Total carloads for this week were 201,823 carloads, down 21.8% compared with the same week in 2019, while U.S. weekly intermodal volume was 255,455 containers and trailers, down 4.4% compared to 2019.

None of the 10 carload commodity groups posted an increase compared with the same week in 2019. Commodity groups that posted decreases compared with the same week in 2019 included commodities such as coal, down 26,340 carloads, to 52,392; metallic ores and metals, down 8,176 carloads, to 14,459; and nonmetallic minerals, down 6,839 carloads, to 29,478.

For the first 25 weeks of 2020, U.S. railroads reported cumulative volume of 5,306,511 carloads, down 15.7% from the same point last year; and 5,933,616 intermodal units, down 10.8% from last year. Total combined U.S. traffic for the first 25 weeks of 2020 was 11,240,127 carloads and intermodal units, a decrease of 13.2% compared to last year.

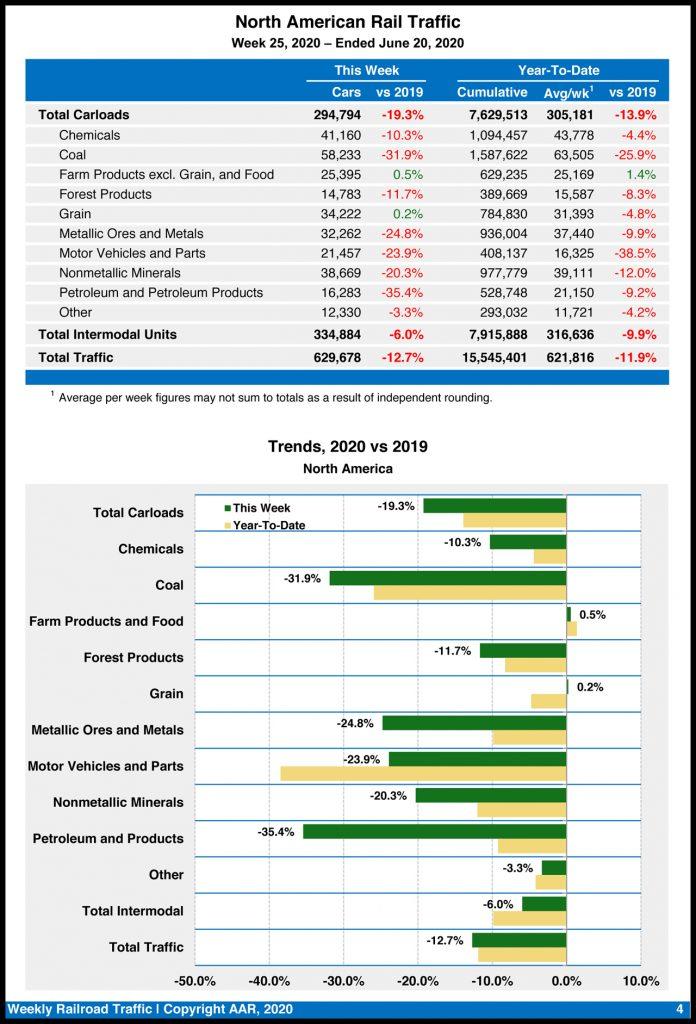

North American rail volume for the week ended June 20, 2020, on 12 reporting U.S., Canadian and Mexican railroads totaled 294,794 carloads, down 19.3% compared with the same week last year, and 334,884 intermodal units, down 6% compared with last year. Total combined weekly rail traffic in North America was 629,678 carloads and intermodal units, down 12.7%. North American rail volume for the first 25 weeks of 2020 was 15,545,401 carloads and intermodal units, down 11.9% compared with 2019.

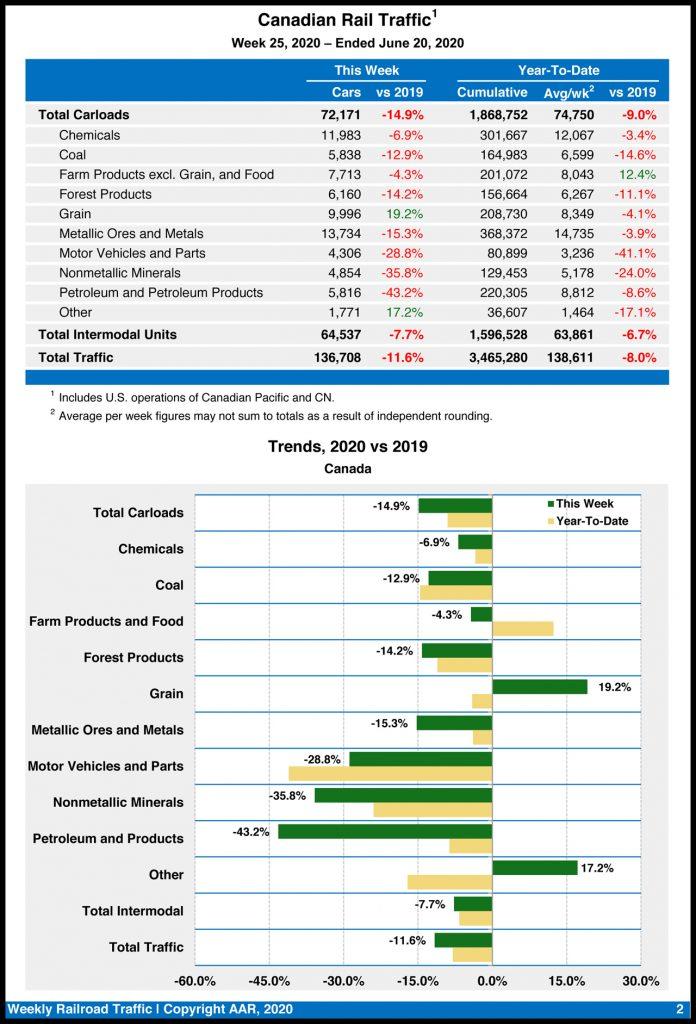

Canadian railroads reported 72,171 carloads for the week, down 14.9%, and 64,537 intermodal units, down 7.7% compared with the same week in 2019. For the first 25 weeks of 2020, Canadian railroads reported cumulative rail traffic volume of 3,465,280 carloads, containers and trailers, down 8%.

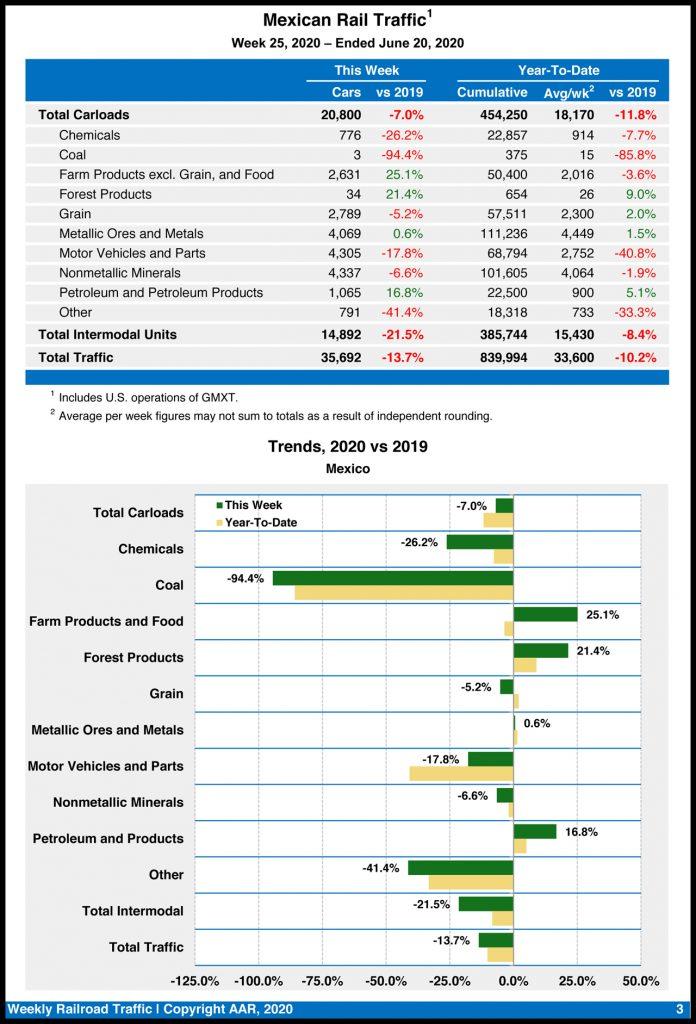

Mexican railroads reported 20,800 carloads for the week, down 7% compared with the same week last year, and 14,892 intermodal units, down 21.5%. Cumulative volume on Mexican railroads for the first 25 weeks of 2020 was 839,994 carloads and intermodal containers and trailers, down 10.2% from the same point last year.

via ZeroHedge News https://ift.tt/3ey54XC Tyler Durden

“Hard To Build Bullish Argument” – Corn Futures Pummeled On Prospects Of Bumper Crop Tyler Durden

Thu, 06/25/2020 – 21:30

Well, it’s that time of year when grain prices can have a quick reaction to weather forecasts and or trade data.

Chicago corn futures dipped 2% on Thursday morning after favorable crop weather in the Midwest supported the view of a big harvest this year. Disappointing weekly U.S. exports also weighed down prices.

“With a bumper 400 million tonnes of U.S. corn crop coming our way, it is hard to build a bullish argument for corn,” Ole Houe, director of advisory services at agriculture brokerage IKON Commodities in Sydney, told Reuters.

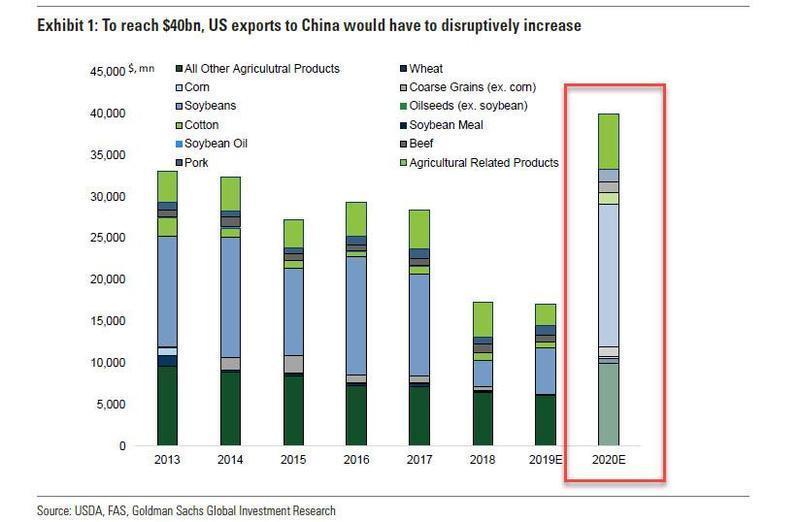

Uncertainty over Sino-US relations has led to concerns about weak Chinese purchases of U.S. farm goods, including corn and soybeans.

If readers recall, we used vessel tracking software to determine a “rush hour traffic” of bulk carriers carrying soybean were flowing from Latin America to Asia/China – while very little activity was seen in North Amerca.

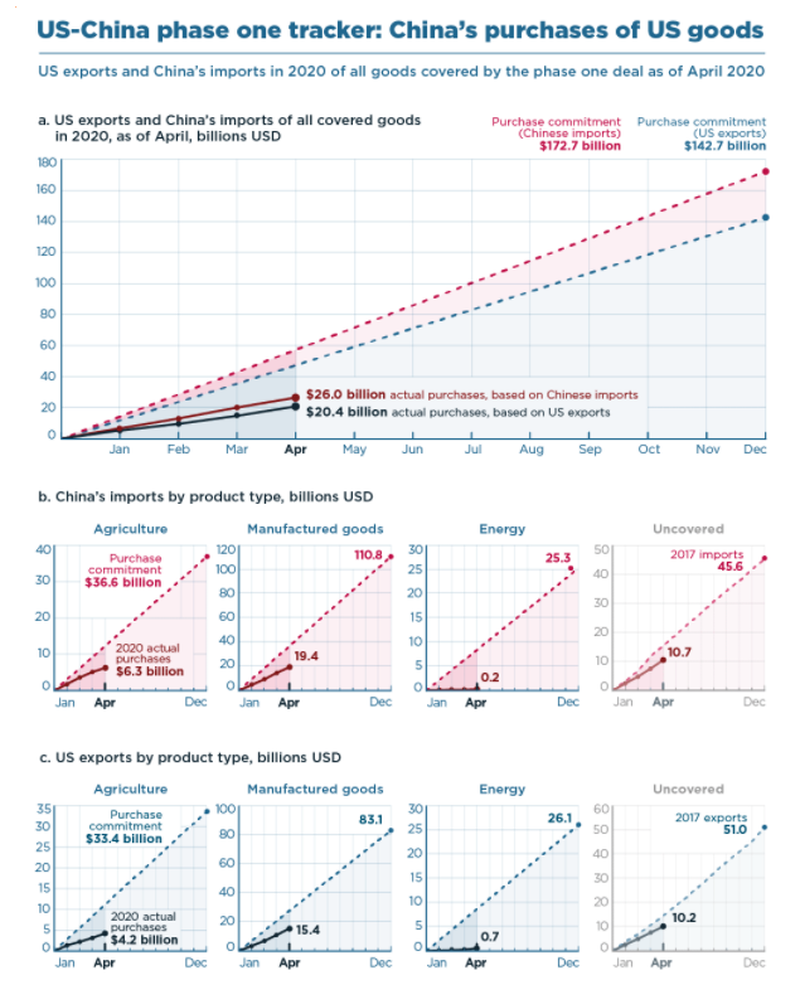

A US-China phase on tracker chart via the Peterson Institute for International Economics (PIIE) shows China’s monthly purchases of U.S. goods covered by the phase one deal is still way below commitments agreed upon in early 2020.

Iowa Soybean Association president Tim Bardole told NBC News that President Trump’s signing of the phase one trade deal had been a disappointment, and China’s commitments as per the trade deal will likely not be met.

“At this point, it hasn’t done near what we were hoping would happen with it,” Bardole said. “At this point, we’re kind of running out of time for it to get close to the numbers we might have hoped.”

Bardole had discussions with the House Ways and Means Committee last Wednesday, U.S. Trade Representative Robert Lighthizer told him that China is expected to satisfy trade deal purchase agreements – though as we’ve noted, from day one, the commitments were unrealistic targets.

via ZeroHedge News https://ift.tt/3fWk95x Tyler Durden

Modern monetary theory (MMT) has a new champion, and a new bible. Stephanie Kelton, economics professor at SUNY Stony Brook, is the author of The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy. Professor Kelton was an advisor to the Bernie Sanders presidential campaigns, and her ideas increasingly find purchase with left progressives.

It is certainly possible that she has a future either in a Biden administration or even on the Federal Reserve Board, which is a testament to how quickly our political and cultural landscape has shifted toward left progressivism. And left progressivism requires a “New Economics” to provide intellectual cover for what is essentially a political argument for painless free stuff from government.

Kelton’s essential argument, first advanced by MMT guru Warren Mosler in the 1990s, is quite simple: federal spending is unconstrained by revenue. Taxes function only to regulate demand and hence inflation; federal borrowing functions only to regulate interest rates. Sovereign government treasuries can create and spend as much money as they like to stimulate growth, especially when the economy is underperforming. If inflation spikes, taxes can be imposed to take money out of the economy.

Thus the only constraints on unlimited government spending are political. Unleashing ourselves from these “self-imposed” constraints, as Mosler puts it, is purely a matter of political will. Revenue is irrelevant to how you fund a government, so why not use government to fund the economy as a whole?

I direct readers to Dr. Bob Murphy’s recent substantive review of Kelton’s book here, as Bob does a thorough and effective job of debunking MMT and providing Austrian rebuttals to her claims regarding money, debt, and deficits. But I would make three quick points of my own:

MMT is not modern. Kings have used seigniorage and currency debasement for centuries to fund their endeavors, always at the expense of their subjects.

MMT is not monetary. It is primarily a fiscal approach to state finance, focused on tax policy as the economic accelerator and brake. Its roots predate the US Federal Reserve Bank, and in fact predate the present notion of “monetary policy.” MMT finds origins in early twentieth-century chartalism, whose proponents opposed gold in favor of paper money issued by government and mandated as legal tender. It is also a genealogical heir to the Greenbackers of the late 1800s, who believed Congress should direct the issuance of unbacked paper currency.

MMT is not a theory. It is accounting. In fact, it relies on an accounting subterfuge which bizarrely claims government deficits represent private (societal) surpluses. Because government is the font from which currency springs, all financial assets (denominated in that currency of issue) exist thanks to government! Thus, under “national accounting,” the more government spends, the richer we the people get. When tax revenue is $100 but government spends $120, Americans are richer by $20. And so on. This is not a theory; this is accounting gimmickry almost purposefully designed to obscure what’s really going on.

In the relentlessly circular world of MMT, government is the source of all finance and in effect all wealth. Taxpayers don’t fund government, because after all government first provides the “tokens” (currency) taxpayers need to pay their IRS bills! Government funds taxpayers, which is broadly speaking what the American left really believes. It’s a version of Obama’s “You didn’t build that” rewritten into policy.

But let’s not kid ourselves: the US federal government already finances its operations of MMT. Twenty twenty federal spending may exceed $8 trillion as Congress and the Trump administration blow the roof off the authorized $5 trillion budget with COVID relief bills. More than half of that amount, maybe as much as $4 trillion, will be “deficit financed”—a nice way of saying not financed by tax revenue. This is a first in American history, to put it mildly.

This $4 trillion will not simply issue forth from Treasury Department printing machines, as Kelton would prescribe, but the effect is the same: the Treasury issues debt to cover the shortage, which the “public” buys, implicitly understanding that the Fed will always provide a ready market for such debt. And where does the Fed get the money to buy Treasurys? It creates it from nothing, in Keltonite fashion.

Chicagoites, market monetarists, supply-siders, NDGP targeters, and other free market proponents frankly don’t have much to say about MMT. They already accept the premise of “monetary policy,” i.e., that government or central banks should issue and control money in society. They already accept treating the money supply and interest rates as forms of policy tools. They already accept deficits and taxes as methods to prime or slow the economy. So although they may object to how Ms. Kelton wants to use money politically, they can’t much object to whether money is used politically.

Kelton deserves credit for writing a book aimed at lay audiences instead of for her peers in academic economics. Unlike most of those peers, she seems genuinely interested in helping us understand how the world works. And unlike most left progressive academics, she also seems interested in helping average people improve their lot in life. Perhaps most importantly, she does not display the kind of contempt and anger toward Red State America we see from the Paul Krugmans and Noah Smiths.

It’s easy for those of a free market bent to dismiss MMT out of hand, but the impulse to create something from nothing resides deep in the human psyche, and politics is where this impulse finds expression. We should not underestimate the allure of MMT in the midst of our current upheavals, because it appears to make possible every left progressive program: unlimited public works and federal jobs, useless and uneconomic green energy schemes, reparations for black Americans, Medicare for All, free college, free housing, and a host of others. MMT is the perfect economic proposal for those who sincerely and deeply believe wealth simply exists in America, and will continue to exist, regardless of incentives. All we need to do is figure out how to more fairly divvy it up—and so why not through government spending?

The promise of something for nothing will never lose its luster. MMT should be viewed as a form of political propaganda rather than any kind of real economics or public policy. And like all propaganda, it must be fought with appeals to reality. MMT, where deficits don’t matter, is an unreal place.

via ZeroHedge News https://ift.tt/2Z7QijS Tyler Durden

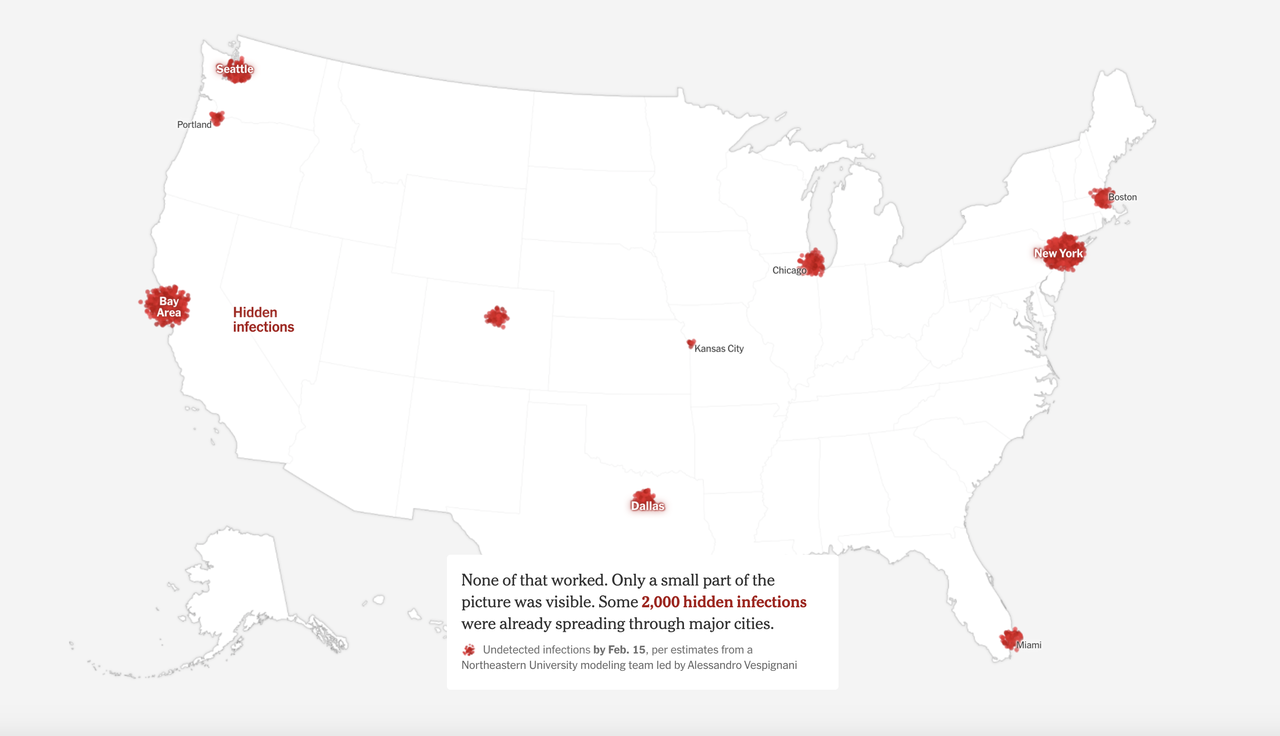

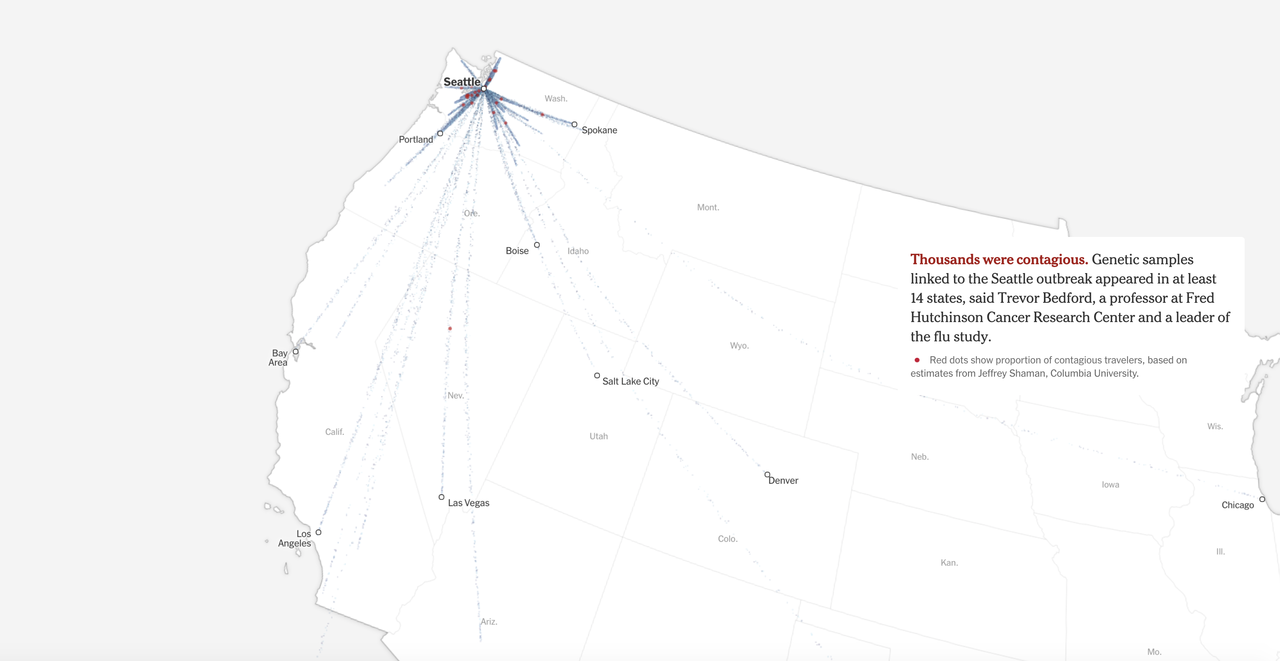

This Map Shows How The Coronavirus Spread Across The US Tyler Durden

Thu, 06/25/2020 – 20:50

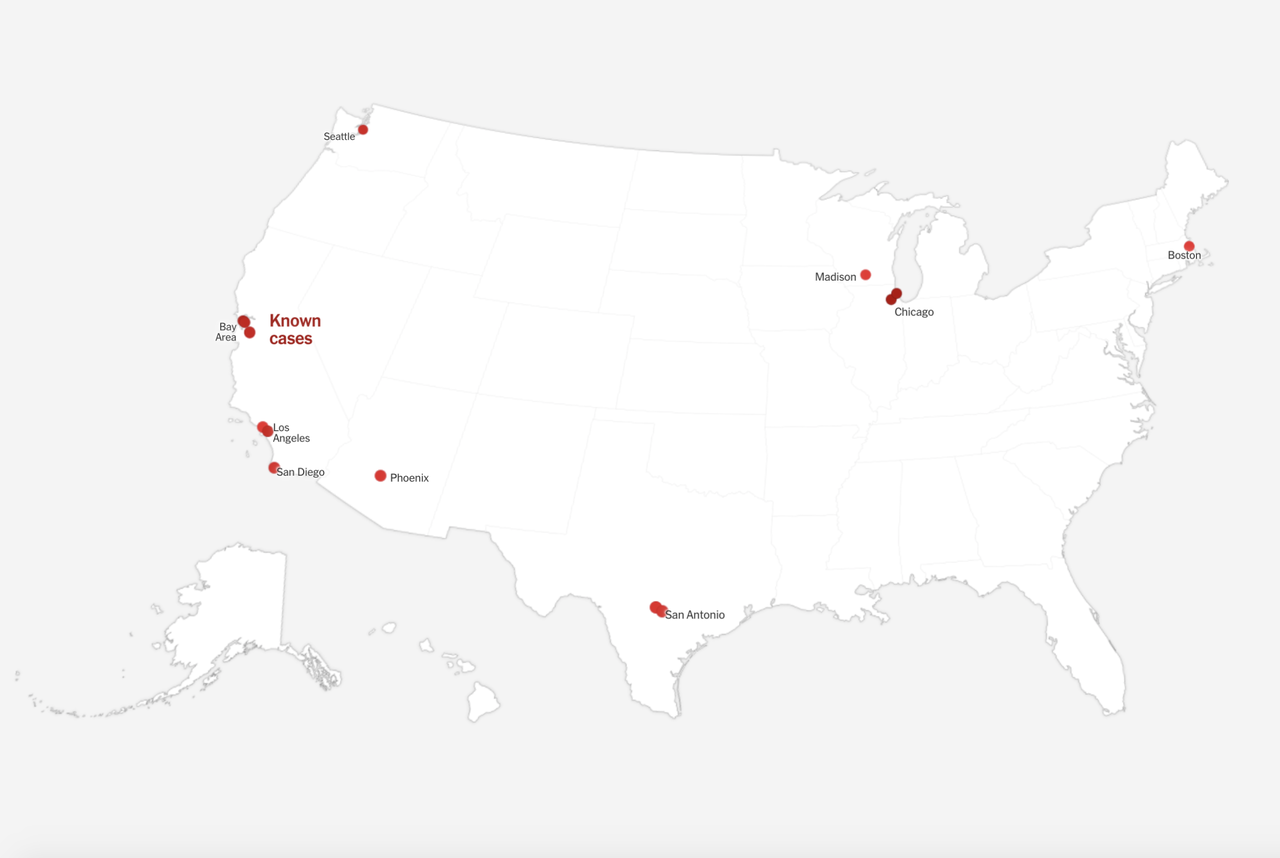

Working with a team of researchers, the New York Times has put together a comprehensive map of how the coronavirus spread from China and Europe to the US that, ironically, helps to undermine some of the paper’s own criticisms of President Trump’s decision to close the borders to travelers from China, while confirming that the initial delays in testing caused by faulty CDC tests and what has been described as “bureaucratic arrogance” greatly contributed to the spread.

Still, the picture painted of the American response to the virus isn’t pretty. Again and again, the states just didn’t act quickly enough to stop the virus from taking root in their communities. Outside the northeast and California, most moved far too slow. And even those states just named didn’t act swiftly enough.

The NYT’s narrative starts in early February, as the first known cases arrived in Seattle and Chicago.

By mid-February, there were only 15 known coronavirus cases in the United States, all with direct links to China. It was around then that President Trump triumphantly declared that the 15 cases would soon fall back to zero.

The problem is, by mid-February, there were already thousands of infections spreading across the country.

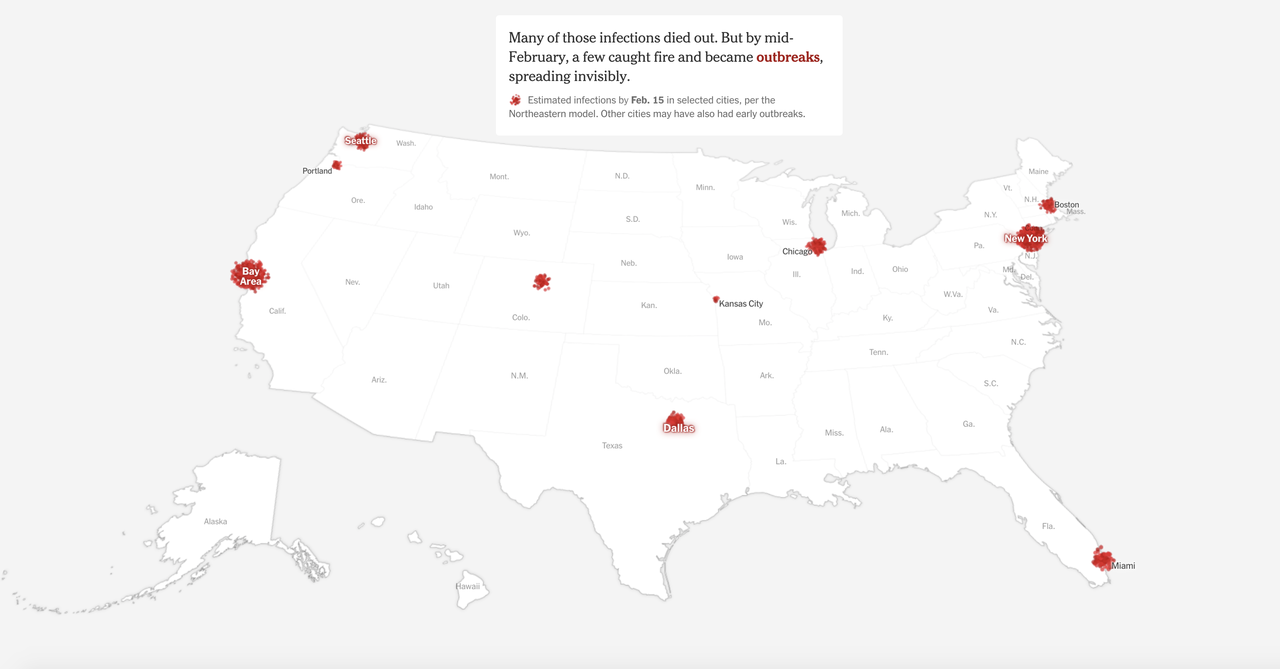

Unfortunately, by this point, the American response was weeks behind, per the NYT, as it would take 8 more weeks for testing capacity to start ramping up, and 10 in total after that until most states achieved widespread availability for tests. Still, NYT acknowledges that the China travel ban was a “partial” success. The problem is it wasn’t enough, and Trump should have listened to several advisers who were urging him to close travel to the EU. By the time Trump imposed the restrictions on China Feb. 2, only a few cases had made it to the US. but the decision to let the EU off the hook was a mistake.

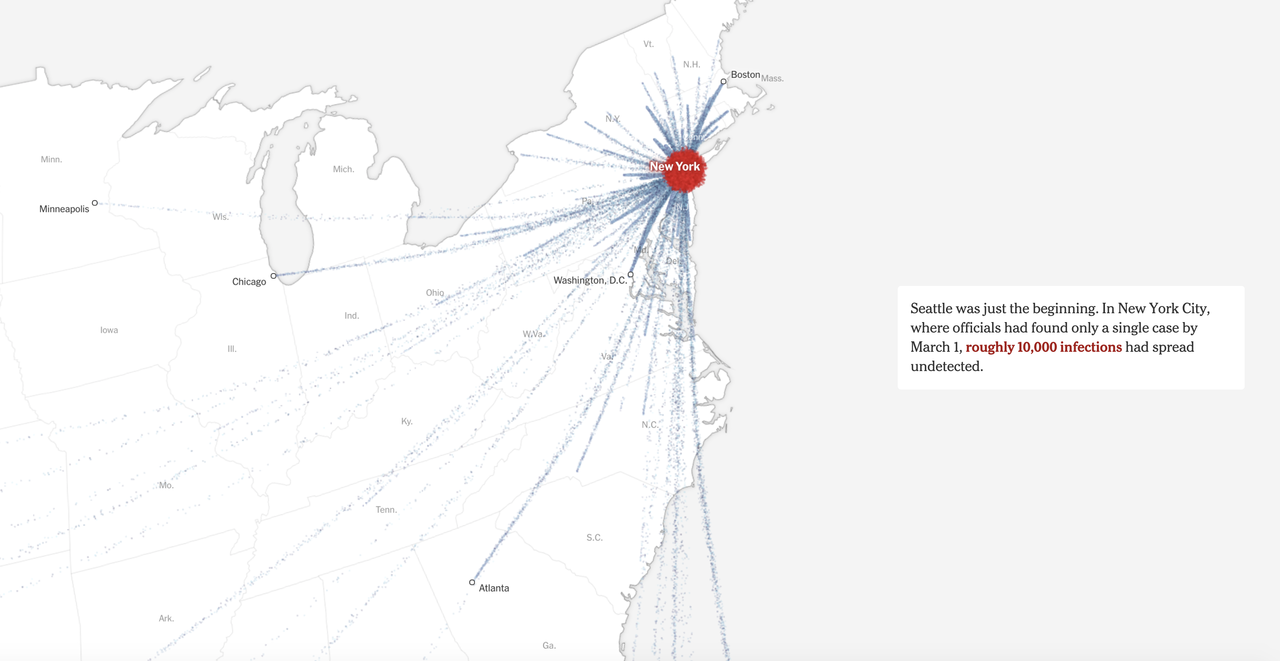

But by the end of February, the flow of infected travelers had turned into a wave, as more than 1,000 infected patients are believed to have arrived in the US by the end of February, each kicking off a mini-flareup of their own.

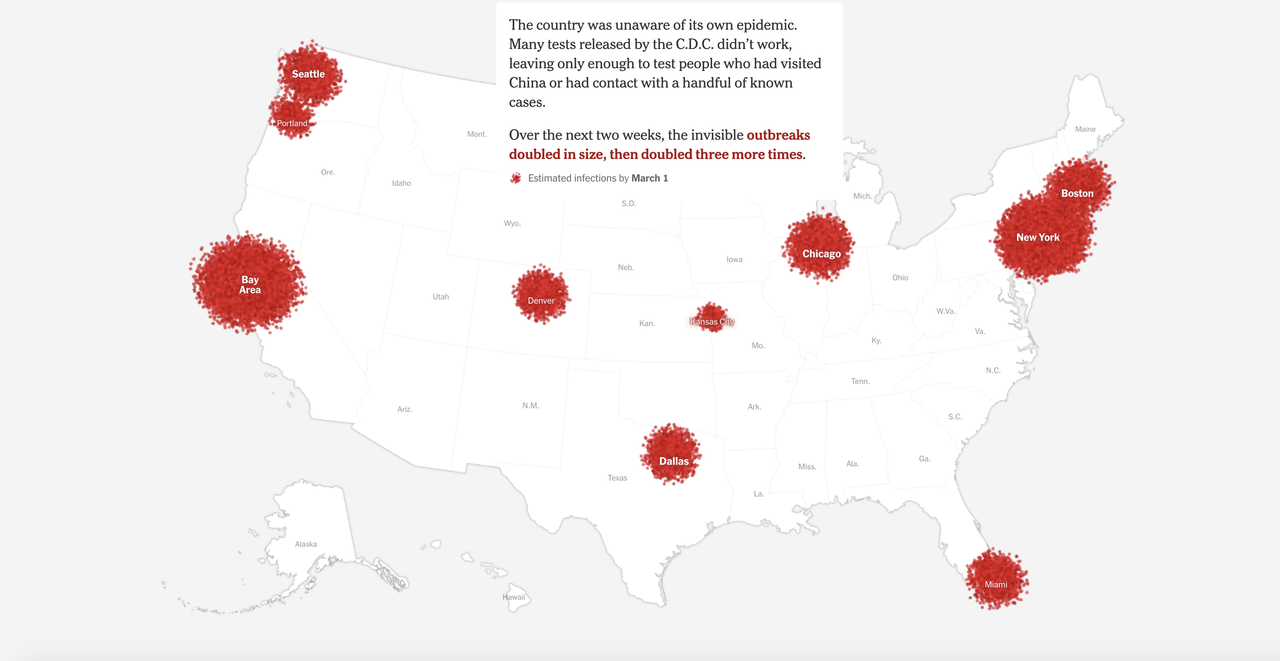

By March 1, the number of infections had doubled 4 times as the exponential rate of spread was in full swing.

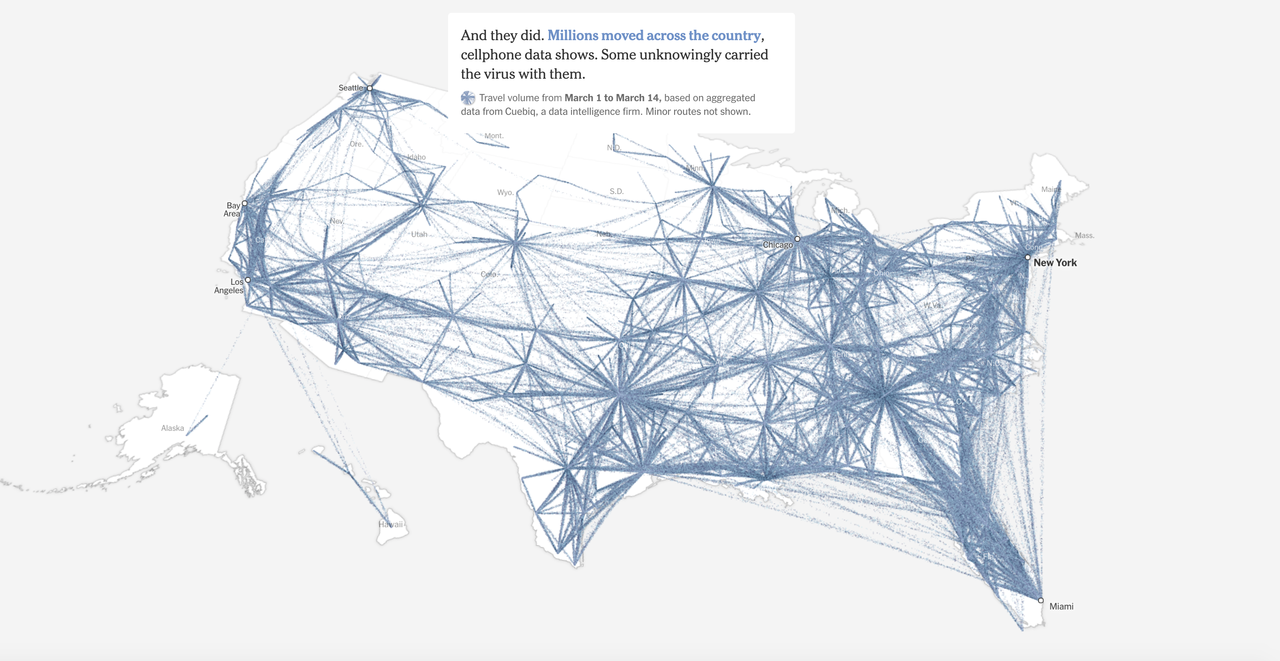

As President Trump pressed his administration not to be too ‘alarmist’ about the outbreak, he continued to encourage Americans to go about their lives, and they did, spreading the virus across the country as millions continued to travel.

The first sign that the outbreak was badly out of control, and that “community spread” was already well under way, arrived in late February when the first patient who hadn’t traveled to China was identified as infected om Seattle. Infections from this first community spread case in Seattle eventually spread to 14 states.

By March 1, when NYC Mayor Bill de Blasio was encouraging New Yorkers to “go about their lives as normal”, there were already more than 1,000 infected people roaming around the city.

Then more than 5,000 contagious travelers had left the city by mid-March, when the ‘stay at home’ orders in the Bay Area were first handed down, inspiring the lockdowns. Traveling New Yorkers spread the virus as far as New Orleans, where that city’s outbreak, which kicked off the outbreak in Louisiana more broadly, was later tied back to NYC.

Tracking so called “signature” mutations in genetic material of viral strains isolated in sick patients has allowed scientists to assemble a rough timeline, while providing more evidence to help them trace the spread of the virus around the country. By the time Trump blocked travel from the EU by mid-March, the restrictions were mostly useless; the virus was already widespread in the US as the Louisiana outbreak helped seed infections across the South.

A man returning from a basketball tournament in Tucson Ariz introduced the virus to the Navajo Reservation, the largest in the country.

Cellphone location data shows Americans didn’t start to curtail their movements until around March 10.

For more, the rest of the NYT’s project can be found here.

via ZeroHedge News https://ift.tt/3eAWPtQ Tyler Durden

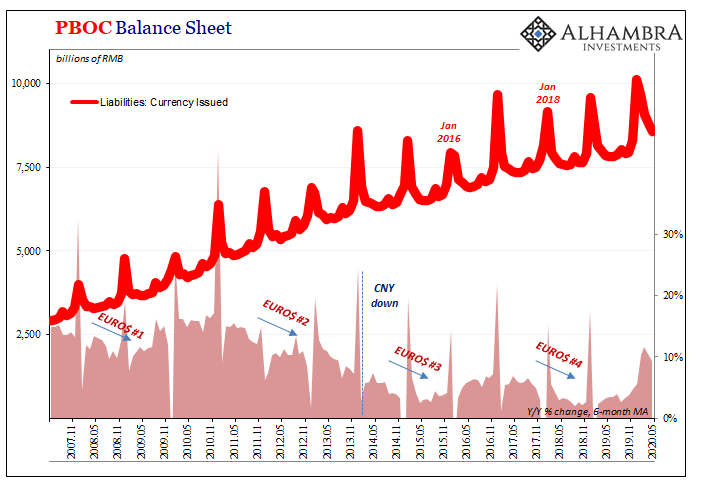

Where central banks are concerned, it’s not conspiracy theory so much as the term “off-balance sheet.” There’s a reason Enron kicked off that mass-migration into the footnotes. For monetary officials, there’s the choice to be like Montagu Norman and what he thought of good practice at central banks. Silence.

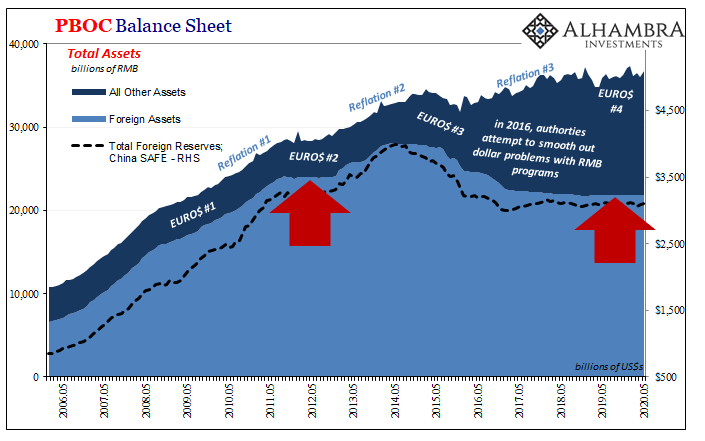

For years, the Chinese have tried it the other way. Big Mama typically left huge muddy footprints wherever its clumsy feet might land. It certainly was that way back in 2015 when Euro$ #3 was strangling CNY and thus confusing the hell out of everyone over here (and more than a few over there):

By far the most openly audacious intervention came starting in March 2015. China’s currency for reasons the mainstream just couldn’t fathom had been falling and unsteady for over a year. At the same time, the Chinese economy had shown equally unsteady signs, the accumulation of shocking weakness.

There was no way Communist authorities would allow it go any further. The PBOC intervened first in February 2015 with a “double shot”, rate and RRR cuts, followed in March by a CNY exchange rate that looked like it was purposely put under control. Many were relieved by what they saw as Big Mama very publicly and skillfully planting a green shoot at just the right time.

No dice; the whole thing blew up later that summer, making August 2015 memorable for all the wrong reasons (and people today still call falling currencies “stimulus”).

Here’s the thing, though. While that was taking place, you could tell the PBOC was involved because of its own balance sheet figures. Each month SAFE would first report lower levels of foreign “reserves” which then got confirmed by the PBOC’s balance sheet lines, a central bank system which begins and often ends at the number for forex.

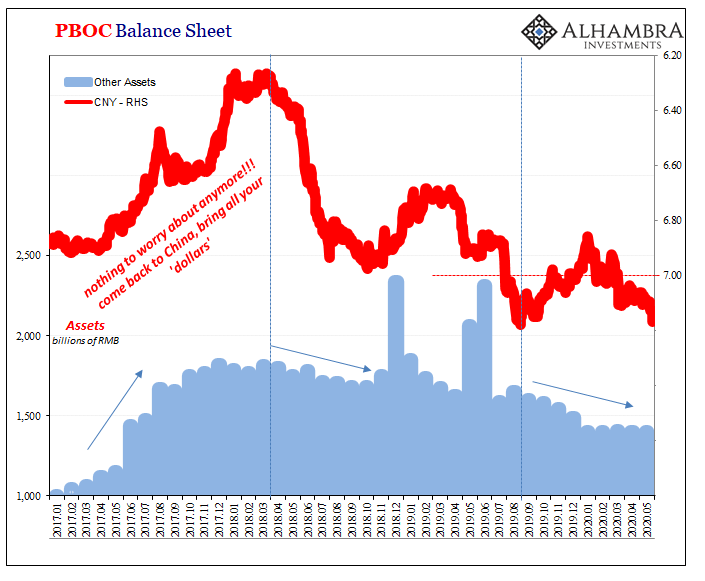

What’s going on now is a mockery – or an intentional shift in programming. Both SAFE and the PBOC report that foreign assets have been stable; in terms of the monetary base of the latter, suspiciously stable. I mean, hardly any variation month to month, a trend that’s gone on so long now it’s really year to year.

That can’t be an organic result, not in a dynamic world particularly the one we inhabit being ravaged by any number of potentially titanic forces that so often seem to get their start in this very country. What I’m saying is that there is almost certainly effort to the straight line (not the first time, either).

But what, exactly, is going on isn’t showing up anywhere. Not even on the one or two lines where in the past we could link them to hypothetical backdoor activities (the ubiquitous and useful “other”).

The ticking clocks became too noticeable and obvious? I think so; as did the decline in visible “reserves” which created the opposite effect of what was intended, amplifying negative monetary pressures market-wide (the nightmare scenario). The PBOC, unlike Western Economists, may just have found out that following the orthodox textbook where these things (the basics like money and dollars) are concerned will get your economy killed.

Reserves aren’t insurance against a dollar shortage, they are confirmation you’re the big target. Maybe better not to so blatantly advertise your dollar struggle?

Purposefully or not, a straight line isn’t expansion, either. And that still means the same thing in China: very little room for monetary growth. In what to me looks like more Xi vs. Li, currency growth has been bumped up for COVID-19 and the shutdown depression; bank reserves have not.

Quality growth in the real economy as opposed to quantity growth led by flooding banks.

Though it may be more difficult to see it as it unfolds because of the PBOC’s sideways baseline, what I wrote in the middle of 2015 might still apply today especially where CNY remains concerned:

Even the Chinese yuan has become far more stable despite the rash of nasty economic indications and even more uncertainty about what the PBOC might or might not do about it. In other words, forget what is happening in China, the yuan is all about the “dollar” in the purest financial sense.

Especially when there are, curiously, no more muddy footprints at all.

via ZeroHedge News https://ift.tt/2B42sCm Tyler Durden

“Big News!!” – LeBron James Raises $100 Million To Build Media Empire Tyler Durden

Thu, 06/25/2020 – 20:10

NBA star LeBron James and his business partner Maverick Carter have raised $100 million for their newly created entertainment firm, The SpringHill Company.

Bloomberg reported James and Carter received a cash infusion from global investment and financial services firm Guggenheim Partners LLC, UC Investments, News Corp. heir Elisabeth Murdoch, and SC.Holdings, the investment fund managed by entrepreneur Jason Stein.

The firm’s board consists of Carter, Serena Williams, Murdoch, Marc Rowan, co-founder of private equity firm Apollo Global Management, Live Nation Entertainment CEO Michael Rapino, Minerd, Paul Wachter, who is James’ wealth manager, and Tom Werner, chairman of the Boston Red Sox and English soccer club Liverpool.

The SpringHill Company is a consolidation of James’ marketing firm Robot Co. and several entertainment companies, including SpringHill Entertainment and Uninterrupted LLC. SpringHill Entertainment is the company behind the production of the upcoming sequel to “Space Jam.”

The company is described “as a media company with an unapologetic agenda: a maker and distributor of all kinds of content that will give a voice to creators and consumers who’ve been pandered to, ignored, or underserved,” Bloomberg noted.

“Big news Announcing the next chapter as THE SPRINGHILL COMPANY: a media company with an unapologetic agenda – a maker and distributor of all kinds of content that will give a voice to creators and consumers who’ve been pandered to, ignored, or underserved,” The SpringHill Company’s Instagram wrote.

Bloomberg didn’t elaborate on the deal structure or the sizes of each investors’ stake, but it was mentioned James and Carter formed the company at the start of the coronavirus pandemic in March.

“When we talk about storytelling, we want to be able to hit home, to hit a lot of homes where they feel like they can be a part of that story. And they feel like, Oh, you know what? I can relate to that. It’s very organic to our upbringing,” James told Bloomberg.

“When you grow up in a place like where we were, no matter how talented you are, if you don’t even know that other things exist, there’s no way for you to ever feel empowered because you’re like, I’m confined to this small world. That’s our duty. A lot of exposure,” Carter added.

The pair recently signed a TV production deal with Walt Disney Co and is working with Netflix on a basketball-themed movie.

via ZeroHedge News https://ift.tt/384q6KI Tyler Durden

Fear of COVID-19 absolutely crippled the U.S. economy during the first half of this year, and now it appears that there are some people that are pushing for that to happen again during the second half of 2020.

Earlier this evening, I came across a headline that boldly declared that there will be “180,000 U.S. deaths of COVID-19 by October”, and right now just about every mainstream news outlet is running stories about how the number of confirmed cases in the U.S. is surging. And it is definitely true that we are seeing an alarming rise in the number of confirmed cases. In fact, the number of new cases in the U.S. on Wednesday set a new record…

The U.S. broke its record for the highest coronavirus cases recorded in a single day, with 36,358 new positives reported on Wednesday, according to a tally by NBC News.

Wednesday’s cases top the previous highest day count from April 26 — the first peak of the pandemic in the U.S. — by 73 cases, according to NBC News tracking data. The World Health Organization saw its single-day record on Sunday with more 183,000 cases worldwide.

The mainstream media is treating this as some sort of a big shock, but of course the truth is that this shouldn’t be a surprise to anyone.

[ZH: we do note that while cases are surging, deaths are falling as the median age of positive infections falls dramatically and people recover]

For months, I have been telling my readers that the lockdowns would “flatten the curve” for a while and that the number of cases would start to spike again once the lockdowns ended. That is exactly what has happened, but anyone with even a little bit of common sense could have anticipated this.

Earlier this year, states in the northeastern portion of the nation were the epicenter for the outbreak in this country, but now it is states in the southern and western sections of the nation that have become the most prominent hotspots…

Arizona, California, Texas, Florida, Oklahoma and South Carolina reported record-high new daily coronavirus cases during this week, as case counts continue to rise in more than half of U.S. states.

Texas Governor Greg Abbott said the state is facing a massive outbreak with another 5,000 cases reported Wednesday. California Gov. Gavin Newsom reported Wednesday 7,149 tested positive, a record number for the nation’s largest state. Both states this week surpassed the entire European Union on the average number of daily cases.

Things are particularly bad in California. Over the past two days, we have seen a 69 percent increase in the number of newly confirmed cases…

The California Department of Public Health reported its second straight record jump in coronavirus cases on Wednesday as the state joins a handful of others with growing case numbers.

California reported an additional 7,149 Covid-19 cases since Tuesday, a 69% increase in two days, bringing the state’s total to 190,222 cases, according to the state’s health department. The previous highest day jump was reported on Tuesday when the state recorded 5,019 additional new cases.

Needless to say, the snowflake politicians in California are going to be even less eager to return to business as usual than they were before. And since the state of California accounts for more economic activity than any other U.S. state does, this is going to be a major drag on the U.S. economy as a whole.

If this pandemic keeps dragging on for a couple more years, what are states like California going to do? Many had anticipated that life would be getting back to normal by now, but instead we are starting to see things go in reverse. In fact, we just learned that the reopening of Disneyland has been postponed indefinitely…

Disney is delaying the phased reopening of Disneyland and Disney California Adventure, the company’s flagship theme parks in California, the company said on Wednesday.

The resort, located in Anaheim, California, was set to welcome back guests on July 17 after being closed for months because of the coronavirus pandemic.

On Friday, stocks slumped as second wave fears were reignited following a report that Apple would temporarily shutter 11 U.S. retail stores across Florida, Arizona, North Carolina and South Carolina.”Due to current COVID-19 conditions in some of the communities we serve, we are temporarily closing stores in these areas,” an Apple spokesman said in a statement.“We take this step with an abundance of caution as we closely monitor the situation and we look forward to having our teams and customers back as soon as possible.”

Fast forward to today, when with stocks already sliding on renewed virus of a second wave of virus infections, moments ago Apple reported that it would re-close another 7 stores in Houston and Texas due to the coronavirus spike.

According to the optimists, this wasn’t supposed to happen. The worst part of this pandemic was supposed to be over, and it was supposed to be all downhill from here.

But instead it has become exceedingly clear that this virus will be with us for a long time to come. New York, New Jersey and Connecticut have all announced that those traveling in from nine different states where COVID-19 is out of control will be forced into mandatory quarantine for 14 days, and police in New York will actually be actively searching for vehicles that have license plates from those particular states…

In New York, cops will stop cars with license plates from the affected states to ask the person why they are not quarantining and how long they have been in the state for.

The quarantine applies to any state with infection rate of 10 infections per 100,000 people on a seven day rolling average or 10 percent of the total population testing positive.

Speaking of New York, this pandemic has already had a much larger financial impact than most observers had anticipated.

In particular, New York City is facing a nine billion dollar reduction in tax revenue, and Mayor Bill de Blasio says that the city may be forced to let 22,000 workers go…

New York Mayor Bill de Blasio said the city is considering 22,000 layoffs and furloughs among its 326,000 employees to cut $1 billion of expenses after lockdown-related revenue losses.

De Blasio has projected a $9 billion loss in tax revenue over the next two years because of the pandemic.

Sadly, a whole lot more government workers will be fired across the country before this crisis is over.

Of course things are even worse for the private sector, and we continue to get more examples of this every single day. On Tuesday, we learned that GNC has decided to declare bankruptcy…

GNC Holdings Inc., which filed for Chapter 11 bankruptcy protection late Tuesday, has released an initial list of stores that will close.

The list posted at the Pittsburgh-based chain’s site, GNCevolution.com, includes 248 closing stores, including 219 U.S. locations and 29 in Canada.

The coronavirus pandemic could spell the end of Chuck E. Cheese. The popular kid’s restaurant had to close its 610 locations nationwide during the outbreak. Now, $1 billion in debt has Chuck E. Cheese’s parent company, CEC Entertainment, approaching bankruptcy.

The Wall Street Journal reports that CEC is asking lenders for a $200 million to keep its business going.

I haven’t been to a Chuck E. Cheese in many years, but when I was a kid I absolutely loved to eat there.

As a youngster, it seemed like such a magical place, and now it deeply saddens me to hear that the company may not survive.

In the end, a lot more iconic companies will go under as America plunges even deeper into this new economic depression.

Fear of a virus has turned our economy completely upside down, and thanks to the mainstream media much of the population is going to remain deathly afraid of this virus for the foreseeable future.

via ZeroHedge News https://ift.tt/3i4QcSw Tyler Durden

“One-Third Of NYC Hotels Could Go Bankrupt” Due To COVID-19, Riots, Starwood Owner Warns Tyler Durden

Thu, 06/25/2020 – 19:30

Seemingly every major real-estate broker in the tri-state area has appeared on CNBC over the past 3 weeks to talk about how their phone has been ringing off the hook with Brooklyn-based millennial couples looking to get the hell out of New York City.

Most are looking into the first-ring suburbs around the city, stretching as far as Connecticut’s Fairfield County (and even parts of southern Litchfield), while all of North Jersey is potentially accessible for office workers who will likely never return to the daily commute. Meanwhile, brokers in NYC, who enjoyed a decade-long post-crisis, are assuring their TV audience that the city’s real estate market will always bounce back, just like it did after 9/11.

Not everyone is so optimistic, especially when it comes to New York City. Even before the pandemic, the city was struggling with a crumbling subway, surging homelessness. Taxes have been raised, while city services have deteriorated. And as the NYPD pulls hundreds of undercover officers off the street, virtually guaranteeing that the open air drug markets of the 1970s, 1980s and 1990s will make a comeback, along with myriad other quality of life problems, some of the city’s most successful real estate investors think young people are probably better off staying in the suburbs, or moving to some other smaller, better-run city.

During a wide-ranging Bloomberg interview, Barry Sternlicht, the billionaire founder of Starwood Capital Group, shared a vision for NYC that sounded like the beginning of a disaster movie: office buildings in the city will lose 40% of their value – putting unprecedented pressure on the family businesses of the president and his son-in-law, Jared Kushner – one-third of all hotels in the city will go bankrupt, and – most importantly – residential rents will plummet as the wave of gentrification that priced out many minorities from the neighborhoods in which they grew up happens in reverse.

While the looting and the violence witnessed during the protests over George Floyd’s murder didn’t help, the protests and the virus aren’t the City’s only problem. In fact, some of the forces driving this trend have nothing to do with the virus, Sternlicht said. Instead, he blamed a “blue-state mentality” that has brought the city to its present “tipping point”.

Democrats see upping taxation as the best way to close state budget gaps. When taxes on the wealthiest rise substantially, many of those people leave, creating even bigger holes in the state’s revenue stream. Sternlicht isn’t the only NYC financier to relocate to Miami in recent years.

As the tax base shrinks, services deteriorate, and taxes rise on those who are increasingly unable, or unwilling, to pay them. People leave, setting off a vicious cycle.

“If they raise taxes, more people leave and the social burden of those that are less fortunate falls on an ever-smaller revenue base,” he said. “The services of the city get worse, the city gets dirtier, the police show up less often. It’s a negative cycle.”

So long as there’s no COVID-19 vaccine and the virus continues to spread, big city tourism, sports and conventions – a major source of revenue for city businesses and tax revenue for city and state government – will remain largely on hold. While Sternlicht’s Starwood, which has some $60 billion in assets, can withstand the hit to its 1 Hotel locations near Central Park and on the Brooklyn waterfront, as well as to its Baccarat Hotel New York in midtown Manhattan, others won’t be so lucky. In the end, one-third of hotels will go bankrupt.

“I think a quarter, a third of hotels in New York City could go bankrupt,” Sternlicht said. “It’s going to be ugly. You tell me when big businesses are going to force their clients or customers or employees to go to a group meeting in Vegas or in New Orleans or in Orlando.”

Outside NYC, Sternlicht says, his company’s properties are faring much better. Hotel bookings in markets like Miami are still happening. But NYC’s top retail corridors – like Fifth Avenue and SoHo – will be hard pressed to convince shoppers to return, as more Americans have come to rely on Amazon. This could take a sledgehammer to retail rents in the city, which started showing weakness as far back as 2018.

As fewer young people are willing to move to the city, big tech companies that signed huge leases in Manhattan or Brooklyn office buildings will simply walk away.

WeWork, still the city’s biggest corporate landlord, is on track to substantially shrink its footprint, if the company doesn’t collapse outright. Tech firms like Facebook and Google are planning to allow far more workers to work remotely. Even on Wall Street, banking executives are talking about needing less overall space. With all of this factors hitting at once, NYC is bound to become the toughest commercial real estate market in the country.

All told, the result may be the city’s biggest real estate slump in at least three decades. According to Cushman & Wakefield data going back to 1990, Manhattan rents haven’t fallen by more than 20% in a single year. “Rents could drop 25% in New York – office rents. I think expenses could go up 25%. You could see office values drop 40% because of that,” Sternlicht said. “It’s probably going to be the toughest office market in the country.” Read more: Gorman sees Morgan Stanley future with ‘much less real estate’ And if jobs move elsewhere, the residential market will collapse too. landlords are “desperate” to retain young tenants and increasingly willing to cut apartment rents by as much as 25%, Sternlicht said.

In summary, Sternlicht’s “negative cycle” theory is pretty simple: first, the income base erodes. That puts strain on city services and infrastructure, that causes quality of life to deteriorate while cost of living rises, prompting more wealthier residents to leave.

Put another way: New York City’s drain is the sunbelt’s gain (that is, if the coronavirus outbreak doesn’t swallow up the entire region).

Starwood Capital has been investing in so-called red states with Republican governors, such as Florida, Texas and Tennessee, Sternlicht said, because they have growing populations, companies are relocating there and the non-union construction costs are much lower than in blue states run by Democrats. “I don’t think you can make New York miserable for the affluent and expect it to be successful for everyone,” Sternlicht said. “There are other incredible places in the country – or they will be incredible when all the New Yorkers populate them.”

Of course, Sternlicht’s businesses are feeling substantial strain from the coronavirus pandemic. While he insists Starwood’s hotels business will make it through relatively unscathed, its malls business is defaulting on its debts.

via ZeroHedge News https://ift.tt/2VhWPHo Tyler Durden

A few moments ago, I blogged about Department of Homeland Security v. Thuraissigiam. This case turned on the scope of the Suspension Clause. Justice Alito wrote the majority opinion. Justice Sotomayor wrote the dissent. They disagree, vigorously, about the proper role history should play when interpreting the Suspension Clause.

The majority required the Thuraissigiam to identify a specific case that supports his claim for relief. A close analogy is not enough.

Despite pages of rhetoric, the dissent is unable to cite a single pre-1789 habeas case in which a court ordered relief that was anything like what respondent seeks here. The dissent instead contends that “the Suspension Clause inquiry does not require a close (much less precise) factual match with historical habeas precedent,” and then discusses cases that are not even close to this one.

In dissent, Justice Sotomayor writes that Boumediene does not require such a close historical fit:

But as the Court implicitly acknowledges, its inquiry is impossible. The inquiry also runs headlong into precedent, which has never demanded the kind of precise factual match with pre-1789 case law that today’s Court demands.

For sure, Justice Kennedy’s framework in Boumediene was far more fluid. Justice Sotomayor writes:

But this Court has never rigidly demanded a one-to-one match between a habeas petition and a common-law habeas analog. Boumediene is even clearer that the Suspension Clause inquiry does not require a close (much less precise) factual match with historical habeas precedent. There, the Court concluded that the writ applied to noncitizen detainees held in Guantanamo, despite frankly admitting that a “[d]iligent search by all parties reveal[ed] no certain conclusions” about the relevant scope of the common-law writ in 1789.… But crucially, the Court declined to “infer too much, one way or the other, from the lack of historical evidence on point.” Instead, it sought to find comparable common-law habeas cases by “analogy.”

I understand Justice Sotomayor’s frustration. I don’t think this decision is consistent with Boumediene. But Boumediene is no longer a viable precedent. Justice Kennedy is gone, and Chief Justice Roberts sees no institutional need to retain it. It will be whittled away.

Justice Sotomayor describes the majority’s test as an exercise in futility. Immigration law is largely a novel invention. It would be impossible to find any relevant caselaw:

To start, the Court recognizes the pitfalls of relying on pre-1789 cases to establish principles relevant to immigration and asylum…. The Court nevertheless seems to require respondent to engage in an exercise in futility. It demands that respondent unearth cases predating comprehensive federal immigration regulation showing that noncitizens obtained release from federal custody onto national soil. But no federal statutes at that time spoke to the permissibility of their entry in the first instance; the United States lacked a comprehensive asylum regime until the latter half of the 20th century. Despite the limitations inherent in this exercise, the Court appears to insist on a wealth of cases mirroring the precise relief requested at a granular level; nothing short of that, in the Court’s view, would demonstrate that a noncitizen in respondent’s position is entitled to the writ. See also Neuman, Habeas Corpus, Executive Detention, and the Removal of Aliens (1998) (noting the inherent difficulties of a strict originalist approach in the habeas context because of, among other things, the dearth of reasoned habeas decisions at the founding).

In response, Justice Alito faults Justice Sotomayor for scoffing at originalism:

The dissent reveals the true nature of its argument by suggesting that there are “inherent difficulties [in] a strict originalist approach in the habeas context because of, among other things, the dearth of reasoned habeas decisions at the founding.” But respondent does not ask us to hold that the Suspension Clause guarantees the writ as it might have evolved since the adoption of the Constitution. On the contrary, as noted at the outset of this discussion, he rests his argument on “the writ as it existed in 1789.”

Justice Alito also rejects a “living” model of the Suspension Clause, which Justice Breyer advocated for in his concurrence:

What the dissent merely implies, one concurring opinion states expressly, arguing that the scope of the writ guaranteed by the Suspension Clause “may change ‘depending upon the circumstances’ ” and thus may allow certain aliens to seek relief other than release. Post (BREYER, J., concurring in judgment) (quoting Boumediene). But that is not respondent’s argument, and as a general rule “we rely on the parties to frame the issues for decision and assign to courts the role of neutral arbiter of matters the parties present.” United States v. Sineneng-Smith (2020).

Justice Sotomayor has produced another impressive historical dissent, akin to her Promesa dissent.

I was surprised Justice Kagan joined Justice Sotomayor’s dissent. Here, Kagan is throwing down a gauntlet against originalism. I would think the savvier move would be for her to join Breyer’s more moderate dissent.

from Latest – Reason.com https://ift.tt/2Ywd5qh

via IFTTT

Today the Supreme Court decided Department of Homeland Security v. Thuraissigiam. I have now had a chance to read the entire 98-page decision. We have edited the case down to 19 pages for the Barnett/Blackman supplement. Please e-mail me if you’d like a copy: josh-at-josh-blackman-dot-com.

Between 2004 and 2008, the Supreme Court decided several cases involving Guantanamo Bay detainees. Since Boumediene v. Bush (2008), the Supreme Court has largely ignored Guantanamo Bay. Thuraissigiam is the first major decision to discuss the Suspension Clause in nearly a decade. I’m on the fence whether it warrants a place in our constitutional law casebook.

On the plus side, the composition of the Court has changed significantly since Boumediene was decided. Critically, Justice Kennedy was replaced by Justice Kavanaugh. The majority reads Boumediene quite narrowly. In dissent, Justice Sotomayor accuses Justice Alito of ignoring that 5-4 decision. She’s probably right. Thuraissigiam provides a current, and accurate statement of the Court’s suspension clause jurisprudence.

Also, this case is far more relevant to attorneys today. Few lawyers will ever work on detainee rights. But many law students will work on immigration law. This case is significant. Moreover, the Due Process Clause analysis will likely prove more important than the Suspension Clause analysis. We may soon see the Trump Administration release the long-awaited expedited removal policy. I first blogged about it in February 2017, and tweeted about it in July 2019.

On the negative side, it isn’t clear how “canonical” this case will be. The doctrine may be limited to the unique contexts of aliens who crossed the border, and were immediately apprehended. Justice Sotomayor points out how the Ninth Circuit will likely interpret the case:

Perhaps recognizing the tension between its opinion today and those cases, the Court cabins its holding to individuals who are “in respondent’s position.” Presumably the rule applies to—and only to—individuals found within 25 feet of the border who have entered within the past 24 hours of their apprehension. Where its logic must stop, however, is hard to say.

26 feet + 25 hours= Due Process.

But it is a good case to study. I’ll write some more about it.

from Latest – Reason.com https://ift.tt/37Zn8Y8

via IFTTT

Announcing the next chapter as THE SPRINGHILL COMPANY: a media company with an unapologetic agenda – a maker and distributor of all kinds of content that will give a voice to creators and consumers who’ve been pandered to, ignored, or underserved,” The SpringHill Company’s Instagram wrote.

Announcing the next chapter as THE SPRINGHILL COMPANY: a media company with an unapologetic agenda – a maker and distributor of all kinds of content that will give a voice to creators and consumers who’ve been pandered to, ignored, or underserved,” The SpringHill Company’s Instagram wrote.