a buyer. I don’t believe in such government meddling, but viewed the reaction as understandable. Officials rarely want to lose companies—even old, smelly ones—that fund their budgets and employ their residents.

California, however, is a different animal. Democratic leaders have long lived up to one of Ronald Reagan’s best quotations: “Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

Lately though, they have taken this further by singling out the innovative tech sector for torment—as if they’re purposely trying to drive these companies to Texas or Arizona. Unlike in Rust Belt states, that industry provides jobs and money without the air-polluting stench. In fact, these are among the most environmentally friendly industries imaginable.

California officials are constantly bleating about our status as the world’s fifth-largest economy. Its $2.7 trillion Gross Domestic Product has surpassed Great Britain—putting California behind the United States as whole, China, Japan, and Germany. The biggest economic driver here is the tech economy.

Officials should not provide tech firms with special favors—nor should they hobble them. The most obvious example of the latter is Assembly Bill 5, which codifies the California Supreme Court’s 2018 Dynamexdecision. The court created a strict new “ABC Test” for determining when a company can use contractors as workers. Simply put, they can never use them to fulfill core company functions (e.g., drivers for a delivery company).

Lawmakers carved out myriad exemptions for traditional businesses (lawyers, engineers, insurance brokers, etc.)—and have agreed to carve out more (musicians) after the law’s implementation led to widespread job losses. But the measure specifically targeted Transportation Network Companies (TNCs) such as Uber and Lyft, and app-based delivery services such as DoorDash and Amazon. The state refuses to relent, even though AB 5 undermines these companies’ business model.

This month, the California Public Utilities Commission, which regulates these businesses, announced that these “drivers are presumed to be employees and the commission must ensure that TNCs comply with those requirements that are applicable to the employees of an entity subject to the commission’s jurisdiction.” The agency will not wait until lawsuits and a November ballot initiative resolve matters.

Meanwhile, Attorney General Xavier Becerra and city attorneys from Los Angeles, San Diego and San Francisco last month filed a controversial lawsuit against Uber and Lyft. They alleged that, “the illicit cost savings defendants have reaped as a result of avoiding employer contributions to state and local unemployment and social insurance programs totals well into the hundreds of millions of dollars.” Gov. Gavin Newsom included $20 million to fund enforcement actions.

In a separate matter, the California Department of Tax and Fee Administration last year sent letters to small businesses across the country that sell products to Californians on online platforms such as Fulfillment by Amazon. The department told them they owe eight years of back taxes. It considers these mostly mom-and-pop firms to have a “physical presence” in California if they distributed products through a third-party warehouse. It was a troubling attack on small businesses, but also on the tech-based firms that drive California’s economy.

During the coronavirus shutdowns, Tesla CEO Elon Musk became so frustrated with California officials that he threatened to move his Palo Alto headquarters to Texas. He announced plans to defy stay-at-home orders and even sued Alameda County, where his Fremont factory is located, but later dropped the suit after working out a deal with the county. The issue was resolved, but it’s telling when a prominent business leader has to threaten to move to get regulatory relief.

In recent years, local governments haven’t been particularly friendly to their hometown companies, either. San Francisco officials have been blaming tech firms for growing income inequality and soaring home prices—even though such problems are largely the fault of the city’s tax and regulatory policies. They’ve proposed hefty taxes that target—and punish—tech companies and they sometimes direct vitriol toward them.

There’s no need to pity successful companies or grant them special deals. It’s strange, however, when state officials are so blinded by their anti-corporate ideology that they become immune to the smell of jobs and money.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/3eGicda

via IFTTT

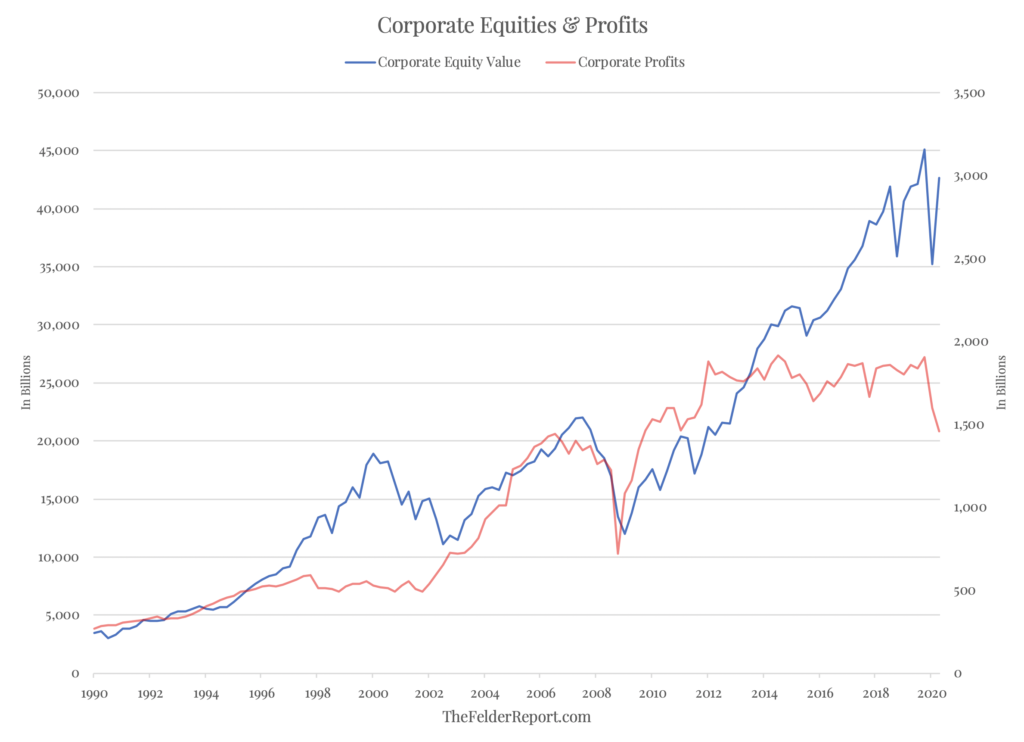

Everyone is talking about the massive disparity between stock prices and fundamentals right now. To paraphrase Jeremy Grantham, we now find ourselves in the top 1% of stock market valuations and the bottom 1% of economic outcomes (based on the annualized rate of decline in second quarter GDP). A popular way to demonstrate this gap is seen in the chart below which plots total equity values along with total corporate profits.

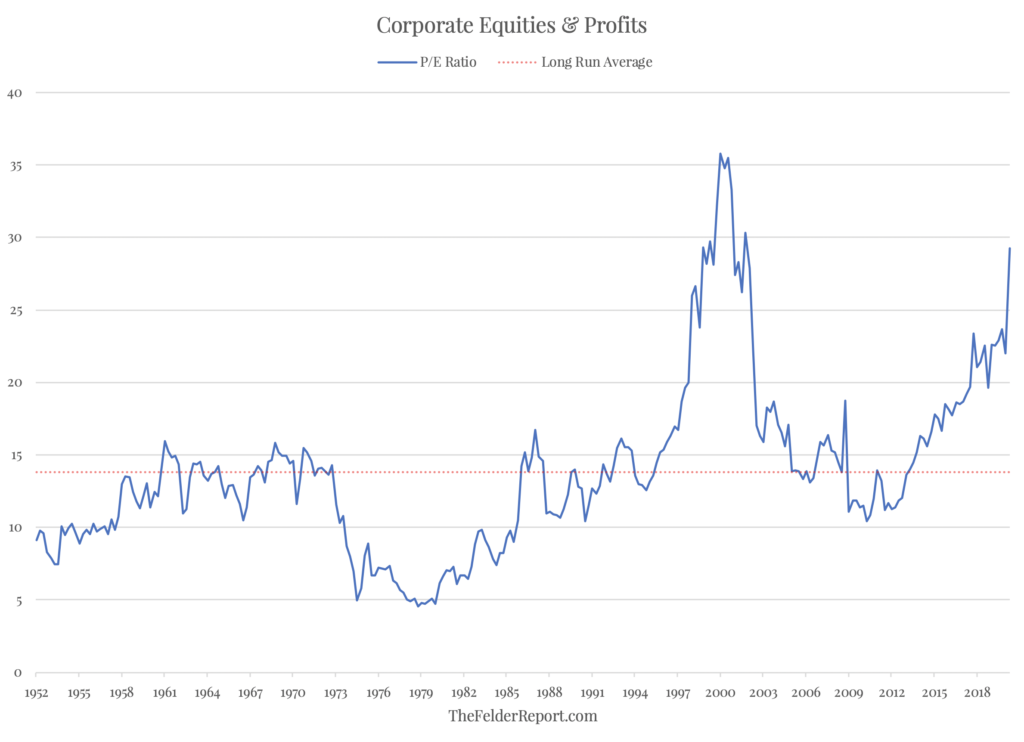

At first glance, it appears this is the biggest disconnect between prices and profits in at least 30 years. However, if we turn this into a price-to-earnings ratio, it becomes clear that the stock market bubble of 20 years ago actually takes the cake.

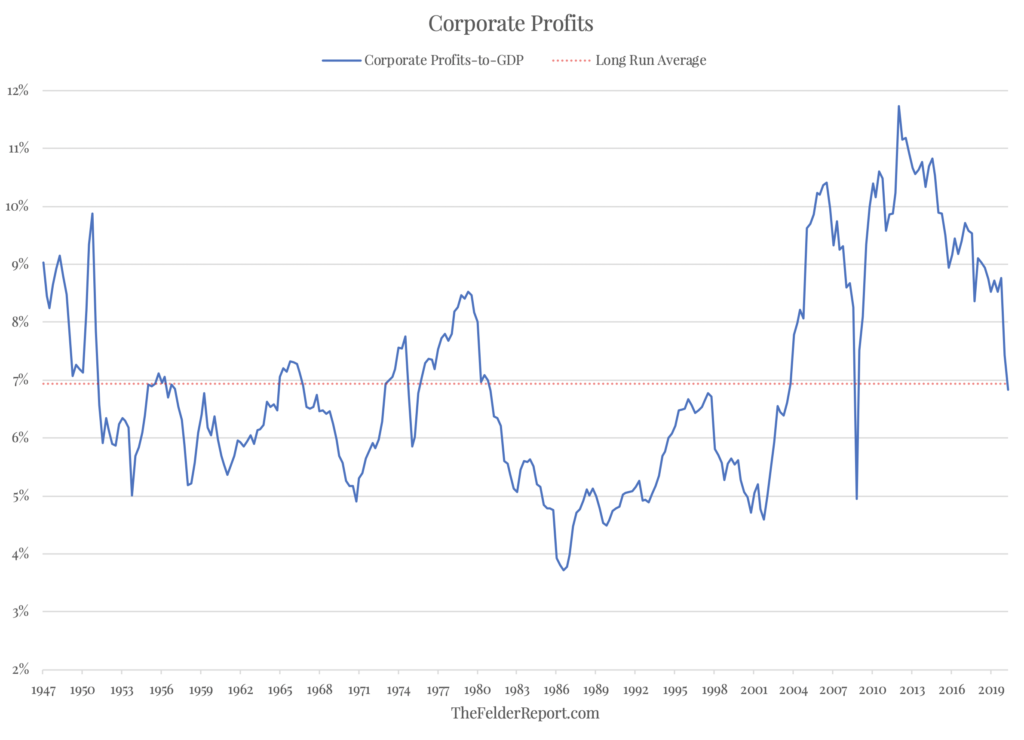

But what a simple price-to-earnings ratio doesn’t account for is the fact that Dotcom bubble appears so severe in the chart above largely because profit margins were relatively depressed at the time. Furthermore, profit margins in recent years became extremely inflated. This serves to make stock prices over the past few years look less expensive than they otherwise would.

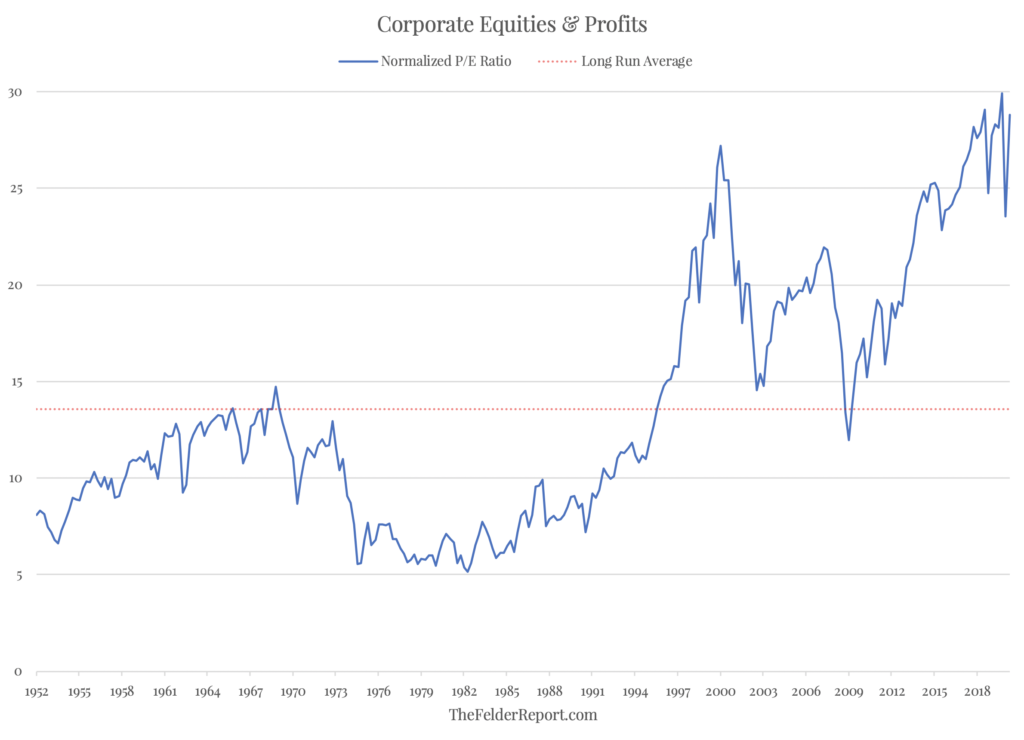

So if we normalize profit margins (hat tip, John Hussman), we can see that stock prices today are more expensive than they were 20 years ago at the peak of the Dotcom mania. It turns out that the current disconnect between stock prices and sustainable profits is, in fact, greater than anything we have seen in modern history.

The last time we saw prices and earnings disconnect in such an extreme way famously led to a “lost decade” for the stock market from 2000 to 2010. Is it unreasonable to think the current extreme in valuations could lead to another “lost decade,” especially if profit margins are only beginning to revert to their historical mean?

via ZeroHedge News https://ift.tt/2YA0GSb Tyler Durden

Hi-Crush To File For Bankruptcy: Shares Crash After Robinhooders Went All-In Tyler Durden

Fri, 06/26/2020 – 08:04

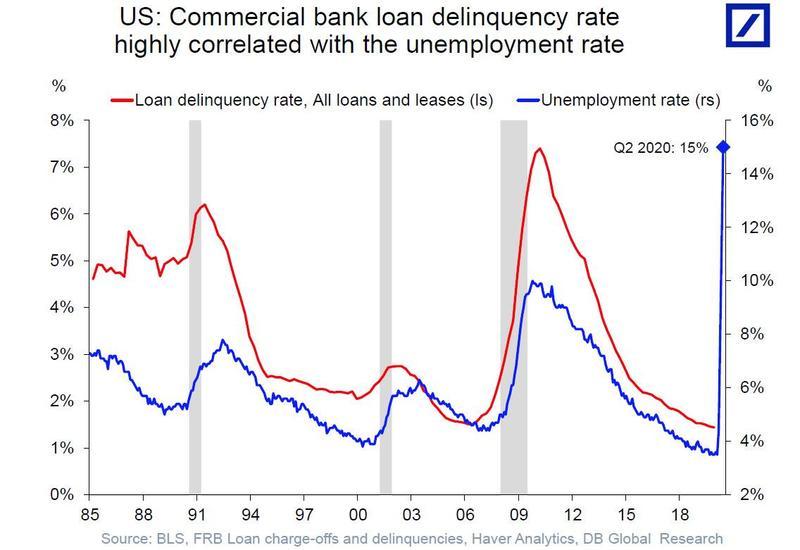

As we’ve been warning – a bankruptcy tsunami has only just begun – there’s a striking correlation between the unemployment rate and loan delinquencies.

So it comes at no surprise, yet another company, Hi-Crush (HCR), a fracker with shale plays in Texas, the Midwest, and interior Northeast, is working on the terms for a prearranged bankruptcy filing with lenders, reported Reuters.

HCR is expected to file for bankruptcy imminently regardless of the terms and conditions of a prearranged filing agreed upon with its debt holders. With already signed forbearance agreements, lenders will not exercise default-related rights on the company until July 5.

As oil prices corrected and went negative during the pandemic (read: US Shale Faces Bankruptcy Wave) – management had no other choice but to slash the workforce by 60% and idle three production units as demand for oil collapsed. HCR took a $145.7 million asset impairment charge on its production and terminal facilities in Q1, which resulted in a $1.46 per share loss.

Shares of HCR plunged 29% in pre-market Friday after the news of imminent bankruptcy.

Ahead of officially announcing insolvency – you’re never going to guess who was loading up on HCR shares. Well, Robinhood daytraders, of course…

Add HCR to the long list of bankrupted companies Robinhood daytraders have been panic buying. Just yesterday, we noted these inexperienced pajama traders loaded up on GNC Holdings as it filed for bankruptcy protection.

via ZeroHedge News https://ift.tt/2VoQKJs Tyler Durden

US Sees Record Jump In COVID-19 Infections For 2nd Day In A Row As Biden Claims He’d Make Mask-Wearing Mandatory: Live Updates Tyler Durden

Fri, 06/26/2020 – 07:48

As we reported last night, the US saw another record (or near record, depending on who you ask) jump in newly confirmed COVID-19 cases yesterday thanks to new records in Florida and Texas, and record (or near-record) numbers across much of the south and west.

According to the Washington Post, the final count for Thursday’s increase was 39,327 new infections reported by state health departments across the country. That number surpasses WaPo’s total set a day earlier (though some sources put the number of cases reported Wednesday as high as 45k). Texas alone reported a record 5,996 new cases (along with another record high for coronavirus hospitalizations) last night and, as WaPo points out, the Lone Star State’s rolling average has increased by 340% since Memorial Day.

With the US facing an unexpectedly large pickup in new cases, the median age of those infected has fallen sharply, down from 65 to around 35 today. This has been widely cited as one reason why deaths have continued to plateau, or even trend lower, amid all the insanity.

For the first time in nearly two months, the White House coronavirus task force will hold a news briefing on Friday to address the situation. But unlike previous briefings, VP Mike Pence will lead, and President Trump isn’t expected to make an appearance.

Last night, Joe Biden just took the “politicization” of mask-wearing up a notch by declaring that, if he were president, he would mandate mask-wearing in public, even though masks are only recommended to be worn in indoor locations (especially those with poor ventilation), or in outdoor areas where social distancing simply isn’t possible.

Coronavirus hospitalizations in New York dipped below 1,000 for the first time since March 18, Gov. Andrew M. Cuomo said Thursday. The WHO also said the virus could once again “push health systems to the brink” in Europe after 30 countries across the continent have seen cases rebound over the past 2 weeks.

As Australia learns the hard way that there’s nothing worse than declaring “victory” over the virus, only for it to come surging back a few weeks later, supermarkets around the country are being forced to impose limits on toilet paper purchases as Australians engage in another wave of “panic buying” amid fears that lockdowns might return (even though the number of cases reported over the last week is relatively minuscule). Victoria alone saw 30 new cases reported Friday, while a few other regions have reported one, or a handful, of new cases.

Seriously Melbourne? Is toilet paper stockpiling back? This is a Woolworths at Craigieburn Plaza right now (Wednesday morning). pic.twitter.com/Ogbifw89Nk

However, deaths in the US have continued to fall, with the 7-day average for the entire US hitting its lowest level since March.

The 7-day average of COVID-19 deaths is now 560.

But with this many cases piling up, it seems unlikely to keep falling for much longer. pic.twitter.com/9rhtuXcwPj

— The COVID Tracking Project (@COVID19Tracking) June 25, 2020

Of course, every pundit inevitably points out that this trend likely won’t last for too much longer even as there’s plenty of reason to believe that deaths this time around won’t be as severe since we’ve learned more about how best to protect the most vulnerable to serious illness – ie those in long-term care homes, who in several instances died by the dozens as the virus tore through institution after institution.

Taking a step back, all but one of the 15 states seeing the biggest accelerations in new cases and hospitalizations are situated in the south or the west. That state is Missouri, which, as the Atlantic correctly points out, is sometimes lumped in with the south.

Zooming back out, 15 states have now set their record for reported cases since June 19. All but one (Missouri) is in the South and West.

— The COVID Tracking Project (@COVID19Tracking) June 25, 2020

Yesterday marked another reported high in the outbreak according to the Atlantic’s stats from last night. Of course, the final numbers reported a day earlier ended up being over 45k for the day, according to some estimates. But according to the data, both Tuesday and Wednesday of this week saw record or near-record numbers of newly confirmed cases. Furthermore, while testing is rising across the country,

Even subtracting Wisconsin’s probables, today marked a new record high for reported cases in the outbreak at just over 39k. pic.twitter.com/oSl6FF9hKa

— The COVID Tracking Project (@COVID19Tracking) June 25, 2020

As Beijing unwinds more restrictions following its latest flare-up, Japan has just confirmed more than 100 new daily COVID-19 cases, the largest daily total since May 9, while in India, the biggest 24-hour spike in cases (17,296 new infections reported) pushed the country’s total case number close to half a million (490,401 in total) while deaths climbed by 407 bringing the death toll to 15,301. On the bright side, the country is seeing an improvement in the recovery rate for the most severe cases, with it climbing to 57.43%. Also, deaths per 100,000 stood at just 1.86, well below the global average of 6.24 per 100,000, per Al Jazeera.

via ZeroHedge News https://ift.tt/2VjHO8b Tyler Durden

Futures Jerk Around Inexplicably In “Abysmally” Illiquid Markets Tyler Durden

Fri, 06/26/2020 – 07:45

US index futures swung in an illiquid overnight session in which Bloomberg’s Richard Breslow said “volumes have been utterly abysmal”, concluding a volatile week for stocks, this time ignoring the resurgence in new virus infections across the country that sent them lower earlier in the week. European shares gained on low volumes, 10Y yields dropped by 1.5bps, while the dollar was unchanged.

And speaking of Breslow, he summarizes the overnight moves perfectly:

You know it’s going to be a tough day when the answer to the question of “why thus-and-so has done what it has, such as it has,” is simply, “because.” Ask for more color than that and you get a blank stare. Or, that the S&P 500 was up yesterday, so it’s sagging this morning.

So without trying to piece together a narrative, spoos are shrugging off concerns that a second wave of the pandemic could force policymakers to reverse plans to re-open. On Thursday, virus cases rose across the US by at least 39,818 the largest one-day increase of the pandemic. The governor of Texas temporarily stopped the state’s reopening on Thursday as infections and hospitalizations surged.

“Even though we continue to see some pretty scary virus numbers coming out of the U.S., it’s not really dented sentiment – not to any sustained degree at least,” said Timothy Graf, head of EMEA macro strategy at State Street.

Graf added that recent temporary downward corrections of market optimism have had very little follow-through. And at least on Friday, he was spot on: the MSCI world equity index was up 0.3%, extending gains from late on Thursday.

“There is a disconnect between what you feel should be the case looking at virus numbers and equities and riskier currencies holding up relatively well and volatility receding, but at the same time we’ve never seen a policy response like this, not in the last 80 years at least,” Graf explained. One wonders if that’s how residents of the USSR felt in the mid/late 1980s?

There was a trace of capitalism left when Nike reported extremely disappointing earnings late on Thursday: the company reported Q4 20 EPS of -0.51, far worse than the exp. 0.07, revenue of 6.3bln also missed exp. 7.32bln, while Gross Margin plunged to 37.3% (exp, 43.5%, prev. Y/Y 45.5%).

In Europe, shares opened higher, with the Stoxx 600 up 0.8% and London’s FTSE 100 up 1% in early trading. Air France-KLM climbed after securing a bailout from the Dutch government.

With China still closed, Asian markets traded mostly higher as the region took impetus from Wall Street after US regulators approved to relax Volcker rules, but with some advances in banking names retraced after-market following the Fed stress tests in which it capped dividend payments and banned share repurchases in Q3 for 34 of the largest banks. On Thursday, the Senate passed legislation that would impose mandatory sanctions on people or companies that back efforts by China to restrict Hong Kong’s autonomy, in another potential Sino-U.S. flashpoint. However, with China on holiday the news barely registered with either the Yuan or Chinese stocks.

The Bloomberg Dollar Spot Index held its ground and Treasuries were little changed amid quarter-end flows. The Treasury curve bull-flattened modestly with 10Y yield dropping, while the dollar traded mixed against G10 peers, with moves confined within narrow ranges; the yen led gains, supported by haven demand amid concerns over a second wave of coronavirus infections. The New Zealand dollar rose versus the greenback after the New Zealand Treasury Department documents showed RBNZ has limited scope to increase the size of its quantitative easing program under the existing indemnity with the government. The pound was steady and headed for its first weekly gain since early June following a week of choppy trading on variable risk sentiment. Demand for safe euro zone government debt was little changed, with Germany’s 10-year Bund yield close to monthly lows, at -0.479%.

Oil traded near $39 a barrel in New York as Russia slashed exports of its flagship crude Urals to the lowest in at least 10 years. Gold was near $1,765 an ounce, heading for a third weekly advance, the longest winning run since January. Copper was on track for a sixth weekly advance, with prices edging toward $6,000 a ton.

Economic data include personal income and spending, U. of Michigan sentiment survey

Market Snapshot

S&P 500 futures down 0.4% to 3,058.00

STOXX Europe 600 up 0.4% to 361.23

MXAP up 0.6% to 159.65

MXAPJ up 0.3% to 516.21

Nikkei up 1.1% to 22,512.08

Topix up 1% to 1,577.37

Hang Seng Index down 0.9% to 24,549.99

Shanghai Composite up 0.3% to 2,979.55

Sensex up 0.4% to 34,983.24

Australia S&P/ASX 200 up 1.5% to 5,904.08

Kospi up 1.1% to 2,134.65

German 10Y yield fell 0.5 bps to -0.473%

Euro up 0.09% to $1.1228

Brent Futures up 0.9% to $41.43/bbl

Italian 10Y yield rose 3.7 bps to 1.177%

Spanish 10Y yield fell 0.7 bps to 0.451%

Brent Futures up 1.4% to $41.64/bbl

Gold spot little changed at $1,763.36

U.S. Dollar Index down 0.1% to 97.33

Top Overnight News

ECB President Christine Lagarde said the recovery from the coronavirus pandemic will be “restrained” and will change parts of the economy permanently

The staggering pace of U.K. borrowing runs the risk of uprooting the market calm that has allowed pandemic relief efforts to run smoothly. Britain is likely to issue 410 billion pounds ($508 billion) of bonds for the fiscal year that runs through next March, almost 75% more than the previous record, according to the median estimate of a Bloomberg survey of primary dealers

Germany’s coronavirus infection rate fell to the lowest in three weeks, while the number of new cases remained well below the level at the height of the outbreak

Oil headed for just its second weekly decline since late April as a surge in coronavirus cases in the U.S. clouded the demand outlook, but the pessimism was tempered by signs Russia is determined to curb output

Asia-Pac markets traded mostly higher as the region took impetus from Wall St’s financial-led gains after US regulators approved to relax Volcker rules, but with some advances in banking names retraced after-market following the Fed stress tests in which it capped dividend payments and banned share repurchases in Q3 for 34 of the largest banks. ASX 200 (+1.5%) was underpinned as the top-weighted financials mirrored the outperformance of the sector stateside and amid positive reports for some of the ‘Big 4’ including Nippon Life considering an additional investment NAB’s wealth management business and Westpac winning a Federal Court decision against ASIC’s appeal regarding the responsible lending suit. Conversely, Qantas was at the other end of the spectrum in which its shares fell on a resumption of trade following its recent announcement for an equity raising, mass job cuts, 100-planes grounding and revoke of its interim dividend. Nikkei 225 (+1.1%) was lifted by the positive momentum and with gains spearheaded by financials which saw the index climb back above the 22500 level, while the Hang Seng (-0.9%) lagged on return from its holiday closure and played catch up to yesterday’s losses. Furthermore, the absence of participants in mainland China and mixed US-China headlines also clouded sentiment after the US Senate passed the bill punishing China for Hong Kong actions, although it was also reported the US was to consider an extension of China goods tariff exclusions. Finally, 10yr JGBs were indecisive as initial pressure from the mostly constructive risk tone, was counterbalanced by this week’s support near the 152.00 level and with the BoJ present in the market for JPY 660bln of JGBs with 1yr-5yr maturities.

Top Asian News

Alibaba Replaces CEO of Southeast Asian Arm Lazada

Tokyo Inflation Stays Near Zero Even After Emergency Ends

China-India Tensions Continue Despite Pledge to Disengage

Jakarta Subway Operator Mulls Bond Sale to Expand Network

European equities trade firmer (Eurostoxx 50 +1.4%), after a somewhat choppy start to the day which has seen them trade in negative territory before receiving more of a grinding bid ahead of the US’ entrance; with US futures flat/mixed but moving similarly higher. Stocks have been relatively resilient despite the mounting COVID-19 concerns stateside which has seen Florida and Texas pause their reopening efforts, with ICU’s in the latter state having reached maximum capacity. Furthermore, weakness in the banking sector (US banks were seen lower in after-hours trade) stemming from the latest Fed stress test results has failed to provide any sway on the broader tape thus far with financials in Europe currently the only sector in the red. As a reminder, the Fed capped dividend payments and banned share repurchases in Q3 for 34 of the largest banks. From a sectoral standpoint, positivity at the open was largely seen in the travel & leisure sector with Air France (opened higher by around 9.6%) leading the charge after the French and Dutch governments struck a EUR 3.4bln agreement to bail the Co. out. Furthermore, IAG (+2.2%) shares have also seen support after the Co.’s British Airways unit offered pay rises for some cabin crew members. However, as gains in European indices were trimmed, other travel & leisure names succumbed to the pressure and as such, the sector is trading broadly inline with its peers. Elsewhere, sectors are relatively mixed with price action in some areas lead by stock-specific developments. Notably, it has been another session of heavy losses for Wirecard (-48%) amid reports that Visa & Mastercard are considering withdrawing Wirecard’s ability to process payments on their network. Elsewhere to the downside, shares in Intu Properties (-54%) have been crushed this morning after the Co. noted that insufficient alignment has been achieved with creditors, as such and in order to protect stakeholder interests, they are now likely to involve the appointment of administrators. Finally, in the retail space, H&M shares are lower this morning after posting a SEK 6.48bln pretax losses in the three months through May and as such are laying the groundwork to issue fresh debt to help shore the Co.’s finances up.

Top European News

Lufthansa Faces Arduous Climb Out of Crisis After Bailout Sealed

Lessons From the Pandemic Add Urgency to ECB’s Focus on Climate

U.K. Mall Landlord Intu Likely to File For Administration

ECB’s Lagarde Warns of Complicated, Transformational Recovery

In FX, the broader Dollar and index remain within a tight range early-doors as the latter stays afloat above 97.000, albeit off best levels (97.482), having dipped from yesterday’s high 97.600 high and below the 97.500 mark. Looking ahead, today’s data docket sees US personal income, PCE & core PCE price index, Uni. of Michigan (F).

EUR – The European outperformer having had kicked off the final trading day of the week with a string of early-morning ECB speakers including Holzmann who downplayed the use of the deposit rate as an instrument, while president Lagarde remarked the economy is possibly past the COVID-19 trough, albeit this was accompanied with a second outbreak caveat. The president, alongside Governing Council member Rehn, also reaffirmed using instruments in a way which provides the most proportional response. However, Lagarde did express caution over a Recovery Fund deal reached at the mid-July summit – sentiment that has been expressed by some members of the Frugal Four. From a technical standpoint, EUR/USD’s 50 DMA has now risen above its 200 DMA, marking a golden cross which is typically perceived as a bullish signal. EUR/USD resides around 1.1225 having recovered from its earlier 1.1203 low, with a sizeable EUR 2.2bln of options expiring at the round figure at the NY cut.

NZD – Continued consolidation seen in the Kiwi from post-RBNZ lows of ~0.6400, with an added tailwind after the NZ treasury and central bank reached a funding agreement to ensure central bank has adequate resources to meet increasing responsibilities. NZD/USD sees itself just under 0.6450 having found an intraday base at 0.6415, albeit still a way off its 100 WMA and current weekly high at 0.6522 and 0.6532 respectively.

JPY, CHF – Currently the top gainers among G10s as the risk tone further sours despite an absence of fresh fundamental catalysts thus far heading into the weekend. USD/JPY dipped and remains below the psychological 107.00 (coincides with 10 DMA) and yesterday’s 106.97 low from a high of 107.24. USD/CHF lingers sub-0.9500 with a current base at 0.9471 ahead of yesterday’s 0.9469 low.

GBP – Sterling remains subdued in early-trade, potentially more-so on the back of the firmer EUR as EUR/GBP hovers around 0.9050 having found support at its 10 DMA at 0.9015. UK specific newsflow has remained light ahead of post-Brexit trade talks next week, with little by way of fireworks expected between the sides. Elsewhere, the UK alongside some European countries offered to limit the scope of proposed digital tax following the US threat which could offer some solace in bilateral post-Brexit relations with Washington. Cable dipped below 1.2400 having had earlier tested the level to the downside.

In commodities, choppy trade in the crude complex once again amid quietened trade heading into the end of the week, with little by way of fresh fundamental newsflow to influence price action. WTI and Brent Aug futures have regained a firmer footing after the latter briefly dipped into negative terriroty in price action that coincided with that in stocks. WTI meanders around USD 39/bbl, having had found a current base at 38.63/bbl, while its Brent counterpart trades on either side of USD 40.50/bbl having touched a low print of USD 41.05/bbl. Looking ahead, traders will be, as usual, eyeing macro newflow in regard to the COVID-19 case count alongside potential US-China or geopolitical developments, whilst data docket sees the weekly Baker Hughes rig count. Spot gold remains within a contained USD 8/oz range around 1765/oz. Copper mimics price action across the equity-space.

US Event Calendar

8:30am: Personal Income, est. -6.0%, prior 10.5%; Personal Spending, est. 9.2%, prior -13.6%

PCE Deflator MoM, est. 0.0%, prior -0.5%; PCE Core Deflator YoY, est. 0.9%, prior 1.0%

PCE Deflator YoY, est. 0.5%, prior 0.5%; PCE Core Deflator MoM, est. 0.0%, prior -0.4%

10am: U. of Mich. Sentiment, est. 79.2, prior 78.9; Current Conditions, est. 88, prior 87.8; Expectations, est. 74, prior 73.1

DB’s Jim Reid concludes the overnight wrap

Despite the latest virus stats making for more bleak reading, a late bounce into the close on Wall Street saw risk assets stage an impressive turnaround from the lows last night. We’ll get to that shortly but first to quickly recap the main headlines yesterday. In Texas the Governor halted the new phases of reopening the state’s economy as the number of cases rose by over 5000 for the fourth day in a row. It came as they also suspended elective surgery in the state’s biggest cities and headlines hit suggesting that Houston-area ICU wards were full. Meanwhile in Florida, case growth also continued to grow strongly, with a further 4.6% increase yesterday (vs. previous 7-day average of 4%). The recent outbreak in Florida has caused Apple to close an additional 14 stores in the state. This means the company has closed 32 stores in the past two weeks as cases have surged in the southern states. In total, the US added 39,596 new cases yesterday – a new daily high – and in percentage terms new cases grew by 1.7% which is the highest daily increase in 39 days.

That said, the news clearly wasn’t entirely negative, with the original epicentre of New York reporting that the number of virus hospitalisations was now below a thousand for the first time since March 18th. New York City is set to enter “phase 3” of reopening on July 6th, including in-door dining and personal-care services, as well as access to basketball and tennis courts, though capacity will continue to be limited.

However, the real catalyst for the late rally yesterday came in the last hour after the CEOs of Houston area hospitals tried to assure the public that the Texas Medical Centre had the required capacity to deal with the hospitalisations. When it was all said and done, the S&P 500 ended the session up +1.10%, a reversal of 1.97% from the lows. That does mask what was actually a fairly calm session for the most part. In fact after recovering from an early dip about half an hour into trading, the index traded in just a 26pt range for the majority of the session, until the surge at the close. That tight range was less than half the average daily range over the last month (54pts) for the S&P. The index was already recovering slightly before the headline, helped primarily by a strong performance for bank stocks (+3.57%) – the best industry performing industry group in the S&P yesterday.

The move higher in bank stocks came after the Fed, the Office of the Comptroller of the Currency, and the FDIC approved changes to the Volcker Rule. The rule changes will allow lenders to increase their business with certain funds, including venture capital funds. Regulators also amended a requirement that lenders had to hold margin when trading derivatives with their affiliates, and this reversal could free up an estimated $40 billion for US banks. However, regulators have added a new threshold, which limits the scale of margin that could be forgiven. This was followed by the stress test results after the NY close which included the Fed telling the major US banks that dividends would be capped at second quarter levels and buybacks would be not be allowed through at least Q3.

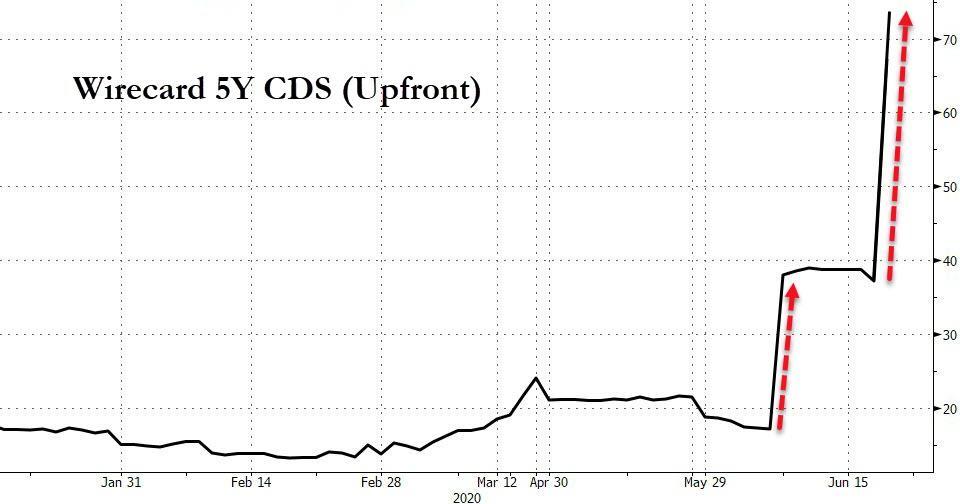

It was a similar story for the other US indices, with the NASDAQ (+1.09%) and the Dow Jones +1.18%) also seeing late surges. Europe was slightly weaker, with the STOXX 600 up +0.72% as bourses moved higher across the continent. Similar to the US, European Financial Services (+2.24%) and Banks (+1.58%) were among the best performing sectors. Wirecard was once again the worst performer on the STOXX 600, falling by a further -74.90% yesterday after the company filed for insolvency.

The momentum has continued in Asia this morning with the Nikkei (+1.12%), Kospi (+1.06%) and ASX (+0.91%) all up. The Hang Seng is trading down -0.55% having reopened following a holiday while Chinese markets remain closed. Futures on the S&P 500 are flat, as are bond markets. Elsewhere, WTI and Brent oil prices are up around 1% following news that Russia slashed exports of its flagship crude Urals to the lowest in at least 10 years.

In terms of overnight news, the US senate has approved a bipartisan measure that would penalize banks doing business with Chinese officials involved in the national security law that China is seeking to impose on Hong Kong. The bill would require the State Department to report to Congress every year about officials who seek to undermine the “one country, two systems” model that applies to Hong Kong. It gives the President the power to seize the assets of and block entry to the US for those individuals. A companion bill has already been introduced in the House of Representatives for its approval.

Back to yesterday, and markets didn’t appear to be too fussed by the latest weekly initial jobless claims numbers in the US, which for the 2nd week running came in worse than expected. Looking at the detail, there were 1.48m initial claims in the week through June 20th (vs. 1.32m expected), while the previous week’s reading was revised up by +32k. Although that’s now the 12th consecutive week of declining claims from the peak in late March, the last 2 weeks have seen the numbers fall by just -60k this week and -26k the week before, which is a big change from the previous 10 weeks where even the smallest decline was over -200k. The number of continuing claims for the week ending June 13th were somewhat better however, falling to 19.522m (vs. 20m expected), and the insured unemployment rate fell half a point to 13.4%.

Core sovereign bonds were slightly mixed amidst the abrupt turn in sentiment, with yields on 10yr Treasuries (+0.7bps) higher while bunds (-2.8bps) fell. UK gilts outperformed in particular, and yields on the country’s 2yr debt closed at a record low of -0.08%. 10yr gilts similarly closed at a record low of 0.15%, though this was still above their low of 0.075% on an intra-day basis back in March.

In other news, though it was some way down the headlines, the ECB released the minutes from their June meeting yesterday, when they announced an expansion of their Pandemic Emergency Purchase Programme (PEPP) by €600bn. Perhaps the most important aspect was the discussion on the proportionality of the PEPP, as well as the monetary stance more broadly. Bear in mind that one of the German Constitutional Court’s requirements in their ruling was for the ECB to decide on the proportionality of their asset purchase programme. In the minutes, a notable passage was that “there was broad agreement among members that while different weights might be attached to the benefits and side effects of asset purchases, the negative side effects had so far been clearly outweighed by the positive effects of asset purchases on the economy in the pursuit of price stability.”

Elsewhere, ahead of next week’s round of Brexit negotiations in Brussels, we got some interesting comments on Twitter from the UK’s chief negotiator, David Frost. The most notable was that he said “the Government will not agree to ideas like the one currently circulating giving the EU a new right to retaliate with tariffs if we chose to make laws suiting our interests. We could not leave ourselves open to such unforeseeable economic risk.” This is interesting since the possibility of the UK diverging from the level playing field in return for the EU having the right to respond with tariffs had been floated as a possible compromise recently. Following little progress in the negotiations so far, the plan is now for negotiations to take place every week over the next five weeks.

Finally, yesterday’s other data included the preliminary durable goods orders from the US for May. That saw a higher-than-expected increase of +15.8% (vs. +10.5% expected). Meanwhile the Kansas City Fed’s manufacturing index rose to 1 (vs. -1 expected).

To the day ahead now, and the data highlights include French consumer confidence for June, Euro Area M3 money supply for May, and Italian economic sentiment for June. Over in the US, there’ll also be personal income and personal spending for May, along with May’s PCE core deflator and the final University of Michigan sentiment indicator for June.

via ZeroHedge News https://ift.tt/3g4jL55 Tyler Durden

EU Launches Investigation Into German Regulator That Helped Cover Up Wirecard’s Historic Fraud Tyler Durden

Fri, 06/26/2020 – 06:53

It’s a saying seemingly as old as humanity itself: The bigger they are, the harder they fall.

Yesterday, Wirecard, an enterprise once valued at more than $20 billion on the public markets, filed for insolvency as its shares are now almost worthless while many who bought insurance against the company’s debt (an extremely cost-effective position thanks to its low theta) have earned returns as high as 300% or 400%, or, in some cases, even more.

For those who haven’t been closely following the Wirecard saga over the past 2 years (as the FT’s Dan McCrum and other members of the investigations team doggedly persevered in their coverage of what’s undoubtedly the biggest corporate accounting fraud in German post-war history), one of the most interesting aspects of the story is the role that Germany’s financial regulators played in fending off threats to the DAX 30 component, even at times openly citing “contagion risk” to fragile European markets as its motivation for protecting what turned out to be a gang of criminal profiteers.

And finally, it appears BaFin, the Munich-based regulator who caused the FT so much stress during the investigation, will soon receive its just desserts as Brussels calls for a probe into the German regulator.

According to the FT, Valdis Dombrovskis, the EU’s executive vice-president in charge of financial services policy, is writing to the bloc’s top markets supervisor asking it to assess BaFin’s handling of the Wirecard fiasco. Dombrovskis reportedly said the EU should be prepared to investigate the German regulator for “breach of union law” if the preliminary probe by the European Securities and Markets Authority (better known as ESMA) uncovers any rule-breaking. “We will be asking Esma to investigate whether there have been supervisory failures and if so to set out a possible course of action,” Dombrovskis told the FT. “We need to clarify what went wrong.” He will set a mid-July deadline for Esma to reply.

Brussels is worried that the company’s collapse, something more redolent of Chinese and Hong Kong markets, where ongoing frauds are routinely given a sheen of legitimacy, threatens investor trust in the EU, and could have lasting implications if it’s not dealt with swiftly. Regulators must show that they’re learning from these massive mistakes.

As the FT writes, the investigation is an “embarrassment” for Germany just as it’s assuming the rotating presidency of the bloc.

“This is certainly something that requires investigation,” Mr Dombrovskis said. “As we deepen capital markets and we move forward with the next stages of the Capital Markets Union, an important element is investors’ trust investing in publicly listed companies.” “Investors need to be sure that they are receiving proper and truthful information . . . and that provision of this financial information is properly supervised,” he said. Mr Dombrovskis’s call on Esma to intervene is an embarrassment for Germany only days before it assumes the rotating presidency of the EU. He told the FT that the question was whether BaFin fulfilled its obligations to enforce an EU law on listed companies’ financial statements, known as the transparency directive. The law hands clear responsibilities to national supervisors like BaFin to make sure companies fulfil their obligations. Esma, a pan-EU watchdog based in Paris, sets “common enforcement priorities” for national regulators each year.

[…]

“Given longstanding allegations about Wirecard’s financial accounting, we expect the German authorities including BaFin will now thoroughly investigate whether Wirecard accounts correspond to EU legislation,” Mr Dombrovskis said.

As BaFin prepares for its well-deserved comeuppance after effectively allowing itself to be pimped out by a (soon-to-be-former) DAX 30 (soon to be DAX 29) member, acting like a formidable attack dog fending off journalists and short-sellers alike, one of the most satisfying twists in the Wirecard saga was the vindication of dogged FT investigative journalist Dan McCrum. McCrum pursued Wirecard despite becoming the target of a BaFin investigation into stock manipulation which was, as we now know, based on suspicions that were 100% baseless. He faced down myriad threats, both real and perceived, over a period of a couple of years. The level of pushback was stunning, as McCrum explained. At times, he felt like he was being gaslighted. But in the end, the old journalists’ intuition that the harder the pushback, the bigger the truth, won out.

via ZeroHedge News https://ift.tt/2NxsrEF Tyler Durden