America’s Jobless Claims Data Refuse To Confirm V-Shaped Recovery Narrative Tyler Durden

Thu, 06/25/2020 – 08:46

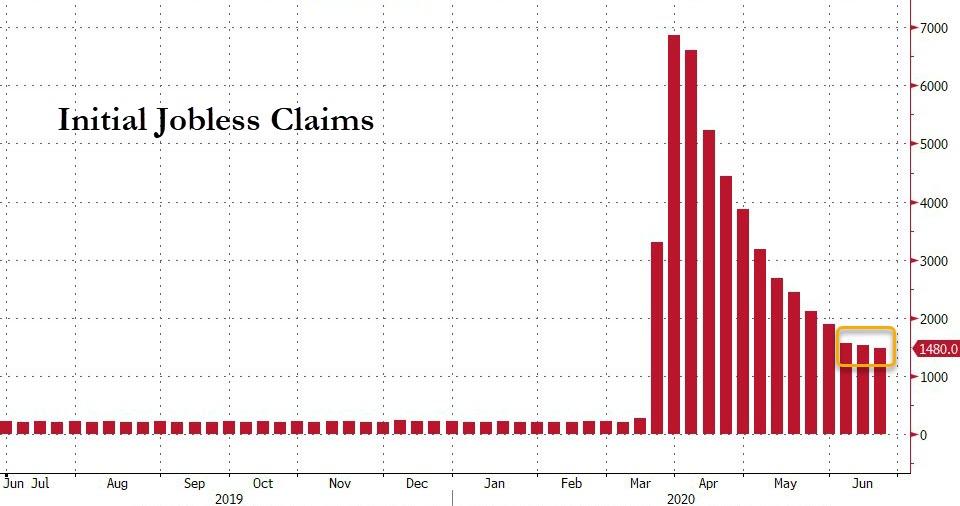

As fears of a second wave of COVID (and the concommitant risk of re-lockdowns for America) soar, the last week saw 1.48 million more Americans filed for unemployment benefits for the first time (notably worse than the 1.32 mm expected).

Source: Bloomberg

That brings the fourteen-week total to 47.25 million, dramatically more than at any period in American history. However, as the chart above shows, the second derivative has turned the corner (even though the 1.48 million rise this last week is still higher than any other week in history outside of the pandemic)

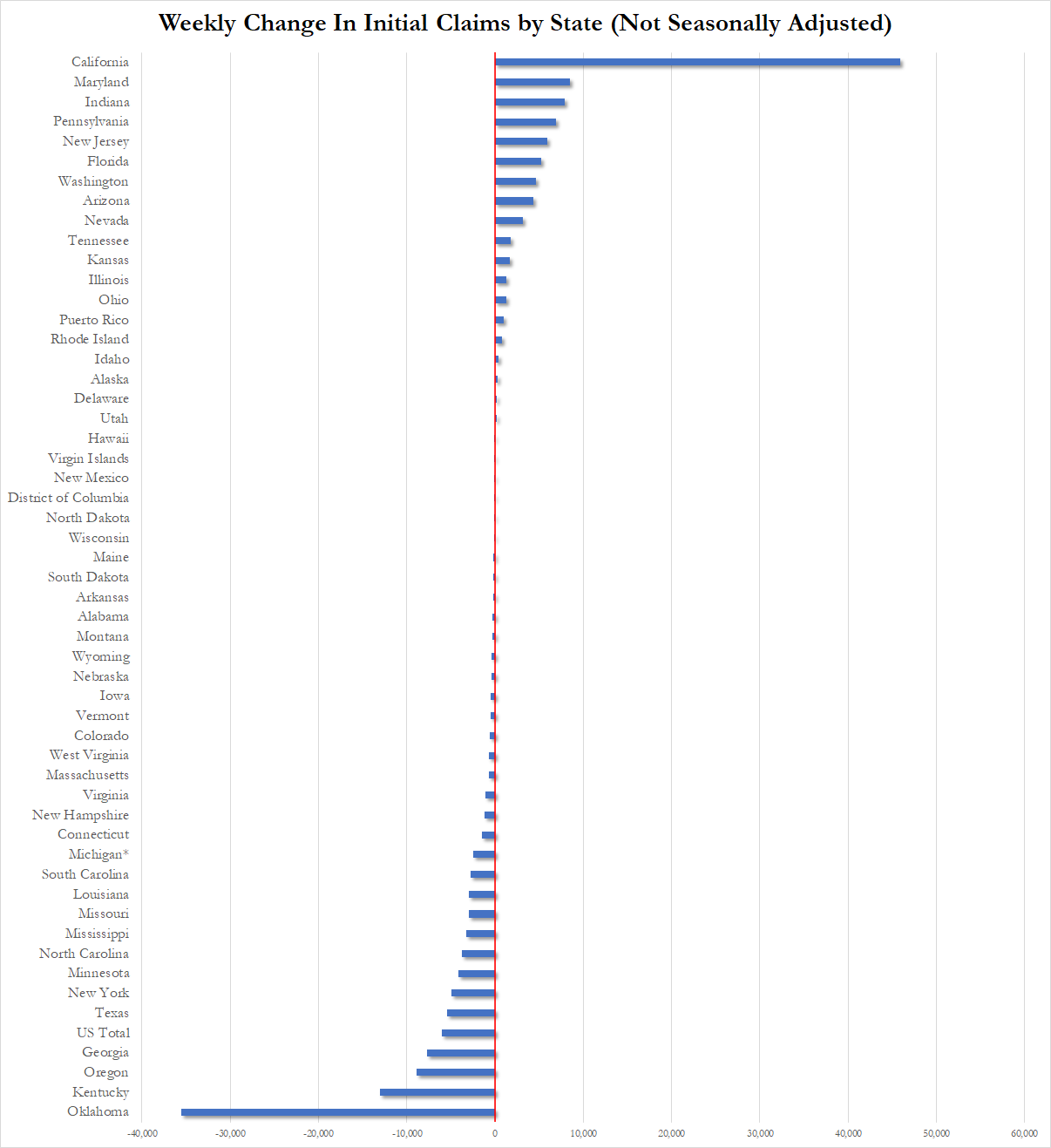

California and Maryland were the worst states for jobless claims in the prior week with Oklahoma and Kentucky showing the biggest improvement…

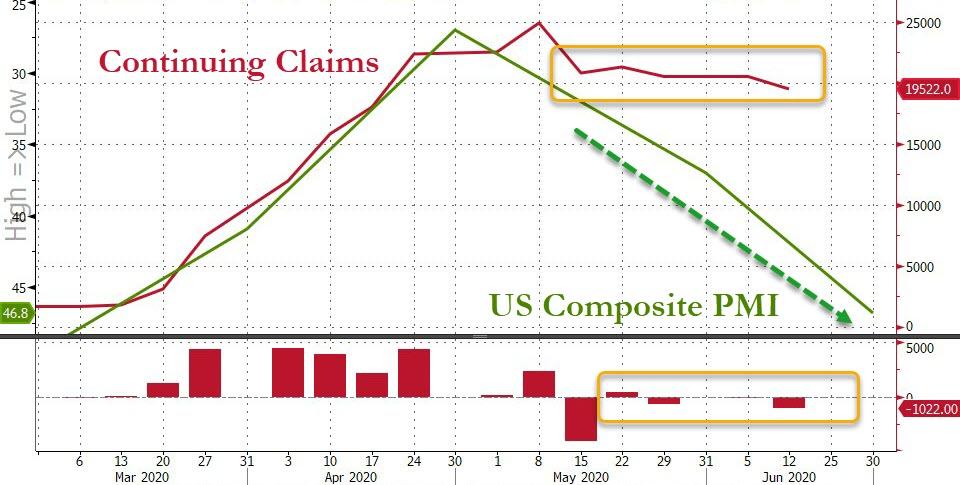

Continuing Claims did drop modestly but hardly a signal that “re-opening” is occurring! And definitely not confirming the PMI data…

Source: Bloomberg

And as we noted previously, what is most disturbing is that in the last fourteen weeks, more than twice as many Americans have filed for unemployment than jobs gained during the last decade since the end of the Great Recession… (22.13 million gained in a decade, 47.25 million lost in 14 weeks)

Worse still, the final numbers will likely be worsened due to the bailout itself: as a reminder, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed on March 27, could contribute to new records being reached in coming weeks as it increases eligibility for jobless claims to self-employed and gig workers, extends the maximum number of weeks that one can receive benefits, and provides an additional $600 per week until July 31.

Finally, it is notable, we have lost 387 jobs for every confirmed US death from COVID-19 (121,979).Was it worth it?

The big question remains – what happens when the $600 CARES Act bonuses stop flowing? Will those who stayed home (thanks to making more money siting on their couch than working) be able to find a job?

via ZeroHedge News https://ift.tt/2Yu2PPo Tyler Durden

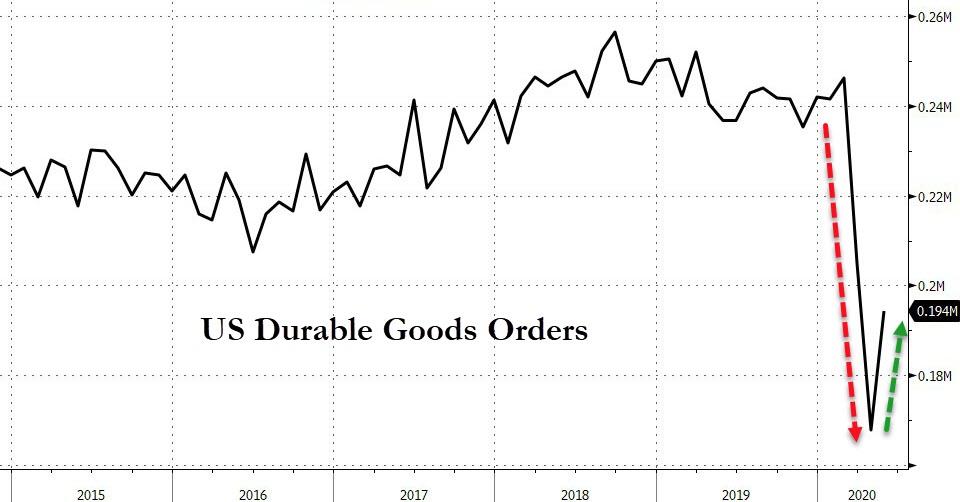

After March and April’s collapse, US Durable Goods Orders were expected to rebound strongly in May and according to preliminary data, they did as headline data soared 15.8% MoM – the most since July 2014. However, on a year-over-year basis, duirable goods orders remain down 21.4%…

The MoM rise of 15.8% was better than the expected 10.% rise (but off a revised lower -18.8% drop in April)…

Source: Bloomberg

Is the ‘V’ you’ve been looking for?

Source: Bloomberg

Closely watched core capital goods orders, which exclude aircraft and military hardware, rebounded 2.3% in May after a 6.5% revised lower decrease a month earlier. Shipments of those goods, a proxy for equipment investment in the government’s gross domestic product report, rose just 1.8% (after a revised lower 6.2% drop in April)…

While states have begun letting business reopen, manufacturing will likely remain slow to recover as fewer people shop and businesses rein in capital spending projects. But, of course, this is all in the rear-view mirror, stocks tell you what happens next, right? V-shaped recovery any second!

via ZeroHedge News https://ift.tt/3ewbx5m Tyler Durden

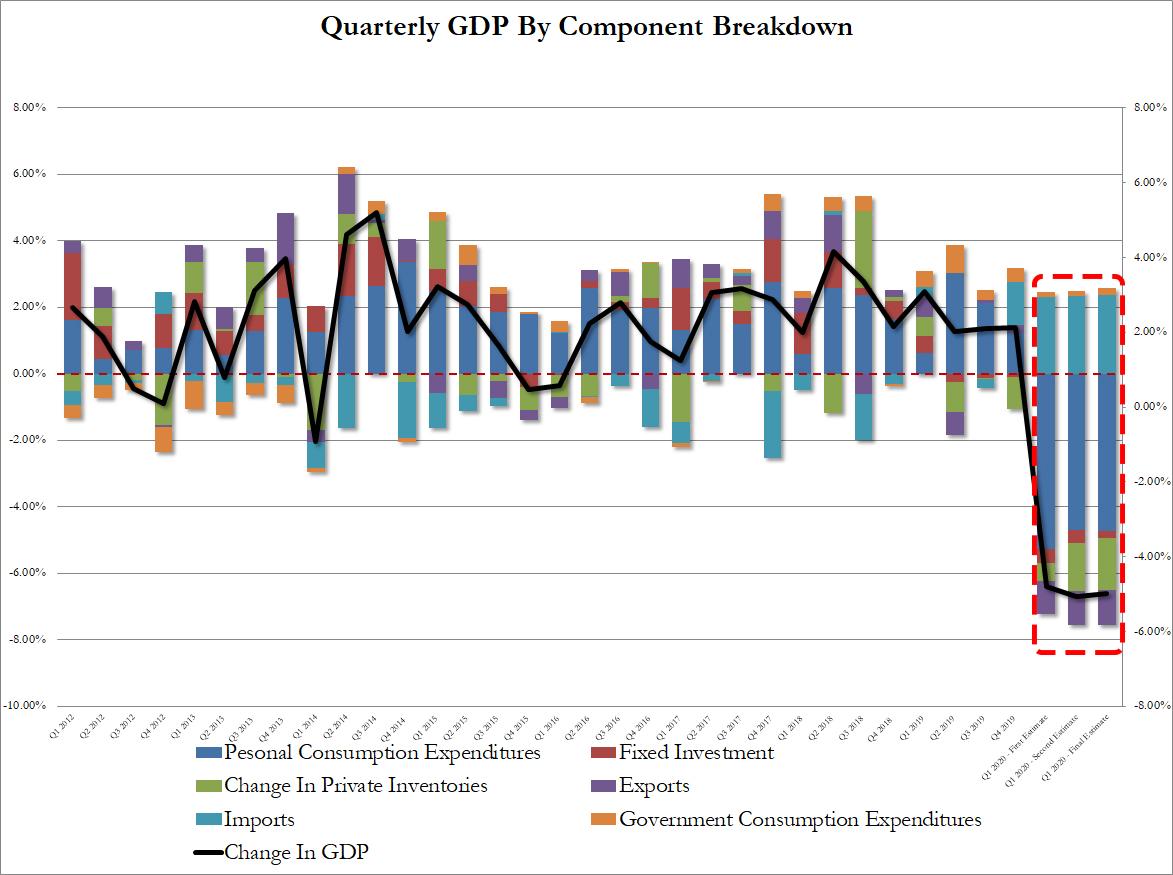

Q1 GDP Unchanged At -5.0% In Final Revision As Corporate Profits Tumbled 12.3% Tyler Durden

Thu, 06/25/2020 – 08:44

While hardly even worth mentioning at a time when everyone is focusing not so much on Q2 GDP but whether Q3 will stage a V-shaped recovery, it is perhaps worth noting that today’s final Q1 GDP revision came in right on top of expectations, and unchanged from the 2nd revision of -5.0% annualized.

While the overall change in GDP was unrevised from the second estimate, an upward revision to business investment was offset by downward revisions to inventory investment, consumer spending, and exports.

The changes between the first and second estimate are as follows:

Personal Consumption revised lower: from -4.69% to -4.73%

Fixed Investment revised higher: from -0.41% to -0.21%

Change in Private inventories revised higher: from -1.43% to -1.56%

Exports revised slightly lower: from -1.02% to -1.06%

Imports also largely unchanged: from 2.34% to 2.37%

Government Consumption was also flat: from 0.15% to 0.20%.

Personal consumption fell 6.8% in 1Q after rising 1.8% prior quarter, and also in line with expectations.

The GDP price index rose a modest 1.4%, also in line with last quarter, and also unchanged, while core PCE posted a modest increase and beat, coming in at 1.7% vs 1.6% expected and in the 2nd revision.

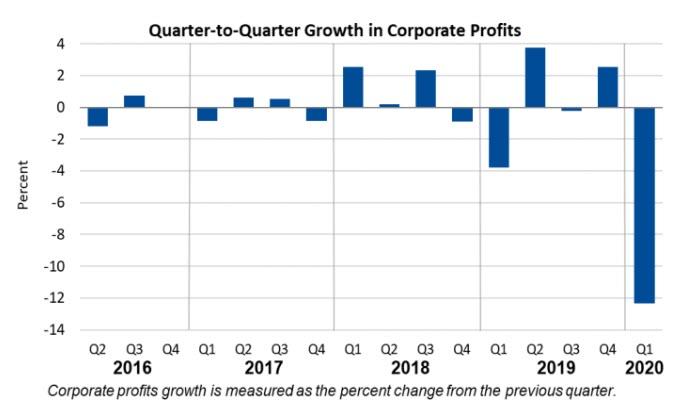

Corporate profits decreased 12.3% at a quarterly rate in the first quarter after increasing 2.6% in the fourth quarter. Corporate profits decreased 6.9% in the first quarter from one year ago.

Profits of domestic nonfinancial corporations decreased 15.4 percent after increasing 4.8 percent.

Profits of domestic financial corporations decreased 9.2 percent after increasing 0.2 percent.

Profits from the rest of the world decreased 8.0 percent after decreasing 0.3 percent.

While we knew that this would be the worst print since the financial crisis, the real question is what Q2 GDP will be, and more importantly whether Q3 GDP for a quarter that begins in less than a week, will show the dramatic improvement already priced into stocks.

via ZeroHedge News https://ift.tt/3fUYieG Tyler Durden

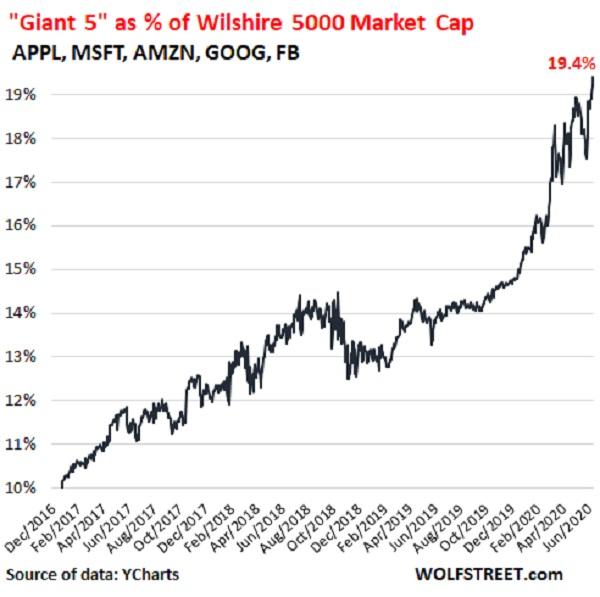

Wolf Richter just published some charts that, for anyone with a sense of stock market history, are pretty ominous. It seems that the major market indexes that recently soared back to record highs are being elevated by an amazingly small number of stocks – Apple, Microsoft, Amazon, Google and Facebook to be specific — which he calls the “Giant 5.” These stocks now account for nearly one-fifth of the Wilshire 5000 stock index’s value:

That kind of dependence on just a handful of companies is intuitively scary. What’s even scarier is that we’ve been here before, and each time the result was ugly.

In the 1960s and early 1970s the US stock market was dominated by a group of large-cap stocks that took on a life of their own, elevating the market far beyond what it would have been without them. See if this Investopedia entry sounds familiar:

The Nifty 50 refers to the fifty most popular large-cap stocks that traded at high valuations in the 1960s and 1970s. They included household names such as Xerox (XRX), IBM, Polaroid and Coca-Cola (KO). Due to their proven growth records and continual increases in dividends, the Nifty Fifty were viewed as “one-decision” picks: investors were told to buy and never sell.

Many Nifty 50 stocks sported price-to-earnings (P/E) ratios as high as 100 times earnings. They propelled the bull market of the early 1970s, only to come crashing down in the 1973-74 bear market.

Then in the 1990s, a group of Big Tech stocks strikingly similar to today’s Giant 5 so dominated the market that they gained global significance:

In May 1999, former Fed Chair Paul Volcker told an audience, “The fate of the world economy is now totally dependent on the growth of the U.S. economy, which is dependent on the stock market, whose growth is dependent on about 50 stocks, half of which have never reported any earnings.”

Volcker saw the bubble. Greenspan missed it. Just a few weeks after Volcker’s speech, Greenspan testified before Congress, saying “Bubbles generally are perceptible only after the fact. To spot a bubble in advance requires a judgment that hundreds of thousands of informed investors have it all wrong. Betting against markets is usually precarious at best.” But the so-called “informed investors” were acting in response to Greenspan’s policy of lowering rates to help the financial markets.

In 2000, inevitably, the bubble popped. Minutes of FOMC meetings show that Greenspan was blind to the fact that the market had been racing up precisely because of his reckless monetary policy. The market crash ruined many naive speculators. Meanwhile, economic researchers began to take issue with Greenspan’s beloved productivity growth. One found that productivity had actually decreased during the late 1990s.

Here’s what happened to the Nasdaq index when that generation of Big Tech stocks returned to their intrinsic value in 2000:

Now back to the current variation on this theme, which Wolf Richter summarizes as follows:

This is how dependent the stock market, and broad portfolios reflecting it, have become on the “Giant 5.” It’s not that there aren’t a bunch of other companies that have gained as much or more than the “Giant 5” in percentage terms – there are – but in dollar terms, and in weight in the market, they just don’t measure up to these five giants.

Apple and Microsoft both are now worth over $1.5 trillion. Amazon is at nearly $1.4 trillion, Alphabet at $1.0 trillion. These are gigantic valuations. They also speak of an immense concentration of power in a single company.

Among the losers in that rest of the market are companies that used to be the largest in the US stock market, such as Exxon-Mobil, which since January 26, 2018, has lost 48% of its value. The entire and once vast oil-and-gas sector has gotten crushed.

The market, and broad portfolios, are immensely dependent on the Giant 5. That was great on the way up – on their way to becoming giants, when their share of the overall market doubled in three-and-a-half years, from 10% in January 2017 to nearly 20% today.

But if they sell off – there are myriad reasons why giants sell off, as all prior giants have found out – the impact of these five companies is going to be proportional to their giant size.

via ZeroHedge News https://ift.tt/2YuFQUq Tyler Durden

Plaintiffs are a religious, family-run business offering art instruction “to individuals ranging in age from nine to adult.” Plaintiffs promote their art lessons on their website. “Although Plaintiffs express their religious identity in their website, the services they provide are nonsectarian.” The following is one example of religious content on Plaintiffs’ website:

“We have come to realize that our eyes see beauty that others sometimes miss. In that beauty we see purpose and meaning. From a decrepit old building or the many colors found on a rusty old car, to the barren stillness of our desert valley to a wondering child’s face, we believe the world around us reflects the beauty and glory of its Creator.”

Inspire operates charter schools throughout California, receives public funding, and “partner[s] with vendors in providing students with various products and services.” Jones is employed by Inspire as the “Vendor Support Team Lead.” “Vendors who are approved enter into a private contractual relationship with Inspire, but do not provide outsourced governmental functions as independent contractors.” To be approved as a vendor, applicants must complete Inspire’s application survey.

In August 2019, Plaintiffs completed one such survey, attempting to contract with Inspire to provide art instruction. Plaintiffs then received an email from Jones rejecting the application, stating “the services appear to be religious in nature or have religious inclinations.” After Plaintiffs asked for clarification, Jones responded that the “decision was based upon the content included on your website.” He continued: “All services and content on websites must be secular in nature for a vendor to be eligible for enrichment funds.”

After Plaintiffs requested clarification concerning what content was preventing approval of their application, Jones advised that Plaintiffs must remove Bible verses and references to “the Creator” on their website to have their application approved. Jones later advised that “[i]f all services are secular and [i]f you were willing to remove this content from your website, we could continue the approval process.” ….

Plaintiffs’ version of the facts, taken in a light most favorable to Plaintiffs and reading the [Complaint] liberally, sets out a violation of Plaintiffs’ First Amendment rights.

Plaintiffs applied to provide nonsectarian art instruction to Inspire and Jones rejected that application due to religious content on Plaintiffs’ website. Jones then conditioned Plaintiffs’ eligibility to contract with Inspire on removing this content from the website, regardless of any potential impact the content may have on Plaintiffs’ art instruction.

Defendants maintain that denial of Plaintiffs’ application was permissible due to California Education Code section 47605(d)(1), which provides in part: “In addition to any other requirement imposed under this part, a charter school shall be nonsectarian in its programs, admission policies, employment practices, and all other operations.” In other words, Defendants argue that their obligation to be “nonsectarian” in administering a school program required them to exclude any vendor that publicly espoused religious views. Defendants are incorrect. Trinity Lutheran Church of Columbia, Inc. v. Comer, (2017).

In Trinity Lutheran, Missouri instituted a nonprofit grant program to replace playground surfaces. Missouri’s Department of Natural Resources had a “strict and express policy of denying grants to any applicant owned or controlled by a church, sect, or other religious entity.” Id. Missouri thus denied Trinity Lutheran’s application solely because it was a church. The Supreme Court concluded that Missouri had violated the Free Exercise Clause of the Constitution because it had expressly discriminated against Trinity Lutheran based on its status as a religious organization. The Supreme Court concluded, “the exclusion of Trinity Lutheran from a public benefit for which it is otherwise qualified, solely because it is a church, is odious to our Constitution … and cannot stand.”

Defendants’ policies here are even more preclusive than the unconstitutional policies in Trinity Lutheran. Not only do Defendants’ policies exclude all churches from providing services, they apparently preclude all services by any potential vendor with religious statements on their website. Defendants do not explain how institution of such a categorical requirement is in keeping with their obligation to facilitate “nonsectarian” services, nor do they offer facts to support that Plaintiffs’ application implicated Establishment Clause concerns.

Instead, without addressing controlling Supreme Court precedent or offering authority of their own, Defendants maintain that by allowing Plaintiffs “to become an approved vendor without modifying its website to remove sectarian references, Inspire could potentially be favoring plaintiffs’ religious views in violation of the No Preference and Establishment Clauses.” The Supreme Court in Trinity Lutheran rejected similarly vague citation of religious establishment concerns, stating that “[i]n the face of the clear infringement on free exercise before us, that interest cannot qualify as compelling.” And like in Trinity Lutheran, the policy here “expressly discriminates against otherwise eligible recipients by disqualifying them from a public benefit solely because of their religious character” and therefore “imposes a penalty on the free exercise of religion that triggers the most exacting scrutiny.” …

I think the charter school could require that contract art teachers not include religious messages in their lessons; the teachers would be viewed as speaking on the school’s behalf, and could be told by the school to teach the way the school wants. But the school can’t exclude such teachers because their out-of-school speech is religious.

from Latest – Reason.com https://ift.tt/2CyccVA

via IFTTT

I’ve been talking this week about principles of good writing that can be learned from Lincoln, Churchill, Holmes, and others whose words have stood the test of time. The ideas are drawn from this new book.

Yesterday’s post showed how Oliver Wendell Holmes used some of the same methods Lincoln did to create memorable sentences. Holmes had an instinct for contrasts. Polarities that ran throughout his writings gave them great force.

Holmes often would say something twice: once in Latinate words, then in words that are Saxon and also highly visual, often because they use a metaphor. In these next examples we see the Saxon finish that has now become familiar, but other kinds of action, too:

I don’t believe in the infinite importance of man—I see no reason to believe that a shudder could go through the sky if the whole ant heap were kerosened. —Holmes, letter to Harold Laski (1921).

No doubt behind these legal rights is the fighting will of the subject to maintain them, and the spread of his emotions to the general rules by which they are maintained; but that does not seem to me the same thing as the supposed a priori discernment of a duty or the assertion of a preexisting right. A dog will fight for his bone. —Holmes, Natural Law (1918).

Both examples end with a run of Saxon words that stand out in contrast to the Latinate flavor of what came before. They also end in animal metaphors, for which Holmes had a deft touch. And in both cases the simple, visual clincher at the end is really a restatement of what he had just said differently. In effect he makes his claim twice, in two languages: once for the head, once for the gut. The second example shows how this can be done in separate sentences.

Those passages also show something else: how the flow of the diction can follow the sense of the words. The higher and more pompous idea is put in words that came into English from Latin (a priori discernment, infinite importance). The hard truth that follows is put mostly in older and simpler words (dog, fight, bone, shudder, sky, ant, heap); kerosene is from Greek, but it now has some of the easy visual qualities of a Saxon word.

The point: Holmes liked to skewer pompous claims. He also liked to blow up linguistic balloons and then pop them. The two habits went together.

Tomorrow I’ll make a few more general remarks about other kinds of contrasts. In the meantime, you can find more about all these themes in the book from which these posts are drawn.

from Latest – Reason.com https://ift.tt/2VfopFq

via IFTTT

Plaintiffs are a religious, family-run business offering art instruction “to individuals ranging in age from nine to adult.” Plaintiffs promote their art lessons on their website. “Although Plaintiffs express their religious identity in their website, the services they provide are nonsectarian.” The following is one example of religious content on Plaintiffs’ website:

“We have come to realize that our eyes see beauty that others sometimes miss. In that beauty we see purpose and meaning. From a decrepit old building or the many colors found on a rusty old car, to the barren stillness of our desert valley to a wondering child’s face, we believe the world around us reflects the beauty and glory of its Creator.”

Inspire operates charter schools throughout California, receives public funding, and “partner[s] with vendors in providing students with various products and services.” Jones is employed by Inspire as the “Vendor Support Team Lead.” “Vendors who are approved enter into a private contractual relationship with Inspire, but do not provide outsourced governmental functions as independent contractors.” To be approved as a vendor, applicants must complete Inspire’s application survey.

In August 2019, Plaintiffs completed one such survey, attempting to contract with Inspire to provide art instruction. Plaintiffs then received an email from Jones rejecting the application, stating “the services appear to be religious in nature or have religious inclinations.” After Plaintiffs asked for clarification, Jones responded that the “decision was based upon the content included on your website.” He continued: “All services and content on websites must be secular in nature for a vendor to be eligible for enrichment funds.”

After Plaintiffs requested clarification concerning what content was preventing approval of their application, Jones advised that Plaintiffs must remove Bible verses and references to “the Creator” on their website to have their application approved. Jones later advised that “[i]f all services are secular and [i]f you were willing to remove this content from your website, we could continue the approval process.” ….

Plaintiffs’ version of the facts, taken in a light most favorable to Plaintiffs and reading the [Complaint] liberally, sets out a violation of Plaintiffs’ First Amendment rights.

Plaintiffs applied to provide nonsectarian art instruction to Inspire and Jones rejected that application due to religious content on Plaintiffs’ website. Jones then conditioned Plaintiffs’ eligibility to contract with Inspire on removing this content from the website, regardless of any potential impact the content may have on Plaintiffs’ art instruction.

Defendants maintain that denial of Plaintiffs’ application was permissible due to California Education Code section 47605(d)(1), which provides in part: “In addition to any other requirement imposed under this part, a charter school shall be nonsectarian in its programs, admission policies, employment practices, and all other operations.” In other words, Defendants argue that their obligation to be “nonsectarian” in administering a school program required them to exclude any vendor that publicly espoused religious views. Defendants are incorrect. Trinity Lutheran Church of Columbia, Inc. v. Comer, (2017).

In Trinity Lutheran, Missouri instituted a nonprofit grant program to replace playground surfaces. Missouri’s Department of Natural Resources had a “strict and express policy of denying grants to any applicant owned or controlled by a church, sect, or other religious entity.” Id. Missouri thus denied Trinity Lutheran’s application solely because it was a church. The Supreme Court concluded that Missouri had violated the Free Exercise Clause of the Constitution because it had expressly discriminated against Trinity Lutheran based on its status as a religious organization. The Supreme Court concluded, “the exclusion of Trinity Lutheran from a public benefit for which it is otherwise qualified, solely because it is a church, is odious to our Constitution … and cannot stand.”

Defendants’ policies here are even more preclusive than the unconstitutional policies in Trinity Lutheran. Not only do Defendants’ policies exclude all churches from providing services, they apparently preclude all services by any potential vendor with religious statements on their website. Defendants do not explain how institution of such a categorical requirement is in keeping with their obligation to facilitate “nonsectarian” services, nor do they offer facts to support that Plaintiffs’ application implicated Establishment Clause concerns.

Instead, without addressing controlling Supreme Court precedent or offering authority of their own, Defendants maintain that by allowing Plaintiffs “to become an approved vendor without modifying its website to remove sectarian references, Inspire could potentially be favoring plaintiffs’ religious views in violation of the No Preference and Establishment Clauses.” The Supreme Court in Trinity Lutheran rejected similarly vague citation of religious establishment concerns, stating that “[i]n the face of the clear infringement on free exercise before us, that interest cannot qualify as compelling.” And like in Trinity Lutheran, the policy here “expressly discriminates against otherwise eligible recipients by disqualifying them from a public benefit solely because of their religious character” and therefore “imposes a penalty on the free exercise of religion that triggers the most exacting scrutiny.” …

I think the charter school could require that contract art teachers not include religious messages in their lessons; the teachers would be viewed as speaking on the school’s behalf, and could be told by the school to teach the way the school wants. But the school can’t exclude such teachers because their out-of-school speech is religious.

from Latest – Reason.com https://ift.tt/2CyccVA

via IFTTT

I’ve been talking this week about principles of good writing that can be learned from Lincoln, Churchill, Holmes, and others whose words have stood the test of time. The ideas are drawn from this new book.

Yesterday’s post showed how Oliver Wendell Holmes used some of the same methods Lincoln did to create memorable sentences. Holmes had an instinct for contrasts. Polarities that ran throughout his writings gave them great force.

Holmes often would say something twice: once in Latinate words, then in words that are Saxon and also highly visual, often because they use a metaphor. In these next examples we see the Saxon finish that has now become familiar, but other kinds of action, too:

I don’t believe in the infinite importance of man—I see no reason to believe that a shudder could go through the sky if the whole ant heap were kerosened. —Holmes, letter to Harold Laski (1921).

No doubt behind these legal rights is the fighting will of the subject to maintain them, and the spread of his emotions to the general rules by which they are maintained; but that does not seem to me the same thing as the supposed a priori discernment of a duty or the assertion of a preexisting right. A dog will fight for his bone. —Holmes, Natural Law (1918).

Both examples end with a run of Saxon words that stand out in contrast to the Latinate flavor of what came before. They also end in animal metaphors, for which Holmes had a deft touch. And in both cases the simple, visual clincher at the end is really a restatement of what he had just said differently. In effect he makes his claim twice, in two languages: once for the head, once for the gut. The second example shows how this can be done in separate sentences.

Those passages also show something else: how the flow of the diction can follow the sense of the words. The higher and more pompous idea is put in words that came into English from Latin (a priori discernment, infinite importance). The hard truth that follows is put mostly in older and simpler words (dog, fight, bone, shudder, sky, ant, heap); kerosene is from Greek, but it now has some of the easy visual qualities of a Saxon word.

The point: Holmes liked to skewer pompous claims. He also liked to blow up linguistic balloons and then pop them. The two habits went together.

Tomorrow I’ll make a few more general remarks about other kinds of contrasts. In the meantime, you can find more about all these themes in the book from which these posts are drawn.

from Latest – Reason.com https://ift.tt/2VfopFq

via IFTTT

Disney Delays Reopening Of American Theme Parks Tyler Durden

Thu, 06/25/2020 – 08:17

After announcing earlier this month that it would triumphantly reopen Disneyland Resort and Disney California Adventure Park, pending approval from state and local government, on July 17, Disney has taken a step back due to the renewed outbreaks in California and Florida and decided to delay the reopenings of its American theme parks.

Indeed, the company announced Wednesday that the state approvals needed to reopen likely wouldn’t arrive in time for its July 17 target date.

Disney’s “Park News” twitter account shared more information on the company’s plans.

— Disney Parks News (@DisneyParksNews) June 25, 2020

According to the statement, a new reopening date will be announced “once we have a clearer understanding of when guidelines will be released.”

However, Disney’s “Downtown Disney”, which includes restaurants and retail shops, will still reopen on July 9 as planned.

Josh D’Amaro, the Chairman of Disney Parks, Experiences and Products, wrote in a blog post on June 10 that the company was “purposefully taking baby steps during this very intentional phased approach.”

Those steps included introducing a reservation system that will require all guests, including annual passholders, to reserve their park entry in advance, as well as putting a pin in all displays that draw crowds, like fireworks displays, parades etc.

Notably, the company in its statement assured its customers that, if left to its own devices, the company would reopen the parks, but it emphasized that local governments had to hit the breaks.

“You would think Disney would be taking a far more cautious approach and it wouldn’t be the government basically pushing back on Disney,” says @RichLightShed. “It shows you $DIS is under a lot of pressure financially. They are feeling the pressure to open.” pic.twitter.com/kAf3ROtf3V

Futures Accelerate Slide On “Second Wave” Fears Ahead Of Jobless Claims Tyler Durden

Thu, 06/25/2020 – 08:02

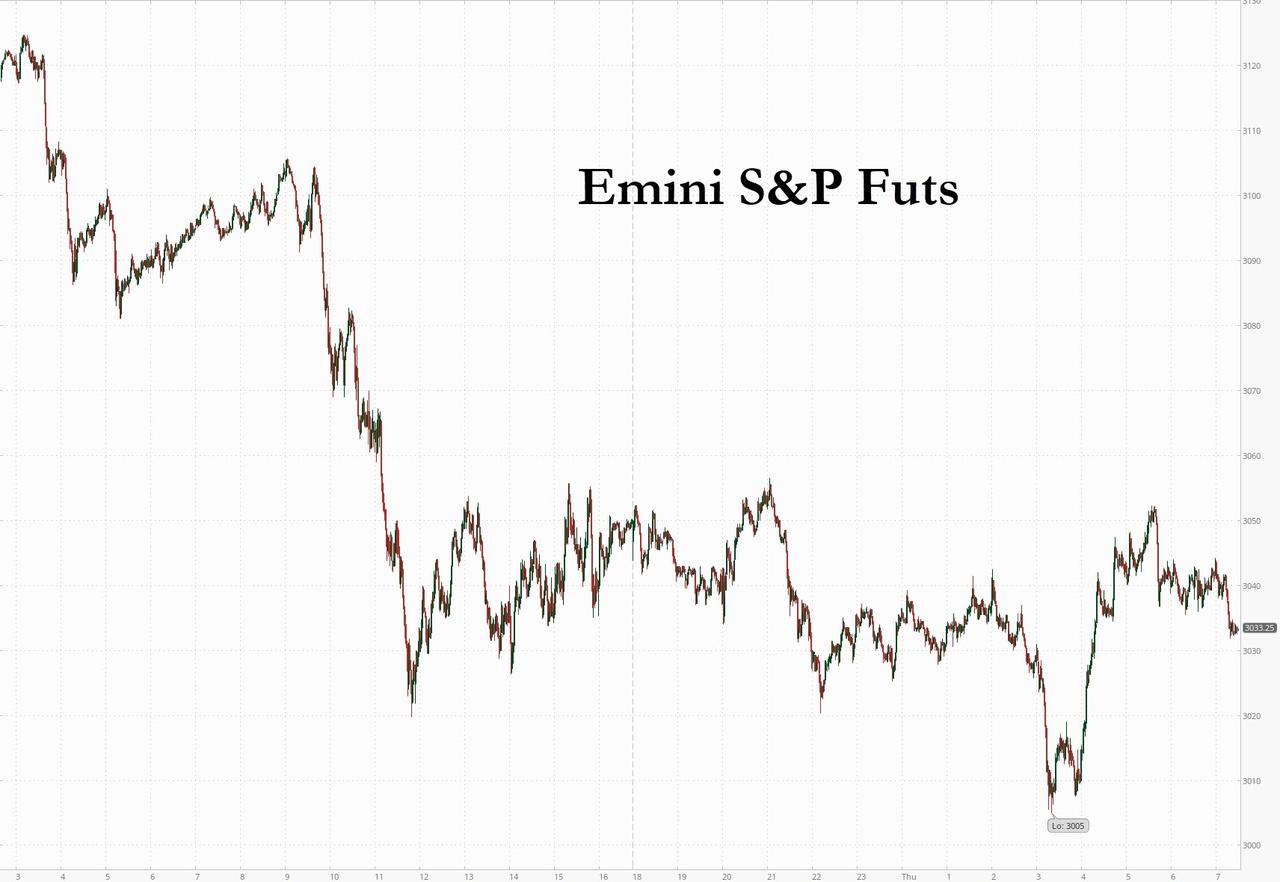

US stock futures fell for a second straight day on Thursday following Wall Street’s worst day in two weeks, as risk appetite took a hit from an alarming rise in new coronavirus cases and on expectations of elevated weekly jobless claims, although futures rebounded from a sharp drop thanks to gains in large-cap tech shares following Europe’s open which dragged down the Emini as low as 3,005 before stabilizing above 3,030. Treasury yields dropped to 0.66% while the dollar rose for a second day.

As has become the norm in recent overnight sessions, Nasdaq 100 futures erased most of an earlier decline. Walt Disney slipped 1.4% in premarket trading after it delayed the reopening of theme parks due to the health crisis. Boeing fell 2.7% as Berenberg reduced its rating to “sell”, noting the planemaker’s near-term risks are elevated due to the COVID-19 pandemic, the pace of recovery in air travel and uncertainty related to production rates.

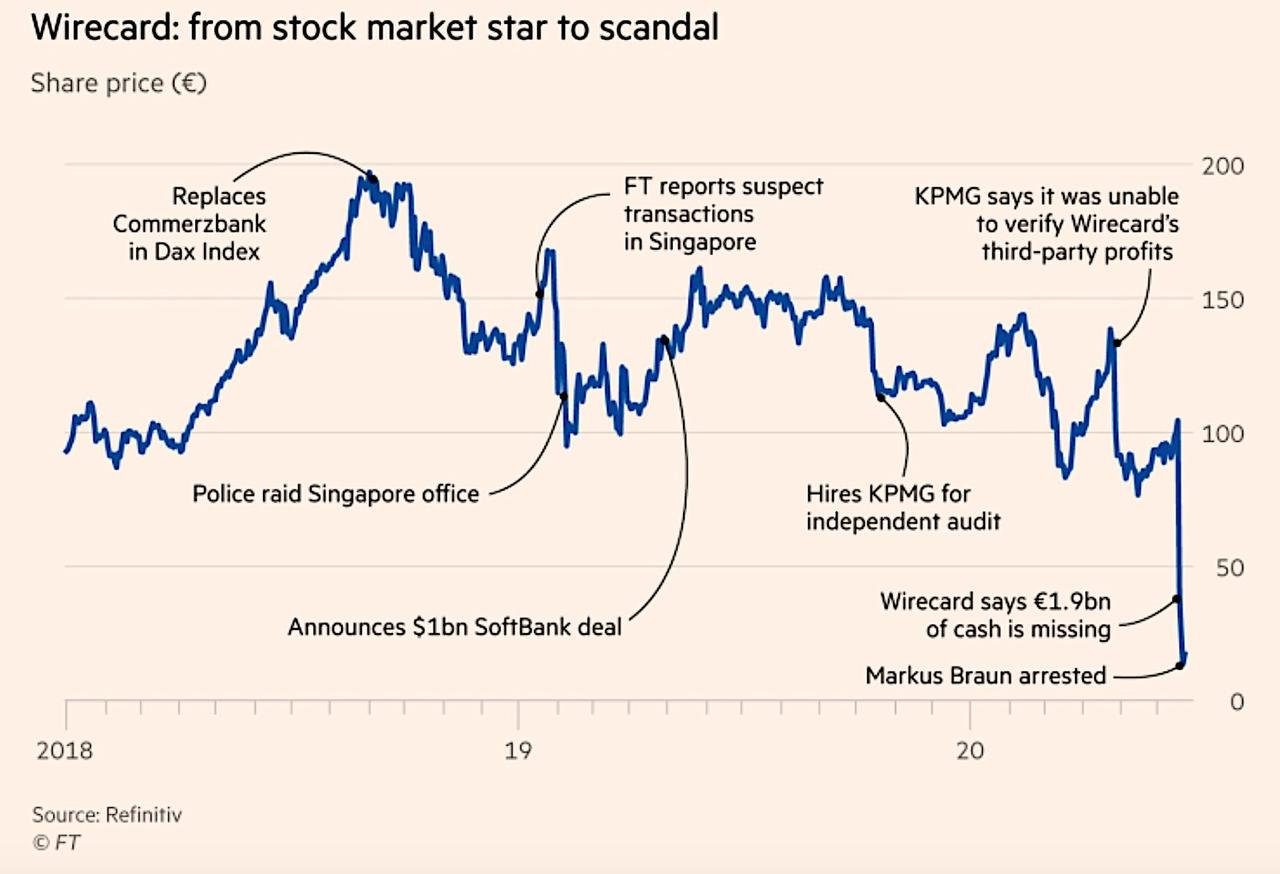

In Europe, stocks swung from a loss to a gain, with Deutsche Lufthansa rallying as its biggest shareholder backed a government rescue package. Meanwhile, the saga of German fintech Wirecard ended with the company filing for insolvency, sending its stock crashing over 80% to all time lows.

Earlier in the session, Asian stocks fell the most in almost two weeks. China and Hong Kong were shut for holidays. Local markets suffered from spillover selling after the weakness seen in global counterparts as risk appetite took a hit from several fronts including the record COVID-19 infection rates in US, half-year end rebalancing which according to JPM is as much as $170BN in selling, and a US-EU tariff threat after reports of US targeting USD 3.1BN of exports from France, Germany, Spain and UK for new tariffs.

Growing fears that lockdowns will be reimposed and economies re-opened more slowly has hurt sentiment, as investors weigh reports of new daily records for infections in Texas, Florida and California. Meanwhile, Bloomberg reports that health leaders called on the U.K. to prepare for a possible second wave, and Australia recorded its largest spike in cases since April.

“The market really got the shivers over the prospect of a big increase in Covid and maybe starting to see places that were opening up have to close up,” Wells Fargo PM Margie Patel said on Bloomberg TV. “We’ve had such a great run from the end of March it’s only inevitable that we should get at least a little step back.”

Besides the pandemic, data due at 8:30 a.m. ET is expected to show about 1.32 million Americans signed up for unemployment benefits in the latest week. Although that figure is down from 1.5 million in the prior week, the pace of declines has slowed as weak demand forces U.S. employers to lay off workers.

In rates, Treasuries were higher led by long end, trimming yields in 20- to 30-year sector lower by nearly 2bp. Price action echoed the wider bull-flattening for the German curve, while gilts outperformed, sending U.K. five-year yields to a record low of minus 0.047% and the curve flattened, after some investors were caught out from bets on a steeper curve following last week’s Bank of England meeting. At the same time, 3M USD Libor rose by over 2bp, a headwind for front-end eurodollar futures. Today the Treasury auction cycle concludes with $41b 7-year note sale at 1pm ET; WI 7- year yield at ~0.51% is ~4bp richer than last month’s result and below April’s record low 0.525%.

In FX, the dollar traded mixed versus Group-of-10 peers after Antipodean and Scandinavian currencies swung from losses to gains as sentiment improved. The kiwi dollar led G-10 gains and outperformed its peer in Australia, where sentiment was hit by a surge in virus cases and job cuts at the national airline.

In commodities, West Texas crude oil fell below $38 a barrel, while gold pared an earlier gain.

Economic data include initial jobless claims, durable goods orders and the third print of first-quarter GDP. Nike is set to report earnings.

Market Snapshot

S&P 500 futures down 0.4% to 3,036.75

STOXX Europe 600 up 0.1% to 357.59

MXAP down 1.1% to 158.82

MXAPJ down 0.8% to 515.49

Nikkei down 1.2% to 22,259.79

Topix down 1.2% to 1,561.85

Hang Seng Index down 0.5% to 24,781.58

Shanghai Composite up 0.3% to 2,979.55

Sensex up 0.2% to 34,933.13

Australia S&P/ASX 200 down 2.5% to 5,817.68

Kospi down 2.3% to 2,112.37

German 10Y yield fell 1.4 bps to -0.454%

Euro down 0.1% to $1.1238

Brent Futures down 0.8% to $39.98/bbl

Italian 10Y yield rose 1.1 bps to 1.14%

Spanish 10Y yield unchanged at 0.468%

Brent Futures down 0.8% to $39.98/bbl

Gold spot up 0.2% to $1,765.37

U.S. Dollar Index up 0.1% to 97.28

Top Overnight News from Bloomberg

The U.S. economic recovery is showing incipient signs of weakening in some states where coronavirus cases are mounting. The ebbing is evident in such high-frequency data as OpenTable restaurant reservations and follows a big bounce in activity as businesses reopened from lockdowns meant to check the spread of Covid-19

Germany’s coronavirus infection rate fell to the lowest in almost three weeks, easing concerns that local outbreaks would prompt a resurgence of the pandemic

Germany’s constitutional court rejected a separate challenge against the European Central Bank’s 2015 Expanded Asset Purchase Program as inadmissible

The European Central Bank will set up a precautionary facility to provide euros to central banks outside the currency area to help ease any liquidity stress as a result of the coronavirus pandemic

Asian stocks suffered from spillover selling after the weakness seen in global counterparts as risk appetite took a hit from several fronts including the record COVID-19 infection rates in US, half-year end rebalancing and a US-EU tariff threat after reports of US targeting USD 3.1bln of exports from France, Germany, Spain and UK for new tariffs. ASX 200 (-2.5%) was led lower by underperformance in the energy sector due to lower oil prices and with hefty losses seen in travel stocks after Qantas announced several cost-cutting measures. Nikkei 225 (-1.2%) was pressured by the ill-effects of the predominantly firmer domestic currency and KOSPI (-2.3%) traded downbeat following South Korea’s announcement of a capital gains tax on stock trading from 2023, while trade for the region was also hindered by key holiday closures with mainland China, Hong Kong and Taiwan all closed for the Dragon Boat Festival. Finally, 10yr JGBs were flat as prices failed to take advantage of the risk averse tone, advances in T-notes and with the latest update showing the BoJ’s share of the JGB market increased to 44.2% as of end-March vs 43.7% Q/Q, with participants kept sidelined amid the 20yr auction in which nearly all metrics pointed to a weaker result.

Top Asian News

Philippines Surprises With Half-Point Rate Cut to Boost Economy

NTT Buys NEC Stake in Bid for Slice of Global 5G Gear Market

In Asia, Brands Built on Racist Stereotypes Face Scrutiny

Pandemic Gives Singapore Air Chance to Grab Emirates India Share

Price action for European stocks has been relatively choppy thus far with downside initially emanating from the soft leads presented by the US and APAC sessions as the COVID-19 case count in certain areas of the US continues to deteriorate. Stocks in Europe were presented some reprieve as the session progressed with not much in the way of standout fundamentals behind the move. Some have attributed part of the move to the ECB announcing a new Eurosystem repo facility to provide euro liquidity to non-euro area central banks, however, stocks were already gaining ahead of this announcement. Note, it is plausible that equities could struggle for direction in the first half of the session until COVID-19 case count data from the US is released mid-afternoon; something which has been a key source of price action over the past few days. From a sectoral standpoint, it is a relatively mixed picture thus far with some cyclical areas such as Autos and banks faring slightly better than peers, whilst the travel & leisure sector is a noteworthy underperformer. Despite stellar gains for Deutsche Lufthansa (+16.5%) following reports that shareholder Thiele (15.5% stake holder) said he will vote for the rescue package in today’s EGM, travel names have taken greater direction from easyJet (-5.6%) after the Co.’s latest earnings update in which the Co. also announced it is to launch a GBP 450mln rights issue. Wirecard (-79%) remain in focus with shares opening lower in the wake of the recent scandal with the latest chapter in the saga seeing the Co. announce it has applied for insolvency proceedings – shares were halted at EUR 10.74 ahead of the announcement before slumping to EUR 2.50 upon resumption. On a more positive footing, albeit of best levels, Bayer (+1.4%) shares have been supported since the get-go after news the Co. will pay up to USD 10.9bln to settle a string of cancer claims linked to the Roundup weedkiller case. Finally, Royal Mail (-8.2%) shares are also seen lower this morning after post a decline in profits to GBP 180mln in the year to March 2020 which has subsequently forced the Co. to lower its headcount by 2,000.

Top European News

Top Lufthansa Investor Backs $10 Billion Bailout Before Key Vote

Some of U.K.’s Largest Retailers Withheld Quarterly Rent: Times

Royal Mail Cuts Management Jobs as Virus Hits Demand

Swedish Scientist Who Doubted Face Masks Reconsiders Their Use

In FX, the DXY Index holds onto yesterday’s gains above 97.000 but trades in a relatively tight 97.160-404 intraday band thus far as safe-haven demand keeps the broader Dollar propped up amid rising COVID cases across the US and other economies such as Germany, Japan, Australia and China heading into the half-year, quarter and month-end, while participants remain on the lookout for a follow-up to US tariff threat on the EU and UK. Looking ahead, the data-docket sees an abundance in Tier 1 data in the form of Durable Goods, Q1 GDP (F) and Initial Jobless Claims, albeit focus will likely remain on COVID-19 case counts State-side and abroad.

EUR, GBP – The Single-currency has trimmed losses against the Buck, but more so on USD-dynamics with little reaction seen to the improvement in Gfk consumer sentiment. Meanwhile, reports early-doors noted that the German Constitutional Court has rejected a separate case in regard to the ECB’s asset purchase programme, but details remain vague at the time of writing. This followed reports overnight that the ECB has agreed to provide the Bundesbank with documents on proportionality, as expected. Next up, the ECB’s accounts from the June meeting could provide some meat on the bone over the decision-making process on the PEPP ramp up to 1.35tln from 750bln. EUR/USD meanders around 1.1250 having had printed a current band at 1.225-60 with option expiries seeing a sizeable EUR 1.6bln at strike 1.1200, EUR 805mln at 1.1260 and almost EUR 1bln at 1.1300. Meanwhile, Cable continues to grind higher above its 50 DMA (1.2417), and resides around 1.2450 (ahead of its 10 and 21 DMAs both at 1.2488-89) with little by way of fresh fundamentals ahead of remarks from BoE’s Haldane – who voted against the BoE’s QE ramp up last week. Thus, EUR/GBP trickles lower towards the 0.9000 mark, with short-term support seen around the 0.9014-18 ahead (lows over the last three trading sessions).

AUD, NZD, CAD – All firmer against the USD, albeit to different degrees with the Kiwi the marked outperformer as it consolidates from its post-RBNZ losses despite a relatively lacklustre May trade balance release overnight. NZD/USD however, remains sub-0.6450 with its 10 DMA at around the psychological level. AUD/USD moves in tandem with the Dollar as price action remains contained within a 30-pip range (0.6848-84), whilst upside technicals see the 100 WMA situated at 0.6909. The Loonie fails to reap the same benefits as its high-beta peers as gains remain somewhat hampered from a sovereign downgrade at Fitch (AA+ from AAA-; outlook Stable). USD/CAD holds onto a 1.3600 handle but resides around session lows (1.3620) amid an attempted recovery in the energy markets.

JPY – Safe havens trade choppy within tight ranges as the pairs track sentiment and price action in stocks. USD/JPY keeps its 107.00 handle having had dipped below the figure overnight, with its 50 DMA at 107.39.

In fixed Income, core bonds initially began the European session somewhat softer, after a comparatively uneventful overnight session where they were subject to a grinding bid as sentiment remained subdued following yesterday’s stock pullback. Interestingly, even given the strong risk-off trade seen yesterday the UST yield curve only saw modest bull-flattening, with similar price action being seen currently and as such expanding on yesterday’s action; for instance, today’s UST 10yr yield low stands at 0.6630% just below yesterday’s 0.6760% floor. On this, desks have highlighted that US steepeners are, given additional pressures from supply and inflation, seen to be outperforming their European peers ahead; with some option premium measures having surpassed pre-COVID levels – potentially explaining some of the recent magnitude discrepancies. European hours have seen pronounced choppiness across the debt complex, as well as markets more broadly, with initial bond upside derived around the EU equity cash open and just before, but seemingly unrelated to, reports the GCC have rejected a separate case regarding ECB QE; note, details on this headline are still very vague and on the subject attention is on today’s ECB minutes. Nonetheless, at the time Bunds sharply retreated and BTPs saw a firm bid; albeit, both moves were within session ranges failing to test the sessions low/high of 176.09 and 143.80 respectively and ultimately pared back. Since then, while debt has been subject to periods of choppiness as sentiment in general struggles to find direction, we are overall marginally firmer on the day for core counterparts but seemingly capped by the session’s ranges. In terms of focus for the session ahead, we do have the aforementioned ECB minutes alongside a number of central bank speakers and US data – but focus will likely remain on the COVID-19 count and particularly updates from the key US states of Florida, NY and Texas.

In commodities, choppy trade in the crude complex as price action is predominently dicatated by market sentiment in which the downbeat APAC session saw WTI and Brent August contracts relinquish the USD 38/bbl and USD 40/bbl level respectively. However, amid an improvement in broader sentiment as European trade is underway, the benchmarks have rebounded off lows of USD 37.13/bbl and USD 39.50/bbl respectively, with the latter reclaiming USD 40/bbl to the upside. News-flow has been light for the complex but price action is likely to be influenced by COVID-19 developments ahead of Tier 1 US data. Elsewhere, spot gold remains relatively steady around USD 1765/oz within today’s range despite the whipsaws seen cross-market, with initiall impetus derived as European players entered the markets to a softer APAC session. Copper trades with modest gains as the red metal retraced earlier downside amid a recovery in stocks, but price action remains contained within recent ranges.

US Event Calendar

8:30am: GDP Annualized QoQ, est. -5.0%, prior -5.0%; Core PCE QoQ, est. 1.6%, prior 1.6%

8:30am: Personal Consumption, est. -6.8%, prior -6.8%

8:30am: Retail Inventories MoM, est. -2.8%, prior -3.6%; Wholesale Inventories MoM, est. 0.4%, prior 0.3%

8:30am: Durable Goods Orders, est. 10.45%, prior -17.7%; Durables Ex Transportation, est. 2.1%, prior -7.7%

8:30am: Cap Goods Orders Nondef Ex Air, est. 1.0%, prior -6.1%; Cap Goods Ship Nondef Ex Air, est. -1.0%, prior -5.7%

8:30am: Initial Jobless Claims, est. 1.32m, prior 1.51m; Continuing Claims, est. 20m, prior 20.5m

11am: Kansas City Fed Manf. Activity, est. -3, prior -19

DB’s Jim Reid concludes the overnight wrap

I’ve got the rest of the day off today as the golf course I’m a member of opposite my house is hosting a charity pro-am. So I’ll be playing with a touring pro and they’ll be competing for a healthy prize. So the big question on everyone’s lips at the golf club last night as I went to the range to try to limit my embarrassment today was who they’ll be playing with. Yes the pros were all wondering which of them will be playing with the author of the EMR. Lucky them. Sky Sports News have their cameras here at Worplesdon all day so there’s the outside chance you’ll see my dodgy swing on the bulletins. Without much live sport at the moment they have a lot of airtime to fill. I’ll have mixed feelings if Liverpool win the league tonight for the first time in 30 years and it bumps my pro-am appearance off the sports news.

The business channels have had no such problems filling air time over the last few months and they will again have plenty to discuss today. A plethora of bad news about the virus led to a major sell-off in risk assets yesterday as volatility returned to financial markets once again. It wasn’t a single bad headline that led to the plunge, but a drip-feed of negative stories that all combined to show increasing signs of a deteriorating situation on the virus, most obviously in the US. In terms of the news there, Florida (the 3rd most populous US state) saw its number of Covid-19 cases rise by 5.3% yesterday, some way above the previous 7-day average of 3.7%, and the number of hospitalisations rose by 256 in the state, the largest increase in a month. California also saw a record jump in cases, with over 8800 new ones yesterday. This equated to a 4.8% rise – notably above the 2.5% average daily rise over the last week. Covid-19 ICU cases have risen 18% in the last 2 weeks according to the state, but the rate of fatalities has thankfully not picked up in recent days. This could be still to come, but perhaps it is a sign that hospitals have gotten better at treating the virus now that we are further into the pandemic and maybe that the average age of new cases has fallen. In the pdf today (click “view report”) we show graphs of 7 day rolling cases against 7 day rolling fatalities with a lag of 7 days for the 4 troubled US states and also the US overall, alongside NY and Germany. These last three are included to show the correlation earlier in this pandemic and how it might be changing. We say might because the graphs show we’re at a critical point where fatalities should be going up. However there is evidence from the US overall and the four states that this isn’t happening to the same degree it did in other parts of the world in March and early April. An important few days ahead then. Note that the pdf also includes the usual case and fatality tables.

Meanwhile, in what represents a notable reversal from earlier in the pandemic, the three states of New York, New Jersey and Connecticut are going to order visitors coming from virus hotspots to quarantine for 14 days. Texas was one of the states that originally ordered those restrictions on Northeastern states. And yet yesterday the 2nd most populous state in the US had news come through from Houston that intensive-care units were currently at 97% capacity and are likely to exceed tomorrow. With the state as a whole right up to its limit of ICU beds, Texas Medical Center is currently projecting that they will access their surge capacity starting this week. They are also likely to surpass that capacity (887 surge ICU beds) in about two weeks if current virus trends continue. The rise in Texan cases yesterday was followed by headlines that Apple was moving to close seven stores in the Houston area, with 18 stores now closed nationwide following their reopening. Overall the US saw cases rise by 1.6%, above the 1.3% average daily rise over the last week, while the number of new cases per week is now approaching the highs of the pandemic. See our US economists piece last night (link here) that suggests states with faster case growth are now underperforming economically based on measures of small business activity, restaurant bookings and consumer spending particularly in the southern states already mentioned.

Looking at the market reaction, these revived concerns about the virus saw equity markets lose substantial ground yesterday, a move that more than erased Tuesday’s gains. Looking at the major indices, the S&P 500 was down -2.59% (-3.17% at the intra-day lows), with energy stocks leading the decline on the back of plunging oil prices. It was the worst daily performance for the index since June 11th (-5.89%) and the second worst since May 1st (-2.81%). Elsewhere the NASDAQ snapped a run of 8 successive gains to fall by -2.19%, down from its fresh record the previous day. Over in Europe the picture was somewhat worse with all the major indices closing at their lows of the day and missing the small bounce that US assets saw late in their session. The STOXX 600 was down -2.78% as energy similarly led the declines with the DAX (-3.43%), CAC 40 (-2.92%) and the FTSE 100 (-3.11%) also falling back. The selloff in Europe and the US was incredibly broad with only about 3.5% of stocks in each of the S&P 500 and STOXX 600 up on the day.

While the moves haven’t been quite as severe, Asian markets are lower this morning too with the Nikkei (-1.23%), Kospi (-1.82%) and ASX (-1.62%) all down. Markets in Hong Kong and China are closed for a holiday. In FX, the US dollar index is up another +0.18% building up on yesterday’s gains. Yields on 10y USTs are down a further -1bp overnight to 0.670% while futures on the S&P 500 are down -0.52%.

In overnight news, the Pentagon has put up a list of 20 Chinese companies that it says are owned or controlled by China’s military, opening them up to potential additional US sanctions. The list includes Huawei Technologies Co. and Hangzhou Hikvision Digital Technology Co. amongst others.

In terms of those other moves yesterday, oil lost ground as mentioned earlier with Brent crude down -5.44% to $40.31/bbl. Unsurprisingly, oil-producing currencies underperformed in response, as both the Norwegian krone (-1.53% vs. USD) and the Russian ruble (-1.03%) weakened. The US dollar had a fairly strong performance however, up +0.52% in its best day in over a week. Over in fixed income, sovereign bond markets see-sawed as they oscillated between gains and losses through the session. By the close, core bond yields had moved lower, with those on 10yr Treasuries and bunds down -3.3bps and -3.2bps respectively. BTPs underperformed however, coming off their nearly 3-month lows with a +1.1bps increase.

Staying with Europe, this week our Economist team published a report titled ‘Bank credit, economic growth and the COVID shock: an adjusted perspective’ . Watch a new video with Mark Wall, Chief Economist, EMEA (link here to the video and report) where he explains that the focus of the note is on bank credit in the euro area – on its surprising, and misleading, strength during the COVID shock and where it is likely to go next.

Keeping on the economic theme, the mood was dampened further yesterday by updated forecasts from the IMF, who downgraded their outlook for the global economy compared with their April forecasts. They now see the world economy undergoing a -4.9% contraction this year (vs. -3.0% previously), before growing by +5.4% in 2021 (vs. +5.8% previously). The downgrades were seen in both advanced as well as emerging market and developing economies, while their projections for the volume of global trade sees a decline of -11.9% this year.

In other news, with just over 4 months to go now until the US election, a New York Times/Siena College poll out yesterday gave Joe Biden a 50%-36% advantage over President Trump. This is but the latest in a pattern evident for some weeks now of a widening lead for Biden. FiveThirtyEight’s polling average now puts him +9.3% ahead of Trump. This has been reflected on the betting and prediction markets too, with Biden now the favourite there as well. It’s also worth noting that Trump’s approval rating at this point in his term is below that of his 3 immediate predecessors who went on to win re-election.

Staying on politics, and yesterday we had a statement from the Elysee that President Macron and Chancellor Merkel would be meeting on Monday, with the EU budget and the recovery fund on the agenda. Remember that this comes ahead of another EU leader’s summit on the 17-18th July, where the 27 leaders will meet in person in Brussels to hold further discussions on the recovery fund. That said, there’s still substantial differences between the different member states on this, particularly with the so-called Frugal Four, and any final agreement will require unanimity between the member states. On a side note however, Euro Area inflation expectations rose to their highest level since early March yesterday, with five-year forward five-year inflation swaps closing above 1.10% for the first time since then.

Looking at yesterday’s data releases, the main highlight was the Ifo business climate indicator from Germany, which rose to 86.2 in June (vs. 85.0 expected), up from a revised 79.7 in May. Nevertheless, this is still some way from the 95.9 reading in February before the economic impact of the pandemic hit. Otherwise, the FHFA US house price index rose by +0.2% in April (vs. +0.3% expected).

To the day ahead now, and data releases include the weekly initial jobless claims data from the US, as well as the third reading of Q1 GDP. In addition, there’ll be the preliminary data on durable goods orders and wholesale inventories for May. From central banks, the ECB will be releasing the account of their June monetary policy meeting, and speakers include the ECB’s Schnabel, Mersch and Knot, the Fed’s Bostic and Kaplan, along with the BoE’s Haldane. There’ll also be monetary policy decisions from central banks in Turkey and Mexico.

via ZeroHedge News https://ift.tt/2YwdhFT Tyler Durden